Healthcare Compliance Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

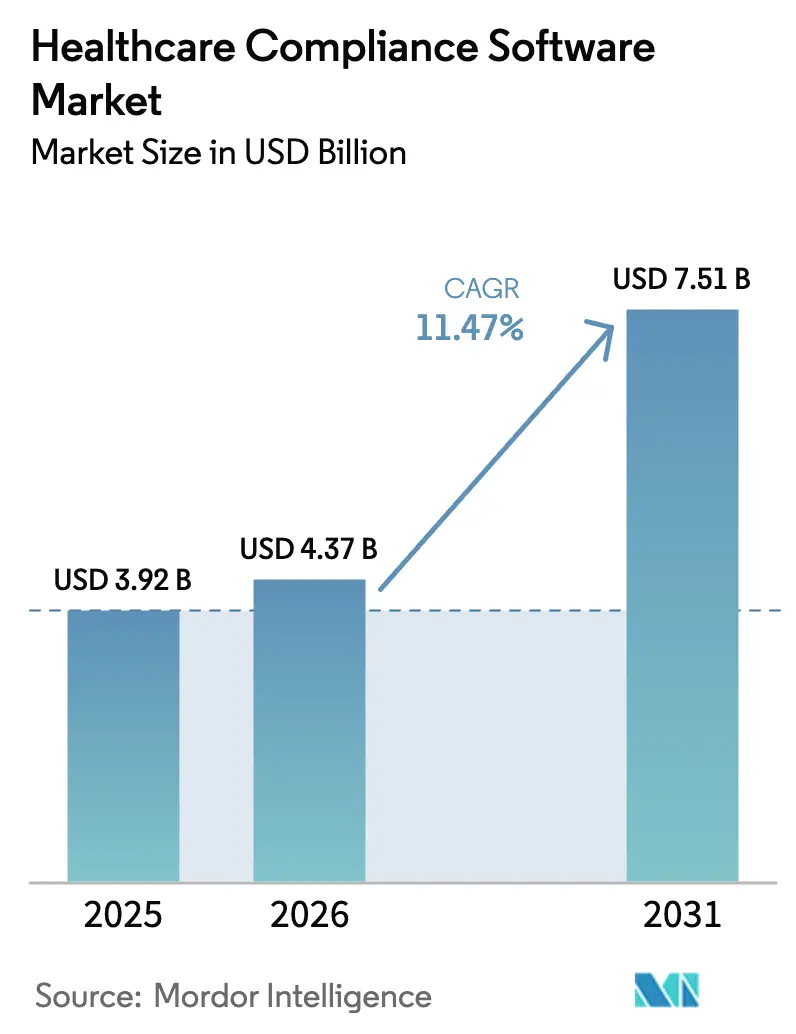

| Market Size (2026) | USD 4.37 Billion |

| Market Size (2031) | USD 7.51 Billion |

| Growth Rate (2026 - 2031) | 11.47% CAGR |

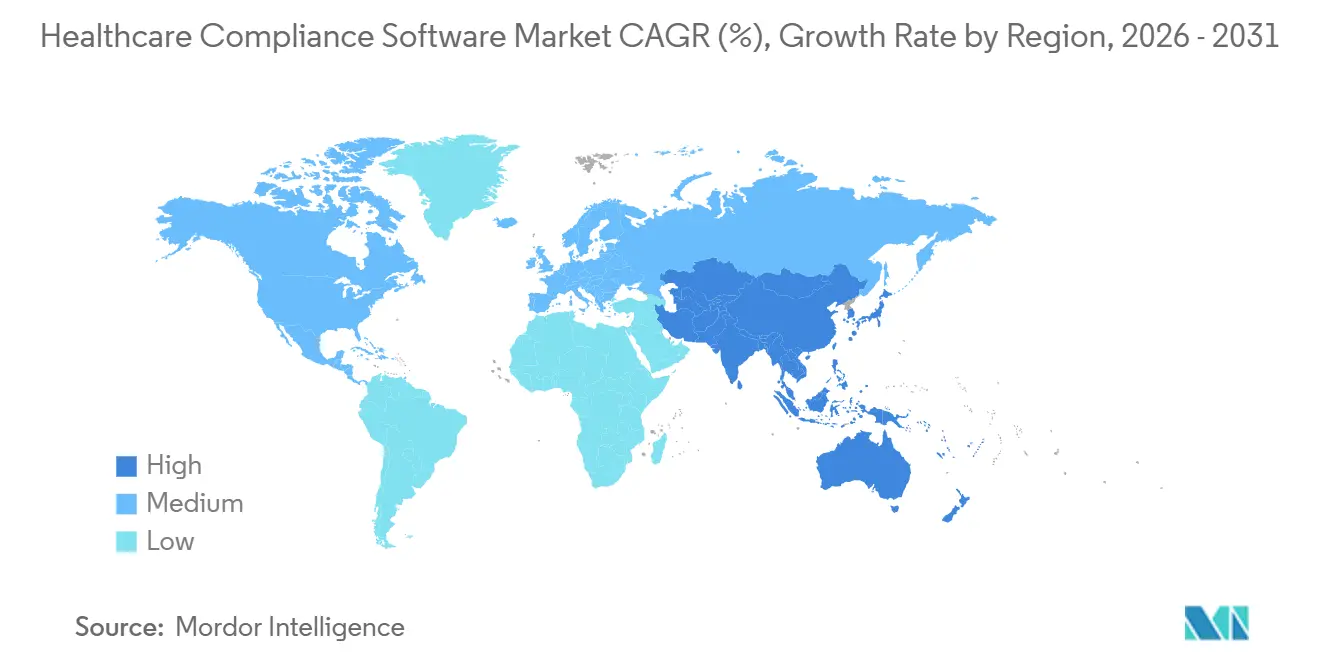

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Compliance Software Market Analysis by Mordor Intelligence

The Healthcare Compliance Software Market size is expected to grow from USD 3.92 billion in 2025 to USD 4.37 billion in 2026 and is forecast to reach USD 7.51 billion by 2031 at 11.47% CAGR over 2026-2031.

Rapid digitization of clinical workflows, telehealth expansion, and AI-enabled auditing position compliance platforms as strategic tools for risk mitigation rather than mere regulatory checklists. Vendors that integrate natural language processing to flag rule changes and automate audit trails are capturing market share because hospitals report up to 50% reductions in workload after deployment. Cloud delivery models remain the preferred choice, enabling provider organizations to scale capacity without incurring capital expenditures while meeting stringent HIPAA and GDPR security mandates.

Key Report Takeaways

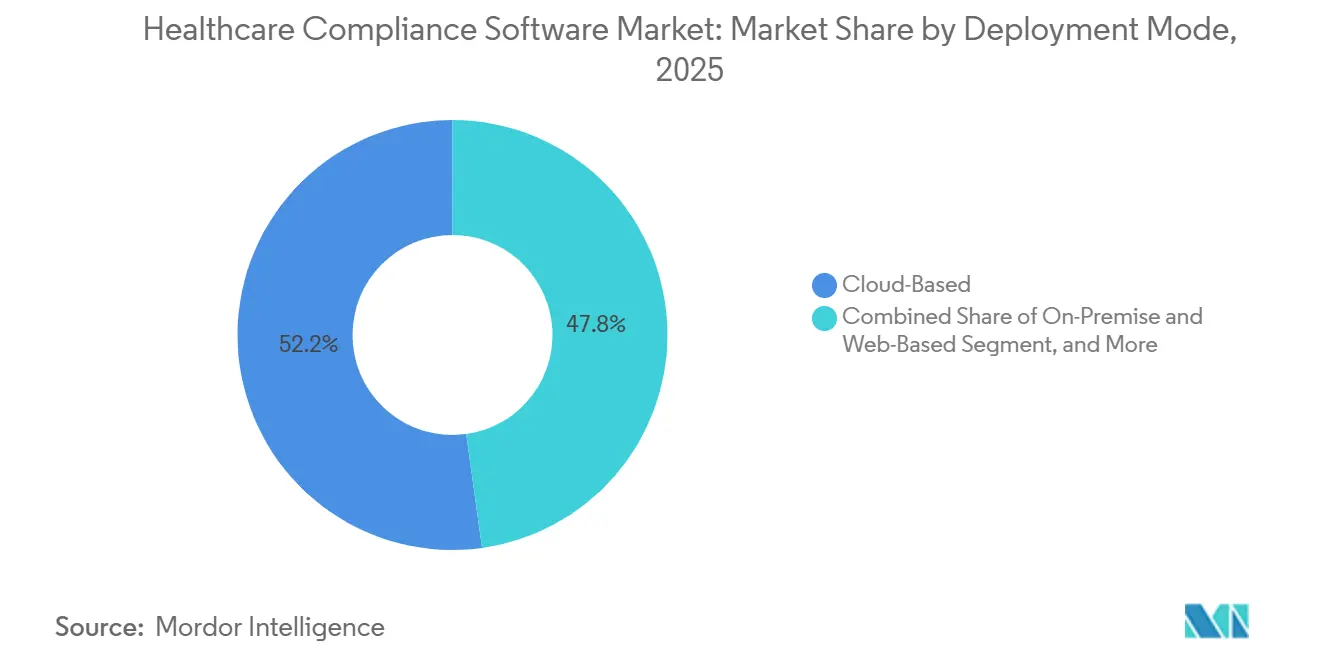

- By deployment mode, the cloud-based segment captured 52.19% of the healthcare compliance software market share in 2025 and is projected to advance at a 17.42% CAGR through 2031.

- By solution module, policy & procedure management accounted for 22.94% of the healthcare compliance software market in 2025, while accreditation management is forecast to grow at a 19.22% CAGR between 2026 and 2031.

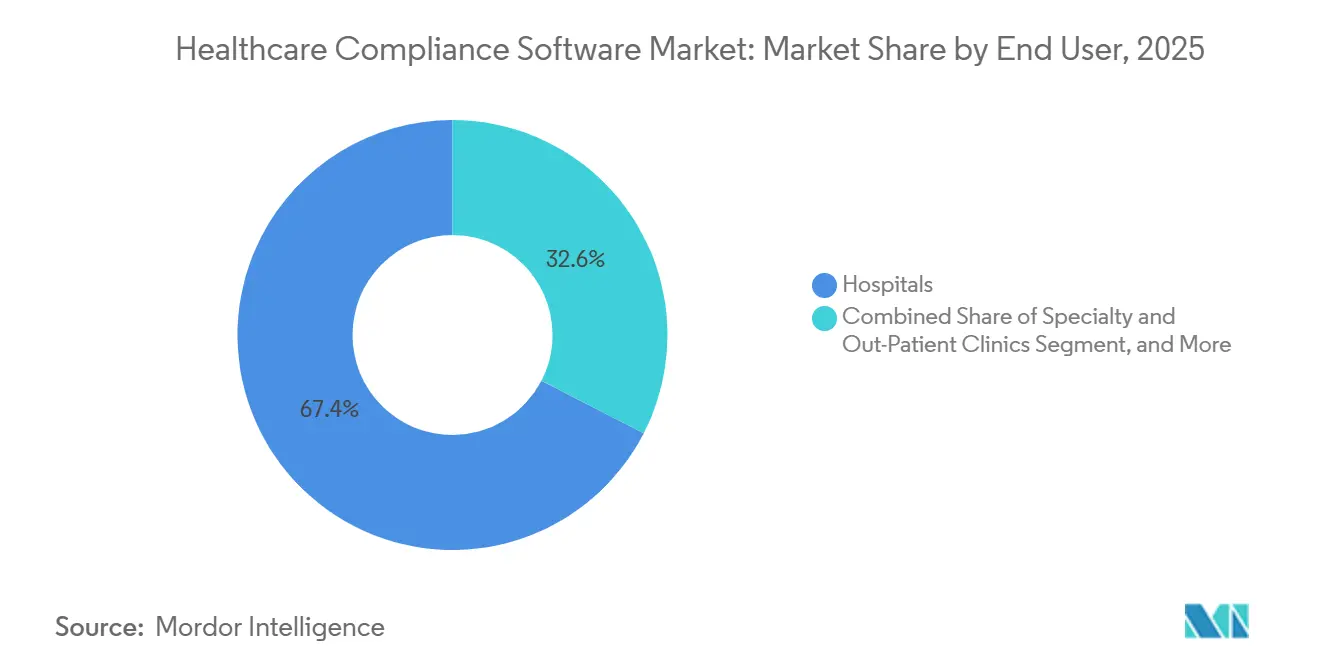

- By end user, hospitals led the healthcare compliance software market share in 2025, with 67.44%. Specialty and outpatient clinics recorded the fastest growth, at a 15.86% CAGR, from 2026 to 2031.

- By geography, North America captured 44.68% of the healthcare compliance software market in 2025; the Asia-Pacific region is projected to grow with an 18.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Compliance Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shift from manual to automated compliance | +2.8% | Global, early gains in North America & EU | Medium term (2–4 years) |

| Rising healthcare data breaches & penalties | +3.1% | North America, EU, APAC core | Short term (≤2 years) |

| Growing regulatory complexity & privacy laws | +2.5% | Global | Long term (≥4 years) |

| GenAI-driven predictive compliance analytics | +1.9% | North America, EU, spill-over to APAC | Medium term (2–4 years) |

| Growth of remote virtual audit workflows | +0.9% | Global, accelerated in North America | Short term (≤2 years) |

| Embedded compliance inside EHR & RPA ecosystems | +1.2% | North America, EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shift From Manual to Automated Compliance

Hospitals in the United States must document 17 Conditions of Participation for every inspection cycle. Manual oversight, previously reliant on isolated spreadsheets and paper attestations, is no longer sufficient. Centralized platforms now automate version control, timestamp staff acknowledgments, and generate surveyor-ready reports, reducing policy-update cycles from weeks to days. Continuous visibility into compliance status allows officers to focus on proactive risk mitigation. Digital signatures establish a robust audit trail, meeting regulatory standards. Integration with workforce portals ensures role-specific updates are seamlessly incorporated into clinicians’ workflows, increasing adoption rates without additional training. This shift transforms software from a cost center into a strategic asset that protects reimbursement and reputation.

Rising Healthcare Data Breaches & Penalties

In 2024, healthcare breaches exposed 133 million patient records, a 22% increase that resulted in USD 28.3 million in penalties, including a USD 4.75 million settlement for failing to conduct a risk assessment.[1]U.S. Department of Health and Human Services, “HIPAA Compliance and Enforcement,” hhs.gov Compliance suites now include incident-response modules that ensure timely completion of mandated reports and patient notifications. The stringent fines under GDPR have driven a significant increase in adoption among European providers. Cyber-insurance carriers now require evidence of encryption, role-based access logging, and automated vulnerability scans as prerequisites for coverage. Compliance software has become an operational necessity, with embedded frameworks accelerating certification, enabling providers to negotiate lower premiums and recover from breaches more efficiently.

Growing Regulatory Complexity & Privacy Laws

Privacy regulations are expanding across jurisdictions, layering federal, state, and specialty-specific mandates, which increase documentation requirements for care settings. California’s Confidentiality of Medical Information Act intensifies HIPAA obligations, while Brazil’s LGPD enforces GDPR-like standards across Latin America. China’s Data Security Law requires patient records to remain on domestic servers, compelling multinational corporations to establish regional clouds and undergo new security audits.[2]Yew Lun Tian, “China Data Security Law Raises Stakes,” Reuters, reuters.com Similarly, India’s Digital Personal Data Protection Act mandates data localization, altering deployment strategies for global vendors. Accreditation bodies are updating standards more frequently, requiring providers to monitor changes continuously rather than on a triennial basis. These developments add thousands of control points, making automated policy libraries and continuous monitoring essential for effective compliance management.

GenAI-Driven Predictive Compliance Analytics

Generative AI is transforming the healthcare compliance software market by analyzing historical audit data and identifying policy gaps to provide proactive risk alerts, reducing surprise citations by up to 35%. Natural-language processing engines interpret regulatory notices and draft updates for legal teams to refine, significantly reducing revision timelines. Adaptive training modules personalize quiz questions based on individual staff performance, accelerating remediation when competency gaps are identified. The classification of healthcare compliance analytics as high-risk under the EU AI Act requires vendors to document algorithmic origins and ensure outputs are explainable. This upfront investment differentiates vendors during provider evaluations. In the United States, forthcoming FDA guidelines are expected to validate AI-driven quality systems, signaling broader regulatory acceptance when transparency measures are in place.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High implementation & maintenance costs | -2.2% | Global | Short term (≤ 2 years) |

| Limited it resources & awareness in SMB providers | -1.9% | Global | Medium term (2-4 years) |

| Fragmented data-residency laws hindering cloud | -2.4% | Emerging markets | Short term (≤ 2 years) |

| Algorithmic-transparency concerns for AI modules | -2.0% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation & Maintenance Costs

For mid-size hospital networks, initial license fees, configuration workshops, and workforce training often exceed USD 250,000. This financial strain is particularly challenging for rural facilities operating on tight budgets. Multi-month deployment cycles consume limited IT resources, especially when staff must map legacy policies to new taxonomies and validate role-based access controls. Annual subscription renewals include escalation clauses tied to rising user counts, while frequent regulatory updates demand additional testing hours. Providers without dedicated compliance teams face hidden costs, diverting clinicians or finance managers into extensive data-cleanup efforts. As a result, smaller community hospitals delay purchases or opt for partial modules, limiting overall adoption despite clear ROI.

Fragmented Data-Residency Laws Hindering Cloud

National security concerns are driving governments to enforce in-country data storage requirements, forcing vendors to maintain multiple regional clouds. This increases infrastructure costs and extends release cycles. China's Data Security Law mandates local servers, India's regulations require real-time data mirroring, and Russia restricts cross-border transfers, creating fragmented vendor strategies. In Europe, providers face challenges from the Schrems II ruling, which requires thorough vetting of United States-based subprocessors under Standard Contractual Clauses. This complex legal environment raises review costs and delays feature availability across regions. Global health systems operating in multiple jurisdictions often manage hybrid deployments locally on-premise and centrally in the cloud, adding complexity to vendor support and upgrade processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Architectures Dominate as Remote Audit Protocols Normalize

Cloud platforms accounted for 52.19% of the healthcare compliance software market share in 2025, as providers prioritized scalability and remote access. The segment’s 17.42% forecast CAGR exceeds that of on-premises systems because subscription pricing converts capital expenditures into predictable operating costs and speeds implementation within weeks. Leading vendors bundle automated backup and disaster recovery, ensuring data resilience amid cyber incidents that targeted multiple U.S. hospitals in 2024. Cloud hosting also simplifies continuous rule updates; once a regulation changes, providers receive patches without downtime, unlike traditional installations that require local IT intervention. In parallel, regulatory frameworks such as HIPAA and GDPR publish guidance clarifying that certified cloud providers can meet security mandates, boosting confidence among compliance officers.

Cloud vendors further differentiate by embedding AI micro-services for real-time anomaly detection, which would be resource-intensive to run on local servers. Hospitals leveraging these analytics report double-digit reductions in audit cycle times. Country-level initiatives, including India’s ABDM digital health program and Japan’s Medical Information System infrastructure, reference cloud architectures, and strengthen regional demand. Consequently, cloud deployments will remain the primary engine driving the healthcare compliance software market through 2031, especially among multi-site health systems seeking unified oversight across geographies.

By Solution Module: Accreditation Automation Surges as Continuous Survey Readiness Replaces Cyclical Preparation

Policy & procedure management retained 22.94% of the healthcare compliance software market size in 2025 because every provider must document guidelines and secure acknowledgments from clinicians. However, accreditation management is projected to register a 19.22% CAGR, reflecting reimbursement linkages to Joint Commission, NCQA, and ISO certifications. Automated accreditation modules centralize evidence collection, schedule mock surveys, and trigger reminders when corrective actions lag. Health systems that employ predictive analytics within these modules detect gaps 6 months before survey windows, averting costly re-inspections. Interoperability with maintenance and biomedical engineering systems also helps demonstrate environment-of-care compliance, broadening its utility beyond policy documentation.

Financial stakes are high; facilities risk suspension of Medicare payment if accreditation lapses. Consequently, boards approve incremental budgets for dedicated accreditation workflows, accelerating module uptake. Vendors integrating gazette-based rule engines adapt quickly when accrediting bodies update standards, shielding customers from non-conformities. The shift underscores a strategic evolution in the healthcare compliance software market, where advanced modules move compliance from static record-keeping to dynamic performance oversight.

By End User: Specialty Clinics Outpace Hospitals as Regulatory Density Extends Beyond Inpatient Settings

Hospitals accounted for 67.44% of the healthcare compliance software market share in 2025, driven by complex operating environments that include inpatient, outpatient, and ancillary services. Their need for enterprise-grade credentialing, incident reporting, and supply-chain compliance keeps demand steady. Yet specialty and outpatient clinics are projected to expand at a 15.86% CAGR as telehealth and remote monitoring intensify data privacy risks. Modular, cloud-based offerings minimize implementation burden and include specialty-specific content such as radiation-dose tracking in oncology or prescription monitoring in pain management. Several vendors now provide template libraries that map standard specialty codes to documentation requirements, cutting configuration hours by 40%.

Lower price points and rapid deployment timelines resonate with clinics facing reimbursement pressures yet seeking to avoid costly HIPAA violations. As payers increasingly audit provider networks for compliance maturity, clinics view software investments as competitive differentiators when negotiating contracts. The specialty-driven growth wave complements hospital adoption, broadening the healthcare compliance software market's footprint across the continuum of care and creating new revenue opportunities for vendors.

Geography Analysis

North America preserved 44.68% of the healthcare compliance software market share in 2025, supported by rigorous enforcement of HIPAA, HITECH, and the False Claims Act. Widespread cloud adoption accelerates software deployment; surveys reveal 91% of U.S. hospitals now run portions of their infrastructure in the cloud. CMS’s push toward total accountable-care participation by 2030 further elevates documentation and quality-reporting requirements, compelling investment in integrated compliance platforms. Provider organizations increasingly bundle compliance modules with EHR upgrades, driving cross-selling opportunities. AI-powered audit capabilities are gaining traction as board-level scrutiny of fraud and waste intensifies following multiple high-profile enforcement actions in 2024.

Asia-Pacific records the highest growth, forecast at 18.12% CAGR, significantly outpacing the global average. China’s Personal Information Protection Law and India’s Digital Personal Data Protection Act impose strict penalties, motivating providers to deploy automated monitoring to avoid fines. Public-private partnerships in Japan and Australia fund telehealth expansion in rural regions, and each initiative requires compliance technology to secure patient data transmissions. Multinational life-science firms operating across the region adopt unified platforms to harmonize anti-bribery, pharmacovigilance, and data privacy controls, thereby further scaling the healthcare compliance software market.

Europe contributes steady demand as GDPR fines reach new highs, with several hospitals ordered to pay multi-million-dollar penalties for data breaches in 2024. Providers prioritize solutions that consolidate healthcare-specific regulations with broader data-protection mandates, streamlining reporting to supervisory authorities. Middle East & Africa and South America remain emerging markets, but post rising adoption in tertiary centers located in the United Arab Emirates, Saudi Arabia, Brazil, and Colombia. Mobile-friendly compliance apps enable frontline staff to complete checklists in low-bandwidth environments, supporting incremental market penetration in areas with sparse fixed networks.

Competitive Landscape

The healthcare compliance software market contains a balanced mix of established healthcare IT vendors, specialized compliance firms, and AI-centric start-ups. RLDatix’s series of acquisitions broadened its portfolio from incident reporting to credentialing and policy management, yielding a unified operations suite that appeals to multi-facility systems. HealthStream leverages its dominant learning-management footprint to cross-sell compliance modules, bundling workforce education with policy attestations to create closed-loop governance. Symplr emphasizes configurable dashboards and EHR integrations, releasing automated monitoring updates in November 2024 that attracted mid-tier hospitals seeking rapid time-to-value.

AI capability is the principal competitive differentiator. Vendors embedding machine-learning models for predictive risk scoring routinely secure contracts over rivals offering rule-based engines. Smaller disruptors focus on underserved niches such as behavioral health and home care, providing template-driven solutions that match specialized billing rules and documentation standards. Strategic partnerships with EHR vendors enhance market access; for example, RLDatix’s collaboration with Steward HealthCare brought its suite into 39 facilities, demonstrating the leverage gained via enterprise roll-outs. Pricing models trend toward tiered subscriptions linked to facility size and module count, balancing affordability with upsell potential.

Mergers, private-equity backing, and venture funding continue to reshape market dynamics. Investors favor firms with cloud-native architectures and proven AI pipelines that reduce manual audit hours. Competitive tension also rises around interoperability standards as health systems demand seamless data exchange across policy, credentialing, and revenue-cycle platforms. Consequently, vendors invest heavily in open APIs and HL7 FHIR compatibility, strengthening ecosystem integration while expanding the total addressable healthcare compliance software market.

Healthcare Compliance Software Industry Leaders

RLDatix

Atlantic.Net

ByteChek, Inc.

Healthicity LLC

HealthStream Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Polysight, incubated by Catalyst by Wellstar, launched an AI-native compliance intelligence platform and began a pilot at Wellstar Health System backed by USD 1 million seed funding.

- January 2026: Medispend and RLDatix Life Sciences completed a merger under the Medispend brand, creating an integrated suite spanning regulatory compliance, medical affairs, and revenue management.

- January 2026: The U.S. Centers for Medicare & Medicaid Services interoperability and prior-authorization final rule took effect, requiring FHIR APIs that expose compliance data and accelerating the need for out-of-the-box connectors.

- April 2025: ENTER launched an AI-driven HIPAA compliance platform focused on threat detection, predictive analytics, and automated document parsing.

- January 2025: HealthStream released an enhanced compliance program that layers continuous monitoring and fraud prevention onto its existing workforce-training portfolio.

Global Healthcare Compliance Software Market Report Scope

As per the scope, compliance monitoring refers to ensuring that healthcare organizations, suppliers, and providers adhere to appropriate regulations, standards, and laws that govern the provision of medical services and the handling of medical information. It involves overseeing compliance with privacy laws such as HIPAA, as well as quality care standards, antifraud and abuse laws, and mandatory reporting requirements.

The Healthcare Compliance Software Market is segmented by product type, category, end user, and geography. By product type, the market is segmented into on-premise, cloud-based, and web-based. By category, the market is segmented into policy and procedure management, auditing tools, training management and tracking, medical billing and coding, license, certificate, and contract tracking, incident management, accreditation management, and other categories. By end user, the market is segmented into hospitals, specialty clinics, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| On-Premise |

| Cloud-Based |

| Web-Based |

| Policy & Procedure Management |

| Auditing Tools |

| Training Management & Tracking |

| Medical Billing & Coding |

| License, Certificate & Contract Tracking |

| Incident Management |

| Accreditation Management |

| Other Category |

| Hospitals |

| Specialty & Out-Patient Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Mode | On-Premise | |

| Cloud-Based | ||

| Web-Based | ||

| By Solution Module | Policy & Procedure Management | |

| Auditing Tools | ||

| Training Management & Tracking | ||

| Medical Billing & Coding | ||

| License, Certificate & Contract Tracking | ||

| Incident Management | ||

| Accreditation Management | ||

| Other Category | ||

| By End User | Hospitals | |

| Specialty & Out-Patient Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current healthcare compliance software market size?

The market size is USD 4.37 billion in 2026 and is forecast to reach USD 7.51 billion by 2031.

Which deployment model is expanding fastest?

Cloud-based solutions lead with a 17.42% CAGR thanks to lower upfront costs and rapid rule-update capabilities.

Why is accreditation management growing so quickly?

Providers link successful accreditation to reimbursement and market positioning, driving a projected 19.22% CAGR for accreditation modules.

Which region offers the highest growth opportunity?

Asia-Pacific registers an 18.12% CAGR as governments enforce new data-privacy laws and fund healthcare digitization initiatives.

How does AI improve healthcare compliance?

AI automates anomaly detection, predictive risk scoring, and regulatory scanning, reducing false positives by up to 85% and cutting review cycles by 30%.

What challenges slow adoption among specialty clinics?

Limited IT staff, cost perceptions, and lack of specialty-specific templates hinder uptake, though modular cloud tools are narrowing the gap.

Page last updated on: