United States Customer Relationship Management Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

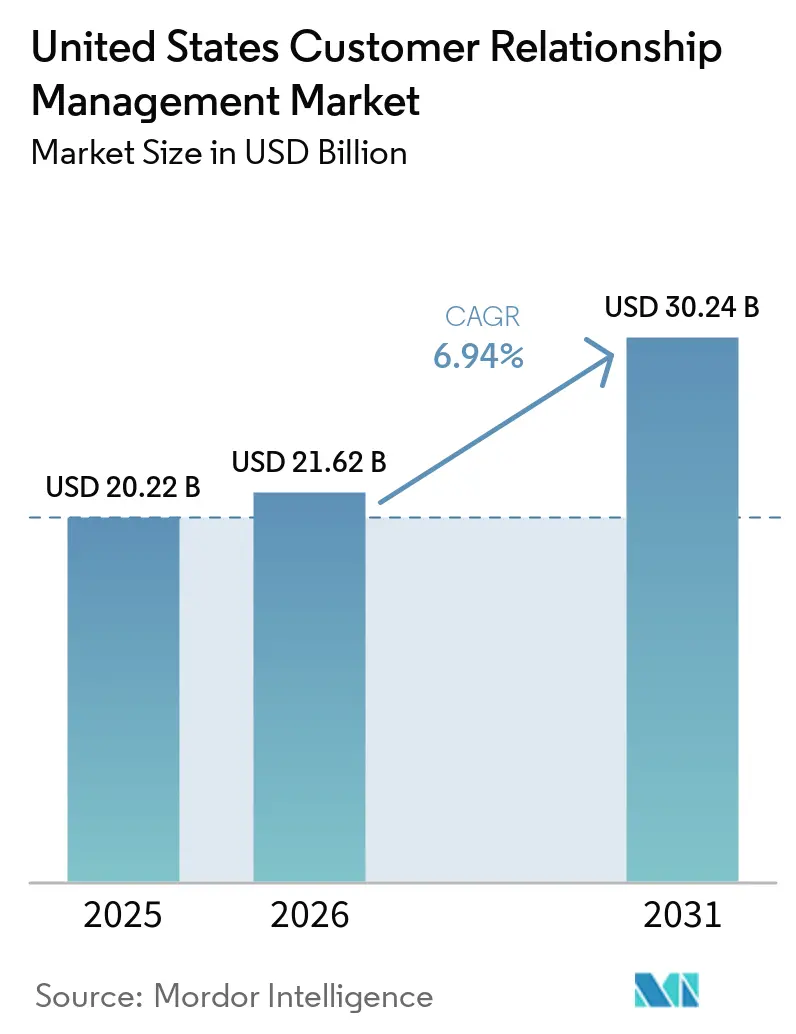

| Base Year Market Size (2025) | USD 20.22 Billion |

| Market Size (2026) | USD 21.62 Billion |

| Market Size (2031) | USD 30.24 Billion |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Customer Relationship Management Market Analysis by Mordor Intelligence

The United States customer relationship management market size was valued at USD 20.22 billion in 2025 and is estimated to grow from USD 21.62 billion in 2026 to reach USD 30.24 billion by 2031, at a CAGR of 6.94% during the forecast period (2026-2031). The United States customer relationship management (CRM) market is moving from contact management and record storage toward broader platform intelligence that supports automation, data activation, and service coordination across core customer-facing functions. Growth is being supported more by deeper use inside existing accounts than by large waves of first-time deployment, which is lifting revenue per active user even as seat expansion becomes more measured. Vendor pricing is also shifting toward usage-led and outcome-linked structures, which are changing how buyers evaluate long-term platform value and how vendors plan recurring revenue. Privacy compliance, AI governance, and integration complexity remain clear barriers, yet they are also pushing enterprises toward more capable platforms that can manage these demands within daily workflows. That combination keeps the United States CRM market on a durable expansion path through 2031, supported by AI investment, compliance-led upgrades, and broader adoption among smaller businesses.

Key Report Takeaways

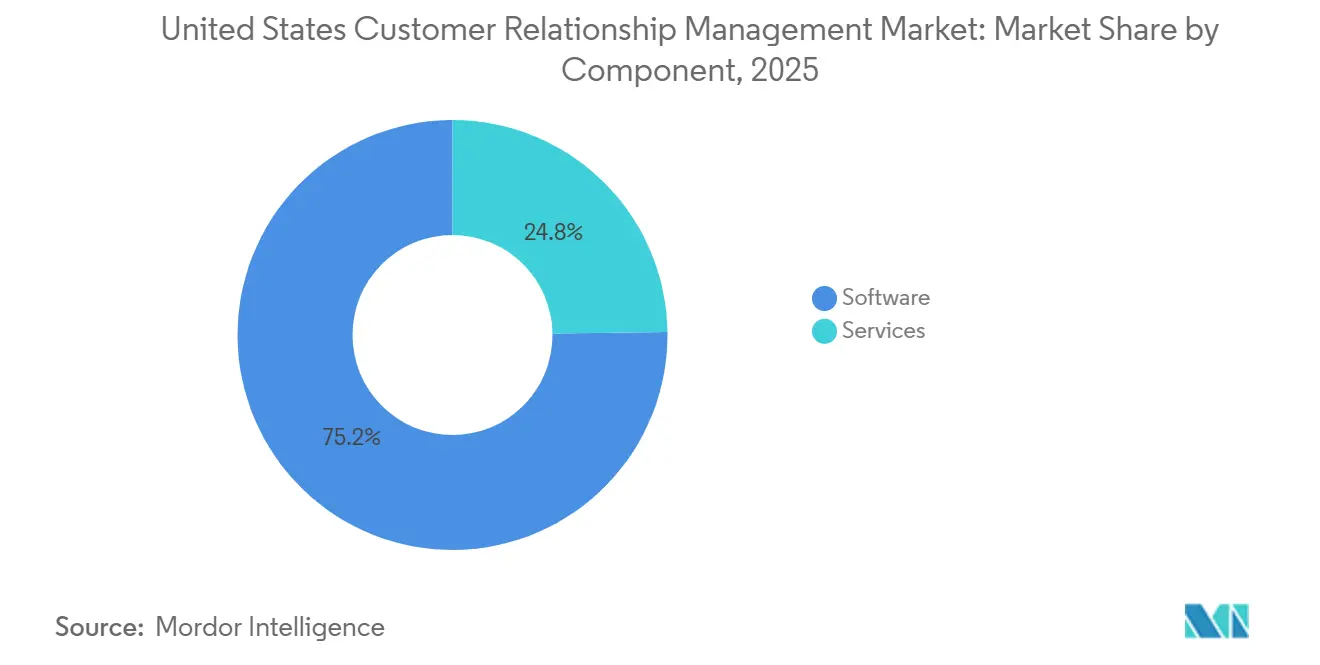

- By component, Software accounted for 75.22% of revenue in the United States customer relationship management market in 2025, while Services is projected to expand at a 7.12% CAGR through 2031.

- By deployment mode, Cloud accounted for 79.54% of revenue in the United States customer relationship management (CRM) market in 2025, while Hybrid is expected to record the fastest growth at a 7.67% CAGR through 2031.

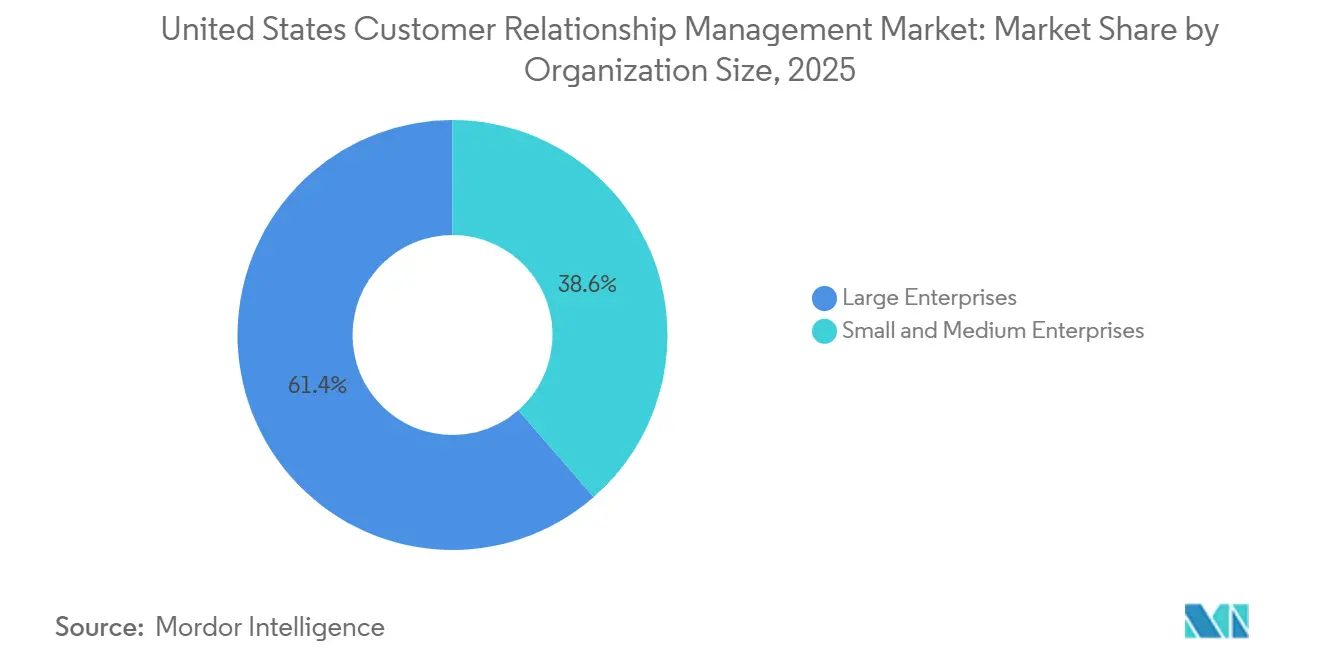

- By organization size, Large Enterprises held 61.42% of revenue in the US customer relationship management market in 2025, while Small and Medium Enterprises are projected to grow at a 7.87% CAGR through 2031.

- By application, Customer Service and Support captured 28.33% of revenue in the United States CRM market in 2025, while Revenue Operations is forecast to expand at a 7.56% CAGR through 2031.

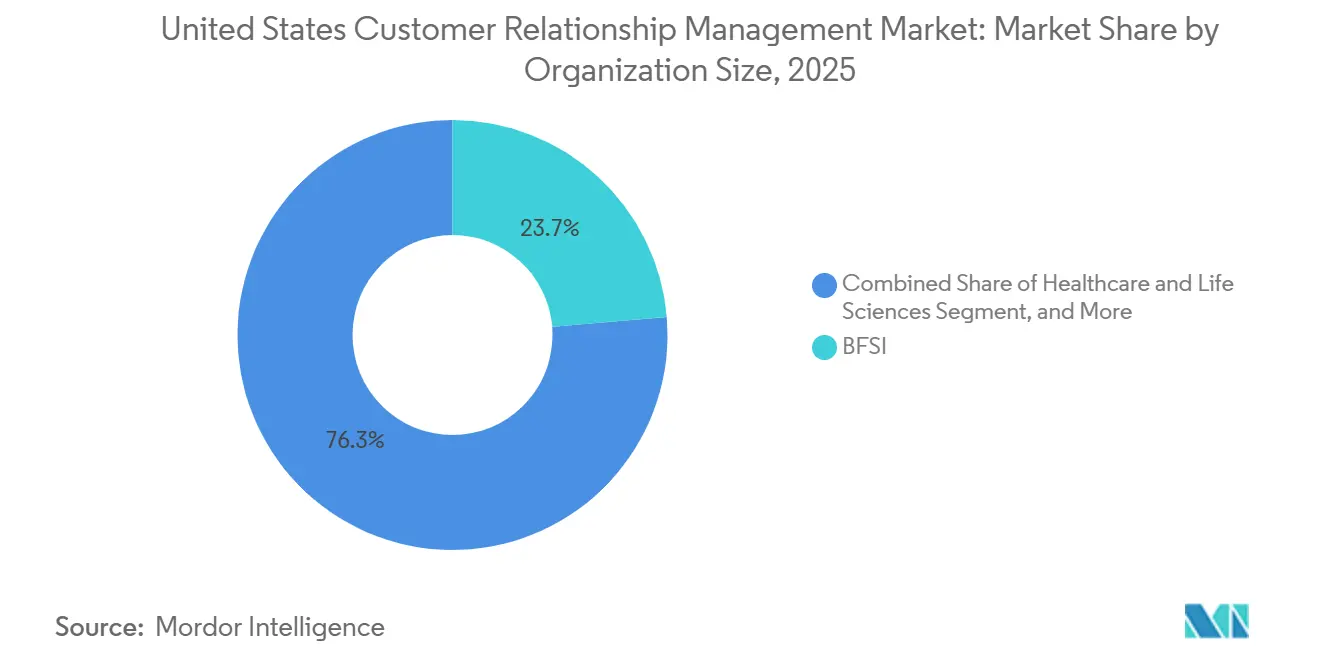

- By end-user industry, BFSI held 23.67% of revenue in the US CRM market in 2025, while Healthcare and Life Sciences is projected to grow at a 7.89% CAGR through 2031.

- By geography, the United States accounted for 38.22% of United States CRM market revenue in 2025, while the same geography is expected to post the fastest CAGR at 7.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Customer Relationship Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Copilots And Autonomous Agents In Frontline Workflows | +1.8% | National, with early concentration in California, New York, and Texas enterprise corridors | Short term (≤ 2 years) |

| Cloud-First CRM Modernization | +1.4% | National, with enterprise clusters in Pacific Northwest, Southeast, and Mid-Atlantic | Medium term (2-4 years) |

| First-Party Data Unification Through CDPs | +1.1% | National, with cross-border compliance posture shaped by California and EU regulatory frameworks | Medium term (2-4 years) |

| SME Adoption Via Lower-Cost Modular Suites | +0.9% | National, with early gains in Sun Belt SME corridors, including Texas, Florida, and Georgia | Short term (≤ 2 years) |

| Zero-Copy And Headless CRM Activation | +0.7% | National, with highest uptake in data-mature enterprise hubs | Long term (≥ 4 years) |

| RevOps Automation For Routing And Forecast Accuracy | +0.6% | National, with early gains in B2B SaaS clusters, including the San Francisco Bay Area, New York, and Austin | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI Copilots and Autonomous Agents In Frontline Workflows

AI agents inside frontline systems are moving the United States customer relationship management market away from feature comparison and toward measurable workflow execution. ServiceNow said in May 2026 that its Autonomous CRM for Sales and Service was already resolving more than 100 million customer cases, orchestrating more than 16 million orders, and configuring more than 7 million quotes each month, which gives the market a clear operating benchmark for large-scale autonomous work. Salesforce also framed this shift around continuous digital labor, positioning Agentforce Sales as a 24-7 workforce that can execute repetitive selling tasks inside CRM environments.[1]Salesforce, Inc., “Salesforce Agentforce Sales: The 24/7 Digital Workforce that Ends the Sales Grind,” Salesforce News, salesforce.com As more L1 and L2 tasks move to software agents, human teams are being redirected toward exception handling, approvals, and judgment-heavy work, which raises the value of each active user rather than simply expanding user counts. That dynamic increases switching friction because the vendor increasingly owns the work layer, not only the system of record. California's effective 2026 rules also add human oversight and opt-out obligations around automated decision-making, which means adoption in the United States customer relationship management (CRM) market is rising alongside governance requirements, not outside them.

Cloud-First CRM Modernization

Cloud modernization remains a central growth engine for the United States CRM market because vendors are now using rapid release cycles as a product advantage. Salesforce's Summer '26 release added multi-agent orchestration, Slack-first workflows, real-time data activation, and broader AI engagement tools, showing how new functionality is being delivered through cloud-native update cadences rather than periodic upgrade projects. ServiceNow followed a similar path in 2025 and 2026 by recasting CRM around one unified platform for selling, fulfillment, and service, then layering governed AI controls on top of that operating model.[2]ServiceNow, “ServiceNow Turns Enterprise AI Chaos into Control with the Platform for Governed, Autonomous Work,” ServiceNow Newsroom, servicenow.com The result is that cloud migration is no longer centered only on infrastructure efficiency, it is increasingly tied to access to new AI functions, faster service releases, and better interoperability across adjacent systems. That shift also explains why service demand is rising, because cloud-led modernization often requires integration redesign, change management, and ongoing administration. In the US CRM market, this makes cloud migration both a software growth driver and a services growth driver at the same time.

First-Party Data Unification Through CDPs

First-party data unification is becoming a core design requirement in the United States customer relationship management market because AI features depend on current, governed, and connected customer context. Salesforce's acquisition of Informatica in November 2025 directly addressed this need by bringing data catalog, governance, quality, privacy, metadata management, and master data capabilities into the platform environment. That direction continued in 2026 when Salesforce and Google Cloud announced deeper integrations for Agentforce and Gemini Enterprise, including zero-copy data federation with Google Lakehouse planned for late 2026. Informatica also expanded collaboration with Microsoft Fabric in May 2026 to improve trusted data movement from hundreds of enterprise sources into Fabric OneLake and Fabric Data Warehouse, which reflects the same push toward cleaner and broader activation paths. These moves matter because identity, consent, and activation are increasingly being treated as native CRM functions instead of bolt-on tools. In practice, this raises data gravity inside the United States customer relationship management (CRM) market and makes replacement decisions more disruptive once the customer graph is embedded into daily operations.

SME Adoption Via Lower-Cost Modular Suites

SME expansion is widening the demand base of the United States customer relationship management market because modular suites are lowering the commitment required to get started. HubSpot's Spring 2026 Spotlight introduced updates across Sales Hub Breeze and Customer Agent capabilities, which showed that AI-assisted CRM functions are now being packaged for customers well below enterprise budget levels. HubSpot also upgraded its Claude and ChatGPT connectors in February 2026 so users could create and update CRM records, log activities, and access engagement history from AI chat interfaces, reducing manual work for smaller teams that do not have dedicated administrators. In May 2026, the company opened the public beta of its redesigned Smart CRM Index, which further simplified data handling and reporting tasks inside the product. This kind of packaging lets smaller businesses activate sales, marketing, and service tools in phases rather than taking on full-platform complexity on day 1. That gradual entry point is a major reason the United States CRM market is seeing stronger momentum below the large-enterprise tier.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-By-State Privacy and Consent Complexity | -1.2% | National, with strongest effect in California, Colorado, Virginia, Texas, and Oregon | Short term (≤ 2 years) |

| Legacy Integration and Switching Costs | -1.0% | National, with highest concentration in mid-market enterprises in Midwest and Southeast manufacturing corridors | Medium term (2-4 years) |

| AI-Ready Data Quality Gaps | -0.8% | National, with most severe impact in BFSI and healthcare relying on decades-old structured data architectures | Long term (≥ 4 years) |

| Agent Governance and Auditability Burden | -0.5% | National, with early compliance pressure in BFSI, healthcare, and government-adjacent verticals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

State-By-State Privacy and Consent Complexity

State privacy fragmentation remains one of the clearest constraints on the United States customer relationship management (CRM) market because CRM data flows now sit directly inside consent, personalization, and automated decision-making processes. IAPP said that 20 comprehensive state privacy laws were in effect as 2026 began, which means companies must manage materially different obligations across multiple jurisdictions. California's updated CCPA framework also took effect on January 1, 2026, with rules around opt-out processing, risk assessments, and other compliance obligations that directly affect CRM operating models.[3]California Privacy Protection Agency, “California Consumer Privacy Act of 2018, Effective January 1, 2026,” CPPA, cppa.ca.gov For platform buyers, that turns privacy variation into a product selection issue, because consent workflows, jurisdiction logic, and audit trails have to work inside daily operations instead of being handled through manual workarounds. It also lengthens implementation cycles because national deployments cannot assume a single compliance standard. In the United States CRM market, that slows some projects even while it pushes demand toward platforms with stronger policy controls.

Legacy Integration and Switching Costs

Legacy integration debt slows the United States CRM market because replacement decisions are often constrained by connected systems rather than by the CRM license itself. Salesforce's introduction of Headless 360 at TDX 2026, which exposes platform functions as APIs, Model Context Protocol tools, and CLI commands, showed how much demand exists for architectures that can extend value without forcing full replacement at once. The Informatica acquisition also points to the same issue, because buyers need governance, quality, metadata, and master data controls to modernize old estates without breaking dependent workflows. Many enterprises already have CRM connected to quoting, service, billing, marketing, and analytics layers, so a migration decision usually triggers a wider systems redesign. That makes modernization slower and more selective, especially when current platforms still support core workflows well enough. As a result, the US CRM market often advances through phased extension, hybrid architectures, and targeted service engagements instead of rapid full-stack replacement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Reframes the Platform Revenue Model

Software accounted for 75.22% of the United States customer relationship management market size in 2025, which kept the revenue base anchored in platform ownership across sales, marketing, service, and data functions. This leadership reflects the central role of CRM software as the operating layer for customer records, workflow routing, campaign execution, and service resolution across large enterprises and growing mid-market users. In the United States customer relationship management (CRM) market, software also remains the main point where vendors differentiate on AI, data activation, low-code configuration, and user productivity. Customer data management and analytics functions are drawing a larger share of product investment because the value of CRM now depends on how well the platform can unify customer context and activate it across multiple teams. Salesforce's November 2025 Informatica acquisition reinforced this direction by adding data catalog, governance, quality, privacy, metadata management, and master data management capabilities that strengthen the data foundation sitting under CRM workflows.

Services, while smaller in revenue terms, is projected to grow at a 7.12% CAGR during 2026-2031, which places it ahead of the overall market and signals a shift in how value is captured. The United States CRM market is becoming harder to implement through simple template rollouts because organizations are connecting more clouds, more data sources, and more AI-enabled processes inside one operating model. That change favors implementation partners, managed service providers, and specialist consultants that can redesign processes, not only configure screens. Service revenue is also being supported by longer onboarding cycles, more governed AI deployment, and greater demand for ongoing platform administration after go-live. In effect, software still anchors spending, but the US CRM market is increasingly monetizing the complexity required to make those platforms work well at scale.

By Deployment Mode: Hybrid Signals Regulatory Architecture, Not Technological Ambivalence

Cloud held 79.54% of the United States customer relationship management (CRM) market share by deployment mode in 2025, confirming that SaaS delivery remains the preferred model for most organizations. Cloud leadership reflects the need for continuous feature delivery, elastic scaling, and direct access to new AI capabilities that are arriving through frequent vendor releases. In the United States customer relationship management market, these benefits matter more as enterprises tie CRM to workflow automation, real-time data activation, and cross-functional collaboration. Salesforce's Summer '26 release and its broader Agentforce roadmap show how quickly new capabilities are now being introduced into production environments, which favors cloud-centered operating models. That pace makes on-premise environments less attractive for organizations that want immediate access to autonomous service, guided selling, and AI-assisted administration.

Hybrid is expected to grow at a 7.67% CAGR during 2026-2031, which makes it the fastest-growing deployment approach in this segmentation. That trend does not signal hesitation about cloud adoption, instead it reflects a practical architecture choice for organizations that need tighter control over sensitive data and regulated workflows. The United States CRM market is seeing hybrid demand from sectors that cannot move every process into a pure public cloud model while still needing cloud-native innovation. Salesforce Headless 360 supports this pattern by letting organizations expose CRM logic through APIs and tools while controlling how data is surfaced across external environments. On-premise remains relevant in narrower regulated settings, but hybrid is the segment that best captures how buyers are balancing innovation speed with control requirements.

By Organization Size: SME Momentum Reshapes The Competitive Map Below The Enterprise Tier

Large Enterprises held 61.42% of revenue in 2025, which shows that the United States customer relationship management (CRM) market still derives most value from large accounts with complex workflows and long vendor relationships. These organizations usually run broad deployments that span sales, marketing, service, analytics, and governance, which makes CRM a deeply embedded operating system rather than a stand-alone application. Their spending also stays elevated because AI features, data governance tools, and workflow automation are being layered onto existing estates rather than replacing them outright. Salesforce's Q1 FY2027 disclosures showed combined AI and Data ARR of USD 3.4 billion and Agentforce ARR above USD 1 billion, which illustrates how revenue expansion is now tied to deeper use inside major installed accounts. This pattern keeps the enterprise tier central to the United States customer relationship management market even as seat growth becomes less important than platform depth.

Small and Medium Enterprises are projected to grow at a 7.87% CAGR through 2031, which makes them the fastest-moving organization size segment. Much of that momentum comes from modular packaging, lighter administration, and the ability to activate only the functions that match current operating scale. HubSpot's 2026 product updates, including AI connectors and Smart CRM Index changes, show how smaller teams can now manage records, activities, and insights with less manual effort and fewer specialized staff. The United States CRM market is therefore broadening from the top down and the bottom up at the same time, with enterprise users deepening capabilities while smaller firms cross earlier affordability barriers. This dynamic is making the competitive field more layered, because vendors now need one strategy for complex enterprise estates and another for modular mid-market and SME demand.

By Application: RevOps Consolidation Marks The Next Phase Of Enterprise CRM Investment

Customer Service and Support accounted for 28.33% of the United States customer relationship management (CRM) market size in 2025, which made it the largest application segment. That leadership reflects the scale of contact center modernization, omnichannel case management, and AI-assisted support deployment across both enterprise and upper mid-market accounts. Service workflows are often where CRM value is most visible to end customers, so organizations tend to prioritize spending where response time, resolution quality, and self-service outcomes can improve quickly. ServiceNow's enterprise messaging around Autonomous CRM and Otto reinforces that momentum by placing AI directly into service execution and governed conversational workflows. In the United States customer relationship management market, this keeps customer service at the center of ongoing platform budgets even as adjacent functions gain importance.

Revenue Operations is forecast to grow at a 7.56% CAGR during 2026-2031, which shows where incremental investment is moving next. LeanData said in its 2026 report that many B2B organizations still struggle with clean routing, handoff visibility, qualification alignment, and duplicate records, which creates a clear use case for stronger RevOps coordination inside CRM environments. The same report also showed that the average revenue technology stack contracted from 62 tools in 2025 to 37 tools in 2026, which supports the case for consolidation around integrated operating models. That matters for the United States CRM market because RevOps is increasingly viewed as the layer that connects selling, marketing response, and forecast discipline. Sales force automation and marketing automation remain important, but RevOps is where buyers now expect more unified control over pipeline and handoff quality.

By End-User Industry: Healthcare's Compliance Mandate Converts Regulatory Pressure Into Platform Demand

BFSI held 23.67% of revenue in 2025, which made it the largest vertical in the United States CRM market. Financial institutions continue to invest in client engagement platforms because relationship managers, advisors, insurers, and service teams need a consistent view of the customer across product lines and channels. The vertical also tends to adopt workflow automation quickly when it can improve retention, cross-sell relevance, case handling, and service consistency in high-value relationships. CSI's May 2026 launch of its Customer Intelligence Suite for financial institutions shows how AI-powered insights are being positioned to deepen customer relationships and decision support in this vertical. That keeps BFSI at the top of the spending mix even as other verticals accelerate.

Healthcare and Life Sciences is projected to expand at a 7.89% CAGR through 2031, the fastest pace among end-user industries in the US CRM market. Growth is tied to compliance-led refresh activity, stricter expectations around security and auditability, and the need for platforms that can support sensitive workflows without weakening usability. Vendor selection in this vertical is increasingly shaped by regulated data handling, formal agreements, and architecture choices that fit healthcare operating requirements. Those conditions favor platforms that can combine CRM workflows with stronger governance, identity controls, and integration flexibility. Retail and e-commerce, IT and telecom, manufacturing, media and entertainment, and professional services continue to add steady demand, but healthcare and life sciences stands out because regulation is directly pushing upgrade decisions into active budget cycles.

Geography Analysis

The United States accounted for 38.22% of revenue by country in 2025 and is projected to grow at a 7.65% CAGR through 2031, which makes it both the largest and the fastest-growing geography within the study scope. This gives the United States customer relationship management (CRM) market a strong domestic center of gravity, where platform depth, AI adoption, and compliance-led modernization are all moving together. The regulatory backdrop is one reason the domestic market remains active, because buyers increasingly want systems with built-in consent management, policy controls, and auditable automation. IAPP said 20 comprehensive state privacy laws were in effect as 2026 began, while California's rules added further operational detail around consumer rights and automated decision-making oversight. At the same time, Salesforce's Q1 FY2027 disclosures showed 13% year-over-year revenue growth to USD 11.133 billion, with Agentforce ARR above USD 1 billion, which reflects the scale of enterprise spending now tied to AI-native CRM expansion.

Canada remains the second-largest geography in the study and reflects a mature digital environment where SMB adoption, cloud preference, and modernization in healthcare-related settings continue to support demand. The United States customer relationship management market influences this pattern strongly because many cross-border organizations standardize on the same core platforms for sales, service, and customer data workflows. Canadian buyers still operate within their own federal and provincial privacy requirements, which increases the importance of deployment flexibility, governance, and data control. That creates a favorable setting for vendors that can offer strong cloud capability without forcing a one-model architecture across all regulated workflows.

Mexico holds the smallest country share in scope, yet it represents an emerging expansion path tied to nearshoring and cross-border operating integration. As US manufacturers extend production and partner networks into Mexican industrial corridors, CRM deployments are also being extended to sales teams, service operations, and partner management functions. This makes Mexico more relevant to the United States CRM market than its current revenue share alone might suggest, because deployment growth is often linked to broader North American operating footprints. USMCA-related digital trade alignment also supports cross-border data use cases, which lowers one of the barriers that previously limited unified customer and partner architectures across the 3 countries.

Competitive Landscape

The United States customer relationship management (CRM) market remains concentrated at the enterprise tier, but it becomes progressively more fragmented in the SMB and mid-market, where packaging, ease of use, and focused workflows carry more weight. Salesforce continues to set much of the competitive pace through platform expansion, ecosystem depth, and acquisition-led data and AI integration. The November 2025 Informatica acquisition strengthened its control over data governance and quality, while the March 2026 Momentum acquisition added deeper unstructured data and conversational insight capabilities to Agentforce 360 and Slackbot workflows. Salesforce also completed the acquisition of Qualified in April 2026, which expanded agentic marketing and autonomous pipeline creation inside its broader platform strategy. These moves show how the United States customer relationship management market is being contested through stack depth and workflow ownership rather than through stand-alone feature launches.

ServiceNow is emerging as a stronger competitive force by approaching CRM from the process layer, not only from the traditional front-end application layer. Its 2025 CRM repositioning and 2026 Otto launch were both centered on governed autonomous work across sales, fulfillment, and service, which gives buyers an alternative model for AI-led execution. HubSpot is shaping the lower end of the market differently, focusing on modular adoption, AI-assisted record management, and simpler data interaction for teams that need faster value with less administration. This layered competition means the United States CRM market is not moving toward one uniform competitive pattern. Instead, enterprise competition is intensifying around autonomy and data control, while SMB competition is widening around usability and modular pricing.

Zendesk also remains relevant where service-led automation is the entry point for broader CRM value. At Relate 2026, the company introduced the Autonomous Service Workforce, which reflects a clear push toward verified AI resolution and more automated support operations. Freshworks and other focused vendors still matter in narrower buyer groups, but the broadest strategic moves are coming from platforms that can link AI, data, workflow, and governance into one architecture. Salesforce's Headless 360 announcement is especially notable because it exposes platform capabilities through APIs, tools, and command interfaces, which supports a future where agents can invoke CRM actions from many surfaces. The US CRM market is therefore becoming harder for narrow vendors to defend unless they own a specific workflow, a pricing advantage, or a regulated use case that larger platforms do not serve well enough.

United States Customer Relationship Management Industry Leaders

Salesforce, Inc.

Microsoft Corporation

Adobe Inc.

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Salesforce introduced its Summer '26 Release, delivering multi-agent orchestration, Slack-first workflows, real-time data activation, and AI-powered customer engagement capabilities. Available from June 15, 2026, the release operationalizes the Agentic Enterprise vision at production scale, enabling human and AI agents to collaborate seamlessly across enterprise workflows.

- May 2026: Salesforce introduced its Summer '26 Release, delivering multi-agent orchestration, Slack-first workflows, real-time data activation, and AI-powered customer engagement capabilities. Available from June 15, 2026, the release operationalizes the Agentic Enterprise vision at production scale, enabling human and AI agents to collaborate seamlessly across enterprise workflows.

- May 2026: Salesforce's Informatica expanded its collaboration with Microsoft on May 20, 2026, unveiling integrations for Microsoft Fabric that enable mass ingestion, Change Data Capture, and trusted data flow from over 300 enterprise sources into Fabric OneLake and Fabric Data Warehouse, accelerating AI and analytics readiness for joint Salesforce-Microsoft customers.

- April 2026: Salesforce and Google Cloud announced an expanded partnership at Cloud Next '26 on April 22, 2026, enabling AI agents to execute end-to-end workflows across both platforms using Agentforce and Gemini Enterprise, with zero-copy data federation with Google Lakehouse planned for late 2026.

United States Customer Relationship Management Market Report Scope

The United States Customer Relationship Management (CRM) Market refers to the industry encompassing software, services, and solutions designed to help organizations manage interactions with customers, streamline processes, and enhance profitability through improved customer satisfaction and loyalty. This market includes a wide range of offerings such as cloud-based and on-premise CRM platforms, analytics tools, and customer engagement applications that support sales, marketing, and customer service functions.

The United States Customer Relationship Management Market Report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises and Small and Medium Enterprises), Application (Sales Force Automation, Marketing Automation, Customer Service and Support, Digital Commerce, Analytics and Insights, Revenue Operations, and Partner Relationship Management), End-User Industry (BFSI, Retail and E-Commerce, Healthcare and Life Sciences, IT and Telecom, Manufacturing, Media and Entertainment, Professional Services, and Others), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Sales Force Automation Platforms |

| Marketing Automation Platforms | |

| Customer Service and Support Suites | |

| Customer Data Platforms | |

| Digital Commerce Engines | |

| Analytics and Insights Tools | |

| Services | Implementation and Integration |

| Consulting | |

| Training and Support | |

| Managed Services |

| Cloud | Public Cloud |

| Private Cloud | |

| Multi-cloud | |

| On-premise | |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Sales Force Automation |

| Marketing Automation |

| Customer Service and Support |

| Digital Commerce |

| Analytics and Insights |

| Revenue Operations (RevOps) |

| Partner Relationship Management |

| BFSI |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| IT and Telecom |

| Manufacturing |

| Media and Entertainment |

| Professional Services |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By Component | Software | Sales Force Automation Platforms |

| Marketing Automation Platforms | ||

| Customer Service and Support Suites | ||

| Customer Data Platforms | ||

| Digital Commerce Engines | ||

| Analytics and Insights Tools | ||

| Services | Implementation and Integration | |

| Consulting | ||

| Training and Support | ||

| Managed Services | ||

| By Deployment Mode | Cloud | Public Cloud |

| Private Cloud | ||

| Multi-cloud | ||

| On-premise | ||

| Hybrid | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Application | Sales Force Automation | |

| Marketing Automation | ||

| Customer Service and Support | ||

| Digital Commerce | ||

| Analytics and Insights | ||

| Revenue Operations (RevOps) | ||

| Partner Relationship Management | ||

| By End-user Industry | BFSI | |

| Retail and E-Commerce | ||

| Healthcare and Life Sciences | ||

| IT and Telecom | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Professional Services | ||

| Other End-user Industries | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the 2026 size of the United States customer relationship management market?

The United States customer relationship management market reaches USD 21.62 billion in 2026 and is forecast to reach USD 30.24 billion by 2031 at a 6.94% CAGR.

Which component leads spending in the United States customer relationship management space?

Software led with 75.22% of revenue in 2025, showing that platform ownership still anchors spending more than services.

Which deployment model is growing fastest in the US CRM platform landscape?

Hybrid is the fastest-growing deployment mode with a 7.67% CAGR through 2031, even though Cloud remained the largest at 79.54% in 2025.

Why are smaller businesses adopting CRM platforms faster in the United States?

SMEs are growing at a 7.87% CAGR because modular suites, phased activation, and AI-assisted administration lower the cost and effort of adoption.

Which application area is seeing the strongest momentum through 2031?

Customer Service and Support remained the largest application at 28.33% in 2025, while Revenue Operations is growing fastest at a 7.56% CAGR.

Which end-user vertical is expanding most quickly in this market?

Healthcare and Life Sciences is the fastest-growing end-user segment at 7.89% CAGR, while BFSI remained the largest vertical with a 23.67% share in 2025.

Page last updated on: