Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

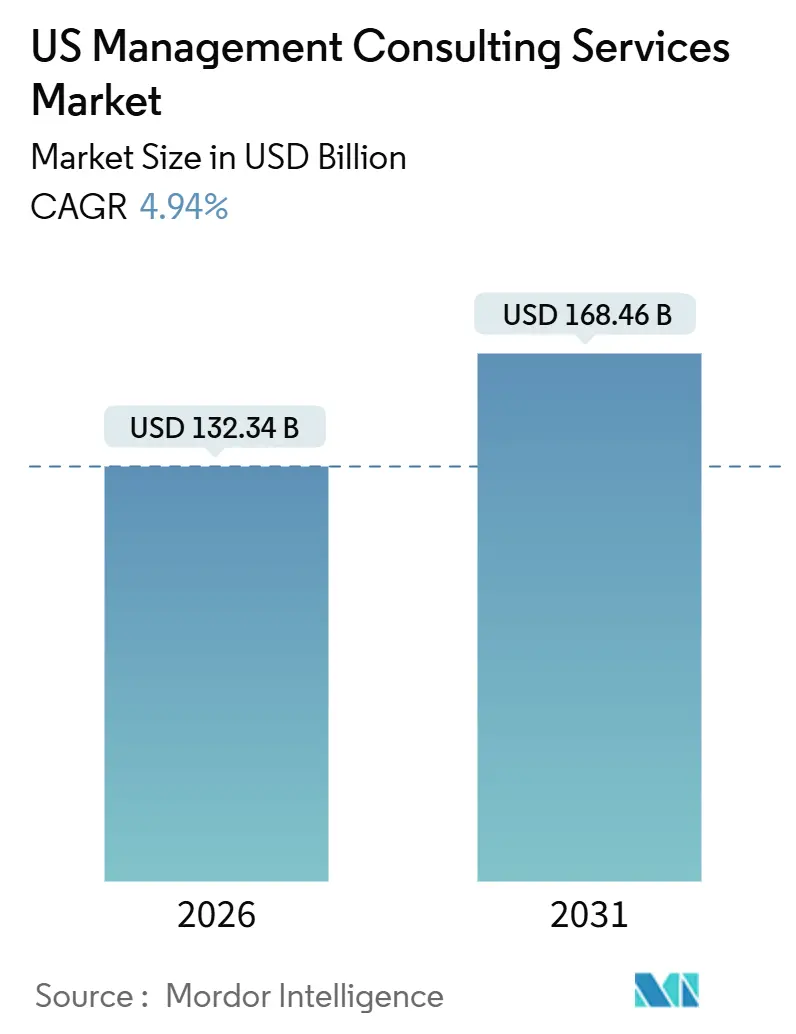

| Market Size (2026) | USD 132.34 Billion |

| Market Size (2031) | USD 168.46 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Management Consulting Services Market Analysis by Mordor Intelligence

The US management consulting services market size reached USD 132.34 billion in 2026 and is projected to climb to USD 168.46 billion by 2031, advancing at a 4.94% CAGR over the forecast window. Shifting client priorities toward technology-enabled transformation, regulatory compliance, and outcome-based engagements are reshaping advisory spend. Enterprises are fusing cloud migration, generative-AI deployment, and zero-trust cybersecurity into unified modernization programs, encouraging consultancies to blend strategy with deep implementation skills. At the same time, Fortune 500 companies are expanding in-house strategy units that siphon routine optimization work from external advisors. Wage inflation, especially at the partner level, is compressing margins, forcing firms to automate junior-consultant tasks and experiment with fixed-fee or gain-share models. Competitive intensity is escalating as hyperscalers formalize co-delivery partnerships that blur the boundary between infrastructure provisioning and strategic counsel.

Key Report Takeaways

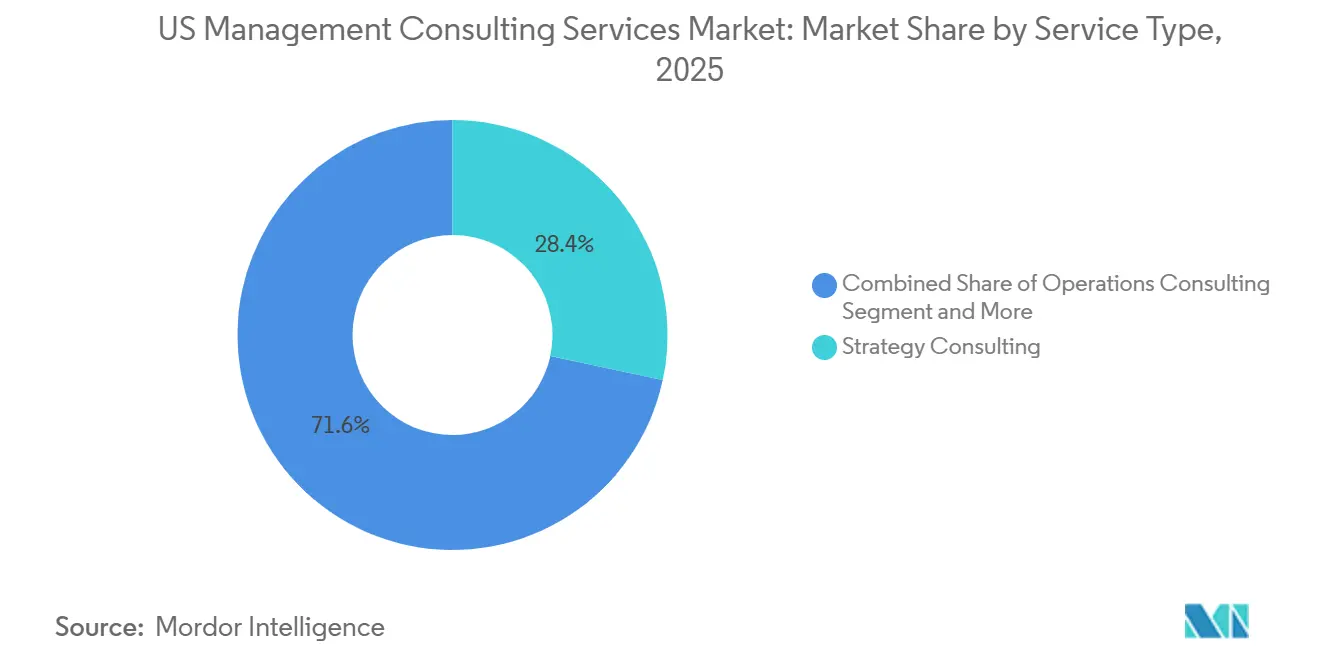

- By service type, Strategy Consulting led with 28.36% revenue share in 2025, whereas Technology Advisory is advancing at a 5.88% CAGR through 2031.

- By client size, Large Enterprises controlled 72.16% spending in 2025, while Small and Medium Enterprises are expanding at a 5.96% CAGR to 2031.

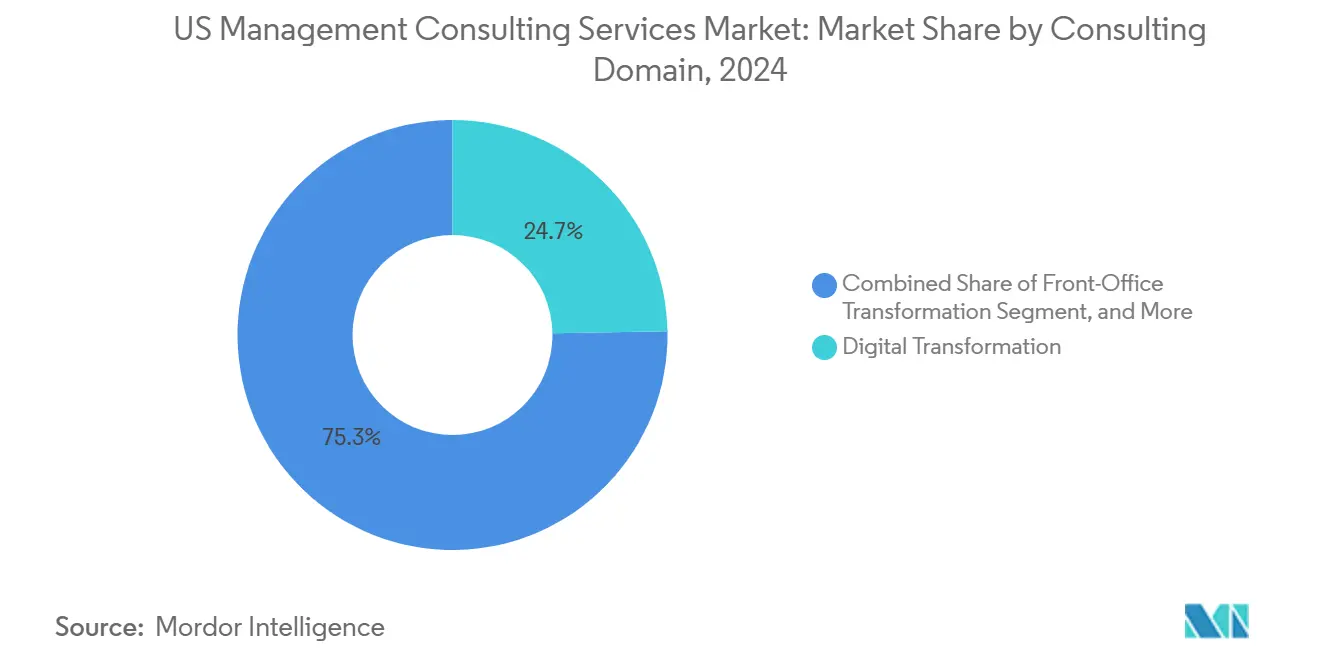

- By consulting domain, Digital Transformation accounted for 24.73% of the US management consulting services market share in 2025 and is progressing at a 6.11% CAGR over the forecast period.

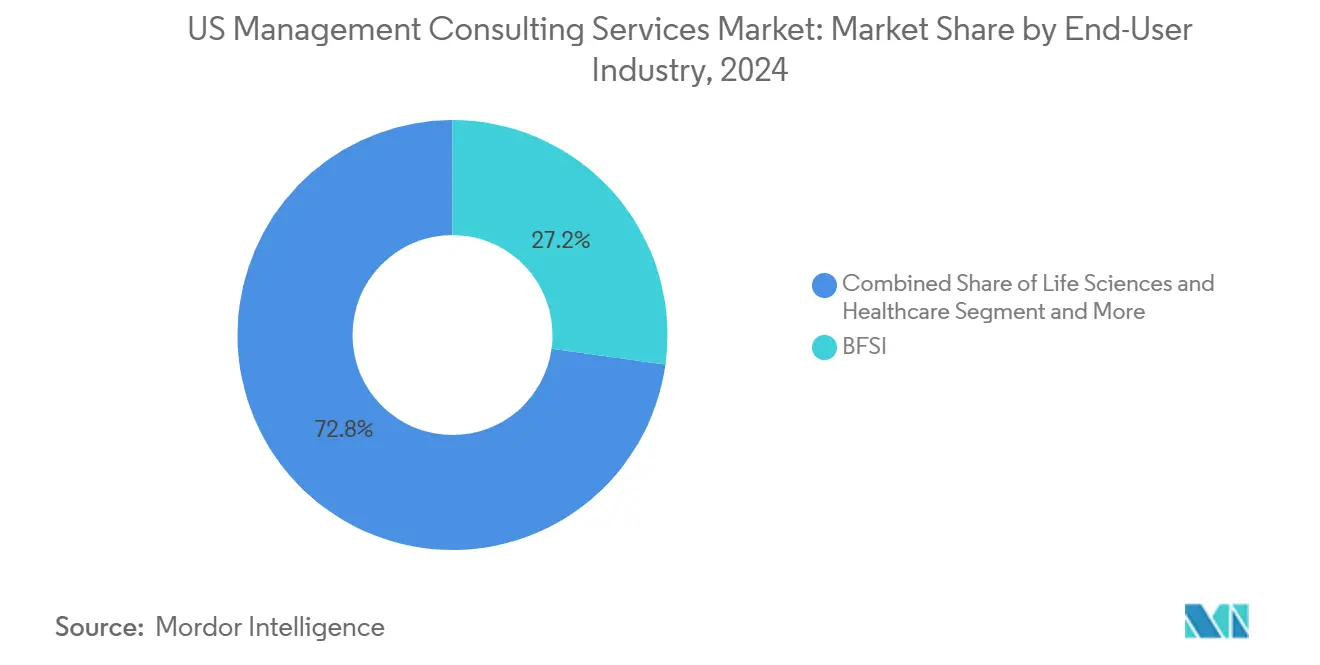

- By end-user industry, Life Sciences and Healthcare posted the fastest 6.21% CAGR, outpacing Banking, Financial Services, and Insurance, which held 21.52% of the 2025 value.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Transformation Demand | +1.2% | National, led by technology hubs and manufacturing corridors | Medium term (2-4 years) |

| Regulatory-Driven Advisory Spend | +0.9% | BFSI centers and biopharma clusters | Short term (≤ 2 years) |

| Cost-Out and Operational Excellence Focus | +0.6% | Manufacturing and industrial regions | Medium term (2-4 years) |

| Outcome-Based Pricing Uptake | +0.4% | Early adopters in technology and healthcare | Long term (≥ 4 years) |

| Generative-AI Copilots Creating White-Space | +0.8% | Early-adopter enterprises across technology and retail | Medium term (2-4 years) |

| Ecosystem-Led Consulting Partnerships | +0.7% | Cloud-mature industries nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-First Transformation Demand

Companies are consolidating previously siloed modernization projects into enterprise-wide programs that tie customer experience, supply-chain visibility, and workplace automation to a single investment thesis. Manufacturing clients are deploying Internet-of-Things sensors that cut unplanned downtime by up to 50%, yielding a quick ROI that justifies premium advisory fees. Banks are re-platforming core systems onto cloud-native stacks to meet real-time payment mandates, a path that demands both regulatory fluency and change-management discipline. The driver therefore tilts spend toward firms that integrate strategy, engineering, and managed services in a single engagement. As transformation programs grow in scope, boardrooms increasingly demand outcome-based contracts with dashboards tracking value capture in real time.

Generative-AI Copilots Creating Advisory White-Space

Large language models are automating research, slide production, and document review, reducing reliance on junior-consultant labor while creating new consulting demand in prompt engineering, model tuning, and AI governance. Boston Consulting Group expanded its BCG X unit in 2024, embedding machine-learning engineers in engagements to co-develop proprietary models rather than merely advising on vendor selection. Accenture disclosed generative-AI bookings in excess of USD 3 billion for fiscal 2024, a signal that clients want end-to-end build services, not PowerPoint recommendations. Outcome-based pricing is becoming feasible because AI provides live telemetry on productivity gains, allowing fees to flex with realized benefits. Yet the same technology commoditizes lower-value tasks, compelling firms to reskill juniors for higher-order synthesis and C-suite facilitation.

Regulatory-Driven Advisory Spend

Rulemaking is intensifying across climate disclosure, capital standards, and drug approvals. The Securities and Exchange Commission finalized emissions-reporting requirements in 2024, compelling publicly listed issuers to integrate Scope 1 and Scope 2 metrics into filings.[1]U.S. Securities and Exchange Commission, “SEC Finalizes Climate Disclosure Rules,” Sec.gov The Food and Drug Administration broadened its Real-Time Oncology Review pilot in 2025, shortening approval cycles to six months but demanding rolling data submissions. Meanwhile, the Federal Reserve is expected to lock in Basel III endgame rules in 2026, raising risk-weighted asset calculations for operational and market risk.[2]Federal Reserve, “Basel III Endgame Proposal,” Federalreserve.gov These overlapping mandates steer BFSI and biopharma clients toward consultancies staffed with former regulators and industry technologists who can interpret guidance while architecting compliant technology stacks.

Ecosystem-Led Consulting Partnerships With Hyperscalers

Cloud providers are teaming with consultancies to co-deliver strategy and infrastructure. Amazon Web Services upgraded its collaboration with Bain in 2024 to accelerate client migrations and generative-AI deployments. Microsoft and Ernst and Young integrated Azure AI services into audit workflows the same year to automate document scrutiny. Google Cloud and Boston Consulting Group formed a joint practice around Vertex AI, granting consultancies early access to beta functions that differentiate their offerings. Clients benefit from one-stop access to cloud capacity, AI tooling, and change management, while partners share implementation revenue and marketing reach. The model is gaining traction in data-sensitive sectors such as healthcare and finance, where hybrid-cloud blueprints demand both technical rigor and regulatory awareness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consulting Talent Wage Inflation | -0.7% | Major metropolitan areas | Short term (≤ 2 years) |

| Client In-House Consulting Build-Outs | -0.5% | Fortune 500 clusters | Medium term (2-4 years) |

| GenAI Commoditizing Research-Heavy Tasks | -0.4% | Firms with high junior leverage | Medium term (2-4 years) |

| Consulting Commodity Marketplaces | -0.3% | Early adoption in tech and professional services | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consulting Talent Wage Inflation

Median partner compensation climbed to USD 672,000 in 2024, with strategy partners fetching roughly USD 1.07 million, far outpacing the 3.9% salary-budget increase that The Conference Board projected for 2025.[3]The Conference Board, “2025 Salary Increase Budgets,” Conference-board.org Private-equity firms and technology giants are poaching seasoned advisors to steer portfolio-company transformations, inflating wage benchmarks and driving partner churn 49% above historical norms. Immigration policy adds pressure: the 2024 shift to a wage-weighted H-1B selection process raises salary floors for international hires.[4]U.S. Citizenship and Immigration Services, “H-1B Visa Wage-Weighted Selection Process,” Uscis.gov To preserve margins, consultancies are automating repetitive tasks, rebalancing staffing pyramids, and experimenting with offshore delivery centers in lower-cost locales.

Client In-House Consulting Build-Outs

Fortune 500 organizations are assembling internal advisory teams staffed by alumni from McKinsey, Bain, Boston Consulting Group, and Deloitte. These units handle strategy refreshes, merger integration, and operational excellence without external fees, preserving institutional knowledge and accelerating decision cycles. Private-equity sponsors echo the trend by embedding value-creation experts in portfolio companies to drive EBITDA improvement pre-exit. Although in-house teams excel at context-rich projects, they lack cross-industry benchmarking and large-scale transformation muscle, leading enterprises to retain external firms for disruptive initiatives. The resulting demand pattern encourages consultancies to differentiate through proprietary data, deep technology alliances, and measurable impact guarantees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technology Advisory Accelerates Modernization

The US management consulting services market size for Technology Advisory is on track to expand at a 5.88% CAGR to 2031, outpacing legacy practices anchored in pure strategy. Clients are channeling budgets toward cloud architecture, cybersecurity hardening, and generative-AI integration, areas where execution speed outweighs theoretical frameworks. Strategy Consulting, while still holding 28.36% of 2025 revenue, sees growth moderating as companies internalize strategic planning and reserve external spend for complex market entry or M&A due diligence. Operations Consulting finds renewed momentum through digital twins and predictive maintenance that reduce working capital, while Financial Advisory benefits from capital-optimization mandates tied to Basel III and emerging ESG disclosure rules. HR Consulting is pivoting to workforce analytics platforms that map skills gaps, and Risk and Compliance Consulting remains a steady revenue stream amid regulatory volatility. The convergence of cloud, AI, and cyber requires integrated advisory offerings, pushing firms to own both blueprint and build phases, an approach validated by Accenture’s roll-up of Oracle and Workday specialists between 2024 and 2025.

Client expectations have evolved from slide decks to continuous value delivery; as-a-service contracts grew 24% year-over-year in first-half 2024, highlighting appetite for consumption-based models that spread cost with benefit accrual. Technology Advisory engagements now bundle architecture, implementation, and managed services under outcome-based pricing, tying consultant compensation to productivity metrics such as defect-rate reduction or cycle-time compression. The push for rapid deployment favors firms with deep cloud alliances, proprietary accelerators, and multidisciplinary pods that merge strategists, engineers, and change managers into one team.

By Client Organization Size: SMEs Close the Service Gap

Small and Medium Enterprises are growing their share of the US management consulting services market at a 5.96% CAGR through 2031 as cloud platforms democratize access to analytics and advisory tooling. Modular engagements let SMEs buy targeted expertise, regulatory filings, vendor selection, or digital-marketing optimization, instead of full-blown transformation programs. Outcome-based pricing resonates with cash-constrained clients willing to share upside rather than fund hourly retainers. SaaS analytics tools enable internal pre-work, so consulting hours focus on higher-value judgment rather than data collection. The trend lowers entry barriers and spawns specialized boutiques that cater exclusively to the mid-market with verticalized playbooks and rapid-deployment kits.

Large Enterprises, however, still command the lion’s share of spend, maintaining 72.16% of 2025 outlays. Their complex footprints, multi-regulatory exposure, and legacy system entanglements require multi-year programs staffed with cross-disciplinary teams. Vendor consolidation is a recurring theme: clients want a single master services agreement covering strategy, build, and run phases, with milestone-based payments that tie fees to measurable key-performance indicators. Accenture’s sequential acquisitions of Inspirage, Namos Solutions, and Cientra illustrate how scale players bolster end-to-end coverage to remain on preferred-vendor rosters. Large Enterprises also demand transparent value dashboards, prompting consultancies to integrate telemetry tools that quantify ROI in near real time.

By Consulting Domain: Digital Transformation Sustains Momentum

Digital Transformation captured 24.73% of 2025 revenue and is forecast to grow at a 6.11% CAGR, reinforcing its role as the nucleus of enterprise change agendas. Organizations are scaling AI agents, robotic-process-automation bots, and data-mesh architectures from pilot to production across global operations. McKinsey noted in 2024 that 72% of U.S. businesses plan to embed generative AI into customer-facing applications within 12 months. The US management consulting services market size for Digital Transformation assignments is thus expanding faster than traditional enterprise-strategy work streams. Front-Office Transformation projects deploy conversational AI, recommendation engines, and predictive lead scoring that lower acquisition cost and lift conversion rates. Supply-chain digitization leverages control towers and blockchain-based traceability to mitigate geopolitical and tariff risks.

Cyber-Risk and Regulation services surge in tandem, as ransomware incidents rose 35% year-over-year in 2024 according to the Cybersecurity and Infrastructure Security Agency. Clients, therefore, seek packages that integrate zero-trust design, compliance automation, and 24-hour incident response. M&A and Restructuring activity swings with rate cycles but remains robust in technology consolidation and distressed retail. Consultants that combine sector expertise, data-driven insights, and tool-agnostic implementation capacity are capturing repeat engagements, particularly when they can deliver results under gain-share or fixed-fee structures.

By End-User Industry: Life Sciences Surges Ahead

Life Sciences and Healthcare leads growth at a 6.21% CAGR through 2031, propelled by accelerated FDA approvals, decentralized clinical trials, and value-based reimbursement. The Real-Time Oncology Review expansion compresses drug-approval timelines from 10 to 6 months, demanding adaptive trial designs and continuous regulator dialogue. Biopharma sponsors invest in wearables, synthetic control arms, and data-fabric architectures, requiring consultancies fluent in both clinical science and digital engineering. Provider systems navigating the shift to outcome-based care need predictive analytics to flag high-risk patients and optimize care pathways, further enlarging advisory opportunities. The US management consulting services market size for Life Sciences engagements is therefore set to outstrip horizontal averages.

Banking, Financial Services, and Insurance maintained 21.52% of 2025 spend, with demand rooted in Basel III capital recalibration, real-time payments, and open-banking APIs. Operational-resilience principles published by the Basel Committee in 2024 oblige banks to map critical services and establish recovery objectives. Consultants deliver playbooks for stress testing, liquidity optimization, and cyber-resilience, bundling technology, risk, and compliance skills into integrated mandates. IT and Telecommunications invest heavily in 5G densification and edge computing, engaging advisors for spectrum strategy, network slicing, and cloudification. Manufacturing sectors accelerate digital twin adoption, demanding combined operations and data capabilities to reduce downtime and working capital.

Geography Analysis

The United States holds a significant share of global management consulting revenue due to its concentration of multinational headquarters, venture capital investments, and regulatory diversity. Technology hubs such as San Francisco, Austin, and Seattle drive strong demand for consulting services focused on artificial intelligence and cloud technologies. Financial centers like New York and Charlotte lead engagements related to regulatory and risk management, while manufacturing regions in the Midwest attract advisors specializing in optimizing nearshore facilities. Biopharma clusters in Boston and San Diego fuel demand for life sciences consulting, particularly from firms that integrate clinical science with digital engineering.

State-level privacy laws, such as the California Consumer Privacy Act, necessitate detailed data governance frameworks, increasing the need for privacy-engineering consultants. Energy-producing states are investing in carbon-capture strategies to meet both federal and state emission targets, creating opportunities for ESG-focused advisory services. Federal regulatory requirements add further complexity, as companies must comply with simultaneous mandates from the SEC on climate reporting, the Environmental Protection Agency on emission caps, and the Occupational Safety and Health Administration on workplace guidelines. Firms with expertise in multi-jurisdictional compliance and localized delivery centers near client sites are well-positioned to secure repeat business.

The presence of hyperscaler data centers in Virginia, Oregon, and Iowa is shaping consulting delivery models by enabling low-latency deployments. The 24% growth in as-a-service contracts in 2024 highlights a client preference for fee structures aligned with outcomes. Consultancies are establishing operations near data hubs and forming agile teams capable of rapid cloud-native deployments. Regional talent pools further support specialization, with cybersecurity expertise concentrated in Washington D.C., analytics hubs in Chicago, and design studios in Los Angeles influencing the structure of consulting practices.

Regulatory Landscape

US management consulting engagements are being shaped by a faster-moving U.S. policy environment around digital platforms, AI, and telecom infrastructure, which is increasing demand for advisory services that combine compliance interpretation with technology implementation. In 2026, the Federal Trade Commission (FTC) intensified its posture on AI-related consumer protection. This included a July 2026 action to seek public comment on a policy statement addressing AI accuracy under Section 5 of the FTC Act, and a February 25, 2026 COPPA policy statement that incentivizes age-verification technologies, both of which raise expectations for governance, documentation, and auditability in AI-enabled customer experiences.

Alongside this, the Federal Communications Commission (FCC) advanced network and licensing-related actions that affect communications and digital infrastructure programs that often require consultancies for operating model and compliance work. An FCC Report and Order dated March 26, 2026 targeted barriers that prolong legacy telecommunications networks as part of the all-IP transition, while a Federal Register notice published April 10, 2026 introduced foreign adversary control disclosure requirements for certain license holders (effective June 9, 2026). Together, these steps reinforced supply-chain and ownership transparency workstreams that typically expand into telecom, cloud connectivity, and managed services transformation programs.

Competitive Landscape

Tier-1 players such as Deloitte, PwC, Accenture, McKinsey, EY, KPMG, Boston Consulting Group, and Bain continue to dominate large enterprise budgets through global reach, vertical specialization, and technology alliances. Acquisition activity highlights a shift toward owning build capabilities. Accenture acquired Inspirage, Namos Solutions, and Cientra to strengthen Oracle and Workday expertise. Deloitte integrated Argano for cloud transformation, while PwC added Surfaceink to enhance customer-experience design. These acquisitions enable firms to bundle strategy, implementation, and managed services under a single invoice, helping them defend wallet share against boutique firms and hyperscalers.

Boutique consultancies succeed by embedding former regulators and industry veterans who provide real-time insights on evolving frameworks. Hyperscalers are increasingly influencing the competitive landscape. Amazon Web Services, Microsoft Azure, and Google Cloud are building relationships with C-suite executives through joint go-to-market initiatives, shifting some advisory influence toward infrastructure providers. In-house consulting units at Fortune 500 companies are intensifying competition by handling routine optimization work, pushing external advisors to focus on transformational mandates. Commodity marketplaces that connect clients with individual experts are capturing smaller projects but lack the scale to manage multi-year programs, allowing incumbents to maintain their hold on complex engagements.

The evolving landscape rewards firms that differentiate through proprietary data sets, industry accelerators, and performance-linked contracts. Companies that can attract and retain multidisciplinary talent while automating low-value tasks will achieve higher margins. On the other hand, firms that are slow to adopt AI-enabled delivery models or partner ecosystems risk becoming commoditized.

US Management Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Limited

Ernst & Young Global Limited

KPMG International Limited

PricewaterhouseCoopers LLP

McKinsey & Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large enterprise transformation budgets continue to shift toward AI-enabled build-and-run programs, creating whitespace for consultancies that can package strategy, engineering, and governance into repeatable offerings rather than bespoke advisory. In 2026, major firms reinforced this direction through named alliances and platform-led practices, including McKinsey and Google Cloud launching the McKinsey Google Transformation Group (April 2026), Deloitte launching an agentic transformation practice with Google Cloud (April 2026), and Bain expanding its partnership with Palantir (March 2026). These moves point to intensifying competition around agentic AI delivery, data platforms, and change adoption at scale, particularly when clients require measurable outcomes and faster deployment.

Public sector modernization programs are also adding a visible lane for consulting growth, with security, compliance, and delivery capability acting as baseline requirements. The Technology Modernization Fund (TMF) issued a July 2026 call for initial project proposals focused on AI capability adoption (with a July 24, 2026 submission deadline), reinforcing near-term demand for firms that can build compliant AI solutions while operating within federal procurement and risk frameworks. IBM Consulting also expanded its asset-based hybrid-AI services in May 2026, including FedRAMP-authorized deployment options on AWS GovCloud, underscoring client pull for implementation-ready offerings that reduce time-to-value in regulated environments.

Recent Industry Developments

- July 2026: The US Federal Trade Commission (FTC) sought public comment on a policy statement addressing AI accuracy and the application of Section 5 of the FTC Act to AI-related practices. The move tightens the operating environment for AI-enabled customer-facing programs and increases demand for consulting support around AI governance, testing, claims substantiation, and documentation.

- September 2025: Huron acquired Wilson Perumal & Company (WP&C), adding strategy and operations consulting talent into its Innosight team. The deal expands Huron's capacity to deliver transformation and operational excellence programs alongside implementation work, raising competitive pressure on mid-tier firms serving large enterprises.

- September 2025: BearingPoint and ABeam Consulting launched a US joint venture, BearingPoint NA LLC, to provide SAP consulting and implementation services, including SAP Business AI. The launch strengthens the ecosystem-led delivery model in ERP modernization and AI-enabled process transformation, where clients increasingly prefer bundled advisory and implementation under a single delivery umbrella.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from third party management consulting work delivered to clients in the United States, where advisory and related implementation support are provided for business and operating decisions.

Scope exclusions: This sizing excludes internal captive consulting teams and spending that sits purely under audit, legal, market research, or training services.

Segmentation Overview

- By Service Type

- Operations Consulting

- Strategy Consulting

- Financial Advisory

- Technology Advisory

- HR Consulting

- Risk and Compliance Consulting

- Other Service Type

- By Client Organisation Size

- Large Enterprises

- Small and Medium Enterprises

- By Consulting Domain

- Enterprise Strategy

- Front-Office Transformation

- Supply-Chain and Operations

- Digital Transformation

- Cyber-Risk and Regulation

- MandA and Restructuring

- Other Consulting Domain

- By End-User Industry

- BFSI

- Life Sciences and Healthcare

- IT and Telecommunications

- Manufacturing and Industrial

- Other End-User Industry

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market perimeter, build the starting demand indicators, and check whether growth patterns look realistic across years. We reviewed public and official sources such as the US Census Bureau Economic Census and County Business Patterns, the Bureau of Labor Statistics series on Professional and Technical Services employment and wages, and BEA national accounts for cross-checking business services activity. We also referenced IRS Statistics of Income where available for industry level receipts context, along with Federal Reserve releases that help explain changes in corporate spending conditions.

To add practical context on how consulting revenues show up in company reporting, we reviewed sources such as SEC filings, annual reports, investor presentations, association publications, and reputable business press coverage of major consulting demand themes. Paid subscriptions for company financials and intelligence, news and financials, and patent databases were used selectively to fill private company visibility gaps and to confirm timing of major demand shifts (for example, technology modernization waves). The desk research sources mentioned here are illustrative and not exhaustive, since many other public documents and data points were reviewed for validation and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test what gets counted as management consulting revenue and to convert high level indicators into working assumptions, especially around billing rates and utilization. We spoke with executives, practice leaders, and delivery managers across the United States, and the feedback was used to confirm service mix, engagement duration patterns, and how demand differs by major client industries.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | |

| Mid tier: 58% | Functional/Unit leaders: 43% | |

| Smaller Players: 16% | Managers: 44% |

Market-Sizing & Forecasting

The model starts with a top-down build of the US consulting revenue pool, using official business statistics for relevant professional services activity and then filtering to management consulting through service mix ratios that were cross-checked in interviews. Once the demand pool is formed, it is linked to practical drivers such as billable headcount, utilization rates, average billable hours, and realized billing rates, and then adjusted for the share of work delivered as advisory plus light implementation support.

To keep totals grounded, we corroborated results with selective bottom-up approximations, including sampled revenue roll ups from public filings, channel checks on common project sizes, and an ASP times volume view for representative engagement types. When company level visibility is limited, gaps are handled using peer group averages and size band scaling, followed by another pass using primary feedback. For forecasting, scenario analysis is used around macro conditions and client budget cycles. The final outlook is anchored on expert consensus for inputs like GDP and business investment expectations, technology transformation intensity, regulatory and compliance workload, and public sector consulting demand.

Data Validation & Update Cycle

Outputs are checked against independent signals such as professional services employment trends, billing rate direction, and the implied revenue per billable employee, so unusual jumps can be questioned early. If year to year variances look too high, assumptions such as utilization, the mix of outcome based pricing, and implementation intensity are reviewed again.

Before sign-off, a multi step analyst review is completed, and any material mismatch triggers targeted re-contact with interviewees for clarification. The report is refreshed annually, with interim updates when major events can change corporate spending or delivery models. Right before publication, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's US Management Consulting Services Market Sizing Compared With Other Published Estimates

Published market sizes for US management consulting services often do not match, and differences usually trace back to what gets counted as consulting revenue, the year used, and how implementation work is treated. Gaps can also appear when one estimate leans heavily on industry codes, while another leans on survey based spend shares and then applies a more aggressive growth path.

Audit and legal professional services revenues sit outside Mordor Intelligence's scope, which helps explain why some broader industry revenue figures land far above the consulting only totals shown here.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 132.34 B (2026) | |

| Industry Database A | USD 411.70 B (2026) | Uses a wide industry revenue definition that can capture broader professional services activity under the same industry code, which can pull in adjacent services beyond fee based management consulting engagements. |

| Syndicated Publisher B | USD 63.09 B (2025) | Uses an earlier base year and a narrower captured revenue pool, and it is not always clear how implementation support and subcontracted delivery are treated in the total, which can suppress the stated market size. |

The spread in the table is mainly explained by scope width and year alignment, rather than a dispute over demand direction. When the market is bounded to fee based consulting engagements and then cross-checked with billable headcount, utilization, and billing rate signals, the total becomes easier to trace and repeat across updates.

Key Questions Answered in the Report

How large is the US management consulting services market in 2026?

The market stood at USD 132.34 billion in 2026, with a projected value of USD 168.46 billion by 2031.

Which consulting domain is expanding fastest?

Digital Transformation leads with a 6.11% CAGR, driven by AI deployment, cloud migration, and cybersecurity mandates.

Why are Technology Advisory services gaining ground?

Enterprises prioritize cloud architecture, generative-AI integration, and zero-trust security, areas that require hands-on implementation alongside strategic guidance.

What is driving demand in the Life Sciences vertical?

Accelerated FDA approval pathways and decentralized clinical trials demand consultancies that combine regulatory expertise with digital-health capabilities.

How are pricing models evolving?

Clients increasingly favor outcome-based or gain-share contracts that tie fees to measurable business improvements rather than billable hours.

Page last updated on: