United States Customer Technical Support Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

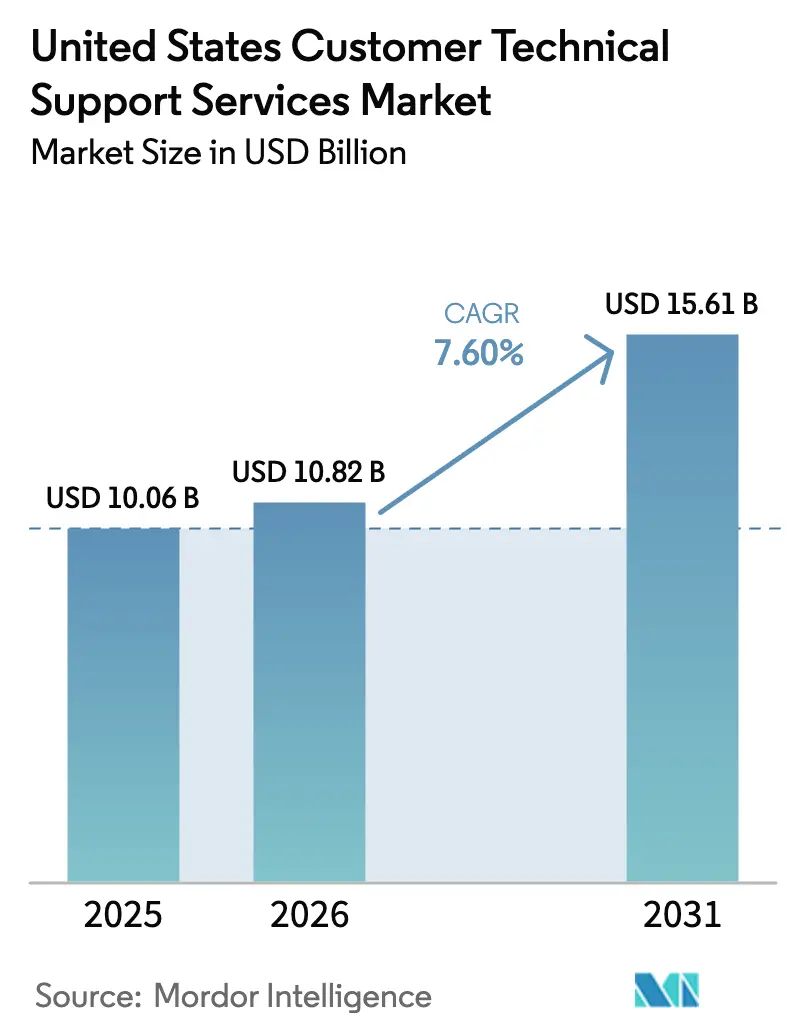

| Base Year Market Size (2025) | USD 10.06 Billion |

| Market Size (2026) | USD 10.82 Billion |

| Market Size (2031) | USD 15.61 Billion |

| Growth Rate (2026 - 2031) | 7.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Customer Technical Support Services Market Analysis by Mordor Intelligence

The customer technical support services market size in 2026 is estimated at USD 10.82 billion, growing from 2025 value of USD 10.06 billion with 2031 projections showing USD 15.61 billion, growing at 7.60% CAGR over 2026-2031. Momentum comes from the rapid uptake of smart-home devices, the expanding remote-work culture and rising adoption of predictive AI diagnostics. Traditional computers and laptops remain the core workload driver, but connected living-room ecosystems are deepening demand for multi-device assistance. Remote and online delivery models dominate because they trim cost per ticket and widen geographic reach, while subscription support bundles are anchoring recurring revenue strategies. Competitive intensity is moderate as telecom carriers, device makers and specialist outsourcers race to embed generative AI in resolution workflows and to secure first-call closure advantages.

Key Report Takeaways

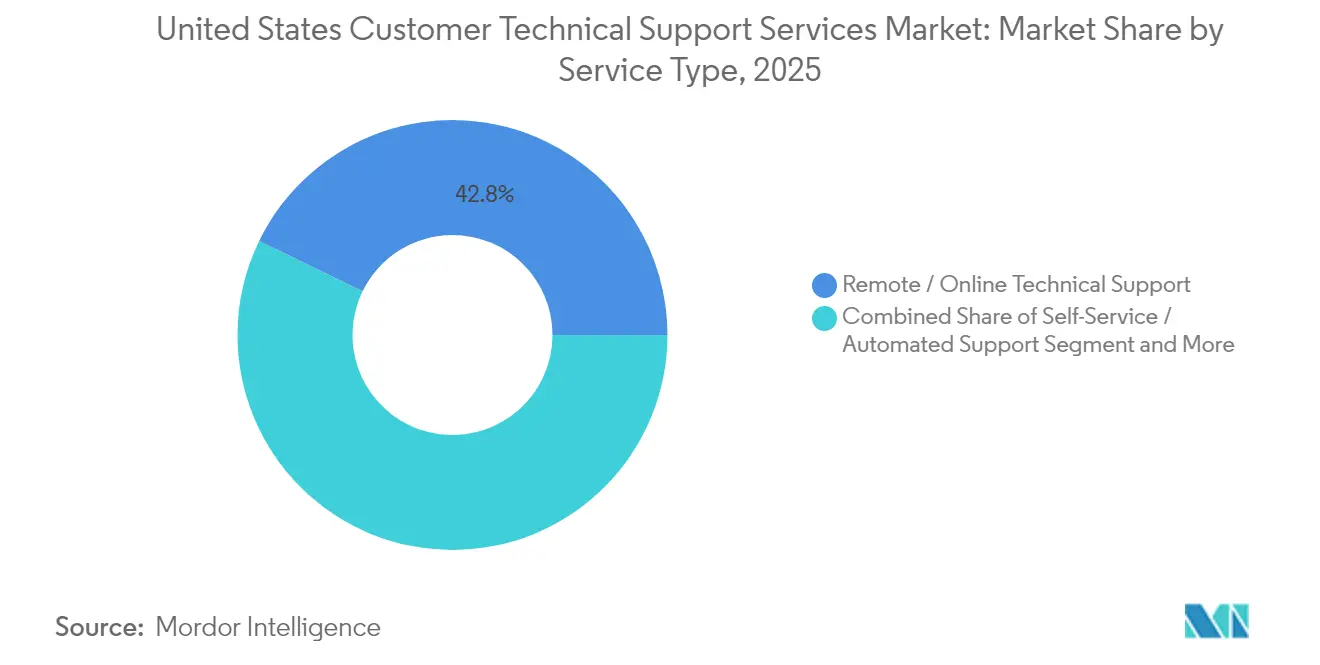

- By service type, remote and online technical support led with 42.80% of customer technical support services market share in 2025, whereas self-service and automated support is projected to expand at an 8.02% CAGR through 2031.

- By device type, computers and laptops accounted for a 33.90% slice of the customer technical support services market size in 2025, while smart-home devices are growing fastest at an 8.55% CAGR to 2031.

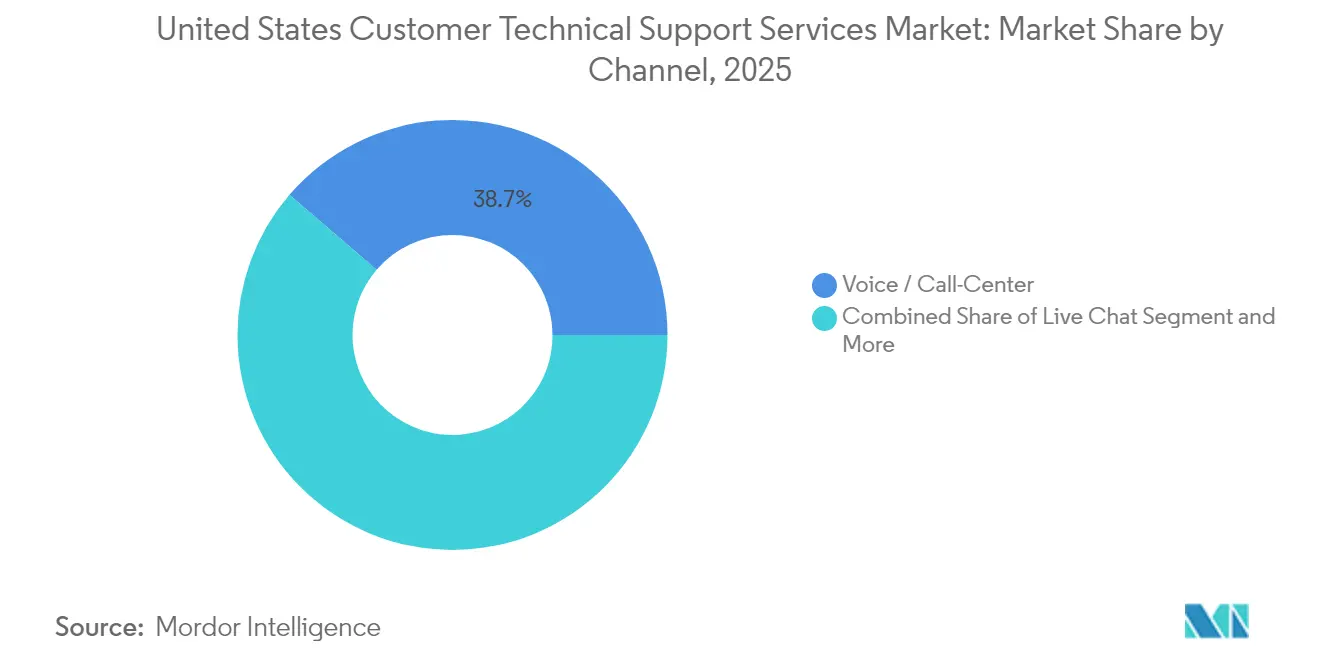

- By channel, voice and call-center interactions held a 38.70% share of the customer technical support services market size in 2025, and social-media support shows the highest growth at an 8.18% CAGR.

- By end-user industry, residential consumers commanded 54.10% of customer technical support services market share in 2025, yet small and medium enterprises are set to post the strongest 7.78% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Customer Technical Support Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing requirement for software updates | +1.8% | National, concentrated in tech hubs | Medium term (2-4 years) |

| Proliferation of smart-home devices | +2.1% | National, higher adoption in suburban areas | Long term (≥ 4 years) |

| Growing complexity of consumer electronics | +1.5% | National, uniform distribution | Medium term (2-4 years) |

| Expansion of remote-work culture | +1.4% | National, concentrated in metropolitan areas | Short term (≤ 2 years) |

| Adoption of predictive-AI diagnostics | +0.9% | National, early adoption in enterprise segments | Long term (≥ 4 years) |

| Rise of subscription tech-support bundles | +0.8% | National, higher penetration in affluent demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Smart-Home Devices

Smart-home installations are reshaping support demand as households juggle device compatibility, cybersecurity and network performance issues. IoT-connected thermostats, cameras and appliances now require technicians who can handle interoperability across multiple protocols and platforms. Healthcare-linked smart-home solutions for remote patient monitoring amplify compliance requirements around HIPAA data handling. Vendors such as Mavenoid have introduced specialized protocols for medical-grade equipment, signaling a deeper need for certified support talent. These dynamics are lifting ticket volumes and lengthening average handling times for residential calls.[1]Absalom E. Ezugwu, “Smart Homes of the Future,” Transactions on Emerging Telecommunications Technologies, wiley.com

Growing Complexity of Consumer Electronics

Hardware makers embed AI features, cloud connectivity and subscription applications in devices, turning post-purchase care into an ongoing relationship. Firmware updates, algorithm tuning and data-privacy inquiries often converge in a single case, driving multi-layered workflows. Apple’s switch to subscription-only AppleCare+ underscores a shift from episodic repairs to lifecycle management.[2]Charles Martin, “Apple to Drop Prepaid Multi-Year AppleCare+, but Keep Subscription Option,” AppleInsider, appleinsider.com As AI accelerates, support teams must tackle questions about model performance, personalization and consent, raising training obligations and boosting resolution times.

Expansion of Remote-Work Culture

Remote work penetration rose from 19.9% to 23.6% nationally, lifting demand for support that extends beyond office firewalls into home networks. Technical agents are now asked to optimize Wi-Fi mesh setups, secure VPN endpoints and integrate productivity suites across mixed operating systems. Providers are investing in screen-sharing diagnostics and self-install kits that lower truck rolls while ensuring compliance with corporate cybersecurity policies. The distributed workforce trend is therefore anchoring remote-first support design.[3]Lumenalta Editorial Team, “7 Examples of Predictive Analytics in Customer Services,” Lumenalta, lumenalta.com

Adoption of Predictive-AI Diagnostics

Predictive analytics is turning support from reactive to proactive by spotting anomalies before users log tickets. Machine-learning models categorize issues, trigger automated patches and prioritize high-risk cases, reducing downtime and trimming average handling time by up to 75%. Successful deployment calls for high-quality telemetry, clear KPIs and a workforce skilled in data interpretation. Investment in these platforms is climbing as providers chase first-contact resolution gains and customer-experience differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising tech-support-related fraud | -1.2% | National, concentrated in vulnerable demographics | Short term (≤ 2 years) |

| High labor and compliance costs | -0.9% | National, higher impact in regulated industries | Medium term (2-4 years) |

| Data-privacy concerns in remote diagnostics | -0.7% | National, stricter enforcement in California | Medium term (2-4 years) |

| Self-service cannibalizing paid support | -1.1% | National, accelerated in tech-savvy demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Tech-Support-Related Fraud

Consumer losses from scams topped USD 175 million in 2023, prompting the Federal Trade Commission to tighten telemarketing rules and impose stronger record-keeping on inbound support calls. Fraudulent voice cloning and deepfake tactics erode trust and push legitimate providers to adopt multi-factor authentication, verified channels and real-time fraud detection. Compliance spend is rising, particularly for outsourcers servicing elderly or low-literacy segments.

Self-Service Cannibalizing Paid Support

AI chatbots and knowledge bases now handle 30-40% of tickets with higher accuracy and faster turnaround than manual triage. While this lifts customer satisfaction for routine queries, it trims billable human-agent volumes and compresses enterprise margins. Provider strategies therefore balance automation with premium live assistance for complex issues, acknowledging that 71% of users still prefer human help when troubleshooting escalates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Remote Support Maintains Leadership

Remote and online assistance accounted for 42.80% of the customer technical support services market size in 2025, reflecting its cost-effective reach and compatibility with distributed work patterns. Subscription-driven programs, such as AppleCare+ and Best Buy memberships, improve lifetime value by bundling priority access, claims handling and device replacement. The self-service and automated support segment, growing at an 8.02% CAGR, benefits from conversational AI and video walkthroughs that resolve simple issues without agent intervention. On-site support remains crucial for enterprise infrastructure rollouts and intricate hardware faults, while managed outsourced support gains traction among budget-constrained SMEs seeking specialized talent. Providers that blend remote diagnostics with field services secure stickier contracts, particularly in regulated verticals that mandate physical verification.

The shift toward predictive maintenance is already reshaping ticket mix. AI engines surface firmware irregularities, prompting pre-emptive outreach that heads off failures and cuts warranty costs. As these capabilities mature, remote resolution is expected to reach 70% of total tickets by 2030, consolidating its market dominance and widening the gap with purely reactive models.

By Device Type: Smart-Home Acceleration Outpaces Legacy Computing

Computers and laptops held 33.90% customer technical support services market share in 2025, tied to their foundational role in productivity and gaming. Smart-home devices, however, register the fastest 8.55% CAGR through 2031 as households adopt connected thermostats, video doorbells and voice assistants. These ecosystems generate cross-device conflicts that elevate troubleshooting complexity. Smartphones and tablets occupy a mature yet stable niche, with calls centering on OS upgrades, cloud sync and app permissions. Consumer electronics such as televisions and consoles see moderate lift, spurred by streaming service integrations and rising esports engagement.

Wearables and ancillary IoT sensors extend support scope into health data and privacy compliance. HIPAA considerations grow in importance when smart-home hubs interface with remote patient monitoring solutions. Providers that certify technicians in medical-device protocols and encryption standards gain an edge when courting healthcare payers and hospital groups.

By Channel: Voice Dominates but Digital Channels Surge

Voice interactions retained 38.70% of the customer technical support services market size in 2025 as callers seek real-time reassurance for complex issues. Investment in AI-guided agent assist and natural-language IVRs is pushing first-call resolution above 90% for leading players such as Verizon’s Project 624. Email and live chat continue to bridge the gap between asynchronous convenience and detailed troubleshooting, while in-app support embeds contextual help directly into software interfaces.

Social media support, growing at an 8.18% CAGR, caters to digitally native consumers expecting rapid brand engagement on public platforms. Providers must balance transparency with data-privacy obligations as sensitive information often surfaces in open threads. Generative AI is enabling sentiment analysis that prioritizes escalations and guides agents toward empathic resolutions.

By End-User Industry: SME Momentum Reconfigures Demand

Residential consumers contributed 54.10% of 2025 revenue, underscoring the ubiquity of multi-device households. Small and medium enterprises, advancing at a 7.78% CAGR, welcome outsourced expertise that keeps pace with cloud migrations, security audits and industry-specific compliance. Their lean staffing models amplify the appeal of managed subscriptions that bundle hardware coverage, software updates and cybersecurity monitoring. Large enterprises continue to purchase high-touch services, focusing on AI-powered analytics, hybrid-cloud orchestration and global service-level agreements.

Differences between enterprise and SME needs are widening. Enterprises demand strategic road-mapping, AI governance and zero-trust security architectures, whereas SMEs prioritize affordability, rapid deployment and consolidated dashboards that simplify oversight. Vendor portals offering tiered service options therefore tailor depth of engagement to organizational maturity.

Geography Analysis

Regional dynamics mirror technology adoption patterns and infrastructure availability. Coastal hubs such as Silicon Valley, Seattle and Austin show the highest ticket density because of concentrated device ownership and early uptake of smart-home ecosystems. These metro areas also host clusters of remote workers whose reliance on cloud collaboration tools raises support complexity. Suburban regions witness accelerating demand as households retrofit legacy wiring with mesh Wi-Fi and smart security systems.

Regulatory variations introduce divergent compliance burdens. California’s Consumer Privacy Act raises documentation and consent requirements for remote diagnostics, prompting providers to deploy stricter data-handling protocols for west-coast tickets. Fraud incidence skews toward states with larger senior populations, necessitating targeted awareness campaigns and multi-factor verification at first contact.

Infrastructure investment is mitigating historical service gaps. Verizon’s planned USD 20 billion acquisition of Frontier Communications aims to extend fiber to 25 million premises across 31 states, unlocking higher-bandwidth remote support and lower latency for AR-based troubleshooting. Talent pools also influence coverage: regions with dense higher-education networks supply ready technicians, whereas rural areas struggle with recruitment, pushing providers toward centralized virtual agent models.

Competitive Landscape

Market structure is moderately fragmented. Integrated hardware-software brands such as Apple, Microsoft, and Dell secure loyalty through proprietary ecosystems and bundled warranty programs. Specialist service firms, including Geek Squad and Asurion, compete on nationwide coverage and device-agnostic expertise, while business-process outsourcers like Concentrix and HCLTech leverage economies of scale to deliver omnichannel support to enterprise clients.

AI capability is the primary battleground. Verizon’s Gemini-powered workflow reports 95-96% first-call resolution, shrinking agent minutes, and boosting satisfaction. HCLTech and Microsoft are co-developing generative AI playbooks that embed “next-best” prompts into agent desktops, reducing training time and standardizing quality. M&A activity is accelerating: Capgemini’s USD 3.3 billion WNS takeover augments its Intelligent Operations portfolio, while IBM’s USD 6.4 billion HashiCorp purchase strengthens hybrid-cloud support for regulated workloads.

United States Customer Technical Support Services Industry Leaders

Infosys Limited

HCL Technologies

Accenture plc

Tata Consultancy Services

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Verizon launched Project 624, an AI-driven service initiative utilizing Google Gemini to achieve 95-96% first-call resolution and longer live-support hours.

- May 2025: IBM announced a USD 6.4 billion acquisition of HashiCorp to enhance hybrid-cloud capabilities and support AI applications.

- March 2025: Verizon Business introduced a GenAI-powered Business Assistant for SMEs, enabling 24/7 automated customer interactions via text messaging.

- February 2025: Apple transitioned AppleCare+ to a subscription-only model, discontinuing prepaid multi-year plans at retail while maintaining online availability.

United States Customer Technical Support Services Market Report Scope

In the United States Customer Technical Support Services Market, companies provide registered users technical support as a service to help clients. Technical help, which was previously only available by phone, is now also available online or through chat. Most large and midsize businesses currently outsource their tech support functions. Many businesses offer online forums where customers may converse about their products. By using these forums, businesses can cut support expenses without sacrificing the value of client feedback.

| On-site Technical Support |

| Remote / Online Technical Support |

| Self-Service / Automated Support |

| Managed (Outsourced) Technical Support |

| Computers and Laptops |

| Smartphones and Tablets |

| Smart-Home Devices |

| Consumer Electronics (TV, Consoles) |

| Others (Wearables, IoT) |

| Voice / Call-Center |

| Live Chat |

| Social Media |

| In-App Support |

| Residential Consumers |

| Small and Medium Enterprises |

| Large Enterprises |

| By Service Type | On-site Technical Support |

| Remote / Online Technical Support | |

| Self-Service / Automated Support | |

| Managed (Outsourced) Technical Support | |

| By Device Type | Computers and Laptops |

| Smartphones and Tablets | |

| Smart-Home Devices | |

| Consumer Electronics (TV, Consoles) | |

| Others (Wearables, IoT) | |

| By Channel | Voice / Call-Center |

| Live Chat | |

| Social Media | |

| In-App Support | |

| By End-User Industry | Residential Consumers |

| Small and Medium Enterprises | |

| Large Enterprises |

Key Questions Answered in the Report

What is the current size of the customer technical support services market in the United States?

The market is valued at USD 10.82 billion in 2026.

How fast is the customer technical support services market expected to grow?

It is projected to advance at a 7.60% CAGR, reaching USD 15.61 billion by 2031.

Which service type leads the market?

Remote and online technical support holds the largest 42.80% share.

Which device category is growing quickest?

Smart-home devices post the highest 8.55% CAGR due to rising IoT adoption.

Page last updated on: