United States Customer Communication Management (CCM) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

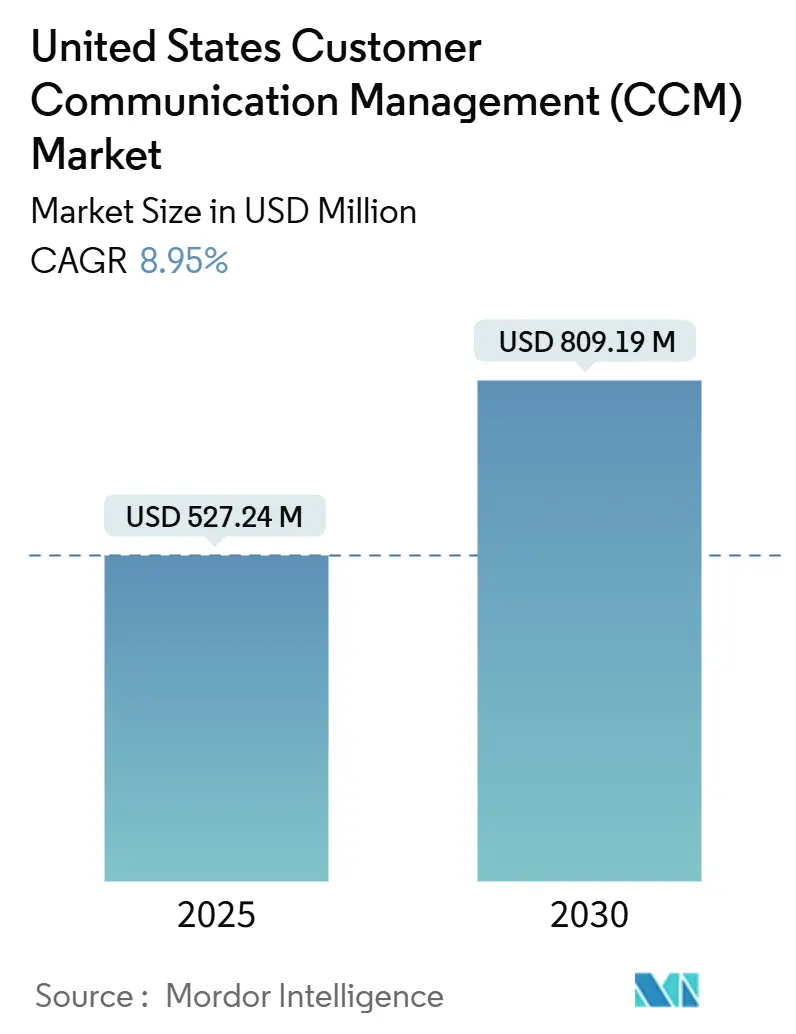

| Market Size (2025) | USD 527.24 Million |

| Market Size (2030) | USD 809.19 Million |

| Growth Rate (2025 - 2030) | 8.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Customer Communication Management (CCM) Market Analysis by Mordor Intelligence

The United States customer communication management market size is USD 527.24 million in 2025 and is projected to reach USD 809.19 million by 2030, registering an 8.95% CAGR. Regulatory mandates, cloud-native platform adoption, and embedded artificial intelligence are accelerating platform refresh cycles, prompting enterprises to shift away from document-centric tools toward real-time, omnichannel engagement hubs. Vendors that unify consent governance, analytics, and AI-driven personalization inside a single stack are winning enterprise deals because they reduce compliance risk and time-to-value. Expanded CPaaS integrations enable real-time, event-triggered messaging, while partnerships with hyperscale clouds shorten implementation timelines. As competitive differentiation shifts to experience management, buyers are increasingly evaluating vendors on guaranteed uptime, template deployment velocity, and measurable ROI, rather than feature counts.

Key Report Takeaways

- By component, software platforms held 48.70% of the United States customer communication management market share in 2024, while services are expected to expand at a 9.20% CAGR through 2030.

- By deployment, the cloud model commanded a 57.40% share of the United States customer communication management market size in 2024 and is forecasted to grow at a 9.80% CAGR to 2030.

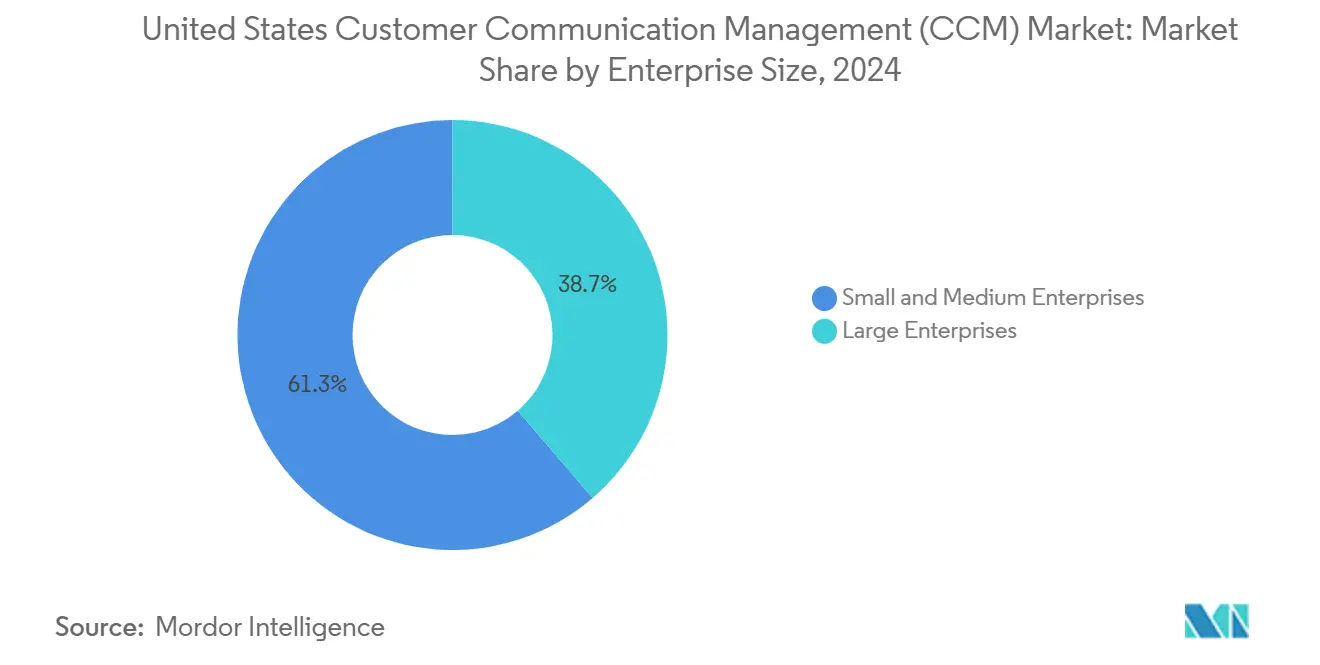

- By enterprise size, small and medium-sized enterprises accounted for a 10.30% CAGR between 2025 and 2030, outpacing the expansion rates of large enterprises.

- By industry vertical, banking, financial services, and insurance captured 26.80% of the United States customer communication management market share in 2024, while healthcare is projected to lead growth at 9.65% CAGR through 2030.

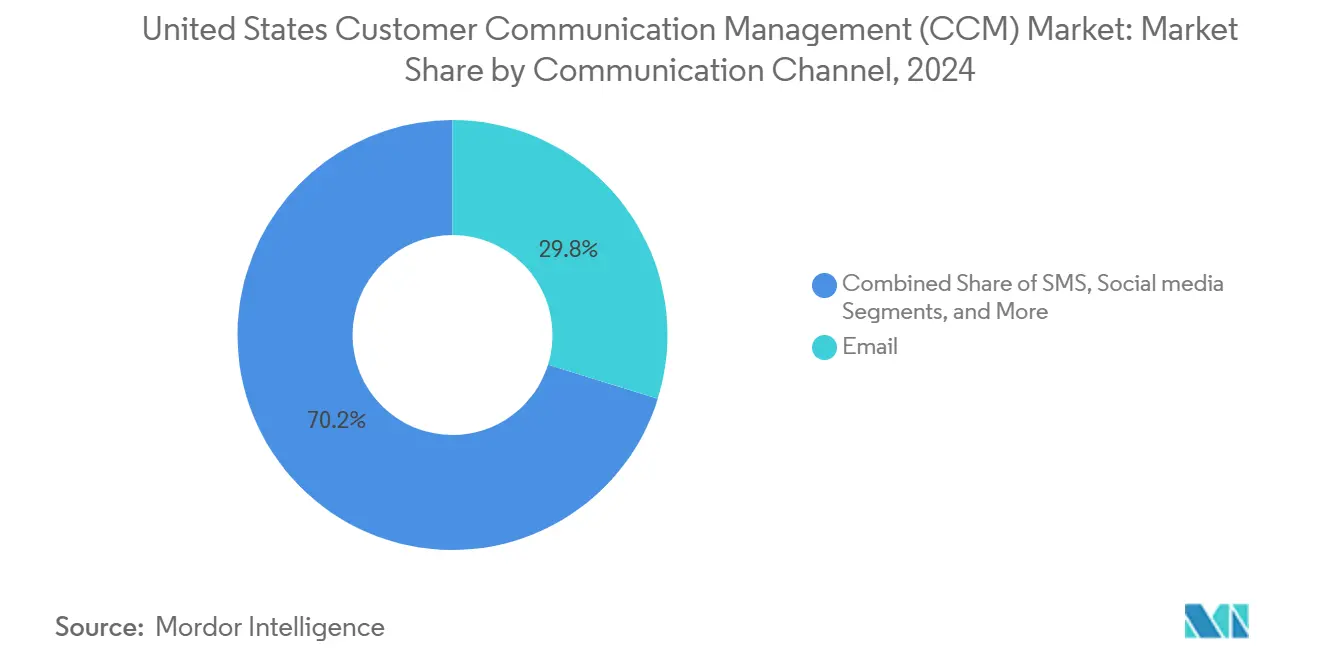

- By communication channel, email led with a 29.80% revenue share in 2024; social media messages are projected to advance at a 10.10% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on customer communication management (ccm) market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Customer Communication Management (CCM) Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerating Migration to Cloud-Native CCM Platforms | +2.1% | National tech hubs | Medium term (2-4 years) |

| Stringent FCC Consent and Opt-Out Rules Driving Compliance Upgrades | +1.8% | Nationwide | Short term (≤ 2 years) |

| Embedded AI-Powered Personalization Capabilities Boosting ROI | +1.9% | Enterprise clusters | Medium term (2-4 years) |

| Omni-Channel Engagement Demand From Digital-First Consumers | +1.4% | Urban and suburban markets | Long term (≥ 4 years) |

| Rise of CPaaS Integration Enabling Real-Time Event-Triggered Communications | +1.6% | Nationwide | Medium term (2-4 years) |

| Transition of Customer Service KPIs From Cost to Revenue Accountability | +1.2% | Nationwide, enterprise segment focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Migration to Cloud-Native CCM Platforms

Enterprises are increasingly decommissioning on-premise suites in favor of elastic, microservices-based solutions that cut hardware costs by 40-60% and support sub-second response times for triggered messages. Cloud control planes deliver weekly feature updates without outage windows, enabling marketing and operations teams to launch new templates in hours rather than weeks. Security certifications, such as SOC 2 and ISO 27001, are now shipped as a baseline, removing historical procurement barriers. Hyperscale data-residency zones satisfy state privacy statutes, while pay-as-you-go pricing aligns communication costs with message volume seasonality. Collectively, these factors transform CCM from a cost center into a growth enabler, solidifying the transition toward cloud as the default architecture.

Stringent FCC Consent and Opt-Out Rules Driving Compliance Upgrades

The FCC’s 2024 consent-revocation order requires companies to honor opt-out requests within 24 hours or face penalties of USD 46,000 per infraction.[1]Enforcement Bureau, “FCC Declaratory Ruling on Consent Revocation,” Federal Communications Commission, fcc.gov High-volume senders in banking and healthcare subsequently replaced batch processes with real-time consent APIs that synchronize preferences across email, SMS, and voice. Modern CCM suites embed rule engines that automatically block non-compliant sends, reducing legal exposure and audit workloads. Vendors with extensive regulatory playbooks now differentiate themselves through ready-made templates that map to federal disclosures and state mini-TCPA clauses. This compliance imperative accelerates refresh cycles, shifting budgets from maintenance toward advanced governance capabilities.

Embedded AI-Powered Personalization Capabilities Boosting ROI

Native machine-learning modules ingest behavioral data, transaction history, and channel engagement to create content variants that increase click-through rates by 25-40% compared to static templates.[2]Azure Marketing Group, “Five Reasons to Move CCM to Azure,” Microsoft, microsoft.com Algorithms dynamically decide send time, subject line, and imagery per recipient, raising campaign revenue and client lifetime value by up to 20%. Predictive models flag consent-risk segments, reducing complaint rates and improving inbox placement. Early adopters report that automated testing and creative generation shrink design timelines from days to minutes, freeing staff for strategic tasks. As gen-AI guardrails mature, firms increasingly demand built-in bias detection and explainability features before green-lighting deployments.

Omni-Channel Engagement Demand From Digital-First Consumers

Consumers expect consistent context when switching between email, mobile push, SMS, and social feeds, compelling firms to unify data models and template logic.[3]Bureau of Consumer Protection, “Omni-Channel Best Practices,” Federal Trade Commission, ftc.gov CCM platforms that orchestrate sequences across channels deliver 23% higher satisfaction scores and 18% more first-contact resolutions versus single-channel programs. Embedded interactive widgets, surveys, video snippets, and one-click service links turn passive documents into two-way experiences. Retailers blend order-status messages with personalized offers, while banks weave advisory content into transaction alerts, driving incremental upsell. This omni-channel imperative drives vendors to expand their API libraries and integrate canned connectors for CRM, analytics, and CPaaS stacks.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Integration Complexity With Legacy Core Systems | -1.4% | Large-enterprise segment | Medium term (2-4 years) |

| Growing Litigation Risk Under Expanding State Mini-TCPA Laws | -1.1% | Select states | Short term (≤ 2 years) |

| Skills Gap In CCM Template Design And AI Governance | -0.9% | National, acute in technical roles | Long term (≥ 4 years) |

| Saturation Of Martech Stack Leading To Tool Under-Utilization | -0.8% | National, enterprise segment focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity With Legacy Core Systems

Many top-tier banks and insurers still operate batch-oriented mainframes that lack real-time APIs, resulting in expensive middleware projects that can double the initial CCM budgets. Schema mapping, data-quality remediation, and service-bus configuration routinely extend deployments by 6-12 months. Organizations juggling multiple heritage stacks face higher maintenance overhead, as each new template must pass through custom integration gates. Without concerted modernization, firms risk relegating CCM upgrades to ancillary channels, limiting full journey orchestration. Vendors now counter by shipping pre-built connectors and low-code tooling, yet deep legacy entanglements remain a gatekeeper for rapid scale-out

Growing Litigation Risk Under Expanding State Mini-TCPA Laws

California, Florida, and Oklahoma have added mini-TCPA statutes that layer specific consent wording and opt-out pathways on top of federal rules.[4]Office of the Attorney General, “California Consumer Privacy Act Updates 2025,” State of California Department of Justice, oag.ca.govPlaintiff firms target automated dialers and bulk-messaging flows, seeking statutory damages of USD 500–1,500 per unauthorized contact. Multistate brands, therefore, require geo-fencing logic and proof-of-consent audit trails inside CCM workflows. Each additional jurisdiction increases the number of testing permutations, thereby raising operational complexity and costs. Until a harmonized federal preemption emerges, enterprises must fund continuous rule-set updates and dedicated compliance officers, which moderately temper the adoption velocity in heavily regulated sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Sustain Momentum Amid Platform Upgrades

Service revenue is growing at a 9.20% CAGR as firms lean on systems integrators for template design, data mapping, and journey optimization projects. Software platforms still account for 48.70% of the overall United States customer communication management market share, driven by document composition and omnichannel orchestration engines. Consulting bundles now include ROI modeling, KPI dashboards, and consent-risk audits, expanding the scope of engagement beyond the initial rollout. Meanwhile, vendors productize accelerators, pre-approved healthcare templates, and banking disclosures that shorten delivery cycles and shift billable hours toward higher-margin advisory tasks.

Platform sub-segments reveal sustained demand for document composition, interactive editing, and analytics. Batch statement generation persists in finance, but interactive documents that enable two-way data collection are gaining popularity. Email engines broaden into behavior-triggered sequences, while SMS and push APIs gain adoption for urgent, time-sensitive alerts. Workflow automation modules embed decisioning to auto-route approvals and content localization. As analytics suites surface real-time engagement metrics, enterprises A/B test subject lines, layout, and call-to-action placement, refining template libraries on the fly for superior campaign ROI.

By Deployment: Cloud Dominance Accelerates

Cloud deployments commanded 57.40% of the United States customer communication management market in 2024. The segment’s 9.80% CAGR is driven by elastic scaling, managed security, and faster feature velocity. Organizations migrating to hosted architectures report 50-70% shorter campaign launch times and 30-40% better system uptime. Hybrid deployment models are growing in highly regulated verticals, allowing sensitive data to remain on private subnets while templating, analytics, and AI modules reside in multitenant clouds.

On-premise suites remain in defense and select public-sector workloads bound by sovereign data regulations, yet ongoing FedRAMP and StateRAMP certifications are eroding these carve-outs. Vendors invest heavily in zero-trust frameworks, encryption at rest, and key management services to satisfy evolving policies. Price-point convergence between private-cloud hosting and capex for hardware refresh further tilts the calculus toward subscription licenses.

By Enterprise Size: SME Adoption Accelerates Through SaaS Accessibility

Small and medium enterprises are posting a 10.30% CAGR, the fastest across any buyer group, thanks to consumption-based billing and low-code template editors. SaaS vendors bundle pre-built integrations for CRM and accounting packages, eliminating the need for heavy IT lift and shortening proof-of-concept cycles to weeks. Large enterprises still control 38.70% of 2024 revenue; however, procurement is shifting from perpetual licenses to enterprise agreements that flex with message volume.

The democratization of AI, automated copy generation, and image-selection wizards enables SMEs to deliver experiences once exclusive to Fortune 500 peers. Built-in compliance libraries simplify state privacy and consent requirements, mitigating litigation exposure for resource-constrained teams. At the top end, conglomerates demand advanced features such as multi-brand tenant stacking, regulatory disclosure management, and real-time language localization. Vendors, therefore, architect multiscale environments capable of underpinning both a 10-user SaaS workspace and a 10,000-user global rollout within a unified codebase.

By Industry Vertical: Healthcare Emerges as Growth Leader

Healthcare is expanding at a 9.65% CAGR as hospitals, insurers, and telehealth platforms modernize outbound patient communications to satisfy engagement mandates and value-based care metrics. Appointment reminders, treatment plan summaries, and post-visit education packets transition from print to interactive digital formats. The United States customer communication management market size for healthcare is expected to double over the forecast horizon as providers embed secure messaging inside patient portals. Banking, financial services, and insurance remain the largest customer cohort, with a 26.80% share, deploying CCM for e-statements, policy updates, and fraud alerts that require stringent compliance controls.

Retail and e-commerce players leverage batch transactional messages, order confirmations, shipping alerts, and layer AI-driven product recommendations to raise conversion rates. Telecommunications companies automate service-activation notices and usage-threshold alerts to reduce the load on their contact centers. Government agencies adopt CCM to enhance citizen-service transparency through digital correspondence, while energy utilities implement outage notifications and consumption analytics. Each vertical’s priorities shape template kits and governance modules, prompting vendors to ship domain-specific accelerators that speed solution adoption.

By Communication Channel: Social Media Catalyzes Diversification

Email retains a 29.80% share and remains indispensable for formal documentation, regulatory notices, and long-form content. Yet, social messaging APIs, from Facebook Messenger to WhatsApp Business, are advancing at a 10.10% CAGR, reflecting consumer appetite for real-time, multimedia interaction. SMS remains the go-to medium for two-factor authentication and urgent alerts, with stable mid-single-digit growth.

Interactive documents with in-line video, dynamic charts, and one-click surveys enhance the efficacy of traditional email, blurring the boundary between channels. Web portals and native apps provide self-service spaces where users can access their bills and update preferences without needing agent assistance. Voice assistants remain an emerging niche; early pilots in banking deliver account balances via Alexa or Google Assistant. Channel orchestration engines within CCM suites sequence touchpoints based on engagement history, optimizing message cadence and reducing fatigue.

Geography Analysis

Technology corridors such as Silicon Valley, Seattle, and Austin account for the highest platform penetration, driven by start-ups that prioritize experience architecture as a competitive edge. Financial services clusters in New York, Charlotte, and Chicago align investments with regulatory communication requirements, thereby spurring the implementation of advanced consent management solutions. Healthcare systems in Houston, Minneapolis, and Boston deploy CCM to support telehealth workflows and reduce no-show rates across large patient bases.

States enforcing stringent privacy acts, notably California under the CCPA, stimulate demand for built-in data-subject-rights automation. Texas energy retailers utilize CCM for outage alerts and usage analytics tailored to smart meter data, while Florida’s aging population drives healthcare providers to adopt multichannel reminder systems that improve medication adherence. Public-sector modernization grants in the Midwest are accelerating the development of citizen-notification portals, signaling a future uplift beyond coastal technology centers.

Uniform federal FCC consent mandates establish nationwide baseline capabilities, but divergent state enforcement intensifies compliance complexity for brands operating in all 50 states. This dynamic favors vendors with geo-aware suppression lists and rules-as-code libraries that adapt templates to account for jurisdictional nuances. As litigation risk rises in headline states, enterprises in neighboring regions proactively upgrade to mitigate potential exposure, propagating CCM adoption inland.

Competitive Landscape

The market remains moderately concentrated, with Quadient, OpenText, and Smart Communications anchoring the 2024 revenue tables, while cloud-native upstarts and CPaaS suites steadily chip away at their share. Incumbents leverage decades-old document composition leadership, broad partner ecosystems, and deep regulatory content libraries to retain large-enterprise contracts. Emerging vendors differentiate via microservices, AI-first design, and low-code builder experiences that resonate with digital-native buyers.

Strategic acquisitions reshuffle capability maps. Quadient’s YayPay takeover knitted accounts receivable workflows into its CCM stack, extending customer lifecycle coverage beyond messaging. Hyland’s integration of Nuxeo fused content services with communication templates, producing a single pane for customer-experience managers. OpenText embedded generative AI to auto-draft personalized messages at scale. CPaaS giants Twilio and Vonage expand from API messaging into template storage and consent vaults, challenging traditional CCM value propositions.

Partnership ecosystems intensify; Messagepoint’s Azure Marketplace listing grants frictionless procurement for Microsoft 365 and Dynamics 365 clients. Kofax adds embedded analytics to tie engagement metrics directly to operational KPIs, while Cincom pushes mobile-first designers who democratize template updates. As vendor value gauges shift from “features shipped” to “conversion points saved,” proof-of-performance dashboards become central to renewal negotiations.

United States Customer Communication Management (CCM) Industry Leaders

Quadient SA

OpenText Corporation

Smart Communications Inc.

Messagepoint Inc.

Cincom Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Quadient completed its USD 120 million acquisition of YayPay, linking accounts-receivable automation with CCM workflows.

- September 2024: OpenText launched Experience Cloud, embedding generative AI to craft personalized content at scale.

- August 2024: Smart Communications secured USD 75 million in Series D funding, led by Insight Partners, to accelerate its cloud development.

- July 2024: Hyland Software acquired Nuxeo for USD 85 million to marry content services with customer communications.

United States Customer Communication Management (CCM) Market Report Scope

| Software | Document Composition |

| Email Marketing | |

| SMS and Push Notifications | |

| Interactive Documents | |

| Other Softwares | |

| Services |

| On-premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare |

| Telecom and IT |

| Retail and eCommerce |

| Government |

| Other Industry Verticals |

| SMS |

| Web and Mobile Portals |

| Social media |

| Chatbots and Voice Assistants |

| By Component | Software | Document Composition |

| Email Marketing | ||

| SMS and Push Notifications | ||

| Interactive Documents | ||

| Other Softwares | ||

| Services | ||

| By Deployment | On-premise | |

| Cloud | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Industry Vertical | BFSI | |

| Healthcare | ||

| Telecom and IT | ||

| Retail and eCommerce | ||

| Government | ||

| Other Industry Verticals | ||

| By Communication Channel | ||

| SMS | ||

| Web and Mobile Portals | ||

| Social media | ||

| Chatbots and Voice Assistants |

Key Questions Answered in the Report

What is the current value of the United States customer communication management market?

It is USD 527.24 million in 2025.

How fast is cloud deployment growing within U.S. CCM solutions?

Cloud adoption is advancing at a 9.80% CAGR through 2030, moving from 57.40% share in 2024 toward two-thirds of spending.

Which industry vertical is projected to grow fastest?

Healthcare leads with a 9.65% CAGR due to patient engagement mandates and the expansion of telehealth.

Why are SMEs adopting CCM platforms rapidly?

Low-code SaaS models eliminate heavy IT lift and align subscription costs to growth, spurring a 10.30% CAGR in SME spending.

What regulatory change most affects CCM roadmaps today?

The FCCs 24-hour consent-revocation rule drives immediate investment in real-time preference management APIs.

Which communication channel shows the highest forecast growth?

Social media messaging APIs are projected to expand at a 10.10% CAGR through 2030 as consumers favor interactive, multimedia exchanges.

Page last updated on: