Spain Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

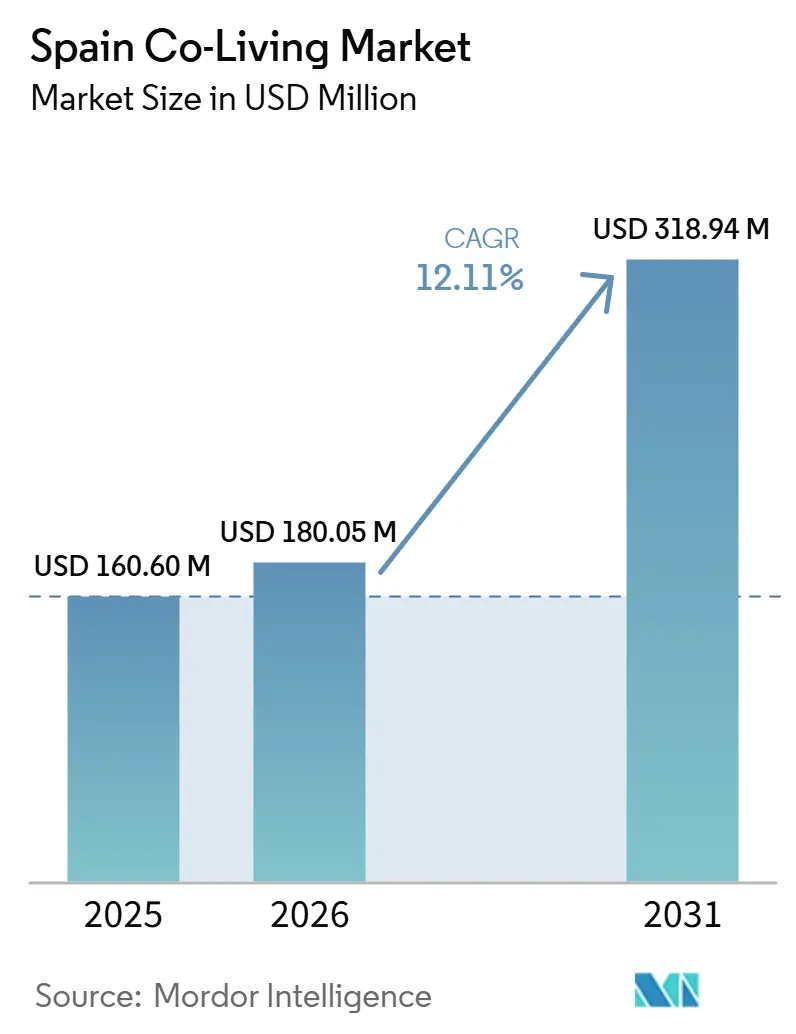

| Base Year Market Size (2025) | USD 160.60 Million |

| Market Size (2026) | USD 180.05 Million |

| Market Size (2031) | USD 318.94 Million |

| Growth Rate (2026 - 2031) | 12.11% CAGR |

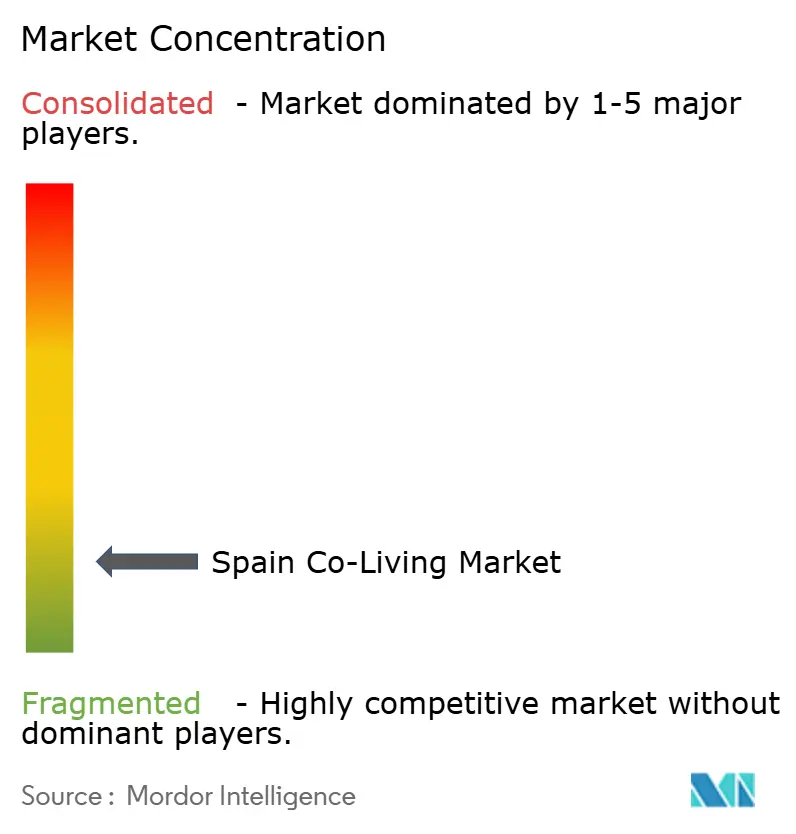

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Co-Living Market Analysis by Mordor Intelligence

The Spain Co-Living Market size is expected to grow from USD 160.60 million in 2025 to USD 180.05 million in 2026 and is forecast to reach USD 318.94 million by 2031 at 12.11% CAGR over 2026-2031.

The Spain co-living market is expanding because Spain’s urban housing system remains short of supply, with a 500,000-home gap still shaping renter behavior in 2025. That shortage has made flexible, service-led housing more relevant for people who need quick access to city accommodation without the friction of long leases, guarantors, and separate utility setup. The Spain co-living market is also drawing larger pools of capital, and recent transactions by Greystar, Neinor Homes, Banco Santander, and PATRIZIA show that the category has moved beyond pilot assets into platform building and planned portfolio growth. Even so, the Spain co-living market still faces a mixed regulatory setting because operators must navigate national rules, regional housing law, and local planning regulations simultaneously, which affects speed to market and project structure.

Key Report Takeaways

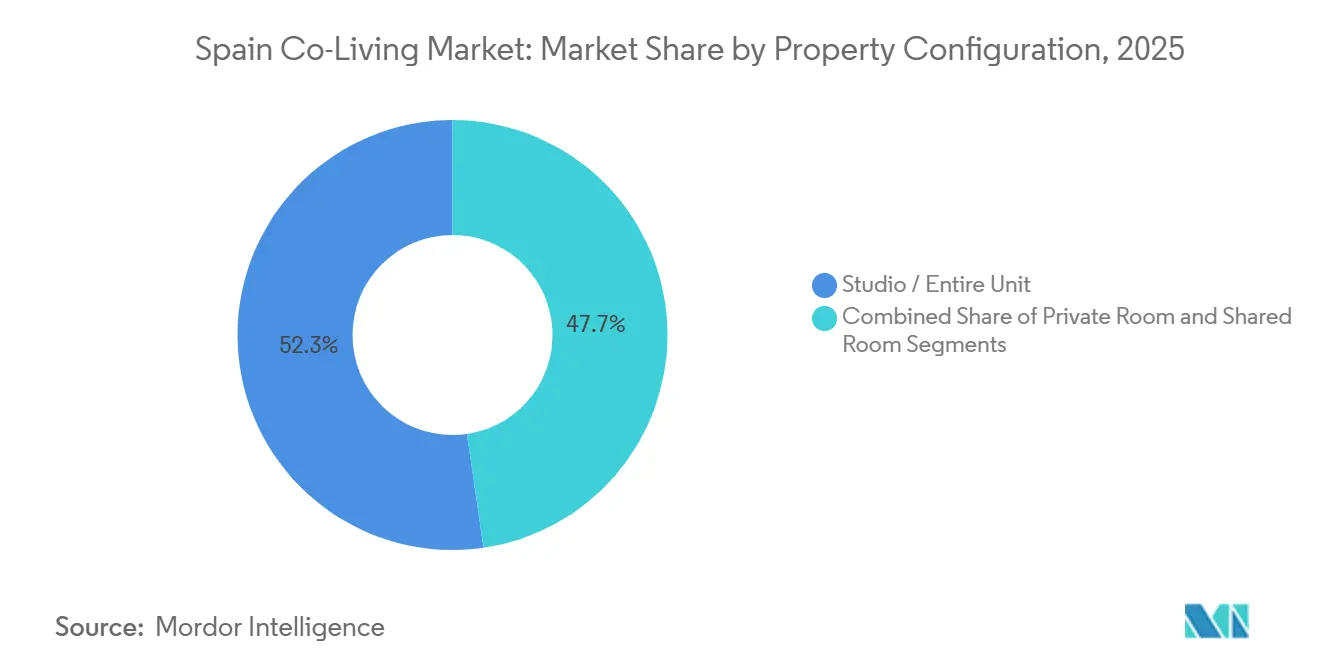

- By property configuration, studio and entire-unit formats held 52.3% of the Spain co-living market share in 2025, while shared rooms are forecast to expand at a 12.78% CAGR through 2031.

- By business model, asset-light master lease or lease arbitrage accounted for 45.1% of the Spain co-living market share in 2025, while the same segment is also projected to record the highest CAGR at 13.12% through 2031.

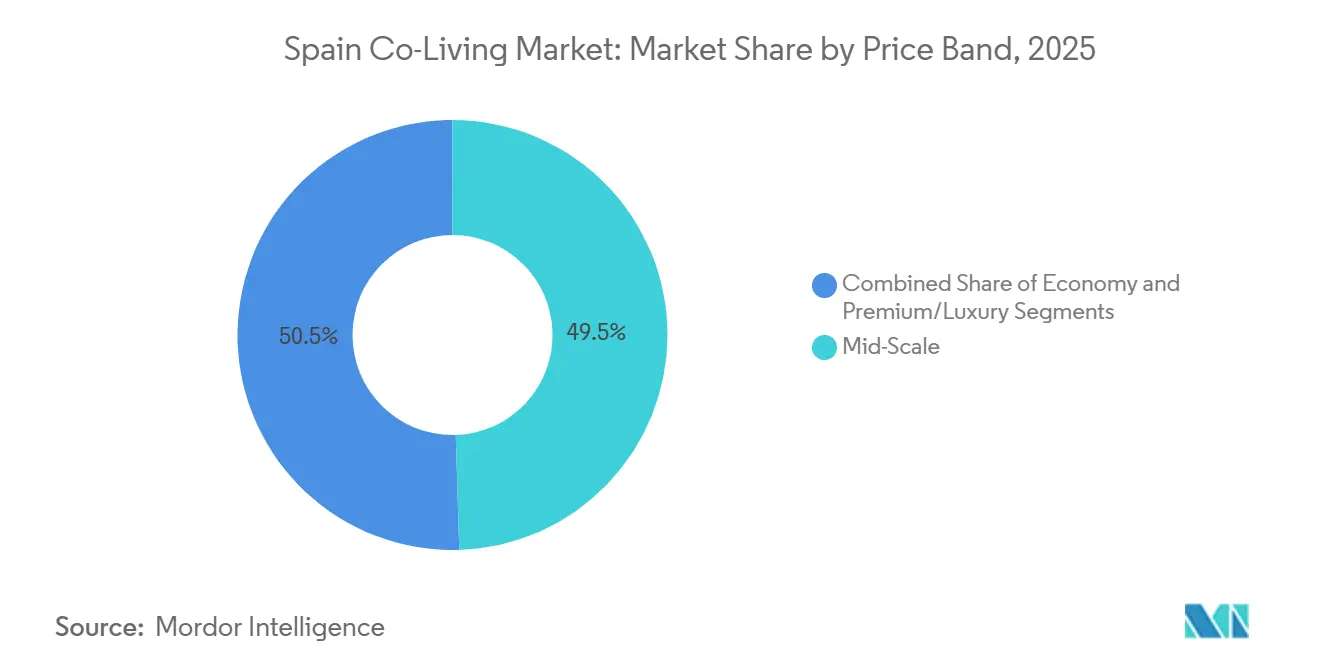

- By price band, mid-scale commanded 49.5% of the Spain co-living market size in 2025, while premium and luxury is forecast to grow fastest at a 13.44% CAGR through 2031.

- By end user, students represented 47.5% of the Spain co-living market size in 2025, while working professionals are projected to advance at a 13.71% CAGR through 2031.

- By geography, Madrid captured 53.2% of the Spain co-living market share in 2025, while Valencia is expected to post the fastest growth at a 13.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban housing affordability pressure | +4.2% | Madrid and Barcelona, with spillover into Valencia and Málaga | Short term (≤ 2 years) |

| Growth in digital nomad, expatriate, and remote worker demand | +2.6% | National, with early concentration in Madrid, Barcelona, Valencia, and Málaga | Short term (≤ 2 years) |

| Higher investor interest in alternative residential assets | +2.0% | National, led by Madrid and supported by expanding secondary city activity. | Medium term (2-4 years) |

| Expansion of operators serving young professionals and international residents | +1.6% | Madrid and Barcelona first, then Valencia, Bilbao, and Seville | Medium term (2-4 years) |

| Growth in technology, startup, and service-sector employment | +1.0% | Madrid, Barcelona, and Valencia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Housing Affordability Challenges in Madrid and Barcelona Channel Demand into Co-living Accommodation

The Spain co-living market is benefiting from a housing system that remains short of supply in its largest cities. The 500,000-home gap shows why managed shared housing is becoming a practical option rather than a niche choice[1]PATRIZIA SE, “PATRIZIA And Urbania Launch Joint Venture Exceeding EUR 130 Million To Develop Sustainable And Affordable Housing In Spain,” PATRIZIA News, patrizia.ag. When renters cannot easily secure conventional units, they place greater value on ready-to-move accommodation that includes utilities, furnishings, and community space. This matters because co-living removes several upfront hurdles at once, including deposits across multiple service accounts, furniture costs, and long setup periods. In that setting, the Spain co-living market is not only attracting residents who want lower friction, but also capturing demand from people who would otherwise stay longer in informal or temporary housing arrangements.

Growing Digital Nomad, Expatriate, and Remote Worker Populations Support Flexible Housing Demand

The Spain co-living market is also drawing support from mobile residents whose housing needs differ from those of long-settled local households. The draft shows that digital nomads, expatriates, and remote workers often arrive without local credit records, domestic guarantors, or established banking relationships, which makes obtaining standard lease access more difficult. Co-living fits this group because contracts are simpler, move-in is faster, and the package already includes the daily living services that new arrivals usually need first. This user profile also values location, broadband quality, and shared work areas, so operators that combine housing with a strong digital leasing process are better placed to hold occupancy. As this mobile renter base widens, the Spain co-living market gains a layer of demand linked to labor mobility and cross-border relocation rather than solely to local housing stress.

Increasing Investor Interest in Alternative Residential Asset Classes with Stable Occupancy Rates

The Spain co-living market is attracting more institutional capital because investors now see flexible housing as a scalable residential platform. Greystar strengthened its position through the acquisition of Bain Capital assets in January 2025, and Neinor Homes formed a co-investment structure with Banco Santander in February 2025 for a flex living project near Madrid[2]Bain Capital, “Bain Capital Announces Sale Of Co-Living Space In Spain To Greystar,” Bain Capital News, baincapital.com. PATRIZIA and Urbania also launched a joint venture in May 2025 focused on sustainable, affordable housing in major Spain metropolitan areas, indicating that capital is being directed into larger development pipelines rather than isolated assets. That shift matters because larger investors can fund land, design, and delivery over longer timeframes, helping them build national exposure. At the same time, smaller operators remain more constrained by financing and access to assets. The result is that the Spain co-living market now has stronger capital backing, but also a tougher operating environment for firms that cannot match institutional scale.

Expansion of Co-living Operators Targeting Young Professionals and International Residents

The Spain co-living market is broadening as operators no longer limit expansion to a small number of showcase buildings. Greystar’s expanded platform, Neinor’s flex-living entry, and Hines’s move into a 650-bed Valencia asset all point to a sector spreading across different cities and demand pools[3]Neinor Homes, “Neinor Homes Steps Into Flex Living With Banco Santander And Will Co-Invest €60mn In A Project Located In Madrid,” GlobeNewswire, globenewswire.com. This pattern is important because young professionals and international residents do not all want the same product, and operators now have to cover studio units, private rooms, and managed communities across different price points. It also underscores the importance of local execution, since city-level planning, zoning, and housing rules still shape the format that can be brought to market. As more operators enter or scale, the Spain co-living market is moving toward a broader competitive field with clearer specialization by resident type, city, and service model.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty in short-term rentals and shared housing | -1.5% | National, with the strongest effect in Barcelona and Catalonia, and growing relevance in Madrid and Valencia | Short term (≤ 2 years) |

| Rising construction and acquisition costs | -1.2% | National, with the strongest cost pressure in Madrid and Barcelona | Medium term (2-4 years) |

| Limited supply of suitable urban conversion assets | -0.9% | Core districts in Madrid and Barcelona, with pressure moving into Valencia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty Regarding Short-Term Rentals and Shared Housing Models

The Spain co-living market still operates without a single national statute that clearly defines co-living across all use cases. Spain implemented Royal Decree 1312/2024 on July 1, 2025, which created a unified lease registry and a digital single window for short-term rental data, in line with European Union Regulation 2024/1028. Organic Law 1/2025 also gave residential communities the power to block new tourist-classified accommodations in their buildings with a three-fifths owner majority, adding another layer of approval risk to mixed-use or mixed-ownership properties. Catalonia and Andalusia have moved in different directions, and Catalonia’s Law 11/2025 adds another regional layer that operators must track alongside local planning treatment. Because the legal path still varies by city and region, the Spain co-living market remains harder to scale nationally than demand figures alone might suggest.

Rising Construction and Property Acquisition Costs Affecting New Project Development

The Spain co-living market is also constrained by economic conditions that have made it more difficult for new projects. The draft shows that rising construction costs, higher new-build values, labor scarcity, and long approval timelines are all making greenfield delivery less straightforward, especially in Madrid and Barcelona. These factors raise the cost per bed and make pricing decisions more sensitive, while still maintaining accessibility for students, early-career professionals, and mobile workers. They also help explain why asset-light models keep gaining ground, since leasing or repositioning existing buildings usually requires less capital than buying land and delivering new stock from scratch. For the Spain co-living market, this means that part of future growth will depend on how well operators secure existing urban assets and control fit-out costs, rather than solely on how much demand exists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Studio Units Hold Volume Leadership as Shared Rooms Scale Rapidly

Studio and entire-unit formats accounted for 52.3% of the market in 2025, making them the largest configuration in the Spain co-living market. That lead shows that many residents want privacy in their units while still using shared kitchens, work areas, lounges, or fitness spaces elsewhere in the building. The format also suits operators who want a broader customer base, because self-contained units are easier to market to professionals, relocators, couples, and residents staying for longer periods. Shared rooms are expected to post the fastest growth, with a 12.78% CAGR through 2031, indicating that affordability pressure remains strong and creates room for lower-cost offerings.

This split gives the Spain co-living market a two-track product structure. Studio-led supply supports revenue stability because private formats tend to appeal to residents who can pay more for autonomy, consistency, and predictable occupancy. At the same time, shared rooms are likely to absorb incremental demand where rent pressure remains high and access to standard leases stays difficult. The Spain co-living market, therefore, does not move in a single direction on product design, because the largest segment favors privacy. In contrast, the fastest-growing segment reflects cost sensitivity and the need for lower entry price points.

By Business Model: Master Lease Economics Dominate as Own-Develop-Operate Scales for Long-Term Returns

Asset-light master lease or lease arbitrage accounted for 45.1% of the market in 2025, making it the largest business model in the Spain co-living market. Its lead reflects a practical fit with a market where operators need speed, lower upfront capital, and room to adjust portfolios city by city. Under this structure, the operator secures control of the building through a lease and then manages the resident relationship, pricing, furnishing, and service package directly. The same segment is also projected to record the highest growth at a 13.12% CAGR through 2031, which confirms that capital discipline and operating flexibility remain central to expansion plans.

The asset-heavy own-develop-operate route still matters, especially for firms backed by stronger capital pools and long investment horizons. Neinor Homes and Banco Santander entered flex living through a co-investment structure in February 2025, which shows that development-led participation remains relevant when the project location and exit horizon are attractive. Even so, the Spain co-living market still leans toward models that reduce capital exposure and enable faster city entry, especially while regulation, construction costs, and asset access remain uneven across regions. This is why the largest and fastest-growing models are in the same segment in the current structure.

By Price Band: Mid-Scale Commands Volume as Premium Tier Drives Fastest Revenue Growth

Mid-scale held 49.5% of the market in 2025, which gives it the broadest volume base in the Spain co-living market. This band meets the needs of students and early-career professionals who want a managed living setup but still need pricing below premium formats. Mid-scale also fits the operating logic of many providers because it balances service scope with occupancy potential across larger urban renter pools. Premium and luxury are forecast to expand at a 13.44% CAGR through 2031, indicating that the upper end is gaining traction even as the center of demand remains more price-sensitive.

The fastest growth in premium and luxury reflects demand from digital nomads, corporate relocators, and international residents who place value on design, brand, location, and community programming. This does not weaken the role of mid-scale, because the Spain co-living market still relies on a larger base of residents whose budgets support managed housing only when pricing stays within reach. The economy tier remains the least developed part of the structure, leaving a gap between strong affordability needs and limited institutional supply. For the Spain co-living market, that means future revenue growth can come from premium formats. At the same time, unit volume still depends heavily on mid-scale products that can hold broader occupancy across city markets.

By End User: Students Anchor Demand While Working Professionals Lead Growth

Students accounted for 47.5% of the market in 2025, which made them the largest end-user group in the Spain co-living market. This lead fits a housing environment where many students still face limited access to organized rental options and need furnished accommodation near transport, education hubs, and city services. Student demand is also easier for operators to plan around because academic cycles, move-in timing, and shared living preferences create recurring occupancy patterns. Working professionals are projected to grow fastest at a 13.71% CAGR through 2031, indicating that employment-related mobility is becoming increasingly important to future demand.

The tenant profile shared in Neinor Homes’ February 2025 communication helps explain why the working professional segment is rising so quickly: a typical flex living resident is aged 31, 73% single, and 61% foreign. That mix supports the view that the Spain co-living market is no longer shaped solely by student demand, as it also serves professionals who value mobility, simple contracts, and service-integrated housing. Students still anchor occupancy and scale, but working professionals are pushing the sector toward more flexible lease terms, stronger amenities, and city locations that work for both living and remote work. This shift broadens the addressable resident base without changing the fact that students remain the largest user group today.

Geography Analysis

Madrid accounted for 53.2% of the market in 2025, which made it the leading geography in the Spain co-living market. Barcelona remained the second-largest city market, and together the two cities still form the main base of current organized supply and operator visibility. Madrid’s position is supported by stronger institutional participation, as seen in transactions such as the Neinor Homes and Banco Santander flex living venture near Madrid. Greystar also strengthened its footprint through assets in Madrid, Barcelona, and Bilbao, underscoring the role of Madrid and Barcelona as anchor locations for scaled platform growth.

Valencia is projected to grow fastest at a 13.66% CAGR through 2031, giving it the clearest growth position beyond the two largest cities. Its appeal stems from a more accessible operating base and a demand mix that serves both students and working professionals. Hines expanded into Valencia through the acquisition of a 650-bed flex-living complex, underscoring that international capital is treating the city as a serious residential asset destination. In value terms, Madrid led the Spain co-living market with 53.2% of the market share in 2025, while Valencia is set to post the fastest city growth over the forecast period.

The rest of Spain, including cities such as Málaga, Seville, and Bilbao, remains smaller in absolute size but increasingly relevant to the Spain co-living market. These cities matter because they extend the operator map beyond the largest hubs and allow firms to build portfolios that balance current scale with future growth. The Spain co-living market will likely become less geographically concentrated as more capital moves into secondary locations, where competition for suitable assets is still less intense than in Madrid and Barcelona. Geography, therefore, reflects a split between scale in Madrid, sustained demand in Barcelona, and higher growth momentum in Valencia and the wider secondary city group.

Competitive Landscape

The Spain co-living market remains fragmented at the operator level, but it is moving toward faster consolidation at the platform level. Greystar strengthened its position in January 2025 through the acquisition of Bain Capital’s Spain portfolio, which added a larger furnished living base across multiple cities. PATRIZIA and Urbania launched a joint venture in May 2025 to develop sustainable, affordable housing across major Spain metropolitan areas, demonstrating that larger capital pools are backing longer-term pipeline strategies. Neinor Homes and Banco Santander also entered the space through a co-investment model, reinforcing the point that major players are using partnerships to secure land, capital, and operating optionality.

Competition in the Spain co-living market now depends as much on access to funding and city-level execution as it does on day-to-day property operations. Large platforms can move faster because they can combine acquisition, development, and branding within one structure, while smaller operators often remain tied to single-city or single-asset strategies. The Bain Capital sale to Greystar shows how quickly ownership can shift toward larger groups once the asset class proves scalable. Hines’s Valencia acquisition shows another route, where international firms use selected city entries to build exposure in growth markets without needing an immediate national rollout. The Spain co-living market is therefore becoming more competitive. However, the advantage still rests with firms that can secure assets early and align the housing product with local demand profiles.

Smaller and mid-sized operators still have room in the Spain co-living market because resident preferences differ sharply by city, price band, and unit format. That said, the strategic moves already seen in 2025 suggest that larger firms are setting a higher baseline for capital access, project scale, and cross-city rollout. Metrovacesa and Vita Group also formed a joint venture in Madrid in 2024, demonstrating that development partnerships remain a viable route into the category for firms seeking a project-based entry. This balance keeps the Spain co-living market open enough for specialist operators, while pointing to a more structured, institutionally backed competitive field by the end of the forecast period.

Spain Co-Living Industry Leaders

Habyt

Urban Campus

Node Living

The Flexy Living

Be Casa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Argis launched Flipco Retiro, its first flex living asset in central Madrid, following a USD 41.7 million investment. The project comprises 179 units, with three additional developments planned.

- March 2026: Patron Capital initiated a recapitalization process for its Vandor co-living platform, valued at USD 428 million, while planning further expansion across Spain's flexible living sector.

- March 2026: Greystar acquired a 1,600-bed purpose-built student accommodation portfolio in Salamanca and Valencia, doubling its operational student housing capacity in Spain.

Spain Co-Living Market Report Scope

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light: Master Lease / Lease Arbitrage |

| Asset-Light: Management Agreement |

| Asset-Heavy: Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium/Luxury |

| Students |

| Working Professionals |

| Madrid |

| Barcelona |

| Valencia |

| Rest of Spain |

| By Property Configuration | Studio / Entire Unit |

| Private Room | |

| Shared Room | |

| By Business Model | Asset-Light: Master Lease / Lease Arbitrage |

| Asset-Light: Management Agreement | |

| Asset-Heavy: Own-Develop-Operate | |

| By Price Band | Economy |

| Mid-Scale | |

| Premium/Luxury | |

| By End User | Students |

| Working Professionals | |

| By City | Madrid |

| Barcelona | |

| Valencia | |

| Rest of Spain |

Key Questions Answered in the Report

What is the current size of Spain's co-living demand?

The Spain co-living market was valued at USD 160.60 million in 2025 and is estimated at USD 180.05 million in 2026, with projected growth to USD 318.94 million by 2031.

How fast will co-living expand in Spain through 2031?

The market is forecast to grow at a 12.11% CAGR from 2026 to 2031, supported by housing shortage, mobile workers, and stronger investor participation.

Which property format leads to co-living in Spain?

Studio and entire-unit formats led with 52.3% share in 2025, while shared rooms are expected to grow fastest at a 12.78% CAGR through 2031.

Which business model is most important in Spain?

Asset-light master lease or lease arbitrage led with 45.1% share in 2025 and is also the fastest-growing model, with a 13.12% CAGR through 2031.

Who are the main resident groups using co-living in Spain?

Students were the largest end-user group with 47.5% share in 2025, while working professionals are expected to grow fastest at a 13.71% CAGR through 2031.

Which city offers the strongest growth opportunity in Spain?

Madrid remained the largest city with 53.2% share in 2025, but Valencia is forecast to expand fastest at a 13.66% CAGR through 2031, supported by growing institutional interest and a more accessible operating base.

Page last updated on: