Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

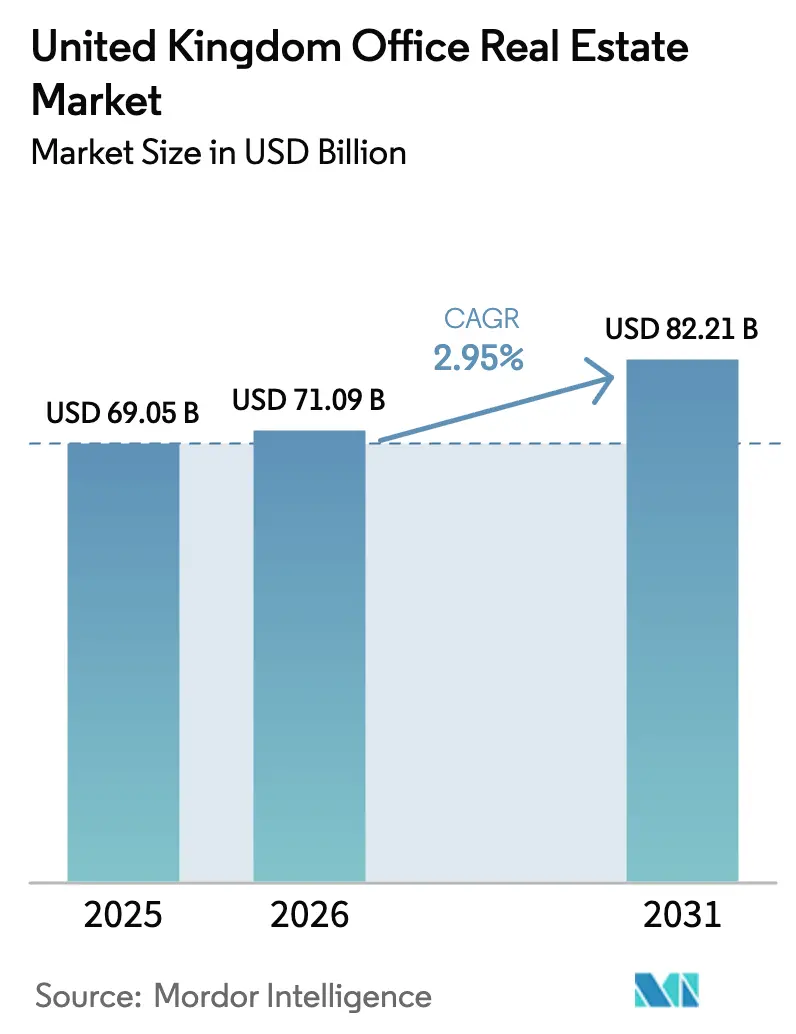

| Base Year Market Size (2025) | USD 69.05 Billion |

| Market Size (2026) | USD 71.09 Billion |

| Market Size (2031) | USD 82.21 Billion |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

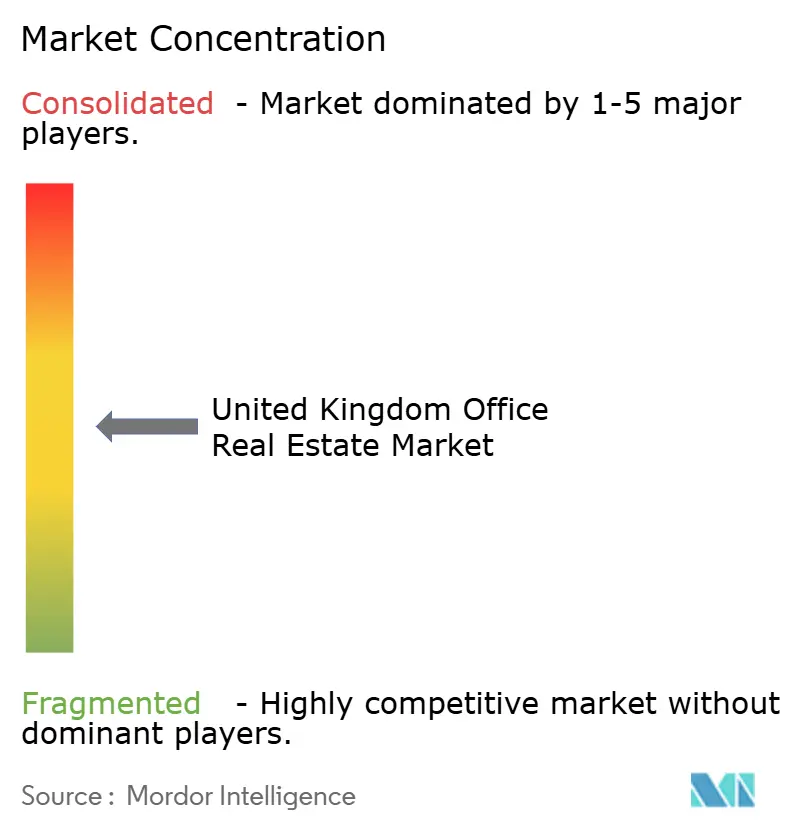

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Office Real Estate Market Analysis by Mordor Intelligence

United Kingdom Office Real Estate Market size in 2026 is estimated at USD 71.09 billion, growing from 2025 value of USD 69.05 billion with 2031 projections showing USD 82.21 billion, growing at 2.95% CAGR over 2026-2031. Growth is steady rather than rapid because hybrid work has settled into a long-term pattern and tenants now focus on energy-efficient, high-specification offices. Survey work by the Office for National Statistics showed that 28% of working adults used a hybrid schedule in autumn 2024, with adoption highest among over-30s, parents and professional staff[1]Tim Vizard, “Hybrid Working in Great Britain, Autumn 2024,” Office for National Statistics, ons.gov.uk. These figures highlight the sector’s ability to expand even as economic conditions and working practices evolve.

Key Report Takeaways

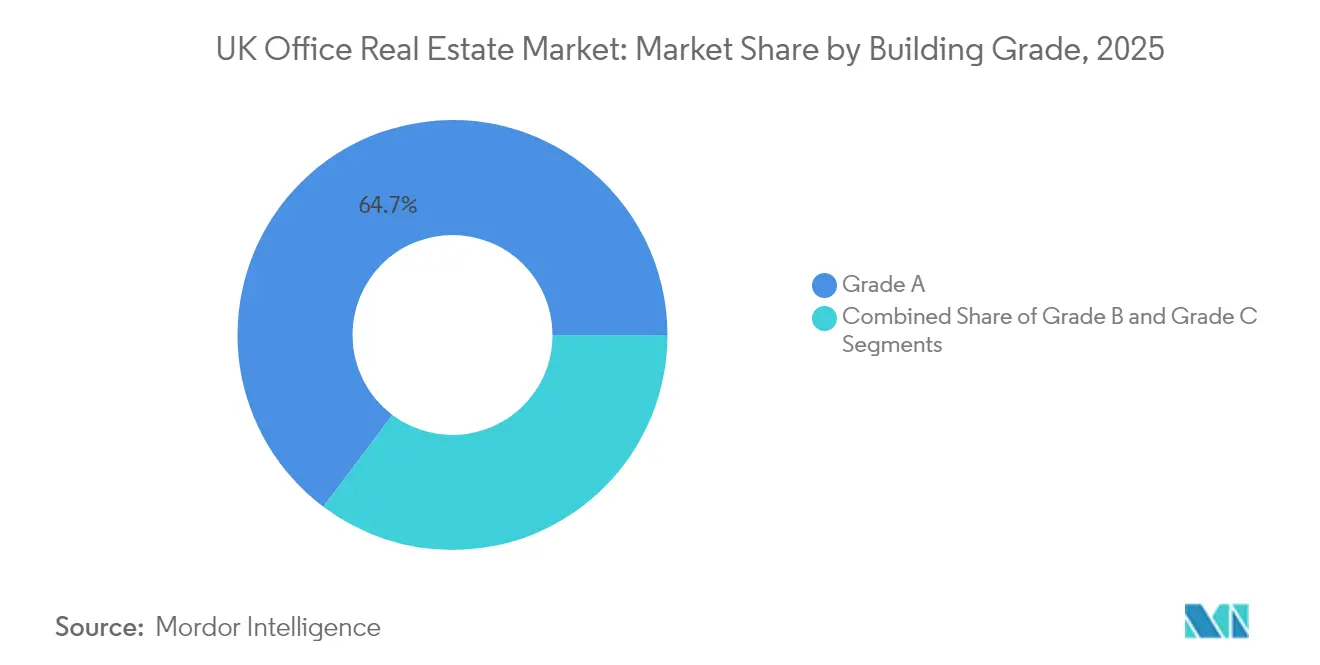

- By building grade, Grade A assets led with 64.74% of the UK office real estate market share in 2025, and this segment is forecast to post a 3.28% CAGR to 2031.

- By transaction type, rental deals accounted for 67.65% of the UK office real estate market in 2025, while sales transactions are projected to advance at a 3.45% CAGR through 2031.

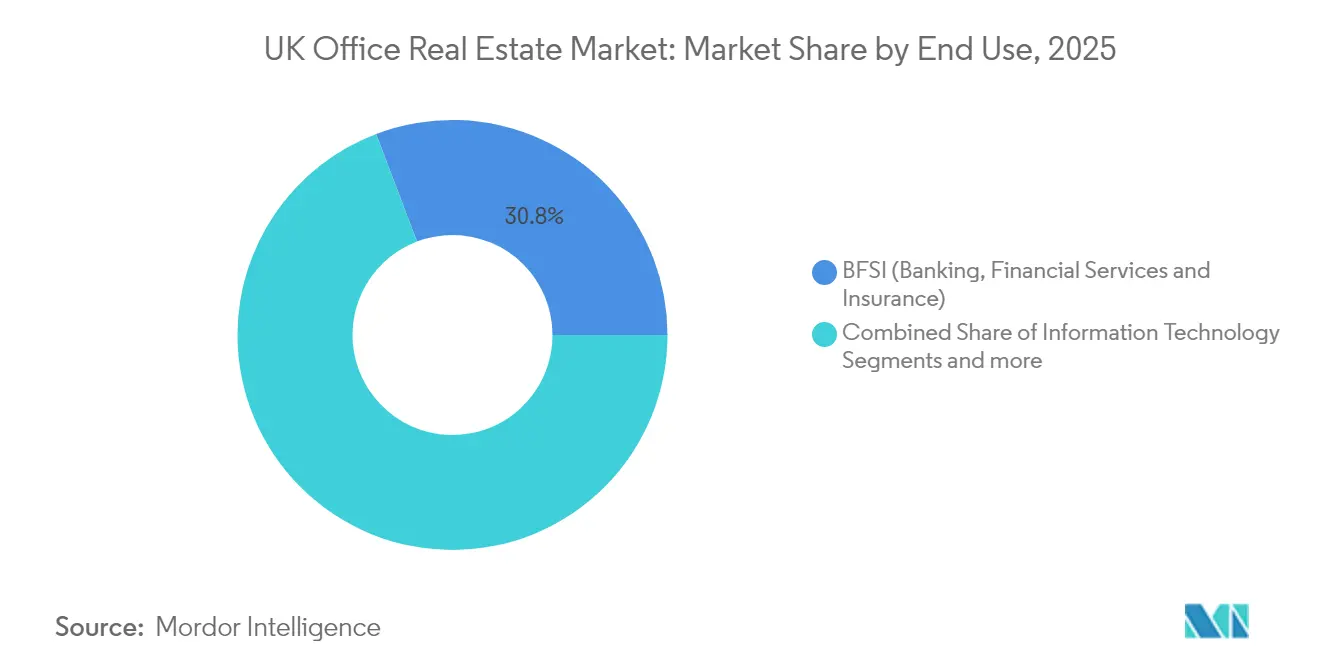

- By end use, the BFSI (Banking, Financial Services and Insurance) segment held 30.78% of the UK office real estate market in 2025; the Information Technology (IT & ITES) segment is expected to expand at a 3.83% CAGR to 2031.

- By country, England captured 80.92% of the UK office real estate market during 2025, whereas Scotland is forecast to grow the fastest at a 4.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewed demand for high-quality space | +0.8% | England, Scotland, Wales | Medium term (2-4 years) |

| Sustainability regulations lifting efficient stock | +0.6% | UK-wide | Long term (≥4 years) |

| Adaptive reuse adding supply | +0.4% | England, Scotland | Medium term (2-4 years) |

| Expansion of flexible workspace | +0.5% | England, Scotland, Wales | Short term (≤2 years) |

| Regional growth through government investment | +0.7% | Scotland, Wales, Northern Ireland | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Renewed Demand for High-Quality Office Space in a Hybrid Work Environment

Mandatory office days have prompted firms to pay for buildings that reward the commute. A peer-reviewed study in Nature found that hybrid arrangements cut employee turnover by one-third without hurting output, with the largest advantages for non-managers, women and staff facing long journeys. ONS data confirm the tilt toward knowledge industries, where 42% of information and communication employees and 42% of professional, scientific and technical workers now follow hybrid models. People with university degrees are 10 times more likely to work this way than those without qualifications, pushing firms to treat the office as a talent platform rather than a fixed cost. Buildings that offer strong digital infrastructure, wellness features and ESG credentials therefore command premium rents.

Sustainability Regulations Driving Demand for Energy-Efficient Buildings

Minimum Energy Efficiency Standards are splitting the market. In Q1 2025, 466,000 Energy Performance Certificates were filed in England and Wales and 84% of new properties scored an A or B rating, underscoring the pace of transition. Academic work shows that certified “green” offices lease faster and sell at higher prices than non-certified stock, with LEED buildings enjoying clear valuation gains. Research also links stronger sustainability disclosure with better operating income and higher enterprise value, encouraging owners to upgrade rather than accept “brown” discounts.

Adaptive Reuse of Commercial Spaces Supporting Office Supply Growth

Construction output in Q4 2024 rose only 0.5%, and maintenance work fell, leaving a gap that retrofit projects can fill. Academic work shows that adaptive reuse delivers lower embodied-carbon footprints than new builds while still meeting modern office needs. Government programmes such as the USD 512 million town-centre regeneration fund and USD 307.2 million housing package support these projects, while updated planning rules encourage brown-field conversion.

Expansion of Flexible Workspace Models in Emerging Markets

Hybrid work is no longer a metropolitan phenomenon. Investment-Zone funding worth USD 409.6 million for Welsh growth corridors is helping operators add capacity beyond London. Studies in organisational psychology highlight that hybrid schedules improve retention without hurting productivity, reinforcing occupier appetite for scalable solutions. Transport pledges of USD 19.97 billion are cutting journey times and letting corporations locate project teams in regional hubs [3]House of Commons Library, “Transport Connectivity Funding Commitments,” UK Parliament, hansard.parliament.uk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost pressures impacting development viability | −0.4% | England, Scotland, Wales | Short term (≤2 years) |

| Compliance challenges for aging stock | −0.3% | UK-wide | Medium term (2-4 years) |

| Weakened public-sector leasing | −0.2% | UK-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Pressures Impacting Development Viability

Inflation in labour and materials joins higher financing costs to push speculative development to a 13-year low, leaving only 1.5 million square feet under construction in regional cities. Developers now require larger pre-lets to de-risk projects, and prime regional yields have risen to 6.75%. Smaller sponsors without institutional backing are ceding ground, enabling well-capitalized firms to acquire stalled schemes at discounts. Until cost curves normalise, the imbalance favours existing landlords and constrains total output.

Compliance Challenges for Aging Office Stock

With 54% of regional buildings at risk of breaching 2028 MEES thresholds, landlords must choose between retrofitting at USD 144-343 per square foot or exiting the sector. RICS surveys reveal widespread repurposing, and lower-grade buildings in secondary locations face the starkest rent erosion. The UK office real estate market is therefore polarising, intensifying competition for compliant space and pressuring owners of obsolete assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Assets Command Market Leadership

Grade A offices held a commanding 64.74% of UK office real estate market share in 2025. Demand for these high-spec assets is projected to rise at a 3.28% CAGR through 2031 as firms embed hybrid work and ESG goals into portfolio strategy. Energy-certified buildings typically match or exceed conventional stock on net operating income and total return while trading at tighter cap rates. Government statistics show 84% of new English offices achieved an A or B energy rating in Q1 2025, confirming the rapid shift toward high-performance inventory.

Grade B space now faces material obsolescence risk: owners must fund mechanical upgrades or reposition assets entirely. Grade C buildings carry the heaviest burden; many require full retrofit or repurposing. A meta-review found that sustainability certifications deliver average sales premiums of 9.54% and rent premiums of 12.10%, with the office segment showing the greatest price sensitivity. As smart-building controls and wellness amenities move from novelty to baseline expectation, the gulf between premium and secondary stock will keep widening.

By Transaction Type: Rental Flexibility Dominates Market Activity

Rental transactions captured 67.65% of the UK office real estate market during 2025, underscoring tenant preference for agility amid macro uncertainty. Flexible office operators have democratized access to prime addresses through membership models, and management agreements now represent 41% of operator-landlord deals. Corporates favour short lease cycles, often three to five years, that align with evolution in headcount policies. This dynamic places pricing power in the hands of landlords with high-spec stock, who can demand premium rents without conceding long commitments.

Sales activity, while smaller, shows a projected 3.45% CAGR to 2031, outpacing rental gains, as interest-rate stability invites long-duration capital. Institutional investors deployed USD 800 million in Q1 2025, chasing yield gaps vs. continental Europe. Prime regional yields near 6.75% present compelling spreads over gilts, especially for buyers that can underwrite sustainability upgrades. Technologies such as digital twins are enhancing due diligence by enabling investors to quantify operational savings from planned retrofits, improving underwriting precision in the UK office real estate market.

By End Use: BFSI Leadership Challenged by Technology Growth

The BFSI (Banking, Financial Services and Insurance) cohort held 30.78% of 2025 demand, reflecting space-intensive trading floors and compliance functions that retain a strong in-office component. Large institutions such as Lloyds signed headline leases of 282,000 square feet, reinforcing the sector’s appetite for Grade A space. BFSI tenants typically favor landmark locations with robust transport links, ensuring continued core district relevance within the UK office real estate market.

Technology occupiers deliver the fastest trajectory at a 3.83% CAGR, fuelled by AI talent clustering and data-center adjacency needs. Leeds has emerged as a magnet, hosting more than 3,000 tech firms that leverage lower occupational costs relative to London Savills. Professional-services firms maintain steady requirements tied to advisory mandates triggered by regulatory change, while sectors such as life-sciences add episodic surges, particularly where lab-enabled office hybrids are feasible. This demand mosaic encourages landlords to design spaces with flexibility in mechanical systems, so single footprints can support multiple operational profiles over lease lifecycles.

Geography Analysis

England commanded 80.92% of 2025 activity, supported by London’s financial services cluster and headquarters density. The Bank of England cut its policy rate to 4.25% in May 2025, easing borrowing costs and supporting deal flow even as it watches inflation at 2.6%.Central and local agencies are spending USD 19.97 billion on city-region transport, a policy expected to unlock new office nodes and housing supply. Yet with construction output edging up only 0.5% in Q4 2024, vacancy rates in prime stock remain tight. Corporations are therefore adding regional back-office hubs that keep talent near London but lower total occupancy costs.

Scotland is the fastest-growing geography, set to expand at a 4.05% CAGR through 2031. Funding rounds include USD 25.6 million for Dundee Waterfront offices and refurbishments. Flexible-work uptake mirrors the broader UK pattern, and the country’s renewable-energy edge helps multinationals satisfy ESG mandates. Lower wages and rental bases relative to London further improve Scotland’s appeal for financial services and tech firms that need skilled labour.

Wales and Northern Ireland occupy smaller shares but benefit from USD 409.6 million Investment-Zone incentives and robust digital-connectivity upgrades. Hybrid policies allow firms to tap regional talent without daily London commutes, encouraging a multi-hub footprint that protects business continuity and cost efficiency.

Regulatory Landscape

The UK office real estate market operates under a tightening building-safety and energy-performance rulebook that is reshaping investment and leasing decisions. The Building Regulations etc. (Amendment) (England) Regulations 2026 (SI 2026/335) implement the Future Homes and Buildings Standards, with key provisions scheduled to come into force from 24 March 2027, supported by updated statutory guidance in Approved Document L (2026) on energy and greenhouse gas emissions.

Governance and lease structuring are also changing. In January 2026, the Building Safety Regulator began transitioning from the Health and Safety Executive to an arm's-length body under the Ministry of Housing, Communities and Local Government, increasing scrutiny around higher-risk buildings and compliance processes. Separately, the English Devolution and Community Empowerment Act 2026 received Royal Assent on 29 April 2026, and it includes a ban on upwards-only rent review clauses in new and renewal commercial leases in England and Wales, shifting focus toward documentation and negotiation for landlords and occupiers.

Value Chain Analysis

The UK office real estate value chain runs from land sourcing and planning through design, construction or retrofit, leasing, and long-term asset and property management. Planning and legal advisory (including lease structuring) interacts closely with development and refurbishment programs as landlords respond to energy-performance requirements, typically measured through EPCs and increasingly benchmarked against frameworks such as BREEAM, LEED, and NABERS UK. In this context, architects, engineers, and building-services contractors gain influence because MEP upgrades, building controls, and envelope improvements determine whether older stock can meet occupier ESG requirements and limit value erosion.

Downstream, brokers and property managers connect tenant demand for high-spec, energy-efficient workplaces with owner-led capital programs. Service-charge management has also become more prominent as occupiers factor energy pricing risk into affordability and site selection. Technology and fit-out supply networks matter as well, since premium Grade A positioning depends on digital connectivity, smart-building systems, and space-utilisation tools that support hybrid work patterns. Overall, the chain is shifting from a build-and-lease model toward an operate-and-improve model, with retrofit delivery, energy reporting, and performance verification forming core value drivers.

Competitive Landscape

The UK office real estate market displays moderate concentration, the five largest advisory and brokerage houses—CBRE, JLL, Savills, Knight Frank, and Cushman & Wakefield—together control a little over 60% of transaction and management mandates. They use scale to secure Grade A leasing instructions and capital-markets deals, but must now couple those strengths with ESG and workspace-strategy services to defend their share. Each has rolled out analytics suites that track utilisation, energy intensity, and wellness metrics in near-real time.

Investment in PropTech is the main strategic theme. The majors are partnering with or acquiring start-ups that supply smart-building operating systems, occupancy sensors, and carbon-footprint dashboards. These tools let the firms deliver outcome-based contracts rather than traditional fee-for-service work, and they help landlords safeguard income as MEES deadlines loom. At the same time, regional specialists use local market knowledge and slimmer fee structures to win mid-cap instructions that the global brands can overlook.

Capital markets activity is increasingly selective. Core plus and value-add buyers focus on assets that can achieve rapid EPC uplifts and meet corporate net-zero targets. Private-equity funds have started to assemble retrofit platforms aimed at re-rating Grade B stock, while sovereign wealth vehicles concentrate on fully let, best-in-class assets. This divergence in risk appetite, combined with tightening debt costs, keeps pricing discipline high and underpins the market’s moderate concentration profile.

United Kingdom Office Real Estate Industry Leaders

CBRE

Jones Lang LaSalle IP, Inc.

Savills

Knight Frank

Cushman & Wakefield

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-led upgrade cycles create room for retrofit-led repositioning, especially for secondary offices facing Minimum Energy Efficiency Standards and tenant ESG screens. In the current report context, 54% of regional buildings are flagged as at risk of breaching the 2028 MEES thresholds, giving owners and capital partners a defined pipeline for works such as MEP upgrades, facade improvements, and smart controls. Market tools (EPC, BREEAM/LEED, and NABERS UK) also help translate performance gains for occupiers and lenders.

Leasing opportunities concentrate where supply is constrained and demand is measurable for high-quality, well-located space. Cost pressures have pushed speculative development in regional cities to a 13-year low, with only 1.5 million square feet under construction, while London and major regional hubs continue to show flight-to-quality dynamics that reward Grade A assets. Capital allocation is also broadening beyond traditional institutions, with CBRE noting increased deployment into UK real estate by defined contribution and local government pension schemes, aligning more closely with strategies focused on income and asset-management improvements than capital growth alone.

Recent Industry Developments

- June 2026: CBRE - Monthly Index: capital values down 0.1%, rental values up 0.4%. The latest print points to marginal price stability alongside firming rents, which should support valuation work and lease planning for Grade A assets. Demand for well specified office stock in prime locations remains a key theme in the month’s data.

- June 2026: CBRE - Monthly Index: capital values down 0.1%, rental values up 0.4% for the month. The figures suggest resilient market momentum and provide inputs for asset management decisions by landlords and investors. In central markets, landlord confidence continues to rest on steady rent performance.

- May 2026: Savills - Central London active demand reach 15.9 million sq ft (end of May 2026). The level indicates sustained occupier appetite and supports the potential for higher leasing activity in core areas. This ties back to Savills’ view that prime market dynamics remain robust through mid 2026.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of office real estate activity across the United Kingdom, capturing the value tied to office space being leased or sold and how that value changes with demand, rents, yields, and occupier needs over time.

Scope exclusions: We exclude residential housing, retail, industrial and logistics assets, and non-office property types even when they are part of mixed-use developments.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI

- Business Consulting & Professional Services

- Other Services (Retail,Lifesciences, Energy, Legal)

- By Country

- England

- London

- Rest of England

- Scotland

- Wales

- Northern Ireland

- England

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a consistent picture of office stock, demand, and pricing signals that can be cross-checked across time. For this, we rely on public and official sources such as the UK Valuation Office Agency non-domestic rating and floorspace statistics, Office for National Statistics labor and workplace indicators (including hybrid working), HM Land Registry datasets where relevant for transaction evidence, and Bank of England series on interest rates and lending conditions that affect yields.

We also review non-paywalled publications from professional bodies and public-facing market monitors, such as RICS survey outputs, plus widely available market updates from major broker research teams and reputable press coverage of large disposals, leasing moves, and development timelines. For company-level grounding, we use annual reports, investor presentations, and filings of listed landlords and property operators to understand rent roll trends, occupancy, incentives, and capex related to upgrades. To fill gaps like deal context and ownership changes, a paid subscription database is used for company financials and news, and another paid dataset is used selectively for patent searches when building standards and retrofit themes need an extra evidence trail. The sources listed above are indicative and not exhaustive, and many other public documents were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to test what desk research cannot fully confirm, especially around leasing incentives, Grade A versus secondary demand splits, and how quickly older stock is being repositioned. We speak with a mix of landlords, asset managers, leasing advisors, and occupier-side specialists across the United Kingdom so assumptions on rents, vacancy direction, and transaction liquidity can be triangulated with the active pipeline and recent negotiations.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | |

| Mid tier: 50% | Functional/Unit leaders: 32% | |

| Smaller Players: 17% | Managers: 52% |

Market-Sizing & Forecasting

Sizing is built from a top-down reconstruction of the UK office value pool, where the starting point is the office stock and its value drivers, which are then adjusted for leasing and sales activity, yield movement, and regional liquidity. The totals are corroborated with selective bottom-up approximations, such as sampling achievable rent by grade and city, applying vacancy and incentive ranges, and then scaling using known floorspace and active stock signals to check that results stay realistic.

A few practical inputs carry most of the weight in the model, and they are refreshed and stress-tested during updates. These include prime and effective rents (net of incentives), vacancy and availability direction, office investment turnover and deal sizes, shifts in financing conditions that affect yields, and refurbishment or new-build delivery that changes Grade A supply. Where local data is thin, we handle gaps by using conservative ranges anchored to nearby comparable cities and then validating the implied outcomes with interview feedback.

For forecasting, we use scenario analysis supported by time series smoothing on the key drivers, because office demand and investment activity can change quickly when rates and occupier strategies shift. The base case is kept consistent with the most repeated expectations from market participants, and then alternative cases are used to test how far rents, vacancy, and yields could move without breaking real-world constraints.

Data Validation & Update Cycle

Validation is done in layers so unusual results are caught early, and then traced back to the driver that caused them. We compare outputs against independent signals such as reported investment volumes, published rental indices, vacancy movements, and rate changes, and then check whether the model implies sensible rent growth and yield paths for each year.

Before sign-off, a second analyst reviews the assumptions and recalculations, and any large variance triggers a re-check of the source series and follow-up questions with selected interviewees. Reports are refreshed annually, with interim updates when material events occur, such as major interest-rate shifts, policy changes affecting energy performance, or abrupt swings in transaction liquidity. Right before delivery, a final pass is performed so clients receive the latest updated view.

Mordor Intelligence's United Kingdom Office Real Estate Market Size Compared Against Other Published Estimates

Published market sizes for UK office real estate often differ because the underlying market value can be constructed in more than one reasonable way. Differences usually come from what is counted as office value, how lease versus sale activity is treated, and how fast assumptions are refreshed when yields, incentives, and vacancy are moving.

In practice, the biggest gap drivers are scope and conversion steps, such as including only investable institutional stock versus also counting smaller private buildings, mixing capital value with annual transaction flow, or applying rent growth without consistently netting out incentives. Another reason is currency timing and the base year used, since the UK market is often modeled in GBP first and then converted to USD, which can shift the reported figure even when the real estate activity is similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 69.05 B (2025) | |

| Global Consultancy A | USD 62.40 B (2025) | This estimate appears to stay closer to office investment turnover and a narrower investable stock set, which tends to undercount smaller regional assets and can lag when leasing fundamentals are stronger than deal flow. |

| Industry Association B | USD 75.80 B (2025) | This figure likely blends office capital value with broader commercial property components or applies stronger rent growth assumptions without consistently netting out incentives, which lifts implied values in prime-led markets. |

The spread in the table mainly reflects whether the number represents a value pool tied to office stock and pricing, or a more transaction-led view that moves with annual deal volumes. When incentives, grade mix, and yield changes are reconciled with office floorspace and leasing and sales checks, the result stays easier to reproduce year to year, which is how the model is kept current at Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the UK office real estate market?

The UK office real estate market is valued at USD 71.09 billion in 2026, reflecting steady recovery from pandemic disruptions.

How fast will the market grow over the next five years?

The market is forecast to expand at a 2.95% CAGR between 2026 and 2031, reaching USD 82.21 billion by the end of the period.

Which building grade holds the largest market share?

Grade A offices dominated with 64.74% of the UK office real estate market share in 2025 owing to corporate flight-to-quality preferences.

Which geographic area is expected to grow the fastest?

Scotland shows the quickest outlook with a projected 4.05% CAGR, supported by over USD 2.18 billion in infrastructure commitments.

Why are flexible workspace models important for landlords?

Flexible leases meet tenant demands for agility and, by attracting a wider occupier base, help landlords keep vacancy low even when corporate space strategies fluctuate.

What is the biggest compliance challenge facing owners?

Meeting Minimum Energy Efficiency Standards by 2028 poses cost-intensive retrofit requirements that can run up to USD 343 per square foot for non-compliant buildings.

Page last updated on: