Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

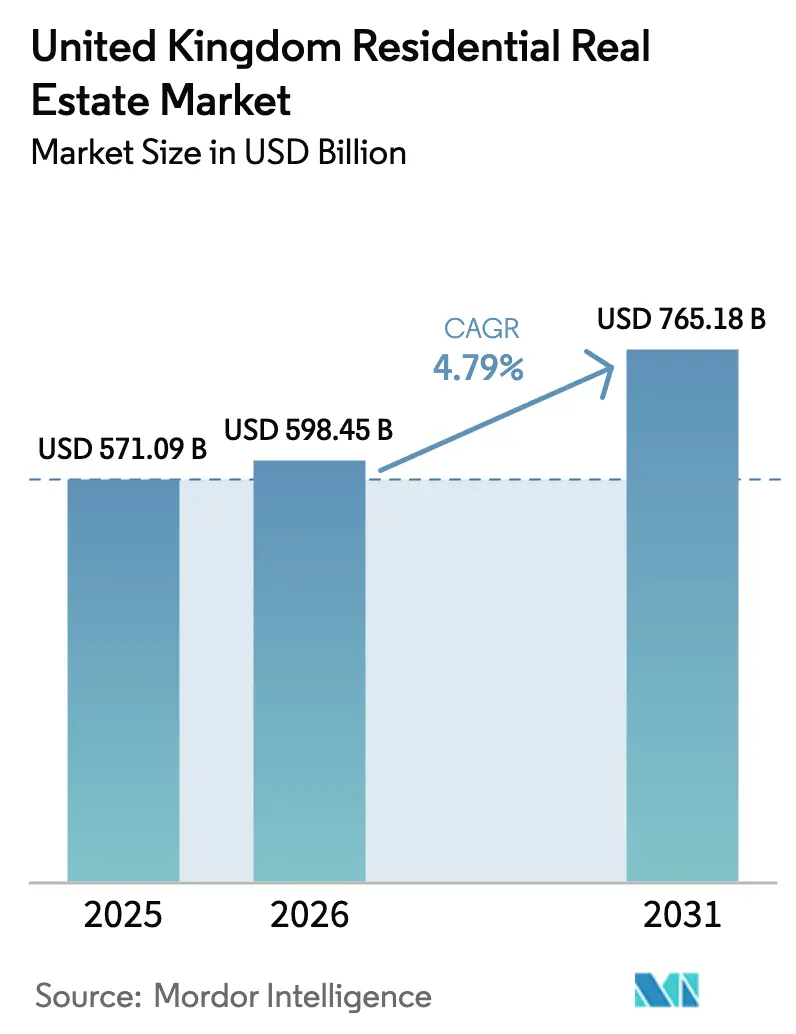

| Base Year Market Size (2025) | USD 571.09 Billion |

| Market Size (2026) | USD 598.45 Billion |

| Market Size (2031) | USD 765.18 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

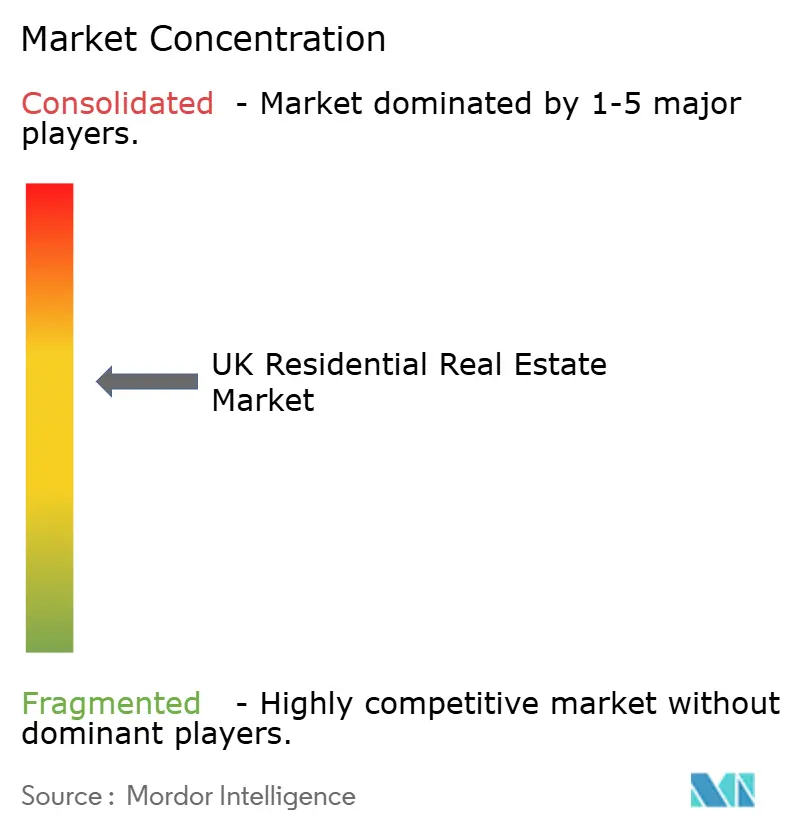

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Residential Real Estate Market Analysis by Mordor Intelligence

The United Kingdom residential real estate market size is USD 598.45 billion in 2026 and is projected to reach USD 765.18 billion by 2031 at a 4.79% CAGR. The United Kingdom residential real estate market continues to benefit from constrained inventory and institutional commitments to build-to-rent platforms, which support both pricing and absorption across core cities and regional growth hubs. Momentum stabilized after a 2019 to 2020 valuation dip and a cumulative 2020 to 2025 expansion as pent-up demand returned and new lending flexibility widened the pool of eligible borrowers. Transaction activity in 2025 surpassed the prior three-year average, while first-time buyers re-emerged as a visible force in completions, reflecting improved sentiment alongside affordability challenges in some southern markets. Regional divergence remains a defining feature, with Northern Ireland accelerating and several southern England submarkets seeing muted gains due to income-to-price misalignment.

Key Report Takeaways

- By business model, sales led with 79% of the United Kingdom residential real estate market share in 2025, while rentals are forecast to expand at a 5.46% CAGR through 2031.

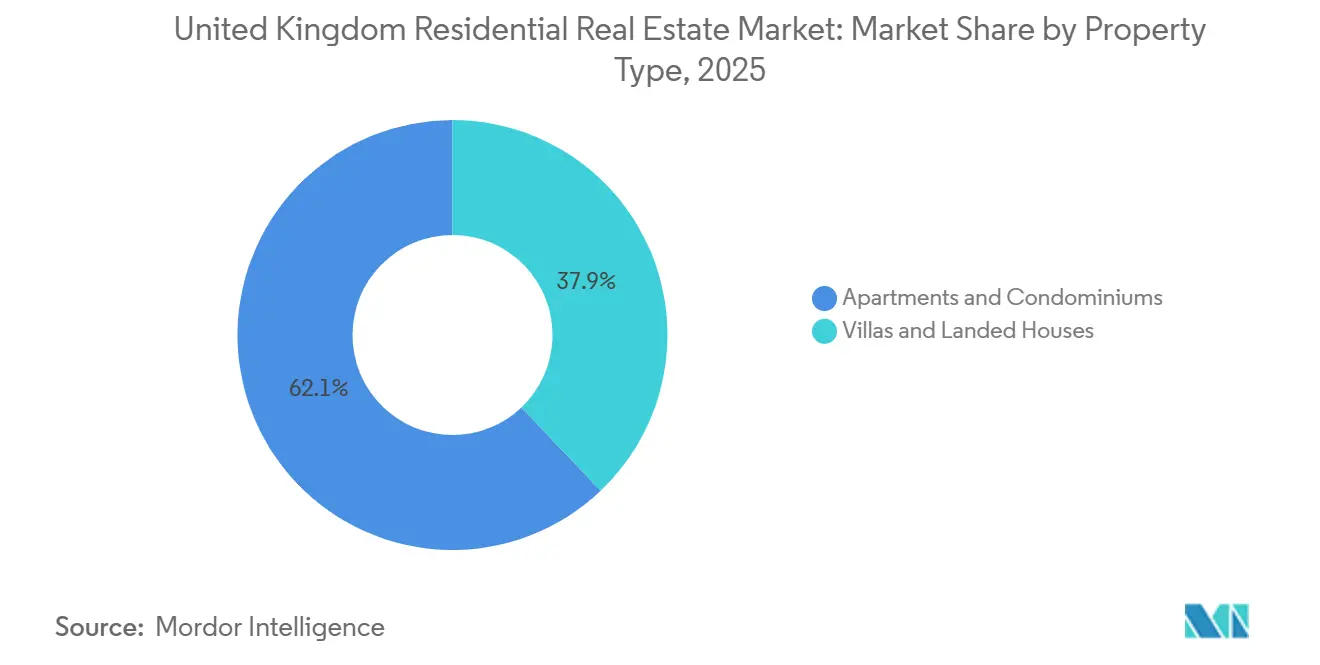

- By property type, apartments and condominiums held 62.11% of the United Kingdom residential real estate market share in 2025, while villas and landed houses are projected to grow at a 5.06% CAGR from 2026 to 2031.

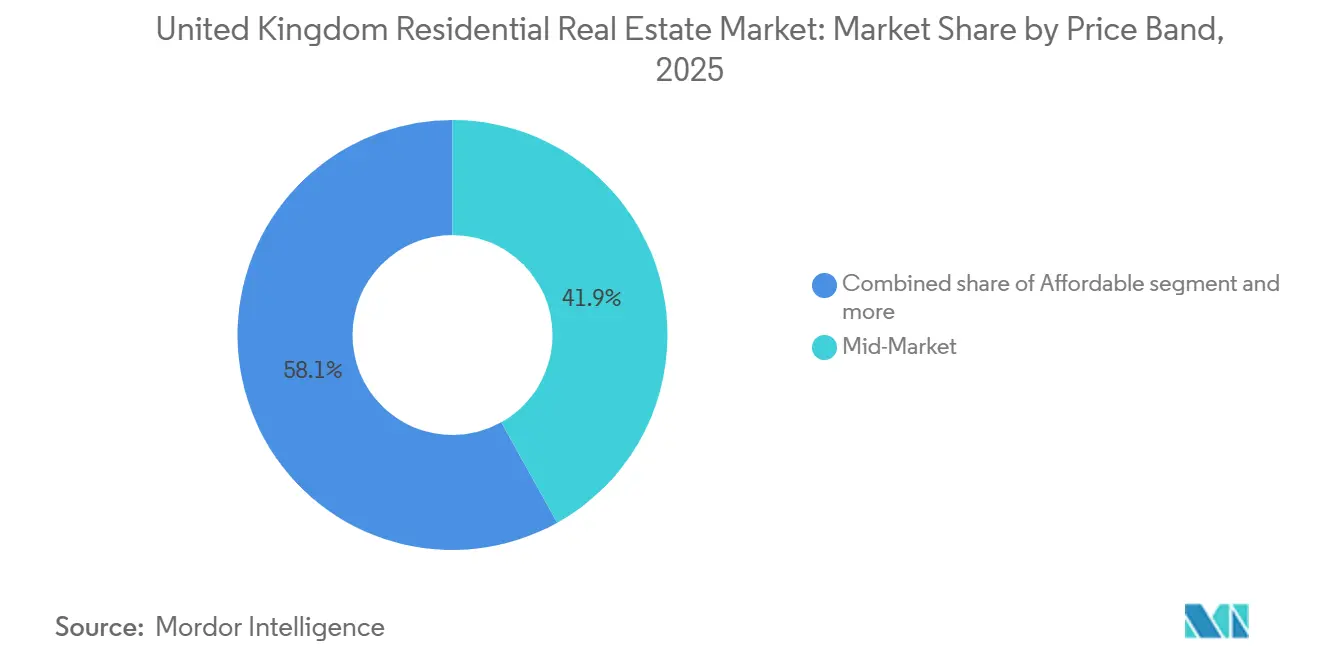

- By price band, mid-market properties captured 41.90% of the United Kingdom residential real estate market size in 2025, while luxury homes are forecast to advance at a 5.22% CAGR through 2031.

- By mode of sale, secondary resales accounted for 79.50% in 2025, while primary (new-builds) are projected to have a CAGR of 5.70% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Housing-Supply Gap vs. Household Formation | +1.4% | National, acute in London, Southeast | Long term (≥ 4 years) |

| Build-to-Rent Institutional Capital Inflows | +1.1% | Global, spill-over to Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Immigration-Led Population Growth in Core Cities | +1.0% | London, Greater Manchester, Edinburgh, Belfast | Medium term (2-4 years) |

| Remote-Work-Driven Sub-Urban and Rural Demand | +0.8% | England regional hinterlands, Scotland Borders, Wales commuter zones | Medium term (2-4 years) |

| 'Help to Buy' / 'First Homes' Scheme Extensions | +0.7% | England (outside London) | Short term (≤ 2 years) |

| Energy-Efficiency Retro-Fit and EPC-Band Pressure | +0.5% | Scotland, England | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Housing-Supply Gap vs. Household Formation

Net dwelling additions reached about 230,000 in the year to mid-2025 against a 300,000 target, and this gap sustains a structural floor under prices and rents in high-demand locations. Completions in the April to June 2025 quarter fell 19% year over year, including segments where development paused due to viability and planning frictions. Affordable housing starts in England totaled 45,418 in FY 2024 to 2025, which is among the weakest annual tallies in several years, setting up tighter availability later in the decade. Population growth from migration is concentrated in a handful of large cities and reinforces the pressure on existing stock as household formation outpaces new supply. In this setting, the UK residential real estate market sees persistent competition for listings in city neighborhoods and satellite towns that combine amenities with job access. Delivery risks in permitting and infrastructure readiness continue to influence where developers commit capital, which keeps supply uneven across regions.[1]https://www.propertymark.co.uk/

Build-to-Rent Institutional Capital Inflows

Institutional allocations to single-family and multifamily rental assets continued to expand in 2024, with commitments to UK single-family portfolios reaching GBP 2.5 billion (USD 3.15 billion) and outpacing 2023 as global capital rotates away from traditional offices. Portfolio activity included platform acquisitions and joint ventures led by established players, which added more than 5,000 homes to long-term rental pipelines and reinforced the view that purpose-built platforms can operate at scale. Even with this momentum, build-to-rent penetration remains near 2% of the UK rental stock, well below levels observed in mature North American and European markets, which signals headroom for multi-year placements. Policy clarity is shaping the operating backdrop, since the Renters’ Rights Act 2025 abolishes Section 21 from 1 May 2026, favoring owners with professional tenant management and compliance capabilities. As smaller buy-to-let landlords retrench, institutional platforms absorb demand and stabilize yields, which supports the UK residential real estate market across core cities and high-growth regional clusters. Forward funding and portfolio aggregation strategies also help de-risk developer pipelines and bring products to market in locations with tight rental supply.[2]https://www.savills.co.uk/

Immigration-Led Population Growth in Core Cities

Net migration added near 1% to the UK population in 2025, with a concentration of asylum hotel usage in London and several local authorities breaching per-capita thresholds that mark system strain. The cost of hotel accommodation averaged GBP 170 per person per day (USD 214) in FY 2024/25 compared with GBP 27 (USD 34) for dispersed provision, which diverted resources and reduced availability in lower-income areas. Policy now operates under a points-based system for skilled workers with narrower discretion and stricter family-reunion income requirements, including proof of adequate housing without public funds. University-linked housing demand remains strong near high-tariff institutions, which has kept pressure on rental availability in key academic cities. Even with tighter visa rules and reduced EU freedom of movement, demand in London, Manchester, Edinburgh, and Belfast continues to outpace rental stock. These factors lift occupancy and pricing power in the UK residential real estate market, particularly where multiple demand drivers converge in core urban centers.[3]https://migrationobservatory.ox.ac.uk/

Remote-Work-Driven Sub-Urban and Rural Demand

Work patterns that took hold during the pandemic have not fully reversed, and the preference for space is still evident in 2025 transaction and pricing data. Semi-detached and detached homes showed positive annual gains in 2025, while flats registered a modest decline, which underscores the shift to suburban and rural homes with outdoor areas and flexible interior layouts. Villas and landed houses are expected to grow at a 5.06% CAGR through 2031, which is above the UK residential real estate market average, as buyers prioritize home offices and wider living areas. Regional markets in the North and Midlands benefit from an affordability advantage and higher gross yields, which continue to draw both households and capital away from London’s core. Investor and developer responses include suburban single-family rental communities and energy-efficient new-builds that appeal to long-term residents seeking lower running costs. These preferences extend the commuter belt and reinforce demand in zones where journey times have become more acceptable due to changing workplace norms.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mortgage Rates and Affordability Stress | -1.3% | National, acute in London, Southeast, Southwest | Short term (≤ 2 years) |

| Planning-Permission Bottlenecks and Local-Plan Backlogs | -1.1% | England, concentrated in the Southeast | Medium term (2-4 years) |

| Skilled-Trades Labour Shortage | -0.9% | National, with acute gaps in Southeast, London, and Scotland | Long term (≥ 4 years) |

| Brexit-Induced Construction-Material Cost Inflation | -0.6% | National, import-reliant regions more exposed | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Mortgage Rates and Affordability Stress

Borrowing costs reset higher in 2025 even as the outlook for policy rates in 2026 turned more constructive, and this elevated the monthly servicing burden for existing and prospective borrowers. A large cohort of households will still refinance in 2026 and roll off pre-2021 deals, and affordability stress is highest where price-to-income ratios are stretched. Average affordability deteriorated to 8.6 years of disposable household income for the typical English home in 2025, which limited move-up activity and delayed purchases in the South. Even with easing inflation and a prospect of policy-rate reductions, lending spreads and market volatility can blunt the pass-through into fixed mortgage offers. Thinner affordability buffers make buyer incentives and pricing discipline more important for maintaining throughput in the UK residential real estate market. In parallel, renters face constrained options in tight markets, which can slow mobility from rental into ownership during 2026.

Planning-Permission Bottlenecks and Local-Plan Backlogs

Planning capacity constraints persisted in 2025, with a majority of local authorities reporting recruiting difficulties and skills gaps in core functions like viability assessment and ecology. A minority of departments felt prepared for National Planning Policy Framework changes, and process delays slowed application handling and decision timelines. The April to June 2025 quarter saw fewer applications received and fewer residential permissions granted, which amplified delivery delays. New legislation gives local authorities the ability to set fees to fund capacity, and the government committed resources to graduate and apprentice planners. However, funding uncertainty beyond the short term and limited training budgets constrain sustainable capability building for many teams. These constraints increase delivery risk for developers and stretch the timeline needed to bring sites to market in the UK residential real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Space Migration Favours Villas Despite Apartment Dominance

Apartments and condominiums led the property-type split with a 62.11% share in 2025, reflecting urban densification, the prevalence of multifamily build-to-rent platforms, and the economics of constrained city sites. City-center apartments remain the backbone for purpose-built student housing and multifamily rental portfolios, and stabilized operations in large schemes continue to attract institutional interest. Average apartment rents in inner London sat at the top of the national range in late 2025, which underscores the role of urban amenity density and transport nodes in pricing. The UK residential real estate market retains a deep pool of apartment inventory in metropolitan cores, even as buyer preferences shifted after the pandemic toward more space. As construction pipelines adjust to the Future Homes Standard, newer apartment stock with strong energy performance can command a quality premium that supports capital values and mortgageability.

Space-driven preferences are poised to lift villas and landed houses at a 5.06% CAGR from 2026 to 2031, supported by remote-work flexibility and family priorities like outdoor areas and school access. Pricing in 2025 reflected this preference change, as flats underperformed while houses posted gains in most regions, and affordability differentials drew buyers to the North and Midlands. Plans for suburban single-family rental communities and zero-bills homes that bundle solar, batteries, and heat pumps illustrate how product innovation aligns with household priorities. Regional housing markets with acceptable commute times and improving infrastructure retain a competitive edge as buyers evaluate trade-offs between space, cost, and access. As these patterns persist, the UK residential real estate market sustains high apartment density in urban cores while shifting incremental growth to family-oriented low-rise formats in regional commuter belts.

By Business Model: Rental Expands as Landlord Exits Sustain Institutional Inflows

Sales transactions accounted for 79.00% of revenue in 2025, supported by owner-occupier activity and a rebound in first-time buyers who reached 39% of completions after lenders loosened income multiple criteria. Completions rose to 1.2 million in 2025, marking a three-year high and a clear normalization in activity after 2024, with entry-level transactions lifting throughput across regional hubs. Higher loan-to-value availability improved access for new buyers, and that dynamic helped offset affordability challenges in southern markets where price-to-income ratios remained stretched. The UK residential real estate market benefited from improving buyer confidence, although regional performance varied with stronger momentum in the North and Midlands. Developers and agents oriented offers and outreach to first-time buyers and movers, which sustained absorption in a market defined by uneven affordability and localized demand surges.

The rental segment is forecast to grow at a 5.46% CAGR from 2026 to 2031, outpacing sales as private landlord exits compress stock and institutional platforms step in to scale portfolios. Regulatory reform in 2025 and 2026 codifies tenant protections and supports professionalized rental management, which tends to favor large platforms that can spread compliance costs and maintain service levels. Institutional investors have increased capital deployment into single-family and multifamily rental, which also provides forward funding that de-risks developer pipelines in locations with solid renter demand. Regional yield dispersion continues to drive capital northward, with yields above 6% in several northern markets compared with sub-3% in London, and this supports occupancy resilience through the cycle. Rental inflation eased in late 2025 from earlier peaks but remained elevated in many urban areas due to persistent stock shortfalls. As these trends play out, the UK residential real estate market adds professionally managed rental capacity while sales continue to anchor overall revenue.

By Price Band: Luxury Resilience Contrasts Mid-Market Volume Engine

Mid-market properties captured 41.90% of the UK residential real estate market size in 2025 and continue to drive volume as mortgage lending and developer product mix target this broad band. The UK average price in December 2025 was GBP 271,068 (USD 341,550), and the modest annual gain signaled stabilization after several years of volatility and shifting demand. Affordable housing delivery rose on completions in FY 2024 to 2025, yet starts fell, which indicates tighter availability ahead if pipeline replenishment does not accelerate. This mid-tier, therefore, anchors the UK residential real estate market, since it concentrates first-time buyers and upgraders and keeps the ecosystem of mortgage providers and volume housebuilders active. As policy funds flow into social and affordable tenures and developers place product into these channels, mid-market throughput should remain relatively steady in the near term.

Luxury homes priced above GBP 2 million (USD 2.52 million) are forecast to grow at a 5.22% CAGR through 2031, powered by wealth migration, tax timing, and selective international demand in prime zones. Prime Central London values saw the rate of decline moderate in late 2025, and this encouraged opportunistic buying from domestic and global capital targeting long-hold assets. Country homes regained interest among remote-work-enabled households, especially in commuter belts within manageable travel times to London and other employment hubs. As lending markets normalize and high-end buyers recalibrate currency and tax considerations, pricing at the top end should continue to find a base and gradually firm in core postcodes. These offsetting dynamics show why the UK residential real estate market can deliver both volume stability in the mid-tier and cyclical recovery in prime segments within the same cycle.

By Mode of Sale: New-Build Momentum Contrasts Resale Dominance

Secondary resales represented 79.50% of completions in 2025, reflecting the large legacy housing stock and buyer preferences for mature neighborhoods with established amenities. Listings rose to multi-year highs in 2025, and choice expanded in several regions, which helped temper national price growth and created a more balanced market. Average resale prices in November 2025 were GBP 270,300 (USD 340,580), up 1.1% year over year, with strong divergence between the best-performing and weakest regions. Transaction costs and mortgage affordability shaped decision-making, and many households chose to improve existing homes rather than move when mobility costs exceeded near-term benefits. The UK residential real estate market, therefore, maintained liquidity in the resale channel even as the forward view for new-build activity improved.

Primary new-build sales are projected to expand at a 5.70% CAGR from 2026 to 2031, supported by the mandate for 1.5 million net additions this Parliament and sizeable funding allocations through Homes England. New-builds in England commanded an average price of GBP 403,000 (USD 508,000) in August 2025, which reflected specification upgrades and energy-efficiency features valued by buyers and lenders. Policy reforms enacted in December 2025 aim to streamline approvals and accelerate starts, while forward sales and institutional funding provide certainty that allows builders to plan outlets. Large housebuilders target steady outlet expansions and have continued to seek planning approvals to position for improved market conditions. As these projects move from approval to construction, the UK residential real estate market adds modern, energy-efficient stock that can lower operating costs for households and attract long-term investors.

Geography Analysis

England accounted for 85.60% of activity in 2025, led by London, where average prices stood well above the national mean even as growth lagged due to affordability pressure. London’s annual price gain was below 1% in late 2025, and the capital’s affordability ratio rose to 8.6 years of disposable income, which weighed on move-up demand. Inner boroughs recorded small price contractions while suburban zones posted modest gains, and this bifurcation aligns with the pattern of families trading space for longer commutes. Several northern regions gained from affordability arbitrage, while regeneration and connectivity plans supported momentum in large metropolitan areas such as Greater Manchester and Leeds. The UK residential real estate market, therefore, showed a normalized but uneven pattern of growth across England in 2025.

Scotland posted about 1.9% annual growth in late 2025 and retained a material affordability advantage against England, which kept demand steady in regional cities and commuter towns. The Scottish Borders captured relocations from Edinburgh and cross-border moves linked to relative price and tax differentials, which underpinned additional buying interest. Regulatory milestones matter for supply and demand, since Scotland’s EPC rules will move markets toward better-performing stock and increase compliance costs for landlords from late 2026. Rental inflation moderated in late 2025 from earlier peaks, yet undersupply persisted as private landlords reassessed portfolios ahead of tighter standards. University-linked demand continued to anchor rental occupancy in Edinburgh and Glasgow, and this stabilized the UK residential real estate market across Scottish core cities.

Wales and Northern Ireland outperformed England’s headline growth rates, with Wales recording a 3.2% annual rise and Northern Ireland leading all territories at 9.7% in Q4 2025. Wales remained accessible for first-time buyers, and rental inflation stayed firm due to stock shortages and regulatory transitions that reshaped landlord incentives. Northern Ireland’s affordability remains favorable at about five years of disposable income, and Belfast’s economy and universities support both transaction and rental activity. Limited institutional build-to-rent presence in Northern Ireland and smaller-scale housebuilders create a market structure where local supply conditions heavily influence pricing. Given these dynamics, Northern Ireland is positioned to sustain faster growth into 2031, which reinforces regional balance within the UK residential real estate market.

Regulatory Landscape

The UK residential market operates under a more active policy agenda across planning, tenure reform, and private-rented-sector (PRS) conduct. The Planning and Infrastructure Act 2025 received Royal Assent on 18 December 2025, supporting the government’s housing delivery target of 1.5 million homes this Parliament through measures aimed at modernizing approvals and enabling local authorities to set certain planning fees to fund capacity. The Renters Rights Act 2025 commenced on 1 May 2026, abolishing Section 21 and expanding enforcement expectations, which tightens PRS requirements and increases compliance demands for landlords.

Building and tenure reforms also add compliance and product-design implications for developers and owners. The Building Regulations etc. (Amendment) (England) Regulations 2026 (SI 2026/335), published in March 2026, set the Future Homes and Buildings Standards pathway for new dwellings, including requirements linked to on-site renewable electricity for new homes and buildings containing dwellings. Separately, the Leasehold and Freehold Reform Act 2024, along with follow-on government roadmap activity in June 2026, and the draft Commonhold and Leasehold Reform Bill (published January 2026) indicate structural change in flat ownership and transaction processes, affecting how new-build apartments are packaged and sold and how long-term management obligations are structured.

Value Chain Analysis

The UK residential real estate value chain begins with land sourcing (strategic land, short-term land, and regeneration sites), moves through planning and enabling works, and relies on development delivery by large housebuilders plus a wider set of contractors and specialist trades. Output depends on mortgage availability and buyer qualification for sales, while rentals depend on institutional and private landlords, supported by letting agents and property managers for leasing, compliance, and resident services. Market consolidation and platform scaling are visible in the supply base, including the CMA clearance in October 2024 for Barratt Developments’ acquisition of Redrow plc, which strengthened a major national housebuilder platform and procurement footprint.

Upstream inputs and downstream operating requirements are increasingly shaped by standards, materials availability, and compliance regimes. Government publications point to a broad base of designated construction product standards (444 as of April 2025), while industry bodies such as the Construction Leadership Council have flagged materials constraints during 2024-2025 (including insulation and timber), reinforcing the need for forward purchasing, framework agreements, and tighter coordination with builders merchants and manufacturers. On the operating side, PRS regulatory tightening from May 2026 under the Renters Rights Act 2025 increases the value of professional property management and data-ready processes for portfolios, while tenure reform and home buying and selling reform initiatives shift workflows across conveyancing, valuation advisory, and brokerage as transaction processes and product structures evolve.

Competitive Landscape

The United Kingdom residential real estate development arena remains moderately concentrated. The UK residential real estate market features scale players among listed and privately owned housebuilders, institutional landlords expanding rental platforms, and national agent networks investing in product and technology. Large housebuilders maintained orderly pipelines and increased their planning submissions in late 2025, which prepared them for outlet growth as mortgage markets stabilized. Regulatory scrutiny remained a feature of the operating landscape, and builders adapted sales strategies and cost structures to manage demand variability across regions. Institutional rental platforms accelerated forward funding and platform consolidation to professionalize rental operations and absorb stock exiting from smaller landlords. Agent networks kept investing in AI-led consumer features and more efficient sales support tools, which help sustain engagement and throughput for sellers and landlords.

Strategic moves illustrate how leading participants are positioning for the next phase of growth. Barratt’s integration program in 2025 included 26 additional planning applications submitted with 13 approvals, a reinforced synergy target of GBP 100 million (USD 126 million), and steady outlet expansion through FY 2028. Homes England published an Investment Roadmap that outlined partnerships such as the MADE joint venture with Barratt and Lloyds and a GBP 50 million (USD 63 million) cornerstone equity commitment to a GBP 500 million (USD 630 million) impact fund, as well as a National Housing Bank concept with up to GBP 16 billion (USD 20.2 billion) capacity slated for 2026. Rightmove reaffirmed its growth ambition for 2030 and set out a 2026 investment plan that boosts AI-based consumer innovation, operations, and R&D while targeting high margins. These moves point to an ecosystem in which housebuilders secure planning and cost advantages, institutions scale stabilized rental assets, and portals enhance digital tools that knit together discovery and transaction. Together, these strategies underpin liquidity and operational resilience in the UK residential real estate market.

Capital markets activity and development transactions added to the backdrop in late 2025 and early 2026. Capital deployment targeted suburban and regional locations where rental yields are stronger, and affordability supports stable occupancy, and this included portfolio acquisitions and site aggregations coordinated by institutional managers. Select agents and managers reported platform investments and operational upgrades to improve resident experience and asset efficiency, which enhances net operating income profiles in stabilized assets. Developers advanced energy-efficient construction methods and specifications aligned with the Future Homes Standard to secure buyer and lender support ahead of December 2026. In parallel, local authorities and national agencies took steps to streamline planning and mobilize funding into social and affordable delivery, which improves forward visibility for high-volume suppliers. These activities support a more balanced risk-reward profile in the UK residential real estate market as it transitions into a multi-year delivery cycle.

United Kingdom Residential Real Estate Industry Leaders

Barratt Developments (Barratt Redrow plc)

Vistry Group

Persimmon

Taylor Wimpey

Bellway

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Affordable and social housing delivery is a clear whitespace channel where funding and policy translate into multi-year development pipelines. Homes Englands Social and Affordable Homes Programme 2026 to 2036 (at least GBP 27.3 billion) and the introduction of the Social Housing Bill into Parliament in May 2026 provide a framework for registered providers, local authorities, and delivery partners to expand supply, with implications for volume housebuilders and contracting partners that can deliver at scale. There is also project-level momentum for large residential phases in prime regeneration locations, including Sisk being appointed in June 2026 as main contractor for a GBP 280 million residential phase at Battersea Power Station (306 homes).

A second opportunity set centers on product redesign and retrofit services driven by energy-performance regulation and the household focus on operating costs. The March 2026 publication of SI 2026/335 establishing the Future Homes and Buildings Standards pathway, together with the industry shift toward very high-efficiency schemes such as Barratt Redrows Bollo Lane development in Ealing (construction started, targeting 900 homes with a Passivhaus program and 50% affordable housing), supports demand for suppliers and developers that can integrate low-carbon building specifications, on-site generation, and fabric-first approaches. In the private-rented sector, the May 2026 commencement of the Renters Rights Act 2025 increases compliance intensity and operational requirements, creating scope for institutional build-to-rent operators and professional managers to absorb demand where smaller landlords exit and where compliance-ready platforms can scale.

Recent Industry Developments

- July 2026: Vistry Group released a trading update and confirmed net debt of GBP 470 million at 30 June 2026, alongside a planned strategic review update scheduled for 24 September 2026. The disclosure underscored the sector's focus on balance sheet management while maintaining delivery capacity, shaping how large builders sequence land spend, partnerships, and output in a tighter affordability environment.

- December 2025: The Planning and Infrastructure Act 2025 received Royal Assent on 18 December 2025, introducing reforms intended to modernize planning approvals and support housing delivery, including enabling certain local fee-setting to bolster planning capacity. The change directly affects development lead times and the economics of bringing new supply to market, particularly in areas facing local-plan backlogs.

- November 2024: Homes England announced the Social and Affordable Homes Programme 2026 to 2036 with at least GBP 27.3 billion in funding, including GBP 1.2 billion of bridge funding from March 2025 and a 60% allocation requirement toward Social Rent tenures. The program strengthened the forward pipeline for affordable delivery partners and increased visibility for developers and contractors aligned with public and housing-association procurement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is sized as the annual value of completed residential property transactions in the United Kingdom, covering new-build and existing homes, and it also includes first-letting value for newly built rental stock.

Scope exclusions: We exclude purpose-built student housing, holiday-park chalets, timeshares, and overseas second-home purchases made by UK residents.

Segmentation Overview

- Sales

- Rental

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model to measurable housing activity and price signals, so the totals do not drift away from real transaction behavior. We used public sources such as national statistics on house prices and transactions, central bank rate series, land registry style price-paid datasets, and planning or housing supply dashboards published by official bodies.

To keep assumptions realistic, broader context was also pulled from sources such as government housing releases, trade and professional bodies covering valuation and housing, listed-company filings and investor presentations, and reputable financial press. Alongside these, we referenced paid subscriptions for company financials and intelligence, and for news and financials, mainly to speed up cross-checks on developer activity, funding conditions, and major deal announcements. The desk sources listed here are illustrative only, and many additional public materials were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what the numbers imply on the ground, especially around buyer demand, achievable prices, time-to-sell, and the share of activity that is new-build versus existing homes. We spoke with market participants such as developers, residential brokers and valuers, mortgage and lending-linked specialists, and rental market operators across the United Kingdom so gaps from desk research could be closed and assumptions could be tightened.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | |

| Mid tier: 48% | Functional/Unit leaders: 30% | |

| Smaller Players: 15% | Managers: 58% |

Market-Sizing & Forecasting

Sizing started with a top-down build where national housing transaction counts and new-build completions are reconstructed, and then translated into value using observed price levels and mix splits that came from public series and interview feedback. The totals were then corroborated using selective bottom-up approximations, such as sampling average selling prices by property type and region, and sense-checking against aggregated developer sales, brokerage throughput, and channel checks where reporting was available.

In practice, the model is most sensitive to a few fingerprints, which were tracked consistently across the study period: completed transaction volumes, house price indices and price-paid signals, mortgage rates and availability conditions, the new-build share versus existing home sales, and rental first-letting momentum for new stock. Where bottom-up inputs were missing or not comparable, gaps were handled through proxy ratios (for example, applying region-level mix based on observed listings and transaction splits), and then re-tested through primary calls.

For forecasting, we used scenario analysis built around interest-rate paths, affordability, and supply response, and then translated these into transaction and price trajectories before converting to market value. The final forecast was only signed off after the direction and magnitude were confirmed by multiple respondent groups, since short-term housing markets can move quickly when rates and confidence shift.

Data Validation & Update Cycle

Outputs were checked against independent signals, including transaction momentum, price movements, and whether the implied value per transaction stayed within realistic bounds. We also ran variance checks across regions and time so sudden jumps could be explained by rates, policy changes, or supply shifts, and then reviewed in a second analyst pass before sign-off.

The report is refreshed annually, and we trigger interim updates when material events occur, such as major rate changes, policy moves that affect housing demand, or visible breaks in transaction activity. Before delivery, a final review pass is done to ensure the latest public releases and key interview feedback have been reflected in the model assumptions.

Mordor Intelligence's United Kingdom Residential Real Estate Market Size Versus Other Published Estimates

Published market values for UK residential real estate can look far apart because the underlying definition is not always the same, and the time anchor can shift between stock value and annual transaction value. Differences also come from whether models use observed transaction and pricing evidence, or lean more heavily on broad macro indicators without checking what they imply for completed deals.

Transaction-count trends, price-paid movements, and rate-driven affordability checks are the evidence points that keep Mordor Intelligence aligned to the annual value of completed home sales plus first-letting of newly built rental stock, instead of mixing in the much larger total value of the housing stock.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 571.09 B (2025) | |

| Industry Publisher A | USD 389.82 B (2024) | Uses an earlier base year and a different forecast window, and its scope framing appears to center on selected residential types and regional breakdowns, which can understate value if first-letting of new rental stock and full transaction coverage are not explicitly counted. |

| Industry Association B | USD 10500.00 B (2023) | Represents total residential property stock value at a point in time (end-2023) rather than the annual flow of completed transactions, so it is structurally larger even if market activity is flat. |

Seen together, the spread is mainly explained by flow versus stock measurement, base-year timing, and whether rental first-letting for new stock is treated as part of the residential value pool. By keeping the scope tied to completed transactions and then checking that against observable price and volume signals, the estimate stays traceable to inputs that can be rechecked each year.

Key Questions Answered in the Report

What is the size and growth outlook for the UK residential real estate market in 2026 and 2031?

The UK residential real estate market size is USD 598.45 billion in 2026 and is projected to reach USD 765.18 billion by 2031 at a 4.79% CAGR.

Which segment leads by business model and which grows fastest through 2031?

Sales led with 79.5% of 2025 revenue, while rentals are projected to grow at a 5.46% CAGR from 2026 to 2031, driven by private landlord stock exits and institutional platform expansion.

What property type accounts for the largest share in 2025?

Apartments and condominiums held 62.11% of the 2025 volume, although villas and landed houses are forecast to grow faster at a 5.06% CAGR as remote-work preferences favor more space.

Which UK region showed the strongest recent price momentum?

Northern Ireland recorded 9.7% annual house-price growth in Q4 2025, the strongest across UK territories during that period.

What are the most important policy developments for housing delivery in 2026?

The Planning and Infrastructure Act 2025 modernizes approvals, Homes England’s SAHP allocates at least GBP 27.3 billion (USD 34.4 billion) through 2036, and the Future Homes Standard takes effect for new starts from December 2027.

How do affordability and mortgage conditions affect demand in 2026?

Affordability stood at 8.6 years of disposable income for the average English home in 2025, and while rate cuts are anticipated, lending spreads may limit pass-through, keeping conditions tight in high-cost regions.

Page last updated on: