UK Residential Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 119.69 Billion |

| Market Size (2026) | USD 123.43 Billion |

| Market Size (2031) | USD 143.86 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Residential Construction Market Analysis by Mordor Intelligence

The United Kingdom Residential Construction Market size is expected to grow from USD 119.69 billion in 2025 to USD 123.43 billion in 2026 and is forecast to reach USD 143.86 billion by 2031 at 3.12% CAGR over 2026-2031. This steady expansion reflects public-sector intervention designed to close the national housing deficit, the revival of Help-to-Buy–type initiatives, and the growing institutional appetite for build-to-rent schemes. Developer strategies now revolve around securing grid capacity, balancing material cost inflation, and accelerating modern methods of construction, while regional opportunities remain shaped by the government’s levelling-up program. Tight labor availability, evolving building-safety rules, and the 2050 net-zero mandate continue to influence planning decisions and capital deployment across the United Kingdom residential construction market.

Key Report Takeaways

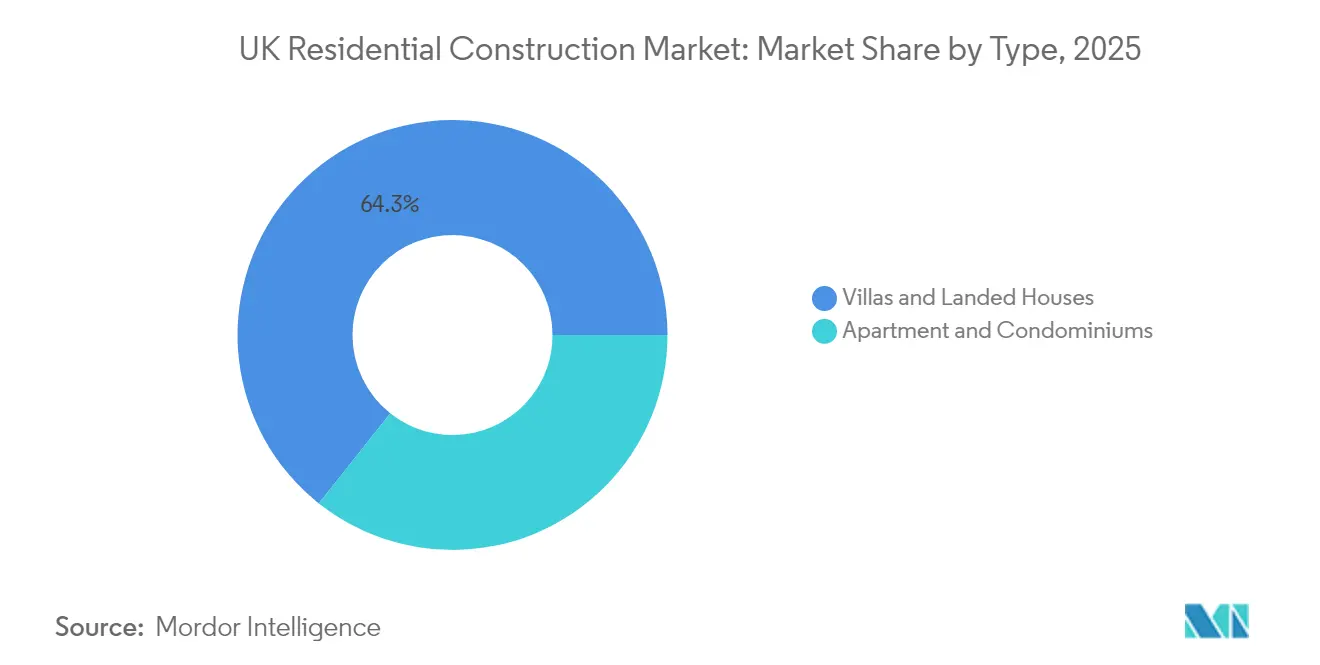

- By type, villas and landed houses led with 64.32% of the United Kingdom residential construction market share in 2025, while apartments and condominiums are projected to advance at a 5.12% CAGR through 2031.

- By construction type, new construction accounted for 76.55% of the United Kingdom residential construction market size in 2025; the renovation segment is expected to expand at a 3.92% CAGR between 2026-2031.

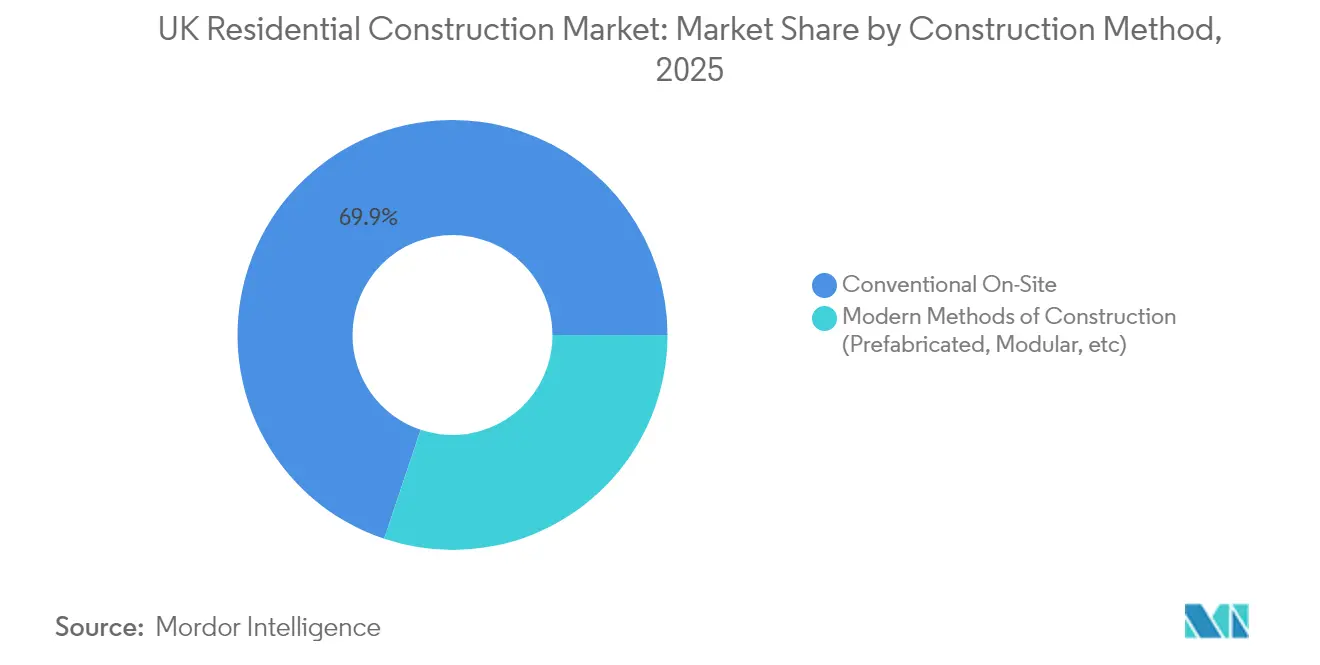

- By construction method, modern methods of construction captured a 30.15% share of the United Kingdom residential construction market size in 2025 and are forecast to post a 5.79% CAGR to 2031.

- By investment source, private capital retained a 60.45% share of the United Kingdom residential construction market size in 2025, whereas public investment shows the fastest growth at a 5.35% CAGR for 2026-2031.

- By geography, London held 29.10% of the United Kingdom residential construction market share in 2025; Manchester is set to record the highest city-level CAGR at 4.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government housing-delivery targets & Help-to-Buy revival | +0.8% | National, with concentrated effects in London, Birmingham, Manchester | Medium term (2-4 years) |

| Institutional build-to-rent investment wave | +0.6% | Urban centers, particularly London and Manchester | Long term (≥ 4 years) |

| Adoption of modern methods of construction (MMC) & modular | +0.5% | National, with early adoption in high-demand regions | Long term (≥ 4 years) |

| Net-zero-2050 mandate spurring low-carbon housing solutions | +0.4% | National, with regulatory compliance focus | Long term (≥ 4 years) |

| Brownfield-site regeneration via Levelling-Up funding | +0.3% | Northern England, Midlands, selected urban areas | Medium term (2-4 years) |

| Fintech-enabled fractional home-ownership demand | +0.2% | London, Manchester, high-value urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Housing-Delivery Targets & Help-to-Buy Revival

Parliament has imposed mandatory annual planning targets of 371,000 homes, a 22% uplift over the prior guideline, forcing local authorities to align zoning decisions with national affordability metrics. A USD 3.75 billion support package announced in November 2024 doubles the ENABLE Build guarantee pool to USD 2.5 billion, specifically unlocking credit for small and medium-sized builders and specialist rental developers. Early assessments suggest the measures could catalyze more than 20,000 additional starts by 2027, though progress hinges on capacity within planning departments and the speed of digital permit processing. The revival of Help-to-Buy-style shared-equity instruments is also amplifying first-time buyer demand in regional cities, underpinning transaction pipelines for private developers. Collectively, these interventions underpin the forward book for the United Kingdom residential construction market[1]Department for Levelling Up, Housing & Communities, “Housebuilding Support Package 2024,” GOV.UK, gov.uk.

Institutional Build-to-Rent Investment Wave

Completed build-to-rent stock now exceeds 100,000 units, representing roughly 2% of the private rental pool and attracting long-duration capital from pension funds seeking inflation-linked returns. Forward-funding deals are concentrating in London and Manchester corridors, where population density supports professional property management economics. Planned Renters’ Rights legislation that raises minimum quality standards is expected to drive further consolidation toward institutional landlords able to absorb compliance costs. The strategic pivot from buy-to-let to purpose-built rental is broadening revenue resilience for contractors focused on multi-family delivery, thereby reinforcing multi-year volume commitments within the United Kingdom residential construction market.

Adoption of Modern Methods of Construction & Modular

MMC penetration climbed to 16% of national starts in 2024, up from 9% seven years earlier, responding to skilled-trade shortages and higher carbon-reduction expectations. Factory-precision modules can reduce build time by 50% and cut operational energy use by more than half compared with masonry builds, a compelling value proposition as wage inflation elevates on-site labor budgets. Government procurement policies now reserve segments of the Affordable Homes Program for volumetric projects, accelerating order pipelines for modular manufacturers. Challenges remain around upfront capital and the 60-year design life that lenders perceive as shorter than traditional structures, yet process innovation and public-sector underwriting continue to support the segment’s advance across the United Kingdom residential construction market[2]Make UK, “Modular Housing: State of the Sector 2025,” MAKE UK, makeuk.org.

Net-Zero-2050 Mandate Spurring Low-Carbon Housing Solutions

Thirty-five large homebuilders have signed the Future Homes Hub transition charter, establishing metric-based pathways to compress embodied and operational carbon across project portfolios. Requirements for lifecycle assessments and heat-pump-ready specifications are already influencing supplier negotiations, pushing steel fabrication, window glazing, and insulation trades toward verified low-emission footprints. Market participants anticipate a steady migration away from natural-gas heating, with zero-carbon regulations for new dwellings scheduled to tighten again in 2028. These obligations stimulate innovation in digital energy modeling and off-site component manufacturing, reshaping cost structures throughout the United Kingdom residential construction market[3]Future Homes Hub, “Net Zero Transition Plan for Homebuilders 2025,” FUTURE HOMES HUB, futurehomeshub.org.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating construction-material inflation | -0.7% | National, with acute effects in high-volume regions | Short term (≤ 2 years) |

| Skilled-trade shortage & ageing workforce | -0.5% | National, particularly affecting complex projects | Medium term (2-4 years) |

| Grid-connection backlogs for all-electric schemes | -0.4% | High-growth areas, new development zones | Long term (≥ 4 years) |

| Post-Brexit divergence of building-product standards | -0.3% | National, with supply chain disruptions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Construction-Material Inflation

Timber, steel, and aggregates experienced cumulative price jumps above 70% between 2021-2023, widening tender spreads and prompting a wave of contractor insolvencies. Although headline indices moderated in early 2025, forward contracts still price in a 17% rise through 2028, compressing developer margins for marginal projects. Smaller builders, often operating on thin working-capital cushions, remain most exposed, leading to selective land-bank releases and deferment of optional schemes. This cost volatility undermines near-term volume targets for the United Kingdom residential construction market and incentivizes rapid adoption of price-stable modular components.

Grid-Connection Backlogs for All-Electric Schemes

Connection queues of up to four years are delaying thousands of planned homes, with National Grid admitting a mismatch between booked capacity and actual energy demand. Planning consultant analyses indicate existing infrastructure could service 2.5 times more dwellings if reservation rules were modernized. The bottleneck forces developers to redesign mechanical systems toward transitional hybrid heating solutions, increasing capital expenditure and threatening net-zero alignment. Unless capacity-release reforms accelerate, these delays will moderate delivery trajectories in the United Kingdom residential construction market, particularly for high-density sites dependent on electric heat networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Urban Densification Drives Apartment Growth

The apartment and condominium segment is forecast to post a 5.12% CAGR, outpacing villas and landed houses, even though detached formats held 64.32% of the United Kingdom residential construction market share in 2025. Institutional build-to-rent capital, regulatory incentives for higher-density zoning, and lifestyle shifts among younger cohorts all propel multi-family uptake in core employment nodes. Higher-rise products also align with municipal sustainability agendas as denser footprints lower per-capita emissions and infrastructure costs. Conversely, suburban villas preserve dominance in out-of-city sub-markets, leveraging remote work patterns and preferences for private outdoor space. Planning reforms that reduce parking minima and favor brownfield conversion continue to tilt incremental supply toward apartments, ensuring a structural rebalancing within the United Kingdom residential construction market.

Complying with post-Grenfell safety standards has raised per-square-foot costs, but developers increasingly mitigate expense through pre-manufactured facade panels and digital quality-control protocols. The segment benefits from transparent rental yield benchmarks, encouraging pension-fund entry and lifting forward-purchase pipelines to record levels. Villas remain the choice for high-net-worth buyers and for locations where land supply outweighs density imperatives, yet even these projects adopt semi-off-site components to control cost. Hybrid construction styles, therefore, sustain both volume segments, reinforcing diversified revenue streams across the United Kingdom residential construction market.

By Construction Type: Renovation Gains Momentum

New-build activity retained 76.55% of the United Kingdom residential construction market size in 2025, yet renovations are set to deliver a 3.92% CAGR as fiscal and sustainability policies reward adaptive reuse. The USD 112.5 million Blackpool regeneration and the USD 25 million Selby Centre retrofit underscore public-funding leverage in transforming vacant commercial assets into mixed-income housing. Renovation projects enjoy expedited approvals and usually sidestep the biodiversity-net-gain metrics required for greenfield schemes, enabling faster realization of capital commitments. Furthermore, embodied-carbon considerations reveal up to 75% savings versus demolition plus rebuild, offering compliance advantages ahead of the 2028 carbon-budget tightening.

Nonetheless, structural unpredictability in historic assets can inflate contingency budgets, and the Future Homes Standard will oblige deep energy upgrades from 2025 onward. To offset risk, developers deploy ground-penetrating lidar surveys and digital twins that model load-path upgrades before procurement. Financial institutions now price renovation loan covenants on verified carbon metrics, tilting the cost of capital toward retrofit outcomes. This ecosystem shift should gradually raise renovation's contribution to volume, but will not dislodge new construction as the anchor of the United Kingdom residential construction market.

By Construction Method: MMC Overcomes Cost Barriers

Modern methods of construction captured a 30.15% share of the United Kingdom residential construction market size in 2025 and are projected to grow at a 5.79% CAGR, reflecting escalating wage pressures and enhanced regulatory confidence in factory precision. Public purchasers are mandating MMC quotas, and leading housebuilders are vertically integrating module plants to secure supply. Capital intensity remains a hurdle; many start-ups collapsed under working-capital requirements before achieving scale. However, improved pipeline visibility following government guarantees is now lowering perceived risk and broadening lender acceptance.

Conventional on-site methods, still owning 69.85% market share, rely on established subcontract networks and flexible sequencing, attributes valued in low-rise or irregular infill plots. Yet chronic craft-skill shortages are eroding their cost edge, with journeyman bricklayer wages rising above USD 37 per hour in London. Over the forecast horizon, hybrid delivery models, such as panelized walls installed on traditional slab-and-frame structures, are expected to dominate, blending efficiency with design flexibility. This evolution aids overall capacity expansion within the United Kingdom residential construction market.

By Investment Source: Public Sector Accelerates

Private capital held 60.45% of the market share in 2025 as volume housebuilders utilized revolving credit to rotate land banks. Nevertheless, public investment is growing at a 5.35% CAGR after the USD 3.75 billion support package widened credit guarantees for SME builders. Direct government funding now addresses brownfield remediation, infrastructure shortfalls, and off-balance-sheet leasing for affordable housing providers. Public-private partnership structures increasingly share risk on large urban extensions, channeling municipal landholdings into mixed-tenure communities that meet net-zero specifications.

Institutional allocations from insurance firms continue to dominate private inflows, favoring stabilized rental and senior-living formats with predictable cash yields. However, taxation uncertainty and interest-rate volatility have tempered speculative land acquisition, pushing developers to tie land options to zoning milestones. The convergence of these trends diversifies financing channels and underpins delivery continuity across the United Kingdom residential construction market.

Geography Analysis

London commands 29.10% of the United Kingdom's residential construction market share, owing to deep pools of international capital and consistent in-migration among high-value industries. Annual planning guidance has been capped at 80,000 units to reflect infrastructure constraints, yet projects such as the USD 37.5 million Riverside Sunderland proof-of-concept underline how public grants can unlock stalled brownfield in outer boroughs. Build-to-rent, co-living, and premium micro-units represent the fastest-growing sub-formats as price-to-income ratios restrict outright ownership, tightening demand for professionally managed rentals.

Manchester exemplifies levelling-up success, with 4.55% CAGR underpinned by transport upgrades, media-tech job creation, and a municipal planning system attuned to high-density infill. Large institutional mandates are underwriting entire city-center blocks, compressing delivery risk and elevating construction volume certainty. In Birmingham, Commonwealth Games legacy projects and metro extensions reinforce brownfield housing appeal, though labor scarcity occasionally elongates program schedules. These two metropolitan cores collectively expand the addressable pool for the United Kingdom residential construction market, absorbing a rising share of public grant allocations.

The remainder of the United Kingdom encompasses diverse conditions. Northern regeneration corridors leverage USD 85 million in brownfield grants to repurpose disused industrial plots, while coastal regions pursue lifestyle-led schemes catering to remote workers. Rural authorities face demographic pressure but attract premium single-lot developments where planning hurdles are lower. Infrastructure gaps, aging housing stock, and small-site heterogeneity require tailored solutions, yet government co-funding and modular pilot schemes are incrementally activating latent land supply. Together, these dynamics broaden geographic dispersion and de-risk excess reliance on any single city within the United Kingdom residential construction market.

Competitive Landscape

Market concentration is intensifying as scale advantages in procurement, land assembly, and regulatory compliance grow more decisive. Barratt Developments’ USD 3.125 billion acquisition of Redrow creates a company capable of delivering more than 22,000 units annually and generating USD 9.4 billion in revenue, raising competitive pressure on mid-tier players. Bellway’s decision to abandon its USD 900 million pursuit of Crest Nicholson demonstrates heightened selectivity, with acquirers favoring balance-sheet strength and geographic complementarity over pure volume gains.

Technology adoption differentiates top-tier builders. Investments in BIM, site robotics, and AI-driven procurement analytics compress build times and enhance cost predictability. Versarien’s prototype 3D-printed village in Accrington, budgeted at USD 7.5 million for 46 homes, signals how additive manufacturing could disrupt traditional brick-and-block paradigms if scalability hurdles are resolved. Supply-chain resilience strategies, including vertical integration of timber frame plants and joint ventures with electrical grid providers, protect margins against material inflation and infrastructure delays.

Regulation also shapes rivalry. Stricter building-safety certification elevates fixed overhead, favoring companies with robust compliance functions. Meanwhile, heightened ESG disclosure requirements encourage early movers to pilot low-carbon concrete and recycled steel, capturing green-finance premiums. As a result, the United Kingdom residential construction market is evolving from volume-centric competition toward capability-centric competition, with mid-decile players seeking mergers or specialized niches to remain viable.

UK Residential Construction Industry Leaders

Barratt Developments plc

Persimmon plc

Taylor Wimpey plc

Bellway plc

Redrow plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Government introduced a USD 3.75 billion housebuilding support package, doubling ENABLE Build guarantees to USD 2.5 billion and targeting over 20,000 new homes nationwide.

- October 2024: Barratt Developments completed its USD 3.125 billion acquisition of Redrow, creating the United Kingdom’s largest homebuilder by revenue.

- October 2024: VINCI Construction agreed to acquire FM Conway, a public-realm maintenance specialist with USD 725 million turnover, subject to regulatory approval.

- October 2024: USD 85 million Brownfield Land Release Fund awarded to 54 councils to prepare sites for 5,200 dwellings, including projects in Manchester and Eastbourne.

UK Residential Construction Market Report Scope

Residential construction includes construction on single-family or two-family dwellings that are occupied or used or are intended to be occupied or used, primarily for residential purposes.

A complete background analysis of theUK Residential Construction Industry Segmentation, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The UK Residential Construction Industry Segmentation is segmented by type (villas and landed houses and condominiums, and apartments). The report offers market size and forecasts for all the above segments in value (USD).

| Apartment & Condominiums |

| Villas and Landed Houses |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

| Public |

| Private |

| London |

| Birmingham |

| Manchester |

| Rest of UK |

| By Type | Apartment & Condominiums |

| Villas and Landed Houses | |

| By Construction Type | New Construction |

| Renovation | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) | |

| By Investment Source | Public |

| Private | |

| By Geography | London |

| Birmingham | |

| Manchester | |

| Rest of UK |

Key Questions Answered in the Report

How large is the United Kingdom residential construction market in 2026?

The market is valued at USD 123.43 billion in 2026, with a forecast to reach USD 143.86 billion by 2031.

Which dwelling type is expanding fastest?

Apartments and condominiums are projected to grow at a 5.12% CAGR through 2031, reflecting urban densification and institutional rental demand.

What role will modern methods of construction play?

MMC already represents nearly one-third of output and is expected to grow at a 5.79% CAGR, driven by labor shortages and sustainability requirements.

How are government policies influencing investment?

A USD 3.75 billion support package, brownfield grants, and mandatory housing targets are accelerating public-sector funding and de-risking private pipelines.

Which region offers the quickest growth?

Manchester leads city-level expansion with a 4.55% CAGR thanks to infrastructure upgrades, job creation, and supportive planning frameworks.

Page last updated on: