Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

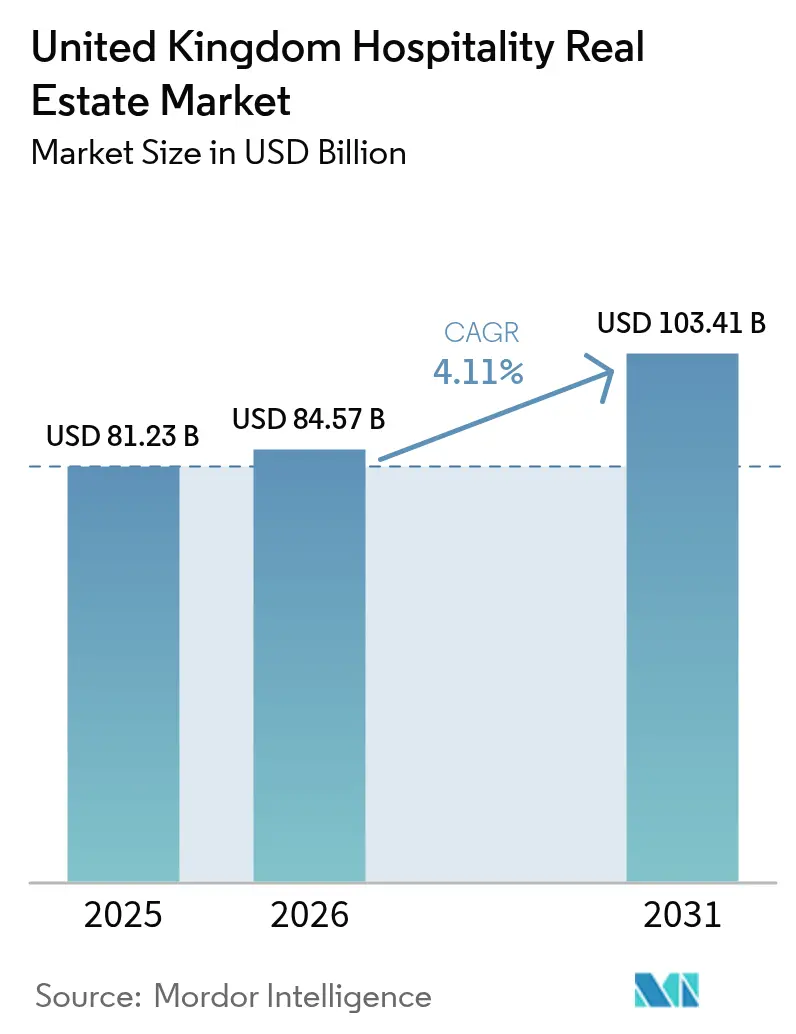

| Base Year Market Size (2025) | USD 81.23 Billion |

| Market Size (2026) | USD 84.57 Billion |

| Market Size (2031) | USD 103.41 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

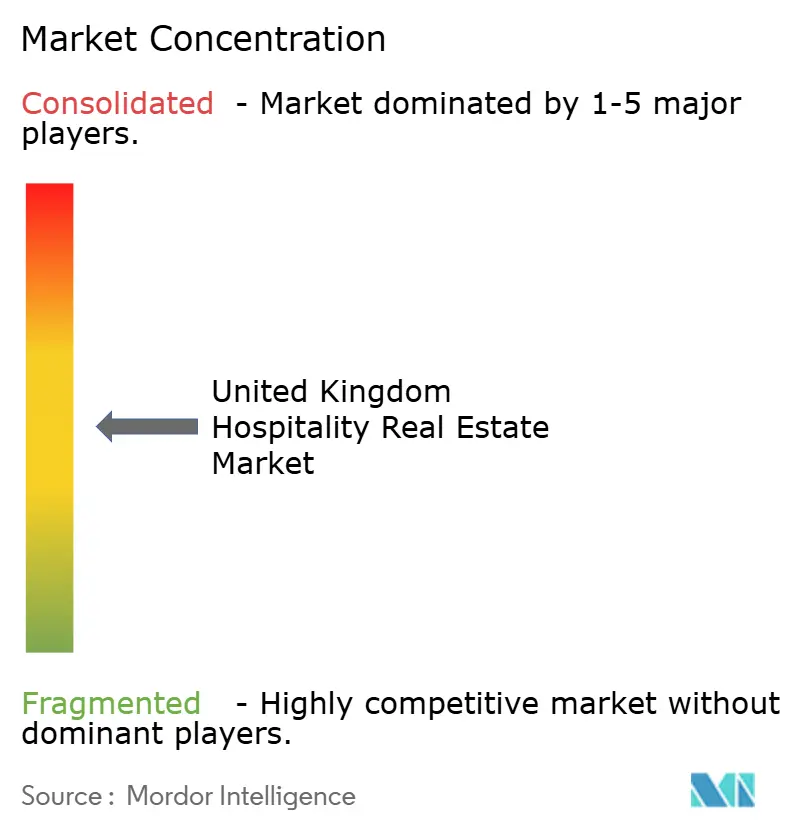

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Hospitality Real Estate Market Analysis by Mordor Intelligence

The United Kingdom Hospitality Real Estate Market size was valued at USD 81.23 billion in 2025 and estimated to grow from USD 84.57 billion in 2026 to reach USD 103.41 billion by 2031, at a CAGR of 4.11% during the forecast period (2026-2031). International arrivals are forecast to reach 43.4 million in 2025, translating into visitor spending of roughly USD 41.8 billion, which is channeled mainly toward upscale and luxury lodging. Institutional capital has rotated from office and retail toward hospitality assets because steady RevPAR growth offsets higher financing costs. Long-haul flight searches climbed 20% year on year in September 2025, sustaining demand for airport-adjacent hotels despite softer domestic volumes. Conversions of under-utilized offices, retail units, and light-industrial sites into hotels are accelerating as developers pursue lower capex and faster delivery than ground-up builds. Operators are simultaneously embracing electrification, on-site solar, and air-source heat pumps to unlock green lending lines and future-proof net operating income.

Key Report Takeaways

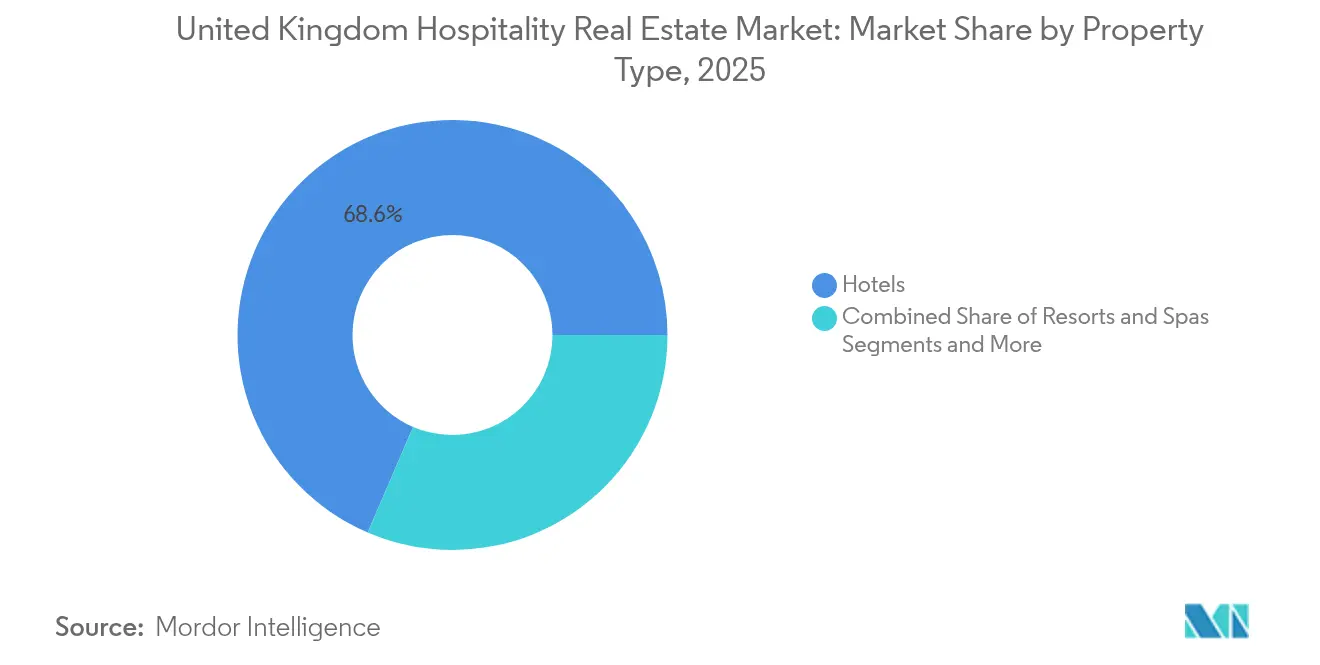

- By property type, hotels controlled 68.55% of the United Kingdom hospitality real estate market share in 2025; serviced apartments are forecast to expand at a 4.53% CAGR to 2031.

- By type, chain hotels held 64.70% of the United Kingdom hospitality real estate market share in 2025, while independent properties are projected to grow at 4.78% CAGR through 2031.

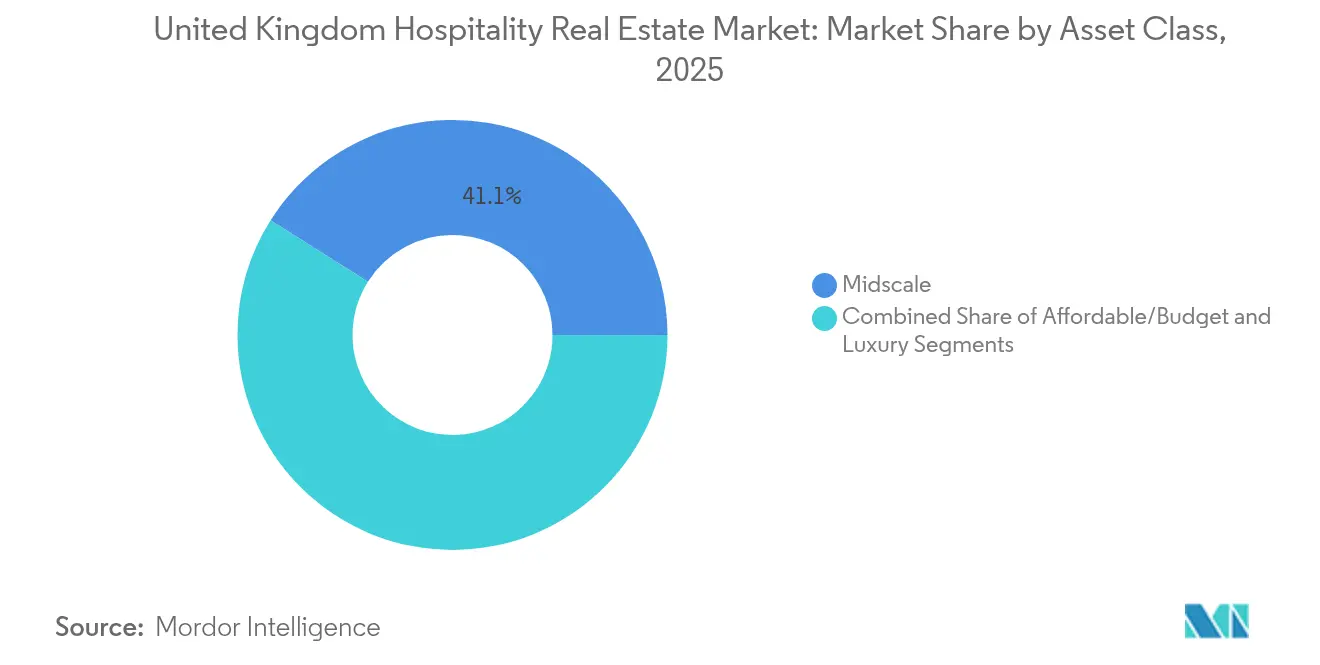

- By asset class, midscale assets captured 41.05% of the United Kingdom hospitality real estate market size in 2025, and luxury properties are advancing at a 4.87% CAGR to 2031.

- By geography, London commanded a 39.65% share of the United Kingdom hospitality real estate market size in 2025; Scotland is expected to post the fastest 5.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Hospitality Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| International tourism rebound elevating occupancy and RevPAR | +1.2% | London, Edinburgh, Manchester | Medium term (2-4 years) |

| Flight capacity rebuild and visa easing boosting long-haul demand | +0.8% | Heathrow, Gatwick, Scotland | Short term (≤ 2 years) |

| Experiential, lifestyle, and extended-stay formats attracting institutional capital | +0.9% | Key urban and leisure hubs | Medium term (2-4 years) |

| Asset conversions of retail and offices to lodging uses | +0.7% | Central London, Birmingham, Edinburgh | Long term (≥ 4 years) |

| Sustainability retrofits unlocking green financing | +0.6% | Major urban clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

International Tourism Rebound Elevating Occupancy and RevPAR

International visits are recovering toward pre-pandemic peaks, with 43.4 million arrivals projected for 2025, a level that channels higher-value travelers into luxury and upscale hotels. Quarter-on-quarter volatility persists, yet spend per guest keeps rising, enhancing RevPAR resilience[1]Office for National Statistics, “Construction and Materials Price Indices,” ons.gov.uk. Airport-gateway markets benefit most from the lift in inbound demand, especially around major sporting and cultural events that spike short-stay bookings. Operators are refining price-optimization algorithms to capture this uplift without eroding brand loyalty. Sustained high-spend international demand has become the cornerstone of revenue strategy, cushioning domestic softness.

Flight Capacity Rebuild and Visa Easing Boosting Long-Haul Demand

Seat capacity on long-haul routes returned faster than intra-European services, funneling travelers through Heathrow, Gatwick, and Edinburgh. Eased visa processing for tourism and seasonal work further supports booking lead-times. Hotel brands have rushed to open or flag conversions near transport hubs, as illustrated by Hilton’s 157-room Heathrow property. Budget-friendly select-service formats positioned near rail and air nodes now capture price-sensitive travelers seeking convenience. Sustained capacity growth combined with favorable exchange rates should prolong this demand tailwind over the next two years.

Experiential, Lifestyle, and Extended-Stay Formats Attracting Institutional Capital

Independent lifestyle hotels are projected to grow at a brisk 4.95% annually, outpacing chain inventory as design-led concepts command a rate premium. Ennismore’s USD 3 billion fundraising plan underscores investor conviction that experiential hospitality can scale while preserving authenticity. Serviced apartments, running at a 4.69% CAGR, draw corporate relocations and long-stay guests seeking kitchen facilities and flexible contracts. Dalata’s 834-room UK rollout exhibits the scalability of such hybrid models. Capital flows are thus channeling into assets that blend community spaces, co-working, and curated F&B, reinforcing this growth vector.

Asset Conversions of Retail and Offices to Lodging Uses

Whitbread’s USD 70.1 million purchase of New London House for hotel conversion exemplifies the economics of adaptive reuse. With office and retail vacancies persisting, local councils increasingly rubber-stamp hotel-led redevelopment to revive high-street vitality. Marriott intends to complete nearly 100 European conversions by 2026, many in the United Kingdom. Conversions lower embodied-carbon versus new builds, supporting ESG targets and shortening time to revenue. As financing stays costly, adaptive reuse remains an attractive route to scale.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High financing costs and stricter underwriting | −0.9% | Nationwide | Short term (≤ 2 years) |

| Construction inflation and supply-chain delays | −0.6% | Principal urban markets | Medium term (2-4 years) |

| Labor shortages and rising wages | −0.7% | London, South East, Scotland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Financing Costs and Stricter Underwriting

Commercial real estate lending shrank 9.8% as lenders raised coverage ratios and cut leverage, inflating equity requirements for new deals[2]Bayes Business School, “Commercial Real Estate Research,” bayes.city.ac.uk. Debt funds fill the gap yet price 200–250 bps over bank margins. Prolonged diligence elongates closing timelines, discouraging speculative projects. Only scale portfolios like KKR-Baupost’s 6,500-key Marriott acquisition can secure favorable structures. Smaller sponsors thus shelve pipelines until rates ease, muting near-term transaction volume.

Construction Inflation and Supply-Chain Delays

Material costs rose 2.6% year on year, while specialized HVAC equipment faces 12-week lead-times, swelling refurbishment budgets. All-electric prototypes such as Premier Inn Swindon prove feasible but require high upfront outlays[3]Whitbread PLC, “Corporate Announcements and Sustainability Reports,” whitbread.co.uk. PPHE’s Westminster Bridge Road project factored contingencies for premium fit-outs to achieve BREEAM Excellent. Developers now phase upgrades, prioritizing guest-facing tech before heavy MEP work, which delays full-property repositioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Hotels Dominate but Serviced Apartments Accelerate

Hotels accounted for 68.55% of the United Kingdom hospitality real estate market share in 2025, maintaining primacy because chains deliver distribution scale and loyalty capture. Serviced apartments, however, are forecast to post a 4.53% CAGR, the fastest within the category, as remote work and corporate relocations lengthen average stay. Dalata’s 834-room UK expansion illustrates how operators layer apartment-style rooms onto select-service footprints for flexibility. Conversions of vacant offices in London and Edinburgh into aparthotels shorten development cycles and lower embodied-carbon, making the model attractive to institutional owners seeking stable yields.

Resorts and spas remain a niche concentrated in rural Wales and coastal England, where performance correlates with leisure demand swings. Yet, upscale countryside spas benefit from wellness tourism that supports higher average daily rates. Hotels confront margin pressure from labor and energy costs, prompting adoption of energy-management tech and partial service concepts. Serviced apartments mitigate that risk by operating with lower staffing ratios and capturing ancillary revenue from co-working leases, positioning the sub-segment for sustained outperformance.

By Type: Chains Hold Scale; Independents Capture Lifestyle Premium

Chain hotels held 64.70% of United Kingdom hospitality real estate market share in 2025, underpinned by Premier Inn’s and Travelodge’s widespread network. Independent assets are expected to grow at a 4.78% CAGR through 2031, buoyed by traveler appetite for localized design and food-forward concepts. Ennismore’s pursuit of outside capital to scale multiple lifestyle brands confirms investor belief in non-standardized experiences. Chains answer through soft brands and acquisitions such as Hilton’s USD 210 million Graduate Hotels purchase, melding global systems with boutique flair.

Despite chain dominance, independents leverage faster refurbishment timelines and curated programming to lift average daily rate. Financing barriers for stand-alone operators are easing as debt funds value differentiated cash flows. Chains, conversely, exploit loyalty ecosystems and centralized procurement to blunt cost inflation, keeping occupancy high in midscale and budget tiers. The resulting spectrum ranges from asset-light franchise contracts to fully owned design-driven properties, with capital flowing to whichever model maximizes risk-adjusted return.

By Asset Class: Midscale Leads Volume; Luxury Drives Growth

Midscale properties captured 41.05% of the United Kingdom hospitality real estate market size in 2025, anchored by the extensive Premier Inn and Travelodge estates. Luxury inventory, though smaller, is projected to expand at a 4.87% CAGR, the highest among classes, because affluent tourists accept rate hikes that offset wage and energy inflation. Knight Frank data reveal double-digit payroll cost growth hitting midscale margins hardest, while luxury hotels pass increases through to guests via premium packages and experiential add-ons.

Budget assets focus on occupancy volume but face rising refurbishment costs to meet sustainability standards. Midscale chains deploy modular construction in conversions to contain expenses. Luxury investors prioritize heritage assets and prime London addresses, betting on limited supply and strong capital-value appreciation. The widening performance gap pushes institutional money toward the upper tier, while scale players fine-tune midscale operating models to preserve profitability.

Geography Analysis

London retained a 39.65% share of the United Kingdom hospitality real estate market size in 2025, yet its forecast growth trails Scotland’s 5.03% CAGR as investors hunt yield beyond the capital. London payroll costs climbed 6.6% year on year, compressing margins and prompting operators to trial automation. Airport-adjacent openings such as Hampton by Hilton Heathrow exploit recovering long-haul capacity and sustained transfer passenger flow.

Scotland’s pipeline benefits from city-center conversions in Edinburgh and Glasgow, supported by government tourism grants and iconic event calendars. Self-catering occupancy dipped slightly in late 2024, yet urban hotels posted a robust rebound, illustrating the region’s ability to absorb new supply. Developers target brownfield sites, with local councils expediting approvals to invigorate post-industrial districts.

Rest of England, led by Manchester, Birmingham, and Leeds, rides corporate relocation and domestic conference traffic. Dalata’s Brighton, Liverpool, and Manchester openings validate regional demand for select-service and extended-stay formats where land is cheaper and planning faster than in London. Wales and Northern Ireland show mixed signals: premium rural resorts thrive on wellness tourism, while mid-tier coastal hotels battle discretionary-spend weakness. Portfolio investors, therefore, balance London’s stability with Scotland and regional England’s superior growth trajectory.

Regulatory Landscape

The United Kingdom hospitality real estate market operates within a planning and building-control system where local authorities govern land-use consent under the National Planning Policy Framework (NPPF), while technical compliance is enforced through Building Regulations. Cost and viability for hotel owners are also shaped by non-domestic rates: Budget 2025 set out measures for retail, hospitality, and leisure, and from April 2026 the next business rates revaluation takes effect based on 2024 values, alongside the Non-Domestic Rating Multipliers (England) Regulations 2026 that set multipliers affecting RHL hereditaments.

Operational compliance is influenced by licensing and safety reforms. Central government has advanced a National Licensing Policy Framework for hospitality and leisure, supported by licensing taskforce work, to standardize approaches and reduce friction for premises licensing across local areas. On the development side, updated fire-safety requirements are being incorporated into Approved Document B amendments (including 2025-2026 updates), raising the compliance bar for complex projects and reinforcing the need to plan early for fire strategy and egress provisions as part of hotel-led regeneration and mixed-use schemes.

Value Chain Analysis

Capital formation and site control sit at the start of the hospitality real estate value chain, spanning institutional investors, REIT-like owners, and owner-operators that assemble land or acquire under-utilized assets for conversion. Development then moves through planning, building control, and procurement, with general contractors and specialist trades, notably mechanical and electrical, shaping schedule certainty and capex outcomes. Persistent constraints in M&E capacity and longer lead times for HVAC and electrification packages have made early contractor engagement and phased refurbishment strategies more common, particularly for conversions that compress build programs.

Downstream, operators, including chains, white-label managers, and independents, provide brand standards, distribution, and operating systems that underpin underwriting. Facility management and energy services increasingly influence NOI through retrofits such as heat pumps, on-site solar, and energy-management platforms. Recent UK activity reflects this chain dynamic: corporate developers have leaned into asset intensification and conversions, including Whitbread-led city-center redevelopment proposals and approvals, while planning and Building Safety Regulator process capacity can extend pre-construction timelines, feeding back into financing, contingencies, and contractor selection.

Competitive Landscape

Competition centers on six large operators—IHG, Accor, Hilton, Marriott, Whitbread, and Travelodge—contesting branding rights, distribution reach, and conversion pipelines. Global groups expand through franchise and management agreements, minimizing capital footprints; Marriott’s plan for 100 European conversions illustrates this approach. Domestic champions Whitbread and Travelodge continue buying freeholds for control over asset value and refurbishment cadence.

In parallel, independents and lifestyle specialists—Ennismore, PPHE, and Dalata—scale design-driven concepts that fetch tariff premiums. Institutional investors funnel equity to these operators, drawn by differentiated demand profiles and lower supply saturation. Technology adoption becomes a decisive lever: chains roll out mobile keys, self-check-in, and AI-based pricing, while boutique brands integrate app-based concierge and community event scheduling.

Sustainability is an emerging battleground. IHG’s Low Carbon Pioneer badge and Whitbread’s full-estate electrification roadmap secure access to green financing and corporate travel contracts tied to carbon thresholds. Debt markets favor branded portfolios with clear ESG narratives, evidenced by KKR and Baupost’s 6,500-key Marriott purchase that commanded competitive loan terms. Smaller owners without decarbonization strategies face refinancing headwinds, pushing them toward brand affiliations or disposals.

United Kingdom Hospitality Real Estate Industry Leaders

Whitbread PLC (Premier Inn)

InterContinental Hotels Group PLC

Accor SA

Hilton Worldwide Holdings Inc.

Travelodge Hotels Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Adaptive reuse and intensification create an execution pathway in a high-cost funding environment, as conversions shorten delivery timelines and reduce embodied carbon relative to ground-up builds. Market activity supports this direction: Whitbread has continued adding conversion-led growth options, including its December 2025 freehold acquisition of Victory House in Kingsway, London for a hub by Premier Inn conversion, while global brands extend UK pipelines through agreements designed for conversions and repositionings, such as IHGs 2026 UK agreements across voco and Garner.

Operational technology and energy retrofits also stand out as investable areas tied to margins and financing access, particularly where owners can standardize systems across estates. A concrete signal came in June 2026 when Focus Group initiated a digital transformation program for Mitchells and Butlers across about 1,700 venues using a USD 17 million Cisco infrastructure investment, highlighting the scale at which UK hospitality owners and operators are prioritizing connectivity, security, and centralized management. Alongside that, the April 2026 business rates revaluation and updated multipliers increase emphasis on asset-level operating cost control, strengthening the case for landlords and operators to pursue integrated retrofit programs, including electrification, HVAC upgrades, and smart controls, during refurbishments and conversion cycles.

Recent Industry Developments

- May 2026: InterContinental Hotels Group (IHG) signed Canary Riverside Plaza in London as a Vignette Collection property with Yianis Group, positioning a luxury conversion-led addition in Canary Wharf with an opening targeted for summer 2026. The deal reinforces the role of collection brands in bringing prime, existing assets into global distribution systems, supporting asset repositioning strategies in supply-constrained central London submarkets.

- December 2025: Whitbread acquired the freehold of Victory House, 30-34 Kingsway, London, to convert the building into a circa 200-bedroom hub by Premier Inn hotel. The transaction expands Whitbreads conversion pipeline and aligns with the broader shift toward reusing existing stock to reduce build risk, shorten time to market, and manage capex under tighter underwriting conditions.

- August 2024: PPHE Hotel Group secured planning approval for its 186-room mixed-use, hotel-led development at 79-87 Westminster Bridge Road on Londons South Bank, designed to target BREEAM Excellent. The consent advances a brownfield, centrally located pipeline that combines hospitality with complementary uses, reflecting how planning-ready, ESG-aligned projects are being structured to attract capital and meet evolving corporate travel and sustainability requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of hospitality-focused real estate in the United Kingdom, where the asset is primarily used to host, accommodate, or serve guests, and where performance is linked to occupancy, room pricing, and related on-site guest spending.

Scope exclusions: We exclude pure residential housing, office and industrial real estate, and standalone infrastructure that is not operated as a hospitality asset.

Segmentation Overview

- By Property Type

- Hotels

- Resorts & Spas

- Others (Serviced Apartments, Boutique Inns, etc.)

- By Type

- Chain Hotels

- Independent Hotels

- By Asset Class

- Affordable/Budget

- Midscale

- Luxury

- By Country

- England

- London

- Rest of England

- Scotland

- Wales

- Northern Ireland

- England

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base around the UK travel and lodging demand pool, and to understand how supply is changing across key destinations. We referenced public sources such as the UK Office for National Statistics for tourism and spending indicators, VisitBritain for inbound and domestic visitor trends, and the UK Land Registry plus HM Revenue and Customs releases where pricing and transaction context was helpful.

To keep the market model grounded, we also reviewed sources such as planning and local authority portals for pipeline signals, peer reviewed real estate and hospitality studies, and selected annual reports and investor presentations for operating and portfolio context. A paid subscription for company financials and intelligence was used selectively to normalize filing formats, and a patent database was checked in a limited way when building assumptions around building efficiency and retrofit activity. These examples are not exhaustive, and many other public and paid sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how UK hospitality assets are valued and how revenue drivers are behaving across different locations and property formats. We spoke with a mix of owners, operators, developers, brokers, and advisors, and we also included lenders and property managers where they could clarify cap rate movement, refinancing behavior, and refurbishment timing. For a UK-only study, outreach was balanced across major cities and leisure destinations, and gaps from desk research were closed through follow-up questions and consistency checks.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | |

| Mid tier: 48% | Functional/Unit leaders: 28% | |

| Smaller Players: 14% | Managers: 58% |

Market-Sizing & Forecasting

Sizing started from a top-down reconstruction tied to the UK hospitality real estate stock and its earning ability, where demand signals and supply additions are translated into value using price and yield assumptions. To keep the totals realistic, we cross-checked with selective bottom-up approximations, such as sampled asset values by major location, typical room counts by property type, and implied value per key under observed transaction ranges.

Inputs used in the model included hotel room supply and pipeline direction, occupancy and ADR movement, RevPAR trend as a combined signal, inbound and domestic visitor volumes, and the share of nights shifting toward branded and extended-stay formats. When a bottom-up input was missing for a sub-area, we used proxy ratios from comparable UK destinations and then adjusted them after expert feedback.

Forecasting relied mainly on scenario analysis, where a base case was built from expected travel demand, new supply delivery, and financing conditions, and then tested with an upside and downside path. The final forward view was set only after interview feedback confirmed that the assumed cap rate and operating recovery path were plausible for the next planning cycle.

Data Validation & Update Cycle

Validation was done through triangulation across independent signals, then by checking that movements made sense at the city and property-type level. Outliers were flagged when implied value growth moved too far from occupancy, ADR, and transaction sentiment, and those items were reworked before sign-off.

A second analyst review was completed to confirm calculations, currency handling, and year alignment, followed by targeted re-contact when a key assumption shifted. Reports are refreshed annually, and interim updates are made when material events occur, such as major policy changes, sharp rate moves, or unusually large deal activity. Before delivery, we run a fresh pass so clients receive the latest updated view.

Mordor Intelligence's United Kingdom Hospitality Real Estate Sector Market Sizing Compared With Other Published Estimates

Published market sizes for UK hospitality real estate can vary a lot, even when the topic label looks the same, because the counted assets and the timing of valuation assumptions are often different. The table below highlights how base year choice, what is treated as a hospitality property, and how exchange rates are handled can quickly move the final USD number.

A common gap driver is scope, where some estimates mix operating industry revenue with property value, or they expand the definition to include adjacent leisure real estate that is not run as a hospitality asset. Differences also come from whether the estimate leans on transaction-led pricing during an active year, or it smooths values using longer-term averages, which changes the implied cap rate and value per key.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 81.23 B (2025) | |

| Global Consultancy A | USD 107.40 B (2023) | Uses an earlier stated year and a different study window, and it can also reflect a broader asset definition that blends more lodging-linked property formats into one total, which raises the value base. |

| Industry Publisher B | USD 87.60 B (2026) | Anchors sizing around a later market value year and applies a faster growth path, which is sensitive to the assumed cap rate direction and the timing of new supply coming online. |

The table shows a noticeable spread that is mostly explained by year alignment and what gets counted as hospitality real estate. In Mordor Intelligence's model, value is tied to hospitality-operated property types and is kept separate from broader hospitality industry revenue, which helps keep inputs traceable to occupancy, ADR, and transaction-based checks.

Key Questions Answered in the Report

How large is the United Kingdom hospitality real estate market in 2026?

The sector is valued at USD 84.57 billion in 2026, with a forecast to reach USD 103.41 billion by 2031.

Which property type is growing fastest across the country?

Serviced apartments and other extended-stay formats are projected to expand at a 4.53% CAGR through 2031.

What region shows the highest growth outlook?

Scotland leads with a 5.03% CAGR forecast, outpacing London and the rest of England.

Why are conversions popular among developers?

Adaptive reuse of offices and retail units lowers capex, cuts development time, and supports ESG goals, improving returns.

How are operators coping with labor shortages?

Chains and independents invest in self-service kiosks, mobile check-in, and robotics to reduce staffing requirements and protect margins.

Page last updated on: