Surgical Imaging Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 4.75 Billion |

| Market Size (2031) | USD 7.18 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

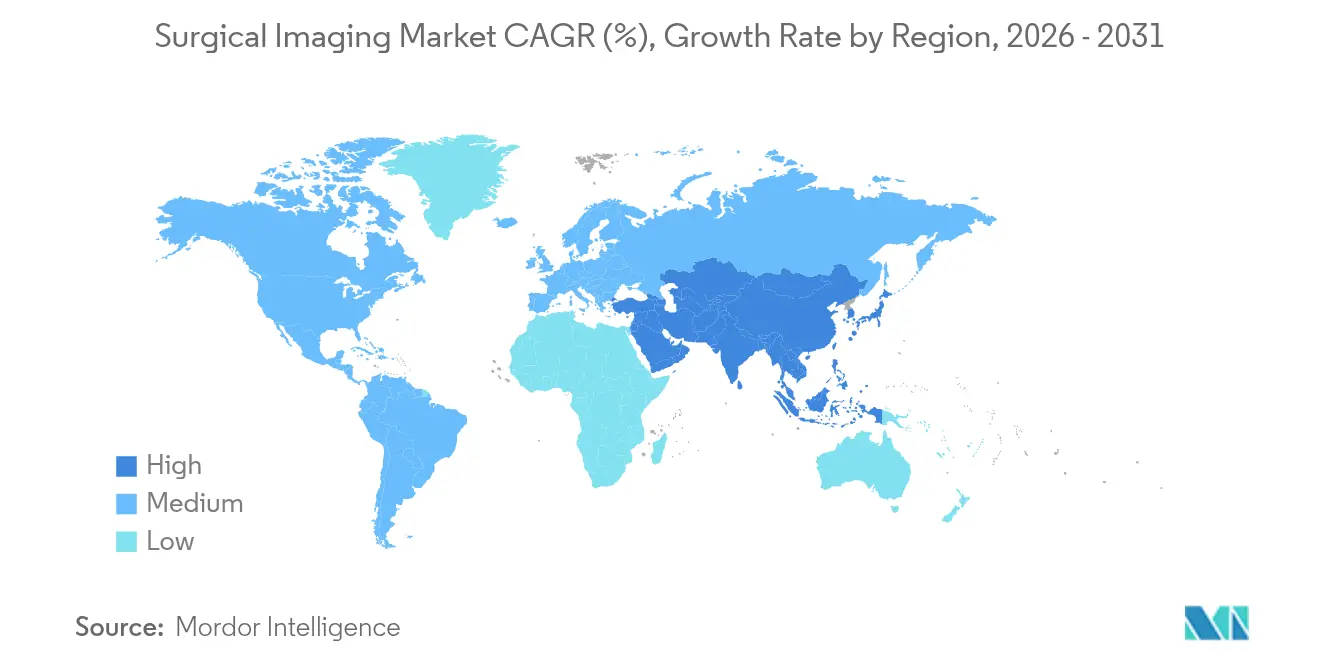

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

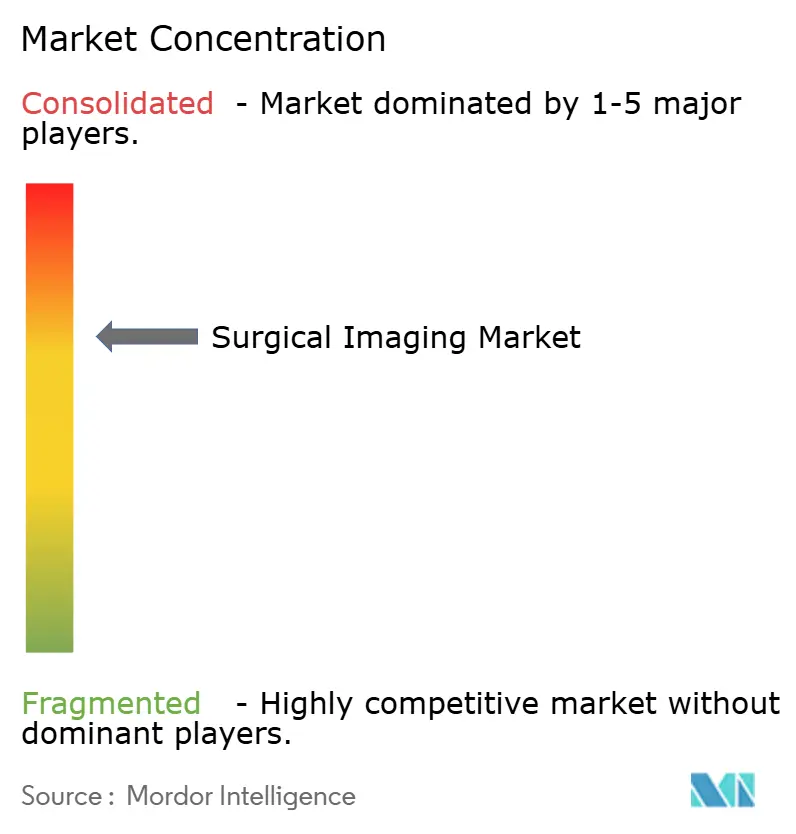

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Imaging Market Analysis by Mordor Intelligence

Market Analysis

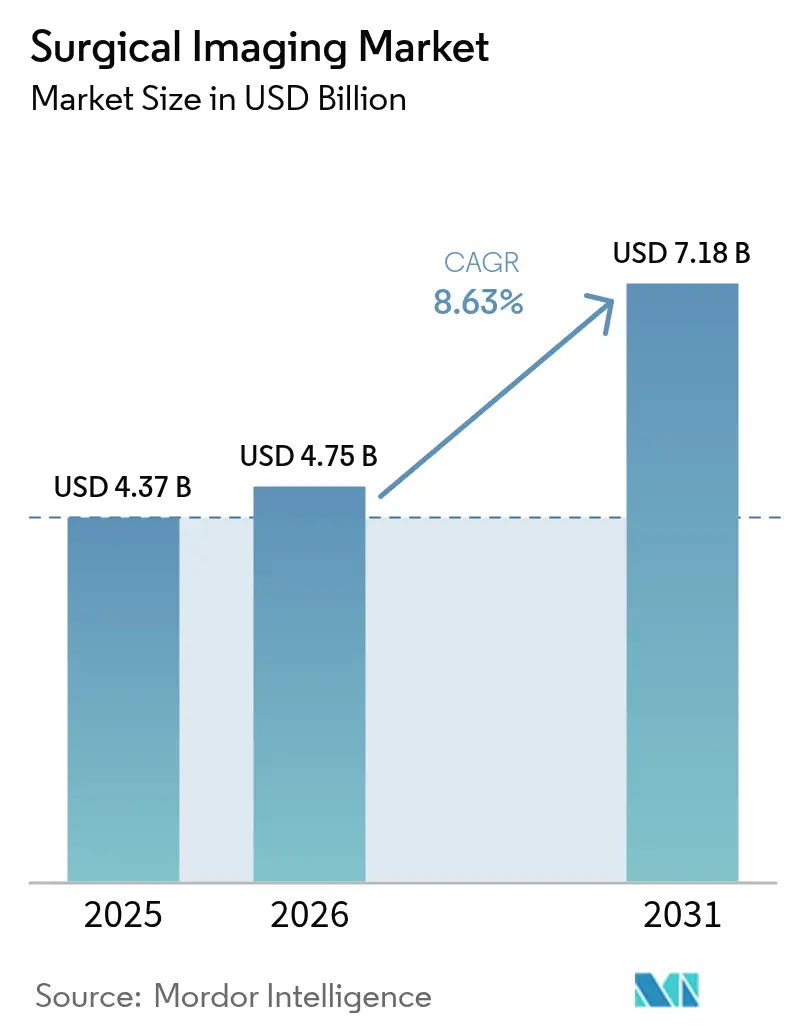

The surgical imaging market size was valued at USD 4.37 billion in 2025 and estimated to grow from USD 4.75 billion in 2026 to reach USD 7.18 billion by 2031, at a CAGR of 8.63% during the forecast period (2026-2031). Escalating demand for real-time visualization in minimally invasive procedures, rapid incorporation of artificial intelligence (AI) into intra-operative workflows, and the need to optimize over-stretched surgical workforces form the fulcrum of current growth. Vendors that seamlessly fuse hardware, software, and decision-support services now compete on workflow efficiency rather than on individual device specifications. Capital spending is pivoting toward mobile, high-performance systems suited to ambulatory settings, while tier-1 hospitals invest in hybrid operating rooms that consolidate surgical and interventional radiology capabilities. Finally, geographic expansion in Asia-Pacific underscores the structural shift of surgical volumes to emerging economies and intensifies rivalry for first-mover advantage in those markets.

Key Report Takeaways

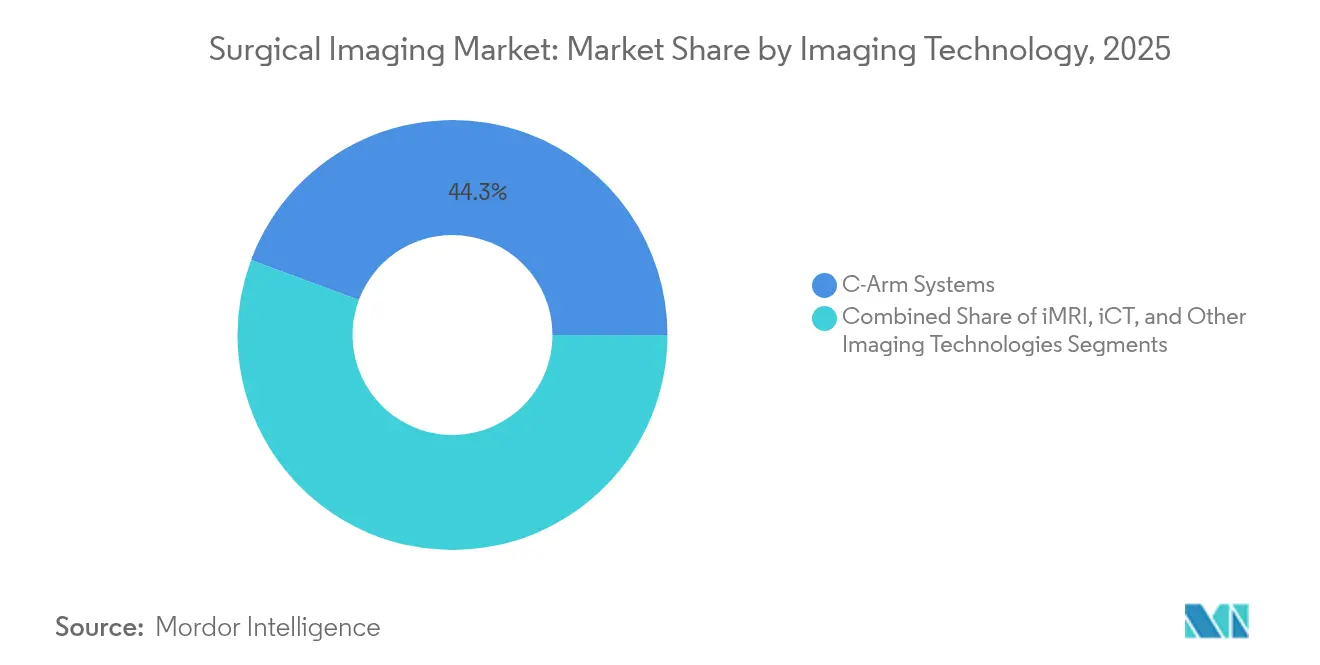

- By imaging technology, C-Arm Systems held 44.32% of the surgical imaging market share in 2025, while intra-operative 3-D/4-D imaging technologies are advancing at a 9.86% CAGR through 2031.

- By application, orthopedic and trauma surgery commanded 28.92% of the surgical imaging market size in 2025, whereas cardiac and vascular surgery is projected to grow at a 9.55% CAGR to 2031.

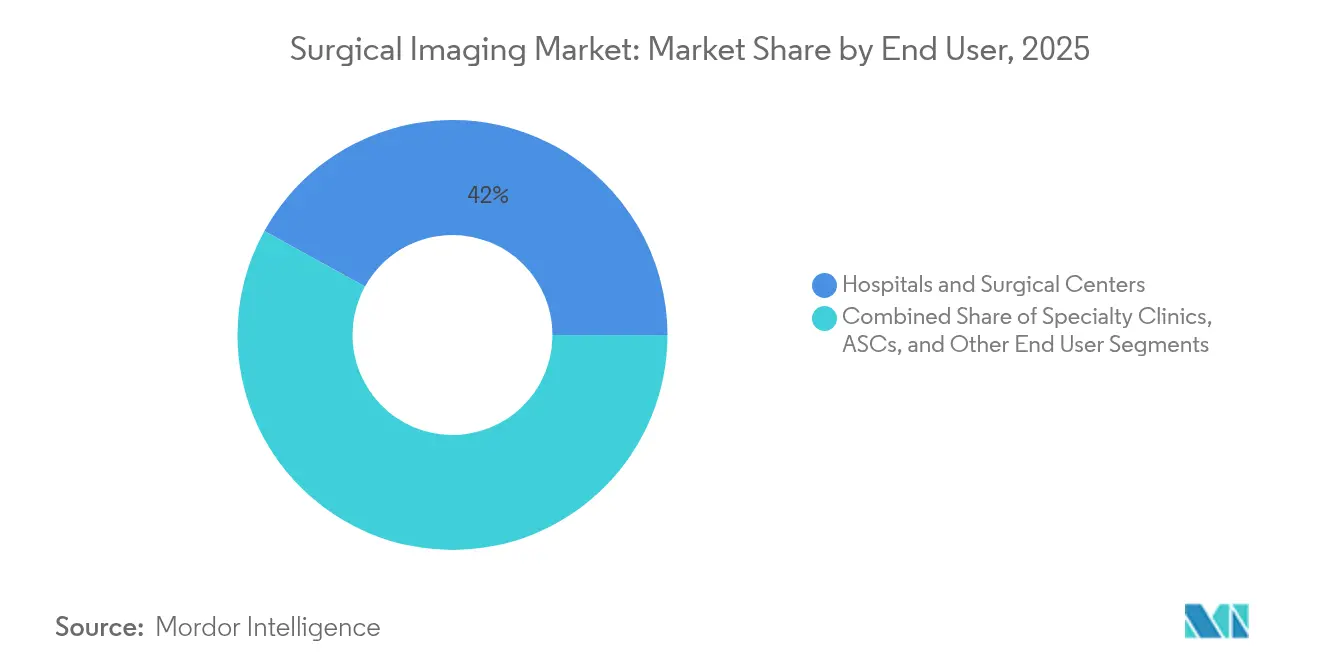

- By end user, hospitals and surgical centers led with 41.96% of revenue in 2025, and ambulatory surgical centers are moving ahead at a 9.83% CAGR during the same horizon.

- By geography, North America accounted for 38.74% of the surgical imaging market share in 2025, while Asia-Pacific is forecast to expand at a 10.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for minimally invasive surgeries | +2.1% | Global; early uptake in North America & EU | Medium term (2-4 years) |

| Rising burden of chronic diseases | +1.8% | Global; aging populations in developed markets | Long term (≥ 4 years) |

| Technological shift toward 3-D/4-K imaging | +1.9% | North America & EU core; spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of hybrid operating rooms | +1.6% | North America, EU, select Asia-Pacific metros | Medium term (2-4 years) |

| AI-driven intra-operative decision support | +2.2% | Global; led by North America & EU | Short term (≤ 2 years) |

| Rapid adoption of mobile C-arms by ASCs | +1.4% | North America & EU; emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Minimally Invasive Surgeries

Minimally invasive approaches replace tactile feedback with image-guided precision, making intra-operative visualization core to procedural success. Advanced C-arms now embed AI-based noise reduction and edge-enhancement algorithms that sharpen critical anatomical landmarks and curtail radiation exposure[1]“Artificial Intelligence and Medical Devices,” FDA.gov. Mobile variants cater to tight ASC footprints by combining slim gantries with automated positioning and rapid boot-up times. Real-time quality improvements reduce conversion to open surgery, shorten length of stay, and strengthen a hospital’s performance metrics under value-based payment models. As payers link reimbursement to outcomes and patient satisfaction, facilities that lack sophisticated imaging capability risk referral leakage to tech-enabled competitors. The surge therefore aligns clinical needs, economic incentives, and patient preferences around a unified migration pathway to high-acuity imaging systems.

Rising Burden of Chronic Diseases

Non-communicable conditions such as cardiovascular disease, osteoarthritis, and cancer escalate lifetime procedural counts and drive recurring imaging demand. Multi-stage patient journeys—pre-operative mapping, intra-operative guidance, and post-operative surveillance—each rely on dedicated visualization systems, creating predictable revenue streams for manufacturers [WHO.INT]. Aging demographics intensify complexity; octogenarian patients often undergo valve replacements, spine fusions, and tumor resections within the same decade, multiplying imaging touchpoints. Hospitals counter volume spikes by standardizing on multimodality suites capable of fluoro-CT fusion or echo overlay, minimizing patient transfers and staff redeployment. This confluence of clinical and operational pressures accelerates procurement of integrated surgical imaging market platforms that can manage diverse disease trajectories without workflow disruption.

Technological Shift toward 3-D/4-K Intra-operative Imaging

Three-dimensional and ultra-high-definition (4-K) outputs recast operative planning from two-plane estimation to volumetric accuracy. Orthopedic teams employ automatic screw-trajectory planning, while neurosurgeons exploit real-time tumor margin visualization to preserve eloquent cortex [CANON-MEDICAL.COM]. AR overlays align reconstructed anatomy to the patient’s surface, freeing surgeons from gaze shifts between screens and operative fields. Early adopters report double-digit cuts in operative minutes, amplifying daily case capacity without additional staffing. The rapid benefits expedite budget approvals, explaining short-term driver prominence despite capital intensity. Downstream, software upgrades enlarge field-of-view and integrate fiber-optic shape-sensing, safeguarding long-term relevance of installed fleets and sustaining the surgical imaging market growth curve.

Expansion of Hybrid Operating Rooms in Tier-1 Hospitals

Hybrid suites marry high-resolution imaging with full surgical infrastructure to address complex aortic repairs, trauma embolizations, and oncologic resections in one setting. Up-front investments topping USD 2 million include lead shielding, laminar airflow retrofits, and ceiling-mounted robotics. However, procedural bundling eliminates inter-departmental transfers, slashes anesthesia turnover, and lifts surgeon recruitment appeal. Academic medical centers spearhead installation counts, but large private hospital chains follow suit to avert patient flight. Hybrid adoption thus reinforces a two-tier market: premium facilities chase all-in imaging ecosystems, while community hospitals weigh modular, mobile alternatives. Both scenarios ultimately buoy the surgical imaging market through differentiated procurement paths aligned to institutional scale.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment & procedure costs | −1.7% | Global; most acute in emerging markets | Long term (≥ 4 years) |

| Stringent regulatory & certification hurdles | −1.2% | Global; jurisdiction-specific variations | Medium term (2-4 years) |

| Reimbursement limitations in emerging markets | −0.9% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Supply-chain vulnerability of flat-panel detectors | −0.8% | Global; concentrated among manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Equipment & Procedure Costs

Total cost of ownership often doubles the sticker price once installation, shielding, and multi-year service contracts are considered. Premium interventional C-arms can cost up to USD 250,000, and hybrid OR build-outs reach USD 2 million when structural retrofits are required [SIEMENS-HEALTHINEERS.COM]. Mid-tier hospitals therefore delay upgrades or enter leasing arrangements that include usage quotas, potentially throttling case growth. Emerging-market providers face import tariffs and currency volatility that inflate acquisition budgets. While refurbished systems offer cost relief, they typically lack AI-ready processors and vendor-supported software pathways, constraining future-proofing and tempering surgical imaging market acceleration.

Stringent Regulatory & Certification Hurdles

Device makers must navigate divergent regional requirements, from U.S. FDA pre-market submissions to the European MDR’s post-market clinical follow-up mandates. AI software add-ons demand continuous algorithm retraining logs and real-world performance tracking, lengthening development by up to 24 months and raising capital needs. Smaller innovators struggle to fund multi-site clinical trials, slowing entry of disruptive solutions that could energize competition. Consequently, regulatory complexity modestly caps the surgical imaging market CAGR by favoring large incumbents and stretching commercialization timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Imaging Technology: AI-Assisted C-Arms Underpin Automation Push

C-Arm Systems retained 44.32% of the surgical imaging market share in 2025 owing to multi-specialty versatility and entrenched surgeon familiarity. Self-driving models such as Siemens Healthineers’ CIARTIC Move combine lidar sensors with phase-recognition software that positions the arm autonomously, trimming fluoroscopy time and radiation dosage. Mobile C-arms remain ASC favorites for their plug-and-play portability, while fixed versions dominate hybrid suites that prize image clarity over space economy. Intra-operative CT (iCT) and MRI (iMRI) target neurosurgery and oncology centers where real-time tissue contrast justifies seven-digit investments. Fluoroscopy and ultrasound hold steady as budget-friendly options for routine cases, although value-added AI may eventually reset their price-performance calculus.

Intra-operative 3-D/4-D imaging outpaces all peers at a 9.86% CAGR through 2031. These systems deliver volumetric data sets with near-real-time reconstruction, enabling spinal alignment checks or transcatheter valve deployment verification before wound closure. Image-to-device registration aligns implant trajectories within sub-millimeter tolerances, accelerating adoption among orthopedic and cardiac teams. Continued declines in GPU costs and cloud-compute pricing should narrow total ownership gaps, fortifying the long-term ascent of this technology cohort and sustaining overall surgical imaging market expansion.

By Application: Cardiac & Vascular Interventions Propel Next-Wave Growth

Orthopedic and trauma surgery generated 28.92% of the surgical imaging market size in 2025, buoyed by high incidence of joint replacements and fracture cases. Imaging-guided screw placement mitigates mal-alignment and lowers revision rates, reinforcing the installed-base appeal of mobile C-arms in emergency departments and trauma bays. Robotic-arm assisted knees and hips further intensify intra-operative visualization needs, entrenching image acquisition as a procedural prerequisite.

Cardiac and vascular surgery is forecast to grow at 9.55% CAGR, fastest among applications, driven by structural heart and peripheral vascular interventions that depend on multi-modality imaging overlays. Transcatheter aortic valve replacement (TAVR) now rivals open surgery volumes, and complex endovascular aneurysm repair necessitates rotational angiography coupled with 3-D echo fusion. As reimbursement codes expand for catheter-based therapies, hospitals recalibrate capital budgets toward advanced angio-CT hybrids, accelerating revenue opportunities inside the surgical imaging market.

By End User: Ambulatory Centers Re-Define Procurement Priorities

Ambulatory surgical centers (ASCs) lead growth at 9.83% CAGR, mirroring payer mandates to shift elective volume away from high-cost inpatient settings. Compact imaging carts offering hospital-grade output align with ASC space constraints and same-day discharge protocols. Subscription service contracts swap capex for opex, letting centers scale technology in step with case ramp-up. Operating efficiencies measured in room turns and staffing ratios push ASCs to favor intuitive UIs and automated exposure settings that minimize training curves and radiation events.

Hospital and surgical centers still commanded 41.96% of revenue in 2025, leveraging centralized purchasing to negotiate enterprise-wide platform deals and shared-service fleets. Emphasis now lies on cross-department standardization that eases technician redeployment and simplifies service logistics. Specialty clinics and academic institutes contribute smaller slices yet shape future trajectories by piloting beta releases and generating peer-reviewed validation that de-risks broader rollouts, thereby lifting the long-range prospects of the surgical imaging industry.

Geography Analysis

North America accounted for 38.74% of 2025 revenue on the back of premium pricing, sophisticated reimbursement policies, and early AI adoption. The U.S. market prioritizes hybrid OR investment, and FDA fast-track programs expedite commercial launches that set global benchmarks. Canada pursues provincial asset-sharing networks to lift equipment utilization, while private Mexican hospitals court medical tourists with newest-generation C-arms and CT-fluoro hybrids.

Europe maintains balanced growth as aging demographics and surgical wait-time targets spur modernization of imaging fleets. Germany and the United Kingdom spearhead intra-operative 3-D program adoption, supported by government diagnostic imaging funds. France and Italy temper spending with value-based procurement models that weigh lifetime costs against measurable outcomes, nudging vendors to present total-care economics rather than hardware price tags. Pan-EU CE-mark standardization lowers compliance friction, smoothing multi-country rollouts and underpinning the surgical imaging market trajectory.

Asia-Pacific is poised for the highest regional expansion at a 10.04% CAGR to 2031. China funnels public-private partnerships into tertiary hospital upgrades, while India’s burgeoning private sector builds ASC chains that source mid-tier but AI-ready imaging solutions. Japan deploys AI decision-support modules rapidly, leveraging domestic electronics expertise; South Korea replicates pace with government innovation grants. Australia, though smaller in volume, reinforces demand through mandatory technology refresh cycles and an aging population with rising orthopedic and cardiovascular procedure counts. Collectively, these factors cement Asia-Pacific as a strategic battleground for share capture within the global surgical imaging market.

Competitive Landscape

Market leadership resides with diversified conglomerates that integrate hardware, software, and lifecycle services into turnkey ecosystems. GE HealthCare’s USD 1.45 billion purchase of MIM Software adds advanced visualization and contouring engines to its OEC and Discovery C-arm lines, pivoting value propositions from equipment capabilities toward workflow orchestration[3]“GE HealthCare Completes Acquisition of MIM Software,” GEHealthCare.com. Siemens Healthineers bundled its CIARTIC Move self-navigating C-arm with Syngo Carbon enterprise imaging to guarantee single-vendor continuum, raising competitor switching barriers. Canon Medical Systems leverages Deep Learning Reconstruction algorithms to retrofit installed CT base, extending revenue without incremental hardware swaps.

White-space entrants concentrate on software-only overlays that enhance existing fleets, demonstrating dose reductions and navigation accuracy gains independent of device brand. Some OEMs now license independent algorithms to stay hardware agnostic, hedging against platform commoditization. Meanwhile, strategic alliances between imaging majors and robotic-surgery firms pursue closed-loop ecosystems where pre-op planning, in-field guidance, and post-op analytics converge seamlessly. Overall, competition pivots from image resolution metrics to end-to-end automation proficiency, keeping the surgical imaging market in an innovation-driven contest.

Surgical Imaging Industry Leaders

Canon Medical Systems Corporation

Siemens Healthineers

GE Healthcare

Ziehm Imaging GmbH

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Siemens Healthineers posted 11.7% organic imaging revenue growth for Q1 FY2025, fueled by CIARTIC Move demand.

- September 2024: Philips gained FDA clearance for the LumiGuide Navigation Wire that offers live visualization during minimally invasive cardiac interventions.

- November 2024: Philips launched the Spectral CT 7500 RT with AI reconstruction aimed at radiation-therapy planning and surgical navigation.

- October 2024: Canon Medical Systems upgraded its Aquilion CT range with AiCE deep-learning reconstruction to lower dose while enhancing image clarity.

Global Surgical Imaging Market Report Scope

As per the scope of the report, surgical imaging is any surgical procedure where the surgeon uses tracked surgical instruments in conjunction with the preoperative or intraoperative images, in order to directly or indirectly guide the procedure. The Surgical Imaging Market is segmented By Technology (Magnetic resonance imaging, Computed Tomography, C-Arm (Fixed C-Arm and Mobile C-Arm), Ultrasound, and Other Technologies), By Application (Cardiac and Vascular Surgery, Neurosurgery, Orthopedic and Trauma Surgery, Gastrointestinal Surgery, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Magnetic Resonance Imaging (iMRI) | |

| Computed Tomography (iCT) | |

| C-Arm Systems | Fixed C-Arm |

| Mobile C-Arm | |

| Fluoroscopy | |

| Ultrasound | |

| Intra-operative 3-D / 4-D Imaging | |

| Other Technologies |

| Cardiac & Vascular Surgery |

| Neurosurgery |

| Orthopedic & Trauma Surgery |

| Gastrointestinal Surgery |

| Spine Surgery |

| Urology & Gynecology Surgery |

| Other Applications |

| Hospitals & Surgical Centers |

| Ambulatory Surgical Centers (ASCs) |

| Specialty Clinics |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Imaging Technology | Magnetic Resonance Imaging (iMRI) | |

| Computed Tomography (iCT) | ||

| C-Arm Systems | Fixed C-Arm | |

| Mobile C-Arm | ||

| Fluoroscopy | ||

| Ultrasound | ||

| Intra-operative 3-D / 4-D Imaging | ||

| Other Technologies | ||

| By Application | Cardiac & Vascular Surgery | |

| Neurosurgery | ||

| Orthopedic & Trauma Surgery | ||

| Gastrointestinal Surgery | ||

| Spine Surgery | ||

| Urology & Gynecology Surgery | ||

| Other Applications | ||

| By End User | Hospitals & Surgical Centers | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty Clinics | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the surgical imaging market in 2026?

The market stands at USD 4.75 billion in 2026 and is forecast to reach USD 7.18 billion by 2031.

Which imaging technology generates the highest revenue?

C-Arm Systems contribute 44.32% of 2025 revenue due to their cross-specialty versatility.

Which application is growing fastest?

Cardiac and vascular procedures are advancing at a 9.55% CAGR through 2031 driven by structural heart interventions.

Why are ambulatory surgical centers important to equipment vendors?

ASCs exhibit a 9.83% CAGR in imaging demand, favoring portable, AI-enabled systems that fit space and cost constraints.

Which region shows the strongest growth outlook?

Asia-Pacific leads with a projected 10.04% CAGR owing to hospital infrastructure investments and rising surgical volumes.

Page last updated on: