Minimally Invasive Spine Surgery Market Size and Share

Market Overview

| Study Period | 2021 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2021 - 2023 |

| Growth Rate | 5.50% CAGR |

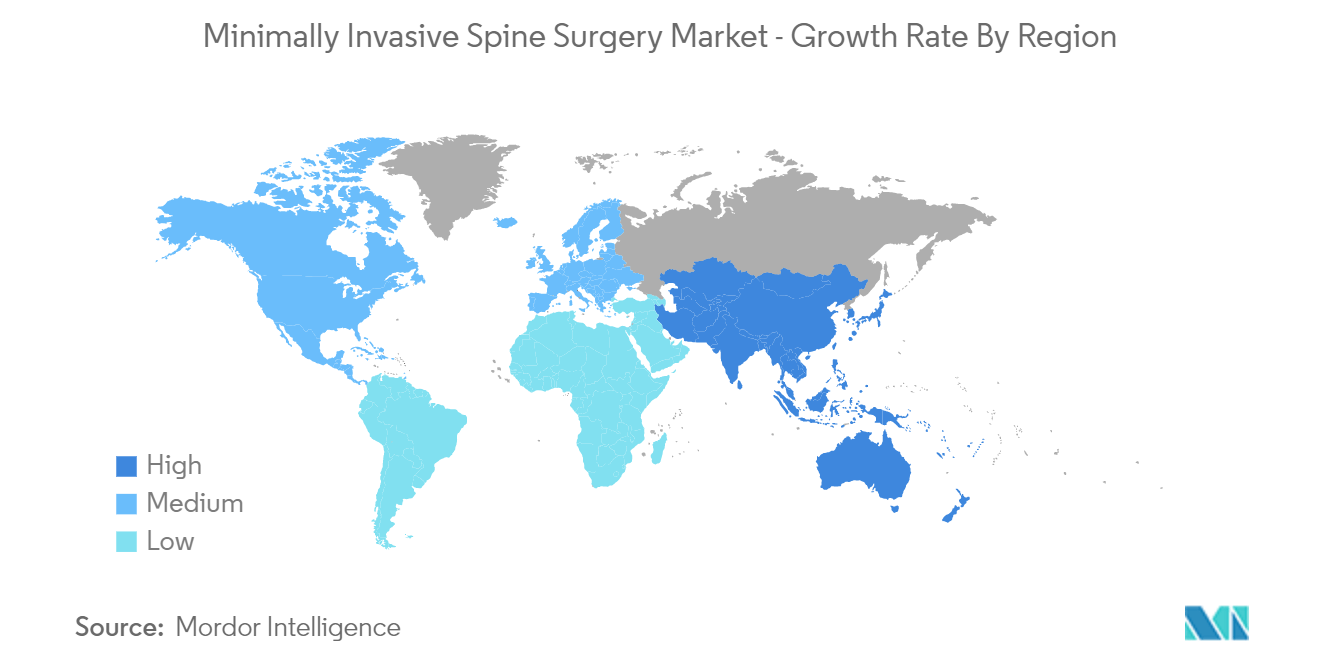

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

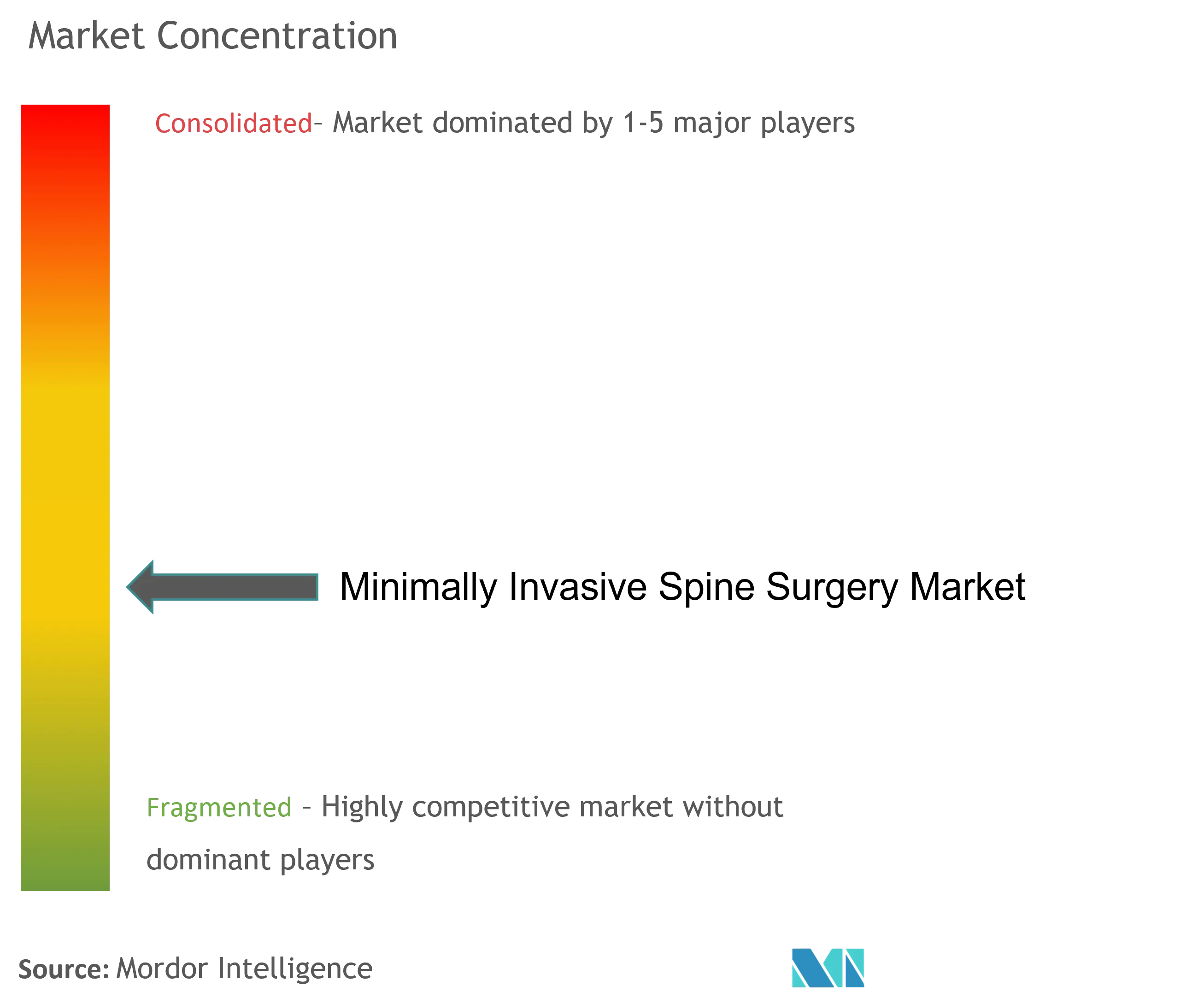

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Minimally Invasive Spine Surgery Market Analysis by Mordor Intelligence

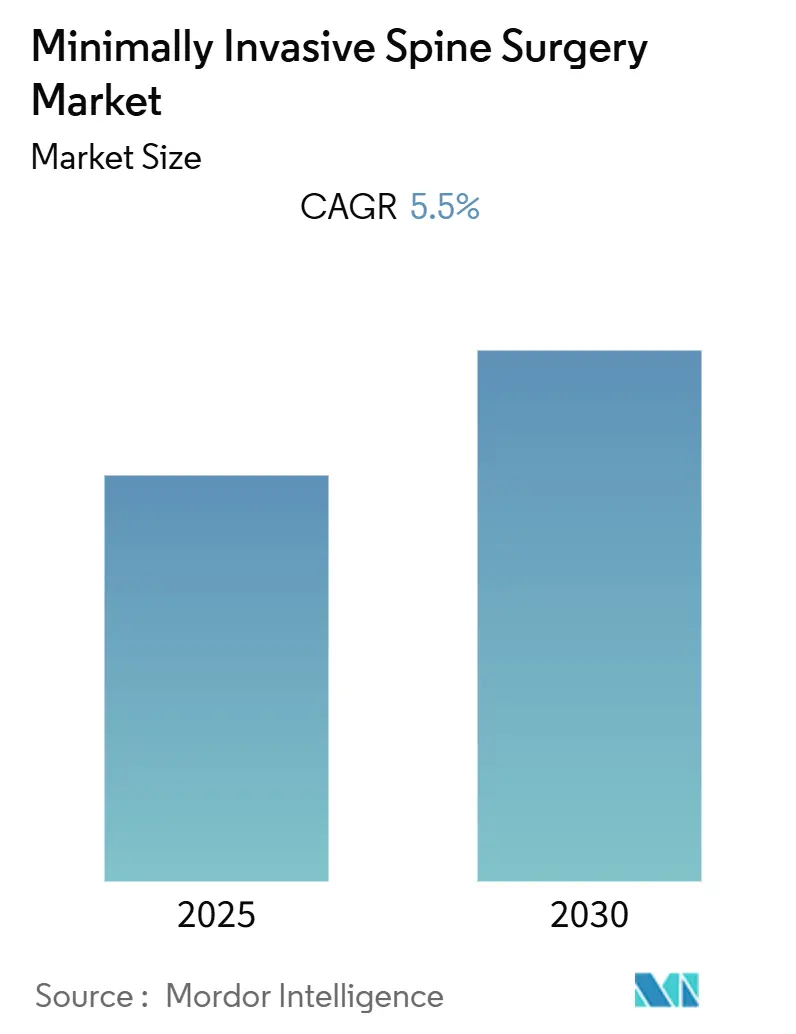

The Minimally Invasive Spine Surgery Market is expected to register a CAGR of 5.5% during the forecast period.

- COVID-19 significantly impacted the minimally invasive spinal surgery market due to the cancellations of elective spine surgeries worldwide in the initial phase of the pandemic. Urgent spine surgeries were performed during the later phase of the pandemic. For instance, an article published in Acta Ortopedica Brasileira journal in July 2022 indicated that urgent surgeries were performed on 60.81% of patients during the later phase of COVID-19 in a tertiary hospital in Latin America. Hence, as the number of COVID-19 cases declined, the market regained its pre-pandemic level in terms of demand for spinal surgery devices.

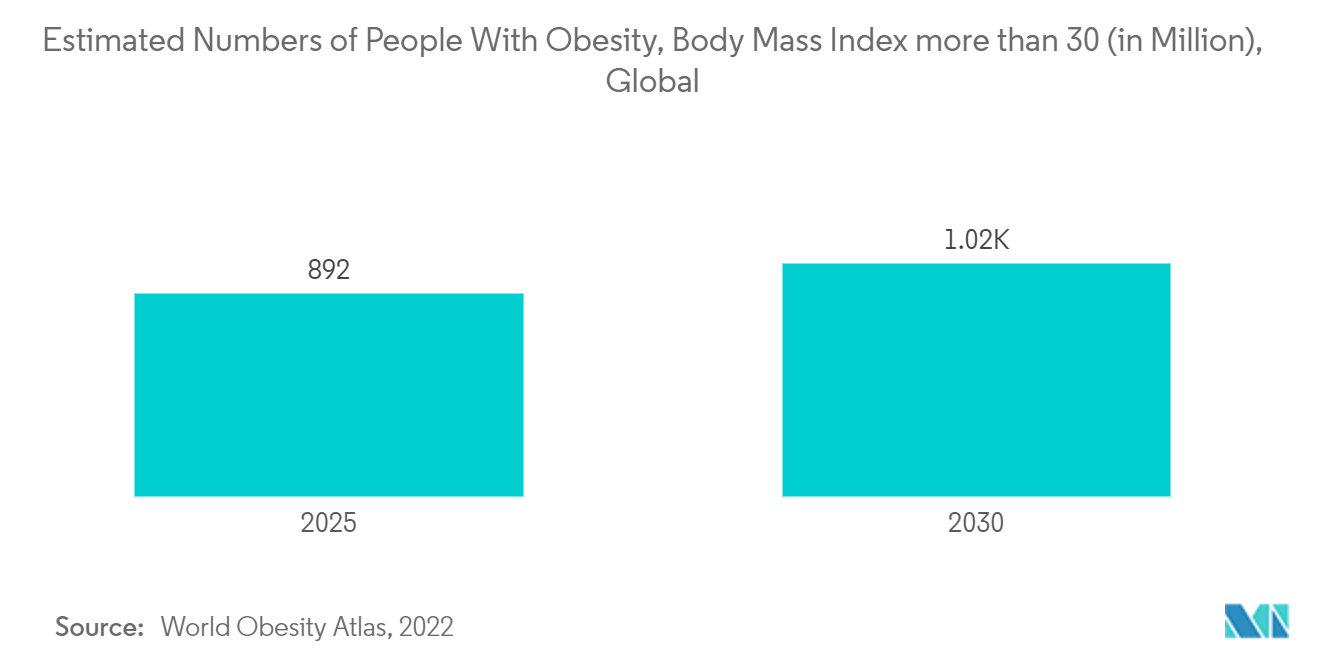

- Additionally, the increase in incidences of spinal disorders, the rising number of ambulatory surgical centers, and the growing geriatric and obese population were the major driving factors of minimally invasive spine surgeries that drove the growth of the studied market over the forecast period.

- Furthermore, the growing geriatric population boosts the demand for inimally invasive spine surgery, accelerating market growth. For instance, according to Statpearls article updated in July 2022, spinal stenosis is a common condition among the elderly population. The same source indicated that 1 in 1000 people over 65 and 5 in 1000 people over 50 are at an increased risk of developing spinal stenosis. Thus, the geriatric population is at high risk of spinal diseases and hence is estimated to propel the market growth during the forecast period.

- Additionally, the advancements in technology and increasing product approvals, along with partnerships and acquisitions by key players, are helping in the market growth. For instance, in June 2022, Xenco Medical launched its Multilevel CerviKit, a single-use cervical spine implant for cervical spine procedures. It can be used in the ambulatory surgery center setting. Such developments are projected to propel the market growth during the forecast period.

- The advancements in minimally invasive devices are a major driver for its adoption across the globe. Robot-assisted surgery is becoming a fast-moving technology that enhances the accuracy of complex surgeries and reduces patient trauma. For instance, in December 2022, BLK-Max Hospital in India installed an advanced integrated robotic system for spine surgery. The robotic system deploys artificial intelligence (AI) to visualize spinal anatomy during complex surgeries. Therefore, due to continual advancements in robot-assisted surgical systems, the market is expected to grow during the forecast period.

- However, the stringent regulatory framework and high costs of surgical procedures are likely to impede the market growth.

Global Minimally Invasive Spine Surgery Market Trends and Insights

Biomaterial Segment is Expected to Witness Growth Over the Forecast Period

- Biomaterial refers to the biocompatible materials in the development of surgical devices and implants used in minimally invasive spine surgeries. It plays a crucial role in the development of devices and implants that are used to stabilize and support the spine, promote fusion between vertebrae, and enhance the healing process. Some common biomaterials include titanium alloys, stainless steel, polymers, and biologics.

- The strategic initiatives by market players, such as launches, partnerships, and collaboration, are expected to drive the segment's growth. For instance, in March 2023, Invibio Biomaterial Solutions launched the Peek-Optima Am filament, an implantable polyetheretherketone polymer for the manufacturing of 3D-printed medical devices, including spinal implants. Also, in December 2021, Spine Wave launched the Defender Anterior Cervical Plate and the Stronghold C 3D Titanium Interbody Device. The Defender Anterior Cervical Plate is made of titanium that provides fixation for anterior cervical fusion procedures. Hence, launches and adoption of advanced biomaterials are projected to boost the segment's growth.

- Furthermore, the research studies using biomaterial for the treatment of various spine surgeries also contribute to the market growth. For instance, in September 2022, DiFusion, Inc., a company engaged in biomaterial technological innovation focused on introducing bioactive polymers in spinal and orthopedic surgery, reported positive results from its retrospective study to determine if a bioactive interbody device reduced the time horizon for Spinal fusions using innovative biomaterial. The research studies are expected to create opportunities for developing an innovative product to fulfill the rising demand for innovations in biomaterials, which is expected to propel the segment's growth during the forecast period.

- Therefore, owing to factors such as rising demand for innovative biomaterials and its launches and research studies, the segment is expected to witness growth during the forecast period. Minimally invasive spine surgery is a type of surgery performed on the spine's bones. This surgery generally uses smaller incisions than traditional surgery and often causes less harm to nearby muscles and other tissues. This minimally invasive surgery can lead to less pain and faster recovery after surgery. The minimally invasive spine surgery market is segmented by product type (implants & instrumentation and biomaterials), application (fusion surgery and non-fusion surgery), treatment (lumbar disc herniation, thoracic disc herniation, spinal stenosis, degenerative spinal disease, and others), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

- The report offers the value (in USD) for the above segments.

North America is Expected to Hold a Significant Share of the Minimally Invasive Spine Surgery Market Over the Forecast Period

- North America is expected to witness significant growth in the minimally invasive spine surgery market over the forecast period owing to factors such as the prevalent spine disorders and technological advancements in spine surgery devices.

- For instance, as per the National Spinal Cord Injury Statistical Centre data published in 2023, the annual incidence of traumatic spinal cord injury (tSCI) is approximately 54 cases per one million people in the United States, representing roughly 18,000 new tSCI cases each year. Spinal cord injury is associated with a high chance of damage to the delicate neural tissue, leading to neurological deficits and functional impairments, requiring minimally invasive spine surgery techniques to minimize tissue trauma and disruption. This is anticipated to boost the market growth.

- Furthermore, the developments by market players also contribute to the studied market growth during the forecast period. For instance, in August 2022, Nexus Spine launched the PressON posterior lumbar fixation system in the United States. Presson features rods that press onto pedicle screws rather than attach using set screws. This innovative design is around one-fourth the size of conventional systems, implants more quickly, is stronger biomechanically and enables the intraoperative creation of patient-specific rods. Also, in March 2022, Accelus completed a surgery that combined its Remi Robotic Navigation, LineSider Spinal System, and FlareHawk Expandable Interbody Fusion Device technologies in one procedure. Thus, the technological advancements in MISS products are likely to boost the demand for such products, which is expected to propel the market growth in the region during the forecast period.

- Therefore, owing to factors such as the high burden of spine disorders and rising launches by market players, the studied market is expected to witness growth in North America during the forecast period.

Competitive Landscape

The competitive landscape provides an outlook of analysis of the various business growth strategies adopted by the industry players, increasing the number of partnerships, agreements, and collaborations among market players and driving the market value. The major players in the market are engaged in product development and strategic alliances to strategically cater to the growing global demand for the market and to gain a robust place in the market. Major companies profiled in the global market report include Globus Medical Inc., NuVasive Inc., Life Spine In, Captiva Spine, Inc., Medtronic, Johnson & Johnson (DePuy Synthes), Boston Scientific, Zimmer Biomet, Aesculap, Inc., RIWOspine GmbH, among others.

Minimally Invasive Spine Surgery Industry Leaders

Medtronic

Johnson & Johnson (DePuy Synthes)

Boston Scientific

Zimmer Biomet

Aesculap, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2022: Wenzel Spine, Inc., a medical technology company providing minimally invasive surgical and diagnostic solutions for the treatment of spinal disorders, launched the S-LIF Procedure for Stand-alone Lumbar Interbody Fusion using the VariLift-LX device.

- July 2022: Nexus Spine, a developer of biomechanically-advanced solutions for spinal pathologies, launched its Stable-C cervical interbody fusion implants featuring integrated anchoring blades.

Global Minimally Invasive Spine Surgery Market Report Scope

Minimally invasive spine surgery (MISS) is a type of surgery performed on the spine's bones. This surgery generally uses smaller incisions than traditional surgery and often causes less harm to nearby muscles and other tissues. This minimally invasive surgery can lead to less pain and faster recovery after surgery.

The minimally invasive spine surgery market is segmented by product type (implants & instrumentation and biomaterials), application (fusion surgery and non-fusion surgery), treatment (lumbar disc herniation, thoracic disc herniation, spinal stenosis, degenerative spinal disease, and other treatments), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Implants & instrumentation |

| Biomaterials |

| Fusion Surgery |

| Non-fusion Surgery |

| Lumbar Disc Herniation |

| Thoracic Disc Herniation |

| Spinal Stenosis |

| Degenerative Spinal Disease |

| Other Treatments |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | GCC |

| South Africa | |

| Rest of Middle-East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Implants & instrumentation | |

| Biomaterials | ||

| By Application | Fusion Surgery | |

| Non-fusion Surgery | ||

| By Treatment | Lumbar Disc Herniation | |

| Thoracic Disc Herniation | ||

| Spinal Stenosis | ||

| Degenerative Spinal Disease | ||

| Other Treatments | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | GCC | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Global Minimally Invasive Spine Surgery Market size?

The Global Minimally Invasive Spine Surgery Market is projected to register a CAGR of 5.5% during the forecast period (2025-2030)

Who are the key players in Global Minimally Invasive Spine Surgery Market?

Medtronic, Johnson & Johnson (DePuy Synthes), Boston Scientific, Zimmer Biomet and Aesculap, Inc. are the major companies operating in the Global Minimally Invasive Spine Surgery Market.

Which is the fastest growing region in Global Minimally Invasive Spine Surgery Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Minimally Invasive Spine Surgery Market?

In 2025, the North America accounts for the largest market share in Global Minimally Invasive Spine Surgery Market.

What years does this Global Minimally Invasive Spine Surgery Market cover?

The report covers the Global Minimally Invasive Spine Surgery Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Global Minimally Invasive Spine Surgery Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: