Endovascular Aneurysm Repair Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

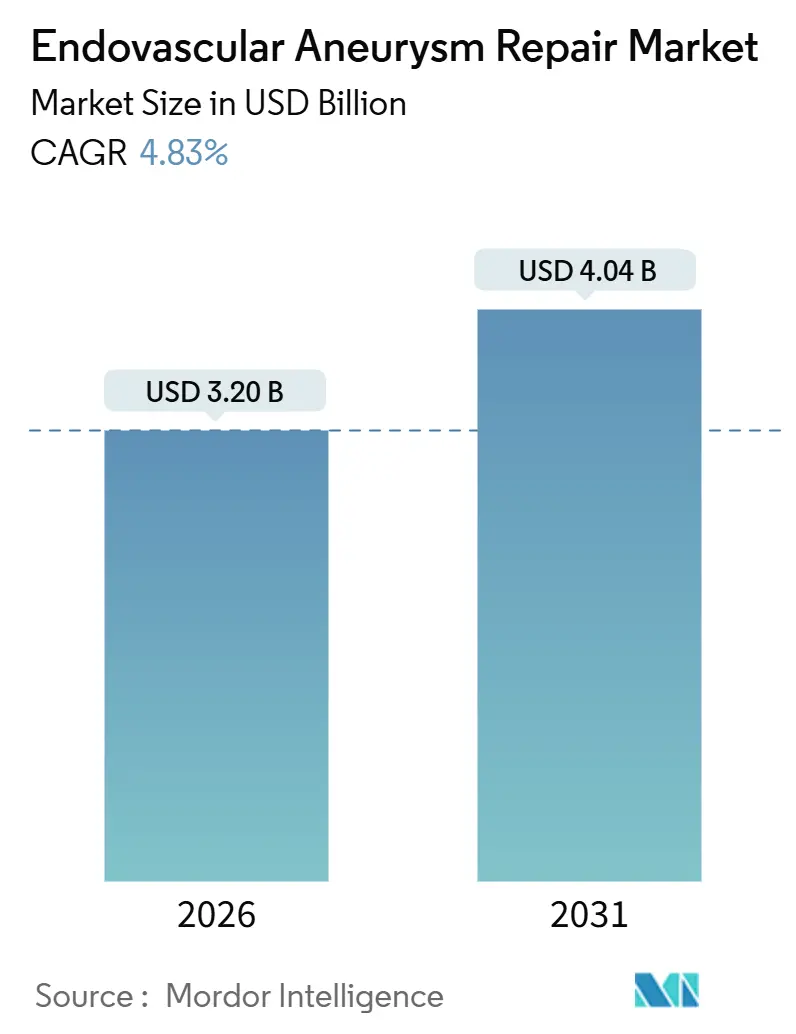

| Market Size (2026) | USD 3.20 Billion |

| Market Size (2031) | USD 4.04 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

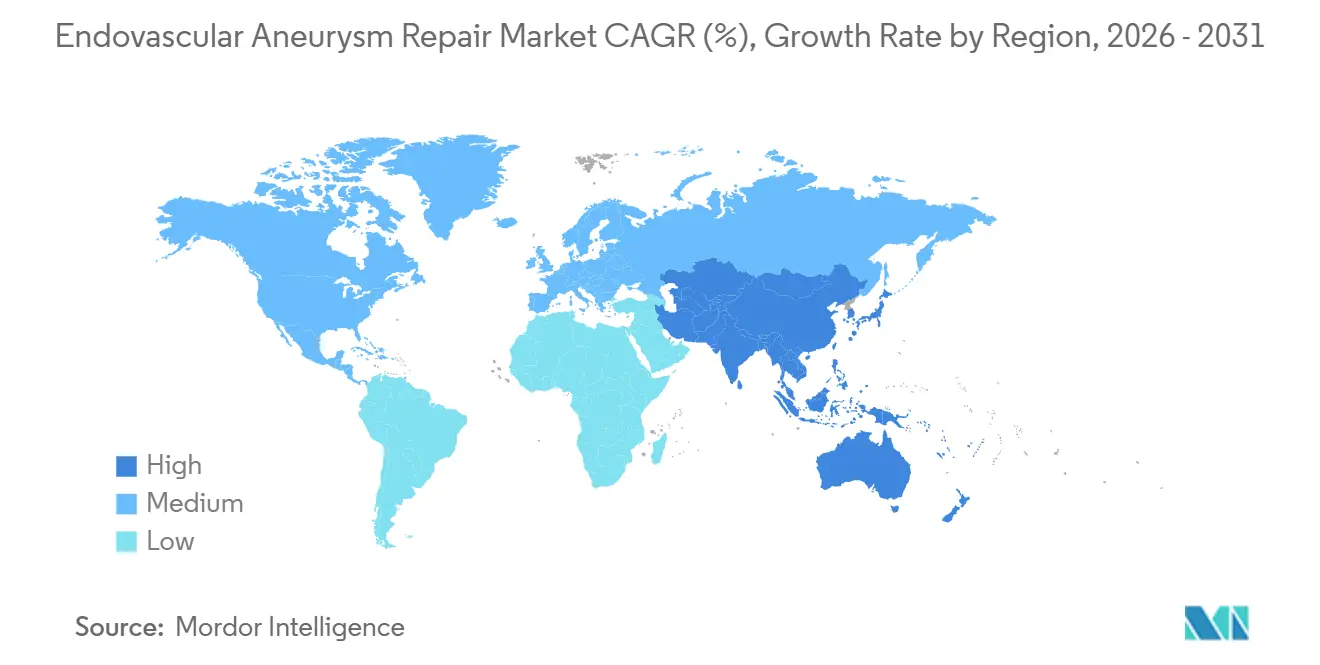

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endovascular Aneurysm Repair Market Analysis by Mordor Intelligence

The Endovascular Aneurysm Repair Market size is estimated at USD 3.20 billion in 2026, and is expected to reach USD 4.04 billion by 2031, at a CAGR of 4.83% during the forecast period (2026-2031).

Procedure growth remains strong, supported by the shift toward minimally invasive therapies, advancements in device conformability, and expanded outpatient capabilities, even as reimbursement levels stabilize in mature regions. The adoption of off-the-shelf branched and fenestrated grafts is increasing anatomic eligibility, while ultra-low-profile delivery systems are enabling access to previously excluded patient groups with challenging iliac anatomy. Competitive differentiation is driven by proprietary graft fabrics, streamlined delivery-catheter profiles, and integrated imaging support, which collectively reduce endoleak risks and enhance operating efficiency. Hospital capital investments remain focused on hybrid operating suites, while ambulatory surgical centers are capturing straightforward infrarenal cases, aided by payer incentives for same-day discharges. Concerns over long-term durability, including a 15-year reintervention probability exceeding 25%, are moderating aggressive market penetration strategies. However, these challenges create opportunities for manufacturers to leverage registry data to demonstrate reduced surveillance requirements and strengthen confidence in product performance.

Key Report Takeaways

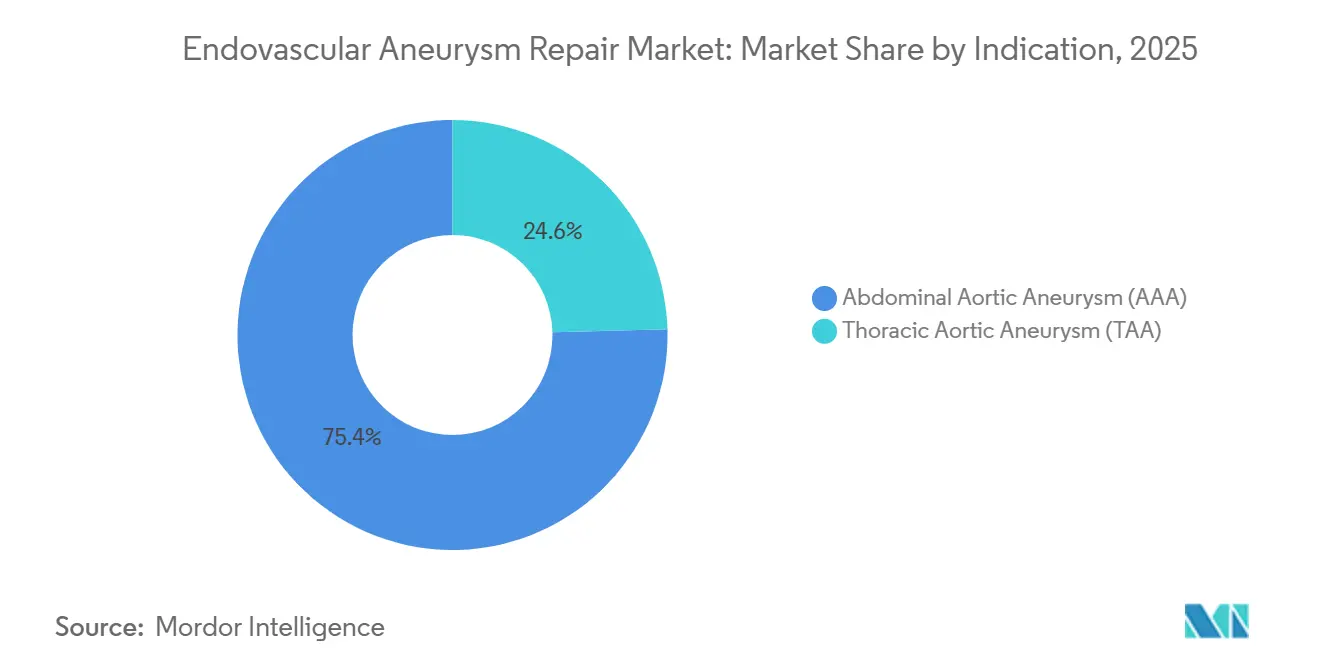

- By indication, abdominal aortic aneurysm led with 75.43% revenue share in 2025, while thoracic aortic aneurysm procedures are projected to grow at a 6.43% CAGR through 2031.

- By site, infrarenal cases accounted for 65.32% of the 2025 volume, while pararenal repairs are forecast to expand at a 7.11% CAGR to 2031.

- By anatomy, traditional profiles represented 60.65% of the 2025 case mix, while complex anatomies are advancing at a 6.23% CAGR through 2031.

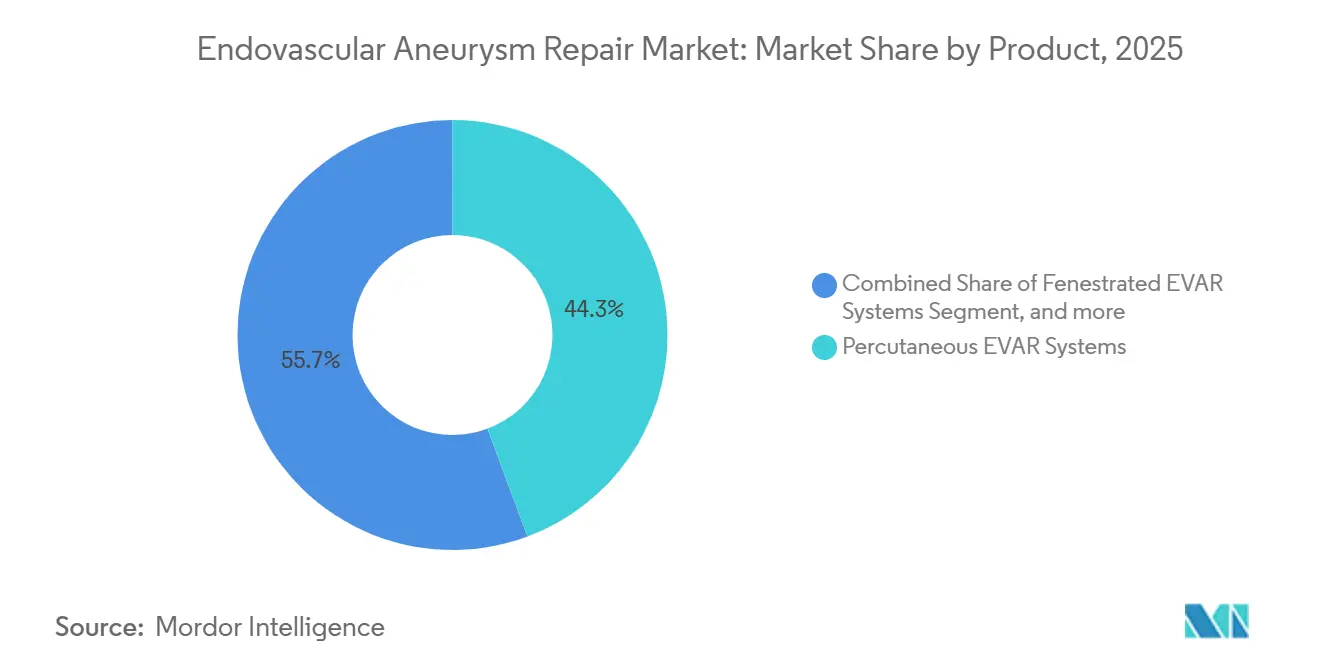

- By product, percutaneous delivery systems captured 44.32% revenue in 2025, while fenestrated systems are poised for 6.87% CAGR growth to 2031.

- By end user, hospitals held 62.13% spending in 2025, while ambulatory surgical centers are expanding at a 7.54% CAGR through 2031.

- By geography, North America commanded 43.12% global revenue in 2025, while Asia-Pacific is expected to post a 5.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Endovascular Aneurysm Repair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden of Aortic Aneurysm Disease | +1.2% | Global, with acute impact in aging North America and Europe | Medium term (2-4 years) |

| Shift Toward Minimally Invasive Vascular Interventions | +1.0% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Advancements in Stent-Graft Engineering and Materials | +0.9% | Global, led by North America and Europe regulatory approvals | Long term (≥ 4 years) |

| Expansion of Outpatient Endovascular Treatment Centers | +0.7% | North America, Western Europe | Medium term (2-4 years) |

| Favorable Reimbursement Policies in Developed Economies | +0.6% | North America, select European Union markets | Short term (≤ 2 years) |

| Healthcare Infrastructure Upscaling in Emerging Markets | +0.5% | Asia-Pacific core, spillover to Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Aortic Aneurysm Disease

Rising life expectancy and expanded abdominal imaging are lifting the diagnosed prevalence faster than declines in cardiovascular mortality, feeding a steady inflow of repair candidates. The Global Burden of Disease Study 2024 recorded an 8% rise in age-standardized abdominal aortic aneurysm prevalence between 2019 and 2024 in high-income regions[1]Institute for Health Metrics and Evaluation, “GBD 2024 Aortic Conditions,” healthdata.org. Screening programs in the United Kingdom and Scandinavia now identify aneurysms below the historical 5.5 cm threshold, creating a watchful-waiting cohort that matures into a cohort with interventional demand. China’s 2025 national survey found an undiagnosed abdominal aneurysm in 1.8% of men over 65, equal to roughly 3 million latent cases. These epidemiologic data underpin procedure stability even when per-case reimbursement stagnates. The endovascular aneurysm repair market, therefore, benefits from sheer patient volume growth rather than price escalation.

Shift Toward Minimally Invasive Vascular Interventions

Patient preference for shorter stays is accelerating the pivot from open surgery to catheter-based repair. Medicare claims showed that 78% of intact abdominal repairs were endovascular in 2024, versus 72% in 2020[2]Centers for Medicare & Medicaid Services, “National Summary of Inpatient Claim Statistics 2024,” cms.gov. Percutaneous closure devices eliminated the need for surgical cutdown in 85% of cases by 2025, reducing the median length of stay to 1.2 days. Society for Vascular Surgery guidelines published in 2025 formally endorsed outpatient repair for low-risk anatomy, codifying a practice that burgeoned during pandemic bed shortages. Device makers responded with 14- to 16-French delivery systems that widen access to older patients with calcified femoral arteries. Consequently, the endovascular aneurysm repair market is seeing rising procedural volume even amid flat overall aneurysm incidence curves.

Advancements in Stent-Graft Engineering and Materials

Polymer-covered grafts made from ultra-high-molecular-weight polyethylene showed 30% lower fatigue in bench tests than their polyester predecessors. Laser-cut scallops and conformable nitinol frameworks enable off-the-shelf fenestrated and branched options, reducing lead times from 6 weeks to under 2 days. The FDA’s January 2024 clearance of Gore’s EXCLUDER Thoracic Branch Endoprosthesis marked the first mass-produced branched device in the United States. Conformable neck-sealing technology lowered type-Ia endoleak rates from 8% to below 3% in registries, strengthening payer confidence. These engineering gains elevate technical success and fortify the long-term competitiveness of the endovascular aneurysm repair market.

Expansion of Outpatient Endovascular Treatment Centers

CMS added CPT 34701 to the ambulatory-surgery-center list in January 2024, reimbursing USD 8,200 per case compared with USD 14,500 in hospital outpatient departments. Private-equity-backed ASC chains opened 47 vascular-focused centers in 2025, each outfitted with fixed C-arms and rapid-recovery bays. Manufacturers now run mobile training units that bring simulation labs to community surgeons, lowering the credentialing hurdle. A multicenter trial published in 2024 documented no rise in 30-day complications for same-day discharge EVAR, reinforcing payer acceptance. Lower facility overhead and bundled device-closure contracts amplify margin potential, making ASCs a structurally advantaged node of the endovascular aneurysm repair market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Endovascular Procedures | -0.8% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Durability and Long-Term Surveillance Uncertainties | -0.6% | Global, particularly Europe with strict HTA requirements | Long term (≥ 4 years) |

| Procedure-Related Complications Such as Endoleaks | -0.4% | Global | Medium term (2-4 years) |

| Shortage of Skilled Endovascular Specialists | -0.5% | North America, rural Asia-Pacific, Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Endovascular Procedures

Device outlays account for up to 70% of the episode cost, straining budgets in the absence of comprehensive insurance coverage. A 2024 JAMA Surgery analysis pegged incremental cost per quality-adjusted life year above USD 75,000 in octogenarians with comorbidities, a level that exceeds willingness-to-pay thresholds in several EU systems[3]JAMA Network Editors, “Cost-Effectiveness of EVAR in Octogenarians,” jamanetwork.com. India’s national plan reimburses only USD 3,500, forcing patients to shoulder USD 8,000-12,000 for branded grafts. China split its market: imported devices remain 2.5 times as expensive as local equivalents, preserving a two-tier supply chain. Hospitals in lower-income settings often revert to open repair because total consumable costs are under USD 500. These affordability hurdles temper adoption rates and cap short-term growth of the endovascular aneurysm repair market.

Durability and Long-Term Surveillance Uncertainties

The U.K. EVAR-1 trial’s 15-year data showed equivalent aneurysm mortality between EVAR and open surgery, but triple the number of secondary interventions in the endovascular group. Lifelong CT or duplex surveillance adds USD 800 annually, layering costs on top of the initial premium. European payers now tie reimbursement to registry participation, delaying payment and adding administrative burdens. Radiation exposure exceeding 100 mSv over a decade also raises patient safety concerns. Younger patients face the prospect of multiple reinterventions, weakening the perceived value of the endovascular aneurysm repair market for that cohort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: AAA Dominance Persists Amid TAA Acceleration

Abdominal repairs accounted for 75.43% of 2025 revenue, reflecting decades of device iteration, standardized sizing algorithms, and broad surgeon familiarity. Thoracic interventions, though smaller, are advancing at a 6.43% CAGR as branched and fenestrated grafts unlock arch and dissection cases that previously defaulted to open repair. The U.S. FDA’s April 2025 approval of Gore’s TAG Thoracic Branch Endoprosthesis gave operators a ready solution for zone-0 and zone-1 disease, reducing planning time and stroke risk. Expanded trauma indications and dissection-specific devices further energize thoracic growth. Consequently, the endovascular aneurysm repair market is gradually rebalancing toward more complex thoracic volumes even while abdominal repairs remain the procedural bedrock.

Procedure complexity shapes revenue intensity. AAA cases, typically performed in community hospitals, rely on off-the-shelf infrarenal grafts with commodity-level pricing. TAA procedures are concentrated in academic centers with hybrid rooms and advanced imaging, which command higher average selling prices. Device miniaturization is beginning to push thoracic work into select ambulatory settings, mirroring the pattern of abdominal migration. As these technological and organizational shifts converge, the endovascular aneurysm repair market size attributable to thoracic pathology is set to rise faster than the traditional abdominal segment, driving mix-driven revenue uplift over the forecast horizon.

By Site: Infrarenal Procedures Lead, Pararenal Cases Surge

Infrarenal aneurysms accounted for 65.32% of the 2025 case volume, owing to favorable neck anatomy that suits standard grafts and streamlined workflows. Pararenal repairs, however, are forecast to grow at a 7.11% CAGR to 2031 as off-the-shelf fenestrated platforms eliminate lengthy customization delays. Cook Medical’s Zenith Fenestrated graft reached U.S. hospitals in 2025, trimming lead times from six weeks to mere days. Post-deployment data show 94% technical success, bringing outcomes closer to open surgery benchmarks.

Volume migration is also driven by chimney and snorkel adjuncts that enable community surgeons to tackle short-neck lesions without resorting to open repair. Payers increasingly accept fenestrated pricing, given reductions in ICU stay and transfusion rates. As a result, the endovascular aneurysm repair market for pararenal anatomy is likely to gain share within the broader infrarenal-dominant landscape, reshaping stocking priorities for hospital supply chains.

By Anatomy: Complex Repairs Gain Traction Through Modular Innovation

Traditional anatomy still made up 60.65% of 2025 cases, yet complex configurations are expanding at a 6.23% CAGR as modular graft designs and imaging fusion techniques improve success rates. Gore’s EXCLUDER Conformable AAA device, cleared for high-angle necks in 2024, achieved 96% freedom from aneurysm-related mortality at one year among hostile neck patients. Variable-stiffness nitinol lets the graft adapt to conical morphology, slashing type-Ia endoleaks below 4%.

Physician-modified grafts remain an interim solution for urgent cases pending formal branched approvals. Societal guidelines now call for standardized reporting of such modifications to inform future device development. Imaging innovation, particularly CT-fluoroscopy fusion, reduces contrast load and shortens procedure time. As operator learning curves flatten, the endovascular aneurysm repair market share linked with complex anatomy is set to climb steadily, albeit from a smaller base than standard neck repairs.

By Product: Percutaneous Systems Command Share, Fenestrated Devices Accelerate

Percutaneous systems held 44.32% revenue in 2025, thanks to sutureless closure devices that facilitate same-day discharge. Medicare’s outpatient list expansion in January 2024 generated an immediate reimbursement tailwind. Thoracic grafts mirror abdominal product evolution but retain higher average selling prices because of longer lengths and branch options. Fenestrated systems, though niche, are forecast to grow at a 6.87% CAGR and command USD 25,000-35,000 per unit, more than double the price of standard infrarenal grafts.

Manufacturers race to lower sheath profiles while embedding pre-loaded guidewires to cut cath-lab time. Adjunct tools such as iliac-branch extensions and embolic coils add incremental revenue per case. Within this dynamic, the endovascular aneurysm repair market size tied to premium fenestrated offerings is set to outpace the broader product pool, boosting blended average selling prices despite commoditization pressure in infrarenal lines.

By End User: Hospitals Retain Majority, ASCs Capture Growth

Hospitals accounted for 62.13% of global end-user spend in 2025, driven by hybrid suites, intensive care support, and multidisciplinary teams. Complex thoracic or pararenal anatomy typically mandates in-house vascular or cardiothoracic backup. Nevertheless, ambulatory surgical centers are projected for 7.54% CAGR growth, buoyed by lower facility fees and payer push toward cost efficiency. Straightforward infrarenal repairs with ASA class I–II patients transition smoothly to the outpatient model.

Private-equity capital continues to fund vessel-specific ASC rollouts that pair imaging with procedure and surveillance under one roof. Device companies deploy mobile simulation trailers to certify ASC physicians without travel downtime. As health systems rebalance care sites, the endovascular aneurysm repair market share held by ASCs will expand, though hospitals will remain indispensable for high-acuity care and training.

Geography Analysis

North America retained 43.12% of 2025 revenue, underpinned by Medicare stability, dense specialist concentration, and a robust registry ecosystem that validates device safety. CMS approval of percutaneous closure in ASCs catalyzed outpatient migration, increasing overall procedural accessibility even as hospital margins compressed. Canada lags because single-payer budgets limit hybrid-suite throughput, leading to longer wait times that skew ruptured aneurysm repairs toward EVAR to mitigate mortality.

Europe contributes a sizable but heterogeneous slice of the endovascular aneurysm repair market. Germany’s DRG incentives drive EVAR penetration above 80% for elective abdominal cases, whereas the United Kingdom balances NICE endorsement of fenestrated repair with NHS budget caps that confine complex procedures to designated centers. France’s 12% device price cut enacted in 2025 pushed manufacturers into volume discounts. Southern and Eastern European uptake remains constrained by limited capital expenditure, but EU Medical Device Regulation harmonization maintains consistent safety standards, reinforcing confidence in imported grafts.

Asia-Pacific is the fastest-growing region at 5.54% CAGR, anchored by China, India, and Japan. China’s bulk-purchase program closed price gaps for domestic devices, opening tier-2 cities and stimulating training initiatives. India’s metro-based private chains invest in hybrid rooms to court medical tourists, while Japan leans on universal coverage but negotiates aggressive price concessions. Australia and South Korea follow mature-market patterns but at smaller volumes. Collectively, emerging economies rely on infrastructure gains and declining device prices to unlock deferred demand, ensuring that the endovascular aneurysm repair market expands beyond its traditional strongholds.

Competitive Landscape

Medtronic, W. L. Gore, and Cook Medical commanded roughly 55%-60% of 2025 revenue through exclusive contracts, comprehensive training programs, and portfolios that span infrarenal, thoracic, and fenestrated segments. Gore’s ePTFE graft material and conformable stent design gained high-angle neck approval in 2024, solidifying its grip on complex anatomy. Medtronic leverages a pre-loaded catheter system that shortens deployment time, appealing to community hospitals migrating from open surgery. Cook’s dissection-specific platform addresses unmet needs in false-lumen hemodynamics not addressed by conventional thoracic grafts.

Second-tier competitors pursue niche angles. Endologix employs polymer sealing to serve short-neck patients, whereas Bolton Medical targets price-sensitive markets with value grafts. Patent filings—Gore registered 14 new aortic device patents in 2025—underscore ongoing R&D investment despite market maturity. Partnerships with imaging firms, such as Medtronic’s work with Siemens Healthineers, integrate fusion guidance into the procedural workflow, reinforcing brand stickiness. Regulatory acceleration via FDA breakthrough designation beckons future entrants specializing in endoleak-sealing polymers or bioresorbable scaffolds, although no such products are yet commercialized.

Pricing pressure intensifies in bulk-purchase regions like China, where domestic players such as MicroPort’s Endovastec leverage cost leadership to win tenders. Western incumbents respond with localized assembly and extended warranty terms. Training remains a competitive moat: companies that can credential new surgeons quickly secure graft pull-through. As product parity grows, service, imaging integration, and cost-of-ownership models decide contract renewals, making the non-device ecosystem integral to the endovascular aneurysm repair market.

Endovascular Aneurysm Repair Industry Leaders

Medtronic plc

W. L. Gore & Associates

Cook Medical LLC

Terumo Corporation

Endologix LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Terumo Aortic launched the Fenestrated TREO pivotal IDE study in the United States to evaluate its new endovascular device. The study aims to support the device's approval for complex aortic aneurysm repairs. This development marks a significant step forward in expanding treatment options for patients with challenging aortic conditions.

- November 2025: ViTAA Medical received the US Food and Drug Administration (FDA) approval for the 510(k) clearance for the AiORTA Plan, which the company describes as a “fully automated, hyper-precise aortic surgery planning solution”.

- October 2025: Medtronic announced that the FDA has approved new labeling for the company’s Endurant stent graft system for use in the treatment of ruptured abdominal aortic aneurysms (rAAA), removing the previous rAAA treatment warning.

Global Endovascular Aneurysm Repair Market Report Scope

As per the scope of the report, endovascular aneurysm repair (EVAR) is a minimally invasive surgical procedure used to treat abdominal aortic aneurysms by inserting a stent graft through the blood vessels to reinforce the weakened artery wall. It reduces the risk of rupture and avoids the need for open surgery. The procedure is performed under imaging guidance and typically offers a quicker recovery time.

The Endovascular Aneurysm Repair Market is Segmented by Indication (Abdominal Aortic Aneurysm and Thoracic Aortic Aneurysm), Site (Infrarenal and Pararenal), Anatomy (Traditional and Complex), Product (Percutaneous EVAR Systems, Fenestrated EVAR Systems, Thoracic Aortic Stent-Grafts, and Adjunct Devices), End User (Hospitals, Ambulatory Surgical Centers, and Specialty Vascular Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Abdominal Aortic Aneurysm (AAA) |

| Thoracic Aortic Aneurysm (TAA) |

| Infrarenal |

| Pararenal |

| Traditional |

| Complex |

| Percutaneous EVAR Systems |

| Fenestrated EVAR Systems |

| Thoracic Aortic Stent-Grafts |

| Adjunct / Other Devices |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Vascular Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Indication | Abdominal Aortic Aneurysm (AAA) | |

| Thoracic Aortic Aneurysm (TAA) | ||

| By Site | Infrarenal | |

| Pararenal | ||

| By Anatomy | Traditional | |

| Complex | ||

| By Product | Percutaneous EVAR Systems | |

| Fenestrated EVAR Systems | ||

| Thoracic Aortic Stent-Grafts | ||

| Adjunct / Other Devices | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Vascular Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current value of the endovascular aneurysm repair market?

The endovascular aneurysm repair market size reached USD 3.20 billion in 2026 and is projected to grow to USD 4.04 billion by 2031.

Which anatomic segment is expanding fastest within this therapy area?

Pararenal repairs are forecast to grow at a 7.11% CAGR through 2031 as off-the-shelf fenestrated grafts become widely available.

How quickly are thoracic endovascular procedures growing?

Thoracic aortic aneurysm interventions are projected to expand at a 6.43% CAGR between 2026 and 2031.

What share of procedures will occur in ambulatory surgical centers?

Ambulatory surgical centers are expected to absorb a growing portion of infrarenal cases, with end-user spending rising at a 7.54% CAGR through 2031.

Which companies dominate global revenue?

Medtronic, W. L. Gore, and Cook Medical together accounted for 55%-60% of 2025 worldwide sales.

What is the biggest cost-related barrier in emerging markets?

High graft prices, which can represent up to 70% of total procedure cost, limit access where insurance coverage is sparse.

Page last updated on: