Lung Cancer Surgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.63 Billion |

| Market Size (2031) | USD 8.06 Billion |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

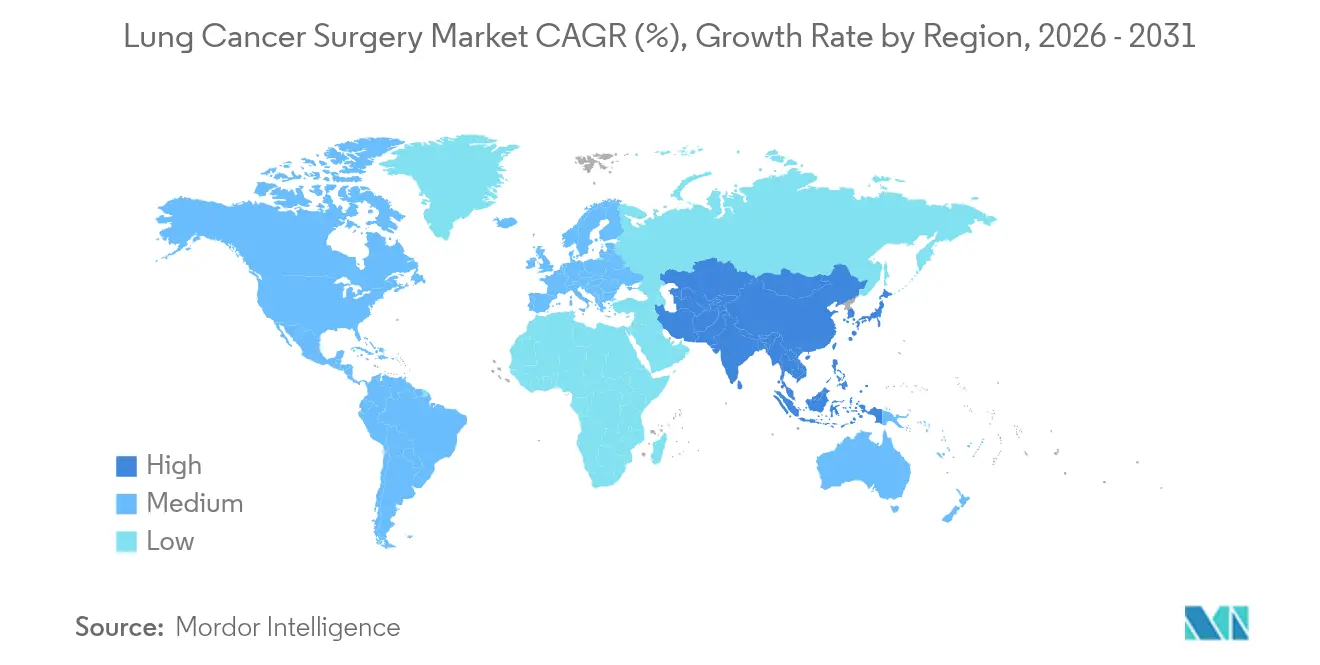

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

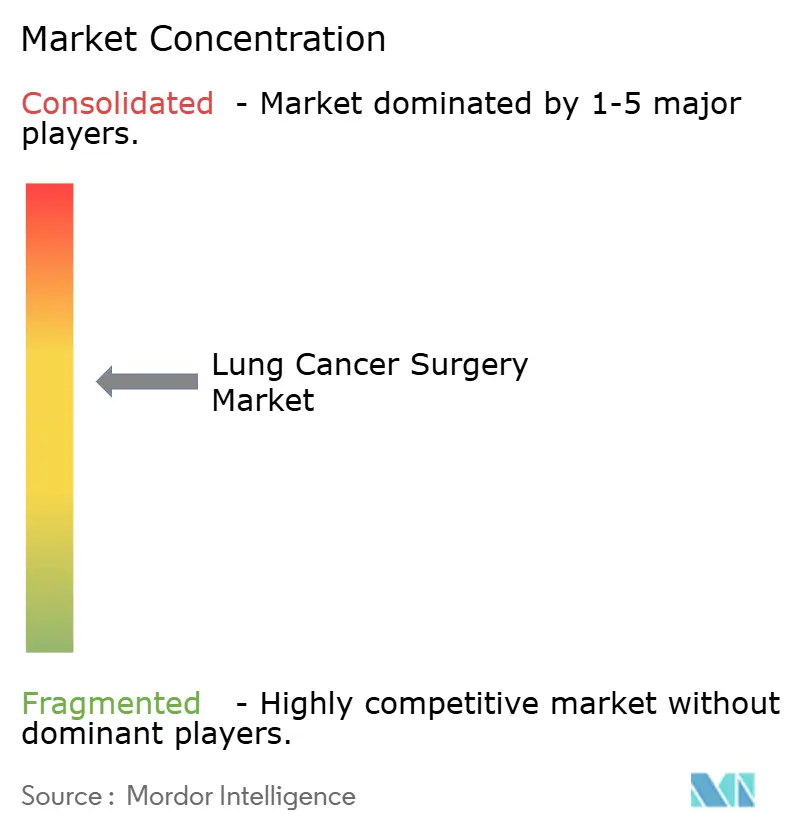

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lung Cancer Surgery Market Analysis by Mordor Intelligence

The Lung Cancer Surgery Market size was valued at USD 6.38 billion in 2025 and estimated to grow from USD 6.63 billion in 2026 to reach USD 8.06 billion by 2031, at a CAGR of 3.98% during the forecast period (2026-2031). Competitive intensity is now shaped less by sheer procedure volumes and more by the sophistication of robotic platforms, advanced stapling systems, and AI-enabled imaging that compress operating times while sustaining oncological precision. Hospitals expand capital budgets for integrated robotic suites even as ambulatory surgical centers adopt lighter single-port systems that fit outpatient economics. Early-stage lung cancer detection through low-dose CT screening funnels an expanding cohort of surgical candidates, yet workforce shortages spur demand for automation that lets surgeons handle higher throughput without compromising lymph-node harvests. At the same time, reimbursement frameworks in North America and parts of Europe reward quality-of-life metrics, incentivizing providers to migrate from open thoracotomy to video-assisted and robotic approaches that shorten length of stay and reduce conversion rates.

Key Report Takeaways

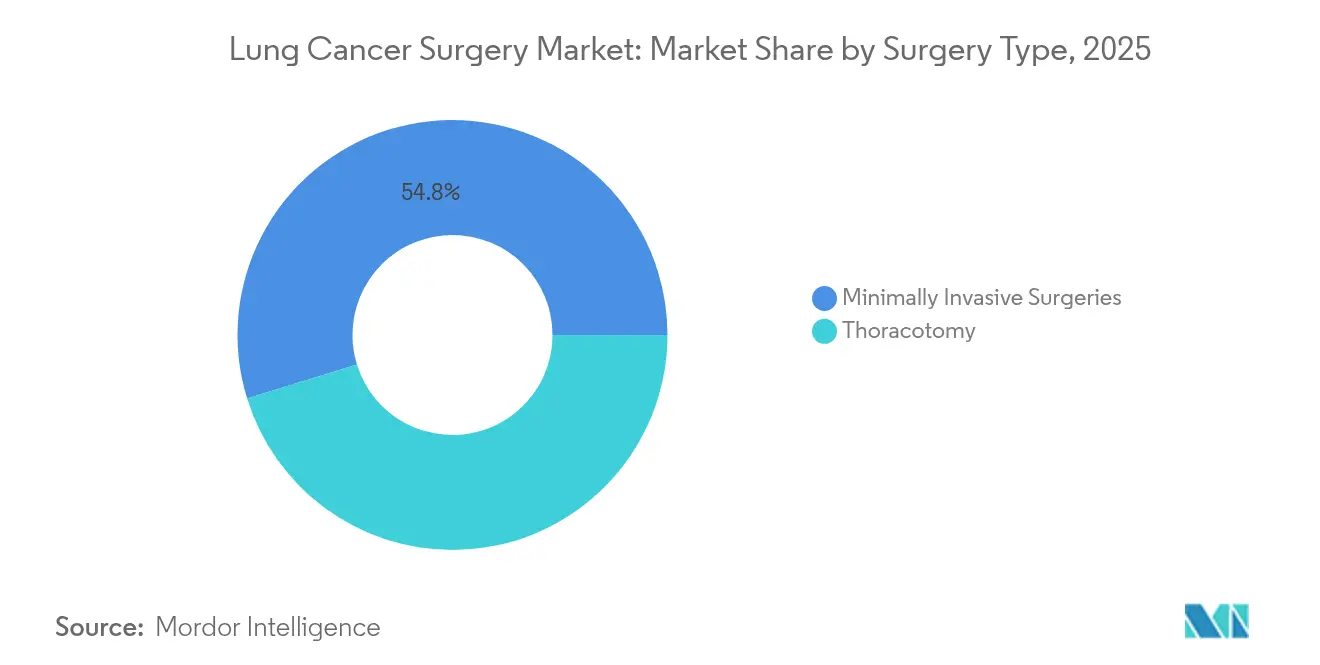

- By surgery type, minimally invasive procedures accounted for 54.78% of the lung cancer surgery market share in 2025, growing at a 5.05% CAGR through 2031.

- By product, surgical devices led with a 59.05% revenue share in 2025; monitoring devices recorded the fastest growth at a 5.74% CAGR from 2025 to 2031.

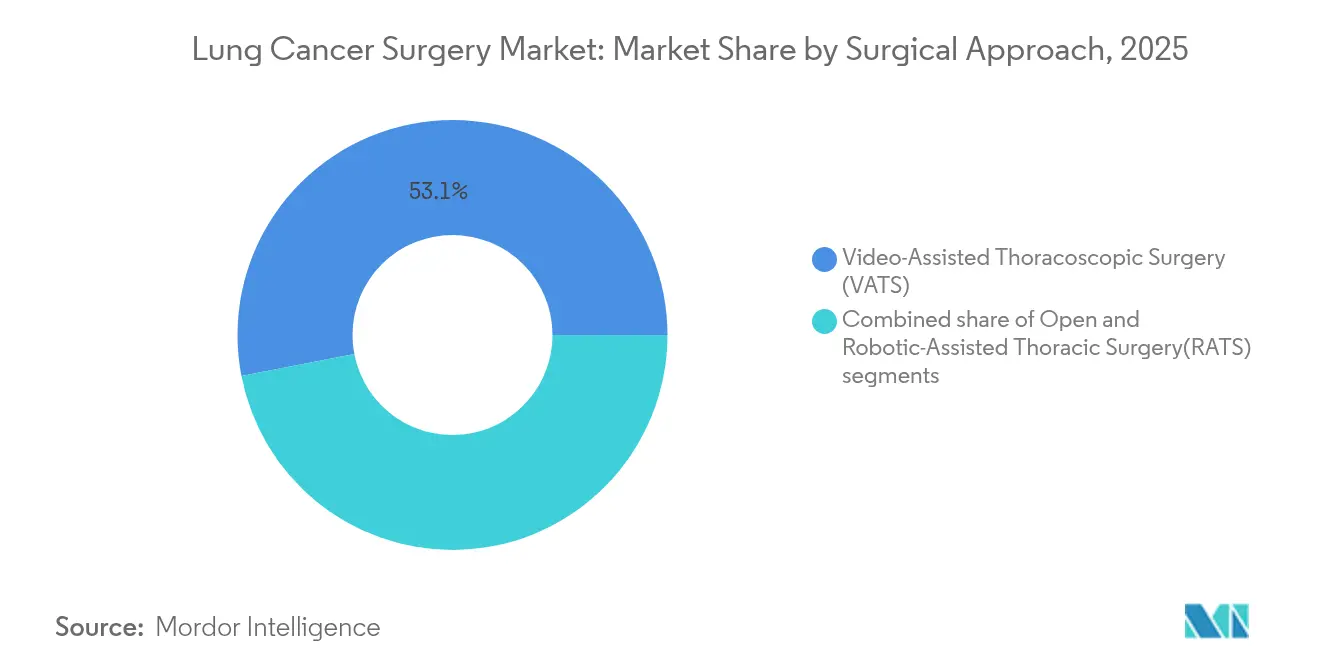

- By surgical approach, video-assisted thoracoscopic surgery accounted for a 53.05% share of the lung cancer surgery market size in 2025, whereas robotic-assisted thoracic surgery is projected to post the highest 5.39% CAGR from 2025 to 2031.

- By end user, hospitals commanded a 62.10% share in 2025; ambulatory surgical centers advanced at a 4.82% CAGR through 2031.

- By geography, North America held 36.10% revenue share in 2025, while the Asia Pacific is projected to expand at a 5.59% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lung Cancer Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of lung cancer | +1.2% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Technological advances in minimally-invasive and robotic surgery | +1.5% | North America & EU leading, APAC catching up | Medium term (2-4 years) |

| Rising air pollution and occupational exposures | +0.8% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Expanding reimbursement for robotic lobectomy | +0.9% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Integration of intra-operative AI imaging & navigation | +0.7% | North America & EU, selective APAC markets | Short term (≤ 2 years) |

| Surge in early-stage detection via low-dose CT screening | +1.1% | Global, with fastest adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing burden of lung cancer

Epidemiological projections indicate a 70% rise in surgical cases by 2035, driven by aging populations and escalating air-pollution exposure in emerging economies. Screening programs in Taiwan already detect 85% of cancers at stage 0–1, sharply increasing operable volumes while lowering per-case complexity. Device makers respond by prioritizing workflow efficiency over premium pricing curves. The epidemiological transition from late-stage palliative care to early-stage curative surgery fundamentally alters device utilization patterns and reimbursement models.

Technological advances in minimally-invasive and robotic surgery

Hospitals installed 147 da Vinci 5 systems in Q1 2025, signifying strategic commitment to articulated instruments and AI-driven analytics that improve lymph-node harvests from 5.6 to 7.5 stations per procedure. Partnerships such as Johnson & Johnson-NVIDIA focus on real-time algorithmic guidance, underscoring a shift toward software as the key differentiator.

Rising air pollution and occupational exposures

PM2.5 exposure increases mortality risk by 44% among lung-cancer patients, concentrating demand in high-pollution APAC corridors that must scale thoracic capacity quickly.[1]Source: Bongkotmas Kosanpipat et al., “Impact of PM2.5 Exposure on Mortality and Tumor Recurrence in Resectable NSCLC,” Sci Rep, doi.org Occupational hazards such as asbestos further regionalize device uptake in heavy-industry zones. Climate change exacerbates these trends, with wildfire-related air quality deterioration increasing lung cancer surgical complexity and post-operative complications.

Expanding reimbursement for robotic lobectomy

HCPCS code S2900 standardizes U.S. billing for robotic supplies, eliminating a major uncertainty barrier and supporting steady system purchases. Cost-utility studies show 73% five-year survival for robotic resection, helping justify capital outlays despite a 36% cost premium over SBRT. The reimbursement landscape shift enables hospitals to invest in robotic platforms while maintaining financial viability, though the lack of additional reimbursement beyond standard surgical codes constrains margin expansion. Insurance coverage expansion for eligible patients under the Affordable Care Act and Medicare creates a broader addressable market for robotic procedures, though prior authorization requirements may limit utilization growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Effectiveness of non-surgical alternatives (SBRT, targeted therapies) | -0.8% | Global, with highest impact in developed markets | Medium term (2-4 years) |

| Workforce shortage of thoracic surgeons | -1.1% | Global, most acute in North America and EU | Long term (≥ 4 years) |

| High capital cost of robotic systems and disposables | -0.6% | APAC and emerging markets primarily | Medium term (2-4 years) |

| Regulatory delays for novel energy devices | -0.4% | Global, with varying impact by regulatory jurisdiction | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Effectiveness of non-surgical alternatives (SBRT, targeted therapies)

SBRT delivers ≥90% local control in inoperable patients and costs USD 8,933 per course versus USD 12,197 for robotic resection, shifting treatment algorithms in frail cohorts. Novel devices must therefore present clear survival or quality-of-life edges to defend cap-ex budgets. The therapeutic landscape shift toward precision medicine and targeted therapies reduces the addressable surgical population, particularly for patients with specific molecular markers who achieve superior outcomes through systemic treatments.

Workforce shortage of thoracic surgeons

A projected 21% supply drop juxtaposed threatens capacity even in advanced markets, pushing hospitals toward automation that extends each surgeon’s productive hours. Training pipeline constraints exacerbate the shortage, with fewer residents entering thoracic surgery despite growing case volumes, creating a structural imbalance that limits device market expansion regardless of technological advancement. Geographic disparities in surgeon distribution create access barriers that prevent optimal device utilization, particularly in rural and underserved markets where surgical expertise concentration limits advanced technology adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Surgery Type: Minimally Invasive Procedures Drive Market Evolution

Minimally invasive techniques captured 54.78% lung cancer surgery market share in 2025 and are growing at 5.05% through 2031, outpacing thoracotomy as payers reward faster discharge and lower complication rates. The shift toward single-port VATS and uniportal robotic approaches trims average operative time to 88 minutes, nearly 28% faster than legacy multi-port procedures. Thoracotomy retains a foothold for extensive resections and complex hilum anatomy, yet its flatter adoption curve signals a limited role outside specialty centers.

Surgeons value minimally invasive workflows for reducing postoperative pneumonia and atrial arrhythmia incidence, translating to shorter 4-day median stays versus 7 days for open surgery. Single-port robotic trials exceeding 100 thoracic cases confirm feasibility for sleeve resections and segmentectomies, signalling a broadening addressable pool once training ecosystems mature.

By Product: Surgical Devices Dominate While Monitoring Accelerates

Surgical devices represented 59.05% revenue in 2025, reflecting their indispensable role in tissue dissection and stapling; however, monitoring devices log the quickest 5.74% CAGR as AI engines tether imaging to operative consoles in real time. Olympus' BF-P190 bronchoscope, equipped with a 2.2 mm channel, exemplifies hardware advances underpinning procedural agility.

Siemens’ AI-Rad Companion positions monitoring gear as data generators for continuous surgical learning, nudging hospitals to bundle analytics subscriptions with capital purchases. Such hybrid revenue models solidify vendor lock-in while supporting device upgrades on software cycles rather than hardware depreciation schedules.

By Surgical Approach: VATS Leadership Challenged by RATS Innovation

Video-assisted thoracoscopic surgery held 53.05% of the lung cancer surgery market size in 2025, capitalizing on widespread surgeon proficiency and lower capital thresholds. Robotic-assisted thoracic surgery, increasing at a 5.39% CAGR, distinguishes itself through 3D optics and wristed instruments that slash conversion rates to 6.3% compared with 13.1% for VATS.

Despite an average USD 4,700 per-patient cost premium, RATS offsets financial drag by trimming average length of stay to 4 days, saving bed-day expenses and enhancing throughput. Continued reimbursement support and fellowship-level training pipelines foreshadow a gradual share shift toward robotics in high-volume centers through 2030. The surgical approach evolution suggests that RATS will capture increasing market share as reimbursement frameworks adapt and surgeon training programs expand robotic competency.

By End User: Hospitals Anchor Market While ASCs Gain Momentum

Hospitals controlled 62.10% demand in 2025 owing to high-acuity infrastructure and ICU backup that complex lobectomies require. Nonetheless, ambulatory surgical centers, advancing 4.82% annually, ride miniaturized robotic carts that fit ORs with lower ceiling heights and simplified draping protocols, reducing setup times to 10 minutes.

Specialty cancer institutes occupy a sweet spot where concentrated caseloads justify enterprise-wide AI platforms integrating pathology, imaging and operative archives, tightening feedback loops for precision oncology programs. Ambulatory surgical centers benefit from lower overhead costs and streamlined patient flow, enabling competitive pricing for appropriate surgical candidates while maintaining quality outcomes. The end-user landscape evolution suggests that technological advancement will continue expanding the range of procedures suitable for outpatient settings, driving market share redistribution toward lower-cost care environments.

Geography Analysis

North America’s leadership stems from harmonized reimbursement and rapid technology clearance under the FDA's 510(k) route, allowing for the continuous infusion of AI-guided imaging and next-generation stapling systems. Intuitive Surgical placed 367 systems in Q1 2025 in the U.S., reinforcing an installed base that already executed 2.63 million procedures in 2024.

Europe sustains stable uptake via MDR-aligned assessments that stress cost-effectiveness; Hungary’s multicenter LDCT projects show pathways for member states to funnel early-stage cases into surgery, maintaining a predictable capital-purchase cadence. Simultaneously, CE-marked innovations such as Optune Lua widen therapeutic alternatives, compelling surgeons to demonstrate superiority on survival and quality-of-life endpoints.

Asia Pacific’s lung cancer surgery market is propelled by urban pollution spikes and government-funded insurance expansion that subsidizes minimally invasive procedures in tier-1 and tier-2 cities. AI-enabled diagnosis projects in China exemplify leapfrogging strategies that integrate deep-learning triage into routine screening, potentially shortening pathways from detection to resection.

Competitive Landscape

The lung cancer surgery market features moderate fragmentation. Intuitive Surgical retains a robust moat in multi-port robotics, but software-centric challengers coalesce around AI navigation layers. Johnson & Johnson’s NVIDIA alliance aims to package predictive analytics with hardware, shifting value from instruments to data stewardship. Siemens Healthineers counters with automated C-arm imaging that halves fluoroscopy time, underscoring cross-modal competition where imaging vendors now target intra-operative space.

White-space exists in outpatient robotics, where compact carts priced below USD 800,000 appeal to ASCs that previously balked at multimillion-dollar platforms. Body Vision Medical’s LungVision overlays AI-driven fluoroscopy onto existing C-arms, enabling facilities to add navigation capabilities without the need for full-scale robotic purchases. Patent activity is gravitating toward semi-autonomous suturing and stapling, portending future regulatory debates over surgeon oversight thresholds.

Strategic moves in 2024–2025 include Stryker joining the IRCAD network to bolster robotic training pipelines and Lexington Medical introducing a next-gen stapler portfolio aimed at improving staple line integrity in dense emphysematous lung tissue. Increasingly, vendors differentiate via bundled service contracts covering simulation, proctorship and AI analytics rather than standalone hardware features.

Lung Cancer Surgery Industry Leaders

Accuray Incorporated

Olympus Corporation

Siemens Healthineers AG

Johnson & Johnson (Ethicon)

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Johnson & Johnson MedTech partnered with Qure.ai to roll out AI-led pulmonary-nodule clinics across India.

- April 2025: Baptist Health-Fort Smith deployed the Ion robotic bronchoscopy system for earlier lung-cancer diagnosis.

- December 2024: Apollo Cancer Centre launched the “LungLife” LDCT screening program across India.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence frames the lung cancer surgery devices market as the total annual revenue generated from instruments and systems that excise, visualize, or monitor malignant lung tissue during curative procedures. All open thoracotomy, video-assisted thoracoscopic (VATS), and robotic-assisted thoracic surgery (RATS) set-ups, plus their single-use accessories, are included, while pharmaceutical therapeutics, post-operative implants, and diagnostic imaging equipment remain outside scope.

Scope exclusion: Non-oncology thoracic devices and palliative ablation kits are specifically left out.

Segmentation Overview

- By Surgery Type

- Thoracotomy

- Lobectomy

- Sleeve Resection

- Segmentectomy

- Pneumonectomy

- Minimally Invasive Surgeries

- Thoracotomy

- By Product

- Surgical Devices

- Monitoring Devices

- By Surgical Approach

- Open

- Video-Assisted Thoracoscopic Surgery (VATS)

- Robotic-Assisted Thoracic Surgery (RATS)

- By End User

- Hospitals

- Specialty Cancer Centers

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We ran structured interviews with thoracic surgeons, OR procurement heads, and regional distributors across North America, Europe, and Asia-Pacific. These conversations validated prevalence-to-procedure ratios, unpacked ASP variation by care setting, and stress-tested our forecast assumptions.

Desk Research

Our analysts began with peer-reviewed epidemiology from sources such as the World Health Organization, GLOBOCAN, and national cancer registries, then paired those numbers with procedure volumes published by agencies like CMS and Eurostat. Trade associations for minimally invasive surgery, customs shipment data, and company 10-Ks supplied unit flows and average selling prices. Where granularity was needed, we tapped paid data tools, D&B Hoovers for company revenue splits and Dow Jones Factiva for transaction trends. This is not an exhaustive list; dozens of additional open databases, academic papers, and regulatory filings informed the evidence pool.

Market-Sizing & Forecasting

A top-down construct converts incident early-stage lung cancer cases into eligible surgical demand, adjusted for staging mix and intervention rates. Select bottom-up checks, supplier revenue roll-ups and sampled ASP × volume math, calibrate the totals. Key variables include national screening uptake, surgeon workforce density, robotic system installed base, reimbursement changes, disposable-to-capital ratio shifts, and learning-curve linked utilization. Multivariate regression against those drivers feeds a five-year ARIMA forecast, and gaps in bottom-up granularity are bridged with interpolation from analogous procedure cohorts.

Data Validation & Update Cycle

Outputs pass a two-level analyst review, anomaly flags trigger re-checks with respondents, and variance versus external benchmarks must narrow below set thresholds before sign-off. Reports refresh annually; any regulatory approval or recall that materially alters volumes sparks an interim update so clients always see the latest view.

Why Our Lung Cancer Surgery Devices Baseline Commands Confidence

Published numbers often diverge because firms pick different device mixes, assume varied robotic penetration, or freeze exchange rates at separate points.

Key gap drivers here include: 1) Mordor's device-only scope versus others folding in imaging consoles; 2) our moderate adoption curve for RATS, while some studies presume universal uptake; 3) annual refresh cadence that irons out currency swings which inflate or deflate rivals' estimates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.38 B (2025) | Mordor Intelligence | - |

| USD 6.61 B (2025) | Global Consultancy A | Broader inclusion of adjunct thoracic oncology equipment and optimistic robotic penetration rates |

| USD 6.22 B (2024) | Trade Journal B | Straight-line incidence growth without cross-checking procedure volumes; limited Asia data |

These comparisons show that, by centering on clearly defined devices, triangulating volumes with field interviews, and updating models every year, Mordor Intelligence delivers a balanced baseline clients can replicate and trust.

Key Questions Answered in the Report

What is the current size of the lung cancer surgery market?

The market stands at USD 6.63 billion in 2026 and is projected to climb to USD 8.06 billion by 2031.

What compound annual growth rate (CAGR) is expected for the market through 2031?

Mordor Intelligence forecasts a steady 3.98% CAGR for the period 2026-2031.

Which surgical approach currently commands the largest share?

Video-assisted thoracoscopic surgery (VATS) leads with 53.05% share, although robotic-assisted procedures are gaining ground fastest.

Which region is projected to grow the quickest?

Asia Pacific is set to expand at a 5.59% CAGR, driven by rapid screening adoption and healthcare infrastructure upgrades.

What role do minimally invasive techniques play in market growth?

Minimally invasive surgeries already hold 54.78% market share and are advancing at 5.05% CAGR thanks to shorter recovery times and lower complication rates.

How are new technologies shaping competitive dynamics?

AI-enabled imaging, real-time navigation and compact robotics are shifting competition from hardware alone to integrated software-plus-service ecosystems, rewarding vendors that combine precision with workflow efficiency.

Page last updated on: