Therapeutic Drug Monitoring Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

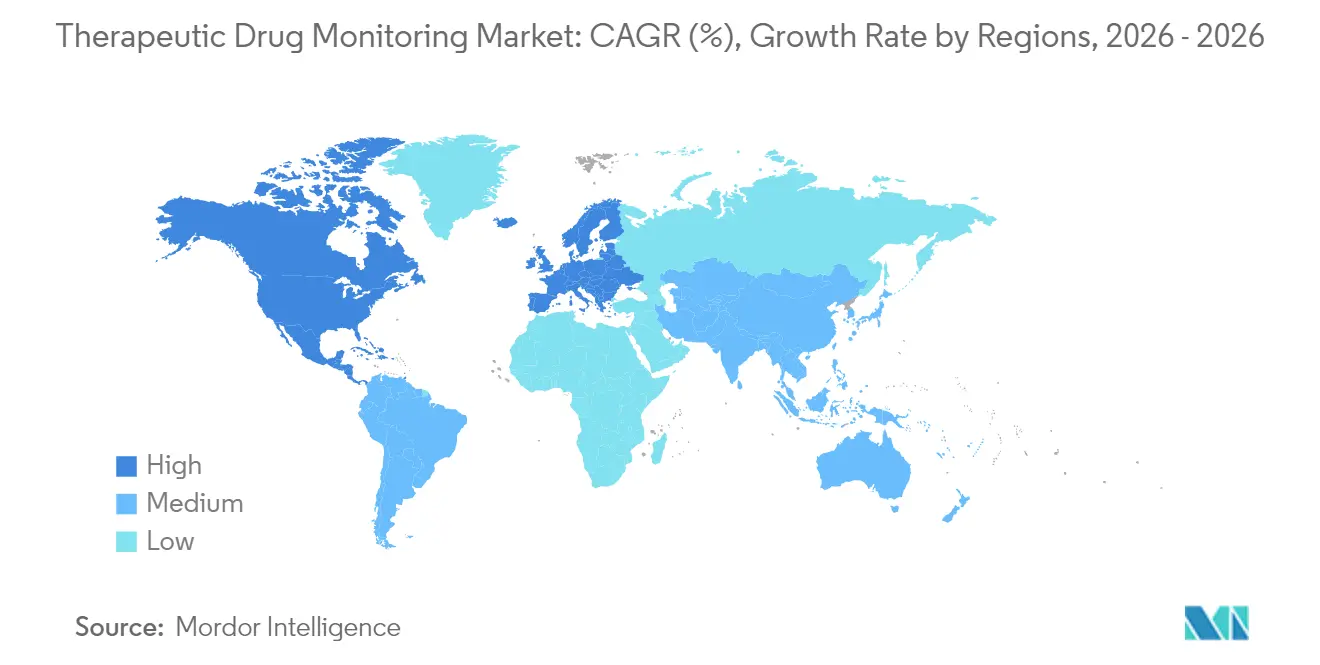

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Therapeutic Drug Monitoring Market Analysis by Mordor Intelligence

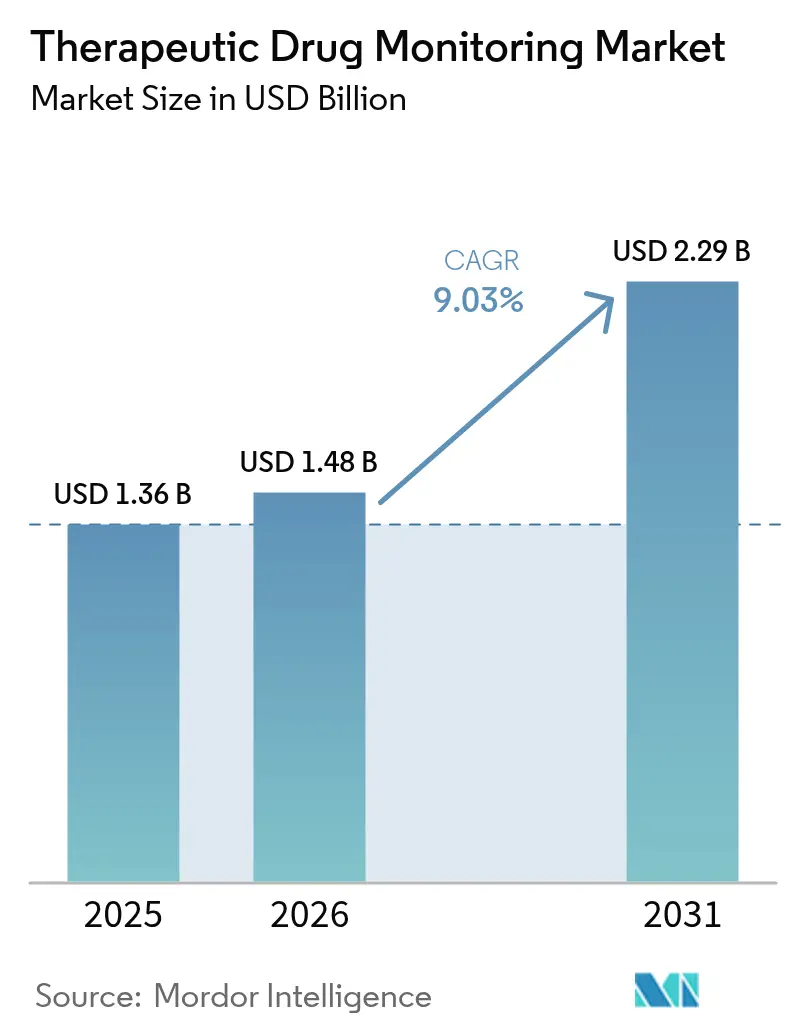

The Therapeutic Drug Monitoring Market size was valued at USD 1.36 billion in 2025 and estimated to grow from USD 1.48 billion in 2026 to reach USD 2.29 billion by 2031, at a CAGR of 9.03% during the forecast period (2026-2031).

Rising adoption of precision-medicine programs, integration of pharmacogenomic decision tools, and expanding decentralized clinical-trial activity anchor this expansion, while cost-pressured hospital systems increasingly favor high-throughput core-lab automation to sustain routine testing volumes. Continuous biosensor platforms and dried-blood-spot sampling are widening access well beyond tertiary centers, enabling remote dose titration and reducing adverse-event risk across oncology, HIV, and autoimmune therapy protocols. Regulatory alignment, including the United States Food and Drug Administration’s phased oversight of laboratory-developed tests, is expected to raise quality baselines and accelerate payer acceptance of broader test panels. Nonetheless, capital constraints in emerging markets continue to limit deployment of liquid-chromatography tandem mass-spectrometry (LC-MS/MS) analyzers, tempering penetration of highly specific assays.

Key Report Takeaways

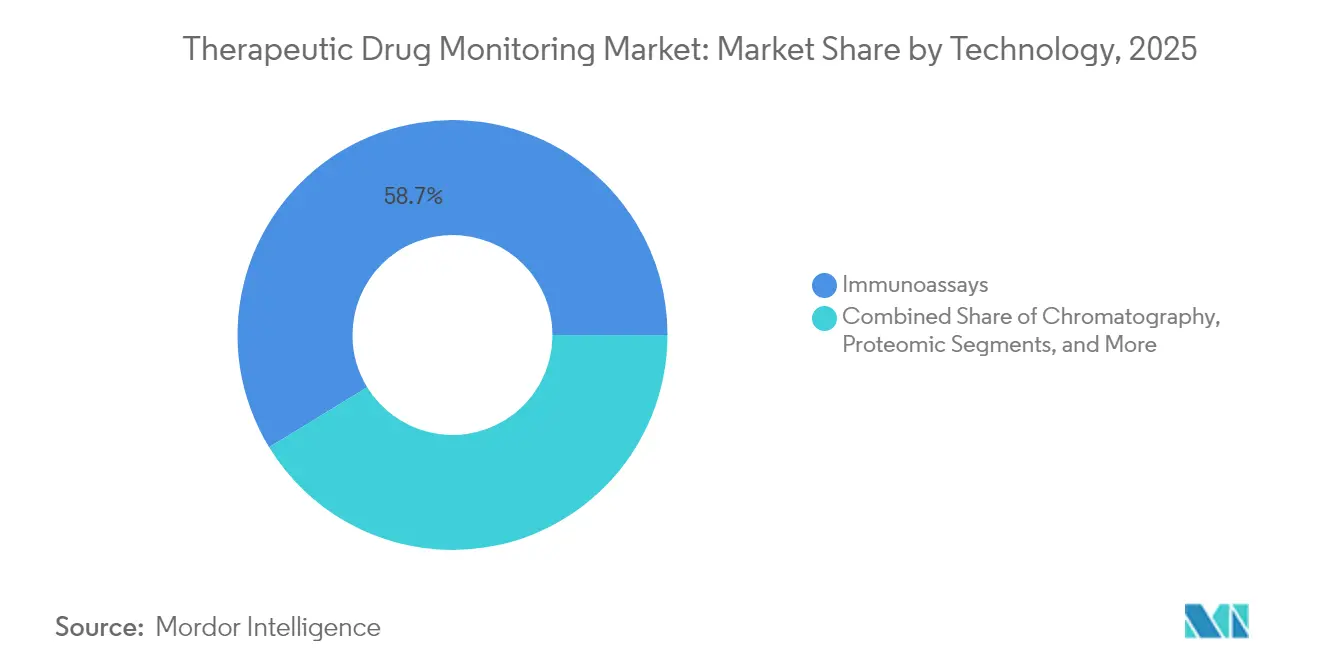

- By technology, immunoassays led with a 58.74% revenue share in 2025, whereas biosensor-based platforms are projected to expand at a 9.74% CAGR through 2031.

- By drug class, antiepileptic agents accounted for 31.88% of the therapeutic drug monitoring market share in 2025, while oncology therapeutics are set to grow at 9.55% CAGR to 2031.

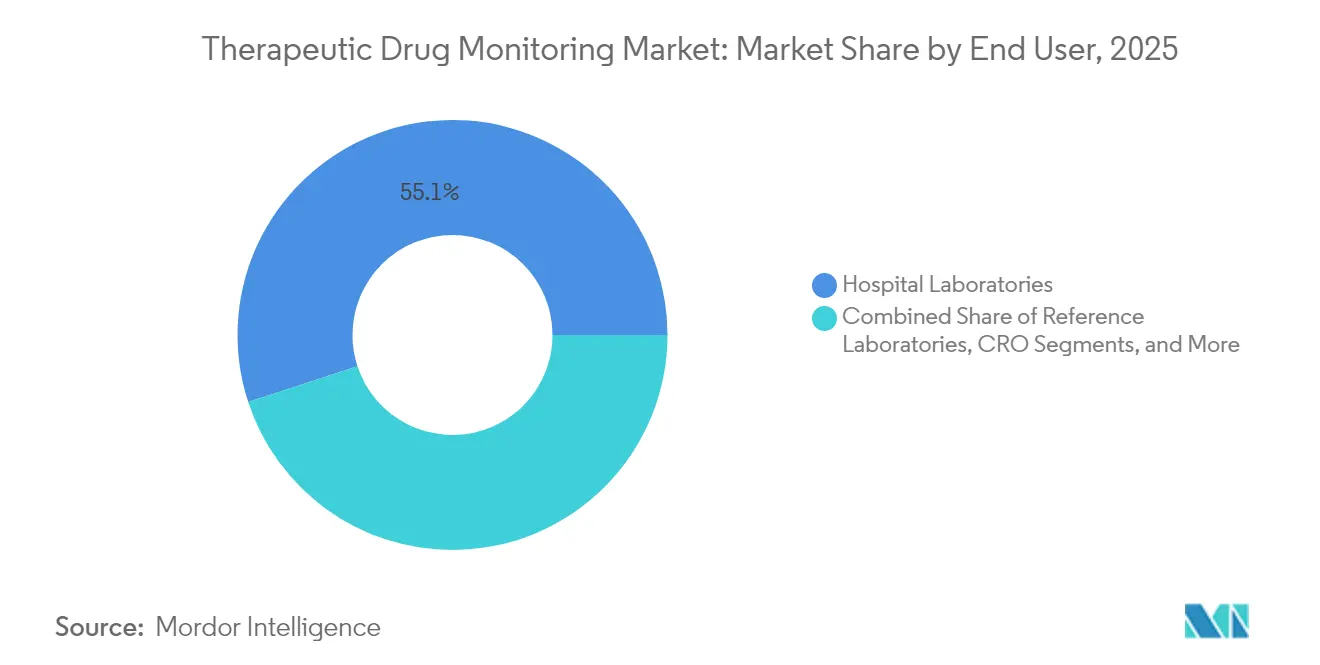

- By end user, hospital laboratories held 55.05% of the market size in 2025; point-of-care sites are advancing at a 10.03% CAGR through 2031.

- By geography, North America commanded 41.80% revenue share in 2025, whereas Asia-Pacific is forecast to register a 10.27% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Therapeutic Drug Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of oncology, HIV, autoimmune & cardiac cases | +2.1% | Global; strongest influence in North America & Europe | Medium term (2-4 years) |

| Expansion of clinical trials & companion-diagnostic mandates | +1.8% | Global; concentrated in major pharmaceutical hubs | Short term (≤ 2 years) |

| Automation & high-throughput immunoassay adoption in core labs | +1.5% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Low-cost dried-blood-spot sampling enabling remote TDM | +1.3% | Global; particularly impactful in emerging markets | Long term (≥ 4 years) |

| Integration of pharmacogenomic data with TDM algorithms | +1.2% | Developed markets initially; global expansion | Long term (≥ 4 years) |

| Wearable micro-fluidic biosensors for real-time drug-level tracking | +0.9% | Technology-advanced markets; gradual global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Oncology, HIV, Autoimmune & Cardiac Cases

Cancer protocols increasingly pair small-molecule kinase inhibitors with monoclonal antibodies, creating narrow therapeutic margins that mandate precise serum-level control to avoid suboptimal tumor inhibition or dose-limiting toxicity [1]Matteo Negrini, “Integration of Pharmacogenomics and TDM in Oncology,” Therapeutic Drug Monitoring, journals.lww.com. Long-acting cabotegravir–rilpivirine combinations for HIV expand monitoring horizons beyond daily oral dosing, requiring confirmation of sustained trough concentrations over monthly or bi-monthly intervals. Autoimmune conditions now routinely employ biologic disease-modifying agents whose clearance rates vary with anti-drug antibody formation, and therapeutic drug monitoring provides an evidence-based path to differentiate primary non-response from immunogenic loss of efficacy. Cardiovascular cases driven by aging populations reinforce volume growth for digoxin and antiarrhythmic level checks to avert iatrogenic toxicity. Together, these disease burdens add consistent patient cohorts to the market, underpinning predictable test-volume increases.

Expansion of Clinical Trials & Companion-Diagnostic Mandates

Regulators now expect dose-optimization evidence across diverse genotypes and comorbidity profiles during pivotal trials, firmly embedding therapeutic drug monitoring into study protocols. Sponsors therefore integrate sample-to-insight workflows that merge LC-MS/MS analytics with pharmacogenomic algorithms, enabling adaptive dosing arms and reducing late-stage attrition. Decentralized trial models accelerate adoption of mailed dried-blood-spot kits, preserving data fidelity while minimizing site visits. Positive experience in trials subsequently informs post-marketing label expansions that specify serum-level guidance, which in turn grows routine clinical demand. The feedback loop converts clinical-development spending into durable revenue streams for assay manufacturers and service laboratories across the market.

Automation & High-Throughput Immunoassay Adoption in Core Labs

Fourth-generation benchtop analyzers integrate pre-analytical robotics, microfluidic reagent packs, and middleware that feeds results into laboratory information systems without manual transcription. Combined with AI-enabled predictive maintenance, uptime surpasses 97%, raising daily throughput beyond 10,000 tests on high-volume campuses. Reduced reagent costs and minimal hands-on time improve profit margins, allowing health-systems to extend test menus to lower reimbursement drugs that were once outsourced. Core labs thereby consolidate hospital networks’ demand, mitigating the clinical toxicologist shortage by leveraging standardized, algorithm-driven interpretive reports. As a result, institutional buyers gravitate toward full-suite vendors, reinforcing brand loyalty and heightening barriers to entry across the therapeutic drug monitoring market.

Low-Cost Dried-Blood-Spot Sampling Enabling Remote TDM

Micro-capillary collection cards store whole blood at ambient temperatures for up to three weeks with negligible analyte degradation, removing refrigerated logistics and expediting rural outreach. Self-collection lowers patient burden and improves adherence to monitoring schedules, leading to richer longitudinal datasets that refine dosing algorithms. Public health programs in Southeast Asia, Latin America, and sub-Saharan Africa now pilot mail-in therapeutic drug monitoring kits for tuberculosis and HIV, demonstrating 30% turnaround-time reductions relative to clinic-based draws. Health insurers recognize downstream savings from avoided adverse events, strengthening reimbursement prospects. Consequently, dried-blood-spot workflows extend the market to populations previously beyond the reach of centralized phlebotomy services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital & service-contract costs of LC-MS/MS platforms | -1.4% | Global; most severe in emerging markets | Short term (≤ 2 years) |

| Shortage of skilled clinical toxicologists in emerging nations | -0.9% | Emerging markets; growing impact in developed regions | Medium term (2-4 years) |

| Fragmented reimbursement coding for TDM panels | -0.8% | Primarily North America; parts of Europe | Medium term (2-4 years) |

| Data-exchange gaps between LIS & decision-support software | -0.6% | Global; varies by healthcare-system maturity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital & Service-Contract Costs of LC-MS/MS Platforms

Entry-level triple-quadrupole systems list at USD 300,000–500,000, and annual maintenance contracts add USD 50,000, stretching budgets of secondary hospitals and private labs in low- and middle-income economies [2]Medical Device Innovation Consortium, “LC-MS/MS Cost Barriers in Emerging Markets,” MSACL, msacl.org. Even in developed markets, fiscal stewardship committees demand robust utilization forecasts before approving purchases. High acquisition thresholds perpetuate send-out testing, lengthening turnaround times and diminishing immediate clinical value, which in turn slows routine test adoption. Pooled-purchasing consortia and reagent-rental models partially mitigate cash-flow constraints, yet many facilities remain reliant on less specific immunoassays, limiting cross-reactivity-sensitive applications such as kinase inhibitors and immunotherapies across the therapeutic drug monitoring market.

Shortage of Skilled Clinical Toxicologists in Emerging Nations

Although automation reduces manual pipetting and calibration steps, expert oversight remains indispensable for method validation, trace-level troubleshooting, and clinical interpretation [3]National Institutes of Health, “Global Workforce Gaps in Clinical Toxicology,” NIH, nih.gov. Training pipelines lag technological complexity; only 10 African universities offer accredited clinical toxicology programs, and attrition to higher-paying pharmaceutical roles exacerbates staffing gaps. Consequently, laboratory directors in South Asia and Latin America adopt narrower therapeutic drug monitoring panels, focusing on antiepileptics and immunosuppressants while deferring oncology assays that carry greater interpretive nuance. Remote-consultation networks are emerging yet cannot fully compensate, keeping skilled-labor scarcity a persistent drag on the therapeutic drug monitoring market’s full potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Immunoassays Dominate Despite Biosensor Disruption

Immunoassays generated the largest revenue portion of the therapeutic drug monitoring market size, holding a 58.74% share in 2025. Integration into legacy chemistry lines, consistent reimbursement coding, and technician familiarity sustain this lead. However, biosensor and wearable platforms are recording a 9.74% CAGR, underpinned by electrochemical transduction advances that enable in-situ drug-level readouts from interstitial fluid. Mass-spectrometry-linked immunochemical hybrids widen menus to encompass small-molecule oncology agents, further reinforcing the incumbent technology’s relevance.

Protein-binding interference, hook effects, and cross-reactivity limitations have propelled tertiary centers toward chromatographic and LC-MS/MS solutions for complex regimens, fortifying multivendor competition. Continuous wearables prototype pipelines, meanwhile, promise sub-minute sampling intervals, redefining therapeutic drug monitoring market paradigms from episodic draws to dynamic pharmacokinetic profiling. Venture-backed start-ups align with pharmaceutical sponsors to pair devices with long-acting injectables, accelerating clinical validation. As regulatory pathways clarify, competitive dynamics will increasingly hinge on usability, data-security architecture, and algorithmic dosing guidance rather than analytical sensitivity alone.

By Drug Class: Oncology Therapies Drive Future Growth

Antiepileptic formulations represented 31.88% of 2025 revenue, mirroring entrenched guidelines requiring routine serum-level checks for valproate, carbamazepine, and related agents. Oncology therapeutics, however, are projected to surge at a 9.55% CAGR through 2031, positioning them as the fastest-growing slice of the market. Precision oncology mandates individually titrated kinase inhibitor doses to optimize tumor exposure and mitigate systemic toxicity, catalyzing broad deployment of LC-MS/MS multiplex panels.

Immunosuppressants retain robust volumes across transplant centers, while renewed stewardship initiatives elevate vancomycin and aminoglycoside monitoring to curb nephrotoxicity. Psychiatric agents such as clozapine remain mandatory candidates, yet broader antipsychotic monitoring adoption hinges on payer policy harmonization. Pharmacogenomic overlay further differentiates dosing paths, effectively merging pre-emptive genotyping with post-dose serum confirmation, a convergence that strengthens the therapeutic drug monitoring market’s strategic relevance across specialties.

By End-User: Point-of-Care Testing Disrupts Hospital Dominance

Hospital laboratories controlled 55.05% of the therapeutic drug monitoring market share in 2025. Their advantage derives from embedded LIS connectivity, existing billing pathways, and clinical proximity for sample collection. Yet point-of-care hubs—ambulatory clinics, dialysis units, and home-based devices—are expanding at a 10.03% CAGR, fueled by compact analyzers delivering results in under 15 minutes from finger-stick blood.

Reference laboratories safeguard specialized assay demand, concentrating high-complexity workflows and benefiting from scale economies. Academic centers maintain early-adopter status, piloting novel biomarkers and wearable integrations. Contract research organizations bolster their service portfolios to accommodate nuanced trial endpoints, underscoring the therapeutic drug monitoring market’s role across R&D and routine care. Digital-health overlays translate numeric drug levels into smartphone alerts, bridging clinician and patient, and reinforcing adherence to therapeutic windows.

Geography Analysis

North America’s 41.80% contribution to the therapeutic drug monitoring market size in 2025 stems from entrenched reimbursement, extensive transplant programs, and pharmacogenomic leadership. Europe mirrors this maturity, albeit under cost-containment pressures that prioritize consolidated procurement and outcome-based pricing. Asia-Pacific exhibits a 10.27% CAGR through 2031, reflecting hospital construction booms, clinical-trial inflows, and national precision-health initiatives. China commands the region’s volume uplift, coupling public-sector infrastructure funding with stringent regulatory reforms that encourage local LC-MS/MS manufacturing. Japan’s super-aged demographics sustain high per-capita test ratios, while India’s expanding health-insurance coverage widens patient access to essential monitoring panels. Middle East and South America show nascent yet accelerating adoption curves as laboratory automation vendors partner with government agencies to modernize diagnostic capabilities, an endeavor that incrementally enlarges the therapeutic drug monitoring market.

Competitive Landscape

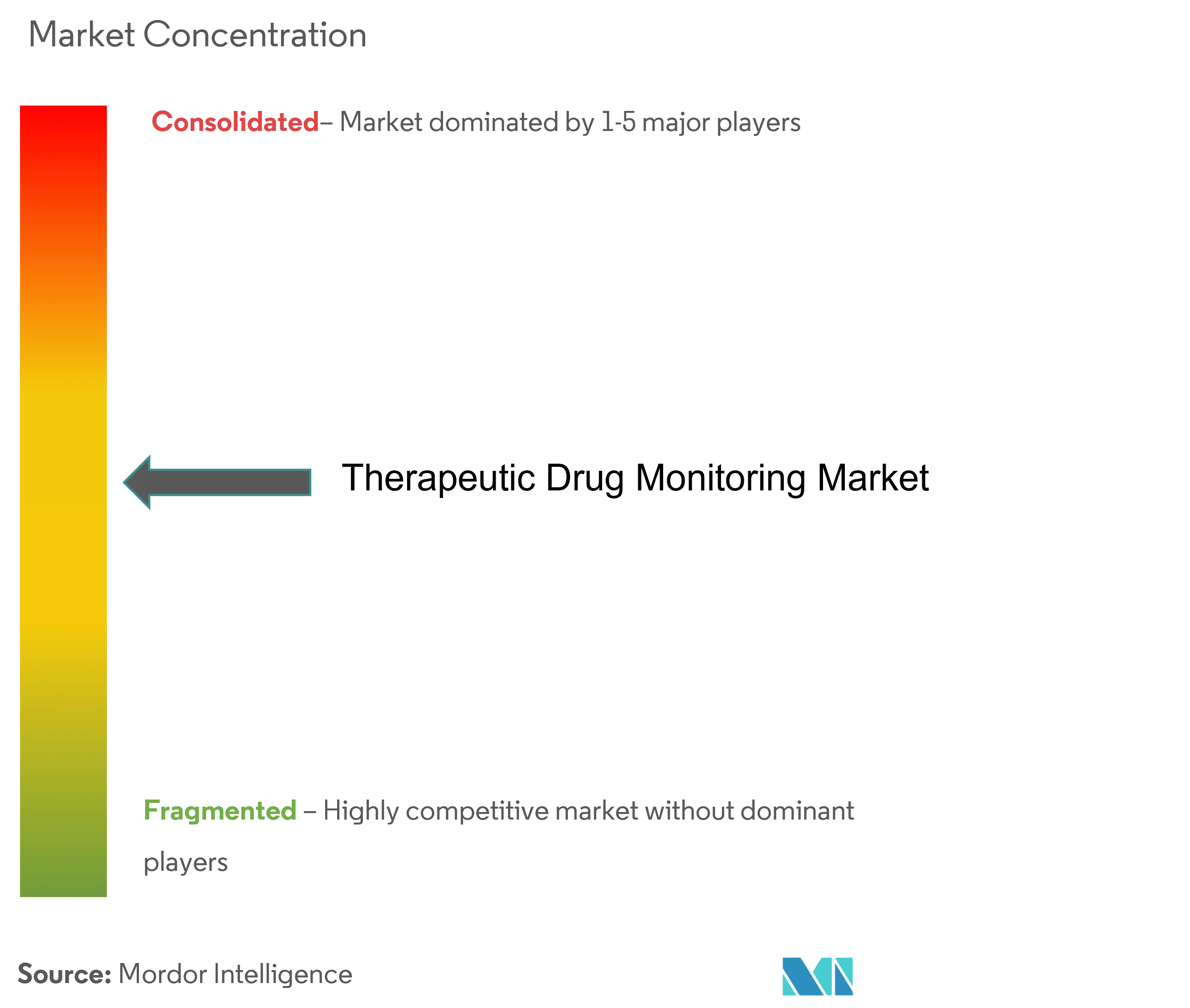

The therapeutic drug monitoring market is moderately consolidated. Abbott, Thermo Fisher, Roche, Siemens Healthineers, and Danaher leverage full-line diagnostic portfolios and established service footprints to protect incumbent positions. Their competitive edge lies in end-to-end offerings—sample collection devices, automation-ready analyzers, assay reagents, and middleware decision-support—that simplify procurement for hospital chains.

Mid-tier firms focus on niche innovation. Bio-Rad exploits multiplex immunoassay panels to shorten turnaround times for transplant monitoring, while niche start-ups deploy cloud-native dashboards that translate biosensor readings into dose-adjustment guidance within minutes. Strategic acquisitions characterize the past two years: Siemens Healthineers absorbed a wearable-sensor developer to accelerate outpatient revenue, and Thermo Fisher integrated an AI algorithm vendor to enhance LC-MS/MS interpretive reporting.

Collaborations between device makers and pharmaceutical companies are intensifying. Oncology drug sponsors embed proprietary assays into clinical-trial protocols to streamline regulatory filings, guaranteeing initial instrument placements. Reagent-rental contracts and outcomes-based pricing models are gaining traction, reflecting broader value-based-care trends. Vendors investing in cybersecurity layers and standardized data interoperability position themselves favorably as digital-health ecosystems mature, shaping long-term contest for therapeutic drug monitoring market leadership.

Therapeutic Drug Monitoring Industry Leaders

Thermo Fisher Scientific

Bio-Rad Laboratories

F. Hoffmann-La Roche Ltd

Danaher Corporation (Beckman Coulter, Inc.)

Siemens Healthcare GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Ferring B.V. launched Rebyota and Adstiladrin in the United States, expanding its therapeutic-class portfolio and creating long-term dosing-monitoring revenue opportunities.

- January 2022: Seer launched a next-generation proteomics research platform. The system can be used for categorizing the tens of thousands of proteins within the human body that drive the biological functions of both life and disease.

Global Therapeutic Drug Monitoring Market Report Scope

Therapeutic drug monitoring is the clinical practice of measuring the concentration of specific drugs with a narrow therapeutic index and/or their breakdown products (metabolites) at timed intervals in a patient's bloodstream. These systems help to maintain a relatively constant concentration of the drug in the blood required to show therapeutic effects and, thus, assist in assessing individual dosage regimens.

Therapeutic Drug Monitoring Market is Segmented by Technology (Immunoassays and Proteomic Technologies), Drug Class (Antiarrhythmic Drugs, Immunosuppressants, Antiepileptic Drugs, and Other Drug Classes), End-user (Hospitals, Diagnostic Centers, and Other End-users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across significant global regions. The report offers the value (in USD million) for the above segments.

| Immunoassays | ELISA |

| Chemiluminescence Immunoassay (CLIA) | |

| Fluorescence & Other IA Formats | |

| Proteomic / LC-MS/MS | |

| Chromatography (GC, HPLC) | |

| Biosensor-Based & Wearables | |

| Other Technologies |

| Antiarrhythmic Drugs |

| Antiepileptic Drugs |

| Immunosuppressants |

| Antibiotics (e.g., Vancomycin, Aminoglycosides) |

| Antipsychotics & Mood Stabilizers |

| Oncology & Targeted Therapies |

| Other Drug Classes |

| Hospital Laboratories |

| Independent / Reference Laboratories |

| Academic & Research Institutes |

| Point-of-Care / Patient Self-Testing |

| Contract Research & CRO Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| South Africa | |

| Rest of Middle East | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Immunoassays | ELISA |

| Chemiluminescence Immunoassay (CLIA) | ||

| Fluorescence & Other IA Formats | ||

| Proteomic / LC-MS/MS | ||

| Chromatography (GC, HPLC) | ||

| Biosensor-Based & Wearables | ||

| Other Technologies | ||

| By Drug Class | Antiarrhythmic Drugs | |

| Antiepileptic Drugs | ||

| Immunosuppressants | ||

| Antibiotics (e.g., Vancomycin, Aminoglycosides) | ||

| Antipsychotics & Mood Stabilizers | ||

| Oncology & Targeted Therapies | ||

| Other Drug Classes | ||

| By End-user | Hospital Laboratories | |

| Independent / Reference Laboratories | ||

| Academic & Research Institutes | ||

| Point-of-Care / Patient Self-Testing | ||

| Contract Research & CRO Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| South Africa | ||

| Rest of Middle East | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Therapeutic Drug Monitoring Market?

The Therapeutic Drug Monitoring Market size is expected to reach USD 1.48 billion in 2026 and grow at a CAGR of 9.03% to reach USD 2.29 billion by 2031.

Which technology segment dominates the therapeutic drug monitoring market?

Immunoassays dominate with a 58.74% revenue share in 2025, though biosensor platforms are the fastest-growing at 9.74% CAGR.

Who are the key players in Therapeutic Drug Monitoring Market?

Thermo Fisher Scientific, Bio-Rad Laboratories, F. Hoffmann-La Roche Ltd, Danaher Corporation (Beckman Coulter, Inc.) and Siemens Healthcare GmbH are the major companies operating in the Therapeutic Drug Monitoring Market.

Which is the fastest growing region in Therapeutic Drug Monitoring Market?

Government-backed hospital expansion, surging clinical-trial activity, and health-technology investments are generating a 10.27% CAGR through 2031 in Asia-Pacific.

Which region has the biggest share in Therapeutic Drug Monitoring Market?

In 2025, the North America accounts for the largest market share in Therapeutic Drug Monitoring Market.

What are the main restraints limiting wider adoption?

High capital costs for LC-MS/MS instruments and a shortage of trained clinical toxicologists—especially in emerging economies—continue to impede broader implementation.

Page last updated on: