Monoclonal Antibodies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 323.89 Billion |

| Market Size (2031) | USD 596.12 Billion |

| Growth Rate (2026 - 2031) | 12.99% CAGR |

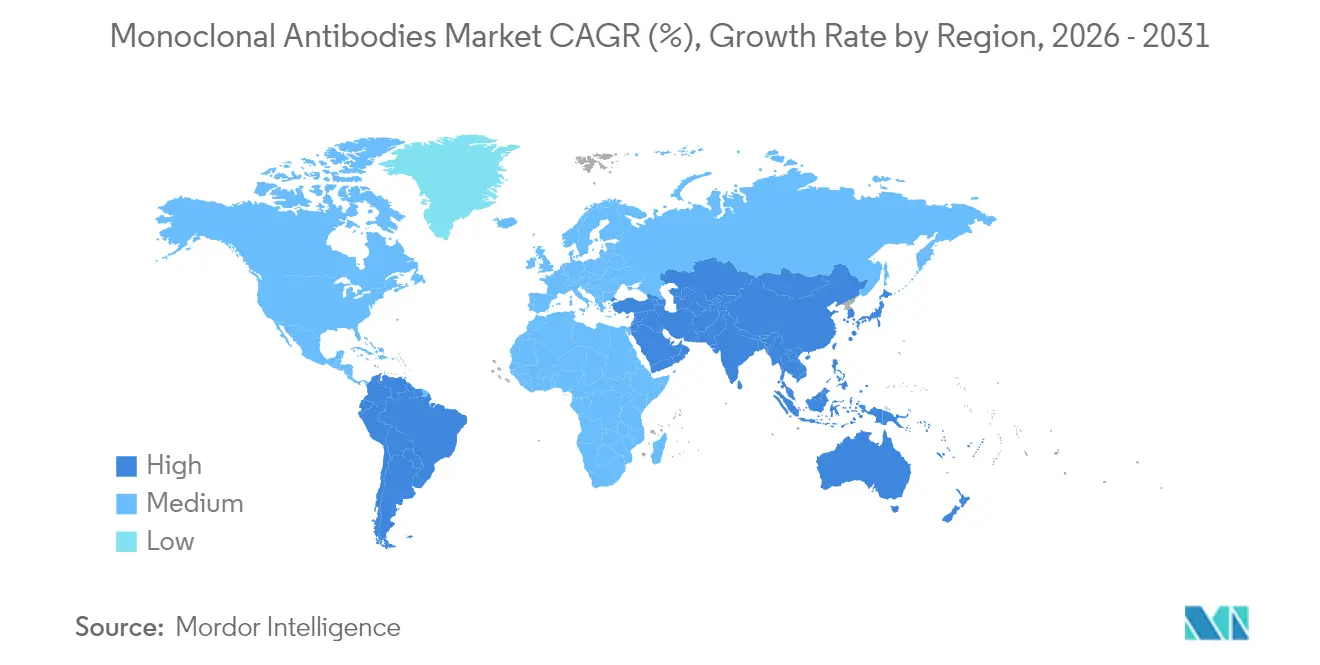

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Monoclonal Antibodies Market Analysis by Mordor Intelligence

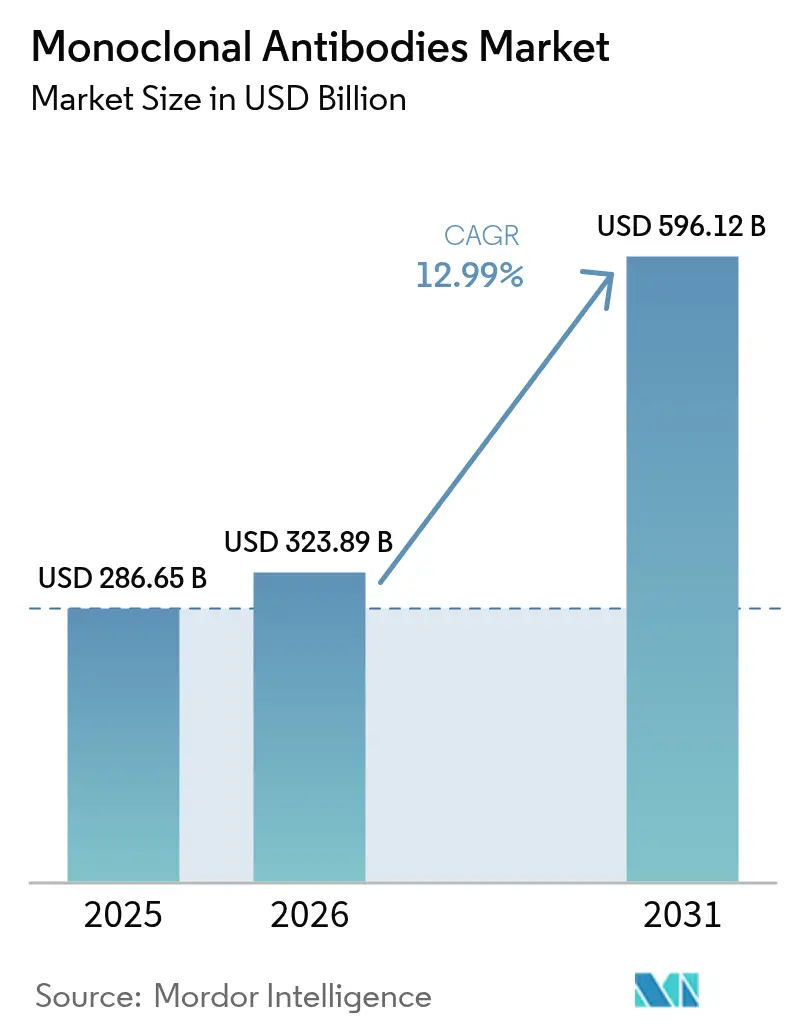

The Monoclonal Antibodies Market size was valued at USD 286.65 billion in 2025 and estimated to grow from USD 323.89 billion in 2026 to reach USD 596.12 billion by 2031, at a CAGR of 12.99% during the forecast period (2026-2031).

Growth reflects the transition of antibody therapeutics from niche biologics to first-line interventions across oncology, autoimmune disorders, and infectious-disease prevention. Catalysts include rapid-fire antibody-engineering platforms, faster regulatory reviews for breakthrough indications, and government pandemic-preparedness outlays that commit USD 79.5 billion to medical countermeasures through 2027. Contract development and manufacturing organizations (CDMOs) now anchor the supply base, with Samsung Biologics booking more than USD 3.3 billion in new contracts during 2024 and WuXi Biologics carrying a USD 20.6 billion backlog, underscoring structural demand. The geographic tilt toward Asia-Pacific capacity, expected to represent 45% of new volume additions by 2028, heightens supply-chain concentration risks while simultaneously lowering unit costs.

Key Report Takeaways

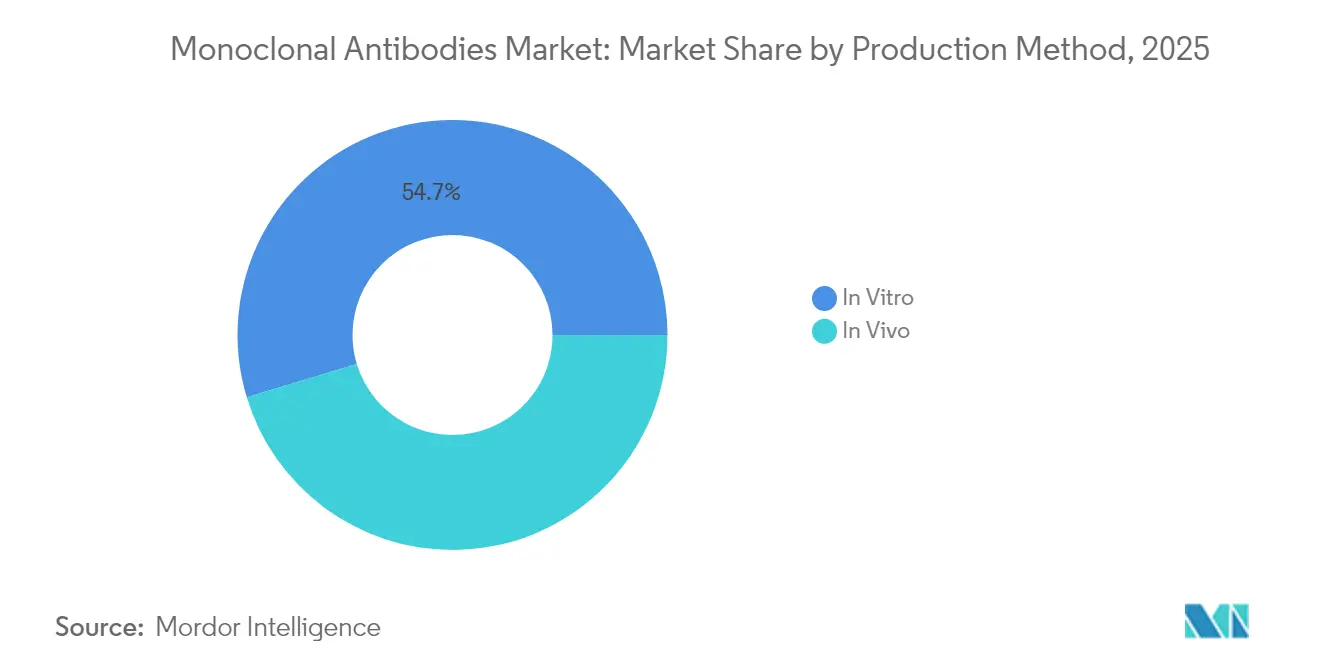

- By production method, in vitro systems accounted for 54.68% of the global monoclonal antibodies market share in 2025; this segment is projected to expand at a 13.95% CAGR through 2031.

- By source, human-derived antibodies led with a 59.02% revenue share in 2025, while humanized variants are poised for the fastest growth, with an 18.02% CAGR to 2031.

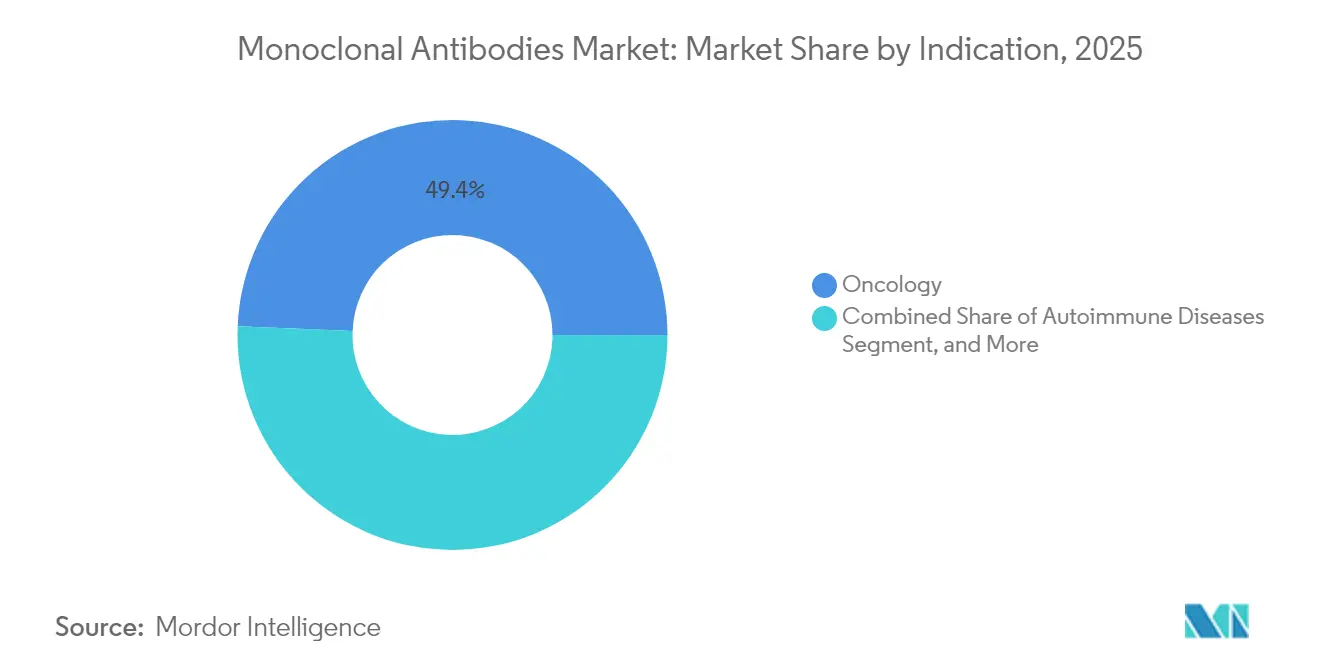

- By indication, oncology accounted for 49.35% of 2025 revenue, whereas autoimmune diseases are forecast to post the strongest 19.22% CAGR to 2031.

- By end user, hospitals captured 39.22% of demand in 2025; specialty and ambulatory centers represent the highest-growth channel, with a 15.98% CAGR toward 2031.

- By geography, North America captured 40.62% of the global monoclonal antibodies market share in 2025; Asia-Pacific region represents the highest growth at 13.11% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Monoclonal Antibodies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Technological Advancements in Antibody‐Engineering Platforms | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Escalating Global Cancer & Chronic-Disease Incidence | +3.2% | Global, with highest impact in aging populations of North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Expanding Government & VC Funding for mAb R&D | +2.1% | North America & Europe primarily, expanding to Asia-Pacific | Short term (≤ 2 years) |

| AI-Driven De-Novo Antibody Design Accelerates Discovery Cycles | +1.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Demand For Highly Potent Single-Use ADC Bioreactors | +1.7% | Global, with manufacturing concentration in Asia-Pacific | Short term (≤ 2 years) |

| Pandemic-Preparedness Stockpiling Initiatives | +1.6% | North America, Europe, with emerging programs in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Technological Advancements in Antibody-Engineering Platforms

High-throughput microfluidics and single-B-cell screening have condensed discovery cycles from months to weeks, enabling developers to locate rare, high-affinity clones with precision. Samsung Biologics’ 2024 launch of the S-HiCon platform allows liquid formulations exceeding 200 mg/mL, resolving viscosity and stability barriers for subcutaneous delivery.[1]Andreas Krömer, “Samsung Biologics Annual Report 2024,” samsungbiologics.com Site-specific conjugation techniques now dominate antibody-drug conjugate (ADC) pipelines, cutting batch variability and smoothing regulatory reviews; 14 bispecific antibodies already hold global approvals as of 2024. These scalable, standardized toolkits shift negotiating leverage to CDMOs that can amortize platform investments over multiple programs, tilting competitive advantage toward large-scale manufacturers.

Escalating Global Cancer & Chronic-Disease Incidence

Projected 77% growth in worldwide cancer cases by 2050 and surging autoimmune diagnoses keep therapeutic demand robust.[2]Generics and Biosimilars Initiative, “Cost Savings From Rituximab Biosimilars,” gabi-journal.net Checkpoint inhibitors illustrate convergence: mechanistic insights gained in oncology are migrating into autoimmune protocols, shrinking development timelines and enlarging patient pools. Monoclonal antibodies serve dual roles—as independent biologics and as precision payload carriers in ADCs—reinforcing their indispensability across disease clusters. Demographic aging in North America, Europe, and Asia-Pacific further raises prevalence, ensuring sustained therapy volumes.

Expanding Government & VC Funding for mAb R&D

U.S. government programs are directing major funding toward the development of next-generation COVID-19 antibodies, with broader public health initiatives also receiving long-term financial support.[3]U.S. Department of Health & Human Services, “Government Investment in Medical Countermeasures,” hhs.gov Canada’s Health Emergency Readiness Canada initiative bolsters domestic capacity for pandemic countermeasures. Venture capital increasingly pools around platform plays; Samsung Life Science Fund II targets AI-enabled antibody discovery startups. Government de-risking frees private capital to underwrite later-stage trials, compressing the journey from benchtop to bedside.

AI-Driven De-Novo Antibody Design Accelerates Discovery Cycles

Machine-learning models now predict epitope binding and structural stability, trimming early discovery timelines by up to 70%. AbbVie’s USD 355 million alliance with BigHat Biosciences and Sanofi’s USD 1 billion collaboration with BioMap spotlight big-pharma appetite for computational biology. AI optimizes sequences for manufacturability, resistance to viral escape, and lowered immunogenicity, elevating the probability of clinical success. Democratized cloud-based platforms also equip smaller biotechs to compete at the ideation stage, reshaping traditional size-based moats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Therapy & Manufacturing Costs | -2.9% | Global, with highest impact in price-sensitive emerging markets | Long term (≥ 4 years) |

| Patent Expiries & Biosimilar Pricing Pressure | -2.1% | North America & Europe primarily, expanding globally | Medium term (2-4 years) |

| Biomanufacturing-Capacity Crunch Vs. Cell-&-Gene Therapies | -1.8% | Global, with acute constraints in North America and Europe | Short term (≤ 2 years) |

| HTA Reimbursement Push-Back on Real-World Cost-Effectiveness | -1.7% | Europe, North America, with emerging pressure in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Therapy & Manufacturing Costs

Median launch prices for specialty biologics reached USD 300,000 per course in 2024, straining payer budgets. Cost-effectiveness studies indicate eculizumab requires a 93% discount to meet QALY thresholds, underscoring affordability gaps. Complex ADC containment, extensive QC protocols, and Protein A resin expenses sustain high cost bases despite single-use bioreactor adoption. Although rituximab biosimilars generated annual savings of USD 208,553 in Chile, uptake lags in the United States, muting price-compression benefits.

Patent Expiries & Biosimilar Pricing Pressure

Blockbusters such as Stelara and Prolia/Xgeva are losing exclusivity, while Keytruda faces biosimilar entry risk by 2028. The adalimumab saga shows originators can retain 97% volume share via aggressive contracting even after 10 biosimilar launches. Oncology biosimilars encounter steeper regulatory and manufacturing hurdles, potentially capping discount depth versus simpler molecules. Nonetheless, pharmacy benefit managers are experimenting with value-based contracts that could accelerate switching once post-approval supply stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Method: In Vitro Platforms Sustain Scalable Leadership

In Vitro systems controlled 54.68% of the monoclonal antibodies market in 2025 and are set to advance at a 13.95% CAGR through 2031. This segment’s productivity edge underpins 2025 revenue dominance as Chinese hamster ovary cell lines push titers above 11.5 g/L, tripling fed-batch output. Continuous perfusion and multicolumn chromatography lower Protein A resin use by 40%, shaving raw-material costs while boosting recovery to 87%. The monoclonal antibodies market size for In Vitro platforms is forecast to widen in lockstep with CDMO capacity rollouts across South Korea and China.

Viral-vector or glycoengineered In Vivo methods now occupy niche applications requiring exotic post-translational patterns. As single-use benchtop systems proliferate, smaller biotech firms gain capital-light manufacturing access, reinforcing the monoclonal antibodies market’s outsourcing narrative. CDMOs integrating continuous upstream and downstream flows can pivot capacity between standard IgG and complex ADC runs without extensive retrofits, a flexibility premium that attracts pipeline-heavy sponsors.

By Source: Humanized Engineering Drives Fastest Upswing

Human antibodies maintained 59.02% revenue share in 2025, yet humanized constructs are accelerating at an 18.02% CAGR on the strength of better immunogenicity profiles. Phage display, yeast display, and transgenic mouse platforms converge to produce quasi-germline sequences that evade anti-drug antibodies, critical for chronic dosing regimens. The monoclonal antibodies market share leadership remains with fully human assets, but the monoclonal antibodies market size attributable to humanized variants is projected to climb sharply alongside autoimmune pipeline expansions.

Computational epitope screening now flags immunogenic hot spots before IND filing, shortening iterative redesign cycles. Chimeric formats persist where speed outweighs tolerability, particularly in late-stage oncology trials. However, third-generation transgenic mice capable of producing diversified human heavy and light chains promise to close the gap, challenging humanized constructs for future mindshare.

By Indication: Autoimmune Diseases Become Next Growth Frontier

Oncology supplied 49.35% of 2025 revenue, yet autoimmune disorders are forecast to compound at 19.22% annually to 2031 as earlier diagnosis, biomarker stratification, and innovative B-cell depletion schemes widen eligible cohorts. Infectious-disease antibodies such as RSV-targeting nirsevimab and clesrovimab illustrate expanding prophylactic roles; nirsevimab cut RSV-related hospitalization by 90% in real-world assessments.

Within oncology, ADCs and bispecifics refresh revenue streams as single-target IgG competitors confront biosimilar erosion. Cross-indication translational learning accelerates asset recycling: mechanisms initially successful in oncology migrate into rheumatoid arthritis and systemic lupus pipelines, compressing development chronologies and enriching return profiles.

By End User: Specialty & Ambulatory Centers Capture Administration Shift

Hospitals generated 39.22% of 2025 consumption, yet specialty centers are progressing at a 15.98% CAGR through 2031. Subcutaneous reformulations like Roche’s Tecentriq Hybrenza trim chair time to seven minutes, aligning with outpatient throughput imperatives. Phesgo’s European cost-minimization analyses report up to 80% savings versus IV infusions, strengthening payer support for migration. The monoclonal antibodies market size flowing through non-hospital channels therefore expands in tandem with high-concentration formulations and digital adherence tools.

Retail clinics and physician-office infusion suites benefit from biosimilar cost deflation, offering multi-source panels that raise scheduling flexibility. Remote-monitoring platforms deliver real-time adverse-event detection, allowing at-home administration in selected populations, a paradigm likely to amplify as payers pursue site-of-care optimization.

Geography Analysis

North America controlled 40.62% of 2025 revenue, underpinned by dense innovation hubs, generous insurance coverage, and a supportive regulatory highway for expedited designations. The region’s multi-year PHEMCE appropriation guarantees baseline demand for antibody countermeasures, while Canada’s Health Emergency Readiness program adds domestic surge capacity. Yet exclusivity cliffs for Stelara and Prolia/Xgeva foreshadow intensifying biosimilar jockeying, prompting a pivot toward value-based contracts and real-world evidence requirements. Health-technology assessment scrutiny already influences formulary adoption, nudging manufacturers toward differential pricing.

Asia-Pacific is the fastest climber at a projected 13.11% CAGR. Capacity supremacy is decisive: Samsung Biologics will bring total volume to 784 kL by April 2025, and WuXi Biologics’ USD 20.6 billion backlog testifies to global sponsor reliance. Policymakers in China, South Korea, and Singapore bundle tax incentives with expedited GMP clearances, luring pipeline assets from Western biotech firms. However, overdependence on regional factories presents geopolitical and logistics fragility, spurring conversations about dual-sourcing and near-shoring strategies in North America and Europe.

Europe remains an innovation heavyweight thanks to entrenched pharmaceutical clusters and sophisticated regulators. Biosimilar adoption rates outpace the United States, sharpening price competition but also validating pathway predictability. Subcutaneous delivery innovation resonates with the region’s cost-containment ethos; Roche’s Phesgo adoption data show 91% of surveyed patients preferring home administration, bolstering pay-for-performance schemes. Emerging markets in Latin America, the Middle East, and Africa contribute incremental volumes as national immunization and oncology programs mature, although reimbursement constraints cap near-term penetration.

Mordor Intelligence provides coverage of the monoclonal antibodies market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Competition in the monoclonal antibodies market is characterized by moderate consolidation: top players integrate discovery platforms, clinical portfolios, and industrial-scale manufacturing. Roche, AbbVie, and Johnson & Johnson continue to lead the monoclonal antibody market through strategic lifecycle management, exemplified by AbbVie’s transition from Humira to newer therapies, such as Skyrizi and Rinvoq. Patent cliffs inject volatility, compelling incumbents to invest in bispecifics, ADCs, and long-acting formulations that differentiate beyond mere target affinity.

CDMOs, such as Samsung Biologics, WuXi Biologics, and Lonza, supply more than 50% of outsourced capacity, granting them significant strategic leverage. Their willingness to co-invest in client pipelines accelerates asset timelines and spreads risk, converting them into quasi-strategic partners rather than transactional vendors. AI alliances redefine borders: AbbVie–BigHat and Sanofi–BioMap collaborations target computational design frameworks capable of generating drug-like antibodies at scale. The RSV space highlights emerging white space; Merck’s clesrovimab complements Sanofi/AstraZeneca’s nirsevimab, opening up multi-billion-dollar pediatric franchises.

Disruptors focus on multi-specific constructs, gene-encoded antibodies, and non-traditional delivery routes such as inhaled formulations. Larger firms counter with targeted acquisitions; Roche’s acquisition of Poseida Therapeutics for its cell-therapy expertise represents a defensive play to secure next-generation technologies. Market entry barriers remain high, given the scale economics of GMP biologics and the steep capital demands for process validation; yet, democratized AI design tools and modular single-use plants modestly lower the hurdles for venture-backed challengers.

Monoclonal Antibodies Industry Leaders

Eli Lilly and Company

Amgen Inc.

Novartis AG

Merck & Co., Inc.

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Merck received FDA approval for clesrovimab (MK-1654), a long-acting monoclonal antibody designed to protect infants from respiratory syncytial virus during their first RSV season, demonstrating 60.5% reduction in medically attended RSV lower respiratory infections and 84.3% reduction in RSV-related hospitalizations in pivotal Phase 2b/3 trials. This approval positions Merck alongside Sanofi and AstraZeneca in the competitive RSV prevention market, expanding therapeutic options for vulnerable pediatric populations.

- June 2025: Novartis reported statistically significant radiographic progression-free survival benefits for Pluvicto in patients with PSMA-positive metastatic hormone-sensitive prostate cancer from the Phase III PSMAddition trial, expanding the radioligand therapy's potential application to earlier disease stages. The positive results support Novartis's expansion of manufacturing capabilities for radioligand therapies to meet growing demand.

- March 2025: Roche announced positive Phase III OUtMATCH study results showing Xolair (omalizumab) demonstrated superior efficacy and fewer side effects compared to oral immunotherapy for food allergies, with 36% of patients on Xolair tolerating significant allergen amounts versus 19% on oral immunotherapy. The head-to-head trial represents the first direct comparison between these treatment modalities, potentially reshaping food allergy management protocols.

- February 2025: Invivyd announced positive Phase 1/2 clinical data for VYD2311, a monoclonal antibody designed as a superior alternative to COVID-19 vaccination, demonstrating 17-fold greater neutralization potency against SARS-CoV-2 variants compared to pemivibart. The enhanced potency suggests potential for less frequent dosing and broader population applicability beyond immunocompromised individuals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global monoclonal antibodies (mAbs) market as the aggregate annual revenues generated from branded and biosimilar, full-length immunoglobulin-based therapeutics that are produced through recombinant cell culture and administered for human disease management across oncology, autoimmune, infectious, and inflammatory indications.

Scope Exclusions: diagnostic antibody kits, antibody fragments, polyclonal preparations, and discovery-stage service revenues are outside the assessed boundary.

Segmentation Overview

- By Production Method

- In Vitro

- In Vivo

- By Source

- Human

- Humanized

- Chimeric

- Murine

- By Indication

- Oncology

- Autoimmune Diseases

- Infectious Diseases

- Inflammatory Diseases

- Other Indications

- By End User

- Hospitals

- Academic Research Institutes

- Specialty & Ambulatory Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with medical oncologists, hospital pharmacy managers, CMOs, and regulatory consultants across North America, Europe, Asia-Pacific, and Latin America. These conversations validated average selling prices, therapy mix shifts (IV to sub-Q), biosimilar penetration assumptions, and near-term capacity expansion plans that secondary sources rarely quantify.

Desk Research

We began with authoritative biomedical and economic datasets such as the World Health Organization's ATC sales files, US FDA and EMA biologic approvals lists, National Cancer Institute incidence registries, OECD health-spend statistics, and UN Comtrade export codes for HS 3002 to size cross-border flows. Company 10-Ks, investor decks, and association portals (e.g., International Federation of Pharmaceutical Manufacturers, Biotechnology Innovation Organization) added pipeline visibility and pricing context. Subscription resources like Dow Jones Factiva and D&B Hoovers supplied historic revenue splits and plant capacities. Numerous additional public and proprietary references supported data cross-checks; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down demand pool was first built from treated-patient cohorts by indication, average therapy cycles, and weighted ASPs. Results were then corroborated with selective bottom-up checks of manufacturer-reported biologic sales, sampled contract prices, and shipment data, thereby aligning totals within a 5 percent error band. Key variables in the model include incidence and prevalence trends for high-burden cancers, therapy line migration rates, biosimilar adoption curves, manufacturing yield improvements, bioprocess capacity additions, and real-world price erosion. Multivariate regression and scenario analysis were subsequently used to forecast through 2030, with parameter ranges fine-tuned through expert consensus when historical volatility exceeded two standard deviations.

Data Validation & Update Cycle

Outputs pass a two-level analyst review where variance against external health-expenditure benchmarks and peer publications is flagged for re-contact. Reports refresh annually, while material events, major approvals, patent cliffs, and supply disruptions trigger interim updates. A final pre-publication sweep ensures clients receive the latest calibrated view.

Why Mordor's Monoclonal Antibodies Baseline Commands Reliability

Published estimates often differ because each firm chooses distinct product inclusions, price assumptions, and refresh cadences.

The main gap drivers stem from whether biosimilar sales are pooled, how off-invoice discounts are handled, and the breadth of indications counted beyond oncology.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 286.65 B (2025) | Mordor Intelligence | - |

| USD 252.60 B (2024) | Global Consultancy A | Excludes hospital mark-ups and vaccines; older base year |

| USD 265.17 B (2024) | Industry Analysis B | Therapeutics-only scope, no biosimilar uplift, limited Asia sampling |

| USD 231.42 B (2024) | Trade Journal C | Relies on list prices without regional discount adjustment |

The comparison shows that, by aligning the right product universe, adjusting for real transaction prices, and refreshing every twelve months, Mordor delivers a balanced, transparent baseline that decision-makers can trace back to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the global monoclonal antibodies market?

The market stood at USD 323.89 billion in 2026 and is forecast to climb to USD 596.12 billion by 2031.

Which therapeutic area contributes the largest share of monoclonal antibody revenues?

Oncology applications generated 49.35% of global revenue in 2025, making it the leading indication.

Which segment is projected to grow the fastest through 2031?

Autoimmune diseases are expected to post the strongest 19.22% CAGR, outpacing all other indications.

How quickly are humanized antibodies expanding?

Humanized variants are advancing at an 18.02% CAGR, the fastest rate among source categories.

Why are specialty and ambulatory centers gaining importance?

Subcutaneous formulations such as Tecentriq Hybrenza cut chair time to about seven minutes, enabling convenient outpatient or at-home administration and driving a 15.98% CAGR for these centers.

Page last updated on: