Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

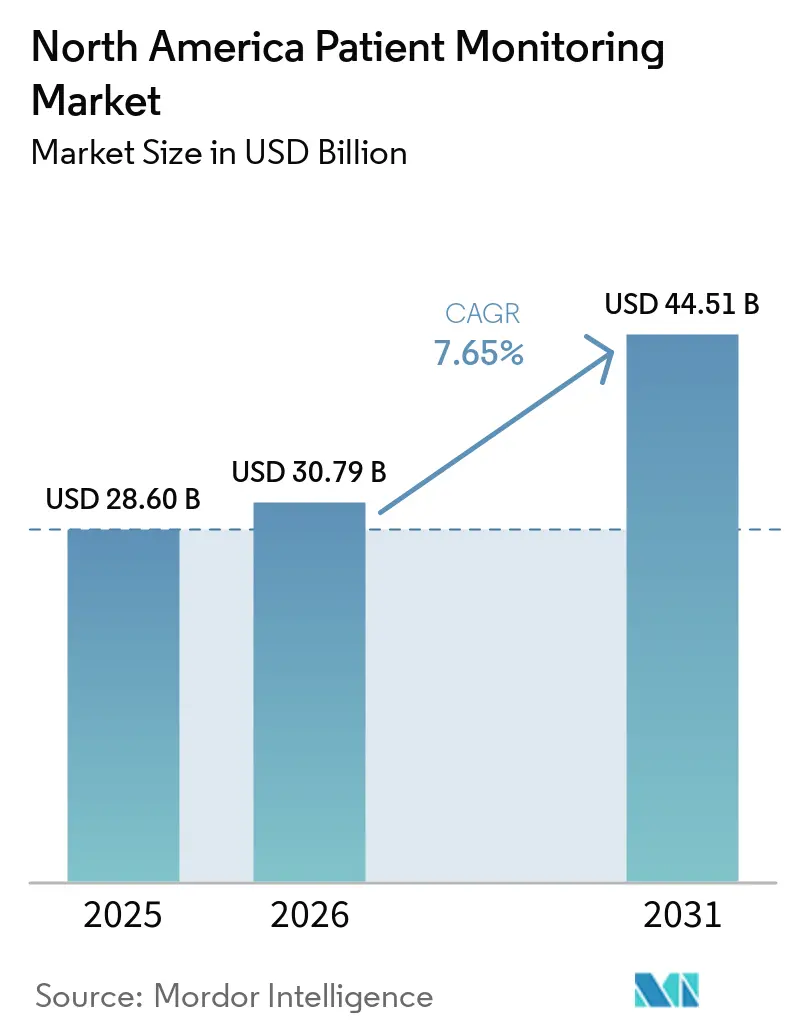

| Base Year Market Size (2025) | USD 28.60 Billion |

| Market Size (2026) | USD 30.79 Billion |

| Market Size (2031) | USD 44.51 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

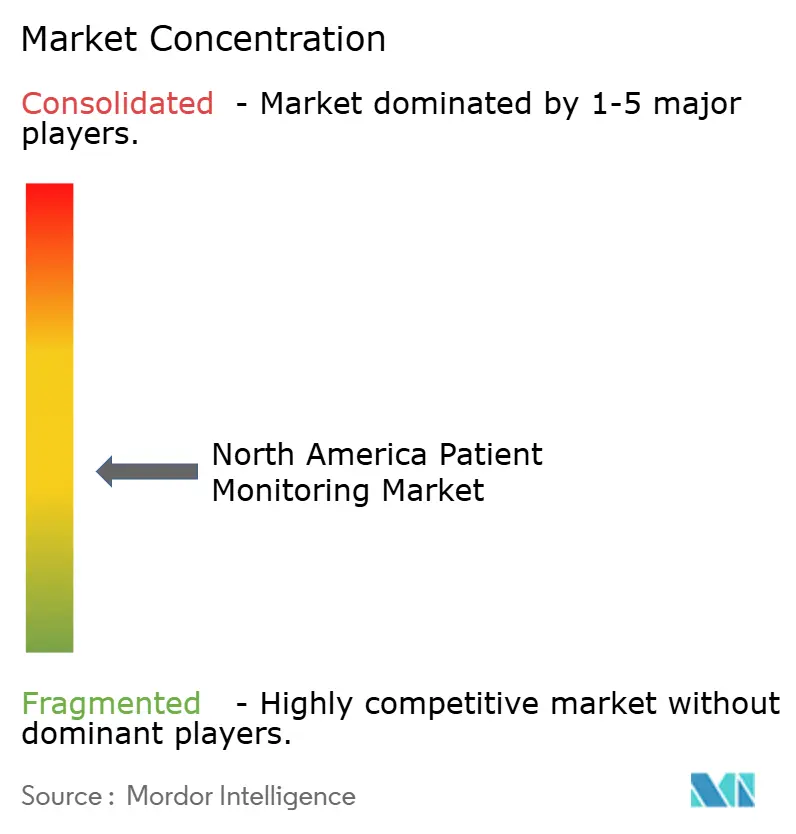

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Patient Monitoring Market Analysis by Mordor Intelligence

The North America Patient Monitoring Market size was valued at USD 28.60 billion in 2025 and is estimated to grow from USD 30.79 billion in 2026 to reach USD 44.51 billion by 2031, at a CAGR of 7.65% during the forecast period (2026-2031).

The North America patient monitoring market is shifting from episodic bedside checks to continuous, algorithm-driven surveillance that covers hospital wards, ambulatory centers, and private homes. Revised U.S. Medicare RPM codes for 2026 are widening reimbursement, while Canada’s Connected Care Act secures parity payments for virtual services, together scaling volumes across the North America patient monitoring market. Device revenues still dominate, but managed services are gaining ground as health systems sign multi-year, equipment-as-a-service contracts that bundle installation, data integration, and triage. Diabetes-focused wearables and single-use sensors are broadening consumer access and reducing infection-control burdens, and AI-enabled early-warning algorithms are helping overwhelmed clinicians filter non-actionable alarms.

Key Report Takeaways

- By type, devices captured 80.18% of the North America patient monitoring market share in 2025, while services are forecast to expand at an 8.22% CAGR through 2031.

- By application, cardiology led with 37.21% revenue share in 2025; diabetes management is projected to grow at a 12.65% CAGR to 2031.

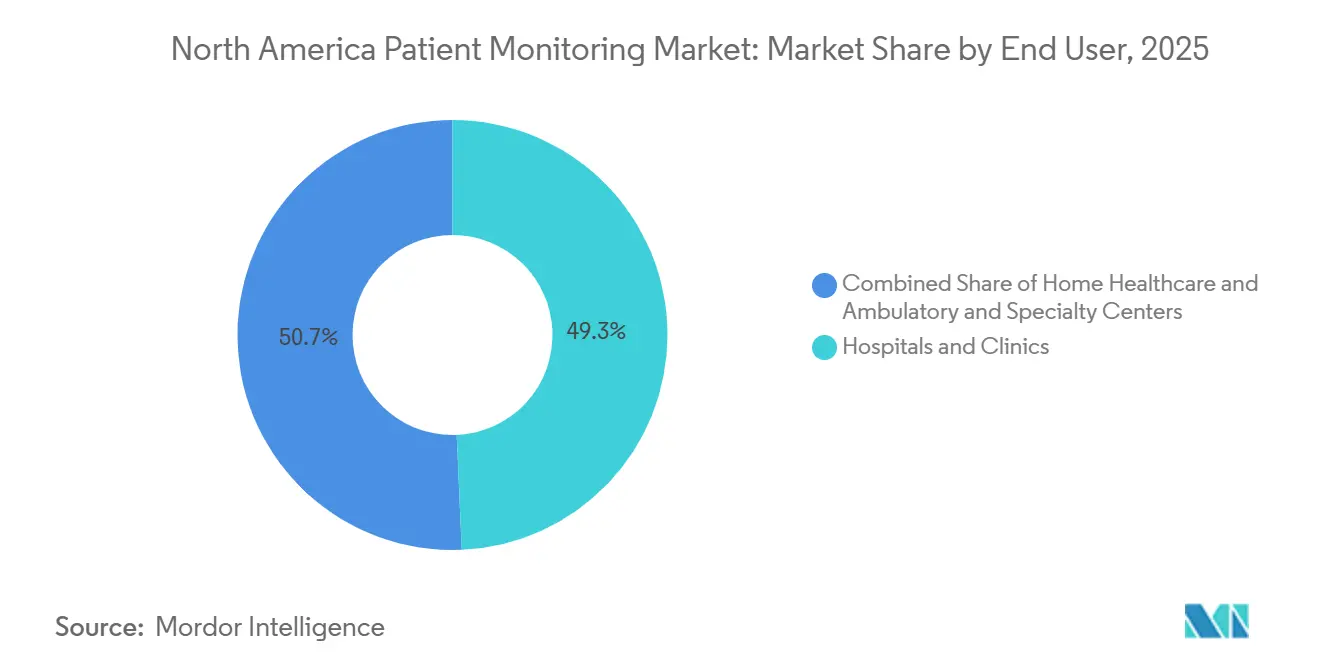

- By end user, hospitals and clinics held 49.32% of spending in 2025; home healthcare is advancing at an 11.12% CAGR through 2031.

- By country, the United States commanded 75.21% of 2025 revenue, whereas Mexico is expanding at a 9.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Patient Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Incidence of Chronic & Lifestyle Diseases Surging | +1.8% | United States, Canada (urban centers) | Long term (≥ 4 years) |

| Ageing Population & Reimbursement Expansion | +1.5% | United States (Medicare), Canada (provincial programs) | Medium term (2-4 years) |

| Post-COVID Preference for Home & Remote Monitoring | +1.3% | Global, with highest adoption in United States | Short term (≤ 2 years) |

| AI-Enabled Early-Warning Analytics | +1.2% | United States (academic medical centers), Canada (pilot sites) | Medium term (2-4 years) |

| Shift Toward Single-Use Sensors | +0.9% | United States, Mexico (cost-sensitive segments) | Short term (≤ 2 years) |

| Federal RPM Code Revisions | +0.7% | United States (Medicare fee-for-service) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Incidence of Chronic & Lifestyle Diseases Surging

More than 133 million U.S. adults live with chronic illness, and 6 in 10 manage at least one condition, driving sustained demand for round-the-clock monitoring[1]Centers for Disease Control and Prevention, “National Center for Chronic Disease Prevention,” cdc.gov. Prevalence climbs further in the 85-plus cohort, where multi-morbidity reached 12.3% in 2024, intensifying care complexity. Continuous glucose monitors illustrate the trend: Dexcom’s Stelo sensor broadened eligibility beyond insulin users, contributing to a 21.6% revenue jump to USD 1.21 billion in Q3 2025. Abbott’s Libre Rio and Lingo followed, pushing adoption into the 37 million U.S. Type 2 population. Each new chronic-care enrollee expands the North America patient monitoring market, because payers now reimburse multi-condition oversight under bundled RPM codes.

Ageing Population & Reimbursement Expansion

Seniors will form 21.6% of North America’s population by 2030, and they consume triple the monitoring resources of younger adults. CMS lifted CPT 99457 to USD 64.41 and added CPT 99458 at USD 51.52 for every extra 20 minutes of review, letting clinics bill for layered comorbidity tracking. Canada’s Connected Care Act mirrors the move, while Ontario earmarks CAD 832 million (USD 615 million) annually for digital care. TELUS Health’s province-wide RPM program already enrolls thousands, demonstrating how reimbursement certainty converts pilots into mainstream workflows.

Post-COVID Preference for Home & Remote Monitoring

The pandemic normalized teleconsults, and attrition rates stay low where reimbursement is intact. A 2025 UC Irvine study showed only 19% of telehealth users dropped services, largely for payment gaps rather than dissatisfaction. Hospitals are embedding monitoring into post-discharge bundles; University Hospitals in Ohio is rolling out Masimo’s Root across 1,500 beds by fall 2026, cutting nurse travel time and compressing alarm response windows. Philips signed a decade-long, equipment-as-a-service pact with Hoag Memorial in 2025, swapping capex for predictable opex. These deals reinforce the North America patient monitoring market by keeping surveillance active beyond hospital walls.

AI-Enabled Early-Warning Analytics

FDA-cleared algorithms now anticipate organ failure hours ahead of vital-sign thresholds. AgileMD’s eCART forecasts sepsis, Ceribell spots neonatal seizures, and Tempus AI’s ECG-Low EF finds heart-failure candidates from routine ECGs. Becton Dickinson’s HemoSphere Alta suggests fluid or vasopressor adjustments in real time. Such tools democratize critical-care insight for community hospitals and amplify clinical productivity, propelling the North America patient monitoring market toward higher-value analytics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Provider Workflow Resistance & Training Burden | -0.8% | United States (community hospitals), Canada (rural facilities) | Short term (≤ 2 years) |

| High Capital & Integration Costs | -0.7% | United States, Mexico (public hospitals) | Medium term (2-4 years) |

| Cyber-Insurance & Section-524B Compliance | -0.5% | United States, Canada (ISO 27001 jurisdictions) | Short term (≤ 2 years) |

| Clinician Alert-Fatigue | -0.6% | United States (large academic medical centers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Provider Workflow Resistance & Training Burden

Alarm overload erodes trust: a UPMC audit logged 65.6 million alerts across wards, 88% technical rather than physiologic, fueling burnout in 40-50% of staff[2]University of Pittsburgh Medical Center, “Alarm Fatigue Study,” upmc.com. Every platform introduces new dashboards, thresholds, and escalation drills, requiring months of coaching. Emory Healthcare’s 2025 virtual-nursing project came with a six-month curriculum and extra staffing. Small hospitals lack volume to justify centralized command centers, limiting adoption and tempering short-run gains in the North America patient monitoring market.

High Capital & Integration Costs

Multiparameter monitors list at USD 10,000-50,000 each; a 500-bed refresh can exceed USD 25 million before networking or middleware. Parrish Healthcare spent USD 25 million on EHR integration in 2025, dedicating a year to connect disparate devices. Mexico’s public facilities still use early-2000s monitors and depend on federal subsidies for refresh cycles. Leasing eases capex but locks buyers into long contracts, delaying pivots to emergent technologies and restraining the North America patient monitoring market in the mid-term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Outpace Hardware as Bundled Contracts Proliferate

Hardware generated 80.18% of 2025 revenue, yet service lines are forecast to deliver an 8.22% CAGR, the quickest in the North America patient monitoring market. Hoag Memorial’s decade-long lease with Philips shows why: hospitals spread payments, lock in upgrades, and secure analytics without large upfront checks. Managed monitoring, middleware development, and triage outsourcing now command premium pricing, turning services into a strategic hedge against hardware commoditization. The North America patient monitoring market size for services is projected to expand faster than devices as more systems convert capex to opex.

Analytics and command-center operations deepen stickiness. West Tennessee Healthcare added 12 intensivists to staff its eICU in 2025, giving rural affiliates 24/7 oversight. Middleware spending, USD 25 million at Parrish Healthcare, shows that interoperability remains a bottleneck. As proprietary data standards fade, vendors able to bundle cloud hosting, cybersecurity, and AI analytics win renewals, reinforcing vendor lock-in across the North America patient monitoring market.

By Application: Diabetes Management Accelerates as OTC CGMs Democratize Access

Cardiology owned 37.21% revenue in 2025, but diabetes devices are outpacing with a 12.65% CAGR. Dexcom’s Stelo and Abbott’s Libre Rio brought continuous glucose monitoring to non-insulin Type 2 users, enlarging addressable demand. Medtronic’s MiniMed 780G, shipping since December 2025, merges Abbott’s sensor and automated insulin dosing, inching toward closed-loop care. The North America patient monitoring market size for diabetes solutions is projected to climb steeply as OTC channels and pharmacy distribution lower entry barriers.

Neurology and respiratory sub-segments also gain momentum. Ceribell’s rapid EEG opens seizure detection to emergency settings, while ResMed’s AI-driven CPAP improves adherence. Fetal-monitoring AI at NYC Health + Hospitals aims to reduce cesareans. Such diversification cushions vendors against cardiology saturation and boosts overall revenue resilience within the North America patient monitoring market.

By End User: Home Healthcare Gains as Post-Acute Pathways Shift Upstream

Hospitals and clinics captured 49.32% of 2025 spending, reflecting heavy investment in high-acuity monitoring and alarm-management overhauls. Yet home care is projected to grow 11.12% annually as Medicare expands RPM billing and providers chase readmission penalties. TELUS Health’s Ontario rollout underscores the model: tracking blood pressure, glucose, and weight outside hospital walls reduced specialist referrals. The North America patient monitoring market share for home care is set to widen as value-based reimbursement rewards continuous surveillance at lower acuity.

Ambulatory centers adopt single-use sensors to speed patient turnover; Philips’ disposable SpO₂ probes remove sterilization delays. Dialysis chains, rehab facilities, and outpatient surgery centers deliver predictable, procedure-based volumes that entice vendors to tailor lightweight, Wi-Fi-enabled devices. Broader end-user diversity stabilizes revenue streams in the North America patient monitoring industry.

Geography Analysis

The United States held 75.21% of 2025 revenue, underpinned by Medicare RPM expansion and a rapid cadence of FDA clearances. High-profile deals, Becton Dickinson’s USD 4.2 billion Critical Care acquisition and Boston Scientific’s USD 14.5 billion Penumbra buy, showcase capital depth and reinforce domestic dominance. OIG’s 2025 fraud probes temper growth but ultimately legitimize the North America patient monitoring market by rooting out abusive billing.

Canada benefits from policy coherence. Bill C-72 mandates reimbursement parity, and CAD 832 million (USD 615 million) in annual federal-provincial funding builds province-wide digital infrastructure. National interoperability standards accelerate cross-border device launches, and TELUS Health’s nationwide RPM enrollment exemplifies public-private alignment. Growth is steady, if slower than the U.S., supported by a single-payer lens that emphasizes outcomes.

Mexico, expanding at 9.53% CAGR, is the bright spot. COFEPRIS slashed approval timelines to as little as 20 days, letting multinationals synch launches with U.S. rollouts[3]COFEPRIS, “Medical Device Fast-Track Guidance,” gob.mx/cofepris. Public-hospital upgrades, financed through federal subsidies, target monitors purchased in the early 2000s. Disposable sensors resonate in cash-constrained wards, sidestepping sterilization costs and speeding turnover. The policy and procurement shifts combine to enlarge the addressable pie inside the North America patient monitoring market.

Competitive Landscape

Market concentration is moderate: Medtronic, Philips, GE HealthCare, Abbott, and Masimo together hold a sizable share, yet dozens of niche players fragment the tail. Scale leaders pursue vertical integration, Becton Dickinson’s hemodynamic plus infusion portfolio and Boston Scientific’s neurovascular gambit bundle adjacent modalities into stickier platforms. Medtronic and Philips announced a 2025 partnership to explore interoperable ecosystems, foreshadowing cross-vendor data exchanges.

Technology differentiation centers on AI and disposability. Philips’ Telemetry Monitor 5500, cleared in 2025, halves false arrhythmia alarms, while ResMed’s Smart Comfort CPAP tunes pressure nightly through AI analytics. iRhythm’s September 2024 BioIntelliSense license and July 2025 Lucem Health partnership pivot its Zio service from passive logging to predictive alerting. Section 524B cybersecurity rules raise entry barriers, likely nudging smaller suppliers toward merger or niche specialization, further shaping the North America patient monitoring market.

North America Patient Monitoring Industry Leaders

Koninklijke Philips N.V.

Medtronic plc

Abbott Laboratories

Masimo Corporation

GE HealthCare Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Royal Philips unveiled a new patient-monitoring innovation roadmap aimed at easing workforce shortages and improving care coordination.

- September 2025: Baxter International launched the Welch Allyn Connex 360 Vital Signs Monitor in the United States.

North America Patient Monitoring Market Report Scope

As per the scope of this report, patient monitoring devices are monitoring devices that continuously monitor the patient's vital parameters, like blood pressure and heart rates, by using a medical monitor and collecting medical (and other) data from individuals.

The segmentation for the North America patient monitoring market is categorized by type, including devices such as hemodynamic monitoring devices, neuromonitoring devices, cardiac monitoring devices, multi-parameter monitors, respiratory monitoring devices, remote patient monitoring devices, and other devices; by service, comprising installation and maintenance services, training and education services, remote monitoring and telehealth services, data integration and interoperability services, analytics and reporting services, and managed monitoring operations and triage services; by application, covering cardiology, neurology, respiratory, diabetes management, fetal and neonatal, weight-management and fitness, and other applications; by end user, including hospitals and clinics, home healthcare, and ambulatory and specialty centers; and by country, focusing on the United States, Canada, and Mexico. The market forecasts are provided in terms of value (USD).

By Type

| By Device | Hemodynamic Monitoring Devices |

| Neuromonitoring Devices | |

| Cardiac Monitoring Devices | |

| Multi-Parameter Monitors | |

| Respiratory Monitoring Devices | |

| Remote Patient Monitoring Devices | |

| Other Devices | |

| By Service | Installation & Maintenance Services |

| Training & Education Services | |

| Remote Monitoring & Telehealth Services | |

| Data Integration & Interoperability Services | |

| Analytics & Reporting Services | |

| Managed Monitoring Operations & Triage Services |

By Application

| Cardiology |

| Neurology |

| Respiratory |

| Diabetes Management |

| Fetal & Neonatal |

| Weight-Management & Fitness |

| Other Applications |

By End User

| Hospitals & Clinics |

| Home Healthcare |

| Ambulatory & Specialty Centers |

By Country

| United States |

| Canada |

| Mexico |

| By Type | By Device | Hemodynamic Monitoring Devices |

| Neuromonitoring Devices | ||

| Cardiac Monitoring Devices | ||

| Multi-Parameter Monitors | ||

| Respiratory Monitoring Devices | ||

| Remote Patient Monitoring Devices | ||

| Other Devices | ||

| By Service | Installation & Maintenance Services | |

| Training & Education Services | ||

| Remote Monitoring & Telehealth Services | ||

| Data Integration & Interoperability Services | ||

| Analytics & Reporting Services | ||

| Managed Monitoring Operations & Triage Services | ||

| By Application | Cardiology | |

| Neurology | ||

| Respiratory | ||

| Diabetes Management | ||

| Fetal & Neonatal | ||

| Weight-Management & Fitness | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Home Healthcare | ||

| Ambulatory & Specialty Centers | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America patient monitoring market in 2026?

The North America patient monitoring market size stands at USD 30.79 billion in 2026.

What is the projected growth rate for the market to 2031?

The market is forecast to expand at a 7.65% CAGR between 2026 and 2031.

Which segment is growing fastest?

Diabetes monitoring devices are expected to post a 12.65% CAGR through 2031 as over-the-counter CGMs reach non-insulin Type 2 users.

Why are services outpacing hardware sales?

Health systems favor multi-year, equipment-as-a-service contracts that bundle analytics, integration, and triage, driving an 8.22% CAGR for services through 2031.

Which country will grow fastest in North America?

Mexico is projected to advance at a 9.53% CAGR to 2031 due to streamlined COFEPRIS approvals and federal hospital upgrades.

How is AI affecting competitive dynamics?

FDA-cleared early-warning algorithms and machine-learning-driven alarm reduction are becoming key differentiators among leading vendors, spurring acquisitions and strategic alliances.

Page last updated on: