Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 63.61 Billion |

| Market Size (2031) | USD 89.39 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

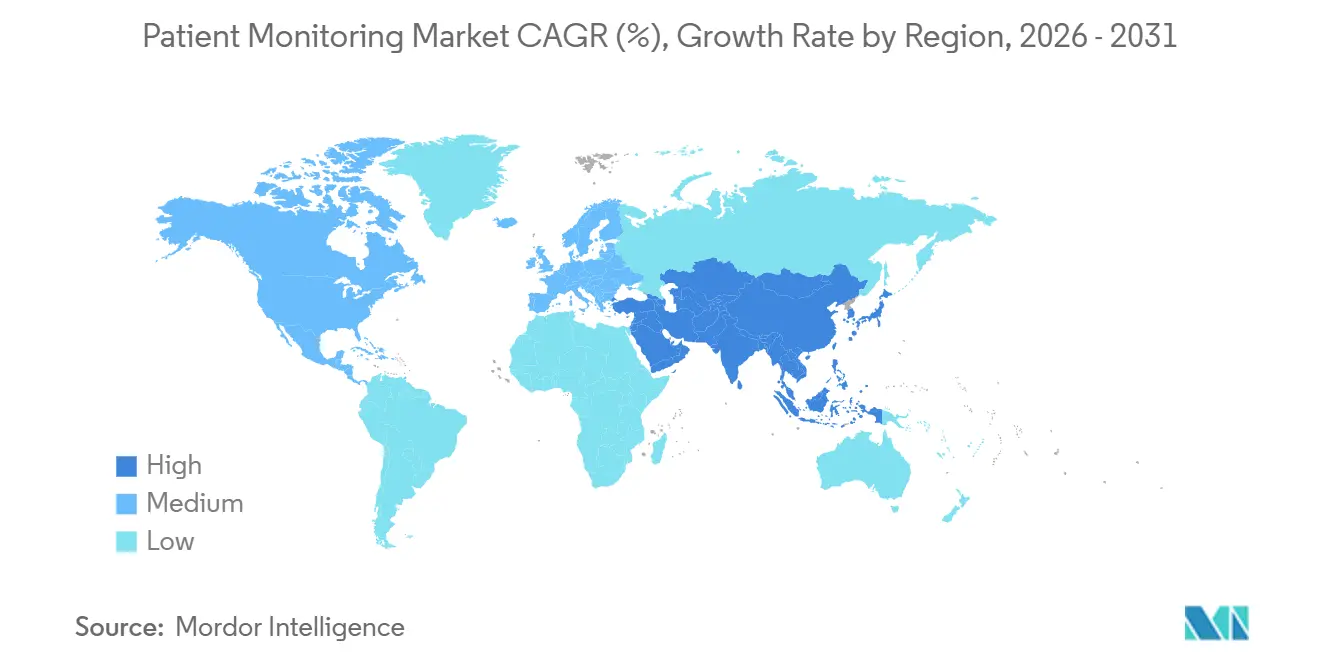

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

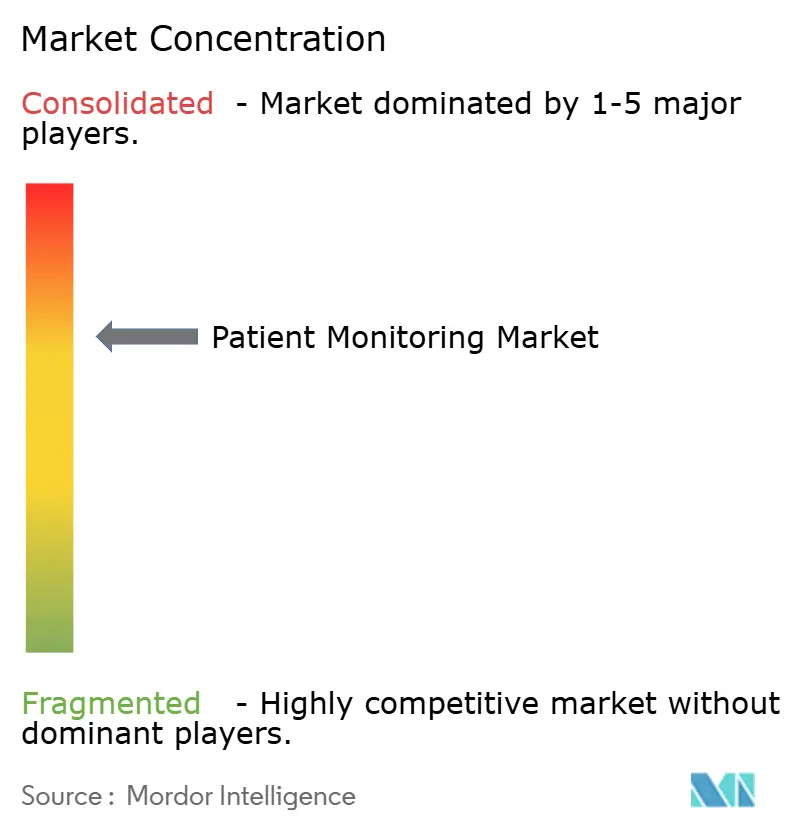

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Monitoring Market Analysis by Mordor Intelligence

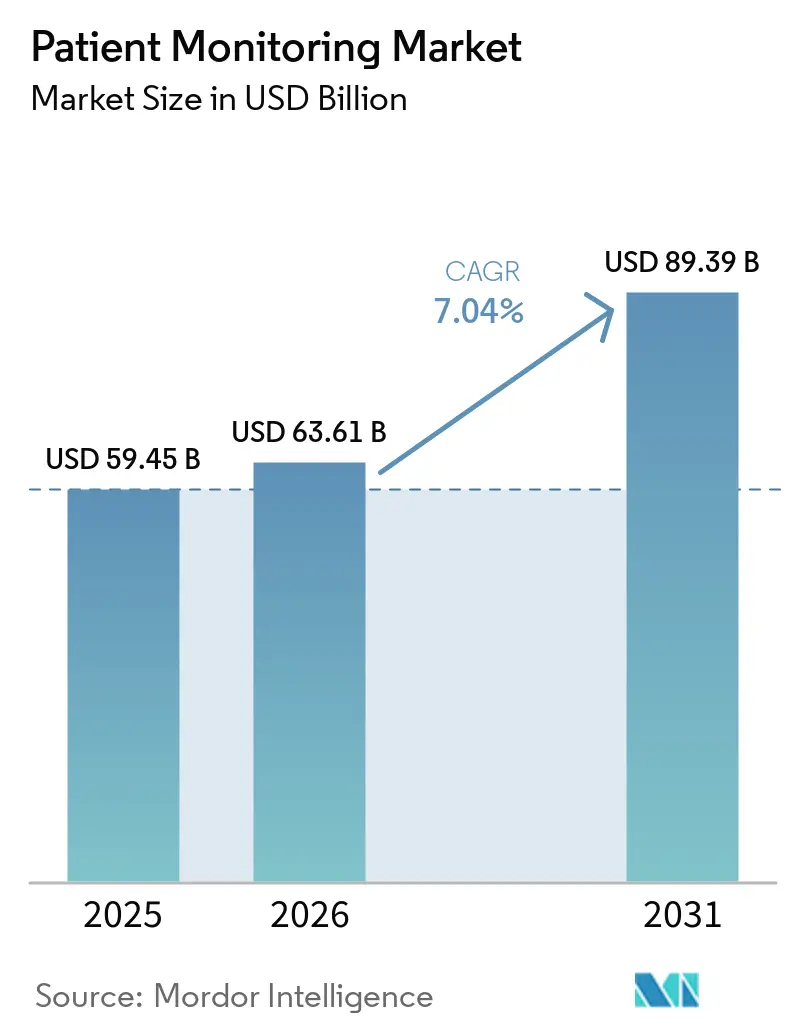

The Patient Monitoring Market size was valued at USD 59.45 billion in 2025 and is estimated to grow from USD 63.61 billion in 2026 to reach USD 89.39 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031).

Reimbursement reforms, edge-computing architectures, and satellite-IoT connectivity are expanding continuous surveillance beyond hospital walls, shifting revenue mix toward subscription models and managed services. Revised Remote Physiologic Monitoring (RPM) codes that cut the billable-time threshold to 10–19 minutes have doubled the addressable patient pool for chronic-condition management in the United States. National digital-health infrastructure programs in China, India, and Japan, together with virtual-ward rollouts in the United Kingdom and Australia, are accelerating adoption in Asia-Pacific. Meanwhile, FDA Section 524B cybersecurity rules are elevating compliance barriers, favoring vendors with mature regulatory footprints and prompting hospitals to reassess total cost of ownership for connected fleets [1]FDA, “Cybersecurity in Medical Devices: Quality System Considerations,” fda.gov. Edge-enabled wearables that execute inference on-device are lowering data-latency below 20 milliseconds, enabling real-time arrhythmia detection while meeting data-sovereignty mandates in the European Union and China. Collectively, these forces position the patient monitoring market for sustained mid-single-digit expansion through 2031.

Key Report Takeaways

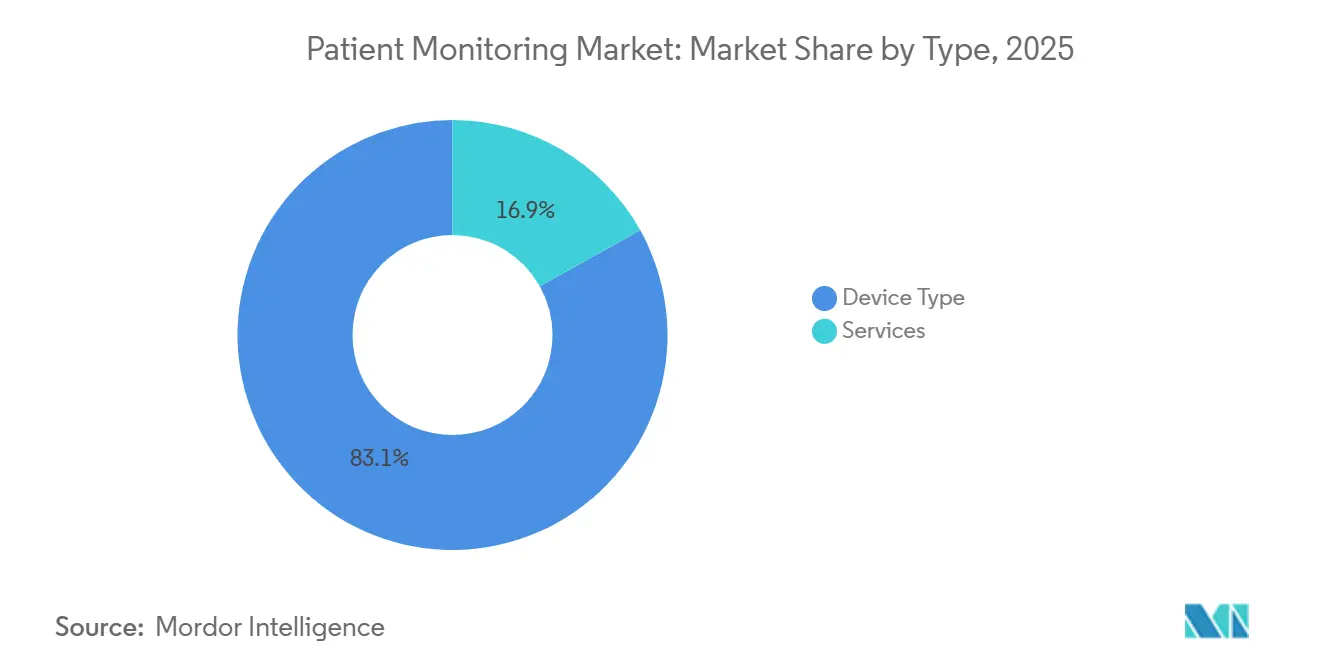

- By type, device offerings held 83.1% of the patient monitoring market share in 2025, while services are advancing at a 9.53% CAGR to 2031.

- By application, cardiology led with an 18.2% share of the patient monitoring market size in 2025, whereas diabetes and metabolic monitoring are projected to expand at a 10.12% CAGR through 2031.

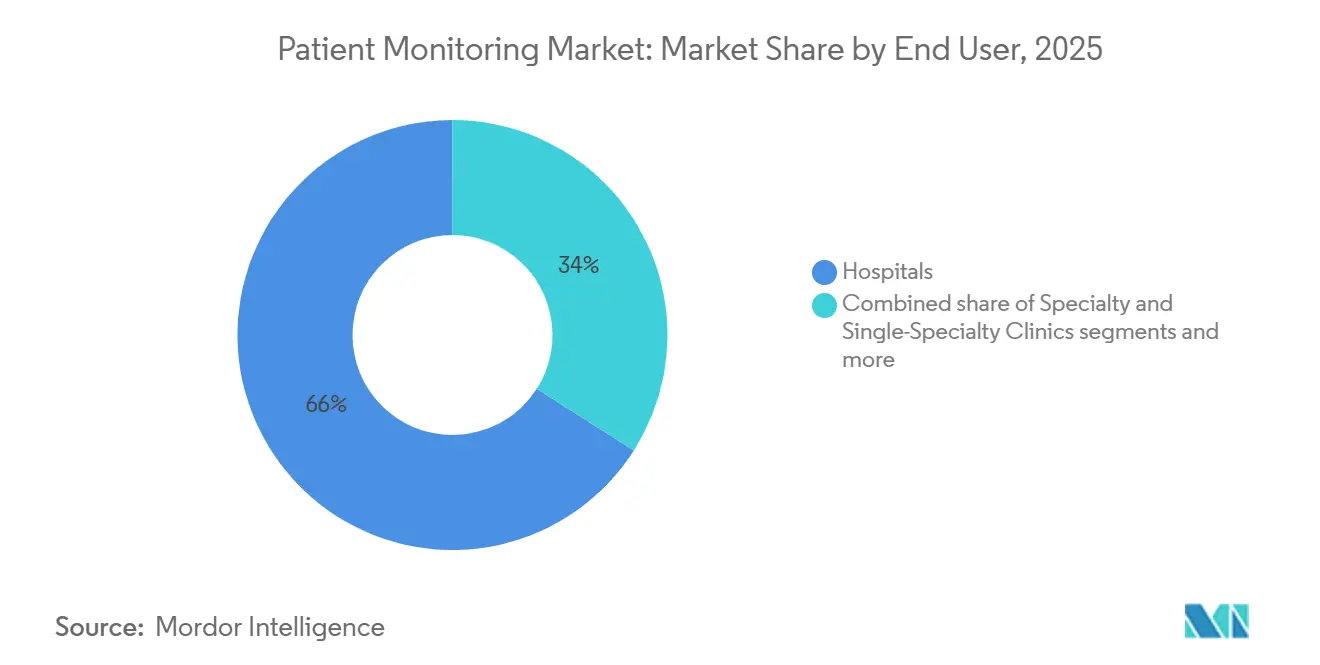

- By end-user, hospitals commanded 65.98% revenue share in 2025; home-healthcare providers recorded the highest expected CAGR at 11.21% to 2031.

- By geography, North America captured 41.2% of 2025 revenue, while Asia-Pacific is forecast to grow at a 10.99% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Patient Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in chronic-disease prevalence & comorbidity clusters | +1.2% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Accelerating shift to hospital-at-home & virtual wards | +1.5% | North America, the United Kingdom, and Australia | Medium term (2-4 years) |

| AI-enabled early-warning systems lowering adverse-event costs | +0.9% | North America & the European Union | Medium term (2-4 years) |

| Reimbursement expansion for RPM | +1.8% | United States, Germany, Japan | Short term (≤ 2 years) |

| Edge-computing wearables are reducing sub-20 ms latency | +0.6% | Global, early uptake in North America & South Korea | Long term (≥ 4 years) |

| Satellite-IoT backhaul unlocking monitoring in black spots | +0.4% | Rural North America, remote Australia, pilot zones in sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Chronic-Disease Prevalence & Comorbidity Clusters

Cardiovascular diseases caused 17.9 million deaths in 2021, and the International Diabetes Federation projects 783 million adults living with diabetes by 2045, a 46% surge that will overwhelm episodic clinic care [2]World Health Organization, “Cardiovascular Diseases Fact Sheet,” who.int. Multiparameter hubs that simultaneously track glucose, blood pressure, and weight are therefore gaining favor over single-parameter devices. The CDC reported in 2024 that 6 in 10 U.S. adults have at least one chronic condition and 4 in 10 have two or more, underscoring demand for continuous surveillance outside hospitals. Value-based contracts penalizing readmissions are pushing providers to deploy post-discharge monitoring that flags decompensation early. As interoperability improves, integrated platforms are expected to crowd out legacy stand-alone monitors within the patient monitoring market.

Accelerating Shift to Hospital-at-Home & Virtual Wards

CMS transitioned its Acute Hospital Care at Home waiver into a permanent pathway in 2025, covering 290 hospitals across 37 states. The United Kingdom scaled virtual wards to more than 10,000 beds by mid-2024, freeing acute-care capacity. Hospital-at-home models require rugged, patient-operated devices that can transmit vitals via cellular or satellite gateways without onsite clinicians. Philips and GE HealthCare now bundle monitors, connectivity, and managed triage into per-patient subscriptions, converting capital expenditure to operating expense. As reimbursement converges across payers, adoption is widening among mid-size community hospitals, thereby broadening the patient monitoring market footprint

AI-Enabled Early-Warning Systems Lowering Adverse-Event Costs

Predictive analytics that flag sepsis, respiratory failure, or cardiac arrest six to twelve hours before deterioration lower ICU length of stay by up to two days, saving hospitals significant labor and bed-capacity costs. The FDA’s 2025 guidance on change-control plans now lets vendors update AI algorithms without fresh 510(k) submissions, speeding iteration.

Early movers such as Epic’s in-EHR sepsis model and GE HealthCare’s AI Command Center are demonstrating measurable ROI, encouraging chief financial officers to expand budgets for analytics modules. As hospital systems integrate bedside streams into unified dashboards, the global patient monitoring market gains a data-layer moat that is difficult for new entrants to replicate.

Reimbursement Expansion for Remote Physiologic Monitoring (RPM)

The January 2026 RPM code revisions slashed the minimum interaction time to 10–19 minutes and created a 2–15-day code that covers post-surgical surveillance, effectively doubling eligible beneficiaries in the United States. Germany’s DiGA pathway had listed more than 50 RPM apps by 2024, and Japan added remote COPD and heart-failure monitoring to its fee schedule in 2024. These decisions elevate RPM from a telehealth add-on to mainstream therapy management. Vendors that master payer contracting and prior authorization stand to capture an outsized share in the patient monitoring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity insurance premiums | -0.8% | North America & European Union | Short term (≤ 2 years) |

| High total-cost-of-ownership in low-resource settings | -1.1% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Fragmented device-data standards | -0.7% | Global, acute in multi-vendor U.S. hospitals | Medium term (2-4 years) |

| Lithium-supply volatility raising battery costs | -0.5% | Global, pronounced in wearables and patch-based monitors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Cybersecurity Insurance Premiums for Connected Devices

FDA Section 524B rules, effective June 2025, now demand software bills of materials and threat-modeling for every networked device, increasing compliance spend and driving insurance carriers to hike healthcare cyber-premiums 15–25%. For a 500-bed hospital, annual coverage can reach USD 300,000, exceeding amortized hardware costs over a seven-year cycle. Smaller hospitals, lacking full-time security staff, either delay purchases or accept higher risk, curbing near-term orders in the market and slowing patient monitoring market size expansion.

High Total-Cost-of-Ownership in Low-Resource Settings

Median public-health spend in sub-Saharan Africa is only USD 50 per capita, leaving scant budget for devices that require cellular data plans and cloud storage. Grant-funded pilots often fail when connectivity subsidies expire, creating monitor graveyards. Vendors are field-testing offline-capable units that sync intermittently over Wi-Fi, yet the loss of real-time alerting reduces clinical value. Unless tiered-pricing or donation programs mature, low-income regions will lag, trimming global patient monitoring market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Outpace Hardware as Managed Triage Scales

Devices retained 83.1% of the patient monitoring market share in 2025, supported by large ICU and step-down installed bases. However, services revenue spanning installation, data integration, analytics, and managed triage is forecast to grow 9.53% from 2026 to 2031, outpacing the overall patient monitoring market by 2.5 percentage points. Hospital executives prefer subscription bundles that convert capital outlays into predictable operating costs, and vendors such as GE HealthCare and Philips now tie monthly fees to active-patient counts rather than hardware units.

Wearable and patch-based monitors are expanding fastest within hardware, propelled by over-the-counter CGMs like Dexcom Stelo and Abbott Libre Rio that address wellness and prediabetes segments. Remote hubs face commoditization as smartphones offer built-in Bluetooth and LTE, pushing value toward cloud analytics. Consequently, the patient monitoring market size for device-only contracts is expected to plateau, while as-a-service models capture incremental spend.

By Application: OTC CGMs Propel Diabetes & Metabolic Monitoring

Cardiology accounted for 18.2% of the global patient monitoring market 2025 revenue, yet diabetes and metabolic solutions are projected to deliver the highest CAGR at 10.12% through 2031. FDA clearances for OTC CGMs removed prescription barriers, unlocking millions of prediabetic and wellness users and enlarging the patient monitoring market size for metabolic tracking.

Respiratory monitoring is also rebounding as connected positive-airway-pressure devices stream adherence metrics to clinicians. Maternal-fetal devices such as Masimo Stork add mobility to labor monitoring, but remain niche. Neurology is evolving toward rapid-response wireless EEG systems that compress diagnosis time from hours to minutes, attracting emergency departments seeking throughput gains. As new use cases mature, application diversity will insulate the patient monitoring market against single-indication slowdowns.

By End-User: Home-Healthcare Providers Lead Growth Curve

Hospitals maintained 65.98% of revenue in 2025, leveraging capital budgets to deploy multiparameter monitors and AI command centers. Home-healthcare providers, however, are forecast to record an 11.21% CAGR from 2026 to 2031 as permanent hospital-at-home reimbursement scales nationally. Consumers now expect the same real-time oversight in their living rooms that they once received in step-down units, expanding the patient monitoring market across residential settings.

Specialty clinics deploy implantable loop recorders and connected spirometers to manage l arger patient panels remotely, while ambulatory surgery centers send post-operative monitoring kits home to avert complications. Long-term-care facilities remain underpenetrated due to reimbursement gaps, yet pilot programs in Singapore have cut emergency transfers by up to 40%. Once payers recognize these savings, adoption could surge, further diversifying end-user demand within the patient monitoring market.

Geography Analysis

North America generated 41.2% of 2025 revenue, buoyed by CMS RPM reforms, Section 524B cybersecurity mandates, and a robust hospital-at-home infrastructure. The region’s high average selling prices and payer willingness to reimburse managed services underpin its outsized contribution to the patient monitoring market size.

Europe holds significant share, supported by Germany’s DiGA reimbursement pathway and the United Kingdom’s virtual-ward expansion. EU Medical Device Regulation enforcement raised compliance costs but improved post-market surveillance, reinforcing trust among clinicians. Despite macroeconomic pressures, statutory insurers continue to fund connected-care pilots, stabilizing demand.

Asia-Pacific is the growth engine, forecast to post a 10.99% CAGR from 2026 to 2031. China’s NMPA approved more than 50 AI-enabled monitors in 2024-2025, while India liberalized telemedicine and Japan expanded coverage for remote COPD and heart-failure monitoring. These policy shifts, coupled with aging demographics, enlarge the patient monitoring market across populous economies. Middle East and Africa remain early-stage, yet Gulf Cooperation Council investments in smart hospitals are expected to seed future demand. South America shows selective uptake, led by private payers in Brazil.

Competitive Landscape

The patient monitoring market is moderately fragmented. GE HealthCare, Philips, and Nihon Kohden defend hospital contracts through multi-year service agreements and deep integration with electronic health records. Wearable specialists Dexcom, Abbott, and Masimo target ambulatory and consumer tiers, leveraging direct-to-consumer channels and employer wellness contracts. Consumer-electronics leaders Apple, Garmin, and Samsung add substitution pressure by embedding health sensors into mainstream wearables, forcing medical-device makers to differentiate on FDA clearance and reimbursement eligibility.

Strategic activity centers on vertical integration into managed services. GE HealthCare extended its Mindray alliance to ambulatory surgery centers in 2026, while Philips secured interoperability pacts with Dräger and Hamilton to consolidate ICU device data. Startups such as VitalConnect and Spire Health deploy adhesive multiparameter patches that challenge bedside monitors for step-down and hospital-at-home use cases. Investment in satellite-enabled connectivity and edge inference continues, as evidenced by more than 200 related patents issued in 2024-2025 [3]U.S. Patent and Trademark Office, “Wearable Biosensor Patents 2024-2025,” uspto.gov.

Regulatory compliance is emerging as a competitive moat. Section 524B cybersecurity filings and EU MDR technical documentation demand specialized expertise that smaller entrants may lack. As consolidation accelerates, leading vendors with global regulatory infrastructure are positioned to capture incremental patient monitoring market share.

Patient Monitoring Industry Leaders

Abbott Laboratories

GE Healthcare

Becton, Dickinson and Company

Dexcom, Inc

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Medtronic secured FDA 510(k) clearance for its MiniMed Go smart MDI system, integrating Abbott’s Instinct sensor with InPen for real-time dose guidance.

- January 2026: Medtronic expanded a strategic partnership with Mindray to supply monitoring solutions to U.S. ambulatory surgery centers.

- July 2025: Philips signed interoperability agreements with Dräger, Hamilton Medical, Getinge, and B. Braun to plug their critical-care devices into the Philips monitoring ecosystem.

Global Patient Monitoring Market Report Scope

As per the scope of the report, patient monitoring is the continuous or repeated observation of a patient's physiological functions to guide clinical decisions and evaluate the effectiveness of medical interventions. These systems use advanced technology to record vital signs, including heart rate, blood pressure, respiratory rate, body temperature, and blood oxygen saturation (SpO2), providing healthcare professionals with real-time, accurate data.

The patient monitoring market is segmented by type, application, end-user, and geography. By type, it is segmented into devices (multiparameter vital-signs monitors, cardiac monitoring devices, respiratory monitoring devices, neuro-monitoring devices, fetal & neonatal monitoring devices, hemodynamic & pressure monitors, wearable & patch-based monitors, remote patient monitoring hubs & gateways, and AI-driven predictive analytics modules) and services (installation & maintenance, training & education, RPM & telehealth services, data integration & interoperability, analytics & reporting, and managed monitoring & triage operations). By application, the market is segmented into cardiology, respiratory, and neurology, diabetes & metabolic, maternal & neonatal, critical care surveillance, and others. By End users, the market is segmented into hospitals, specialty & single-specialty clinics, ambulatory surgical centers, home-healthcare providers, and long-term care & assisted-living facilities.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

By Type

| Device | Multiparameter Vital-Signs Monitors |

| Cardiac Monitoring Devices | |

| Respiratory Monitoring Devices | |

| Neuro-Monitoring Devices | |

| Fetal & Neonatal Monitoring Devices | |

| Hemodynamic & Pressure Monitors | |

| Wearable & Patch-Based Monitors | |

| Remote Patient Monitoring Hubs & Gateways | |

| AI-Driven Predictive Analytics Modules | |

| Services | Installation & Maintenance |

| Training & Education | |

| RPM & Telehealth Services | |

| Data Integration & Interoperability | |

| Analytics & Reporting | |

| Managed Monitoring & Triage Operations |

By Application

| Cardiology |

| Respiratory |

| Neurology |

| Diabetes & Metabolic |

| Maternal & Neonatal |

| Critical Care Surveillance |

| Others |

By End-User

| Hospitals |

| Specialty & Single-Specialty Clinics |

| Ambulatory Surgical Centers |

| Home-Healthcare Providers |

| Long-Term Care & Assisted-Living Facilities |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Device | Multiparameter Vital-Signs Monitors |

| Cardiac Monitoring Devices | ||

| Respiratory Monitoring Devices | ||

| Neuro-Monitoring Devices | ||

| Fetal & Neonatal Monitoring Devices | ||

| Hemodynamic & Pressure Monitors | ||

| Wearable & Patch-Based Monitors | ||

| Remote Patient Monitoring Hubs & Gateways | ||

| AI-Driven Predictive Analytics Modules | ||

| Services | Installation & Maintenance | |

| Training & Education | ||

| RPM & Telehealth Services | ||

| Data Integration & Interoperability | ||

| Analytics & Reporting | ||

| Managed Monitoring & Triage Operations | ||

| By Application | Cardiology | |

| Respiratory | ||

| Neurology | ||

| Diabetes & Metabolic | ||

| Maternal & Neonatal | ||

| Critical Care Surveillance | ||

| Others | ||

| By End-User | Hospitals | |

| Specialty & Single-Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Home-Healthcare Providers | ||

| Long-Term Care & Assisted-Living Facilities | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the patient monitoring market by 2031?

It is forecast to reach USD 89.39 million, expanding at a 7.04% CAGR from 2026.

Which segment is expected to grow fastest through 2031?

Services are projected to grow at 9.53% annually as hospitals adopt subscription-based managed monitoring

How will RPM code changes influence adoption?

Lower interaction thresholds and new short-term codes are set to double the reimbursable patient pool in the United States, accelerating deployments.

Why is Asia-Pacific viewed as the growth engine?

Government-backed digital-health investments and favorable reimbursement reforms in China, India, and Japan underpin a 10.99% regional CAGR.

How are cybersecurity rules affecting vendor competition?

FDA Section 524B compliance raises entry barriers, favoring incumbents with robust regulatory capabilities and driving merger activity.

What risks could slow adoption of next-generation patient monitoring platforms

Capital cost, privacy and security compliance, and reimbursement variability are key risks, with cybersecurity and data governance now central to regulatory reviews and procurement.

Page last updated on: