Market Overview

| Study Period | 2021 - 2031 |

|---|---|

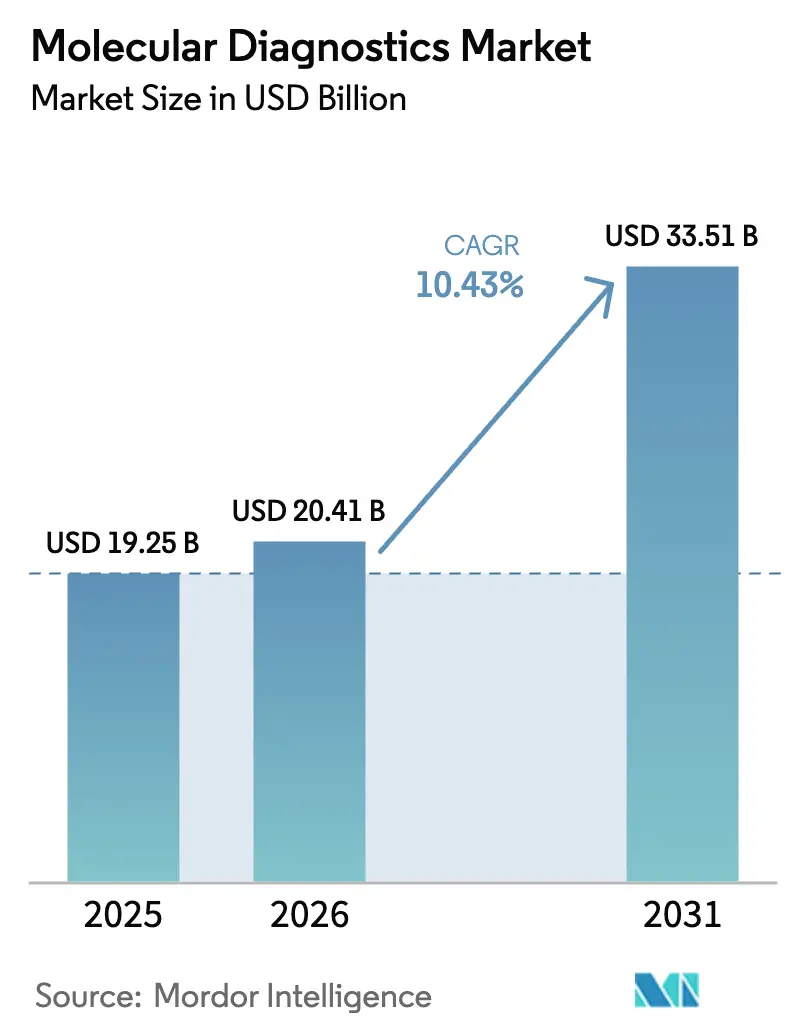

| Market Size (2026) | USD 20.41 Billion |

| Market Size (2031) | USD 33.51 Billion |

| Growth Rate (2026 - 2031) | 10.43% CAGR |

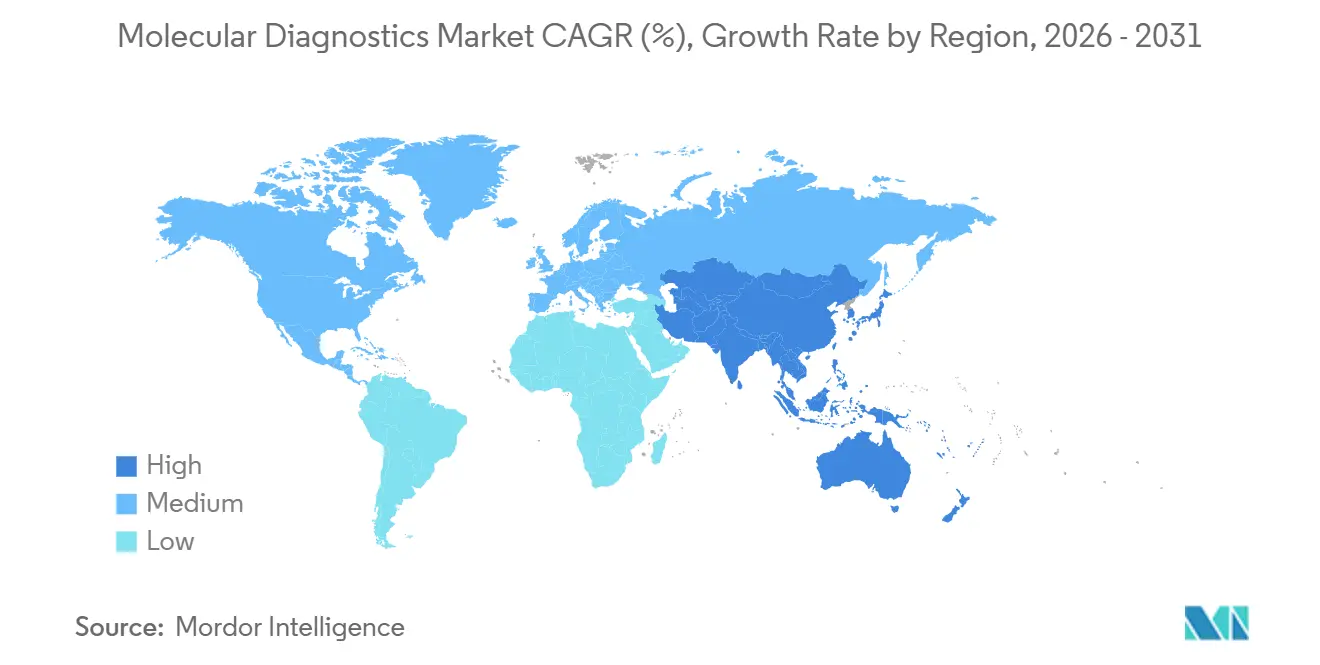

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Molecular Diagnostics Market Analysis by Mordor Intelligence

The molecular diagnostics market size is expected to reach USD 20.41 billion in 2026 and is projected to grow to USD 33.51 billion by 2031, reflecting a 10.43% CAGR. Broadening reimbursement for genomic profiling and establishing clearer regulatory pathways for laboratory-developed tests are facilitating the transition of precision medicine from research to routine care. Sequencing costs below USD 200 per genome, FDA breakthrough device designations for rapid whole-genome platforms, and retail-clinic rollouts of CLIA-waived assays are expanding clinical access. Meanwhile, the European Union’s In Vitro Diagnostic Regulation (IVDR) heightens post-market surveillance and compresses margins for smaller manufacturers, consolidating demand around integrated platforms. Falling per-test prices, multiplex syndromic panel uptake in hospitals, and pharmaceutical vertical integration into in-house genomic services together accelerate adoption across oncology, infectious disease, and population health programs.

Key Report Takeaways

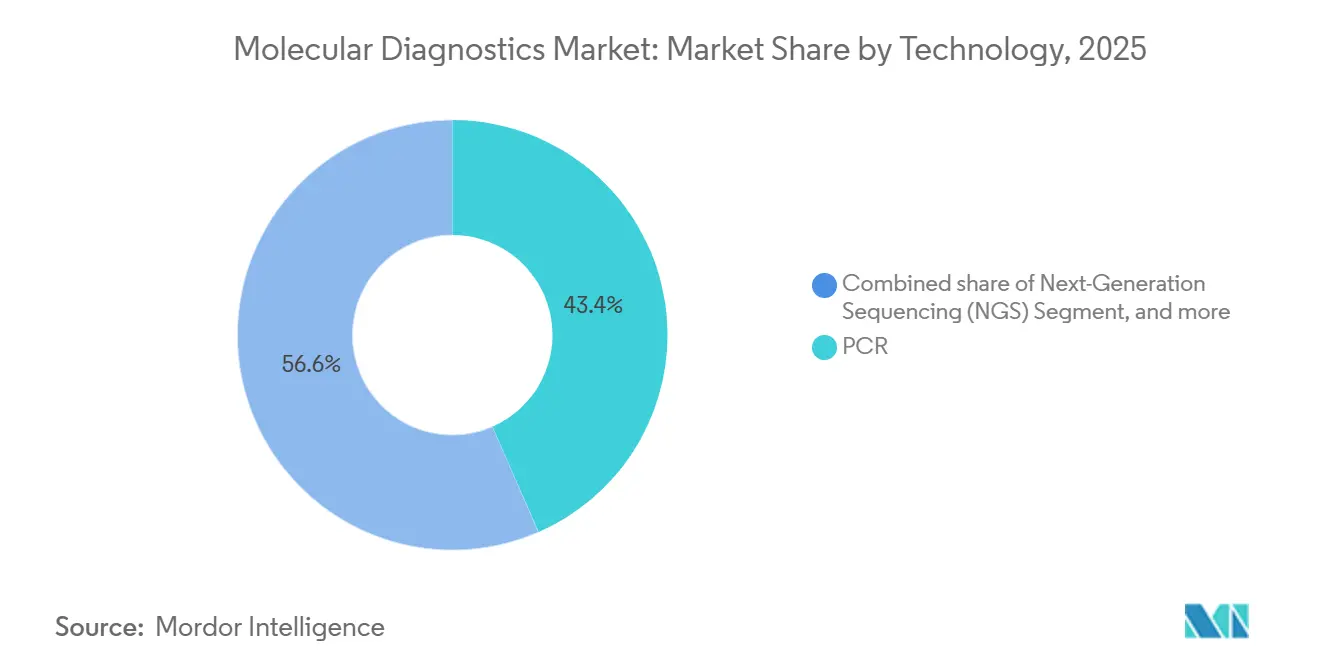

- By 2025, polymerase chain reaction (PCR) captured 43.44% of the molecular diagnostics market share; next-generation sequencing is projected to advance at an 11.56% CAGR through 2031.

- By application, infectious disease led with a 60.57% revenue share in 2025, while oncology showed the fastest growth at a 11.88% CAGR from 2026 to 2031.

- By product, reagents and kits held 77.40% of the molecular diagnostics market size in 2025; instruments and systems are expected to expand at an 13.61% CAGR through 2031.

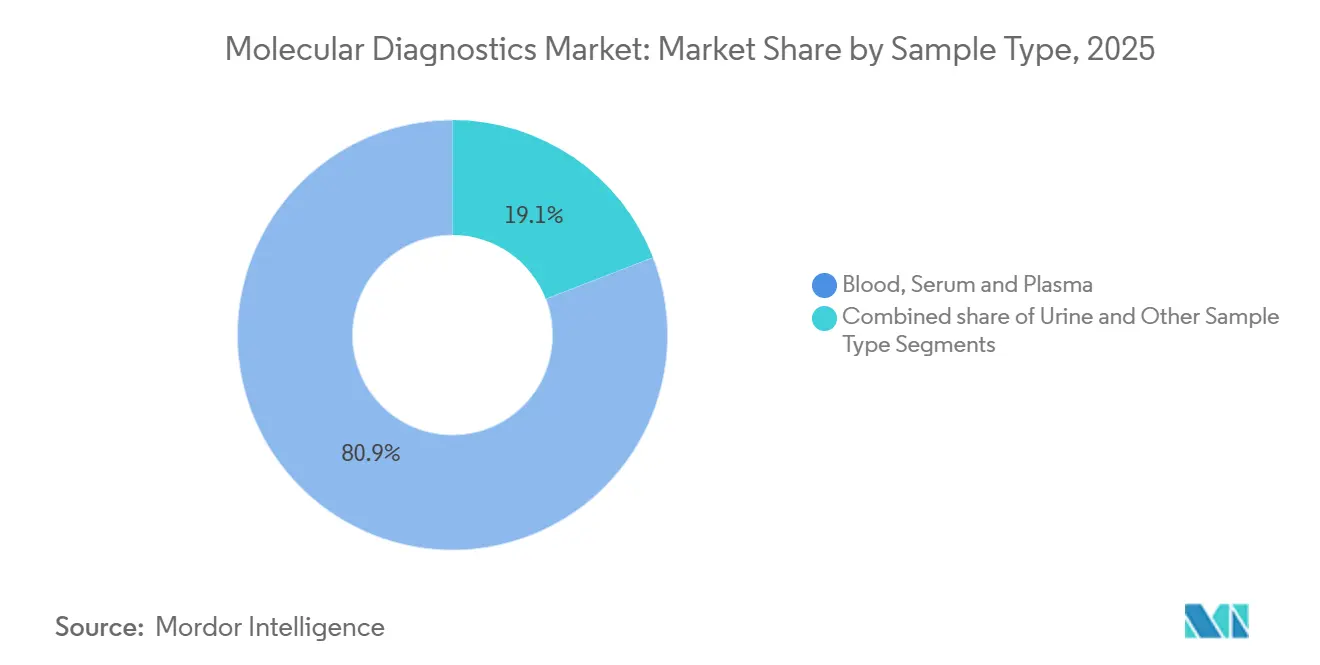

- By sample type, blood, serum & plasma accounted for 80.89% of the molecular diagnostics market size in 2025, whereas urine posted an 11.30% CAGR outlook.

- By end user, diagnostic and reference laboratories accounted for a 22.97% share of the molecular diagnostics market size in 2025, and hospitals are projected to grow at a 9.99% CAGR through 2031.

- By geography, North America dominated with a 42.54% revenue share in 2025, whereas the Asia-Pacific region is projected to record the highest CAGR of 11.35% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Molecular Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Rapid Point-of-Care Molecular Diagnostics | +2.1% | Global, with North America and Europe leading adoption; APAC expansion accelerating | Short term (≤ 2 years) |

| Integration of Companion Diagnostics with Targeted Therapies | +1.8% | Global, concentrated in North America, Europe, and Japan with regulatory pathways established | Medium term (2-4 years) |

| Declining Sequencing Costs and Expanded Clinical NGS Reimbursement | +2.3% | Global, with North America and Europe driving reimbursement; Asia-Pacific following | Medium term (2-4 years) |

| Emergence of Multiplex Syndromic Panels for Infectious Disease Management | +1.6% | Global, with hospital adoption highest in North America and Europe | Short term (≤ 2 years) |

| Decentralization of Testing Through CLIA-Waived Platforms and Retail Clinics | +1.4% | North America leading; early adoption in Europe and select APAC markets | Short term (≤ 2 years) |

| Government-Funded Population Genomics and Pandemic Preparedness Programs | +1.5% | Global, with UK, Japan, China, Saudi Arabia, and UAE investing heavily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Rapid Point-of-Care Molecular Diagnostics

Point-of-care platforms shorten diagnostic cycles from days to minutes, enabling immediate prescribing decisions and cutting inappropriate antibiotic use by 31% in urgent-care clinics. Handheld systems deliver results in under 15 minutes and integrate with electronic health records, matching the workflow of retail clinics where throughput drives profitability. Payers recognize downstream savings from reduced hospital readmissions, and parity reimbursement removes the historic cost advantage of centralized labs. Retail pharmacy chains announced nationwide deployments for respiratory panels in 2025, shifting high-volume testing away from emergency departments. As CLIA-waived clearances expand to chronic disease assays, consumer-initiated testing is set to become a routine component of primary care visits.

Integration of Companion Diagnostics with Targeted Therapies

Regulators now view companion diagnostics as prerequisites for most targeted therapies. The FDA cleared additional KRAS, NTRK, and HER2 biomarker-drug pairs in 2024, broadening single-run genomic profiling utility. EMA guidance mandates validation data at first drug filing, compressing the diagnostic-therapeutic development cycle but raising investment thresholds[1]European Commission, “In Vitro Diagnostic Regulation,” ec.europa.eu. Japan’s fast-track review shortens orphan-drug companion diagnostic approvals to 10 months, incentivizing the development of assays for rare mutations. Tumor mutational burden and microsatellite instability scores bundled into single workflows conserve tissue and accelerate reporting, making multi-biomarker panels the standard of care. Pharmaceutical sponsors are increasingly financing diagnostic R&D to secure drug market access, thereby aligning incentives across the value chain.

Declining Sequencing Costs and Expanded Clinical NGS Reimbursement

The average sequencing cost has fallen 42% since 2022, with whole-genome testing now available at USD 199 per sample in high-throughput labs. CMS now reimburses up to USD 3,000 for comprehensive tumor profiling, and private insurers cover minimal residual disease liquid biopsies for colorectal and breast cancers[2]Centers for Medicare & Medicaid Services, “Colorectal Cancer Liquid Biopsy NCD,” cms.gov. China added 23 NGS oncology panels to its national catalog, offering 70% pay-out ratios, which is expected to triple prospective test volumes in major cities by 2027. Population sequencing programs, such as the UK’s Newborn Genomes Programme and Japan’s All Japan Genomic Medicine Initiative, provide sustained demand for high-capacity instruments and cloud-based bioinformatics pipelines. These factors underpin a robust revenue outlook despite shrinking per-test margins.

Emergence of Multiplex Syndromic Panels for Infectious Disease Management

Syndromic panels group 15-30 pathogens into one assay, reducing the time to appropriate therapy by 22 hours in ICUs compared to culture methods. IDSA guidelines now recommend multiplex panels as first-line tools for community-acquired pneumonia, accelerating formulary inclusion. Post-COVID respiratory panel volumes rebounded during the 2024-2025 influenza season as hospitals sought to differentiate between flu, RSV, and SARS-CoV-2 rapidly. Stewardship programs penalize the overuse of broad-spectrum antibiotics, creating financial incentives for rapid molecular diagnostics that enable targeted prescribing. This shift is expected to migrate into gastrointestinal and bloodstream infection workflows as panel content expands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Operational Costs for Advanced Molecular Platforms | -1.7% | Global, with cost barriers highest in emerging markets and community hospitals | Medium term (2-4 years) |

| Complex and Evolving Regulatory Frameworks (EU IVDR, FDA LDT Rule) | -1.4% | Europe and North America primarily; spillover to export-dependent manufacturers | Medium term (2-4 years) |

| Reimbursement Uncertainties for Broad Genomic Profiling and Liquid Biopsy | -1.2% | Global, with North America and Europe facing coverage gaps; Asia-Pacific lagging | Long term (≥ 4 years) |

| Shortage of Skilled Molecular Laboratory Workforce | -1.0% | Global, with acute shortages in North America and Europe; emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operational Costs for Advanced Molecular Platforms

Benchtop sequencers cost USD 500,000, while high-throughput systems exceed USD 1 million, creating adoption barriers for community hospitals. Annual reagent outlays over USD 300,000 press already thin laboratory margins, and average reagent-plus-analysis cost per comprehensive profile is USD 1,200 even as Medicare pays USD 3,000 per test. Leasing and reagent-rental contracts offset capital costs but lock labs into multiyear commitments. Low-volume institutions resort to send-out models, accepting 7-10-day turnaround times that delay therapy initiation. Economic hurdles thus restrict decentralization, particularly in emerging markets where capital financing is scarce.

Complex and Evolving Regulatory Frameworks (EU IVDR, FDA LDT Rule)

The EU IVDR now mandates notified-body review, adding EUR 50,000–200,000 per assay and up to 18 months to launch timelines. MedTech Europe reports 38% of small IVD firms are considering market exit due to compliance costs. The FDA LDT rule requires high-risk assay submissions by 2027 and moderate-risk assays by 2029, with an estimated compliance cost of USD 1.5 billion over five years. Divergent frameworks compel multinational firms to adopt region-specific portfolios, thereby delaying global rollouts and increasing R&D duplication costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Sequencing Momentum, PCR Entrenched

Polymerase chain reaction generated 43.44% of 2025 revenue, underscoring its dominance in fast-turn infectious disease workflows. Next-generation sequencing is projected to grow at an 11.56% CAGR, driven by oncology profiling and rare disease diagnostics, positioning the molecular diagnostics market for broader multi-omic adoption. PCR’s CLIA-waived footprint supports urgent-care rapid testing, whereas sequencing’s multiplex capacity addresses complex oncology cases and population genomics. Digital PCR emerges as a tool for quantifying rare mutations, complementing NGS rather than displacing it. FDA guidance allowing PCR-based reference standards for sequencing validation reduces redundant confirmatory testing, thereby facilitating smooth transitions from single-gene to comprehensive profiling.

Clinical labs now deploy dual-modality architectures, combining rapid PCR for time-critical decisions with high-throughput sequencing for comprehensive genomic insights. Sequencing platforms that bundle sample preparation through bioinformatics mitigate staffing shortages by automating labor-intensive steps. As multi-cancer early detection assays enter coverage pathways, sequencing’s patient-level economics improve, solidifying its role in the next growth curve of the molecular diagnostics market.

By Application: Oncology Accelerates Beyond Infectious Disease

Infectious disease retained 60.57% share in 2025, but oncology’s 11.88% CAGR through 2031 is set to overtake, reinforcing the molecular diagnostics market’s shift toward cancer management. Liquid biopsy detects molecular recurrence nearly nine months before imaging in colorectal cancer, reshaping surveillance protocols. Medicare coverage for colorectal cancer liquid biopsy, at USD 920 per test, adds a reimbursed screening tool for 50 million eligible Americans. Pharmacogenomics gains traction as EHR alerts flag gene-drug interactions, catalyzing preemptive genotyping in primary care. Syndromic panels in microbiology reduce antibiotic exposure and shorten ICU stays, maintaining stable infectious disease revenues even as oncology growth accelerates.

By Product: Instruments Surge with Decentralization

Reagents and kits delivered 77.40% of the revenue in 2025, while instruments and systems posted an 13.61% CAGR as decentralized sites invest in bench-friendly systems. Closed ecosystems pair hardware with consumables to ensure consistent performance and compliance, locking in recurring sales. Cloud bioinformatics subscriptions, billed per case, shift fixed costs to variable costs, making them attractive to sites with fluctuating volumes. Genomic data accelerators that reduce analysis time from hours to minutes generated USD 180 million in 2024, underscoring the rising prominence of computational infrastructure. Integrated sample-to-report devices have cleared the FDA, enabling hospitals without molecular pathology expertise to rapidly onboard oncology panels.

By Sample Type: Blood Dominant, Non-invasive Specimens Multiply

Blood, serum, and plasma remain primary inputs for oncology and prenatal tests, anchoring sample-type revenues. Urine assays for kidney-transplant rejection and urinary infections expand the menu, aided by donor-derived cell-free DNA quantification. Saliva collection kits facilitate at-home participation in biobank projects, allowing for the stable storage of nucleic acids for years without refrigeration. Swab-based respiratory testing will persist post-pandemic as year-round syndromic protocols become normalized. FDA guidance clarifies variability between plasma and serum in liquid biopsy validation, underpinning assay reproducibility standards. The diversified sample landscape attracts participants who are reluctant to undergo invasive biopsies, thereby expanding the reach of the molecular diagnostics market.

By End User: Point-of-Care Channels Erode Central Lab Share

Diagnostic and reference laboratories held 22.97% revenue in 2025, but hospitals show a 9.99% CAGR, disrupting traditional hub-and-spoke testing. Retail clinics capture demand for acute respiratory testing, serving populations that lack access to primary physicians. Hospital labs are increasingly outsourcing complex sequencing to specialist reference centers, thereby focusing their in-house capacity on fast-turn syndromic panels. Academic centers pivot from test manufacture to clinical interpretation, aligning with FDA quality mandates. Consumer acceptance of pharmacy-based molecular tests resets expectations for turnaround and transparency, embedding decentralized modalities in everyday care pathways.

Geography Analysis

North America generated 42.54% of the 2025 revenue, driven by high per-capita spending and the rapid adoption of precision diagnostics by payers. CMS fee-schedule cuts in 2025 trimmed margins for low-complexity genomic tests, prompting labs to prioritize oncology panels with stronger reimbursement. Canada enlarged coverage to pharmacogenomics for antidepressants and anticoagulants, broadening pre-emptive genotyping in primary care. Liquid biopsy volumes surpassed 2 million U.S. samples in 2024, representing 80% of global activity.

The Asia-Pacific region is forecasted to grow at a 11.35% CAGR, underpinned by increasing funding for population genomics. Japan’s USD 1.8 billion initiative to sequence 1 million genomes by 2028 accelerates local instrument sales. China’s 2024 inclusion of NGS cancer panels with 70% reimbursement drives triple-digit volume growth in tier-1 cities. India’s private hospitals deploy NGS oncology profiling for out-of-pocket clients, while South Korean manufacturers expand PCR panel exports across Southeast Asia.

Europe faces IVDR-related product withdrawals as 38% of small IVD firms contemplate exit, tightening supply. Saudi Arabia’s Human Genome Program and the UAE's newborn sequencing initiatives are making the Middle East a new hotspot for genomic infrastructure investment. Brazil’s public health service funded molecular assays for tuberculosis and HIV drug resistance in 2024, catalyzing adoption despite budget constraints. Geographic momentum, therefore, hinges on reimbursement stability and domestic manufacturing capacity, factors that will dictate market share shifts through 2031.

Competitive Landscape

The top five players control roughly 55% of the 2025 revenue, reflecting a moderate level of concentration. Closed-platform leaders bundle instruments, reagents, and AI-driven clinical reporting under multiyear contracts, while open-architecture challengers court niche assay developers. Sequencing patents around circulating tumor DNA workflows exceed 200 in the U.S., deterring new entrants. AI-enabled interpretation platforms charge USD 500 per oncology case, monetizing data rather than consumables.

Vertical integration intensifies as pharmaceutical firms acquire genomic labs to secure biomarker testing for clinical trials and companion diagnostics. Meanwhile, cartridge-based startups target lower-volume sites with single-use consumable models that avoid capital spending.

ISO-driven reference standards for liquid biopsy aim to harmonize assay performance, potentially lowering barriers for second-mover entrants. Competitive focus thus shifts from raw throughput to clinical decision support, data aggregation, and end-to-end workflow ownership, shaping the trajectory of the molecular diagnostics market through 2031.

Molecular Diagnostics Industry Leaders

F. Hoffmann-La Roche Ltd

Thermo Fisher Scientific Inc.

Danaher Corp (Cepheid & Beckman Coulter)

Qiagen N.V.

Abbott

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Tia Health and Molecular Testing Labs have partnered to offer the first FDA-cleared at-home STI test kit, available virtually and in clinics nationwide. The Abbott simpli-COLLECTTM STI Test detects four common STIs, allowing patients to collect samples privately at home and receive faster results with support from Tia providers.

- July 2025: Matrix Medical Network announced a strategic partnership with CareNexa, LLC, operating as Molecular Testing Labs (MTL). MTL is a certified and accredited laboratory known for its innovation in molecular diagnostics. This collaboration aims to enhance patient health outcomes and provide greater value to Matrix’s clients.

- May 2025: Genesis Healthcare expanded its cloud-based analytics platform on AWS to support large-scale genomic research, underscoring the intensifying link between hyperscale computing and diagnostics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the molecular diagnostics market as all clinical-grade tests that pinpoint DNA or RNA sequences, single-nucleotide changes, insertions, deletions, or rearrangements, used to detect, quantify, or monitor infectious diseases, genetic disorders, and oncology markers in human samples. The valuation covers reagents, consumables, instruments, and software licensed for patient management across central labs, hospital labs, point-of-care settings, and authorized home-collection channels.

Scope exclusion: Research-use-only reagents, veterinary assays, and purely bioinformatics services remain outside our numbers.

Segmentation Overview

- By Technology

- PCR

- Next-Generation Sequencing (NGS)

- In Situ Hybridization

- Chips & Microarrays

- Mass Spectrometry

- Other Technologies

- By Application

- Infectious Disease

- Oncology

- Pharmacogenomics

- Microbiology

- Genetic Disease Screening

- Human Leukocyte Antigen Typing

- Blood Screening

- By Product

- Reagents & Kits

- Instruments & Systems

- Software & Services

- By Sample Type

- Blood, Serum & Plasma

- Urine

- Other Sample Types (Saliva, Tissue, Swabs)

- By End User

- Hospitals

- Diagnostic & Reference Laboratories

- Academic & Research Institutes

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Detailed Research Methodology and Data Validation

Desk Research

We began by compiling production, trade, and procedure-volume data from public pillars such as the World Health Organization, the Centers for Medicare & Medicaid Services, OECD Health Statistics, and the International Trade Centre. We then layered in clinical-trial registries and key peer-reviewed journals (for assay penetration trends). Our team also extracted instrument install bases and reagent pull-through ratios from SEC filings, national tender portals, and trusted news aggregators in Dow Jones Factiva.

Patent families obtained through Questel, plus price lists uploaded to hospital procurement sites, let us benchmark average selling prices and technology refresh cycles. These examples illustrate, not exhaust, the secondary sources tapped by Mordor analysts.

Primary Research

To ground secondary cues, we interviewed laboratory directors, infectious-disease clinicians, oncology genetic counselors, and procurement leads across North America, Europe, and key Asia-Pacific hubs. Their insights on test-menu mix, panel migration from PCR to NGS, and kit re-order frequencies helped us fine-tune utilization coefficients and future adoption curves.

Market-Sizing & Forecasting

A top-down incidence-to-testing build starts with disease prevalence, laboratory procedure volumes, and reimbursement ceilings, which are then reconciled with selective bottom-up roll-ups of major supplier revenue disclosures. Variables such as PCR kit average selling price, NGS run capacity, point-of-care penetration rates, regulatory approvals, and healthcare expenditure per capita drive our model. Forecasts employ multivariate regression, allowing scenario overlays supplied by primary experts on pricing compression and guideline changes. Gaps in supplier roll-ups are bridged through regional shipment proxies and ASP harmonization.

Data Validation & Update Cycle

Before sign-off, our analysts triangulate outputs against import tariffs, quarterly earnings call signals, and external epidemiological datasets; anomalies trigger re-checks. Reports refresh each year, with mid-cycle tweaks if material events, like a major FDA clearance, shift the baseline.

Why Our Molecular Diagnostics Baseline Commands Confidence

Published estimates vary, and we acknowledge that scope choices, pricing ladders, and refresh cadence often drive the spread.

Key gap drivers include whether companion animal kits are counted, if over-the-counter COVID tests inflate totals, the currency year applied, and how aggressively future ASP erosion is modeled; this is where Mordor Intelligence applies disciplined filters and annual source audits.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.94 B (2025) | Mordor Intelligence | - |

| USD 27.00 B (2024) | Global Consultancy A | Includes research-only reagents and double-counts OTC COVID volumes |

| USD 19.48 B (2025) | Industry Association B | Omits price erosion post-patent expiry and assumes static reimbursement |

| USD 45.11 B (2025) | Regional Consultancy C | Blends precision diagnostics and broader IVD segments into definition |

These comparisons show that, by anchoring on patient-care use cases, validated price-volume pairs, and a yearly refresh, Mordor provides a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current value of the molecular diagnostics market?

The market stands at USD 20.41 billion in 2026 and is projected to reach USD 33.51 billion by 2031.

Which technology is growing fastest within molecular diagnostics?

Next-generation sequencing records an 11.56% CAGR through 2031 due to expanded oncology and rare disease applications.

How are retail clinics influencing molecular diagnostics adoption?

CLIA-waived platforms allow pharmacies to offer 15-minute respiratory panels, for point-of-care channels.

Which region is expected to see the highest growth to 2031?

Asia-Pacific leads with a projected 11.35% CAGR, spurred by government-funded population genomics initiatives.

What regulatory changes most impact molecular diagnostics laboratories?

The EU IVDR and FDA LDT final rule add significant compliance costs and extend time-to-market for new assays.

How concentrated is competition among molecular diagnostics suppliers?

The top five firms hold roughly 55% of revenue, reflecting moderate concentration with room for specialized entrants.

Page last updated on: