Biotechnology Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 93.17 Billion |

| Market Size (2031) | USD 116.07 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

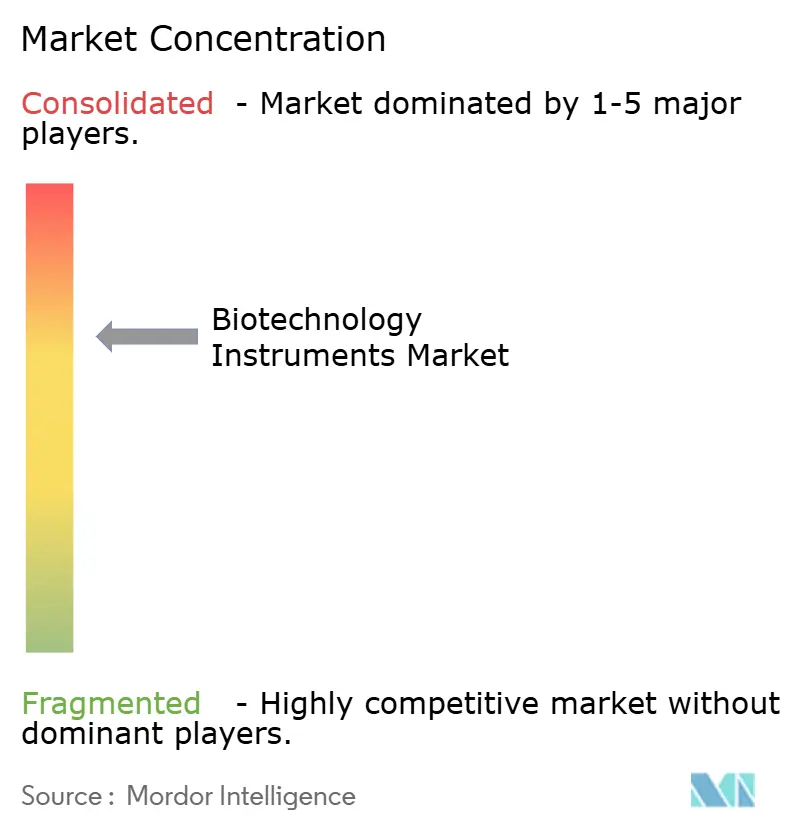

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biotechnology Instruments Market Analysis by Mordor Intelligence

The biotechnology instruments market size is expected to grow from USD 89.17 billion in 2025 to USD 93.17 billion in 2026 and is forecast to reach USD 116.07 billion by 2031 at 4.49% CAGR over 2026-2031. This steady headline figure conceals rapid changes below the surface: laboratory managers now prioritize fully automated, AI-enabled workflows that shorten discovery cycles, guard against human error, and stretch limited technical staff. Growth concentrates in high-throughput applications such as synthetic biology, personalized cell therapy, and point-of-care molecular diagnostics, each of which demands compact instruments that integrate hardware, software, and data analytics. Long procurement lead times caused by component shortages encourage buyers to favor vendors able to guarantee supply continuity through multi-sourced parts and predictive maintenance services. In parallel, strict energy-efficiency regulations in Europe and parts of Asia reward instrument designs with lower standby power and recyclable plastics, giving manufacturers a new path to differentiation.

Key Report Takeaways

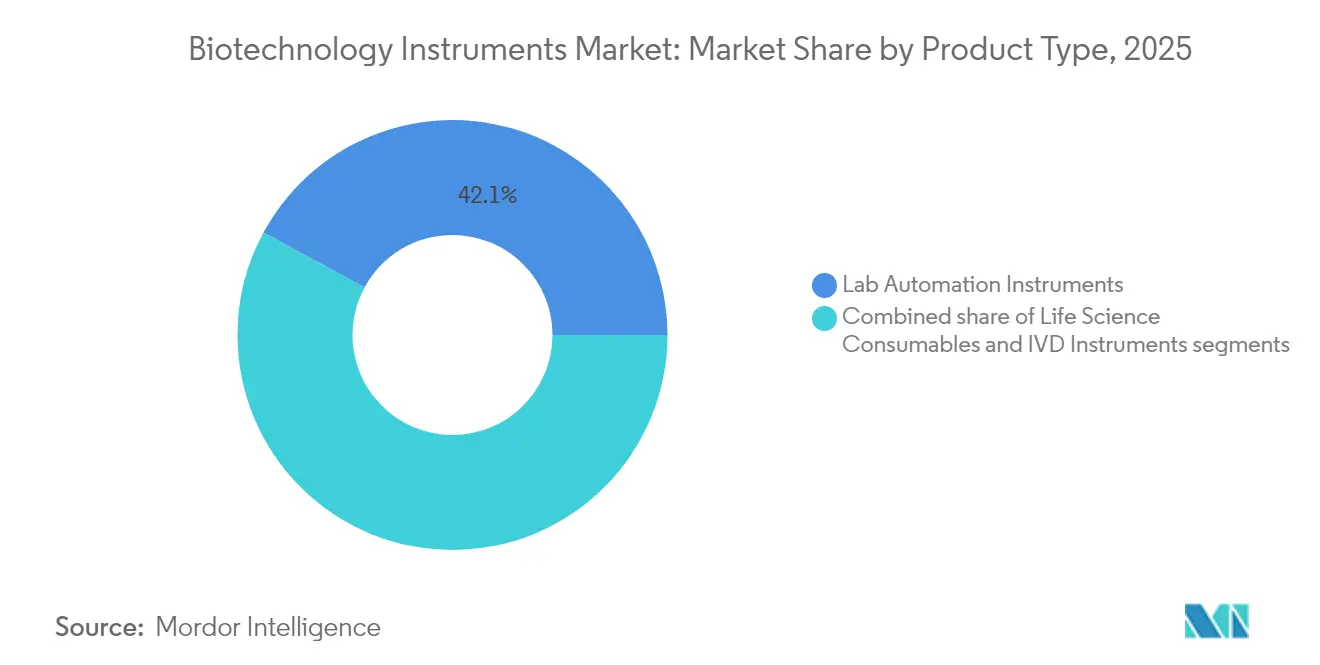

- By product type, lab automation platforms held 42.10% of the biotechnology instruments market share in 2025, while life science consumables are advancing at a 5.77% CAGR through 2031.

- By distribution channel, offline sales accounted for 80.62% of the biotechnology instruments market size in 2025, whereas online platforms are expanding at a 6.64% CAGR to 2031.

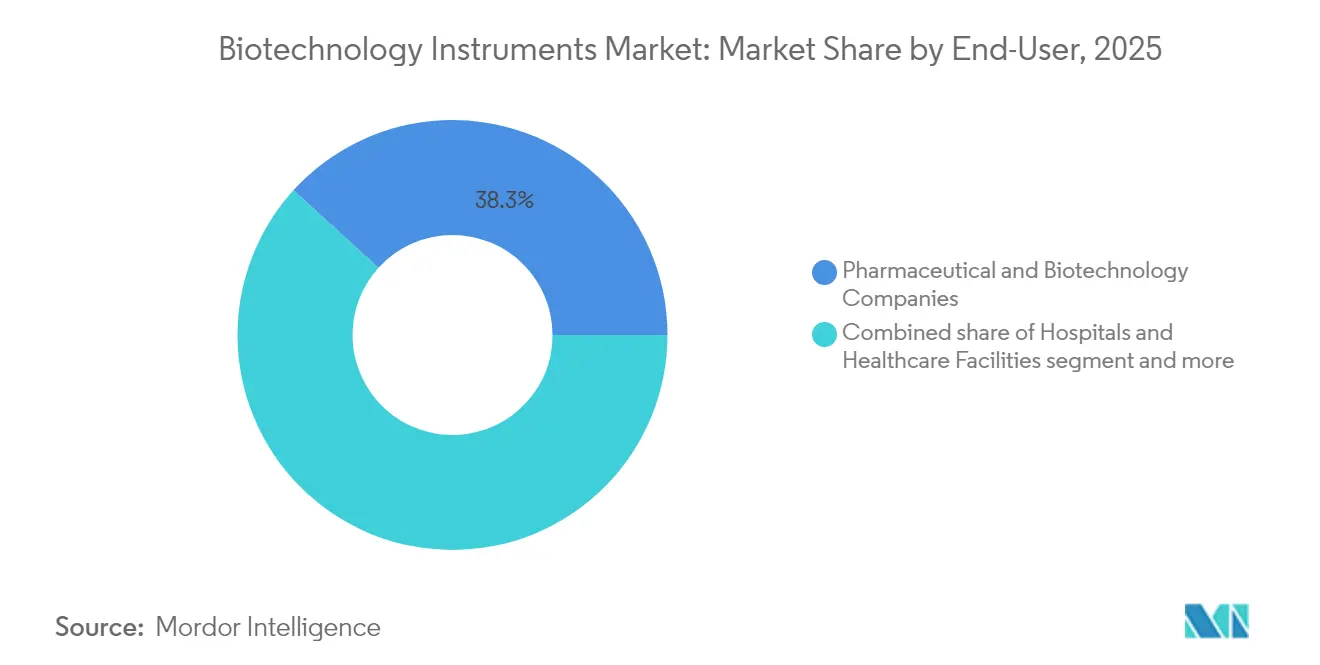

- By end-user, pharmaceutical and biotechnology companies led with a 38.25% share of the biotechnology instruments market in 2025; contract research and manufacturing organizations recorded the fastest 5.36% CAGR.

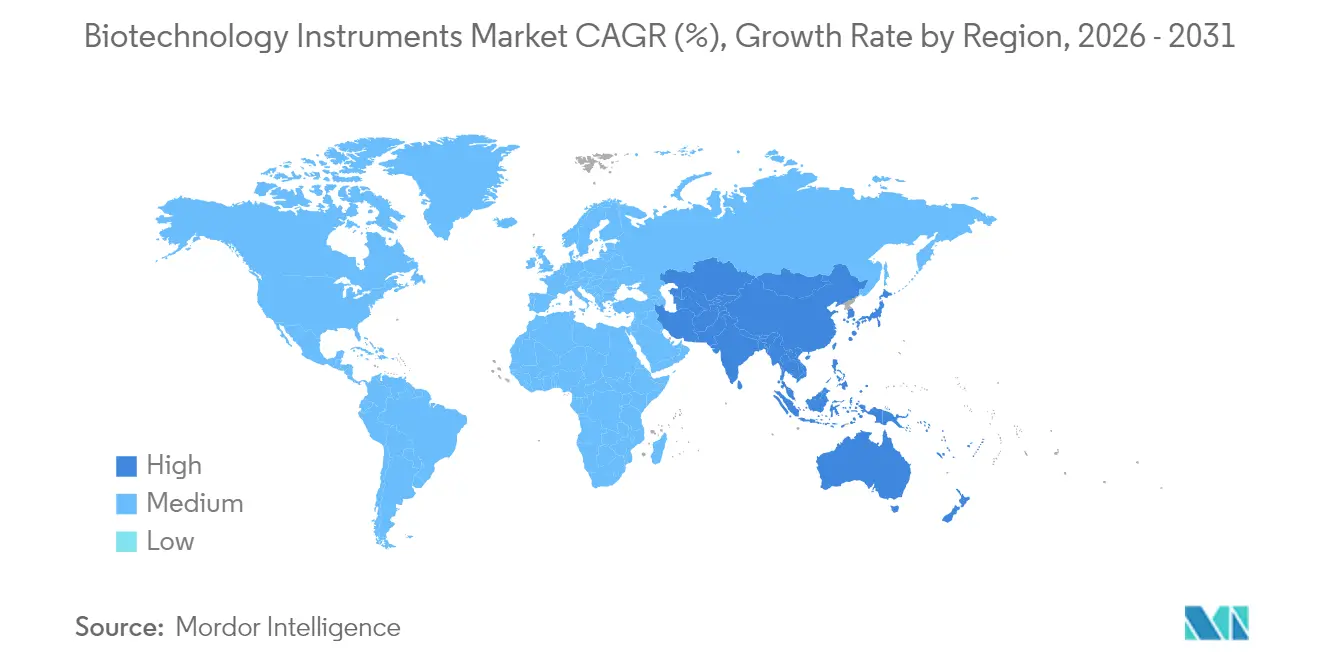

- By geography, North America commanded 40.85% share in 2025, yet Asia-Pacific exhibits the swiftest 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Biotechnology Instruments Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in large-scale biologics & cell-therapy manufacturing | +0.9% | Global, concentrated in US, Germany, Singapore | Medium term (2-4 years) |

| Growth in point-of-care molecular tests | +0.8% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Expansion of high-throughput screening in drug discovery | +0.7% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| AI-driven predictive maintenance cuts instrument downtime | +0.5% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Synthetic DNA foundries demanding next-gen automation | +0.4% | North America & EU | Long term (≥ 4 years) |

| Government decarbonization rules favor low-energy lab devices | +0.3% | EU core, spill-over to North America & APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Large-Scale Biologics & Cell-Therapy Manufacturing

Manufacturers scaling monoclonal antibodies and autologous cell therapies require closed, modular automation that controls sterility, traceability, and batch variability. Platforms such as the CliniMACS Prodigy integrate washing, selection, activation, and formulation in a single enclosed device that meets GMP guidelines while trimming clean-room footprint. This preference for plug-and-play systems pushes suppliers to bundle hardware, single-use consumables, and process software under one contract, raising switching costs and deepening vendor relationships.

Growth in Point-of-Care Molecular Tests

Hospitals that installed rapid PCR analyzers during the pandemic now extend them to antimicrobial resistance, oncology, and transplant monitoring. Sample-to-answer cartridges collapse extraction, amplification, and detection into a handheld format; premium price tags are justified by shorter waiting times and reduced inpatient stays. Emergency Use Authorization pathways set during COVID-19 have also shortened approval cycles for future bedside assays, accelerating volume commitments for compact thermal cyclers and integrated optics.

Expansion of High-Throughput Screening in Drug Discovery

Screening laboratories migrate from microplate readers to acoustic liquid handlers coupled with real-time AI analytics. SCIEX’s Echo MS+[1]SCIEX, “High-Throughput Mass Spectrometry,” sciex.com streams one sample each second and feeds spectral data into machine-learning models that rank hits in hours rather than weeks. This shift compresses discovery timelines and expands demand for integrated decks combining storage, pipetting, incubation, and analytics, thereby locking in long-term reagent and service revenues.

AI-Driven Predictive Maintenance Cutting Instrument Downtime

Predictive algorithms embedded in cloud-connected centrifuges and chromatography systems analyze motor current, vibration, and temperature signals to detect drift days before failure. Thermo Fisher instruments equipped with these features have reported 20% shorter lead times and 30% higher capacity utilization, reinforcing the notion that service ecosystems now influence procurement as strongly as hardware specifications.

Restraints Impact Analysis of Biotechnology Instruments Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy FDA & CE-IVDR change-control cycles | -0.6% | Global, concentrated in US & EU | Medium term (2-4 years) |

| Volatile rare-earth & semiconductor supply for precision motors | -0.5% | Global, acute in APAC manufacturing | Medium term (2-4 years) |

| Shortage of automation-savvy lab technicians | -0.4% | Global, acute in North America & EU | Long term (≥ 4 years) |

| Cyber-security risks in cloud-connected platforms | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy FDA & CE-IVDR Change-Control Cycles

Software updates or minor hardware tweaks can trigger full validation[2]Kathryn Millett, “Cyber-Biosecurity Risk Perceptions in the Biotech Sector,” Frontiers in Bioengineering and Biotechnology, frontiersin.org under CE-IVDR, extending launch timelines by 12–18 months and absorbing scarce regulatory headcount. Mid-tier firms respond by outsourcing compliance documentation to specialized consultancies, but that raises cost bases and discourages frequent iteration of instrument firmware or assay protocols.

Shortage of Automation-Savvy Lab Technicians

Sixty-nine percent of new bioprocess vacancies now list robotics or coding skills, yet most university curricula still focus on manual bench techniques. Firms therefore invest in intuitive graphical user interfaces, self-calibrating sensors, and on-board training wizards that shorten onboarding from months to weeks while keeping error rates low.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Biotechnology Instruments Market Segment Analysis

By Product:

Automation Drives Lab TransformationLab automation platforms held 42.10% biotechnology instruments market share in 2025 as pharmaceutical sponsors prioritized reproducibility across sprawling compound libraries and multi-site trials. The biotechnology instruments market size for automation rose alongside single-use bioreactor adoption, which forces every upstream and downstream step onto robotic carriers. Ten-axis collaborative arms paired with vision systems now load microtiter plates, swap pipette tips, and scan barcodes without human intervention, unlocking overnight run capability. Life science consumables record the swiftest 5.77% CAGR because single-use bags, filters, and tips eliminate labor-intensive cleaning steps and assure sterility in personalized therapies. Reagents pre-validated for specific assay kits further reduce downtime, fostering just-in-time inventory models that tie consumable reorder triggers to instrument software. Although IVD platforms sit in the mature basket, their molecular sub-segment climbs steadily as clinicians embrace syndromic panels that consolidate multiple pathogen targets into one swab, narrowing empirical antibiotic use.

By Distribution Channel:

Digital Transformation AcceleratesOffline specialists controlled 80.62% of biotechnology instruments market size in 2025 because complex installations still require site surveys, custom integration, and validation scripts. Even so, the 6.64% CAGR in online sales underscores a generational pivot toward e-commerce for standardized benchtop devices and kits under USD 20,000. Cloud-based quoting engines now let customers configure modules, choose service tiers, and schedule installation crews in a single session, cutting purchasing cycles from months to days. Vendors supplement virtual showrooms with augmented-reality demonstrations that guide users through footprint planning and cable routing. Consumables benefit most: bar-coded cartridges ordered automatically through application programming interfaces keep critical reagents in stock and feed real-time demand forecasts back to suppliers. Hybrid arrangements are emerging in which enterprise agreements are negotiated face-to-face yet executed through digital portals, blending the assurance of in-person consultation with the speed of web checkout.

By End-User:

CRO/CDMO Growth Reshapes ProcurementPharmaceutical and biotechnology companies retained 38.25% of the biotechnology instruments market share in 2025, thanks to deep R&D pipelines and internal biologics production. Their procurement teams, however, increasingly defer early-stage screening, toxicology, and even late-phase cell-therapy manufacturing to CRO/CDMO partners. These service providers post a 5.36% CAGR because they bundle regulatory documentation, capacity scalability, and client data segregation into one offering. As a result, the biotechnology instruments market now experiences bulk purchases geared toward multi-client workflows, favoring platforms that log sample provenance, automate chain-of-custody audits, and support electronic batch records. Academic and government laboratories remain steady yet budget-constrained, often stretching service contracts and extending depreciation schedules. Hospitals adopt compact molecular systems that slot into emergency rooms and transplant wards, demanding intuitive interfaces that clinicians can master without full-time laboratory oversight.

Geography Analysis

North America and Europe Biotechnology Instruments Market

North America retained the largest share of the biotechnology instruments market in 2025 at 40.85%, supported by clustered biopharma headquarters, deep venture funding, and mature contract service ecosystems. Subsidies for domestic semiconductor fabs also aim to buffer the market against future chip shortages. Europe follows with steady expansion driven by robust industrial-biotech policies in Germany and the United Kingdom's focus on synthetic biology startups. Energy-efficiency mandates such as draft ENERGY STAR specifications spur laboratories to replace legacy freezers and incubators with lower-wattage alternatives.

APAC Biotechnology Instruments Market

Asia-Pacific registers the fastest 6.05% CAGR to 2031 as China pours capital into biomanufacturing parks, Japan revitalizes its regenerative-medicine sector, and India scales contract chemistry services. Singapore, through tax incentives and predictable regulatory pathways, positions itself as a regional cell-therapy hub that demands automated closed-system instrumentation. Local suppliers coexist with multinationals, but integration competence often tips awards toward global brands able to provide 24-hour service coverage.

MEA and South America Biotechnology Instruments Market

The Middle East and Africa record 5.18% CAGR on the back of hospital modernization programs and government-backed research campuses in Saudi Arabia and the United Arab Emirates. South America posts 4.86% growth, with Brazil’s vaccine expansion and Argentina’s seed-trait research driving demand for portable genomic analyzers that function reliably in high-humidity environments. While purchasing power differs widely, the underlying need for quality-assured instruments that meet global accreditation standards converges across regions, aligning vendor roadmaps toward harmonized specifications.

Competitive Landscape

Market consolidation intensifies as diversified conglomerates acquire niche innovators to deliver end-to-end workflows extending from sample prep to cloud analytics. Thermo Fisher Scientific’s USD 4.1 billion acquisition of Solventum’s purification and filtration portfolio exemplifies this platform strategy and strengthens its upstream-to-downstream coverage in biologics purification. Competitors now rush to match breadth, prompting a wave of minority investments, co-development partnerships, and exclusive distribution agreements designed to plug capability gaps without full takeovers.

Technology differentiation centers on AI engines that slash unplanned downtime, embedded sensors that certify each run, and open software development kits that allow third-party apps to optimize protocols. Becton Dickinson’s latest flow-cytometry line couples robotics with spectral imaging to measure up to 50 markers in real time, reducing assay development cycles and opening new multiplexed-analysis revenue streams. Smaller challengers focus on miniaturization and cost, releasing portable mass specs and benchtop next-generation sequencers aimed at resource-limited labs; their success often depends on forging OEM alliances that secure access to stable supply chains.

Price competition remains moderate because validation overhead and operator training lock in installed bases for 7–10 years. Nonetheless, buyers are pushing for outcome-based contracts tied to uptime, throughput, or cost-per-sample. Vendors responding with integrated service bundles—combining consumables, remote monitoring, and on-site support—are capturing premium renewals and deepening customer loyalty. Cyber-security certifications increasingly influence award decisions as regulators scrutinize cloud-connected devices, motivating manufacturers to embed encryption, audit logging, and over-the-air patching into flagship platforms.

Biotechnology Instruments Industry Leaders

Agilent Technologies, Inc.

Becton, Dickinson and Company

bioMérieux SA

Danaher Corporation

Thermo Fisher Scientific

- *Disclaimer: Major Players sorted in no particular order

Biotechnology Instruments Market Companies Covered in this Report

- Agilent Technologies

- Azenta

- Beckton Dickinson

- bioMérieux

- Bio-Rad Laboratories

- Bruker

- Danaher

- Eppendorf

- Roche

- Hamilton Company

- Hudson Robotics

- Illumina

- Promega

- QIAGEN

- Quest Diagnostics

- Revvity Inc

- Siemens Healthineers

- Tecan Group

- Thermo Fisher Scientific

- Waters Corporation

Recent Industry Developments in Biotechnology Instruments Market

- June 2025: Thermo Fisher Scientific unveiled the Orbitrap Astral Zoom and Orbitrap Excedion Pro mass spectrometers, boosting scan speed by 35% and throughput by 40% for complex biomolecule analysis.

- May 2025: BD launched the FACSDiscover A8 Cell Analyzer, integrating spectral and real-time imaging to profile 50 cellular features simultaneously.

- April 2025: QIAGEN outlined its QIAsymphony Connect, QIAsprint Connect, and QIAmini sample-prep instruments, pledging 50% plastic-waste reduction across the line.

- April 2025: Danaher Corporation’s subsidiary Beckman Coulter Life Sciences released the OptiMATE Gradient Maker, trimming viral-vector purification from 3 days to 6 hours and easing AAV manufacturing bottlenecks.

Biotechnology Instruments Market Report Scope and Research Methodology

Market Definition and Coverage

Mordor Intelligence defines the biotechnology instruments market as the global revenue generated from brand-new analytical, automation, diagnostic, and cell-handling systems that enable the isolation, detection, or quantification of biological molecules across research, clinical, and industrial labs. Values are captured at factory gate prices and converted to constant 2025 USD for consistency.

Scope exclusion: refurbished instruments and generic lab plasticware that add no embedded technology value are not counted.

Segments Covered in This Report

- By Product Type

- Lab Automation Instruments

- Liquid Handling Systems

- Automated Plate Handlers

- Robotic Sample Processors

- Life Science Consumables

- Reagents & Buffers

- Microplates & Tubes

- Pipette Tips & Filtration

- IVD Instruments

- Clinical Chemistry Analyzers

- Hematology Analyzers

- Immunoassay Platforms

- Molecular Diagnostics Systems

- Lab Automation Instruments

- By Distribution Channel

- Offline

- Online

- By End-User

- Government & Academic Institutes

- Pharmaceutical & Biotechnology Companies

- Hospitals & Healthcare Facilities

- Contract Research & Manufacturing Organizations

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews and short surveys with lab managers, biomedical engineers, procurement heads, and regional distributors across North America, Europe, and Asia helped validate unit run-rates, average selling prices, and replacement cycles. Feedback also clarified emerging demand for compact next-generation sequencers in oncology labs, closing gaps left by desk research.

Desk Research

Our analysts began by mapping the installed base of PCR cyclers, chromatography units, and clinical chemistry analyzers using public customs dockets, trade association yearbooks such as the Analytical Life Science & Diagnostics Association, and country-level healthcare equipment registries. We then gathered pricing ranges from annual reports and 10-Ks filed by leading instrument makers, which were cross-checked with distributor catalogs and procurement portals. Additional context on R&D outlays, patent filings, and NIH grant trends was pulled through Dow Jones Factiva and Questel to flag demand inflection points. These sources, alongside others not exhaustively listed here, built the secondary foundation.

A second pass tapped UN Comtrade flow tables, OECD health expenditure dashboards, and peer-reviewed studies on lab automation uptake to refine regional splits. Whenever reported figures conflicted, priority went to official statistical releases that were most recently updated and showed complete series continuity.

Market-Sizing & Forecasting

The top-down model reconstructs 2025 demand from production and trade data, which are then adjusted for average channel margins to reach end-market value. Select bottom-up checks, such as regional supplier roll-ups and sampled ASP × installed units, temper the totals and highlight anomalies before reconciliation. Key variables include public and private biotech R&D spending, the number of high-complexity clinical labs, average throughput of cell-culture suites, and annual price erosion tracked through distributor invoices. Five-year forecasts employ multivariate regression that links these drivers with historical shipment trends and macro indicators like GDP-health ratios.

Data Validation & Update Cycle

Outputs pass a three-layer review that compares them with independent capacity, shipment, and revenue signals; variances beyond preset bands trigger analyst rechecks. Reports refresh each year, with mid-cycle updates when material regulatory or technological shifts arise.

How Mordor Intelligence's Biotechnology Instruments Market Size Compares to Other Published Estimates

Published estimates often differ because publishers choose varied product baskets, price definitions, and refresh cadences. Our disciplined scope selection and annual update rhythm reduce such drift.

Key gap drivers include some firms folding in capital-intensive bioprocess hardware, others reporting aggressive post-pandemic demand spikes without validated ASP paths, and a few relying solely on top-down trade tables that undercount direct-to-lab sales.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 89.17 B (2025) | Mordor Intelligence | - |

| USD 87.8 B (2024) | Global Consultancy A | Broad "equipment" scope inflates base and applies one uniform 8 % CAGR |

| USD 93.98 B (2025) | Research Firm B | Includes medical laser systems and projects out to 2035 using static replacement rates |

| USD 80.9 B (2025) | Trade Journal C | Excludes life-science consumables bundled with instruments and relies on trade data only |

Taken together, the comparison shows that Mordor's blended approach, grounded in verified variables, reviewed frequently, and transparent in scope, yields a balanced baseline that decision-makers can trust.

Key Questions Answered in the Report

How is AI adoption influencing maintenance strategies for biotechnology instruments?

Laboratories are embedding machine-learning analytics in centrifuges, chromatographs, and liquid handlers to predict component wear before failure, improving uptime while reallocating technician hours to higher-value tasks.

What factors are driving demand for single-use consumables in biologics production?

Single-use filters, bags, and tips cut cross-contamination risk, reduce cleaning validation workload, and allow rapid changeovers between personalized therapy batches, making them the preferred option for flexible manufacturing.

How are outsourcing trends reshaping instrument purchasing decisions?

Contract research and manufacturing organizations now negotiate multi-platform, service-bundled contracts that favor vendors offering integrated hardware, software, and validation support rather than standalone devices.

Why are point-of-care molecular diagnostic platforms attracting increased investment?

Decentralized PCR and isothermal systems provide rapid, bedside results that shorten clinical decision times, aligning with hospital goals to improve outcomes and relieve core laboratory bottlenecks.

What supply-chain challenges currently affect precision components in lab automation equipment?

Dependence on a limited number of rare-earth magnet suppliers and semiconductor fabs exposes liquid-handling motors and optical sensors to extended lead times and price volatility.

How are sustainability regulations shaping design priorities for new laboratory instruments?

Energy-efficiency targets and plastics-reduction mandates are prompting manufacturers to develop lower-standby-power electronics and recyclable cartridge materials, differentiating products through eco-label certifications.

Page last updated on: