Multiplex Assays Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.3 Billion |

| Market Size (2031) | USD 4.52 Billion |

| Growth Rate (2026 - 2031) | 14.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multiplex Assays Market Analysis by Mordor Intelligence

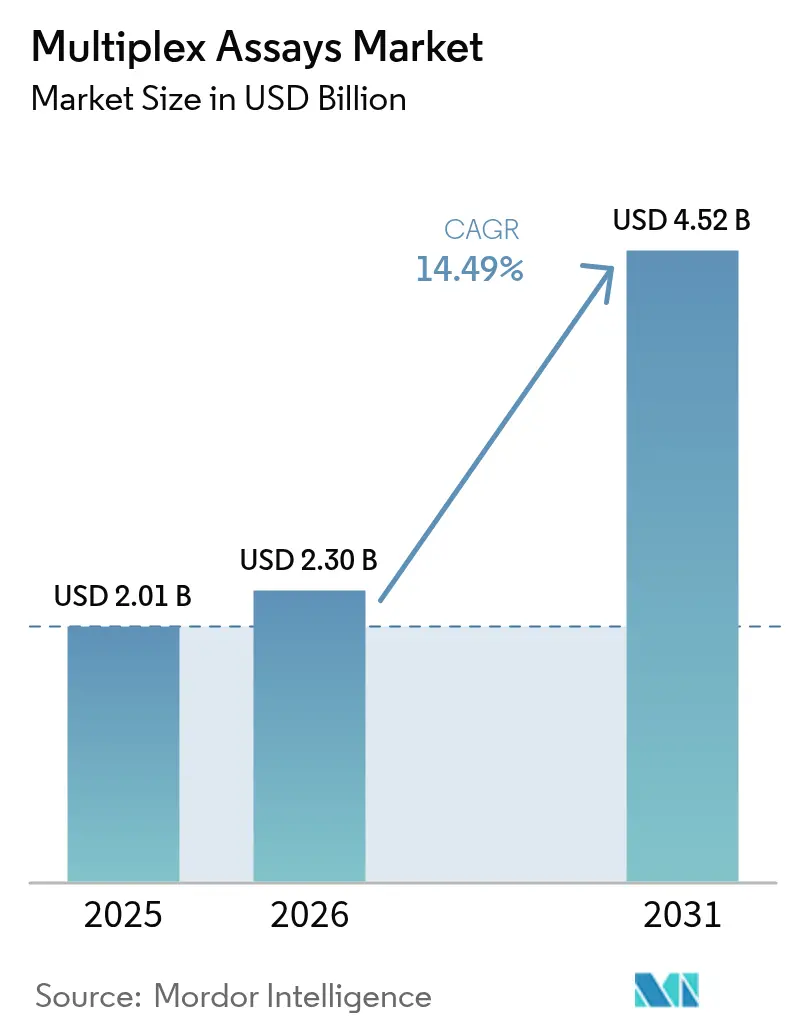

The Multiplex Assays Market size was valued at USD 2.01 billion in 2025 and estimated to grow from USD 2.30 billion in 2026 to reach USD 4.52 billion by 2031, at a CAGR of 14.49% during the forecast period (2026-2031).

A growing commitment to precision medicine, breakthroughs in CRISPR-enabled diagnostics, and routine use of 40-plus-color flow cytometry platforms underpin this expansion. Clinical laboratories favor multiplex formats because they reduce sample requirements, shorten turnaround time, and control costs while delivering multi-parameter insights that singleplex approaches cannot match. Pharmaceutical sponsors are embedding biomarker-rich study designs into trials, and regulatory authorities are clearing ever-broader companion diagnostics that rely on multiplex detection. At the same time, hospitals are adopting syndromic panels for respiratory and sepsis testing to improve bedside decision-making and curb antimicrobial misuse, further propelling the multiplex assays market.

Key Report Takeaways

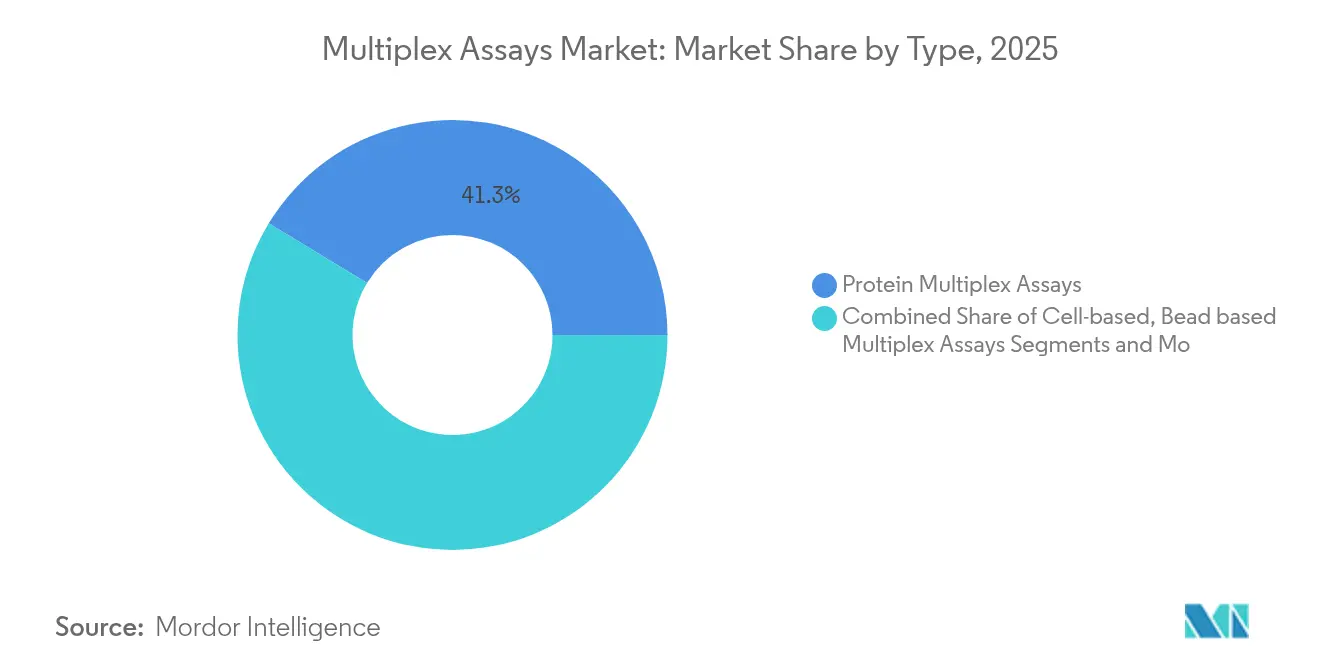

- By type, protein assays held 41.31% of multiplex assays market share in 2025, while nucleic-acid assays are forecast to grow at a 16.98% CAGR to 2031.

- By technology, flow cytometry led with 32.08% revenue share in 2025; mass cytometry is projected to expand at a 15.06% CAGR through 2031.

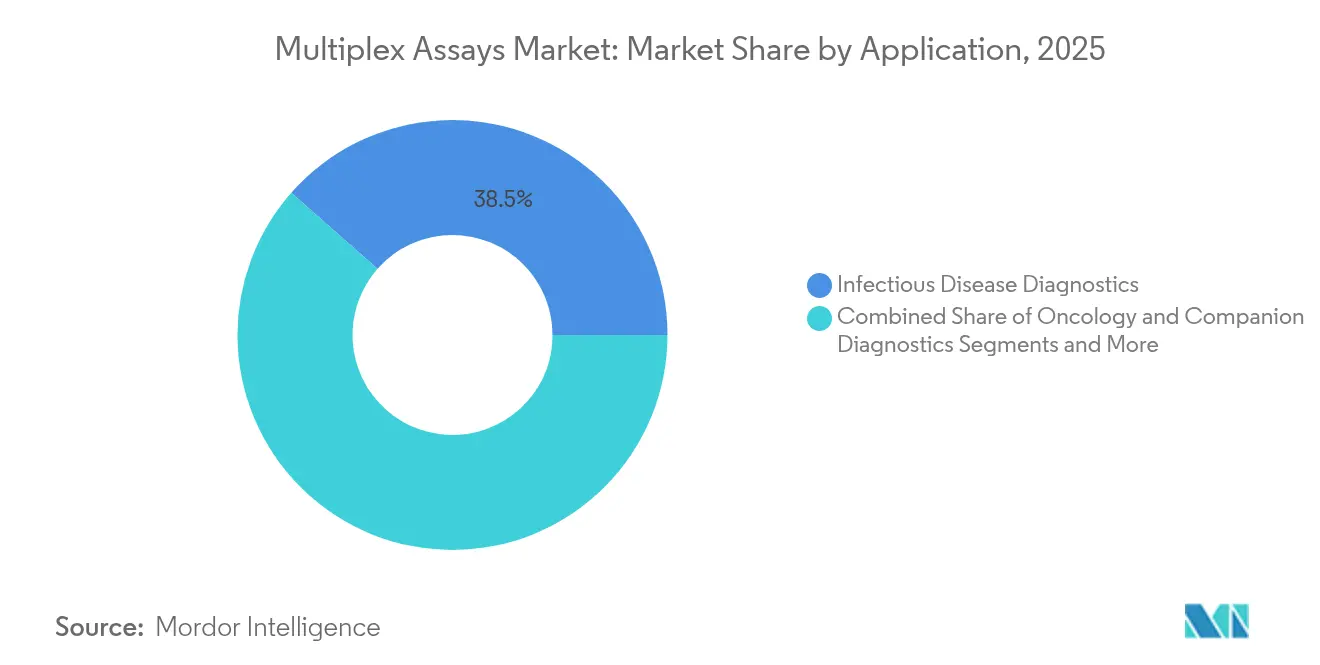

- By application, infectious disease diagnostics accounted for 38.49% of multiplex assays market size in 2025, whereas oncology and companion diagnostics will rise at a 16.33% CAGR between 2026-2031.

- By end-user, pharmaceutical and biopharmaceutical companies commanded 46.12% share of the multiplex assays market size in 2025, while contract research organizations are set to grow at 17.49% CAGR.

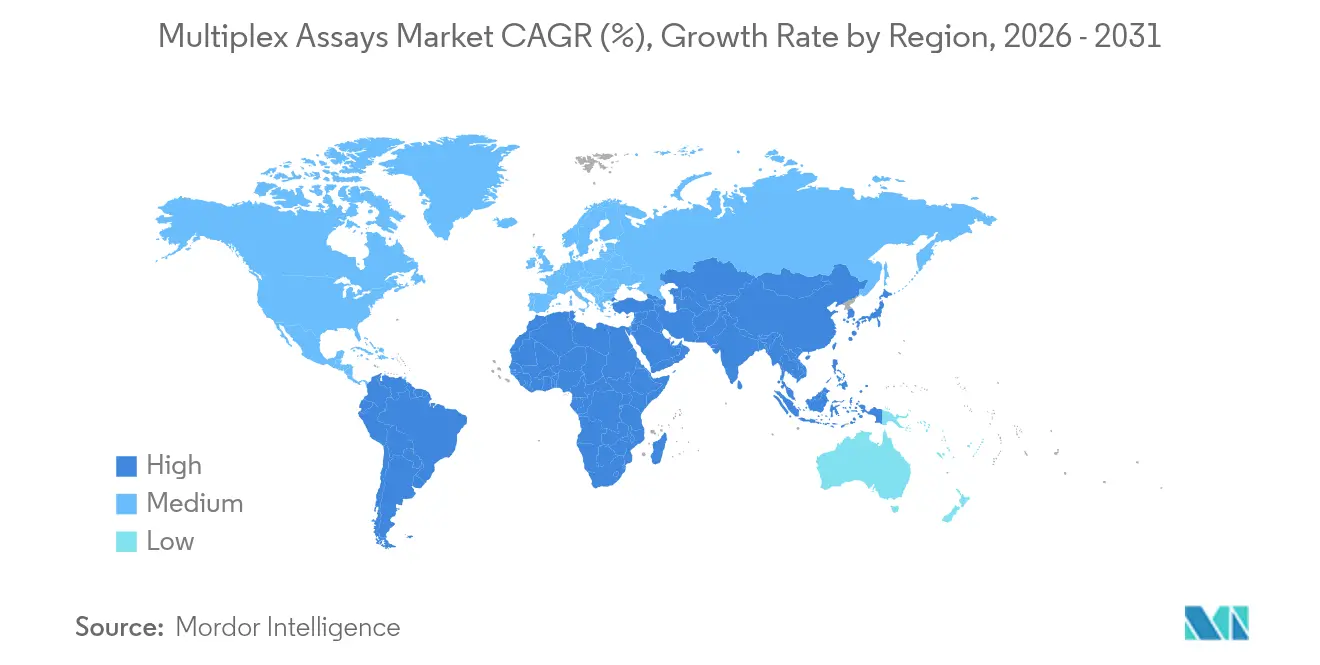

- By geography, North America dominated with 40.02% share in 2025, and Asia-Pacific is expected to achieve the fastest 16.62% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Multiplex Assays Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Precision-Personalized Medicine | +3.2% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Expanding Burden of Chronic & Infectious Diseases | +2.8% | Global, spill-over to APAC & MEA | Long term (≥ 4 years) |

| Distinct Advantages Over Singleplex Assays | +2.1% | Global | Short term (≤ 2 years) |

| Rise of CRISPR-Powered Multiplex POC Panels | +1.9% | North America & EU core, expansion to APAC | Medium term (2-4 years) |

| Clinical Deployment of 40-Plus-Color Flow Cytometry | +1.7% | North America & EU, selective APAC adoption | Medium term (2-4 years) |

| AI-Driven Assay Design & High-Dimensional Analytics | +1.5% | Global, concentrated in tech-advanced regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Precision-Personalized Medicine

Growing reliance on molecule-specific therapies demands tests that read several biomarkers at once. Thermo Fisher’s USD 3.1 billion purchase of Olink in 2024 helped bring high-throughput proximity extension protein panels into mainstream clinical workflows. The FDA endorsed TruSight Oncology Comprehensive, a 500-gene pan-tumor companion diagnostic, illustrating official support for data-dense profiling.[1]U.S. Food and Drug Administration, “FDA Approves TruSight Oncology Comprehensive as First Pan-Tumor Companion Diagnostic,” FDA, fda.gov Large reference labs now routinely combine autoantibody and complement markers to refine lupus diagnoses, studies show improved sensitivity over single analytes.[2]John Smith, “Combined T Cell Autoantibody and TC4d Testing Improves Lupus Diagnosis,” Frontiers in Immunology, frontiersin.org Health systems recognize that multiplex strategies cut repeat testing costs and speed treatment alignment, and machine-learning models further boost interpretive power by distilling complex signatures into clear guidance.

Expanding Burden of Chronic & Infectious Diseases

Aging populations drive chronic disease monitoring while recurrent outbreaks reinforce demand for broad pathogen panels. Prospective trials in intensive care settings confirm that respiratory syndromic tests improve time-to-appropriate therapy versus cultures.[3]Maria Lopez, “Rapid Respiratory Syndromic Panels Improve Critical Care Outcomes,” National Library of Medicine, ncbi.nlm.nih.gov The FDA authorized a 20-minute four-pathogen molecular test for SARS-CoV-2, Influenza A/B, and RSV, underscoring the public-health value of rapid multiplex detection.[4]U.S. Food and Drug Administration, “FDA Authorizes 4-in-1 COVID-19, Flu A/B, and RSV Molecular Test,” Federal Register, federalregister.gov Chronic kidney disease programs now integrate genomics, proteomics, and metabolomics in one assay to flag early deterioration, tightening the clinical link between multiomics and preventive care. Post-pandemic, clinicians expect panels that pivot quickly to new threats while maintaining throughput for routine surveillance, keeping the multiplex assays market on an upward trajectory.

Distinct Advantages Over Singleplex Assays

Operating economies of scale favor platforms that read many targets per well. A ddPCR-based estrogen-receptor mutation kit detects seven variants simultaneously with 0.01% allele-fraction sensitivity and uses 23% fewer reagents than running discrete tests. Academic groups have validated bead technologies capable of generating 18,000 protein measurements in one run, slashing sample use and analyst time. Fewer tube swaps minimize pre-analytical mistakes, a growing concern for labs coping with staff shortages. Pediatric and biobank specimens, often limited in volume, especially benefit from this conservation.

Rise of CRISPR-Powered Multiplex Point-of-Care Panels

Cas enzyme systems unlock accurate results without amplification. Researchers demonstrated bloodstream infection detection within minutes on a compact cartridge, offering real-time therapy guidance in emergency rooms. A disposable paper chip developed at NYU Abu Dhabi conducts multiplex viral screens under basic heating, showing promise for field clinics. Combined CRISPR-LAMP tests for monkeypox proved laboratory-grade specificity in a single isothermal step. Updated FDA guidance now details emergency pathways for these assays, accelerating commercial timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost & Complex Workflows | -2.1% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Stringent Multi-Jurisdictional Regulatory Pathways | -1.8% | Global, varying by region | Medium term (2-4 years) |

| Shortage of Bioinformatics Talent | -1.4% | Global, acute in APAC & emerging markets | Long term (≥ 4 years) |

| Supply-Chain Volatility of Rare Dyes & Beads | -1.2% | Global, supply concentrated in few regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Complex Workflows

A top-tier spectral flow cytometer costs more than USD 500,000, and supporting infrastructure adds to ownership burden. QIAGEN withdrew its automated PCR tower in 2024 due to shallow post-pandemic demand, illustrating commercial risk when capital budgets tighten. Smaller sites face steep learning curves around quality control and data handling, delaying return on investment.

Stringent Multi-Jurisdictional Regulatory Pathways

Europe’s IVDR extension under Regulation (EU) 2024/1860 sets staged deadlines but still requires rigorous performance studies. The FDA will end enforcement discretion for many laboratory-developed tests in 2025, forcing U.S. labs to seek device clearance. Germany’s BfArM demands extensive risk analyses for multiplex companion diagnostics, raising filing costs. Companies must budget for multiple validations per analyte, prolonging launch timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Protein Assays Lead, Nucleic-Acid Gains Momentum

Protein panels accounted for 41.31% of multiplex assays market share in 2025, cementing their status in drug-target validation and clinical decision support. Bead-based immunoassays and proximity extension methods enable simultaneous quantification of hundreds of cytokines from microliter samples. The nucleic-acid category is set to log a 16.98% CAGR to 2031 as CRISPR and next-generation sequencing expand beyond oncology into transplant monitoring and infectious-disease genotyping. Cell-based formats serve immuno-oncology research, while integrated protein-gene workflows herald a multiomics future.

Integration trends reshape product design. Thermo Fisher’s Stellar mass spectrometer, introduced in 2024, delivers ten-fold better quantitative sensitivity, encouraging labs to pair proteomics with genomics on shared automation. Regulatory approval of broad genomic companion diagnostics validates large-scale multiplex sequencing, reinforcing investment in nucleic-acid innovation. As these forces converge, the multiplex assays market continues to diversify across molecular classes.

By Technology: Flow Cytometry Dominance Challenged by Mass Cytometry Innovation

Flow cytometry delivered 32. 08% of 2025 revenue, thanks to entrenched instrument fleets and extensive clinical guidelines. Spectral unmixing now resolves more markers per channel, extending platform life. Mass cytometry, however, is forecast to grow at 15.06% CAGR, leveraging metal-tagged antibodies to read over 100 parameters without spectral overlap. Standard BioTools’ CyTOF XT PRO exemplifies this push toward routine trial workflows.

Real-time PCR remains vital for respiratory and sepsis panels, whereas sequencing platforms capture oncology and rare-disease testing. Luminex xMAP satisfies high-throughput protein needs, and microarrays occupy niche gene-expression applications. Competitive gaps close rapidly as AI tools ease panel design and auto-gating, encouraging broader adoption of advanced flow and mass cytometry in clinical labs.

By Application: Infectious Disease Leadership Meets Oncology Growth

Infectious disease tests delivered 38.49% of multiplex assays market size in 2025, driven by hospital demand for one-swab respiratory panels that differentiate viral and bacterial pathogens within an hour. Similar panels for bloodstream infections reduce empiric antibiotic use and length of stay. Oncology and companion diagnostics will rise at a 16.33% CAGR, buoyed by targeted therapy pipelines that require comprehensive genomic characterization before prescription.

Autoimmune, allergy, and metabolic panels are gaining relevance as clinicians seek wider biomarker snapshots for chronic-care management. Siemens rolled out a seven-plex inflammation panel in 2024, underscoring crossover potential into primary-care settings. Drug-discovery programs also rely on multiplex readouts to streamline lead optimization and safety profiling, broadening the multiplex assays market footprint beyond diagnostics.

By End-User: Pharma Leadership Drives CRO Expansion

Drug makers represented 46.12% of demand in 2025, capitalizing on multiplex assays for biomarker-guided studies and regulatory filings. Contract research organizations, forecast to grow at 17.49% CAGR, attract sponsors aiming to outsource complex assay development and global sample logistics. BD and Quest Diagnostics partnered in 2024 on flow-cytometry companion diagnostics, showing how service alliances can meet rising throughput expectations.

Academic centers remain hubs for method development, while hospital labs execute routine panels that shape real-time clinical care. The “others” bucket—biotech start-ups, public health labs, and environmental testing—adds incremental volume and innovation, sustaining a healthy pipeline of niche applications.

Geography Analysis

North America captured 40.02% of 2025 revenue owing to early technology adoption and clear reimbursement paths. Thermo Fisher pledged USD 2 billion to expand U.S. manufacturing and R&D through 2029, reinforcing the region’s leadership. Europe follows, guided by IVDR mandates that standardize performance claims, though conformity-assessment bottlenecks slow some launches.

Asia-Pacific is poised for a 16.62% CAGR as China, Japan, and South Korea boost biopharma investment and update reimbursement codes for molecular profiling. Government grants fund local manufacturing of reagents and instruments, cutting import dependency. India’s hospital chains adopt multiplex sepsis panels to reduce mortality, illustrating emerging-market potential.

The Middle East and Africa region sees pilot rollouts of syndromic respiratory panels in tertiary centers, often backed by international aid. South America shows selective growth, with Brazil’s leading oncology hospitals installing mass cytometers for immunotherapy monitoring. Across regions, differing regulatory clocks and infrastructure maturity dictate tailored go-to-market plans for multiplex assay vendors.

Regulatory Landscape

Regulation of multiplex assays covers device classification, special controls for instrumentation and software, and evidence requirements that vary with intended use. In the United States, the FDA uses Class II special controls for clinical multiplex test systems, and it has also formalized review lanes for multiplex nucleic acid tests, including respiratory viral panel multiplex NAATs that align with a 510(k) pathway under special controls (final classification order published in August 2025). Separately, the FDA finalized its Laboratory Developed Tests (LDT) rule on May 6, 2024, starting a multi-stage phaseout of enforcement discretion, with Stage 1 beginning May 6, 2025. For labs running multiplex panels as LDTs, this increases compliance and documentation expectations.

In Europe, access is governed by the In Vitro Diagnostic Regulation (IVDR, Regulation (EU) 2017/746) and its updated transitional provisions under Regulation (EU) 2024/1860, effective from July 2024. The staged end-dates extend to 31 December 2027 for Class D, 31 December 2028 for Class C, and 31 December 2029 for Class B devices. Manufacturers still need to manage near-term procedural milestones, including a formal application for conformity assessment by 26 May 2026 for Class C IVDs that previously relied on self-declaration. Across jurisdictions, requirements are more structured but demand stronger evidence packages for multiplex claims, particularly for companion diagnostics, high-plex panels, and software-driven interpretation.

Value Chain Analysis

The multiplex assays value chain starts with specialized raw materials and consumables, then moves through assay design and verification, regulated manufacturing, and downstream distribution and service. Upstream inputs include high-consistency, GMP-grade enzymes and master mixes, fluorescent probes or labeled antibodies, calibration and control materials, and beads or microfluidic consumables, which affect lot-to-lot performance in high-plex formats. Instrument and cartridge manufacturing adds precision components and embedded software, while quality management (commonly aligned with ISO 13485 practices) supports documentation, traceability, and change control.

A recurring scaling bottleneck appears in late-stage manufacturability. Design decisions made in research, such as cartridge gasket complexity, reagent chemistry, and automation compatibility, can be difficult to translate into mass production and validation as volumes rise. This has increased earlier collaboration between assay developers and manufacturing partners to reduce rework and stabilize yields. Downstream distribution runs through direct sales and channel partners serving pharmaceutical and biopharmaceutical companies, CROs, academic centers, and hospital laboratories. Reagent stability also functions as a logistics lever, since room-temperature-stable formulations reduce reliance on refrigerated cold chains in resource-limited settings.

Competitive Landscape

Moderate fragmentation persists, yet consolidation accelerates as large players buy specialized technologies. Thermo Fisher’s Olink deal added high-throughput proteomics to an already deep instrument lineup. BD’s decision to spin off Biosciences and Diagnostic Solutions reflects a sharpened focus on growth verticals.

Emerging entrants concentrate on point-of-care and AI-driven analytics. Start-ups commercialize CRISPR cartridges for 15-minute sepsis diagnosis, while academic spin-outs license isotopic bead coding to push multiplex limits past 1,000 proteins per assay. The FDA’s codification of multiplex nucleic-acid devices under 21 CFR 866.3365 creates predictable review lanes, favoring firms with robust clinical evidence. As data science melds with wet-lab workflows, competitive advantage now hinges on seamlessly integrated, cloud-enabled solutions.

Multiplex Assays Industry Leaders

Bio-Rad Laboratories, Inc.

Merck KGaA

Quansys Biosciences Inc.

Thermo Fisher Scientific

Abcam plc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity sits at the intersection of antimicrobial resistance, syndromic testing, and higher-plex molecular workflows that fit routine lab operations. In Europe, IVDR-labeled launches such as Seegene's Allplex MDRO Assay (May 2026) create a practical pathway for laboratories to broaden multiplex testing beyond respiratory panels into multidrug-resistant organism detection. That expansion creates whitespace for vendors that package assay menus alongside compliant performance files and standardized reporting. In blood screening and transfusion-related testing, Roche's cobas MPX-E assay availability in CE-mark markets (March 2026) points to ongoing demand for multiplex pathogen detection in regulated, high-throughput workflows.

Decentralization is another actionable whitespace, particularly where clinical and operational constraints favor sample-to-answer systems with simplified workflows and appropriate waivers or clearances. In the United States, Baebies' FDA 510(k) clearance and CLIA waiver for a triplex respiratory test on its Finder system (March 2026) shows momentum toward bringing multiplex NAAT capability closer to patient care. The move supports adoption in point-of-care environments that cannot sustain complex molecular infrastructure. Product roadmaps also reinforce pull-through for higher-plex assay kits and analytics: Bruker's MyGenius PRO launch at ESCMID 2026 (April 2026) and QIAGEN's plan to introduce a QIAcuity OneStep High Multiplex Probe PCR Kit (late 2026, up to 12 RNA targets) both emphasize automation and higher multiplexing. As panel complexity rises, demand for integrated software, bioinformatics support, and standardized interpretation becomes more pronounced.

Recent Industry Developments

- July 2026: Bio-Rad Laboratories launched Vericheck ddPCR Kits compatible with its QX700 platform, targeting biopharma quality control and cell and gene therapy workflows. The kits extend multiplex-ready digital PCR into regulated manufacturing and advanced therapy pipelines where rapid release testing and high sensitivity are valued.

- July 2025: Bio-Rad Laboratories expanded its droplet digital PCR portfolio after acquiring Stilla Technologies and introduced the QX Continuum ddPCR system alongside the QX700 series platforms. This combination strengthened instrument throughput and multiplexing capability, supporting labs that are standardizing on digital PCR for oncology research and broader molecular testing needs.

- April 2024: Merck KGaA (MilliporeSigma) launched the Aptegra CHO genetic stability assay, an all-in-one NGS-based test positioned to replace multiple traditional assays in biosafety testing. Consolidating several checks into a single workflow shortens testing cycles for biologics development and increases demand for multiplex-style, information-dense readouts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from multiplex assay solutions used to detect or measure two or more analytes in a single sample, including reagent kits, instruments, and supporting software used in research, clinical testing, and drug development.

Scope exclusions: Single-analyte (singleplex) assay kits and dedicated next-generation sequencing platforms are excluded from this sizing.

Segmentation Overview

- By Type

- Cell-based multiplex assays

- Protein multiplex assays

- Nucleic-acid multiplex assays

- Bead-based immunoassays

- By Technology

- Multiplex real-time PCR

- Flow cytometry

- Bead-based xMAP/Luminex

- Next-generation sequencing-based

- Mass cytometry (CyTOF)

- Microarray & others

- By Application

- Infectious disease diagnostics

- Oncology & companion diagnostics

- Autoimmune & allergy testing

- Drug discovery & biomarker validation

- Others

- By End-User

- Pharmaceutical & biopharmaceutical companies

- Academic & research institutes

- Contract research organizations

- Hospitals & diagnostic laboratories

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build the demand story, and collect measurable inputs that can be checked year over year. We mainly referenced public sources such as the US FDA databases for diagnostics and clearances, the US NIH and ClinicalTrials.gov for research activity signals, the US CDC and WHO for disease and testing-related indicators, and peer-reviewed journals indexed in PubMed for adoption and workflow trends.

On the supply side, we reviewed company filings, annual reports, investor presentations, and press releases to understand product mix and geographic exposure, then cross-checked those points against trade association updates when available. A paid subscription for company financials and intelligence and a patent database were used selectively to confirm product focus shifts and the timing of platform launches. This desk source list is illustrative and not exhaustive, and additional public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the model inputs that are usually sensitive in multiplex assays, especially price bands, replacement cycles, and the mix between consumables and instruments. We spoke with stakeholders across assay manufacturers, distributors, clinical labs, hospital labs, and life science research users, and we balanced feedback across APAC, EMEA, and the Americas to confirm region-level adoption patterns and budget cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | APAC: 44% |

| Mid tier: 52% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 16% | Managers: 54% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the demand pool was reconstructed from testing and research activity signals, and then filtered by multiplex adoption rates by application. Once that structure was in place, we corroborated the results with selective bottom-up approximations such as sampled average selling price (ASP) by product category multiplied by estimated run-rate volumes for consumables, plus channel checks on instrument placements to confirm the installed base.

Key model inputs included, as examples, the split between clinical and research usage, average panel size trends in multiplex formats, instrument replacement and service-life assumptions, reagent pull-through per installed instrument, and regional purchasing patterns that affect realized ASPs. When interview feedback suggested gaps in a specific country or application, proxy indicators were applied (such as research funding intensity or diagnostic testing intensity) and then adjusted back through follow-up validation. Forecasting relied on scenario analysis supported by a simple multivariate regression check, using drivers like R and D spending signals, diagnostic test volumes, and expected ASP progression to keep growth paths realistic across regions.

Data Validation & Update Cycle

Validation was done through multiple checks so the final totals remain consistent with real-world signals and do not overreact to a single input. We compared the model outputs against independent indicators like clinical testing activity, public research funding direction, and the implied consumables-to-instrument revenue balance, then reviewed any anomalies before internal sign-off.

Reports are refreshed annually, and interim updates are triggered when material events occur (such as major regulatory changes, large launches, or sharp currency movements). Before delivery, a fresh review pass is completed so assumptions, currency conversion timing, and ASP ranges reflect the latest information available.

Mordor Intelligence's Multiplex Assays Market Sizing Compared With Other Published Estimates

It is normal to see different market values published for multiplex assays, even when the topic name looks the same. The gaps usually come from timing choices, product boundaries, and how each publisher treats prices and demand indicators across regions.

In our case, the spread is most influenced by refresh cadence and currency timing, because ASPs for reagent consumables and instruments can shift within a year as purchasing contracts reset, and these checks are re-run before final numbers are locked in at Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.30 B (2026) | |

| Global Consultancy A | USD 4.05 B (2024) | Uses an earlier base year and a broader product and service framing, which can pull in adjacent categories and higher software and services allocations, and it may apply smoother ASP progression that does not reflect regional purchasing cycle resets. |

| Industry Publisher B | USD 1.82 B (2024) | Anchors the estimate to a narrower 2024 revenue pool, which can undercount instrument placements and downstream consumables pull-through in faster-growing regions if adoption rates are not revalidated for clinical versus research use cases. |

Taken together, the benchmark table shows that most differences can be traced to scope edges and timing choices, not only growth math. By keeping the scope tied to multiplex formats and by rechecking ASPs, installed base signals, and regional adoption assumptions before the annual refresh, the final estimate stays transparent and repeatable for planning.

Key Questions Answered in the Report

What is the current value of the multiplex assays market?

The multiplex assays market is valued at USD 2.30 billion in 2026 and is projected to reach USD 4.52 billion by 2031.

Which segment dominates multiplex assay types?

Protein multiplex assays lead with 41.31% market share due to their established role in biomarker validation.

Why are CRISPR-based multiplex panels important?

CRISPR workflows deliver fast, amplification-free detection, enabling point-of-care testing that meets modern infection-control demands.

Which region is growing fastest in multiplex assays adoption?

Asia-Pacific is set to expand at a 16.62% CAGR thanks to rising biopharma investment and supportive regulatory reforms.

What is the chief barrier to wider multiplex assay uptake?

High capital equipment costs and complex workflows remain the main hurdles, especially for smaller or resource-limited laboratories.

Page last updated on: