Brazil Renewable Gas From Waste Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

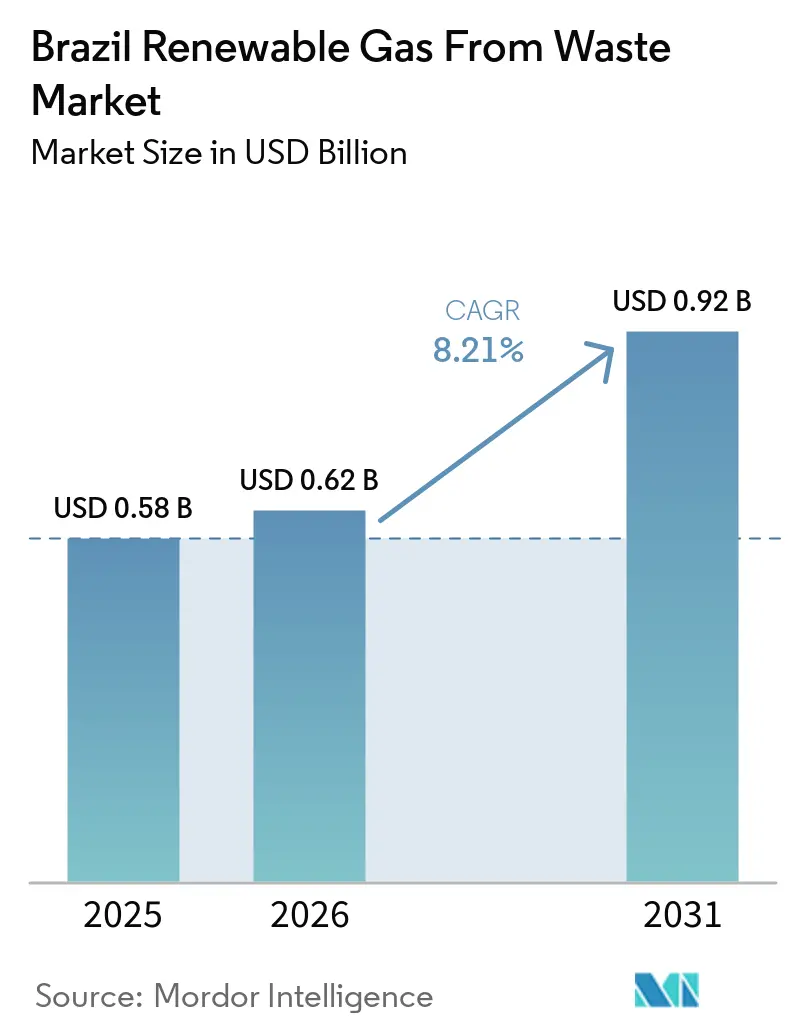

| Base Year Market Size (2025) | USD 0.58 Billion |

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 0.92 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Renewable Gas From Waste Market Analysis by Mordor Intelligence

The Brazil Renewable Gas From Waste Market size was valued at USD 0.58 billion in 2025 and is estimated to grow from USD 0.62 billion in 2026 to reach USD 0.92 billion by 2031, at a CAGR of 8.21% during the forecast period (2026-2031).

Brazil's renewable gas market, primarily driven by waste, is accelerating its growth trajectory, largely due to a surge attributed to a significant policy shift marked by the enactment of Law No. 14,993/2024 and the September 2025 decree that activated the National Biomethane Program. These legislative moves have elevated the sector from a modest biogas niche to a robust compliance-driven gas market, complete with formal buyers and enforceable blending obligations. Agricultural residues continue to dominate as the primary feedstock. Meanwhile, biogas upgrading is gaining momentum, and biomethane is increasingly in the spotlight due to its potential to generate certificate revenue and meet formal offtake demands. However, with the 2026 blending target set at 0.5% below the statutory 1% floor due to limited supply, there's a window of opportunity for mid-tier producers and cooperative mills to secure long-term contracts before obligations tighten. Petrobras has bolstered financing prospects, evidenced by its January 2025 tender for 11-year biomethane supply contracts. Yet challenges remain in inland logistics, and the ambiguous carbon-intensity disclosures of Certificados de Garantia de Origem do Biometano (Biomethane Guarantees of Origin, or CGOB) certificates are hindering project economics in certain segments of Brazil's renewable gas market.

Key Report Takeaways

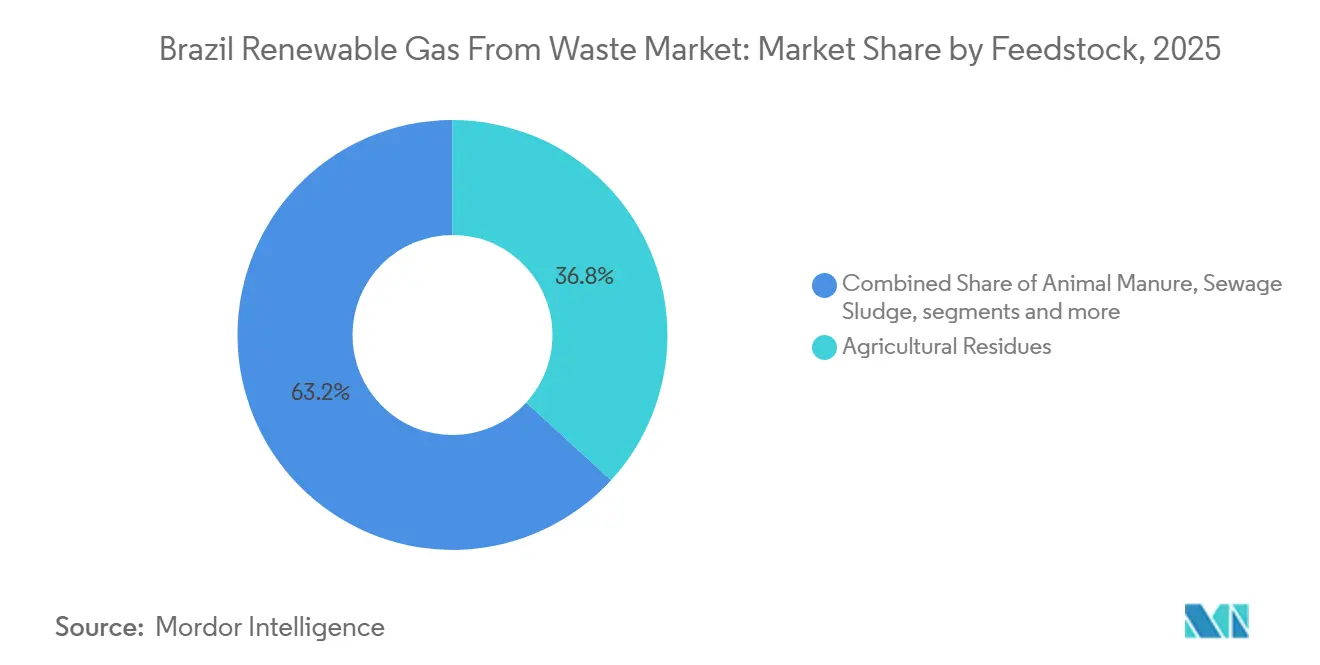

- By feedstock, agricultural residues held a 36.80% of the Brazil renewable gas from waste market size in 2025, while food waste is forecast to expand at a 10.20% CAGR through 2031.

- By technology, anaerobic digestion held a 45.10% of the Brazil renewable gas from waste market share in 2025, while biogas upgrading systems are projected to grow at an 11.60% CAGR through 2031.

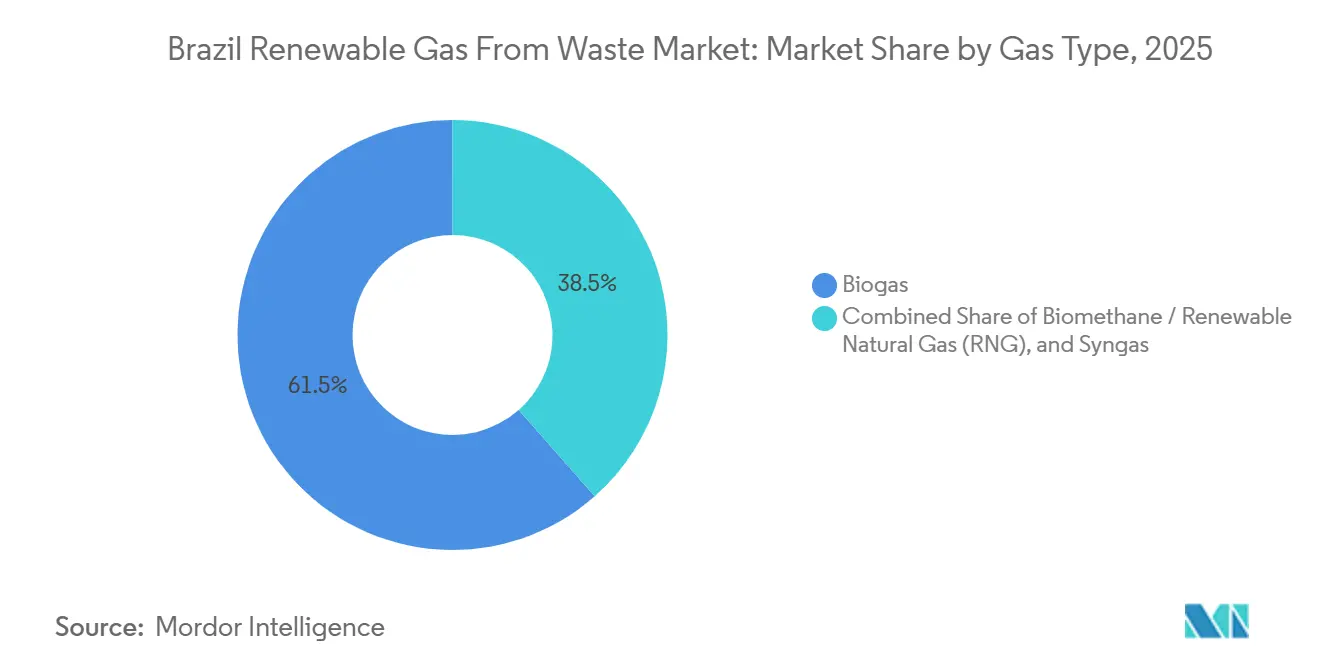

- By gas type, biogas accounted for 61.50% of the Brazil renewable gas from waste market in 2025, while biomethane/renewable natural gas is expected to grow at a 12.40% CAGR through 2031.

- By application, electricity generation accounted for 39.70% of the Brazil renewable gas from waste market in 2025, while transportation fuel is set to grow at a 13.10% CAGR through 2031.

- By component, digesters and fermentation systems held a 32.60% share in 2025, while gas processing and upgrading units are projected to expand at a 12.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Renewable Gas From Waste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel of the Future Law Creating a Mandatory Biomethane Blending Market | +2.8% | National, with concentrated compliance obligations on major natural gas distributors in São Paulo, Rio de Janeiro, and Minas Gerais | Short term (≤ 2 years) |

| Sugarcane Agro-Industrial Residues Providing Structurally Competitive Feedstock | +2.1% | São Paulo, Mato Grosso do Sul, and Goiás, with spillover to Minas Gerais and Paraná | Medium term (2-4 years) |

| RenovaBio CBIO Carbon Credits Adding Bankable Revenue to Project Economics | +1.4% | National, with primary CBIO demand concentrated among São Paulo and Rio de Janeiro fuel distributors | Short term (≤ 2 years) |

| Petrobras Long-Term Procurement Initiative Signaling Institutional Offtake | +1.0% | National, with delivery points across refineries, thermoelectric plants, and pipeline grids, with inland spillover via CGOB certificates | Short term (≤ 2 years) |

| Basic Sanitation Law Redirecting MSW into Engineered Landfills for Gas Recovery | +0.7% | National, with the highest near-term impact in the Northeast and the Center-West | Medium term (2-4 years) |

| Corporate ESG Commitments Driving Pre-Mandate Industrial Offtake Demand | +0.5% | Southeast and South Brazil, driven by industrial clusters in São Paulo, Rio Grande do Sul, and Paraná | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fuel of the Future Law Creating a Mandatory Biomethane Blending Market

Law No. 14,993/2024, enacted in October 2024, was the clearest structural break for the Brazil renewable gas from waste market as it changed biomethane from a voluntary product into a compliance tool.[1]Brazilian Federal Government, “Decree No. 12,614/2025,” Presidência da República, planalto.gov.br The law requires natural gas producers and importers to meet annual greenhouse gas reduction targets through biomethane use or by purchasing Biomethane Guarantees of Origin (CGOBs).[2]World Biogas Association, “Brazil Advances with a New Regulatory Framework for Biofuels,” World Biogas Association, worldbiogasassociation.org Its penalty structure matters because fines are set above the financial gain from avoiding compliance, which gives the mechanism a stronger enforcement base than earlier incentive programs. The Conselho Nacional de Política Energética (CNPE) set the 2026 obligation at 0.5%, and the government also created a monitoring mechanism to track progress toward restoring the 1% level as biomethane supply improves. That gap between the reduced 2026 target and the legal floor effectively marks a measurable supply shortfall, and it gives the fastest movers in the Brazil renewable gas from waste market a chance to capture mandate-linked premiums before the obligation rises further.

Sugarcane Agro-Industrial Residues Providing Structurally Competitive Feedstock

Brazil’s sugarcane complex gives the Brazil renewable gas from waste market a feedstock advantage that is hard for other waste streams to match because volumes are large, recurring, and close to existing industrial energy systems.[3]Ministry of Mines and Energy and Empresa de Pesquisa Energética, “Caderno de Oferta de Biocombustíveis, Plano Decenal de Expansão de Energia 2035,” Governo Federal, gov.br A joint study by Brazil's Ministry of Mines and Energy (MME) and Energy Research Office (EPE), published in September 2024, estimated that vinasse, filter cake, straw, and sugarcane tops could yield 6.4 billion normal cubic meters (Nm³) of biomethane annually, equivalent to nearly 10% of Brazil's natural gas consumption in 2024. The commercial base was already growing by the end of 2025, when 23 agricultural waste biomethane units were either completed or under construction, suggesting a near-doubling of installed biomethane capacity. Vinasse also improves project economics because anaerobic digestion reduces the wastewater-handling burden for mills, giving that feedstock a cost position that municipal solid waste and food waste projects often cannot match. The Cocal plant in Narandiba demonstrated that this advantage can extend beyond on-site use, as it became the first Brazilian agricultural biomethane project to inject into an urban distribution network serving residential and commercial users in Presidente Prudente.

RenovaBio CBIO Carbon Credits Adding Bankable Revenue to Project Economics

RenovaBio provides the Brazil renewable gas from waste market with a second source of revenue, as CBIOs can be sold separately from the gas itself. The 2025 CBIO (Decarbonization Credit) target was 40.39 million credits, and ANP (Agência Nacional do Petróleo, Gás Natural e Biocombustíveis / National Agency of Petroleum, Natural Gas and Biofuels) reported that 40.06 million were retired by year-end, indicating compliance of 99%. ANP Resolution No. 984/2025 refined the certification method under the RenovaBio (National Biofuels Policy) 2025-2035 framework, tightening audit rules and extending the program horizon, both of which support investor confidence in future cash flows. Because CBIO values are tied to decarbonization performance rather than directly to gas commodity prices, they can soften the earnings volatility that would otherwise come from gas price cycles. Decree No. 12,614/2025 also opened a path for the CBIO platform to record CGOBs (Certificados de Garantia de Origem do Biometano / Biomethane Guarantees of Origin), which could eventually simplify the revenue stack for producers across the Brazil renewable gas from waste market.

Petrobras Long-Term Procurement Initiative Signaling Institutional Offtake

Petrobras changed the commercial backdrop of the Brazil renewable gas from waste market when it launched the first public biomethane procurement tender in January 2025. The call requested a minimum of 20,000 m³/day per supplier and offered contract terms of up to 11 years with deliveries starting in January 2026. More than 90 proposals were submitted, and 20 moved to negotiation, while Petrobras accepted proposals for both physical biomethane and CGOB certificate supply. Petrobras estimated its 2026 compliance need at nearly 700,000 m³/day, exceeding the country’s authorized production capacity at the time. That mismatch supports pricing power for early suppliers. The longer contract duration also gives lenders the tenor they need to finance digesters and upgrading units. Petrobras’ 2025-2029 strategic plan shows that the company now views biomethane as an investable line of business rather than only a compliance obligation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Coastal Pipeline Concentration Limiting Inland Biomethane Grid Integration | -1.8% | Interior of São Paulo, Mato Grosso do Sul, Minas Gerais, and Goiás, where feedstock potential is high but pipeline access is limited | Medium term (2-4 years) |

| High Production Costs Reduce Competitiveness Against Fossil Gas Alternatives | -1.2% | National, with the strongest impact on smaller plants and projects located far from gas distribution networks | Short term (≤ 2 years) |

| Absence of Carbon Intensity Disclosure in CGOB Certificates Reducing Credibility | -0.7% | National, with implications for voluntary carbon market participation and external validation | Medium term (2-4 years) |

| Underdeveloped Waste Collection Infrastructure Constraining MSW Feedstock Reliability | -0.5% | Northeast, North, and Center-West Brazil, especially where open dump sites remain active | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Coastal Pipeline Concentration Limiting Inland Biomethane Grid Integration

The Brazil renewable gas from waste market faces its most visible physical constraint: a mismatch between the potential of inland feedstocks and a transport grid that remains concentrated near the coast. ANP reported that Brazil’s gas transport system comprised 51 pipelines spanning 9,389 km, and no new pipeline authorizations or capacity expansions are under review in 2026. Sugarcane mills, feedlots, and organic waste generators are concentrated in inland states such as Mato Grosso do Sul, Goiás, and the interior of São Paulo, meaning the best production zones are often distant from grid injection points. That leaves many projects dependent on compressed biomethane trucking, and the extra logistics cost of BRL 0.50 (USD 0.09) to BRL 0.80 (USD 0.14) per m³ above grid injection compresses returns, especially at smaller plants. TBG’s biomethane hub work and EPE’s gas infrastructure planning provide a possible route to better integration. Still, the main benefits will come after 2028, which limits near-term inland penetration of Brazil renewable gas from waste.

High Production Costs Reduce Competitiveness Against Fossil Gas Alternatives

Production costs remain a direct brake on the Brazil renewable gas from waste market, as the levelized cost of injected biomethane still exceeds that of fossil gas in many use cases. Technical analysis used in Brazil’s regulatory discussion placed the levelized cost of biomethane at BRL 2.20 (USD 0.40) to BRL 3.30 (USD 0.60) per m³ at the plant gate. At the same time, natural gas prices for large industrial buyers often fall below that range. Brazil also does not yet offer a price distinction between biomethane and fossil natural gas, once both enter the same grid, so many projects still depend on CBIO and CGOB revenue to close the economic gap. Capital intensity adds another hurdle, as a mid-scale plant processing 1.6 million liters of vinasse per day requires an investment of close to USD 24 million, which is too large for many smaller cooperatives and municipalities without concessional finance. Imported upgrading systems also keep project budgets exposed to currency swings because Brazil has not yet built a strong local manufacturing base for membrane separation or pressure swing adsorption equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Agricultural Residues Anchor a Diversified Feedstock Base

Agricultural residues accounted for 36.80% of the Brazil renewable gas from waste market share in 2025, while food waste is projected to expand at a 10.20% CAGR over 2026-2031. The agricultural stream converts vinasse, filter cake, bagasse, and tops into commercial gas while reducing wastewater management costs for mills, which is why the segment has become the main feedstock anchor for the Brazil renewable gas from waste market. That structure makes it more competitive than feedstocks that require distributed collection, sorting, and longer transport before digestion can begin. Animal manure also remains a large untapped resource in Mato Grosso, Paraná, and Rio Grande do Sul. However, its dispersed origin means aggregation and transport systems still need to mature before the full opportunity can be realized.

Municipal solid waste used to dominate the commercial base because landfill gas was the most direct route to monetization before the new mandate period, and that legacy still gives it relevance in current project pipelines. The balance is now changing because agricultural projects are scaling faster and because food waste is gaining policy support through wider urban waste separation. Sewage sludge and industrial organic waste currently account for a smaller share. Yet, both are likely to grow in volume as the sanitation universalization target for 2033 expands the stock of treated effluent available for digestion and co-processing. Landfill waste and food waste also benefit from the updated National Solid Waste Plan, which sets 2040 targets of 252 MW for landfill gas and 69 MW for anaerobic digestion, creating an investment queue across municipalities. The certification base for landfill and sewage feedstocks remains directly tied to ANP rules, which means regulatory clarity in those channels will still shape project timing across the Brazil renewable gas from waste market.

By Technology: Anaerobic Digestion Dominates as Upgrading Systems Scale

Anaerobic digestion held 45.10% of the Brazil renewable gas from waste market share in 2025, while biogas upgrading systems are projected to grow at an 11.60% CAGR over 2026-2031. This installed base reflects years of local engineering experience in sanitation and agro-industrial applications, making digestion the most established technology platform in the Brazil renewable gas from waste market. Biogas upgrading systems are projected to record the fastest CAGR through 2031, as producers now have stronger economic reasons to shift from power generation to pipeline-grade biomethane. ANP purity specifications and the economics of CGOB issuance both reward gas upgrading over simple electricity output.

A 2025 industry study found that anaerobic digestion can recover up to 84% of the generated gas, while conventional landfill gas recovery may capture only 3%, supporting the shift toward more productive process routes. Landfill gas recovery still matters because it can be added to existing waste infrastructure with a lower marginal investment than a greenfield digester system. Gasification and pyrolysis remain earlier-stage options in Brazil. They are more suited to dry biomass streams, so their commercial role is more likely to expand in the latter part of the forecast period. The International Council on Clean Transportation (ICCT) also noted in February 2026 that Brazil’s fuel policy package supports methane-capable vehicles and agricultural machinery, which should help sustain demand for compression and dispensing systems beyond the grid injection route. That policy signal supports continued investment in upgrading infrastructure across the Brazil renewable gas from waste market.

By Gas Type: Biogas Leads While Biomethane Narrows the Gap

Biogas accounted for 61.50% share of the Brazil renewable gas from waste market size in 2025. The larger biogas base reflects the country’s accumulated stock of landfill gas and agricultural projects that used gas for on-site electricity generation or combined heat and power rather than upgrading it. This installed base gives biogas a clear volume lead at present, even as the sector's commercial model is starting to change.

Biomethane / renewable natural gas (RNG) is projected to expand at a 12.40% CAGR over 2026-2031. The segment is gaining popularity faster because it can participate in compliance markets and long-term contracts in ways that raw biogas usually cannot. In a bid to restore the 1% level as supply conditions improve, the Conselho Nacional de Política Energética (CNPE) has set the 2026 obligation at 0.5%. Additionally, the government has instituted a monitoring mechanism to oversee this progress. That mechanism reduces policy uncertainty because future target increases are linked to demonstrated capacity growth rather than to arbitrary annual changes. As a result, biomethane is moving from a niche, premium fuel to a more strategic decarbonization fuel in the Brazil renewable gas from waste market. Syngas remains the smallest gas type because it is still tied mainly to pilot-scale or early industrial gasification pathways.

By Application: Power Generation Leads, but Transportation Fuel Disrupts the Mix

Electricity generation captured 39.70% share of the Brazil renewable gas from waste market size in 2025, while transportation fuel is projected to grow at a 13.10% CAGR over 2026-2031. Electricity generation led because early landfill and agro-industrial projects were designed around captive power systems and distributed generation rules rather than around pipeline injection. That legacy kept power generation as the main end use even after the sector began to broaden into other applications. It also reflects the practical ease of monetizing raw biogas through existing power equipment before biomethane demand became more formalized.

Grid injection is becoming more important because the same project infrastructure can serve industrial, commercial, residential, and transport demand, where distribution systems are available. Cocal’s Narandiba facility demonstrated this in January 2026, when agricultural biomethane entered the Presidente Prudente network for multiple end uses simultaneously. Combined heat and power still plays a role in agro-industrial and industrial sites that need thermal efficiency and on-site energy use. Industrial heating and residential heating remain smaller segments because Brazil’s climate limits heating demand, although some industrial users are willing to pay more for decarbonized heat. Mondelēz Brasil’s 2026 agreement with Gás Verde reflects that willingness and shows how the Brazil renewable gas from waste market is adding private industrial demand before the mandate fully deepens.

By Component: Digesters Drive Revenue as Processing Units Scale

Digesters and fermentation systems held 32.60% share of the Brazil renewable gas from waste market size in 2025, while gas processing and upgrading units are projected to expand at a 12.80% CAGR over 2026-2031. Their leading position reflects the capital intensity of primary gas generation infrastructure across both agricultural and municipal waste projects. As sugarcane mills entered the sector through vinasse-based projects and landfill operators upgraded collection assets, digesters remained the largest single destination for project capital. This kept the digestion layer at the center of component demand during the earlier buildout phase of the Brazil renewable gas from waste market.

Gas collection systems, compressors, and storage remain important enabling components because they determine how much of the feedstock resource can actually be captured and delivered. Their role is especially important in landfill projects where retrofits can unlock additional gas from older waste cells. Power generation equipment is likely to decline as a share of total spending, even if absolute CHP capacity continues to grow at co-located industrial sites. Monitoring and control systems are also becoming more important because certification and injection rules require metering-grade quality verification at delivery points. That compliance layer means digital monitoring is taking on a larger role in the Brazil renewable gas from waste market as projects move from basic biogas generation toward certified biomethane supply.

Geography Analysis

The Southeast held the largest share of authorized biomethane capacity in 2025, making it the core operating zone of the Brazil renewable gas from waste market. ANP-linked data cited in 2025 showed more than 547,770 m³/day of operational and near-term capacity in the Southeast, led by São Paulo and Rio de Janeiro. São Paulo’s position comes from the overlap of sugarcane mill density, a more advanced gas distribution system, and proximity to Petrobras refineries and thermoelectric demand points. Empresa de Pesquisa Energética (EPE) hub mapping identified Sertãozinho and Seropédica as likely aggregation nodes because they combine feedstock concentration with better access to gas infrastructure. Gás Verde’s Seropédica expansion plan also suggests that the Southeast will keep its lead through the first half of the forecast period.

The Northeast is the fastest-growing regional cluster in the Brazil renewable gas from waste market because large landfill assets, sanitation needs, and development finance are converging in the same corridor. Orizon’s Jaboatão plant in Pernambuco, inaugurated in March 2026, cost BRL 258 million (USD 46.6 million) and added 108,000 m³/day of biomethane capacity with direct injection into Copergás’ network. Banco do Nordeste helped finance the project, demonstrating how regional development funding can accelerate project buildout in areas where private infrastructure is still catching up. The region also stands to gain as compliance with the Basic Sanitation Law gradually redirects more organic waste to engineered landfills.

The Center-West and South have strong medium-term potential due to cattle, swine, poultry, sugarcane, and corn residues, yet both regions face the largest access gap to the coastal gas grid. Mato Grosso, Goiás, Mato Grosso do Sul, and Rio Grande do Sul, therefore, have feedstock strength without equivalent transport access. TBG’s hub model and EPE’s integrated gas infrastructure planning could improve that connection later in the forecast window, but these projects will not materially ease the constraint in the 2026-2028 period. The North remains a small contributor because waste generation is dispersed, gas infrastructure is limited, and logistics costs remain high across the Brazil renewable gas from waste market.

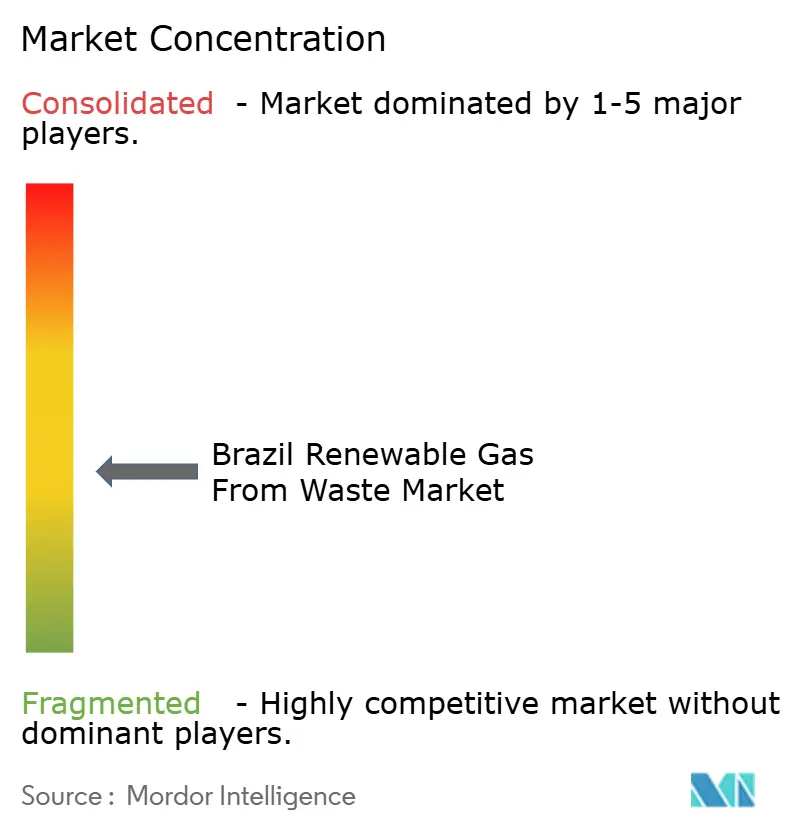

Competitive Landscape

The Brazil renewable gas from waste market is moderately fragmented, with a leading tier of waste management groups and agro-industrial operators holding the main ANP-authorized production positions, while a broader set of developers and utility-linked entrants is still building scale. Companies that control both feedstock and conversion assets have an advantage because concessions on waste or mill residue access reduce raw material risk and improve project bankability. This advantage is stronger in landfill gas and sugarcane-based projects, where long-term feedstock access is often more important than any technology difference. The current competitive advantage is therefore mostly contractual and logistical rather than technological. Petrobras’ willingness to consider minority participation in biomethane special-purpose vehicles adds a new capital-raising route that could favor producers willing to exchange some ownership for lower financing costs.

Strategy in the Brazil renewable gas from waste market centers on feedstock aggregation, early offtake alignment, and the stacking of gas revenue with decarbonization certificates. Petrobras’ January 2025 tender is the clearest example of the second vector because it offered an institutional buyer, contract visibility, and long duration at a point when national supply was still below expected compliance demand. Gás Verde’s January 2026 investment plan is an example of the first vector because it aims to scale national output through plant conversions and a much larger Seropédica complex. Orizon’s Jaboatão project shows the same pattern in municipal waste, where landfill control and direct pipeline access together create a stronger commercial position.

Near-term white space remains strongest in Northeast landfill assets and in food waste, where capture rates are still low, and project competition is not yet as dense as in sugarcane-based corridors. Smaller cooperative mills are beginning to enter because vinasse-based biomethane now has a clearer route to CGOB-linked monetization under the new rules. The pending finalization of ANP certification details also creates a race to qualify supply before reporting cycles become more demanding. Buyers and producers are therefore moving contract formation earlier than they did in the earlier biogas-only phase of the Brazil renewable gas from waste market. That change is lifting competitive intensity, but it has not yet removed the advantage held by firms that secured feedstock positions before the mandate cycle began.

Brazil Renewable Gas From Waste Industry Leaders

Gás Verde

Orizon Valorização de Resíduos S.A.

Petróleo Brasileiro S.A.

Raízen Geo Biogás S.A.

Marquise Serviços Ambientais S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Orizon inaugurated its Jaboatão (Pernambuco) biomethane plant, with an investment of USD 46.6 million and a production capacity of 108,000 m³/day. The facility injects biomethane directly into Copergás' regional gas pipeline, the first in the Northeast to achieve grid injection at this scale, and was partially financed by Banco do Nordeste (BNB).

- January 2026: Gás Verde announced a USD 159 million (BRL 900 million) three-year investment program to expand its national biomethane output from 160,000 m³/day to 650,000 m³/day by 2029. The plan includes converting 10 biogas plants to biomethane-grade production across 7 states and developing a new Seropédica (Rio de Janeiro) complex targeting up to 280,000 m³/day, potentially the largest single biomethane production site globally.

- January 2026: Cocal's Narandiba (São Paulo) sugarcane mill-based biomethane plant became the first in Brazil to supply an urban distribution network for residential, commercial, industrial, and CNG station use in Presidente Prudente, as reported by ANP and Valor Internacional. The milestone demonstrates that agricultural-source biomethane can serve multi-sector urban demand at a commercial scale.

- September 2025: The Brazilian Federal Government published Decree No. 12,614/2025, formally regulating the National Biomethane Program under Law No. 14,993/2024. The decree mandated ANP to issue procedures for biomethane certification within 180 days and established the CGOB certificate architecture, with the CBIO platform to be adapted to record CGOBs.

Brazil Renewable Gas From Waste Market Report Scope

The Brazil Renewable Gas From Waste Market Report is Segmented by Feedstock (Municipal Solid Waste, Agricultural Residues, and More), by Technology (Anaerobic Digestion, Landfill Gas Recovery, and More), by Gas Type (Biogas, and More), by Application (Electricity Generation, Grid Injection, and More), and by Component (Gas Collection, Digesters & Fermentation, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Municipal Solid Waste (MSW) |

| Agricultural Residues |

| Animal Manure |

| Industrial Organic Waste |

| Sewage Sludge |

| Food Waste |

| Others |

| Anaerobic Digestion |

| Landfill Gas Recovery |

| Gasification |

| Pyrolysis |

| Biogas Upgrading Systems |

| Others |

| Biogas |

| Biomethane / Renewable Natural Gas (RNG) |

| Syngas |

| Electricity Generation |

| Combined Heat & Power (CHP) |

| Grid Injection |

| Transportation Fuel |

| Industrial Heating |

| Residential & Commercial Heating |

| Others |

| Gas Collection Systems |

| Digesters & Fermentation Systems |

| Gas Processing & Upgrading Units |

| Compressors & Storage Systems |

| Power Generation Equipment |

| Monitoring & Control Systems |

| Others |

| By Feedstock | Municipal Solid Waste (MSW) |

| Agricultural Residues | |

| Animal Manure | |

| Industrial Organic Waste | |

| Sewage Sludge | |

| Food Waste | |

| Others | |

| By Technology | Anaerobic Digestion |

| Landfill Gas Recovery | |

| Gasification | |

| Pyrolysis | |

| Biogas Upgrading Systems | |

| Others | |

| By Gas Type | Biogas |

| Biomethane / Renewable Natural Gas (RNG) | |

| Syngas | |

| By Application | Electricity Generation |

| Combined Heat & Power (CHP) | |

| Grid Injection | |

| Transportation Fuel | |

| Industrial Heating | |

| Residential & Commercial Heating | |

| Others | |

| By Component | Gas Collection Systems |

| Digesters & Fermentation Systems | |

| Gas Processing & Upgrading Units | |

| Compressors & Storage Systems | |

| Power Generation Equipment | |

| Monitoring & Control Systems | |

| Others |

Key Questions Answered in the Report

What is the current size of Brazil's renewable gas from waste activity, and where is it headed by 2031?

The Brazil renewable gas from waste market is valued at USD 0.62 billion in 2026 and is forecast to reach USD 0.92 billion by 2031, with a 8.21% CAGR.

What is driving faster expansion after 2025?

The key change is the policy shift created by Law No. 14,993/2024 and Decree No. 12,614/2025, which turned biomethane into a compliance-linked gas product with certificate revenue and formal offtake demand.

Which feedstock has the strongest commercial base in Brazil?

Agricultural residues lead because sugarcane mills generate large, recurring residue streams, and vinasse digestion also reduces wastewater-handling costs.

Why is biomethane growing faster than biogas?

Biomethane can access CGOB revenue, Petrobras-style long-term supply contracts, and future blending compliance demand, while raw biogas often remains tied to on-site power uses.

Which region is leading project deployment?

The Southeast remains the most mature region because it combines sugarcane density, better gas distribution links, and proximity to refinery and industrial demand.

What is the biggest constraint on project scale-up?

The main constraint is the mismatch between inland feedstock availability and a pipeline network that remains concentrated near the coast, which increases logistics costs for many producers.

Page last updated on: