Spasticity Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

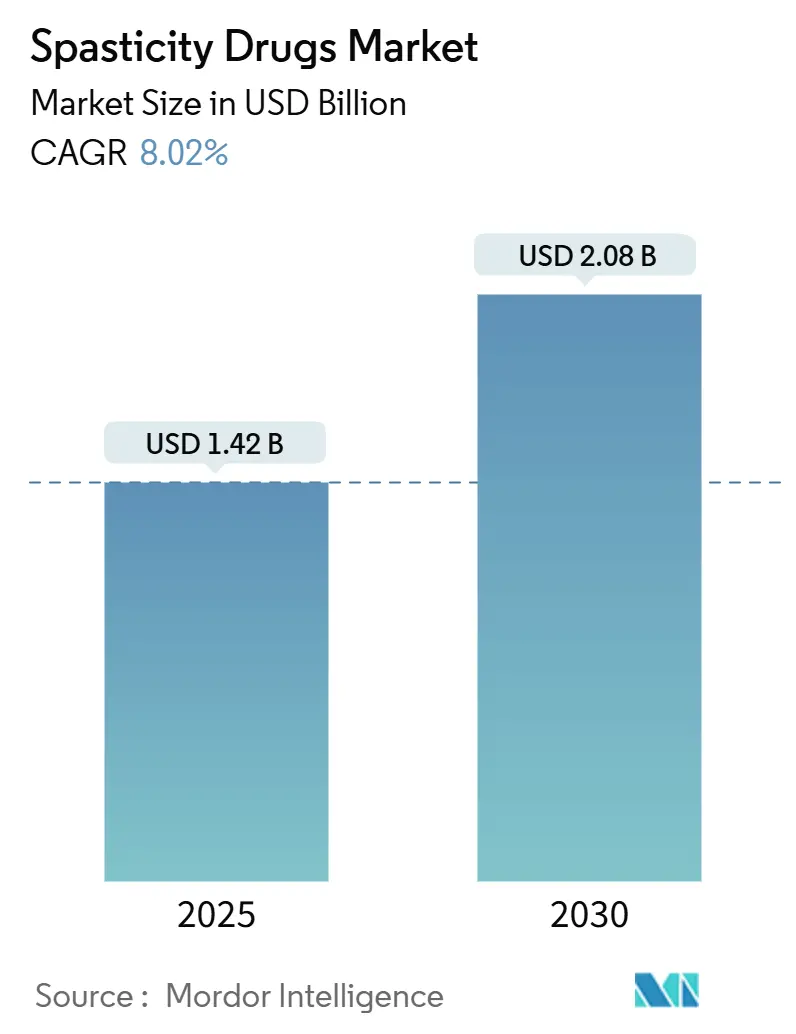

| Market Size (2025) | USD 1.42 Billion |

| Market Size (2030) | USD 2.08 Billion |

| Growth Rate (2025 - 2030) | 8.02% CAGR |

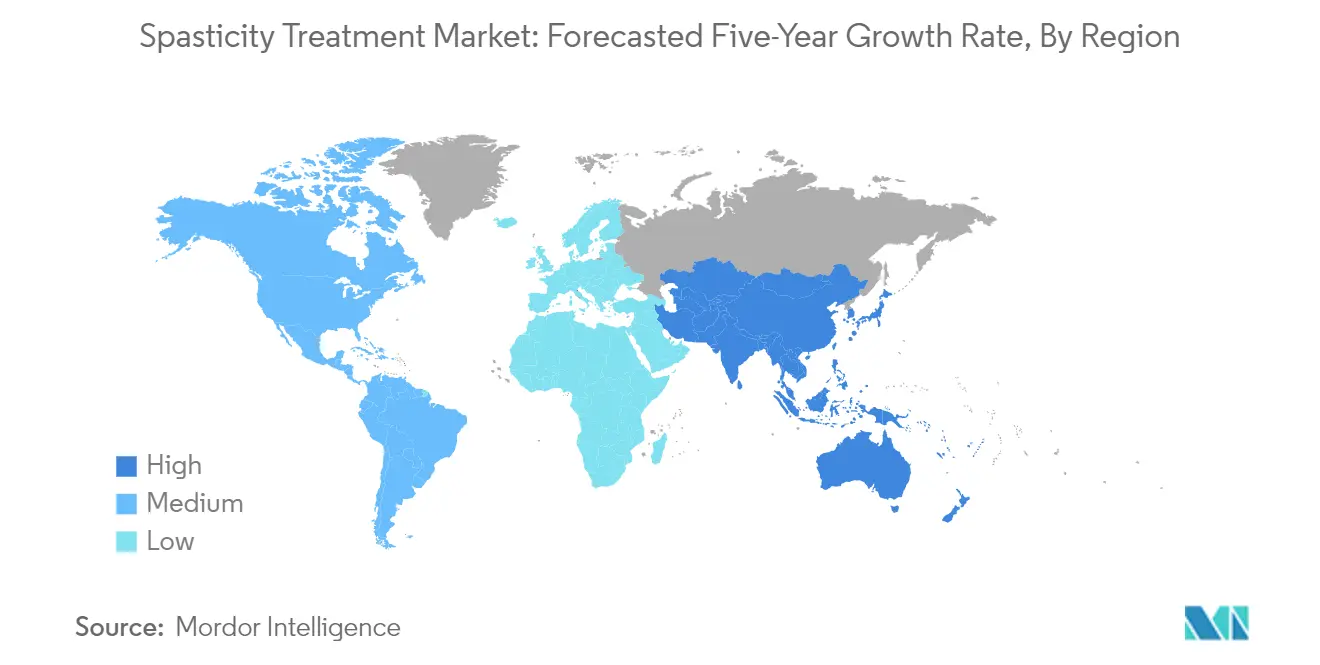

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

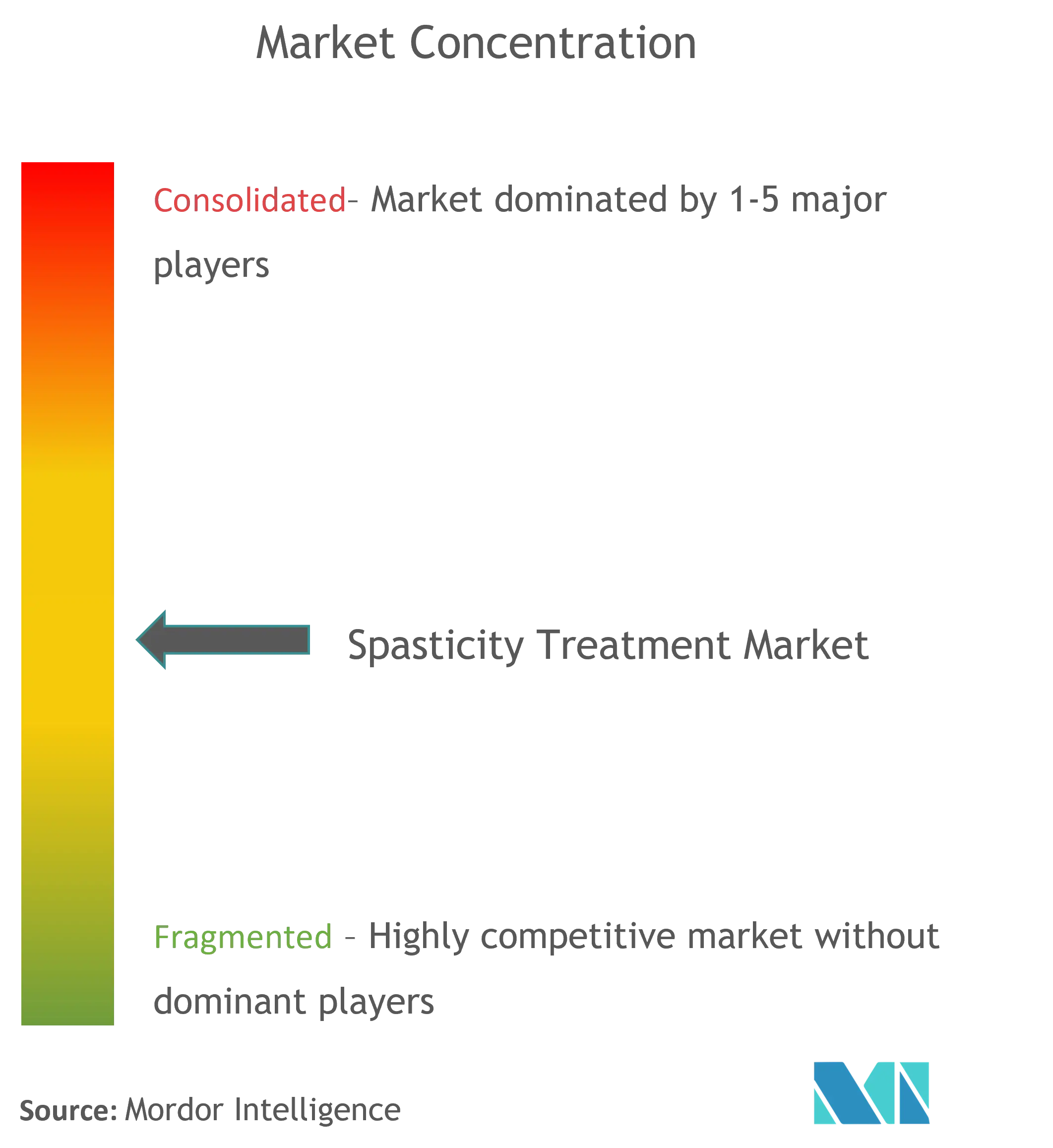

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spasticity Drugs Market Analysis by Mordor Intelligence

The Spasticity Drugs Market size is estimated at USD 1.42 billion in 2025, and is expected to reach USD 2.08 billion by 2030, at a CAGR of 8.02% during the forecast period (2025-2030).

The spasticity drugs market landscape is experiencing significant transformation driven by technological advancements and innovative therapeutic approaches. According to recent data from the Physicians Group LLC in December 2023, approximately 12.0 million people worldwide suffer from spasticity, highlighting the substantial patient base requiring treatment. Contemporary physical therapy approaches, including robotic-assisted therapy, electrical stimulation therapies, and virtual reality therapy, have demonstrated high efficiency in enhancing motor function and reducing spasticity in patients. The integration of these advanced technologies is reshaping traditional treatment paradigms and improving patient outcomes across various healthcare settings.

The industry is witnessing a surge in research activities and clinical trials focused on developing novel treatment modalities. In January 2024, Neurotech International received approval from the Human Research Ethics Committee (HREC) and Therapeutic Goods Administration (TGA) to begin a Phase I/II clinical trial of NTI164 for treating cerebral palsy spasticity. This development reflects the industry's commitment to innovation and evidence-based medicine. Recent studies have shown that over 77% of children with cerebral palsy have the spastic form, emphasizing the critical need for continued research and development in this therapeutic area.

Healthcare infrastructure development and increasing accessibility to specialized treatment centers are playing crucial roles in market evolution. For instance, in July 2023, the El Alcerán Foundation University Hospital in Spain achieved ESCALEM certification, becoming the first Spanish health center to receive this recognition for multiple sclerosis care. The expansion of specialized treatment facilities is complemented by the growing adoption of multidisciplinary treatment approaches, incorporating various therapeutic modalities to address patient-specific needs effectively.

The market is increasingly gravitating towards personalized medicine approaches, with healthcare providers tailoring treatment plans based on individual patient characteristics and response patterns. According to the Multiple Sclerosis Society's data from 2022, over 130,000 people in the United Kingdom have MS, with approximately 90% experiencing spasticity symptoms at some point during their disease course. This high prevalence has led to the development of more targeted therapeutic strategies, including customized dosing regimens and combination therapies designed to address specific patient subgroups and their unique clinical presentations. The use of spasticity medications, neurological drugs, and neuromuscular drugs is becoming more prevalent as part of these personalized approaches, ensuring that treatments are aligned with patient-specific needs.

Global Spasticity Drugs Market Trends and Insights

Rise in Awareness Programs and Adoption of Novel Technologies

The increasing prevalence of spasticity worldwide has led to a significant rise in awareness programs and the adoption of innovative technologies for treatment. According to recent data published by the Physicians Group LLC in December 2023, approximately 12.0 million people globally suffer from spasticity, highlighting the critical need for enhanced awareness and treatment options. Contemporary physical therapy approaches, including robotic-assisted therapy, electrical stimulation therapies, and virtual reality therapy, have demonstrated high efficiency in enhancing motor function and reducing spasticity in patients. The implementation of these novel technologies has been particularly impactful, with studies showing that robotic-assisted sensorimotor therapy exercises applied to stroke subjects with severe spasticity have achieved significant improvements in patient outcomes.

The growing emphasis on awareness is exemplified by initiatives such as the Ninth Annual Infantile Spasms Awareness Week held in December 2023, supported by the Infantile Spasms Awareness Network (ISAN), a coalition of 37 international organizations. These awareness campaigns focus on educating providers, caregivers, and the public about infantile spasms by offering educational materials, announcing new research findings, and informing patients about available support initiatives. Additionally, ultrasound-guided in situ injection techniques with precise and personalized dosages for each muscle group have gained popularity, demonstrating the healthcare community's commitment to adopting more accurate and effective treatment methodologies.

Launch of Advanced Therapeutics and Increased Affordability

The introduction of advanced therapeutic options and increased affordability of treatments has significantly transformed the spasticity treatment landscape. In June 2022, a notable advancement occurred with the commercial launch of baclofen LYVISPAH, a baclofen oral granules specialty product approved by the United States FDA for treating spasticity related to multiple sclerosis and other spinal cord disorders. This innovative formulation, developed as rapidly dissolving flavored granules, provides an alternative solution for patients with spasticity who experience difficulty swallowing pills, demonstrating the industry's commitment to addressing specific patient needs while maintaining therapeutic efficacy.

The development pipeline for spasticity drugs continues to show promising advancement, as evidenced by recent clinical trials and research initiatives. For instance, in January 2024, Neurotech International received approval to begin a Phase I/II clinical trial of NTI164 for the treatment of cerebral palsy, specifically targeting pediatric patients with spastic CP. This development is particularly significant as it represents the industry's focus on creating more specialized and effective treatment options. Furthermore, positive results from clinical trials, such as the Phase II success of SL-1002 for lower limb muscle spasticity with a 100% phase transition success rate, indicate a robust pipeline of advanced therapeutics that will potentially offer more affordable and accessible treatment options for patients.

The role of muscle relaxant drugs, including tizanidine, is increasingly recognized in managing spasticity, providing patients with additional therapeutic avenues. As the market continues to evolve, the integration of neuromuscular drugs into treatment regimens further underscores the industry's dedication to advancing patient care.

Segment Analysis

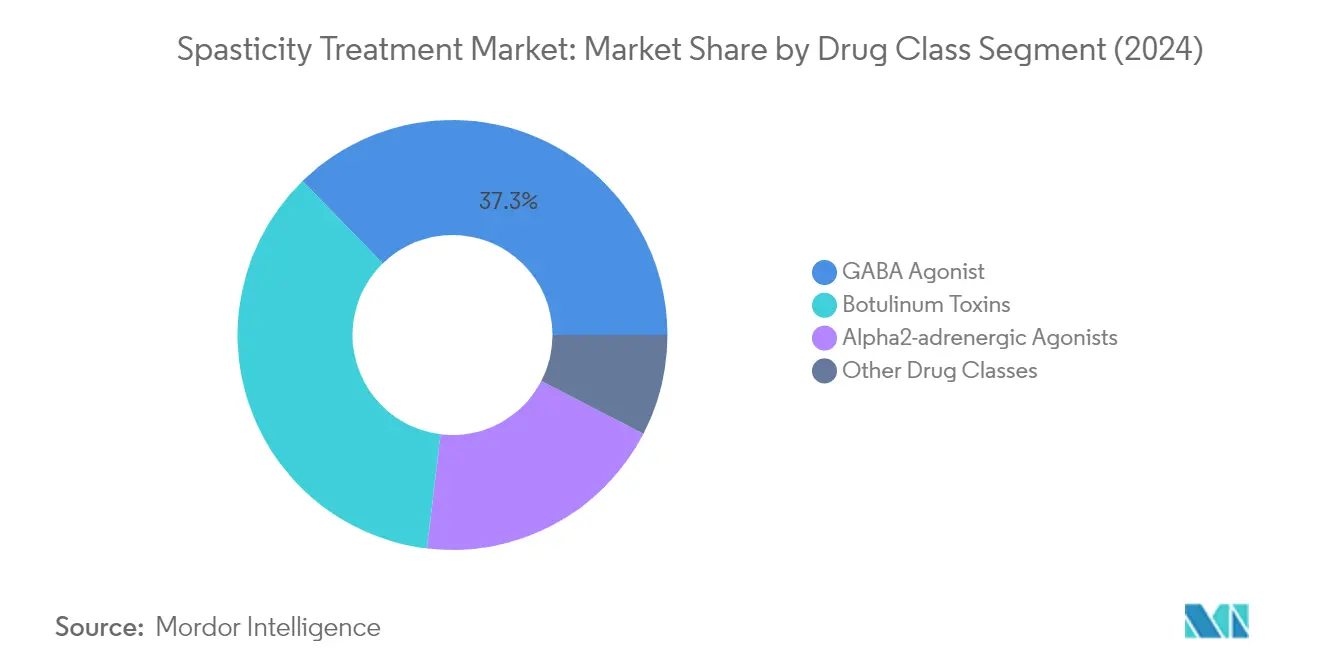

GABA Agonist Segment in Spasticity Drugs Market

The GABA agonist segment has established itself as the dominant force in the spasticity drugs market, commanding approximately 37% market share in 2024. This substantial market position is primarily driven by the increasing adoption of GABA receptor agonists for treating spasticity and their exceptional therapeutic outcomes. The segment's growth is further supported by extensive research demonstrating the effectiveness of GABA agonists in treating neurological complications associated with spasticity. For instance, according to research published in March 2023 in the Spine Journal, Baclofen, a GABA agonist, has proven to be the most effective drug for spasticity treatment, significantly improving patients' overall quality of life and promoting functional recovery after spinal cord injury. The segment's leadership is also reinforced by the FDA's approval of GABA agonists, particularly Baclofen, for managing reversible spasticity, especially for relieving flexor spasms, clonus, and common sequelae of spinal cord lesions and multiple sclerosis.

Remaining Segments in Drug Class Segmentation

The spasticity drugs market encompasses several other significant drug classes beyond GABA agonists. Botulinum toxins represent a substantial segment, offering targeted treatment for spasticity through localized injections that effectively block acetylcholine release at the neuromuscular junction. The Alpha2-adrenergic agonists segment has also carved out an important niche in the market, with drugs like Tizanidine showing significant efficacy in reducing muscle tone and spasticity. These segments are complemented by other drug classes that provide alternative treatment options for patients who may not respond optimally to primary treatments, ensuring a comprehensive approach to spasticity management across different patient populations and condition severities.

Segment Analysis: By Indication

Cerebral Palsy Segment in Spasticity Drugs Market

The Cerebral Palsy (CP) segment dominates the global spasticity drugs market, commanding approximately 37% market share in 2024. This significant market position is primarily driven by the high prevalence of CP cases worldwide, with around 10,000 babies being born with cerebral palsy annually in the United States alone. The segment's dominance is further strengthened by the increasing adoption of various treatment options, including botulinum toxin injections, oral medications, and intrathecal Baclofen therapy. The development of specialized treatment facilities and expansion of existing healthcare infrastructure specifically designed for CP patients has also contributed to the segment's market leadership. Additionally, rising awareness programs and government initiatives focused on early diagnosis and treatment of CP-related spasticity have played a crucial role in maintaining the segment's market position.

Multiple Sclerosis Segment in Spasticity Drugs Market

The Multiple Sclerosis (MS) segment is projected to exhibit the fastest growth rate of approximately 8.4% during the forecast period 2024-2029. This accelerated growth is attributed to the rising global prevalence of MS, with over 2.8 million people estimated to be living with the condition worldwide. The segment's growth is further fueled by increasing research and development activities focused on developing innovative treatment options for MS-related spasticity. The introduction of advanced therapeutic interventions, including novel drug delivery systems and personalized treatment approaches, is expected to drive segment expansion. Additionally, the growing focus on improving patient outcomes through comprehensive care approaches and the increasing availability of specialized MS treatment centers are contributing to the segment's rapid growth trajectory.

Remaining Segments in Spasticity Drugs Market by Indication

The Traumatic Brain Injury (TBI) and Other segments complete the spasticity drugs market landscape. The TBI segment plays a crucial role in the market due to the increasing incidence of accidents and injuries leading to brain trauma, particularly in developing regions. The segment benefits from advancing treatment protocols and growing awareness about early intervention in TBI-related spasticity. The Others segment, which includes conditions such as stroke, hypoxic brain injury, and spinal cord injury, contributes to market diversity by addressing various neurological complications leading to spasticity. These segments are supported by ongoing technological advancements in treatment delivery systems and the development of specialized care protocols for different patient populations.

Segment Analysis: By Route of Administration

Oral Segment in Spasticity Drugs Market

The oral segment maintains its dominance in the spasticity drugs market, commanding approximately 52% of the total market share in 2024. This significant market position is attributed to the convenience and widespread availability of oral medications for treating spasticity. Oral agents like Baclofen, clonidine, and Tizanidine, as well as anticonvulsants such as benzodiazepines and gabapentin, are extensively utilized due to their cost-effectiveness and ease of administration. The segment's leadership is further strengthened by recent developments, including the introduction of novel oral formulations and extended-release medications that offer improved patient compliance and therapeutic outcomes. Healthcare providers often prefer oral medications as the first-line treatment option for managing spasticity, particularly for patients with generalized spasticity requiring systemic treatment approaches.

Parenteral Segment in Spasticity Drugs Market

The parenteral segment is emerging as the fastest-growing segment in the spasticity drugs market, projected to grow at approximately 8% CAGR from 2024 to 2029. This robust growth is driven by the increasing adoption of botulinum toxin injections and intrathecal Baclofen therapy for managing severe spasticity cases. The segment's growth is supported by clinical evidence demonstrating superior therapeutic outcomes of parenteral administration, particularly in cases where oral medications prove insufficient. Technological advancements in drug delivery systems, including improved pump devices for intrathecal administration and precise injection techniques, are further accelerating segment growth. The rising preference for targeted therapy approaches, which minimize systemic side effects while maximizing therapeutic benefits, continues to drive the adoption of parenteral treatments among healthcare providers and patients.

Segment Analysis: By End User

Adults Segment in Spasticity Drugs Market

The adults segment dominates the global spasticity drugs market, holding approximately 74% market share in 2024. This significant market position is primarily attributed to the increasing aging population across the globe and the rising adoption of spasticity treatment among adult patients. The segment's growth is further supported by the high prevalence of conditions like multiple sclerosis, traumatic brain injury, and stroke among adults, which frequently lead to spasticity symptoms. Additionally, the availability of various treatment options specifically designed for adults, including both oral and injectable medications, contributes to the segment's dominance. The segment also benefits from better healthcare infrastructure and insurance coverage for adult patients in developed regions, making treatments more accessible to this demographic.

Pediatrics Segment in Spasticity Drugs Market

The pediatrics segment is projected to experience the fastest growth in the spasticity drugs market from 2024 to 2029. This accelerated growth is primarily driven by the increasing cases of cerebral palsy among children, which is the most common cause of spasticity in pediatric patients. The segment's expansion is further supported by rising awareness about early intervention and treatment options for pediatric spasticity, coupled with technological advancements in pediatric care. Healthcare providers are increasingly focusing on developing specialized treatment protocols for children, considering their unique physiological needs and response to various therapies. The segment is also benefiting from improved diagnostic capabilities, allowing earlier detection and treatment of spasticity in children, along with increasing healthcare expenditure on pediatric care globally.

Geography Analysis

Spasticity Drugs Market in North America

North America represents a dominant force in the global spasticity drugs market, driven by advanced healthcare infrastructure and increasing research initiatives. The region benefits from well-established reimbursement policies and a strong presence of key market players. The United States leads the regional market, followed by Canada and Mexico, with each country contributing uniquely to the market's growth through different healthcare approaches and treatment accessibility programs. The region's market is characterized by high adoption rates of innovative therapies and increasing awareness about spasticity medication options.

Spasticity Drugs Market in United States

The United States holds a commanding position in the North American spasticity drugs market, accounting for approximately 41% of the regional market share in 2024. The country's market leadership is attributed to increasing funding for multiple sclerosis (MS) related research coupled with the development of advanced drug delivery solutions. The presence of sophisticated healthcare infrastructure and favorable reimbursement policies further strengthens the market position. The country has witnessed significant developments in treatment options, particularly in areas such as botulinum toxin therapy and intrathecal baclofen delivery systems. The FDA's proactive approach in approving new treatments and the presence of major pharmaceutical companies contribute to market growth.

Growth Dynamics in United States Spasticity Drugs Market

The United States is projected to maintain its growth momentum with an expected CAGR of approximately 8% from 2024 to 2029. This growth is driven by continuous innovation in treatment modalities and increasing investment in research and development. The country's healthcare system's focus on personalized medicine and patient-centric approaches is expected to drive market expansion. The rising prevalence of neurological conditions and the growing elderly population further contribute to market growth. Additionally, the increasing adoption of advanced therapeutic options and the development of novel drug delivery systems are expected to sustain this growth trajectory.

Spasticity Drugs Market in Europe

The European spasticity drugs market demonstrates a robust framework supported by advanced healthcare systems and strong research initiatives. The region's market is characterized by a well-structured healthcare delivery system spanning Germany, the United Kingdom, France, Italy, and Spain. Each country contributes significantly to the market through different approaches to treatment accessibility and reimbursement policies. The region benefits from strong collaboration between healthcare providers, research institutions, and pharmaceutical companies, fostering innovation in spasticity medication.

Spasticity Drugs Market in Germany

Germany emerges as the largest market for spasticity treatment in Europe, commanding approximately 23% of the regional market share in 2024. The country's market leadership is supported by its robust healthcare infrastructure and comprehensive insurance coverage system. German healthcare providers have shown significant adoption of advanced spasticity treatment options, particularly in areas of botulinum toxin therapy and innovative drug delivery systems. The country's strong emphasis on research and development, coupled with its well-established regulatory framework for spasticity management, continues to drive market growth.

Growth Dynamics in French Spasticity Drugs Market

France demonstrates the highest growth potential in the European region, with an anticipated CAGR of approximately 9% from 2024 to 2029. The country's impressive growth trajectory is supported by its commitment to healthcare innovation and increasing research activities in spasticity treatment. France's healthcare system's focus on patient accessibility and treatment effectiveness contributes significantly to market expansion. The country has shown particular strength in developing and implementing new treatment protocols and maintaining high standards of patient care in spasticity management.

Spasticity Drugs Market in Asia-Pacific

The Asia-Pacific region presents a dynamic market landscape for spasticity treatment, characterized by rapid healthcare infrastructure development and increasing awareness about neurological conditions. The region encompasses diverse markets including China, Japan, India, Australia, and South Korea, each with unique healthcare systems and treatment approaches. The market is driven by improving healthcare access, rising healthcare expenditure, and growing adoption of advanced treatment modalities. The region's large patient pool and increasing healthcare investments create significant opportunities for market expansion.

Spasticity Drugs Market in China

China emerges as the dominant force in the Asia-Pacific spasticity drugs market, demonstrating strong market presence through its extensive healthcare network and large patient population. The country's market leadership is supported by government initiatives to improve healthcare accessibility and significant investments in healthcare infrastructure. China's focus on developing domestic production capabilities for spasticity treatment products and expanding healthcare coverage has strengthened its market position. The country's large population base and increasing healthcare awareness contribute to its market dominance.

Growth Dynamics in Japanese Spasticity Drugs Market

Japan shows the most promising growth trajectory in the Asia-Pacific region, driven by its advanced healthcare system and aging population. The country's healthcare infrastructure excellence and strong focus on innovative treatment approaches support market expansion. Japan's commitment to research and development in neurological treatments, combined with its aging demographic profile, creates favorable conditions for market growth. The country's healthcare policies and emphasis on quality care delivery continue to drive market development.

Spasticity Drugs Market in Middle East & Africa

The Middle East & Africa region presents a developing market for spasticity treatment, characterized by varying healthcare infrastructure levels across different countries. The region encompasses diverse markets including GCC countries and South Africa, with the GCC region emerging as the largest market and demonstrating the fastest growth potential. The market is driven by improving healthcare infrastructure, increasing healthcare spending, and growing awareness about neurological conditions. Government initiatives to enhance healthcare accessibility and the presence of international healthcare providers contribute to market development.

Spasticity Drugs Market in South America

The South American spasticity drugs market shows promising development, with Brazil and Argentina leading the regional landscape. Brazil emerges as both the largest and fastest-growing market in the region, driven by its extensive healthcare network and increasing investment in healthcare infrastructure. The region's market is characterized by improving healthcare access, rising awareness about neurological conditions, and growing adoption of advanced treatment options. Government initiatives to enhance healthcare accessibility and increasing private sector participation contribute to market expansion.

Competitive Landscape

Top Companies in Spasticity Drugs Market

The spasticity drugs market features established pharmaceutical companies and medical device manufacturers who are actively driving innovation through new drug formulations and delivery mechanisms. Companies are increasingly focusing on developing targeted therapies with improved efficacy and reduced side effects, particularly in areas like botulinum toxin treatments and intrathecal baclofen therapy. Strategic partnerships and licensing agreements have become commonplace as firms seek to expand their product portfolios and geographical reach. Market leaders are investing heavily in research and development to create novel treatment options while simultaneously working to improve existing therapies through enhanced delivery systems and patient-centric approaches. The industry has seen a notable trend toward developing comprehensive treatment solutions that combine pharmaceutical interventions with rehabilitation technologies, reflecting a more holistic approach to spasticity management.

Consolidated Market with Strong Regional Players

The spasticity drugs market exhibits a relatively consolidated structure dominated by multinational pharmaceutical corporations with extensive research capabilities and global distribution networks. These major players have established strong market positions through their diverse product portfolios, particularly in areas such as botulinum toxin and muscle relaxant drugs. Regional players maintain a significant presence in their respective markets through specialized product offerings and strong relationships with healthcare providers. The market has witnessed strategic consolidation through mergers and acquisitions, particularly as larger companies seek to acquire innovative technologies and expand their therapeutic offerings in the neurology space.

The competitive dynamics are characterized by a mix of large pharmaceutical conglomerates and specialized neurology-focused companies, each bringing unique strengths to the market. While global players leverage their extensive research capabilities and financial resources to drive innovation, specialized firms often excel in developing targeted solutions for specific patient populations. The market has seen increased collaboration between pharmaceutical companies and medical device manufacturers, particularly in developing integrated treatment solutions that combine drug delivery with rehabilitation technologies. This collaborative approach has become increasingly important as companies seek to provide comprehensive spasticity management solutions.

Innovation and Patient Access Drive Success

Success in the spasticity drugs market increasingly depends on companies' ability to develop innovative treatment options while ensuring broad patient access. Market leaders are focusing on expanding their product portfolios through internal research and development as well as strategic acquisitions, while simultaneously working to improve treatment outcomes and patient compliance. Companies are investing in real-world evidence generation to demonstrate the long-term effectiveness of their treatments, which is becoming increasingly important for market access and reimbursement. The development of patient support programs and rehabilitation protocols has emerged as a key differentiator, as companies seek to provide comprehensive care solutions beyond just pharmaceutical interventions.

For new entrants and smaller players, success lies in identifying and addressing unmet needs in specific patient populations or treatment modalities. Companies are increasingly focusing on developing specialized delivery systems or targeted therapies for specific types of spasticity, creating opportunities for differentiation in a competitive market. Regulatory compliance and safety monitoring remain critical success factors, particularly given the increasing scrutiny of long-term safety profiles for spasticity treatments. The ability to navigate complex reimbursement landscapes and demonstrate clear value propositions to healthcare providers and payers has become essential for maintaining market position and driving growth in this therapeutic area. Additionally, the development of neuromuscular drugs and neurological drugs is gaining traction as companies aim to enhance their therapeutic offerings.

Spasticity Drugs Industry Leaders

Medtronic Plc

Piramal Enterprises Ltd

Allergan plc

Ipsen

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Ipsen revealed the positive result from the AboLiSh study about Dysport (abobotulinumtoxinA) for spasticity treatment at the 7th international conference, TOXINS, in Berlin, Germany.

- June 2022: Amneal Pharmaceuticals Inc. launched LYVISPAH, a baclofen oral granule (5, 10, and 20 mg) specialty product approved by the US Food and Drug Administration for the treatment of spasticity related to multiple sclerosis and other spinal cord disorders.

Global Spasticity Drugs Market Report Scope

Spasticity is a physiological condition in which the contraction of muscles occurs continuously, leading to tightening of muscles and prolonged stiffness. The spasticity may occur due to various disorders such as multiple sclerosis, meningitis, and other conditions such as injury to the spinal cord and others. The spasticity drugs market is segmented by drug class, indication, route of administration, end user, and geography. By drug class, the market segment includes GABA agonists, alpha2-adrenergic agonists, botulinum toxins, and other drug classes. By indication, the market segment includes multiple sclerosis, cerebral palsy, traumatic brain injury, and other indications. By route of administration, the market segment includes oral and parental. By end user, the market segment includes pediatrics and adults. By geography, the market segment includes North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market size and forecasts for all the above segments in value (USD).

| GABA Agonist |

| Alpha2-adrenergic Agonists |

| Botulinum Toxins |

| Other Drug Class |

| Multiple Sclerosis (MS) |

| Cerebral Palsy (CP) |

| Traumatic Brain Injury (TBI) |

| Other Indications |

| Oral |

| Parenteral |

| Pediatrics |

| Adults |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| Drug Class | GABA Agonist | |

| Alpha2-adrenergic Agonists | ||

| Botulinum Toxins | ||

| Other Drug Class | ||

| Indication | Multiple Sclerosis (MS) | |

| Cerebral Palsy (CP) | ||

| Traumatic Brain Injury (TBI) | ||

| Other Indications | ||

| Route of Administration | Oral | |

| Parenteral | ||

| End User | Pediatrics | |

| Adults | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Spasticity Treatment Market?

The Spasticity Treatment Market size is expected to reach USD 1.42 billion in 2025 and grow at a CAGR of 8.02% to reach USD 2.08 billion by 2030.

What is the current spasticity drugs market size?

In 2025, the spasticity drugs market size is expected to reach USD 1.42 billion.

Who are the key players in spasticity drugs market?

Medtronic Plc, Piramal Enterprises Ltd, Allergan plc, Ipsen and F. Hoffmann-La Roche Ltd are the major companies operating in the Spasticity Treatment Market.

Which is the fastest growing region in spasticity drugs market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in spasticity drugs market?

In 2025, the North America accounts for the largest market share in spasticity drugs market.

What years does this spasticity drugs market cover, and what was the market size in 2024?

In 2024, the spasticity drugs market size was estimated at USD 1.31 billion. The report covers the spasticity drugs market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the spasticity drugs market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: