Ankylosing Spondylitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

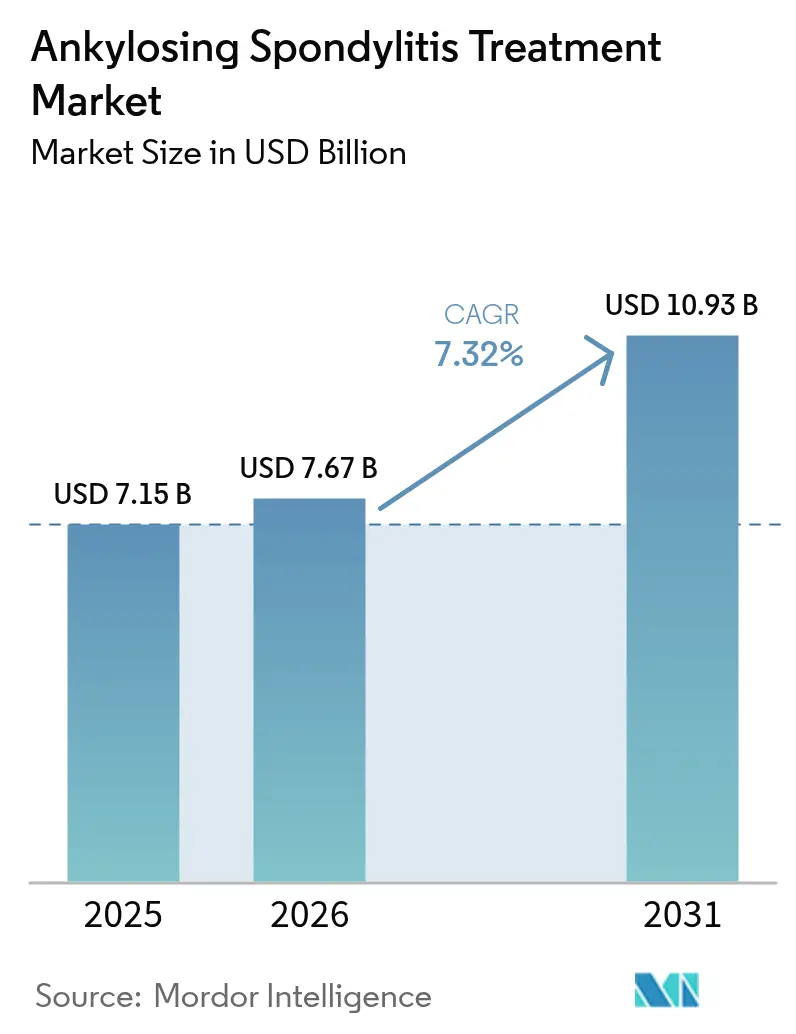

| Market Size (2026) | USD 7.67 Billion |

| Market Size (2031) | USD 10.93 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ankylosing Spondylitis Treatment Market Analysis by Mordor Intelligence

The ankylosing spondylitis treatment Market size was valued at USD 7.15 billion in 2025 and estimated to grow from USD 7.67 billion in 2026 to reach USD 10.93 billion by 2031, at a CAGR of 7.32% during the forecast period (2026-2031). Wider recognition of axial spondyloarthritis as a distinct disease, faster MRI-based diagnosis aided by artificial intelligence, expanding reimbursement for advanced biologics and biosimilars, and a steady stream of dual-target cytokine inhibitors are collectively sustaining growth momentum. Broader payer coverage is narrowing the affordability gap for originator biologics, while algorithm-driven treat-to-target strategies are boosting therapy-switch rates, thereby enlarging the addressable ankylosing spondylitis treatment market. The rapid entry of oral JAK inhibitors brings a non-injectable option into mainstream practice, and heightened competition among biosimilars is accelerating price resets in mature regions. Meanwhile, Asia Pacific’s hospital build-out and growing specialist density are reshaping global demand patterns.

Key Report Takeaways

- By drug class, TNF inhibitors held 53.68% of ankylosing spondylitis treatment market share in 2025, while NSAIDs are projected to expand at an 8.79% CAGR through 2031.

- By route of administration, subcutaneous delivery led with 58.92% revenue share in 2025; oral formulations are forecast to grow at a 8.99% CAGR to 2031.

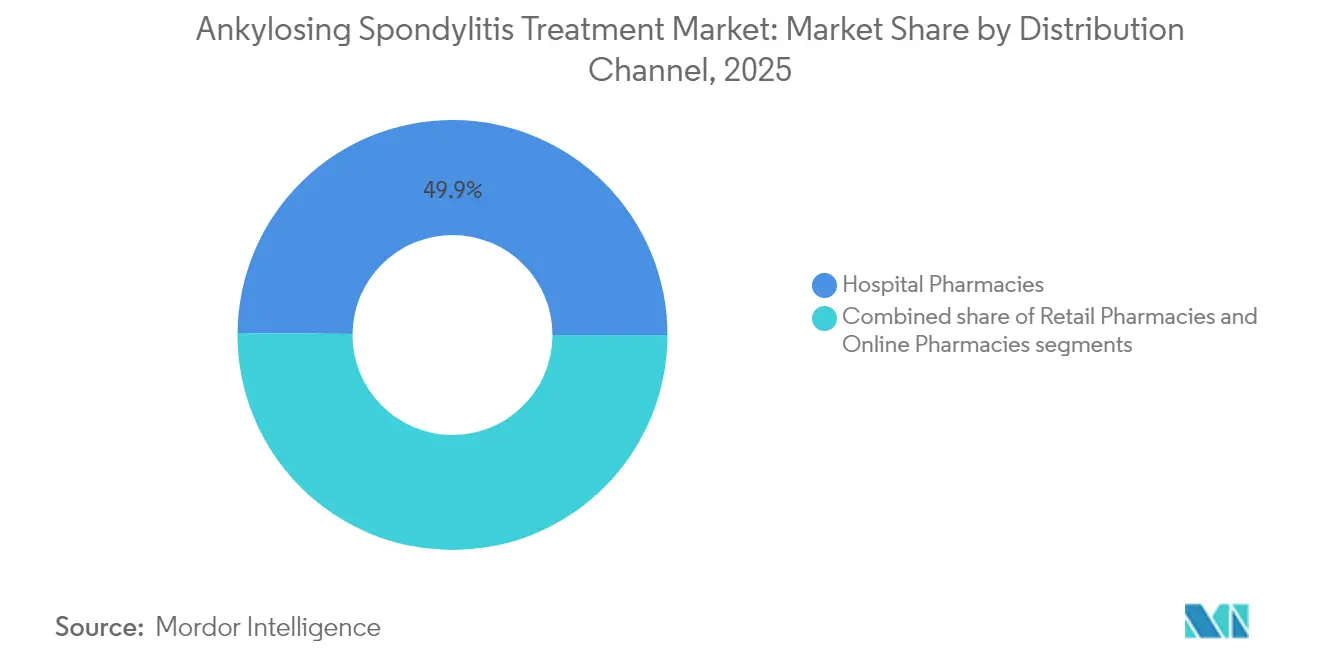

- By distribution channel, hospital pharmacies accounted for 49.85% of the ankylosing spondylitis treatment market size in 2025, whereas online pharmacies are rising at an 8.52% CAGR through 2031.

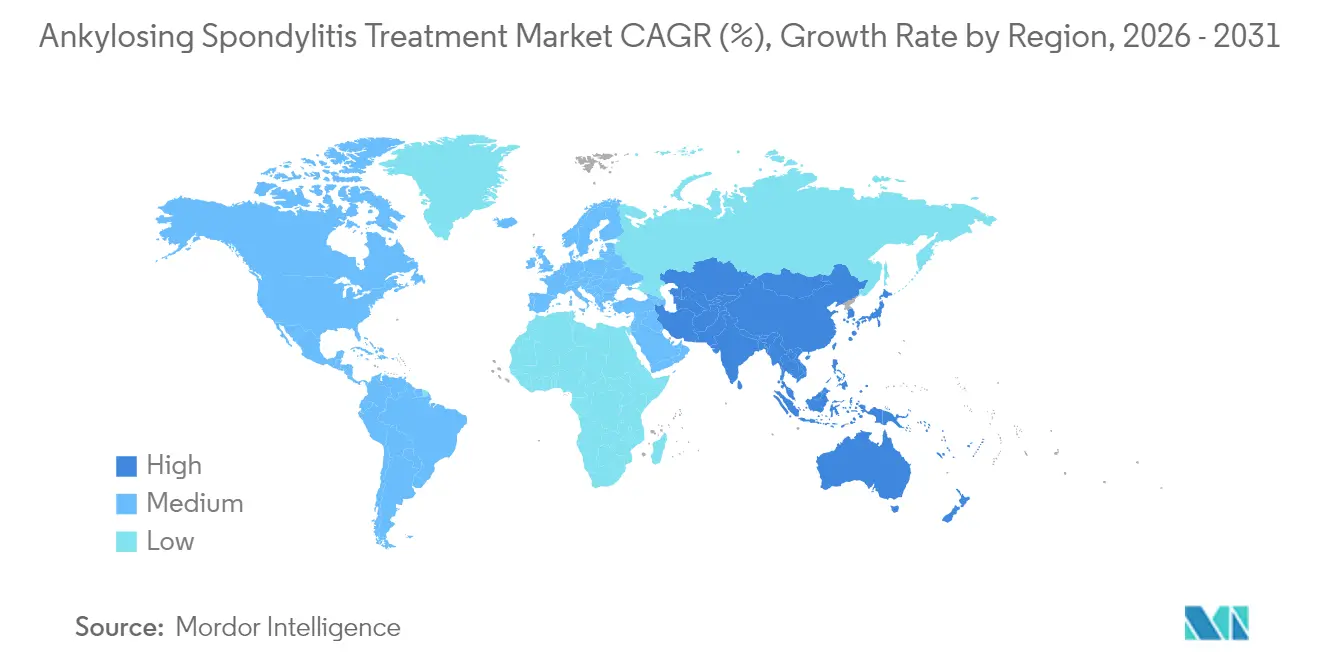

- By geography, North America commanded 40.78% revenue in 2025, but Asia Pacific is set to record the fastest 9.03% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ankylosing Spondylitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global prevalence & earlier diagnosis | +1.2% | Global, with highest impact in Asia Pacific and emerging markets | Medium term (2-4 years) |

| Expanding reimbursement coverage for biologics & biosimilars | +1.8% | North America & Europe, expanding to Latin America | Short term (≤ 2 years) |

| Oral JAK-inhibitors improving patient adherence | +0.9% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| AI-enabled MRI scoring speeding clinical trial timelines | +0.7% | Global, concentrated in research-intensive regions | Long term (≥ 4 years) |

| Treat-to-target guidelines accelerating therapy switches | +1.1% | North America & Europe, gradual adoption in APAC | Short term (≤ 2 years) |

| Emerging dual-IL-17/23 biologics with superior radiographic control | +1.3% | Global, with premium pricing in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Global Prevalence & Earlier Diagnosis

Consensus criteria for “early axial spondyloarthritis” let clinicians intervene before structural damage becomes irreversible, adding previously uncounted patients to the ankylosing spondylitis treatment market.[1]Source: Victoria Navarro-Compán et al., “ASAS Consensus Definition of Early Axial Spondyloarthritis,” PubMed, pubmed.ncbi.nlm.nih.gov Ethnic-specific HLA-B27 subtypes identified in East Asian cohorts refine risk stratification and enable targeted screening. National registries in China and India are reporting higher case ascertainment as rheumatology capacity increases, magnifying demand for both first-line NSAIDs and advanced biologics. These combined shifts are expected to keep new patient starts on an upward curve through the medium term.

Expanding Reimbursement Coverage for Biologics & Biosimilars

Pharmacy benefit managers in the United States now privilege low-priced adalimumab and ustekinumab biosimilars, with several plans offering USD 0 co-pay switching incentives. Parallel moves in the European Union have lifted biosimilar uptake above 70% in certain markets, compressing net prices and broadening access. Latin American payers are adopting tiered formularies that admit two or more biosimilars per molecule, creating multi-supplier competition. Cost savings redirected toward dual IL-17 inhibitors and JAK inhibitors are enlarging the overall ankylosing spondylitis treatment market rather than merely cannibalizing existing spends. Faster market penetration of biosimilars is therefore amplifying volume growth, even as average selling prices soften.

Oral JAK-Inhibitors Improving Patient Adherence

Once-daily upadacitinib and twice-daily tofacitinib ease injection fatigue, helping sustain adherence in younger, professionally active patients. Five-year safety monitoring shows no excess overall malignancy risk versus biologic DMARDs, though vigilance for non-melanoma skin cancer remains prudent. Mechanistic breadth across multiple cytokines offers a therapeutic alternative for patients unresponsive to TNF- or IL-17-targeted agents. Early real-world evidence indicates a measurable decline in outpatient visits linked to easier oral dosing, further incentivizing payers to add JAK inhibitors to preferred tiers.

AI-Enabled MRI Scoring Speeding Clinical Trial Timelines

Machine-learning-based Berlin scoring attains 67% concordance with expert radiologists, while newer convolutional models reach AUC values of 0.96 in test datasets. Automating image reads cuts both subjectivity and labor costs, enabling smaller protocols with higher statistical power. Sponsors report that AI-enhanced endpoints have reduced imaging-related timelines by roughly six months in recent phase III programs. Regulators in the United States and Europe have begun accepting algorithm-supported readouts as secondary efficacy measures, signaling future mainstream adoption. These gains make drug development more attractive in niche inflammatory indications, indirectly expanding the therapeutic toolkit available to the ankylosing spondylitis treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & price-inflation of originator biologics | -1.4% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Safety warnings for JAK inhibitors & long-term immunosuppression | -0.8% | Global, with regulatory focus in North America & Europe | Medium term (2-4 years) |

| Inter-changeability scepticism slowing biosimilar uptake | -0.6% | North America & Europe, less impact in emerging markets | Short term (≤ 2 years) |

| Cold-chain logistics gaps in emerging markets | -0.9% | Asia Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Originator Biologics

List prices for established TNF inhibitors continue to test payer budgets, prompting stricter prior authorization and step-therapy mandates. Although the U.S. Inflation Reduction Act promises relief for Medicare beneficiaries, commercial plans still negotiate rebates on a product-by-product basis. Insurers increasingly channel patients toward preferred biosimilars, but uptake remains slower in regions lacking automatic pharmacy-level substitution. In emerging economies, limited public financing forces many patients to defer biologic initiation, restricting the potential universe for the ankylosing spondylitis treatment market until broader subsidy schemes materialize.

Safety Warnings for JAK Inhibitors & Long-Term Immunosuppression

Post-marketing surveillance has highlighted cardiovascular and thrombotic events, triggering boxed warnings and targeted risk-evaluation strategies. Nevertheless, pooled real-world data from over 53,000 initiations reveal no significant rise in overall cancer rates versus biologics, except for a marginal uptick in non-melanoma skin cancers.[2]Source: European Alliance of Associations for Rheumatology, “New Data Reveals Insights Into Cancer and Cardiovascular Safety of JAK Inhibitors,” News-Medical, news-medical.net Physicians now tailor JAK inhibitor use to younger, lower-risk profiles and employ periodic dermatologic screening. Regulatory agencies continue to refine labeling, which keeps a perceptual cloud over the class and slows its share-of-wallet expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biosimilar Headwinds Meet NSAID Resurgence

TNF inhibitors retained 53.68% ankylosing spondylitis treatment market share in 2025, supported by two-decade clinical familiarity and extensive payer coverage. However, erosive price competition from eight approved adalimumab biosimilars and the expanding footprint of infliximab-dyyb are moderating revenue growth. IL-17 blockers, led by secukinumab and ixekizumab, are enlarging their patient base in biologic-naïve cohorts who value rapid entheseal pain relief. Meanwhile, dual-target bimekizumab is expected to capture early switchers by demonstrating superior radiographic control. JAK inhibitors are carving a niche among patients with prior biologic failure, offering oral convenience and broader cytokine coverage.

NSAIDs are rebounding, registering an 8.79% CAGR to 2031—the highest among all classes—after long-term cohort data confirmed that continuous celecoxib therapy retards spinal damage progression. This evidence has reinstated selective COX-2 inhibitors as quasi–disease-modifying agents rather than mere analgesics. Combined with individualized exercise regimens, etoricoxib has delivered meaningful functional gains, further broadening its uptake. Novel candidates such as anti-GM-CSF antibodies and nanomedicine formulations remain experimental but highlight the innovation pipeline poised to feed future growth in the ankylosing spondylitis treatment market.

By Route of Administration: Oral Surge Challenges Injectable Dominance

Subcutaneous formulations delivered 58.92% of 2025 revenue, reflecting patient self-administration convenience and the broadest commercial portfolio, including adalimumab, secukinumab, and newly launched bimekizumab. Prefilled starter kits and connected autoinjectors are improving dosing accuracy and adherence tracking. However, oral delivery is projected to be the fastest-growing route at a 8.99% CAGR, catalyzed by JAK inhibitor enthusiasm and payer acceptance of tablet-based chronic therapies. Clinical equivalence to biologics in ASAS40 response, combined with easier supply chain logistics, underpins this ascent.

Intravenous infusions, once the mainstay for infliximab, now serve a more specialized subset—patients experiencing injection-site reactions or needing high-dose induction. Hospitals and stand-alone infusion centers are optimizing chair time and adopting biosimilar infliximab to retain volume. Market momentum nonetheless favors modalities that minimize facility dependence, prompting manufacturers to re-engineer IV-only molecules into high-concentration subcutaneous or oral versions. Route flexibility is thus becoming a competitive differentiator in the ankylosing spondylitis treatment market.

By Distribution Channel: Specialty Digital Models Gain Ground

Hospital pharmacies captured 49.85% of overall revenue in 2025, underpinned by integrated infusion services and in-house rheumatology consults. They remain indispensable for biologic initiation, safety monitoring, and adverse-event management. Retail chains hold stable share by dispensing NSAIDs and oral small molecules but continue to cede high-complexity biologics to specialized arms.

Online and specialty pharmacies are on track for an 8.52% CAGR through 2031. Improved cold-chain orchestration, insurer-aligned copay assistance, and doorstep nurse training are boosting acceptance, particularly among working-age patients seeking discretion and convenience. Digital refill reminders and adherence analytics further differentiate these providers. As reimbursement frameworks evolve toward home-based care, e-pharmacy platforms are poised to unlock incremental value across the ankylosing spondylitis treatment market.

Geography Analysis

North America’s 40.78% contribution in 2025 underscores its role as the innovation nucleus for advanced therapeutics and digital management tools. Early FDA approvals for dual IL-17 agents and rapid biosimilar turnover exemplify a dynamic yet price-sensitive environment. Major payers now embed performance guarantees into contracts, while remote monitoring apps gain traction among high-deductible health plan enrollees. Differences in Medicare Part D formularies create state-level access disparities, influencing switching patterns and overall utilization.

Asia Pacific is forecast to deliver the highest 9.03% CAGR through 2031, anchored by China’s 0.26% disease prevalence and distinctive HLA-B27 landscape that makes 88.8% of diagnosed patients genetically predisposed. Rising middle-class insurance coverage, government-funded biosimilar programs, and an expanding network of rheumatology clinics are accelerating first-line biologic uptake. South Korea and Japan continue to operate mature reimbursement models, whereas India’s tiered hospital accreditation system is gradually unlocking infliximab and adalimumab access beyond metropolitan centers. Across Southeast Asia, tele-consult services are shortening wait times and bolstering guideline adoption.

Europe maintains a steady revenue base, aided by the region’s leadership in biosimilar policy and real-world evidence generation. Germany’s national cohort studies inform global dosing optimization, while the United Kingdom’s value-based pricing scheme incentivizes measurable functional improvements. Nationalized health systems leverage pooled purchasing power to secure attractive tender prices, promoting broad access yet compressing manufacturer margins. Central and Eastern European countries are narrowing the gap through EU structural funds dedicated to rheumatology infrastructure, paving the way for more uniform penetration of the ankylosing spondylitis treatment market.

Competitive Landscape

The market sits at a moderate consolidation level. AbbVie’s shift from Humira to the Rinvoq-Skyrizi duo signals a calibrated hedge against biosimilar erosion, while Novartis leverages patient-support programs to cement secukinumab loyalty. UCB’s bimekizumab roll-out across radiographic and non-radiographic indications introduces dual-target innovation and pushes rivals to broaden pipeline strategies.

Biosimilar specialists such as Samsung Bioepis and Celltrion are scaling capacity to undercut originator brands, aided by full interchangeability designations that simplify pharmacy substitution. Their aggressive rebate deals with U.S. payers demonstrate the growing financial leverage of follow-on biologics. Simultaneously, pipeline entrants like Bio-Thera’s BAT1406 and Biocad’s BCD-180 illustrate China- and Russia-based developers’ ambitions to cross-license into Western markets upon clinical validation, intensifying price competition in the ankylosing spondylitis treatment market.

Technology partnerships are becoming pivotal. Imaging-AI vendors collaborate with pharmaceutical sponsors to integrate automated MRI scoring into pivotal trials, shaving development costs and timelines. Digital therapeutics companies offer adherence dashboards that link patient-reported pain scores with refill behavior, creating new data streams for value-based pay arrangements. Over the forecast horizon, competitive advantage will hinge on the ability to pair differentiated mechanisms with wrap-around services that tangibly improve long-term spinal outcomes.

Ankylosing Spondylitis Treatment Industry Leaders

Novartis AG

AbbVie Inc.

Amgen Inc.

Boehringer Ingelheim International GmbH

UCB S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: UCB secured FDA approval for Bimzelx across ankylosing spondylitis and non-radiographic axial spondyloarthritis, expanding its cytokine-inhibition franchise.

- May 2024: Teva and Alvotech launched SIMLANDI in the United States as an interchangeable Humira biosimilar, widening low-cost access across multiple inflammatory indications.

- May 2024: Biocad disclosed plans to introduce its first ankylosing spondylitis biologic in Russia following national registration approval

- December 2023: UCB secured approval from the Japanese Ministry of Health, Labour and Welfare (MHLW) for BIMZELX (bimekizumab). This approval is specifically for treating adults with psoriatic arthritis (PsA), non-radiographic axSpA (nr-axSpA), and ankylosing spondylitis (AS) who haven't adequately responded to current therapies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the ankylosing spondylitis (AS) treatment market as the total annual spending on prescription pharmacotherapies, non-steroidal anti-inflammatory drugs, biologic and targeted synthetic disease-modifying anti-rheumatic drugs, corticosteroids, and emerging JAK or IL-17/23 inhibitors used to manage radiographic and non-radiographic axial spondyloarthritis across all care settings.

Scope Exclusion: medical devices, physical therapy services, and surgical interventions are not counted in market value calculations.

Segmentation Overview

- By Drug Class

- NSAIDs

- TNF Inhibitors

- IL-17 Inhibitors

- JAK Inhibitors

- Biosimilars

- Others

- By Route of Administration

- Oral

- Sub-cutaneous

- Intravenous

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with rheumatologists, payor pharmacists, biosimilar manufacturers, and hospital buyers across North America, Europe, and key Asia-Pacific markets validate uptake curves, discount depth, and switching behavior. Follow-up questionnaires capture patient share splits for oral versus injectable regimens and typical duration on therapy, closing gaps left by secondary data.

Desk Research

Mordor analysts first assemble historical demand indicators from open-access sources such as the WHO Global Health Observatory, national claims datasets (e.g., Medicare Part D), EU EudraVigilance drug safety files, and trade association white papers from groups such as the Spondyloarthritis Research & Treatment Network. Company 10-Ks, investor decks, and FDA/EMA approval databases provide launch dates, patient numbers, and list prices that anchor prevalence and pricing. To enrich therapy mix and regional shipment clues, paid feeds like D&B Hoovers and Dow Jones Factiva are consulted. The sources cited here are illustrative; many additional documents underpin desk analysis.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort model scales region-specific AS prevalence by diagnosis and treatment rates, which are then multiplied with weighted average selling prices to reach the baseline year. Select bottom-up checks, supplier revenue roll-ups and sampled pharmacy claims, test and fine-tune totals. Key variables include diagnosed prevalence, first-line biologic penetration, biosimilar erosion rates, median annual drug cost, and reimbursement coverage ratios. Multivariate regression projects these drivers under three macro-economic scenarios; the consensus case feeds a five-year exponential smoothing forecast. Gaps in bottom-up inputs are bridged through expert-derived substitution factors.

Data Validation & Update Cycle

Outputs pass an anomaly screen that flags variances above ten percent against external gauges such as shipment volumes and public sales. Senior analysts review flagged points before sign-off. The model refreshes yearly, with interim updates triggered by major approvals, reimbursement shifts, or pricing shocks, ensuring clients receive the latest view at download.

Why Mordor's Ankylosing Spondylitis Treatment Baseline Earns Trust

Published estimates often diverge because firms choose different therapy baskets, price concessions, and refresh cadences.

Key gap drivers include: some studies fold physical therapy revenue into drug sales, others apply aggressive biosimilar discounting, and a few report conservative uptake for new oral JAK inhibitors. Mordor standardizes scope to prescription drugs only, applies country-level net pricing, and refreshes annually, decisions that tighten variance and enhance reliability.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.15 B (2025) | Mordor Intelligence | - |

| USD 6.29 B (2024) | Global Consultancy A | Excludes JAK inhibitors and treats biosimilar prices as flat 70 % discount globally |

| USD 5.90 B (2023) | Industry Portal B | Uses list prices without country-specific rebates and aggregates physical therapy spend |

| USD 5.90 B (2024) | Regional Consultancy C | Applies single prevalence rate across regions and updates every three years |

These comparisons show that when scope, price realism, and update frequency are aligned, Mordor's balanced approach yields a dependable baseline that decision-makers can retrace and replicate.

Key Questions Answered in the Report

What technology is shortening the diagnostic journey for axial spondyloarthritis?

AI-enhanced MRI scoring tools now detect sacroiliac inflammation with laboratory-grade sensitivity, enabling clinicians to confirm disease years earlier than traditional image readings.

How are payer strategies influencing drug choice in ankylosing spondylitis?

Large pharmacy benefit managers increasingly give first-line preference to low-priced biosimilars and bundle them with zero-copay incentives, accelerating patient switches from originator biologics.

Why are selective COX-2 inhibitors regaining prominence despite widespread biologic use?

Long-term cohort evidence shows continuous celecoxib or etoricoxib therapy can slow spinal radiographic progression, recasting certain NSAIDs as disease-modifying rather than purely symptomatic options.

What distinguishes dual IL-17A/IL-17F inhibitors such as bimekizumab from earlier biologics?

By simultaneously blocking two closely related cytokines, these agents achieve deeper suppression of entheseal inflammation, translating into faster clinical responses and improved radiographic outcomes.

How is artificial intelligence transforming clinical trials for new ankylosing spondylitis drugs?

Machine-learning algorithms deliver consistent, automated scoring of spinal and sacroiliac MRIs, allowing sponsors to run smaller trials with clearer endpoints and reduced reader variability.

Which distribution trend is most improving convenience for chronic therapy users?

Specialty e-pharmacies that integrate cold-chain logistics, remote nurse training, and digital refill reminders are rapidly displacing hospital pick-ups, boosting adherence for self-injectable and oral treatments.

Page last updated on: