Pruritus Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.39 Billion |

| Market Size (2031) | USD 12.74 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

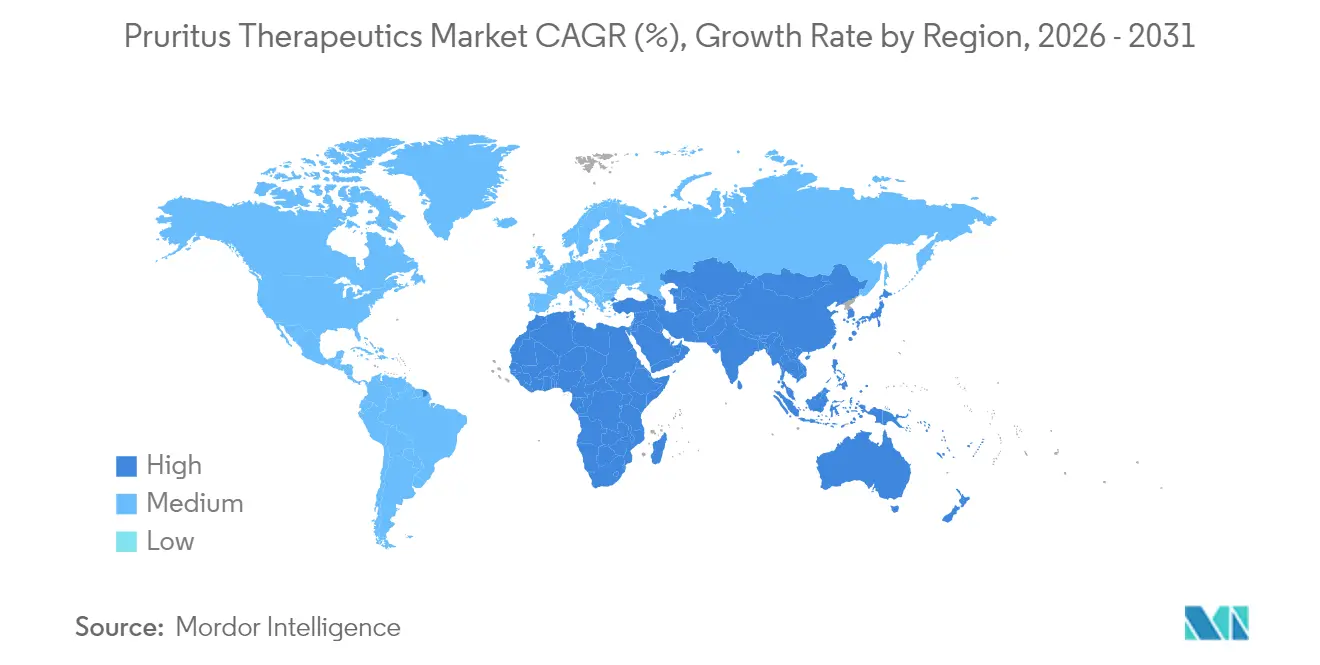

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

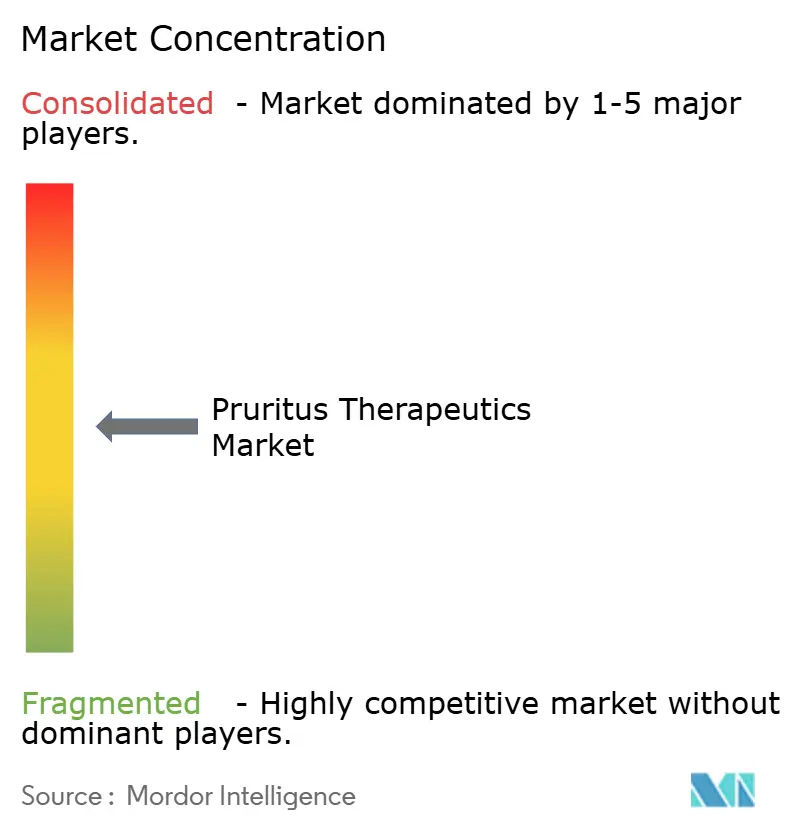

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pruritus Therapeutics Market Analysis by Mordor Intelligence

Pruritus Therapeutics Market size in 2026 is estimated at USD 10.39 billion, growing from 2025 value of USD 9.97 billion with 2031 projections showing USD 12.74 billion, growing at 4.17% CAGR over 2026-2031.

Advancements in mechanism-specific biologics and small-molecule inhibitors are shifting treatment away from broad immunosuppression toward precision medicine, especially after the first-in-class IL-31 receptor antagonist approval in late 2024. Regulatory harmonization and digital health uptake further widen patient reach, while rising disease awareness repositions chronic itch from a symptom to its own therapeutic category. White-space indications such as cholestatic and oncologic pruritus are beginning to attract investment as legacy segments mature. Nevertheless, payer scrutiny and evolving JAK inhibitor safety profiles temper near-term revenue acceleration.

Key Report Takeaways

- By product type, corticosteroids led with 34.98% of pruritus therapeutic market share in 2025, whereas JAK inhibitors are on track for the fastest 5.59% CAGR through 2031.

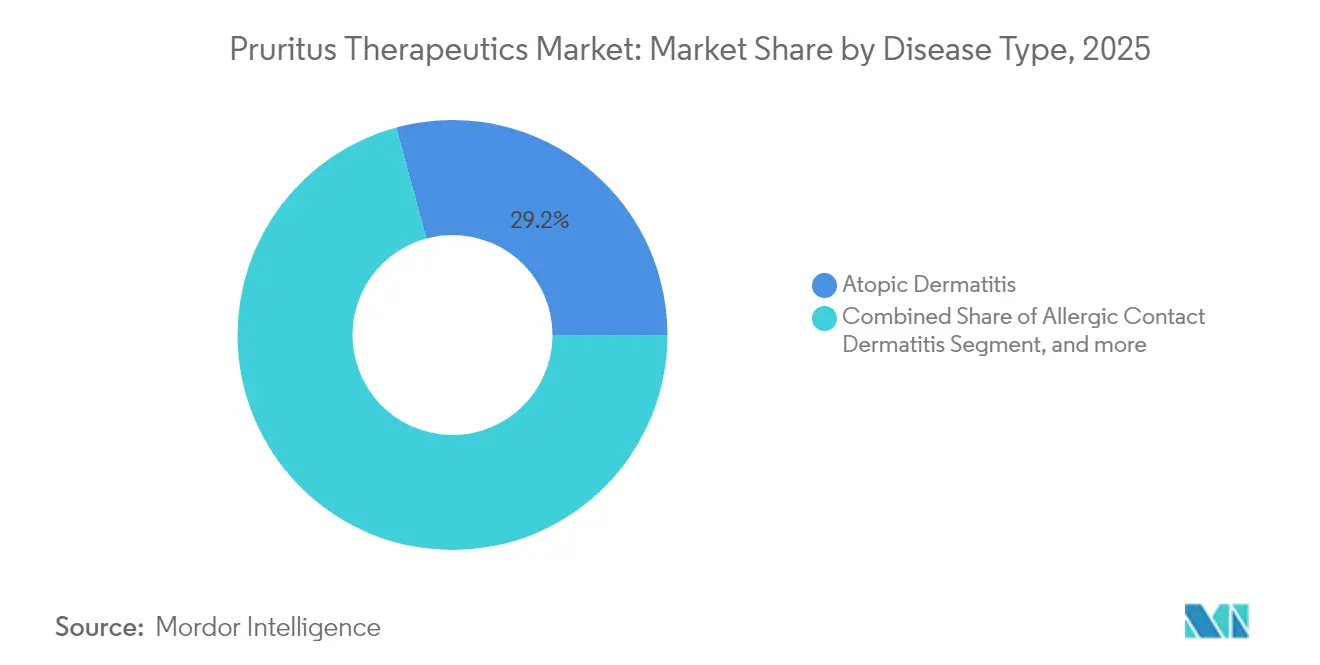

- By disease type, atopic dermatitis held a 29.22% share of the pruritus therapeutic market size in 2025, while neuropathic pruritus is projected to expand at a 6.14% CAGR to 2031.

- By geography, North America dominated with 37.12% revenue share in 2025, while Asia-Pacific is expected to post an 8.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pruritus Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of dermatological disorders | +1.2% | Global, higher in aging populations | Long term (≥ 4 years) |

| Presence of high unmet medical needs | +0.8% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Aging population with chronic inflammatory skin diseases | +0.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Commercial launch of biologics & JAK inhibitors | +1.1% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Rapid uptake of tele-dermatology & e-prescription platforms | +0.5% | Global, accelerated in developed markets | Medium term (2-4 years) |

| Innovative R&D in neurogenic itch mechanisms | +0.7% | Global, led by US & EU research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Dermatological Disorders

Global itch prevalence is outpacing overall population growth; 14.2% of older adults report chronic pruritus compared with 1% among younger cohorts. Climate-linked allergen exposure and urban pollution raise atopic dermatitis incidence, especially in rapidly developing economies.[1]Nature Staff, “Urbanization and atopic dermatitis trends,” nature.com Better diagnostics now classify several orphan pruritic conditions, which expands the treated population. Health systems increasingly assign specific reimbursement codes to chronic itch, lifting access to advanced therapies. As neurologists and oncologists incorporate pruritus management into routine care, the pruritus therapeutic market gains multidisciplinary visibility.

Aging Population with Chronic Inflammatory Skin Diseases

Longer life expectancy raises the pool of patients with recalcitrant eczema, prurigo nodularis, and lichen simplex; regional data show Northern Europe and North America carry the heaviest burden.[2]MDPI Healthcare Authors, “Global burden of chronic pruritus in aging populations,” mdpi.com Physicians prefer targeted biologics over systemic steroids in polypharmacy settings to avoid drug interactions. Universal health-coverage expansion enlarges diagnosis and treatment volumes in Asia-Pacific. Together, these demographic and policy shifts generate a durable demand base for the pruritus therapeutic market.

Commercial Launch of Biologics & JAK Inhibitors

Nemolizumab achieved 85% response rates in long-term studies, validating IL-31 antagonism for severe itch.[3]Galderma, “Nemolizumab two-year data confirm durable efficacy,” galderma.comFDA approvals of lebrikizumab, tapinarof, and roflumilast broaden therapeutic choices across age groups, including pediatrics. In the LEVEL UP trial, upadacitinib delivered 19.9% complete clearance versus 8.9% for dupilumab. Japan’s quick adoption of new labels underpins rapid Asia-Pacific diffusion. Pipeline bispecific antibodies promise further innovation momentum, positioning the pruritus therapeutic market for sustained product refresh cycles.

Rapid Uptake of Tele-Dermatology & E-Prescription Platforms

Tele-dermatology improves diagnostic accuracy and eliminates travel barriers, extending specialist care to under-served regions. Wearable sensors that quantify nocturnal scratching, such as those under the DECODE initiative, enable AI-driven dose adjustments. Automated refill workflows on e-prescription portals shorten time-to-therapy for specialty drugs. These digital advances compress decision loops, supporting quicker adoption of novel agents across the pruritus therapeutic market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited understanding of pruritus pathophysiology | -0.6% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Safety concerns over long-term immunosuppressant usage | -0.8% | Global, particularly in elderly populations | Long term (≥ 4 years) |

| Availability of symptomatic non-prescription alternatives | -0.4% | Global, higher in cost-sensitive markets | Short term (≤ 2 years) |

| Fragmented reimbursement for novel biologics | -0.7% | Mainly developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Understanding of Pruritus Pathophysiology

Neuropathic itch still lacks an FDA-approved therapy; consensus diagnostic criteria only crystallized recently. Complex receptor pathways spanning TRPV1, TRPA1, and IL-31 complicate target validation. Chronic pruritus of unknown origin often affects elderly patients without reliable biomarkers, delaying drug development. Regulators remain cautious about unvalidated digital endpoints, extending clinical-trial timelines and raising costs across the pruritus therapeutic market.

Safety Concerns Over Long-Term Immunosuppressant Usage

FDA and EMA warnings highlight elevated cardiovascular and malignancy risks with prolonged JAK inhibitor use. Limited long-term data for new IL-31 blockers foster caution among prescribers. Intensified infection vigilance in the post-pandemic environment imposes additional monitoring burdens that may deter uptake in smaller clinics. As patient education and laboratory surveillance increase overhead, cost-constrained systems lean toward established symptomatic treatments, moderating growth in the pruritus therapeutic market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: JAK Inhibitors Challenge Corticosteroid Dominance

Corticosteroids retained a 34.98% revenue share in 2025, yet cumulative safety concerns and tachyphylaxis curb repeat prescriptions. JAK inhibitors contributed a modest share in 2025 but are projected to grow fastest at 5.59% CAGR, buoyed by 19.9% complete clearance rates shown by upadacitinib against dupilumab in head-to-head data. The pruritus therapeutic market size for JAK inhibitors could reach USD 2.49 billion by 2031 if label expansions continue. Antihistamines remain first-line for acute flare control, whereas calcineurin inhibitors occupy pediatric niches thanks to favorable safety in thin skin.

Nanofiber transdermal films enhance the delivery of counter-irritants and local anesthetics, raising adherence in mild cases. PDE-4 inhibitors are moving from psoriasis into atopic dermatitis, diversifying topical portfolios. Opioid receptor antagonists now feature in late-stage trials for cholestatic itch, while TRPM8 agonists explore cold-receptor modulation. Combination therapy and precision dosing are emerging norms, further fragmenting the pruritus therapeutic market.

By Disease Type: Neuropathic Pruritus Emerges as Growth Driver

Atopic dermatitis commanded 29.22% of the pruritus therapeutic market share in 2025 on the back of robust biologic pipelines. Neuropathic pruritus, traditionally relegated to gabapentinoids, is forecast to deliver a 6.14% CAGR through 2031 as mechanistic understanding progresses. Urticaria awaits FDA action on dupilumab, potentially redirecting patient flows toward biologics. Cholestatic pruritus awaits the first dedicated therapy following positive Phase III results for linerixibat GSK.

Hematologic and oncologic pruritus segments expand as survivorship climbs, spurring demand for supportive care. Cross-indication use of IL-31 antagonists could blur disease boundaries, accelerating product uptake across the pruritus therapeutic market. Improved patch-test panels aid allergic contact dermatitis management, lifting diagnosis rates. Together, these shifts diversify revenue streams while reducing dependence on atopic dermatitis.

Geography Analysis

North America held 37.12% of 2025 revenue owing to early biologic access; yet, biosimilar competition and tighter PBM formularies are slowing incremental growth. Medicare fee cuts of 46% (inflation-adjusted) on dermatology procedures between 2007 and 2024 are nudging providers toward cost-optimized regimens. Large PBMs have already removed certain high-price biologics to favor low-cost adalimumab biosimilars. Even so, clinical-trial density and swift FDA review times retain the region’s influence on global launch sequencing within the pruritus therapeutic market.

Asia-Pacific is on track for an 8.18% CAGR, benefiting from synchronized adoption of ICH guidelines and middle-class insurance expansion. China approved 228 new drugs in 2024, with accelerated pathways covering 71 molecules. Japan continues to deliver world-first dermatology approvals, including chronic spontaneous urticaria coverage for dupilumab, and facilitates topical roflumilast commercialization through co-development alliances. India’s clearance of abrocitinib underscores regulatory convergence trends, while nationwide telehealth platforms extend specialty care to tier-2 cities.

Europe exhibits steady but moderated growth as biosimilar price competition intensifies. EMA cardiovascular warnings on JAK inhibitors influence physician choice, especially for older adults. Brexit-driven regulatory divergence adds filing complexity, although ICH efforts maintain broad alignment. Long-term opportunities lie in the Middle East, Africa, and South America, where improving infrastructure and NGO-backed access programs broaden the addressable base for the pruritus therapeutic market.

Competitive Landscape

The pruritus therapeutics market is moderately concentrated. AbbVie’s combined Skyrizi and Rinvoq sales exceeded USD 6 billion in 2025, rising 70.5% year-on-year. Strategic M&A is reshaping portfolios—Incyte paid USD 750 million upfront for Escient’s MRGPR antagonist platform, while Johnson & Johnson acquired NM26 bispecific technology for USD 1.25 billion. Digital therapeutics tie-ups are becoming differentiators; Galderma partners with device companies to integrate scratch-monitoring into treatment algorithms.

Patent expiries are accelerating biosimilar waves: 14 adalimumab copies already compete in the United States, and ustekinumab generics debut in 2025. Portfolio diversification now extends into microbiome-based sprays and TRPM8 modulators, enabling smaller entrants to carve niches. Real-world evidence and patient-access programs increasingly underpin competitive advantage, especially where payers demand proof of value across the pruritus therapeutic market.

Legacy immunosuppressants still deliver volume sales in emerging regions but face share erosion in developed markets. Biologic developers are countering with discounted vial programs and outcome-based contracts. Companies that combine broad indication footprints with advanced manufacturing appear best positioned to sustain margin resilience.

Pruritus Therapeutics Industry Leaders

Cara Therapeutics

AbbVie Inc.

EPI Health LLC

Sanofi

Galderma S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Galderma announced two-year data from long-term nemolizumab studies demonstrating sustained efficacy and favorable safety profile, with over 85% of patients achieving significant reductions in eczema severity and itch, reinforcing the drug's strategic importance in the expanding pruritus therapeutic market.

- April 2025: AbbVie reported first-quarter 2025 results with immunology portfolio growth of 16.6%, driven by Skyrizi revenue increase of 70.5% and Rinvoq growth of 57.2%, while receiving European Commission marketing authorization for Rinvoq in giant cell arteritis.

- March 2025: Novartis licensed Kyorin's preclinical chronic hives candidate for USD 55 million upfront in an USD 830 million deal, demonstrating continued strategic investment in the pruritus therapeutic space.

- December 2024: FDA approved nemolizumab (Nemluvio) for moderate-to-severe atopic dermatitis in patients aged 12 and older, marking the first IL-31 receptor alpha-targeting monoclonal antibody approval and expanding treatment options for previously difficult-to-treat patients.

- September 2024: Organon completed acquisition of Dermavant including VTAMA (tapinarof) cream, expanding its dermatology portfolio and market presence in the growing topical treatment segment for psoriasis and atopic dermatitis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pruritus therapeutics market as all prescription and over-the-counter pharmacologic agents, topical, oral, or parenteral, that are clinically employed to relieve or modulate itch arising from dermatologic, systemic, or neuropathic etiologies. Value estimates refer to manufacturer sales in constant 2025 US dollars, aggregated across every geography and therapy class.

Scope exclusion: single-use medical devices and phototherapy equipment are not counted, because their revenue flows differ from drug channels and would inflate drug-only market values.

Segmentation Overview

- By Product Type

- Corticosteroids

- Antihistamines

- Local Anesthetics

- Counterirritants

- Immunosuppressants

- Calcineurin Inhibitors

- Opioid Receptor Antagonists

- Antidepressants

- PDE-4 Inhibitors

- JAK Inhibitors

- By Disease Type

- Atopic Dermatitis

- Allergic Contact Dermatitis

- Urticaria

- Cholestatic Pruritus

- Hematologic Pruritus

- Neuropathic Pruritus

- Oncologic Pruritus

- Other Disease Type

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Targeted interviews and short surveys with dermatologists, nephrologists, hospital pharmacists, and reimbursement managers across North America, Europe, and key Asia-Pacific economies let us confirm real-world prescribing shares, average selling prices, patient co-pay hurdles, and likely uptake trajectories for biologics and JAK inhibitors. Feedback from these conversations feeds directly into assumption vetting and variable weighting.

Desk Research

Our analysts start with structured reviews of reputable, open datasets such as the WHO Global Health Observatory, the Global Burden of Disease project, NIH-funded prevalence studies, and OECD Health Statistics, which supply baseline incidence, treatment-seeking, and demographic ratios. We layer these with regulatory filings, 10-Ks, pricing compendia, and pharmacy dispensation audits, then mine specialized paid sources like D&B Hoovers for company-level revenue splits that anchor leading brand performance. Trade association briefs from bodies such as the American Academy of Dermatology and national renal societies help us spot guideline shifts and formulary additions that reshape demand. The sources mentioned illustrate, rather than exhaust, the wider set consulted.

Market-Sizing & Forecasting

A single top-down and bottom-up loop underpins the model. Prevalence-to-treated-cohort calculations generate demand pools that are priced using blended ASPs; outputs are balanced against sampled supplier roll-ups and channel checks to correct under-reporting. Critical variables include: 1) atopic dermatitis prevalence, 2) chronic kidney disease-associated pruritus incidence, 3) prescription fill rates by therapy class, 4) biologic penetration curves, and 5) retail price inflation differentials. Multivariate regression with an ARIMA overlay projects each driver, while scenario analysis captures uncertainty around safety warnings or label expansions. Where bottom-up estimates lag audited sales, calibration factors redistribute volume using hospital purchase audits.

Data Validation & Update Cycle

Model outputs undergo variance checks against external benchmarks; then a senior analyst re-runs anomaly filters before sign-off. Reports refresh annually; emergency updates trigger after major approvals, safety withdrawals, or reimbursement shocks, ensuring clients meet an always-current baseline.

Why Mordor's Pruritus Therapeutics Baseline Inspires Confidence

Published market values rarely align because firms select different therapy scopes, patient funnels, currency bases, and update cadences.

Key gap drivers include whether OTC antihistamines are counted, how biologic ASP step-downs are treated, and the frequency with which epidemiology inputs are refreshed before currency conversion adjustments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.97 B | Mordor Intelligence | - |

| USD 9.29 B | Global Consultancy A | Excludes OTC topicals and applies a conservative biologic uptake curve |

| USD 11.74 B | Industry Association B | Adds device-based phototherapy revenue and converts currencies at forecast, not base-year, rates |

Taken together, the comparison shows that Mordor Intelligence applies a disciplined definition, transparent variables, and an annual refresh cycle that together deliver a balanced, reproducible starting point for strategic decisions.

Key Questions Answered in the Report

What is the current value of the pruritus therapeutic market?

The pruritus therapeutic market was valued at USD 10.39 billion in 2026 and is projected to reach USD 12.74 billion by 2031.

Which product class is growing fastest in the pruritus therapeutic market?

JAK inhibitors are forecast to expand at a 5.59% CAGR through 2031, the fastest among all product categories.

Which is the fastest growing region in Pruritus Therapeutics Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Why is Asia-Pacific the most attractive growth region?

Regulatory harmonization with ICH guidelines, expanded insurance coverage, and first-in-world approvals in Japan are driving an 8.18% CAGR in Asia-Pacific.

What is the biggest safety concern influencing prescribing trends?

Long-term cardiovascular and malignancy risks linked to JAK inhibitors have prompted FDA and EMA warnings, shaping clinician choice, especially for elderly patients.

Which unmet indication represents a major white-space opportunity?

Cholestatic pruritus remains largely untreated; positive Phase III data for linerixibat could open the first dedicated therapy for this condition and unlock new revenue.

Page last updated on: