Uropathy Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

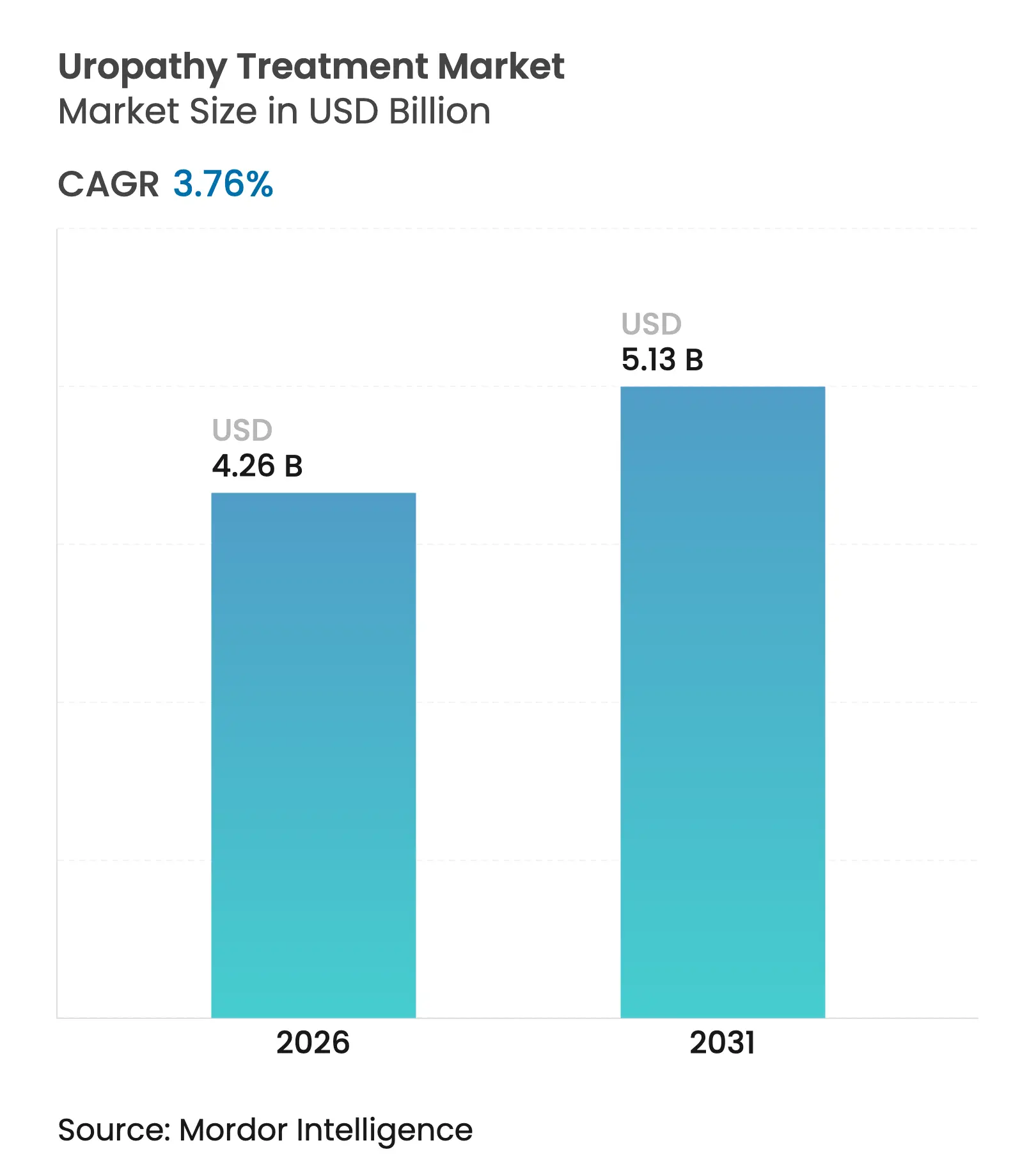

| Market Size (2026) | USD 4.26 Billion |

| Market Size (2031) | USD 5.13 Billion |

| Growth Rate (2026 - 2031) | 3.76 % CAGR |

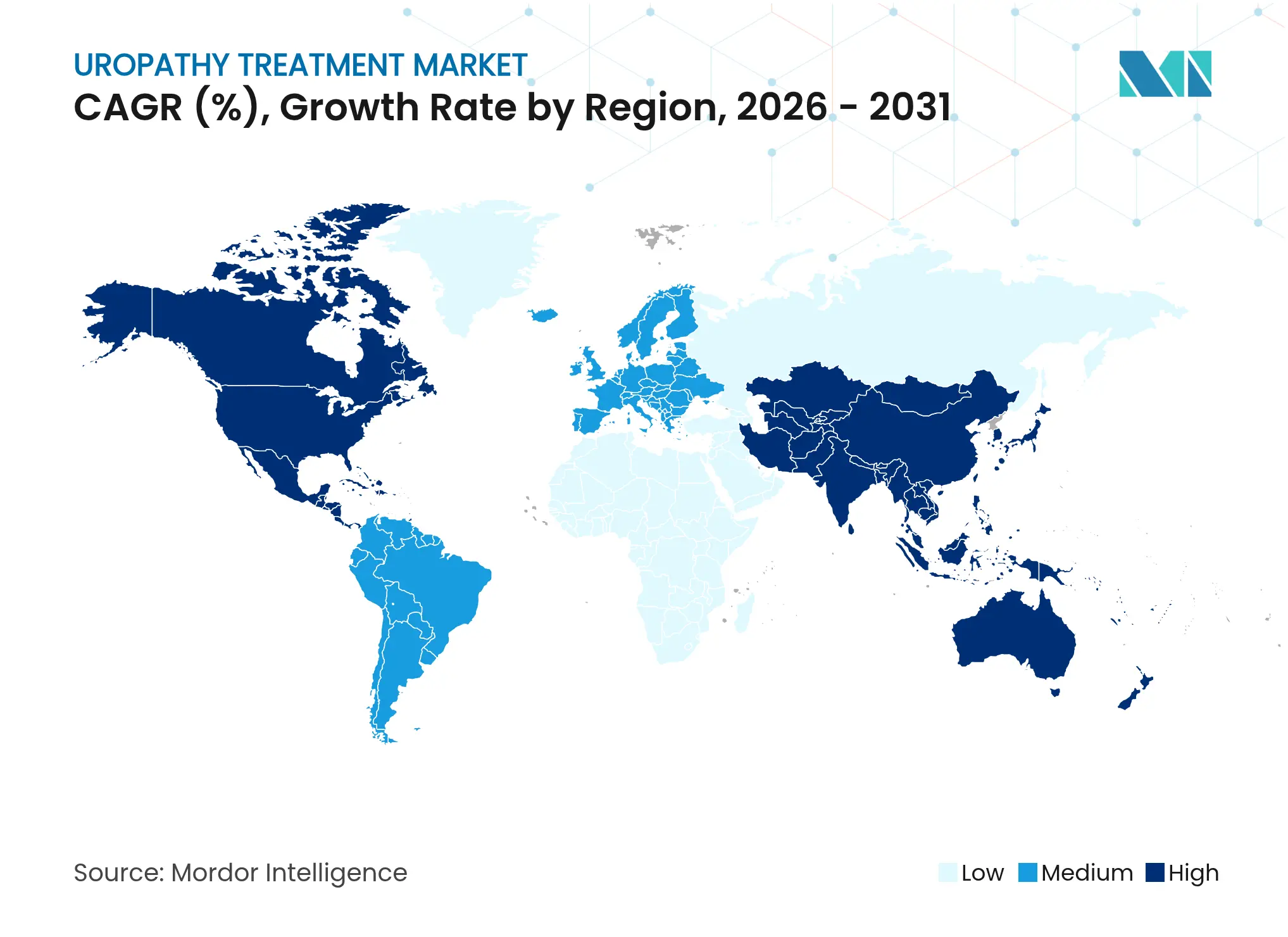

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Uropathy Treatment Market Analysis by Mordor Intelligence

The uropathy treatment market size was valued at USD 4.11 billion in 2025 and estimated to grow from USD 4.26 billion in 2026 to reach USD 5.13 billion by 2031, at a CAGR of 3.76% during the forecast period (2026-2031). This steady pace reflects a mature yet resilient landscape in which essential therapies counterbalance supply-chain stresses, litigation risk and regulatory complexity. Aging populations expand the addressable patient pool, mini-invasive drainage techniques shorten length of stay, and antimicrobial device innovation lifts pricing power [1]Centers for Medicare & Medicaid Services, “Ambulatory Surgical Center Fee Schedule,” cms.gov. At the same time, polymer shortages and stricter product-safety standards lengthen production lead times, preventing the uropathy treatment market from accelerating beyond mid-single-digit growth. Competitive dynamics favor firms that can integrate infection-resistant designs, diversified sourcing and value-based pricing into their offerings, ensuring stable volumes even during economic slowdowns.

Key Report Takeaways

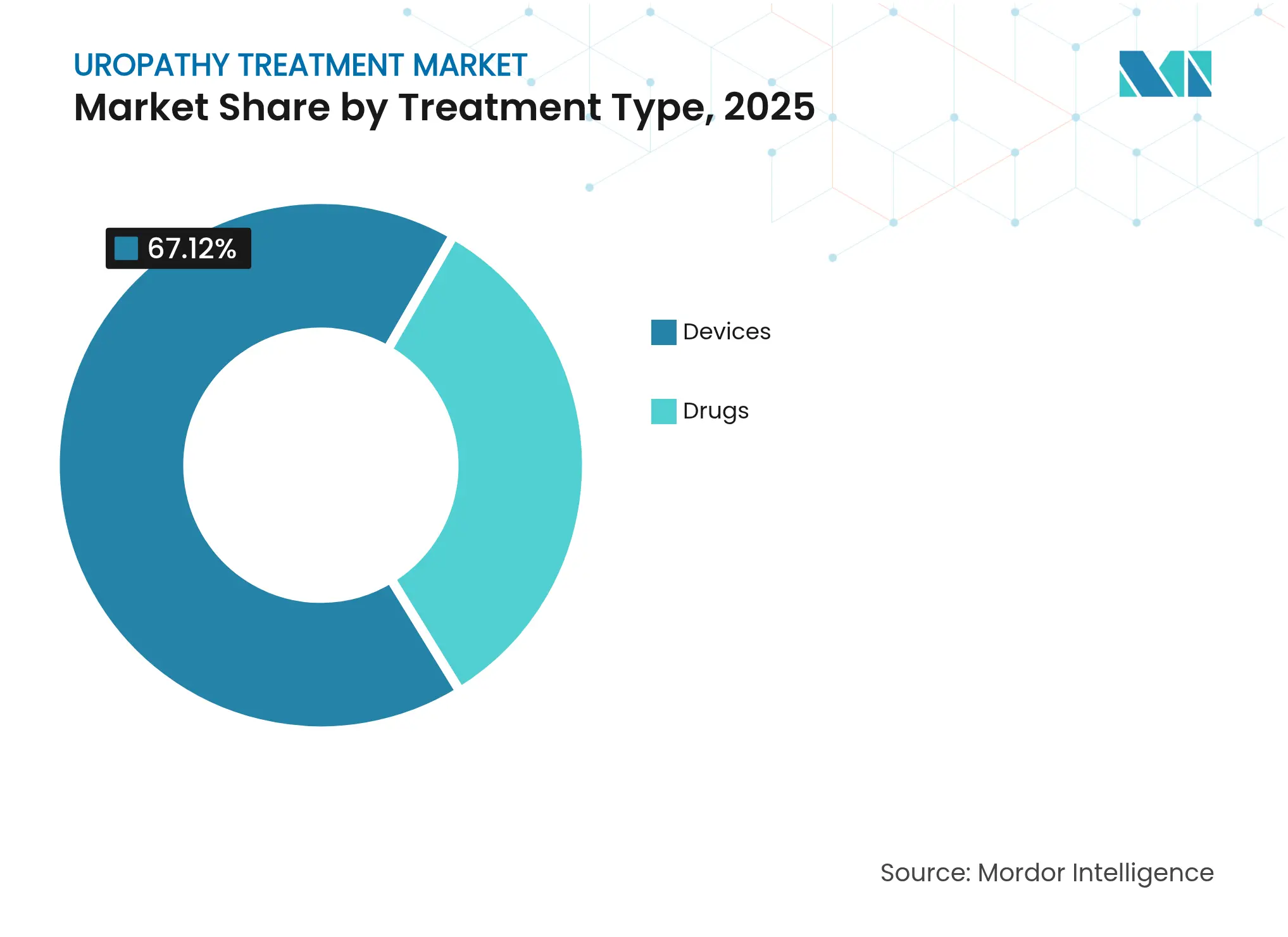

- Device-centric revenue streams commanded a 67.12% uropathy treatment market share in 2025, while the drug segment is advancing at a 4.32% CAGR through 2031.

- The geriatric age group is expanding at a 4.42% CAGR, although adult patients continued to account for 70.68% of demand in 2025.

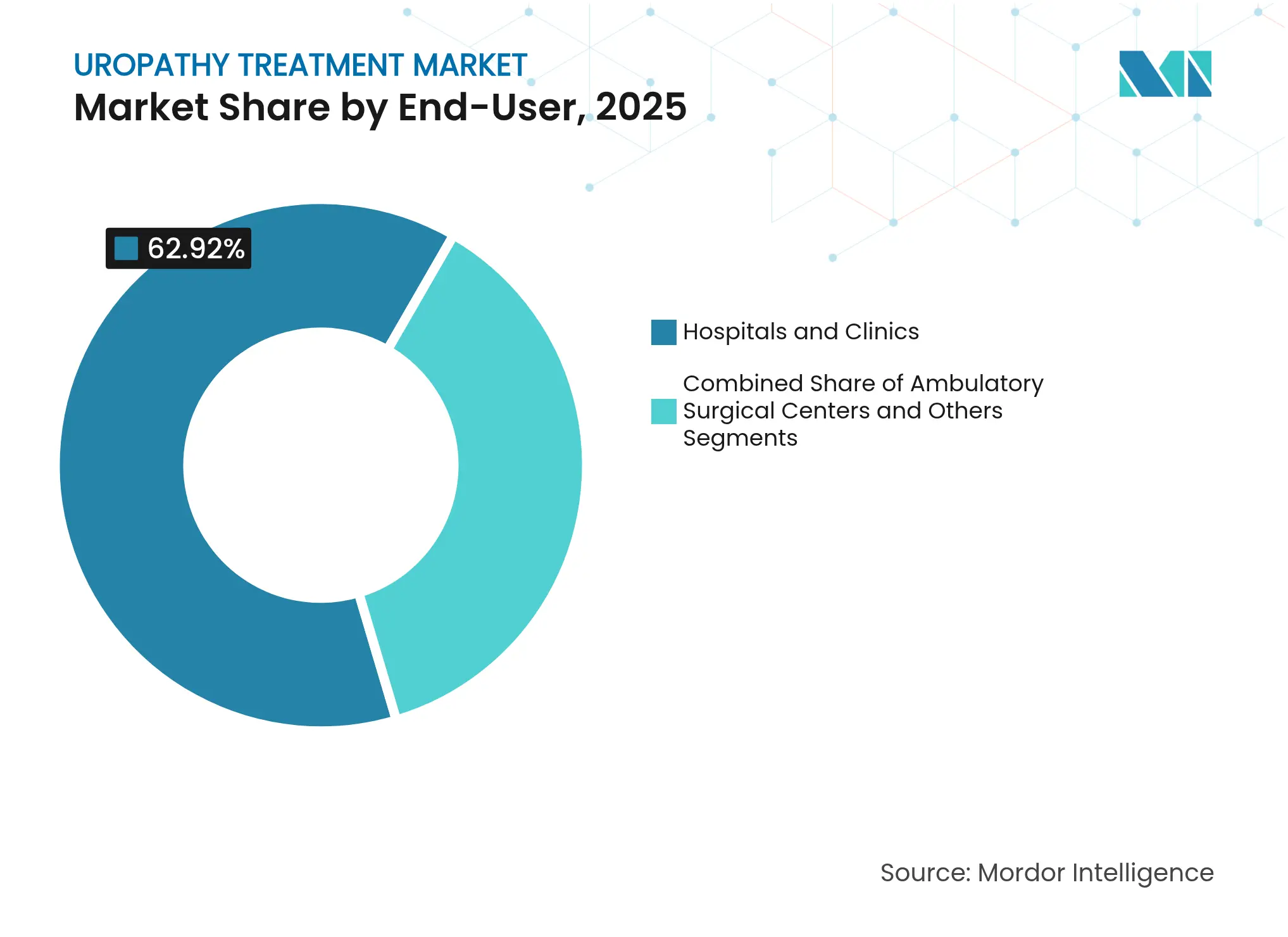

- Ambulatory surgical centers are growing at a 4.37% CAGR, whereas hospitals and clinics retained 62.92% of the uropathy treatment market share in 2025.

- North America held 43.05% of revenue in 2025; however, Asia-Pacific is set to post the fastest regional CAGR at 4.51% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Uropathy Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Mini-invasive drainage demand amid rapid growth of

ambulatory urology centers

Mini-invasive drainage demand amid rapid growth of

ambulatory urology centers

| +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

|

Geographic Relevance

:

North America & Europe, expanding to APAC

|

Impact Timeline

:

Medium term (2-4 years)

|

Aging-population surge in BPH & incontinence cases

Aging-population surge in BPH & incontinence cases

| +1.5% | Global, with concentration in developed markets | Long term (≥ 4 years) | |||

Antimicrobial & hydrophilic catheter‐coating

breakthroughs

Antimicrobial & hydrophilic catheter‐coating

breakthroughs

| +0.8% | Global, led by North America and Europe | Short term (≤ 2 years) | |||

AI-guided imaging for early obstruction detection

AI-guided imaging for early obstruction detection

| +0.6% | North America, Europe, select APAC markets | Medium term (2-4 years) | |||

Transition to home-based intermittent catheterization

Transition to home-based intermittent catheterization

| +0.4% | North America & Europe, emerging in APAC | Medium term (2-4 years) | |||

Reimbursement expansion for outpatient ureteral stenting

Reimbursement expansion for outpatient ureteral stenting

| +0.3% | North America & Europe | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Mini-Invasive Drainage Procedures Drive Ambulatory Center Expansion

Ambulatory surgical centers deliver urological procedures at 38% lower cost than hospital outpatient departments, a differential that propels migration toward specialized outpatient sites. Same-day discharge protocols for percutaneous nephrostomy and ureteral stenting align with ASC throughput models and cut postoperative monitoring expenses. Next-generation drainage catheters with antimicrobial coatings cut post-procedure complications by 23%, improving patient satisfaction in lower-acuity settings. The December 2024 FDA clearance of the RELIEF ureteral stent highlights how regulatory momentum accelerates adoption of mini-invasive solutions [2]U.S. Food and Drug Administration, “Medical Device Approvals and Clearances,” fda.gov. As ASC volumes climb, procurement scale feeds back into pricing leverage, reinforcing a virtuous cycle of cost and quality improvement over the medium term.

Demographic Transition Intensifies BPH and Incontinence Burden

One in two men over 60 develops benign prostatic hyperplasia, and one in four women over 65 experiences urinary incontinence, statistics that rise with longevity gains. Japan’s 34% uptick in urological device utilization from 2020-2024 illustrates the super-aged trajectory fast approaching Western markets [3]World Health Organization, “Ageing and Health,” who.int . Chronic symptom management elevates pharmaceutical relevance because drugs require less infrastructure than surgery and pose fewer peri-operative risks for frail patients. Consequently, healthcare systems allocate more budget to long-term medication regimens that preserve dignity and independence for senior citizens. These dynamics strengthen demand for novel alpha-blocker combinations and targeted bladder therapeutics, sustaining a pipeline of premium formulations.

Antimicrobial Coating Technologies Transform Infection Prevention

Catheter-associated urinary tract infections impose USD 2.3 billion in annual treatment costs worldwide. Silver-ion and chlorhexidine coatings cut bacterial colonization by 65% during extended catheterization, materially lowering the risk profile of long-term drainage. Hydrophilic surfaces reduce urethral micro-trauma, thereby enhancing patient adherence to self-catheter protocols in home settings. The September 2024 FDA approval of the InnoCare Specialty Foley Catheter validates the commercial proposition of infection-resistant designs and secures reimbursement premiums. Hospitals eager to curb malpractice exposure increasingly negotiate purchasing contracts that stipulate antimicrobial features as minimum standards, raising unit ASPs and reshaping competitive moats.

AI-Guided Imaging Revolutionizes Early Detection Protocols

Machine-learning models embedded in ultrasound platforms now detect urinary obstructions with 87% accuracy, outperforming manual interpretation, particularly in elderly patients with anatomical variability. Early identification prevents renal damage and lowers emergency intervention rates by 28%, improving outcomes while trimming acute-care expenditures. Routine screening protocols can be executed by mid-level clinicians, easing workforce constraints and extending access in underserved areas. Diagnostic-equipment vendors differentiate through AI workflows that integrate seamlessly with existing radiology infrastructure, expanding software licensing revenue. The clinical shift toward pre-emptive obstruction management triggers ripple effects across device demand, with earlier valve and stent placement displacing complex restorative surgery volumes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Catheter-associated UTI (CAUTI) litigation risk

Catheter-associated UTI (CAUTI) litigation risk

| -0.7% | North America & Europe, emerging in APAC | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.7%

|

Geographic Relevance

:

North America & Europe, emerging in APAC

|

Impact Timeline

:

Short term (≤ 2 years)

|

Supply-chain scarcity of medical-grade polymers

Supply-chain scarcity of medical-grade polymers

| -0.5% | Global, acute in North America and Europe | Medium term (2-4 years) | |||

Patient non-adherence to self-catheter protocols

Patient non-adherence to self-catheter protocols

| -0.4% | Global, particularly in emerging markets | Long term (≥ 4 years) | |||

Limited skilled labour for complex endourology procedures

in LMICs

Limited skilled labour for complex endourology procedures

in LMICs

| -0.3% | Low and middle-income countries | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

CAUTI Litigation Creates Operational Risk Premium

Average malpractice settlements for catheter-related complications stand at USD 2.5 million, with urethral-injury claims rising fastest. Hospitals institute restrictive catheterization guidelines, curbing device usage and elongating approval pathways. Insurers demand extensive documentation and staff retraining, raising indirect costs and disfavoring smaller providers. The liability climate spurs adoption of antimicrobial solutions yet simultaneously narrows overall procedure volumes, tempering the growth profile of the uropathy treatment market.

Polymer Supply-Chain Vulnerabilities Constrain Production Scalability

Sixty-seven percent of urological-device producers cite silicone and polyurethane shortages as the top manufacturing hurdle. Reliance on Asia-centric suppliers magnifies exposure to shipping delays, while ethylene-oxide sterilization capacity remains oversubscribed. Alternate gamma-irradiation protocols require material reformulation, extending regulatory timelines and inflating R&D budgets. Large incumbents with diversified sourcing absorb these shocks through scale, whereas smaller innovators struggle to maintain product availability, limiting market dynamism.

Segment Analysis

By Treatment Type: Device Dominance Faces Pharmaceutical Disruption

Devices captured a 67.12% share of the uropathy treatment market in 2025, reflecting their indispensability in acute interventions. Recurring needs for catheters, stents and drainage systems underpin stable revenue cycles, while high capital intensity supports premium pricing. The USD 3.7 billion Boston Scientific–Axonics deal in August 2024 spotlights strategic consolidation around sacral neuromodulation, a high-growth frontier within the device universe.

Pharmaceuticals are scaling faster, with a 4.32% CAGR through 2031. Combination alpha-blocker formulations and targeted drug-delivery platforms appeal to payers eager to curtail procedure costs. Predictable approval pathways further encourage investment, positioning drug therapy as the principal disruptor to long-established device revenue streams over the forecast horizon. The uropathy treatment market size attributable to drugs is projected to climb from USD 1.32 billion in 2025 to USD 1.7 billion in 2031, underscoring its role in the long-run growth mix.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Geriatric Surge Reshapes Treatment Paradigms

Adults generated 70.68% of revenue in 2025, validating middle-age prevalence of BPH, overactive bladder and trauma-induced uropathy. However, the geriatric cohort is registering a 4.42% CAGR, outpacing all other segments and foreshadowing a structural demand shift. In Japan, uropathy device utilization climbed 34% between 2020 and 2024 as median age breached 48 years, a pattern likely to replicate first in Europe, then North America.

Providers therefore recalibrate product portfolios toward low-risk, home-friendly solutions tailored to frailty and comorbidity management. The uropathy treatment market share held by geriatric patients is on track to grow from 22.50% in 2025 to about 25.80% by 2031, compelling firms to invest in geriatric-centric design and packaging.

By End-User: Ambulatory Centers Challenge Hospital Hegemony

Hospitals and clinics controlled 62.92% of revenue in 2025, grounded in their capacity to manage complex cases and emergencies. Yet ambulatory surgical centers are rising at a 4.37% CAGR, helped by 38% cost savings versus hospital outpatient departments.

Medicare reimbursement policies now designate many stenting and drainage procedures as ASC-eligible, catalyzing patient and payer migration. To stay relevant, hospitals are opening satellite outpatient suites and partnering with ASC networks, thus blurring traditional boundaries. Meanwhile, home healthcare and specialty clinics in the “Others” category incubate niche opportunities in intermittent self-catheterization and tele-urology consults, supporting diversification strategies for device makers.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for 43.05% of global revenue in 2025, a position reinforced by robust reimbursement, clinical research infrastructure and predictable FDA approval pathways. Broad payer coverage lowers out-of-pocket burden, fostering early adoption of antimicrobial catheters and neuromodulation implants. Demographic aging keeps procedure volumes high even as cost-containment initiatives intensify. The uropathy treatment market size in the United States alone is estimated at USD 1.68 billion in 2026, expanding at a steady 3.56% CAGR.

Asia-Pacific is the growth engine, advancing at 4.51% CAGR through 2031. China’s streamlined device-registration reforms and large unmet patient base accelerate unit sales, while tier-2 city hospital upgrades stimulate capital equipment demand. India’s public-private hospital expansion unlocks procurement for value-oriented catheters and stents suited to constrained budgets. Japan exemplifies how super-aging supports high uptake of intermittent self-catheterization devices, offering lessons transferable to South Korea and Singapore.

Europe delivers moderate growth as the region harmonizes under the Medical Device Regulation. Germany and the United Kingdom lead adoption of AI-enabled imaging, whereas Southern Europe remains price sensitive, favoring proven, lower-cost devices. Brexit adds a layer of logistical complexity, but mutual-recognition agreements are beginning to restore cross-border supply predictability.

The Middle East and Africa lag in volume yet offer upside in medical tourism hubs such as the United Arab Emirates, where premium urological care packages attract international patients looking for short wait times and advanced technology.

Competitive Landscape

Market Concentration

The uropathy treatment market is moderately consolidated, with the top five suppliers controlling roughly 46% of revenue. Boston Scientific’s Axonics acquisition cemented leadership in neuromodulation while illustrating the premium placed on high-growth niches. Coloplast, Teleflex, B. Braun and Cook Medical compete through infection-prevention coatings, ergonomic designs and customer-education platforms. Supply-chain resilience now acts as a strategic differentiator; companies with multi-region polymer sourcing and in-house sterilization secure production continuity and pricing stability.

Innovation pivots on infection resistance and patient comfort. The InnoCare antimicrobial Foley Catheter and the RELIEF biocompatible ureteral stent both received FDA clearance in 2024, raising clinical performance benchmarks. Digital-health entrants develop AI algorithms for early obstruction detection, forcing traditional device vendors to pursue software partnerships or organic build-outs. The competitive intensity is therefore shifting from purely physical hardware to integrated care ecosystems that span diagnostics, devices and remote monitoring.

Uropathy Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: FDA granted 510(k) clearance for the RELIEF ureteral stent, introducing enhanced biocompatible materials and comfort-first design.

- September 2024: InnoCare Specialty Foley Catheter obtained FDA approval, demonstrating 65% reduction in bacterial colonization rates.

- August 2024: Boston Scientific completed its USD 3.7 billion acquisition of Axonics, expanding its neuromodulation platform.

- July 2024: Medtronic announced a USD 150 million investment in automated urological device manufacturing facilities in Ireland.

Table of Contents for Uropathy Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Mini-invasive drainage demand amid rapid growth of ambulatory urology centers

- 4.2.2Aging-population surge in BPH & incontinence cases

- 4.2.3Antimicrobial & hydrophilic catheter‐coating breakthroughs

- 4.2.4AI-guided imaging for early obstruction detection

- 4.2.5Transition to home-based intermittent catheterization

- 4.2.6Reimbursement expansion for outpatient ureteral stenting

- 4.3Market Restraints

- 4.3.1Catheter-associated UTI (CAUTI) litigation risk

- 4.3.2Supply-chain scarcity of medical-grade polymers

- 4.3.3Patient non-adherence to self-catheter protocols

- 4.3.4Limited skilled labour for complex endourology procedures in LMICs

- 4.4Regulatory Landscape

- 4.5Porter’s Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers/Consumers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitute Products

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Treatment Type

- 5.1.1Devices

- 5.1.2Drugs

- 5.2By Age Group

- 5.2.1Pediatric

- 5.2.2Adult

- 5.2.3Geriatric

- 5.3By End-user

- 5.3.1Hospitals and Clinics

- 5.3.2Ambulatory Surgical Centres

- 5.3.3Others

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Boston Scientific Corporation

- 6.3.2Becton, Dickinson & Co.

- 6.3.3Teleflex Inc.

- 6.3.4Coloplast A/S

- 6.3.5Cook Medical

- 6.3.6Olympus Corporation

- 6.3.7B. Braun Melsungen AG

- 6.3.8Cardinal Health

- 6.3.9Medtronic plc

- 6.3.10Merit Medical Systems

- 6.3.11Argon Medical Devices

- 6.3.12ConvaTec Group

- 6.3.13Hollister Incorporated

- 6.3.14Smiths Medical

- 6.3.15Urotronic Inc.

- 6.3.16Coloplast – Atos Medical

- 6.3.17Dornier MedTech

- 6.3.18Siemens Healthineers

- 6.3.19Stryker Corporation

- 6.3.20Inari Medical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Uropathy Treatment Market Report Scope

As per the scope of the report, Uropathy is a disease of the urinary or urogenital organs that may result in the urinary related problems. Urinary system related problems include conditions such as kidney failure, urinary tract infections, kidney stones, prostate enlargement, and bladder control problems. Uropathy Treatment Market is segmented By Treatment type, End-user and Geography.