Postoperative Nausea And Vomiting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

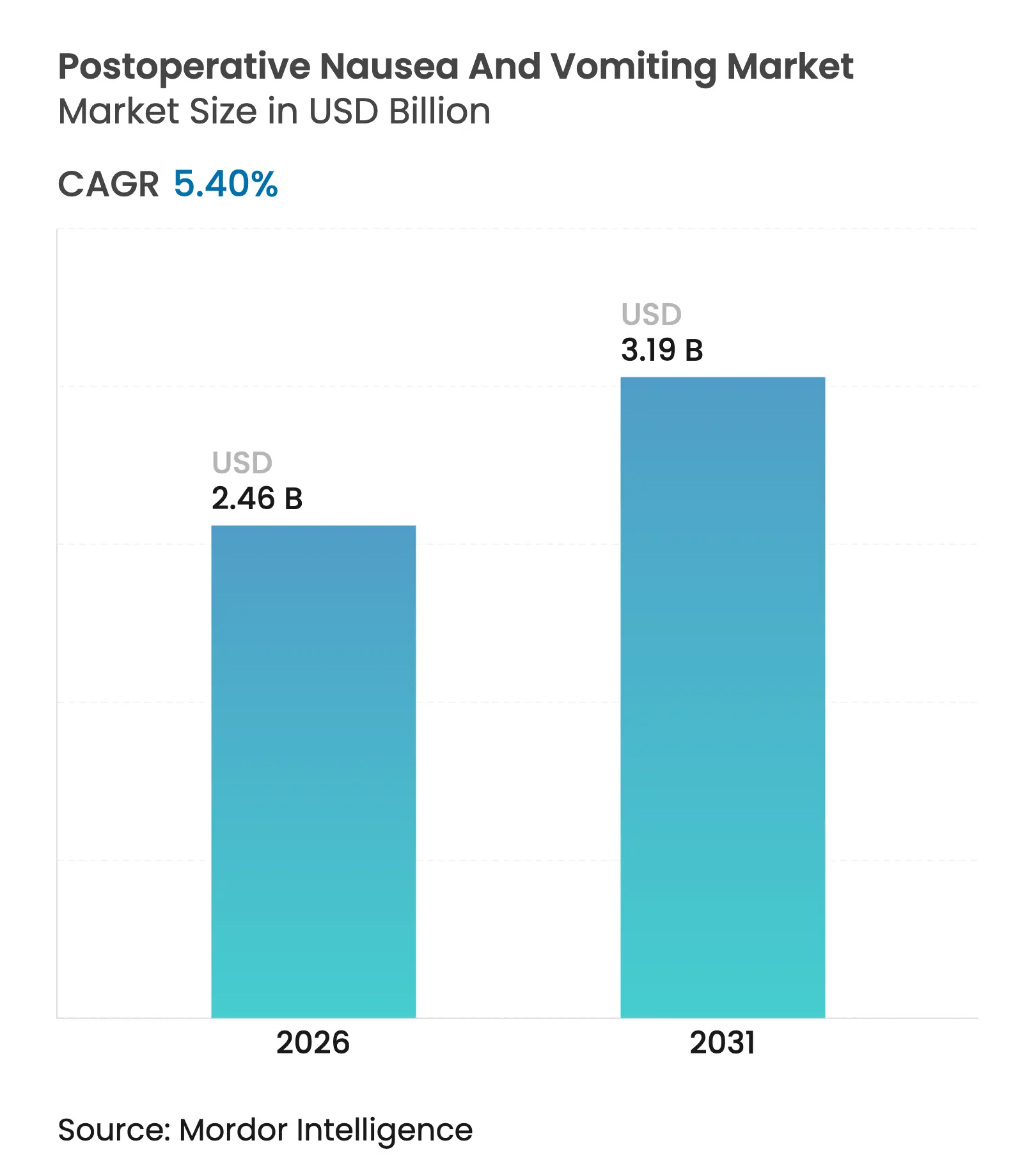

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 5.40 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Postoperative Nausea And Vomiting Market Analysis by Mordor Intelligence

The postoperative nausea vomiting market size is expected to grow from USD 2.33 billion in 2025 to USD 2.46 billion in 2026 and is forecast to reach USD 3.19 billion by 2031 at 5.40% CAGR over 2026-2031. Continuous quality-of-care benchmarking, wider adoption of enhanced recovery after surgery protocols, and pay-for-performance incentives keep prophylactic antiemetic use on every hospital’s scorecard. Higher surgical throughput in outpatient centers, coupled with the growing mix of complex oncological procedures, is also pushing demand upward. At the same time, price competition from generics intensifies, driving an innovation race toward long-acting injectables and fixed-dose combinations that can justify premium reimbursement. Regulatory encouragement for combination labeling and the integration of digital risk-scoring tools further enlarge the addressable patient pool without adding significant administrative burden.

Key Report Takeaways

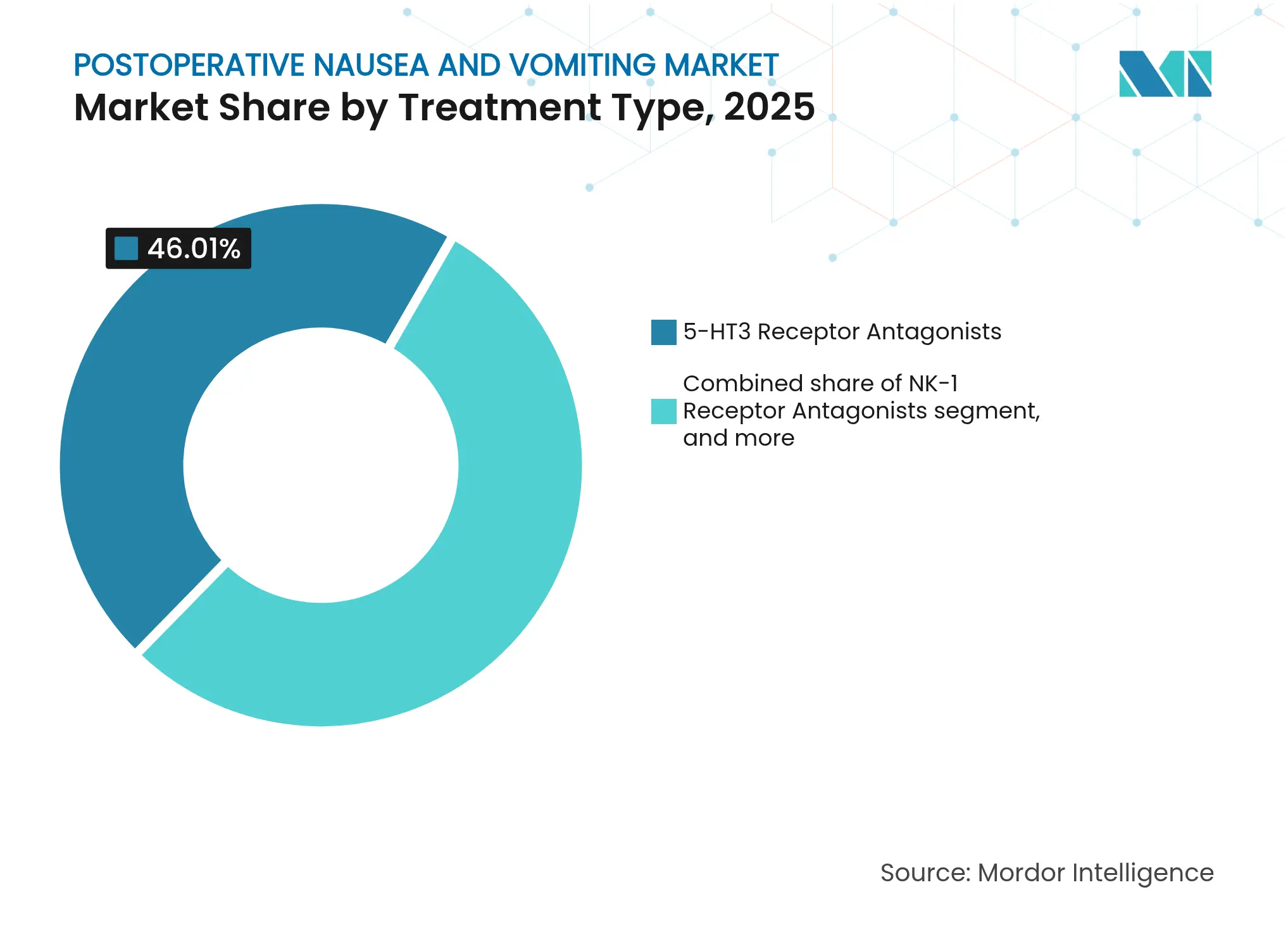

- By treatment type, 5-HT3 receptor antagonists held 46.01% of the postoperative nausea vomiting market share in 2025, while NK-1 receptor antagonists are expanding at a 7.53% CAGR through 2031.

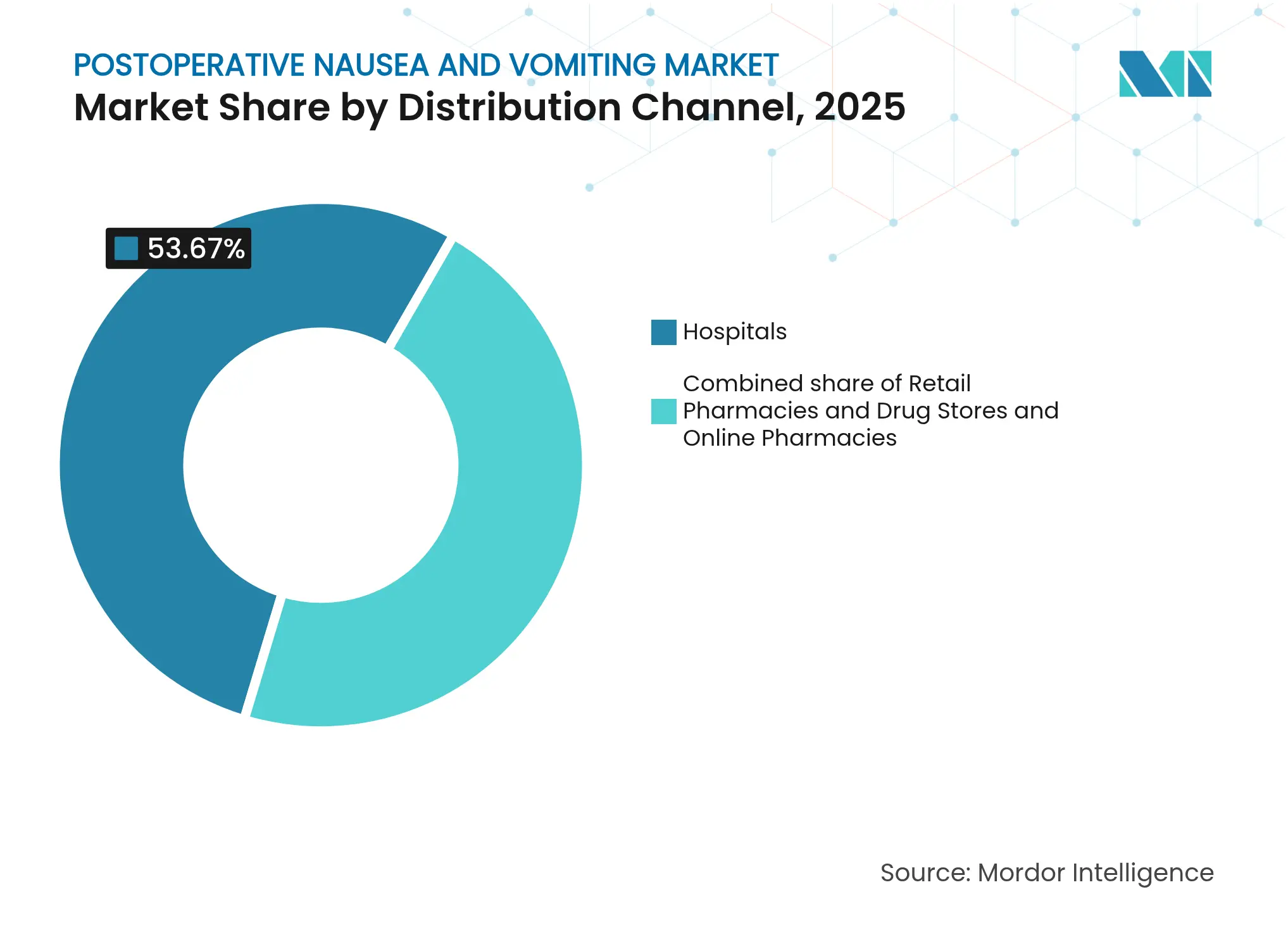

- By distribution channel, hospital pharmacies captured 53.67% of revenue in 2025, whereas online pharmacies are moving ahead at an 8.54% CAGR to 2031.

- By end user, hospitals accounted for 56.12% of the postoperative nausea vomiting market size in 2025; ambulatory surgical centers represent the fastest-growing setting with an 8.32% CAGR over the same horizon.

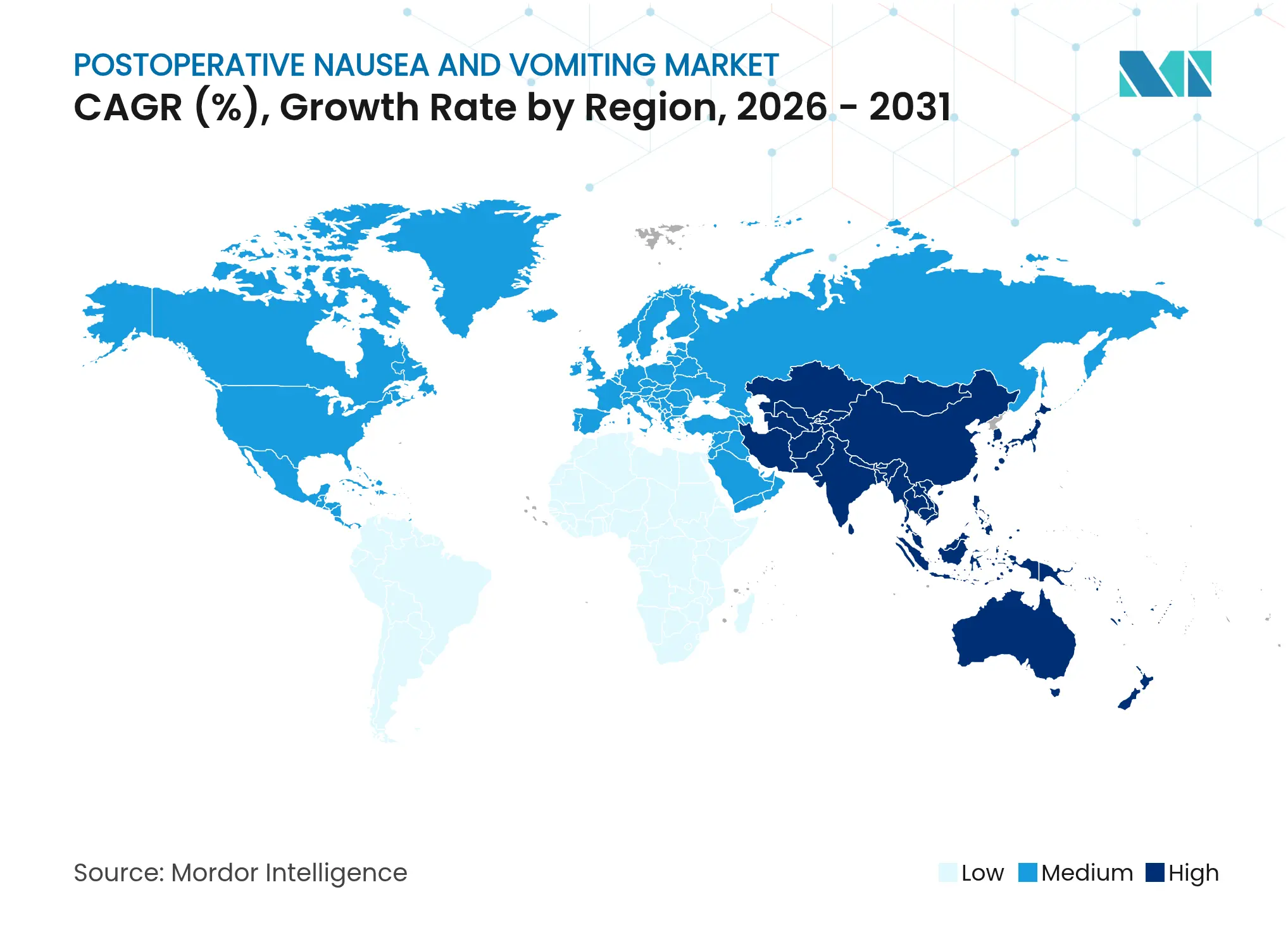

- By geography, North America dominated with a 40.06% share in 2025, while Asia-Pacific is projected to lead growth at a 6.36% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Postoperative Nausea And Vomiting Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing surgical procedure volume Growing surgical procedure volume | +1.2% | Global; strongest in APAC and North America | Medium term (2-4 years) | % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global; strongest in APAC and North America | Impact Timeline:Medium term (2-4 years) |

Rising oncology and geriatric population Rising oncology and geriatric population | +0.9% | Global; emphasis on mature health systems | Long term (≥ 4 years) | |||

Guideline-driven multimodal prophylaxis Guideline-driven multimodal prophylaxis | +1.1% | North America & EU; spill-over to APAC | Short term (≤ 2 years) | |||

Launch of long-acting combination antiemetics Launch of long-acting combination antiemetics | +0.8% | Core markets in North America & EU | Medium term (2-4 years) | |||

Personalized medicine & digital risk tools Personalized medicine & digital risk tools | +0.6% | North America & EU; early uptake in urban APAC | Long term (≥ 4 years) | |||

PACU cost-savings from shorter recovery time PACU cost-savings from shorter recovery time | +0.7% | Global; strongest in cost-sensitive systems | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Surgical Procedure Volume

Global procedure counts continue to climb as aging populations and wider insurance coverage push more patients into operating rooms. Machine-learning reviews of 37,548 cases found that the intensity of surgery—reflected by blood-loss levels—predicts vomiting risk better than raw volume, steering hospitals toward broader prophylaxis protocols[1]Zhaoqiang Zheng et al., “Machine Learning Improves Prediction of PONV,” PLOS ONE, journals.plos.org. Enhanced-recovery pathways link effective PONV prevention to shorter post-anesthesia care unit stays, making antiemetics a cost-avoidance tool rather than a discretionary add-on. Ambulatory surgical centers benefit most because their business model relies on rapid turnover and same-day discharge. As a result, procedure growth translates into disproportionate demand for long-acting and combination antiemetics that guarantee nausea-free recovery windows.

Rising Oncology and Geriatric Patient Population

Cancer patients often arrive for surgery with prior chemotherapy exposure and compromised reserves, elevating their baseline risk of postoperative emesis. Older adults metabolize drugs unpredictably and face polypharmacy interactions, prompting clinicians to favor fixed-dose combinations with wider receptor coverage. Together these cohorts create sustained demand for premium antiemetic regimens that can justify higher reimbursement. Hospitals view reliable control as essential because failed prophylaxis in fragile groups extends hospital stays and raises readmission penalties. The demographic overlap in surgical oncology therefore anchors a high-value segment within the postoperative nausea vomiting market.

Guideline-Driven Adoption of Multimodal Antiemetic Prophylaxis

The Fourth Consensus Guidelines mandate risk-stratified, multi-agent prophylaxis as the new standard of care, replacing single-drug strategies that dominated prior years. Combination regimens cost several times more per case but cut rescue interventions by nearly two-thirds, freeing nursing resources for higher-acuity tasks. North American and European hospitals were first to integrate these protocols because payer scorecards tie quality bonuses to patient-reported outcomes. Asia-Pacific centers are catching up quickly, motivated by medical-tourism competition that prizes high satisfaction ratings. As compliance climbs, formulary committees allocate larger budgets to long-acting injectables and fixed-dose combinations that simplify guideline execution.

Commercial Launch of Long-Acting Combination Antiemetics

Extended-duration products such as the NK-1 formulation APONVIE provide 48–72 hour coverage from a single 30-second IV push, closing the post-discharge nausea gap that affects up to one-third of ambulatory patients. The U.S. Centers for Medicare & Medicaid Services grant separate reimbursement for these drugs, lowering the financial barrier to adoption in hospitals. Because complex delivery systems deter copycat versions, manufacturers enjoy longer effective exclusivity even after molecule patents expire. Ambulatory centers value the reduction in callback visits, which directly influences facility reputation and referral flows. These clinical and economic advantages accelerate uptake, reinforcing overall market growth.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shift to minimally invasive techniques Shift to minimally invasive techniques | −0.8% | Global; led by advanced markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:−0.8% | Geographic Relevance:Global; led by advanced markets | Impact Timeline:Medium term (2-4 years) |

Safety concerns with 5-HT3 & NK-1 classes Safety concerns with 5-HT3 & NK-1 classes | −0.5% | Global; close regulatory scrutiny in developed regions | Short term (≤ 2 years) | |||

Aggressive generic price erosion Aggressive generic price erosion | −1.2% | Global; immediate on older molecules | Short term (≤ 2 years) | |||

Pharmacogenomic variability Pharmacogenomic variability | −0.4% | Global; research concentrated in high-income markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Shift Toward Minimally Invasive and Non-Surgical Alternatives

Robotic and laparoscopic techniques reduce tissue trauma, opioid use and anesthetic exposure, driving PONV incidence down by as much as 40% compared with open procedures. Hospitals performing high volumes of minimally invasive operations now limit prophylaxis to identified high-risk patients, trimming antiemetic utilization despite rising surgical headcounts. Growth in interventional radiology and endoscopic treatments further diverts cases that once required full operating-room support. While severe or lengthy surgeries still demand multi-agent coverage, the expanding share of low-risk procedures tempers overall volume momentum. Manufacturers must therefore innovate to offset shrinking unit demand in routine cases.

Intense Generic Competition Driving Price Erosion

Ondansetron and other first-generation 5-HT3 antagonists now face generic penetration exceeding 90%, slicing average selling prices by up to 80% from branded peaks. Pharmacy benefit managers and national health systems enforce “generic-first” policies, pushing hospitals to start with the lowest-cost option unless strict criteria are met. The pricing squeeze spills into adjacent classes as payers challenge the cost-effectiveness of newer agents lacking differentiation data. Innovator companies respond by bundling drugs with digital decision-support tools or extended-release delivery, but broad market segments remain highly price sensitive. Persistent erosion therefore acts as a drag on revenue growth even while procedure counts and complexity trend upward.

Segment Analysis

By Treatment Type: NK-1 Antagonists Drive Innovation

5-HT3 antagonists captured 46.01% of the postoperative nausea vomiting market share in 2025, reflecting clinical familiarity and multi-source affordability. Their pricing power, however, erodes under sustained generic pressure, pushing innovators toward fixed-dose pairings that include dexamethasone or dopamine blockade for broader receptor coverage. NK-1 antagonists deliver superior delayed-phase control and exhibit the segment’s fastest 7.53% CAGR because guideline authors increasingly recommend them for moderate-to-high-risk patients. Fosaprepitant, for instance, achieved 74.9% rescue success in orthopedic cases where standard care failed, consolidating physician confidence. Non-pharmacologic adjuvants such as acupressure enter bundled pathways but serve more as additive tools than direct competitors.

Combination dosing also improves compliance, an advantage magnified in day-surgery settings where nursing follow-up is minimal. The postoperative nausea vomiting market size for NK-1-based formulations is projected to expand further as innovators add novel transmucosal and subcutaneous routes, simplifying administration in low-resource clinics. Dopamine antagonists continue declining amid extrapyramidal risk, while anticholinergics keep a niche in motion-sensitive cohorts. Overall, therapeutic diversity buttresses total category revenue even where individual compounds mature.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies processed 53.67% of category purchases in 2025 because anesthetists rely on cart-stocked IV formats delivered under strict formulary controls. Yet the online channel posts the highest 8.54% CAGR, propelled by outpatient centers accustomed to direct-to-facility drop-ship arrangements. Integrated e-procurement dashboards allow ambulatory medical directors to reconcile antiemetic usage against case volume daily, trimming waste and favoring vendors offering real-time inventory APIs. That in-platform transparency steers share toward manufacturers capable of instantaneous lot tracing, an emerging tender requirement after supply disruptions in 2024.

Retail outlets hold ground for oral rescue packs dispensed at discharge, especially for bariatric and gynecologic patients prone to delayed symptoms. Specialty pharmacies step into complex oncology pathways, arranging synchronized deliveries of antiemetics alongside chemotherapy cycles. Collectively, channel diversification cushions sales swings and widens geographic reach, reinforcing steady growth in the postoperative nausea vomiting market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Ambulatory Centers Lead Growth

Hospitals retained 56.12% of purchases in 2025 because transplant, cardiac, and high-acuity cancer surgeries still occur largely inside tertiary centers. Large academic institutions embed multimodal prophylaxis bundles into electronic surgical orders, standardizing high-volume demand. Ambulatory surgical centers, however, lead incremental growth at an 8.32% CAGR thanks to payer steering toward lower-cost venues. Their business model prizes same-day discharge, making zero-emesis targets a marketing differentiator. Extended-release injectables match that priority by covering the 72-hour post-op window without repeat dosing.

Specialty clinics—for pain, fertility, or sports injuries—supplement demand with procedure-specific preferences, often favoring shorter-acting or oral options. Innovations such as weight-based NK-1 boluses and personalized genetic dosing will likely debut first in these nimble settings before scaling system-wide. The postoperative nausea vomiting industry finds in ambulatory centers a proving ground for digital risk tools, strengthening the feedback loop between algorithm development and field efficacy.

Geography Analysis

North America held 40.06% of global revenue in 2025, underpinned by mandated quality metrics that tie hospital reimbursement to patient-reported nausea scores. The U.S. Centers for Medicare & Medicaid Services extend separate billing for innovative antiemetics, enabling formulary committees to adopt premium agents such as APONVIE with limited budget friction. Canadian provinces mirror those protocols, albeit with tighter health-technology-assessment thresholds that still favor combination therapy where economic models show shorter recovery room occupancy.

Europe ranks second but imposes centralized price caps and pharmaco-economic dossiers before market entry, prolonging tender cycles. Even so, Northern countries emphasize preventive care and have pushed multimodal coverage rates above 90%, ensuring reliable baseline demand. Southern states exhibit higher generic use yet adopt premium solutions for oncology rotations, balancing cost concerns against clinical imperatives. The European Medicines Agency’s synchronized labeling for palonosetron in pediatrics highlights the region’s coordinated approach, granting manufacturers an efficient pathway to continental scale.

Asia-Pacific is the fastest-growing theatre at a 6.36% CAGR. Japan’s national guidelines drove prophylaxis rates from 91.2% to 96.0% within one year, cutting PONV incidence by double-digits. China’s hospital construction boom and rising medical tourism add high-acuity procedures that require dependable emesis control, boosting uptake of long-acting injectables. India’s generics sector offers low-price 5-HT3 vials that seed basic coverage, while private metro hospitals import NK-1 combinations for affluent patients. Collectively, those trends broaden and deepen the postoperative nausea vomiting market size across a heterogeneous care continuum.

Competitive Landscape

Market Concentration

Competitive intensity is moderate. The top five laboratories command roughly 58% of worldwide revenue through brand longevity and patent portfolios, yet no single drug class enjoys uncontested dominance. Leaders differentiate by pairing legacy molecules with delivery innovations—microsphere suspensions, self-mixing vials, and prefilled push-injectors—imitative options that generics find harder to replicate at scale. Heron Therapeutics maintains a focused salesforce targeting 1,500 acute-care facilities, capturing early share for its long-acting NK-1 line. Mid-tier firms invest in AI-enabled risk calculators that bundle clinical decision support with product access, turning software into a stickier moat around drug supply.

Generic manufacturers compete on price, but hospital buyers increasingly demand evidence packages that include workflow analytics and patient-reported outcome dashboards. That requirement privileges well-capitalized entrants who can run post-marketing registries. Pipeline reviews show a tilt toward pediatric and ultra-long-acting assets, promising up to five-day coverage for transplant surgeries. Takeover interest centers on biotech startups with proprietary nanoparticle carriers deemed complementary to established oral tablets. Though pricing pressure persists, the resulting innovation cycle sustains steady uplift in the postoperative nausea vomiting market.

Postoperative Nausea And Vomiting Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Heron Therapeutics settled with Mylan, deferring CINVANTI and APONVIE generics until June 2032.

- April 2025: Investigational trials launched for ondansetron-gabapentin co-therapy in bariatric surgery and ondansetron-promethazine in gynecology.

- March 2025: European Medicines Agency updated palonosetron labeling to cover pediatric use across all surgical subspecialties.

- February 2025: Heron Therapeutics reported USD 144.2 million net revenue for 2024, driven by APONVIE’s first full commercial year.

- January 2025: FDA cleared Vertex Pharmaceuticals’ suzetrigine for acute pain, potentially reducing opioid-induced nausea in postoperative care.

- January 2025: Kyowa Kirin recorded 12% fiscal-year sales growth, citing R&D expansion in supportive-care assets.

Table of Contents for Postoperative Nausea And Vomiting Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Surgical Procedure Volume

- 4.2.2Rising Oncology and Geriatric Patient Population

- 4.2.3Guideline-Driven Adoption of Multimodal Antiemetic Prophylaxis

- 4.2.4Commercial Launch of Long-Acting Combination Antiemetics

- 4.2.5Advances in Personalized Medicine and Digital Risk-Scoring Tools

- 4.2.6Hospital Cost-Savings From Reduced Post-Anesthesia Care Unit Time

- 4.3Market Restraints

- 4.3.1Shift Toward Minimally Invasive and Non-Surgical Alternatives

- 4.3.2Safety Concerns Over 5-HT3 And NK-1 Receptor Antagonists

- 4.3.3Intense Generic Competition Driving Price Erosion

- 4.3.4Pharmacogenomic Variability Limiting Predictable Drug Efficacy

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat Of New Entrants

- 4.5.2Bargaining Power Of Buyers / Consumers

- 4.5.3Bargaining Power Of Suppliers

- 4.5.4Threat Of Substitute Products

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Treatment Type

- 5.1.15-HT3 Receptor Antagonists

- 5.1.2NK-1 Receptor Antagonists

- 5.1.3Corticosteroids

- 5.1.4Dopamine Antagonists

- 5.1.5Anticholinergics

- 5.1.6Non-Pharmacologic Interventions

- 5.1.7Other Treatment Types

- 5.2By Distribution Channel

- 5.2.1Hospital Pharmacies

- 5.2.2Retail Pharmacies & Drug Stores

- 5.2.3Online Pharmacies

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Ambulatory Surgical Centres

- 5.3.3Specialty Clinics

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Heron Therapeutics Inc.

- 6.3.2Helsinn Healthcare SA

- 6.3.3Novartis AG / Sandoz

- 6.3.4Teva Pharmaceutical Industries Ltd.

- 6.3.5Merck & Co. Inc.

- 6.3.6Kyowa Kirin Co. Ltd.

- 6.3.7Daiichi Sankyo Co. Ltd. (American Regent)

- 6.3.8Eisai Co. Ltd.

- 6.3.9Eagle Pharmaceuticals Inc.

- 6.3.10Fortovia Therapeutics (Galt)

- 6.3.11Pfizer Inc.

- 6.3.12Dr Reddy's Laboratories Ltd.

- 6.3.13Sun Pharmaceutical Industries Ltd.

- 6.3.14Cipla Ltd.

- 6.3.15Hikma Pharmaceuticals PLC

- 6.3.16Fresenius Kabi AG

- 6.3.17Aurobindo Pharma Ltd.

- 6.3.18Accord Healthcare Ltd.

- 6.3.19Johnson & Johnson (Janssen)

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Postoperative Nausea And Vomiting Market Report Scope

As per the scope of the report, postoperative nausea and vomiting (PONV) refer to the common occurrence of nausea, vomiting, or retching after anesthesia or within 24 hours of surgery.

The postoperative nausea and vomiting market is segmented by treatment type, distribution channel, and geography. By treatment type, the market is segmented into serotonin antagonists, steroids, NK-1 receptor antagonists, non-pharmacologic treatment, and others. The others include dopamine antagonists, anticholinergics, and others. By distribution channel, the market is segmented into hospital pharmacies, online pharmacies, retail pharmacies & drug stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market sizing and forecasts have been done on the basis of value (USD).