Cold Pain Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cold Pain Therapy Market Analysis by Mordor Intelligence

The cold pain therapy market size was valued at USD 2.65 billion in 2025 and estimated to grow from USD 2.77 billion in 2026 to reach USD 3.43 billion by 2031, at a CAGR of 4.36% during the forecast period (2026-2031). Demand pivots from simple ice packs to connected, temperature-controlled wearables that deliver consistent therapy guided by artificial intelligence [1]Zehan Liu, "Stretchable multifunctional wearable system for real-time and on-demand thermotherapy of arthritis," Microsystems and Nanoengineering, nature.com. Rising musculoskeletal disease prevalence—osteoarthritis alone affected 607 million people worldwide in 2021—intensifies the need for drug-free pain relief. At the same time, patients increasingly favor self-care solutions that lower healthcare costs and offer immediate relief. Integration of real-time temperature monitoring into flexible wearables further differentiates premium devices, while regulatory clarity from the FDA on thermal evaluation standards lowers market entry barriers for innovators.

Key Report Takeaways

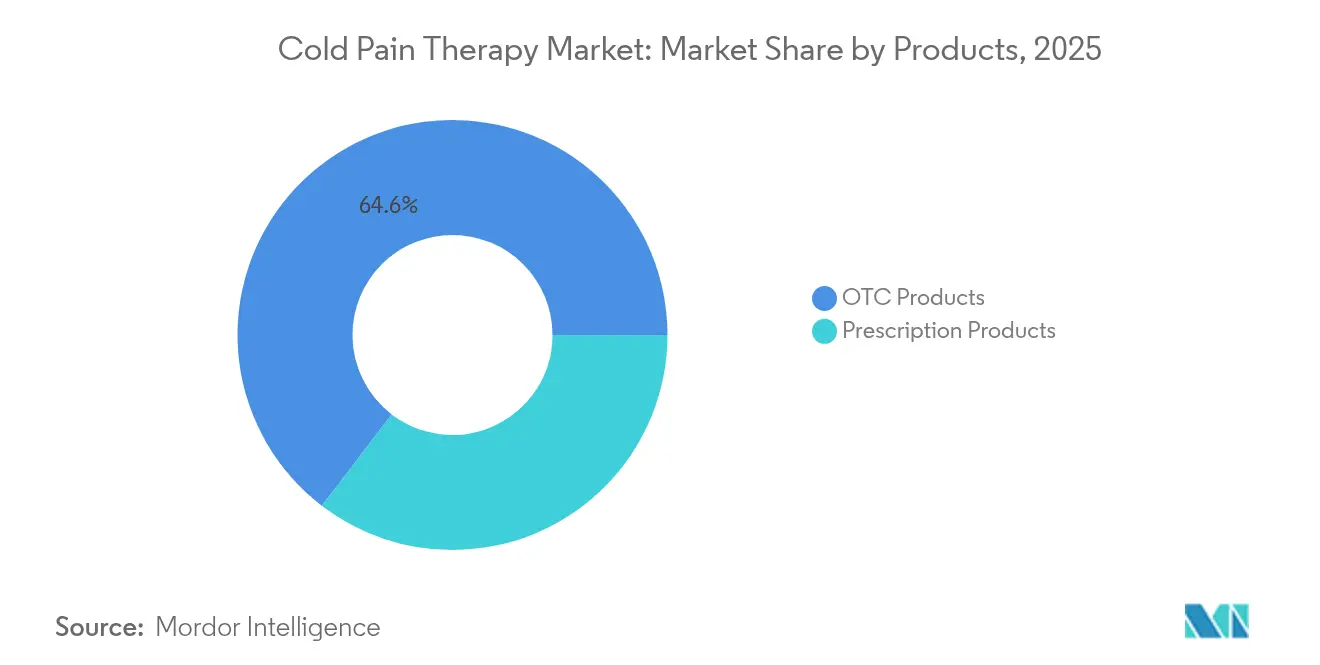

- By product type: OTC products held 64.60% of cold pain therapy market share in 2025, whereas prescription devices are set to expand at a 5.05% CAGR to 2031.

- By application: Sports medicine commanded 37.95% revenue share in 2025; neuropathic & chronic pain applications are projected to grow at 5.12% CAGR through 2031.

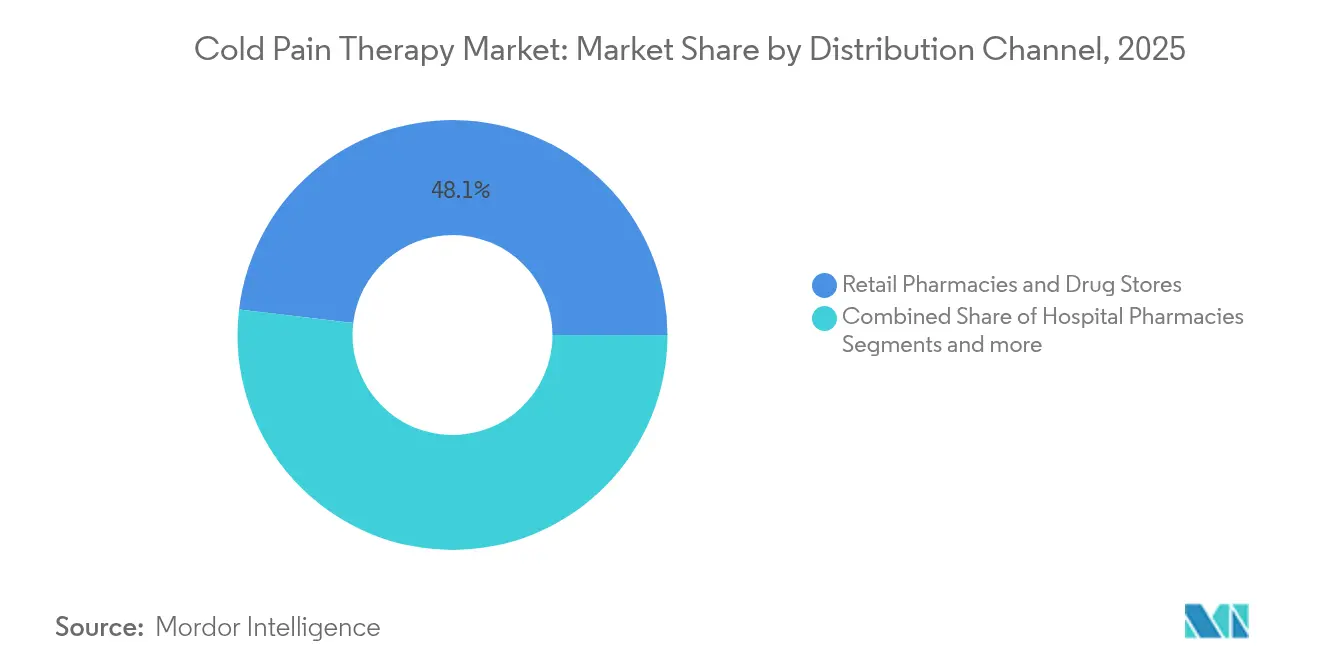

- By distribution channel: Retail pharmacies accounted for 48.10% of the cold pain therapy market size in 2025, while e-commerce shows the fastest channel CAGR of 5.18% to 2031.

- By age group: Adults segment accounted for 53.55% market share in 2025, while the geriatric segment is expanding at 5.22% CAGR amid ageing demographics that heighten demand for easy-to-use pain-relief devices.

- By geography: North America led with a 39.95% share in 2025; Asia-Pacific is the fastest-growing region, advancing at a 5.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cold Pain Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of sports & road-traffic injuries | +0.8% | North America & Europe | Short term (≤ 2 years) |

| Growing prevalence of arthritis & other MSDs in ageing population | +1.2% | Global | Long term (≥ 4 years) |

| Rapid consumer shift toward self-care & OTC topical analgesics | +0.9% | North America, Europe, expanding APAC | Medium term (2-4 years) |

| Increase in post-surgical procedures requiring cold therapy | +0.7% | High-income regions worldwide | Medium term (2-4 years) |

| IoT-enabled smart wearables offering real-time temperature control | +0.6% | North America & Europe | Long term (≥ 4 years) |

| Next-gen TRPM8-modulating cooling compounds in R&D pipeline | +0.4% | United States & European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Sports & Road-Traffic Injuries

Professional leagues and amateur athletes now treat acute injuries within six hours using portable cryotherapy units because evidence shows that recovery outcomes improve when tissue temperature is lowered quickly. Sports bodies mandate on-site cold therapy, shifting budgets from disposable ice toward programmable devices that maintain therapeutic ranges without refills [2]Sarah K. Wesley, “Rapid Cryotherapy in Acute Sports Injury,” bjsm.bmj.com . Urban traffic congestion also raises collision rates, widening the market for first-response kits fitted with compact cooling wraps. As a result, the cold pain therapy market increasingly serves emergency care and sporting venues with quick-deployment solutions.

Growing Prevalence of Arthritis & Other MSDs in Ageing Population

During the last 25 years, osteoarthritis cases among working-age adults more than doubled, intensifying the economic burden of chronic pain. Elderly users gravitate toward wrap-around devices that are lightweight, easy to fasten and capable of maintaining set temperatures for extended periods [3]Michael Langworthy, "Knee osteoarthritis: disease burden, available treatments, and emerging options," Sage Journals, journals.sagepub.com. Emerging cryoneurolysis techniques offer knee-specific relief by cooling targeted sensory nerves, enabling mobility gains without systemic analgesics. Manufacturers position geriatric-friendly designs with intuitive controls to tap this long-term growth driver.

Rapid Consumer Shift Toward Self-Care & OTC Topical Analgesics

Average US household spending on OTC products reached USD 645 in 2024, up 8% from the prior year. The CDC lists non-prescription topical treatments among recommended first-line pain options, normalizing self-management practices. Consumers extend these habits to cooling gels, patches and miniature motorized cuffs purchased online. Subscription models that replenish gel packs or send software updates keep customers within a brand ecosystem, reinforcing loyalty and recurring revenue across the cold pain therapy industry.

Increase in Post-Surgical Procedures Requiring Cold Therapy

Elective orthopedic volumes rebounded in 2024, and clinical protocols now standardize cryotherapy after major joint replacements. A 31-trial meta-analysis showed significant pain score reductions and improved range of motion when motorized cold therapy was used after total knee arthroplasty. Hospitals specify devices with programmable temperature settings to replace ice bags that deliver inconsistent cooling. Vendors that bundle training and data-tracking dashboards secure multi-year supply contracts, further deepening the cold pain therapy market’s penetration in perioperative care pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited or absent third-party reimbursement | -1.1% | United States & other private-payer markets | Medium term (2-4 years) |

| Low patient & clinician awareness in emerging economies | -0.6% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Dermatologic adverse events triggering tighter formulation rules | -0.3% | Global | Short term (≤ 2 years) |

| Substitution threat from laser, contrast & heat-alternation therapies | -0.4% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited or Absent Third-Party Reimbursement

US Medicare classifies most cooling devices as “not medically necessary,” shifting full cost to patients despite favorable trial data. Insurers cite inconsistent outcomes to justify denials, while some regional payers rely on orthopedic society statements that favor simpler ice over motorized systems. Hospitals therefore limit purchases, slowing high-value device adoption in the cold pain therapy market.

Low Patient & Clinician Awareness in Emerging Economies

Training gaps in rural clinics curb adoption of advanced cold therapy devices despite rising musculoskeletal disease incidence. Curriculum shortages in medical schools leave many providers unfamiliar with standardized cryotherapy protocols, while language barriers impede user-manual comprehension. Vendors must invest in localized education programs to unlock these high-population markets and grow global cold pain therapy market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: OTC Dominance Meets Prescription Innovation

OTC solutions controlled 64.60% of cold pain therapy market share in 2025 as consumers favored accessible sprays, gels and patches available without medical oversight. Creams and gels continue to anchor pharmacy aisles, while controlled-release patches win customers who prefer longer relief intervals. The cold pain therapy market size for OTC formats is projected to grow steadily but at a slower pace than technologically sophisticated prescription devices.

Prescription devices, led by motorized circulation systems, exhibit a 5.05% CAGR to 2031. Hospitals adopt these platforms to standardize postoperative protocols that demand precise temperature windows and automated shut-offs. Software-enabled pumps transmit usage logs to electronic health records, helping providers validate adherence for quality metrics. As a result, the cold pain therapy market increasingly bifurcates: mass-market OTC goods dominate volume, whereas high-margin prescription units capture institutional budgets seeking outcome-based solutions.

By Application: Sports Medicine Leadership Faces Chronic Pain Challenge

Sports medicine retained 37.95% of cold pain therapy market revenue in 2025, driven by mandatory cryotherapy access across professional leagues and expanding amateur participation. Portable sleeve systems that fit knees, ankles and shoulders now travel with teams, replacing ice coolers on the sidelines. However, neuropathic & chronic pain cases expand at a 5.12% CAGR as TRPM8 research validates cold modulation for complex pain mechanisms.

Post-operative therapy remains critical, with hospital protocols requiring cold application after replacement surgeries to curb swelling. In trauma & orthopedics, aging populations boost fracture and joint repair volumes, keeping demand high for durable wraps and non-motorized packs. These shifts spread adoption across acute injury management and long-duration chronic care, broadening the cold pain therapy market footprint beyond athletics.

By Distribution Channel: E-Commerce Disrupts Traditional Pharmacy Dominance

Retail pharmacies captured 48.10% of the cold pain therapy market size in 2025 by combining product availability with pharmacist guidance. Yet e-commerce demonstrates a 5.18% CAGR as direct-to-consumer brands bypass intermediaries and leverage targeted social-media outreach. Subscription replenishment of gel inserts keeps customers engaged and raises customer lifetime value, intensifying digital channel competition in the cold pain therapy market.

Hospital pharmacies procure prescription-grade units under group purchasing contracts, but budget ceilings slow upgrade cycles. Sports & specialty stores focus on athletic wraps and braces tailored to high-performance users. Omnichannel strategies that blend online convenience with in-store fittings emerge as essential for sustaining brand presence, given fragmented consumer shopping preferences across the cold pain therapy industry.

By Age Group: Geriatric Surge Drives Market Evolution

Adults represented 53.55% of cold pain therapy market revenue in 2025, reflecting active lifestyles and disposable income for premium gadgets. Nonetheless, geriatric demand is outpacing as degenerative joint disease prevalence rises, leading to a 5.22% CAGR through 2031. Manufacturers redesign interfaces with larger buttons, voice prompts and simplified strapping mechanisms to serve dexterity-limited users.

Pediatric applications, while niche, benefit from heightened parental caution over systemic pain medications. Compact, color-coded wraps appeal to coaches and school nurses managing sports injuries on site. Together, varied age-group needs compel diversified product portfolios that span price points and functionality levels, sustaining multi-segment growth across the cold pain therapy market.

Geography Analysis

North America held 39.95% of the cold pain therapy market in 2025, supported by high healthcare spending and FDA guidance that eliminates regulatory ambiguity for device submissions. The United States leads prescription device adoption, though reimbursement gaps temper hospital uptake. Canada’s single-payer model provides steadier funding for medically necessary cooling systems, while Mexico’s growing middle class boosts OTC category sales.

Europe follows with mature distribution networks and harmonized Medical Device Regulation that eases cross-border sales. Germany and the United Kingdom spearhead adoption of connected wraps that integrate with digital monitoring platforms, reflecting strong telehealth penetration. Southern European markets expand sports medicine segments due to professional football and cycling culture, while the European Medicines Agency’s digital health initiatives encourage further IoT integration.

Asia-Pacific is the fastest-growing region with a 5.30% CAGR to 2031, driven by ageing populations in China and India and high technology acceptance in Japan and South Korea. Local investors back start-ups producing affordable smart cuffs marketed through regional e-commerce giants. Australia acts as a clinical-trial hub for next-generation cooling wearables, leveraging its sports-science expertise. However, limited reimbursement frameworks in parts of Southeast Asia keep adoption below potential, signaling long-run upside for companies that localize education and financing solutions in the cold pain therapy market.

Competitive Landscape

The cold pain therapy market remains moderately fragmented. Legacy orthopedic supplier Enovis leverages long-standing surgeon networks to protect share in hospital channels. In March 2024 the FDA finalized evaluation protocols for thermal devices, leveling the playing field for emergent rivals that bring connected wrap solutions to market.

Start-ups differentiate through IoT-enabled wearables that sync with smartphone apps and deliver adaptive cooling cycles. Subscription models bundle replacement sleeves and data-analytics dashboards, generating annuity revenue in contrast to one-time pack sales. Geriatric-oriented designs with simplified controls and safety lockouts open an underserved niche, intensifying competition across demographics.

Strategic M&A accelerates capability expansion: in 2024 Haemonetics bought Attune Medical to add the ensoETM temperature regulation device, broadening its procedural portfolio. Similar bolt-on deals are expected as incumbents seek specialized technologies that shorten R&D timelines and defend share against connected-device entrants in the cold pain therapy market.

Cold Pain Therapy Industry Leaders

-

Breg Inc.

-

Brownmed Inc.

-

Össur hf

-

Cardinal Health Inc.

-

Enovis Corporation (DJO Global Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mercy Health added iovera, a targeted cold therapy system for joint pain relief, to its clinical offerings.

- January 2025: KT Health released the Ice Therapy Pack designed for broad muscle groups such as the back and shoulders.

- March 2024: The FDA issued final guidance on evaluating thermal effects in medical devices, providing standardized premarket testing protocols.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cold pain therapy market as all over-the-counter creams, gels, sprays, wraps, cold packs, and prescription cryotherapy devices that apply controlled cold to relieve acute or chronic musculoskeletal pain, sports injuries, or post-operative discomfort.

Scope Exclusions: Whole-body cryosaunas and non-medical wellness services are not counted to keep the healthcare focus intact.

Segmentation Overview

-

By Product

-

OTC Products

- Creams

- Gels

- Patches

- Sprays & Roll-ons

- Wraps & Pack Systems

- Other OTC Products

-

Prescription Products

- Motorized Devices

- Non-motorized Devices

-

OTC Products

-

By Application

- Sports Medicine

- Post-operative Therapies

- Trauma & Orthopaedics

- Neuropathic & Chronic Pain

- Other Applications

-

By Distribution Channel

- Retail Pharmacies & Drug Stores

- Hospital Pharmacies

- E-commerce

- Sports & Specialty Stores

-

By Age Group

- Adults

- Geriatric

- Pediatric

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- Middle East

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with orthopedic surgeons in Germany, sports physicians in the United States, rehabilitation therapists across India, and product managers from cooling-device makers in Japan to confirm usage rates, price corridors, and channel shifts.

Desk Research

Our analysts begin with tier-1 public datasets such as Centers for Disease Control and Prevention injury files, Eurostat hospital discharge statistics, UN Comtrade export codes for elastic therapeutic supports, and peer-reviewed studies in the Journal of Sports Medicine. Company revenue splits are refined through D & B Hoovers, while emerging patent clusters are checked with Questel.

We complement these foundations with investor filings, national sports-federation participation surveys, customs shipment records, and association newsletters, creating the first demand and supply baselines. The sources named above are illustrative; many additional references informed data collection and sense checking.

Market-Sizing & Forecasting

Mordor's model first applies a top-down build that reconstructs demand from annual sprain and strain cases, elective orthopedic surgeries, and therapy penetration levels. It then cross-checks totals with selective bottom-up estimates drawn from retailer sell-through samples and supplier roll-ups. Key variables include sports injury incidence, geriatric population share, average OTC unit price, e-commerce share of pain care spending, and reimbursement uptake trends. Forecasts employ multivariate regression anchored to aging index and organized retail growth, with scenario analysis to gauge price elasticity shifts.

Data Validation & Update Cycle

Before any figure is released, analysts run variance screens against historical series, peer metrics, and fresh interview feedback. They escalate anomalies for senior review and refresh the workbook each year, issuing interim updates if major regulatory or technology shocks occur.

Why Mordor's Cold Pain Therapy Baseline Warrants Confidence

Decision makers often notice that published market values differ. The gap typically depends on scope choices, pricing assumptions, and refresh cadence.

Mordor sets a clearly clinical scope, converts revenues at constant 2024 dollars, and refreshes every twelve months. Other publishers may mix wellness devices, apply list prices, or roll forward older estimates, which introduces divergence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.65 Billion (2025) | Mordor Intelligence | |

| USD 2.56 Billion (2025) | Global Consultancy A | Omits prescription cryotherapy devices and updates biennially |

| USD 2.33 Billion (2025) | Industry Association B | Relies on manufacturer self-reported shipments without retail mark-ups |

| USD 2.10 Billion (2025) | Regional Consultancy C | Uses conservative OTC price points and excludes e-commerce sales |

Together, these comparisons show that Mordor's disciplined scope definition, dual validation model, and quick refresh cadence deliver a balanced baseline that clients can trace back to transparent inputs and repeatable steps.

Key Questions Answered in the Report

What is the current size of the cold pain therapy market?

The cold pain therapy market size is USD 2.77 billion in 2026 and is projected to reach USD 3.43 billion by 2031.

Which product category leads the cold pain therapy market?

OTC products hold the lead with 64.60% market share as of 2025.

Which application is growing fastest in the cold pain therapy market?

Neuropathic and chronic pain applications are expanding at a 5.12% CAGR through 2031.

Why is Asia-Pacific considered the fastest-growing region?

Ageing populations, healthcare infrastructure investment and rapid e-commerce adoption drive a 5.30% regional CAGR.

How are IoT wearables influencing the cold pain therapy industry?

Connected wraps with real-time temperature control enhance treatment precision and provide usage data for clinicians, opening premium price tiers.

What are the main barriers to wider adoption of cold pain therapy devices?

Limited third-party reimbursement and low awareness in emerging economies remain the largest obstacles.

Page last updated on: