Cystic Fibrosis Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

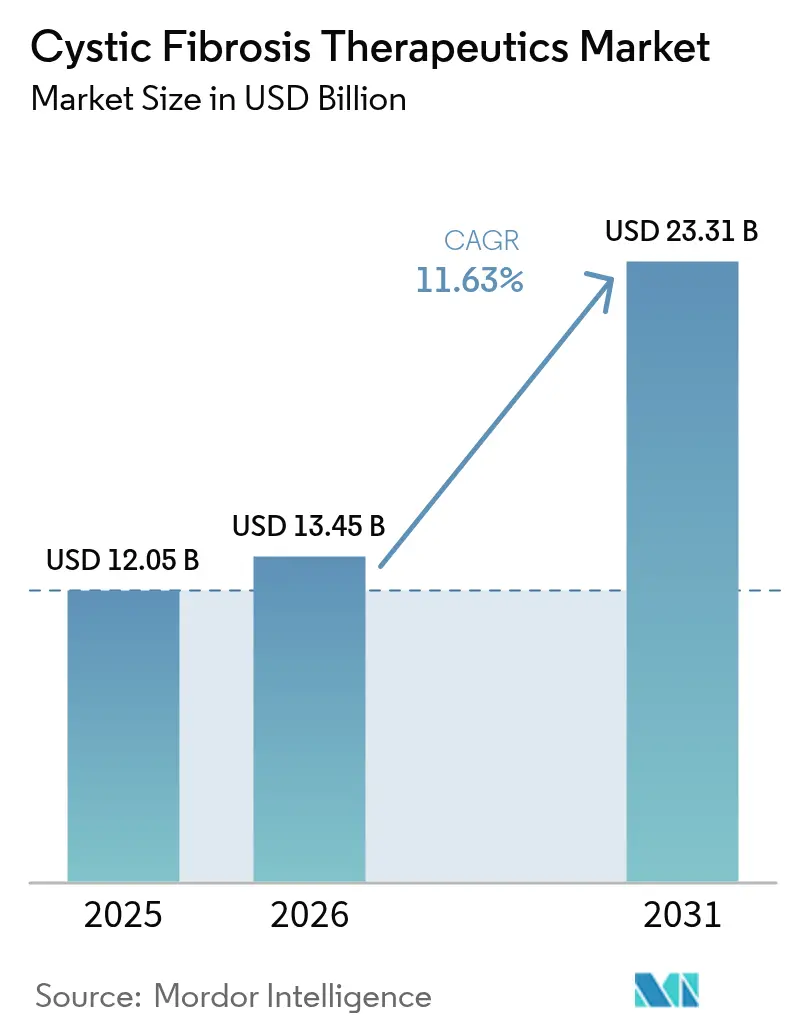

| Market Size (2026) | USD 13.45 Billion |

| Market Size (2031) | USD 23.31 Billion |

| Growth Rate (2026 - 2031) | 11.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cystic Fibrosis Therapeutics Market Analysis by Mordor Intelligence

The Cystic Fibrosis Therapeutics Market size is expected to grow from USD 12.05 billion in 2025 to USD 13.45 billion in 2026 and is forecast to reach USD 23.31 billion by 2031 at 11.63% CAGR over 2026-2031.

Growth is anchored in the rapid uptake of CFTR modulators, which generated 65.37% of 2024 revenue and continue to reshape standards of care through broader mutation coverage and once-daily formulations. Rising diagnosis rates, particularly in ethnically diverse populations, enlarge the treated patient pool and reinforce demand for precision therapies. Robust capital inflows into rare-disease pipelines accelerate both small-molecule and gene-based innovations, while government orphan-drug incentives extend commercial exclusivity and support premium pricing models. Despite strong momentum, access disparities persist; only 12% of the global CF population currently receives triple-combination regimens, highlighting a substantial untapped opportunity, especially in middle-income regions.

Key Report Takeaways

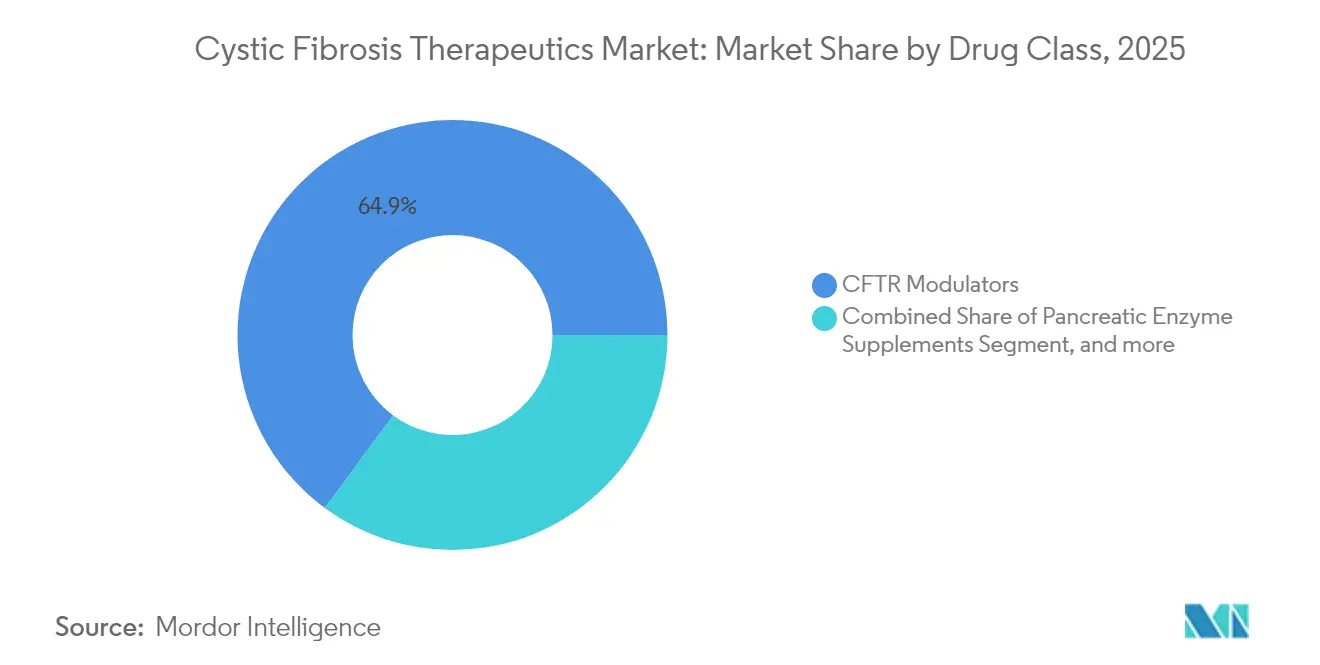

- By drug class, CFTR modulators held 64.88% of cystic fibrosis therapeutics market share in 2025, while gene-delivery candidates are projected to post a 14.92% CAGR through 2031.

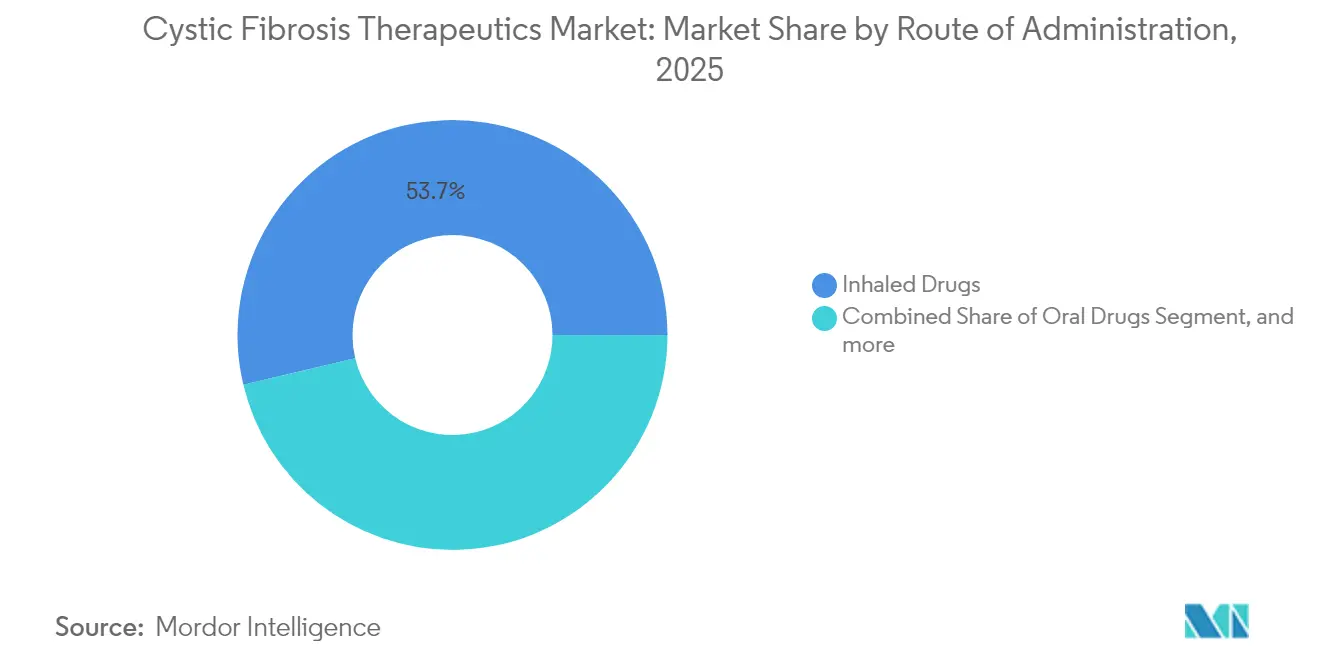

- By route of administration, inhaled drugs commanded 53.72% share of the cystic fibrosis therapeutics market size in 2025; gene delivery is forecast to expand at the highest 14.92% CAGR to 2031.

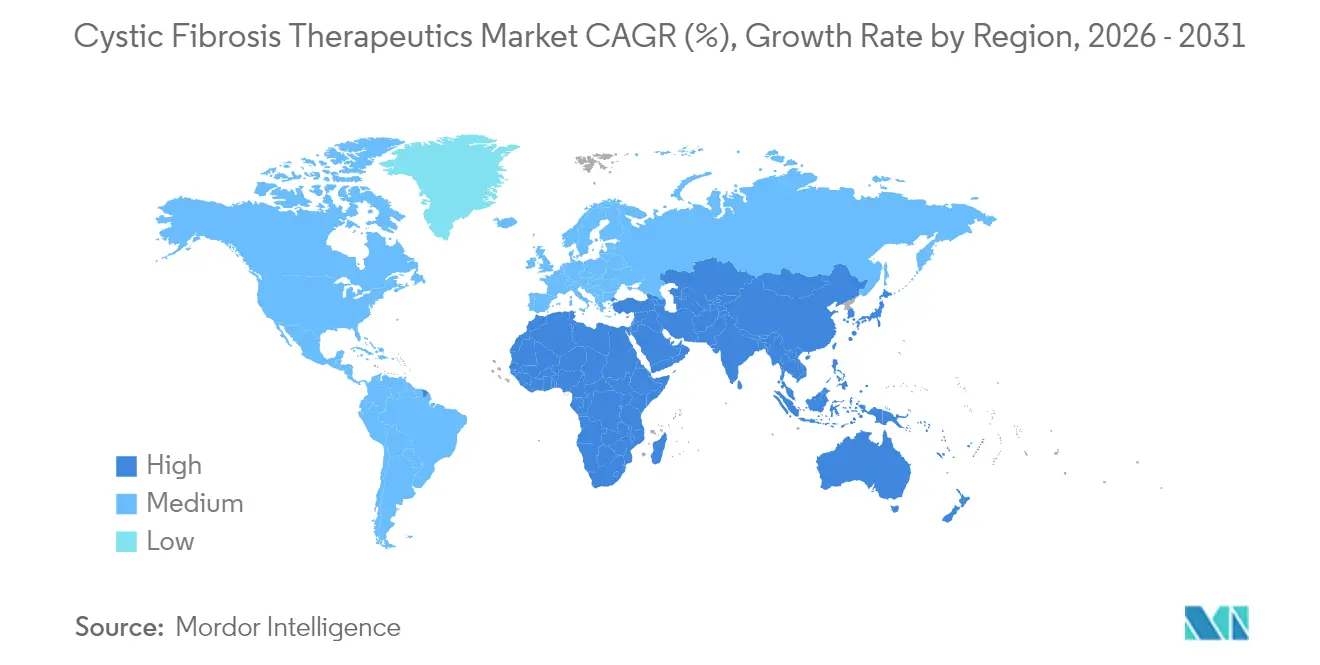

- By geography, North America led with 43.21% revenue share in 2025, whereas Asia-Pacific is set to grow at 16.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cystic Fibrosis Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence & earlier diagnosis | +2.1% | Global; strongest in North America & Europe | Medium term (2-4 years) |

| Expanding approvals of CFTR modulators | +3.2% | North America & EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Government orphan-drug incentives | +1.8% | Global; notably US & EU | Long term (≥ 4 years) |

| Capital inflow into rare-disease R&D | +2.4% | Global; concentrated in biotech hubs | Medium term (2-4 years) |

| Expansion of newborn genomic screening | +1.5% | North America & Europe leading, Asia-Pacific following | Long term (≥ 4 years) |

| mRNA / gene-editing platforms enter pipeline | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence & Earlier Diagnosis

Uniform newborn screening protocols adopted in 2024 elevated detection across under-represented ethnic groups, reversing historic under-diagnosis in Black, Hispanic, Asian, and multiracial infants.[1]John Pohl, “Equitable Newborn Screening for Cystic Fibrosis,” washington.edu California’s statewide sequencing program confirmed the value of mutation-inclusive panels, prompting similar initiatives in Texas and New York. In India, academic registries now estimate 3,600 CF births per year, quadrupling prior counts and underscoring unmet therapeutic need. Earlier identification enables CFTR modulators to be prescribed before irreversible lung damage sets in, improving long-term outcomes and supporting premium pricing. These trends expand the cystic fibrosis therapeutics market by converting latent prevalence into active treatment demand.

Expanding Approvals of CFTR Modulators

Regulators moved decisively in 2024–2025. The US FDA cleared once-daily ALYFTREK for patients aged 6 and older with 31 additional mutations, while TRIKAFTA secured a label extension covering 94 non-F508del variants.[2]Vertex Pharmaceuticals, “2024 Annual Report,” vrtx.com Europe approved KALYDECO for infants from 1 month of age, setting a new precedent for early intervention. These actions extend therapeutic reach to previously untreated genotypes, fuelling double-digit adoption rates and reinforcing Vertex’s first-mover advantage. Broader eligibility also improves payer economics by reducing hospitalizations and transplant rates, sustaining growth for the cystic fibrosis therapeutics market.

Government Orphan-Drug Incentives

More than half of FDA novel approvals in 2024 carried orphan status, continuing a decade-long policy trend that offers 7–12 years of market exclusivity, fee waivers, and tax credits. Japan streamlined multi-regional trial requirements, allowing CF therapies to bypass local phase I studies and reach patients faster. Fast-track designations for inhaled lentiviral and mRNA platforms shorten development cycles and de-risk first-in-class mechanisms. These incentives anchor investor confidence, ensuring sustained funding for high-cost gene and cell therapies that target the remaining refractory population segment within the cystic fibrosis therapeutics market.

Capital Inflow into Rare-Disease R&D

Venture and strategic financing broke records in 2024. Sionna Therapeutics raised USD 182 million to advance CFTR correctors aimed at NBD1 stabilization. The Cystic Fibrosis Foundation committed USD 2.3 million toward breath diagnostics that detect Pseudomonas aeruginosa colonization earlier than sputum culture methods. ReCode Therapeutics attracted fresh capital for inhaled mRNA delivery, partnering with Intellia to accelerate gene-editing programs recodetx.com. This influx fuels a robust innovation pipeline and heightens competitive pressure within the cystic fibrosis therapeutics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost burden | -1.9% | Global; most acute in low- and middle-income countries | Short term (≤ 2 years) |

| Patent expiries & generic erosion | -1.2% | North America & Europe | Medium term (2-4 years) |

| Adherence burden of multi-drug regimens | -0.8% | Global | Long term (≥ 4 years) |

| Cold-chain gaps for inhaled biologics | -0.6% | LMICs, Sub-Saharan Africa, parts of Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost Burden

Annual list prices for triple-combination modulators range from USD 326,000 to USD 370,000, exceeding average household income in most middle-income nations. Only 12% of the estimated 162,400 global patients access these drugs, with coverage highly concentrated in wealthy jurisdictions. South African litigation seeks compulsory licensing, while EU investigations show poorer member states paying proportionally higher per-patient costs.[3]Sarah Drury, “Global Burden of Untreated Cystic Fibrosis: A Call to Action,” frontiersin.org These affordability gaps suppress uptake and slow volume growth for the cystic fibrosis therapeutics market.

Patent Expiries & Generic Erosion

Zenpep patents expire in February 2028, paving the way for generic pancreatic enzyme supplements that serve 80–90% of patients. Supply shortages during 2024 highlighted fragile manufacturing networks and signalled potential price declines post-patent cliff. Older CFTR modulators face similar timelines, prompting innovators to fast-track next-generation assets. While complex biologics will deter immediate biosimilar entry, looming erosion pressures incentivize differentiation strategies across the cystic fibrosis therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: CFTR Modulators Consolidate Leadership

CFTR modulators held 64.88% of overall sales in 2025 and outpacing every other treatment class. The cystic fibrosis therapeutics market size for CFTR modulators is projected to surge at 12.48% CAGR through 2031, buoyed by ALYFTREK’s once-daily regimen and expanded mutation coverage. Oral bioavailability, favourable safety, and clear lung-function gains underpin clinician preference, although high costs continue to challenge payers outside Group A economies.

Pancreatic enzyme supplements remain indispensable to 80–90% of patients, but recurrent shortages and an impending generic wave temper revenue prospects. Mucolytics, anchored by dornase alfa, supply symptomatic relief across 65 countries yet face declining usage as modulators improve mucus clearance. Antibiotics such as inhaled tobramycin and aztreonam retain a role in managing chronic Pseudomonas infections, though altered airway microbiomes under modulator therapy may reduce dosing frequency. Anti-inflammatory agents and bronchodilators round out polypharmacy regimens but contribute modest share to the cystic fibrosis therapeutics market.

By Route of Administration: Gene Delivery Accelerates

Inhaled formulations captured 53.72% revenue in 2025, reinforcing the value of direct pulmonary deposition for antibiotics, mucolytics, and emerging biologics. Oral agents, led by CFTR modulators and enzyme supplements, dominate daily pill burden yet benefit from patient convenience. Intravenous antibiotics remain vital for acute exacerbations but show volume decline as modulators curtail hospitalization rates.

Gene delivery stands out as the fastest-growing route at 14.92% CAGR, driven by phase 1/2 programs deploying mRNA or viral vectors via aerosol. If initial efficacy translates to durable FEV₁ improvement, this segment could re-define the cystic fibrosis therapeutics market size for advanced modalities. Manufacturing scalability, immunogenicity management, and payer acceptance will determine the speed of commercial adoption.

Geography Analysis

North America commanded 43.21% of the cystic fibrosis therapeutics market revenue in 2025, supported by comprehensive insurance schemes, specialized care centres, and aggressive patient-advocacy funding. US adoption of triple combinations surpasses 85% of eligible patients, and Cystic Fibrosis Foundation grants continue to seed diagnostic and therapeutic innovations. Canada reported a 62% drop in hospital admissions and a 20% reduction in emergency visits after TRIKAFTA reimbursement, confirming real-world cost offsets. Mexico shows incremental uptake through private channels, though public reimbursement remains limited.

Europe represents a mature yet fragmented landscape. The United Kingdom secured a long-term pricing deal that unlocks broad access to TRIKAFTA, SYMKEVI, and ORKAMBI, ending years of negotiation stalemate. Germany, France, and the Nordics exhibit near-universal modulator coverage, whereas Lithuania and Poland contend with budget constraints that delay roll-out. The European Commission’s approval of KALYDECO for infants as young as 1 month sets a new baseline for early treatment, though implementation varies by healthcare funding model.

Asia-Pacific is the fastest-growing territory with a 16.55% CAGR outlook, reflecting both rising diagnosis rates and policy reforms. China’s national registry reveals genotype diversity that may require tailored drug development strategies. Japan’s relaxed trial regulations expedite foreign entry, and South Korea added CF therapies to its rare-disease reimbursement list in 2025. Australia resolved cost-effectiveness debates and listed TRIKAFTA on PBS, while India expands neonatal screening as prevalence estimates climb. Cold-chain and fiscal obstacles persist across many ASEAN states, but targeted aid programs signal gradual improvement, enlarging the cystic fibrosis therapeutics market.

Regulatory Landscape

Regulatory Landscape sits around the US FDA CDER and EMA CHMP as the primary gating bodies for CFTR modulators. Labeling decisions are increasingly tied to CFTR variant responsiveness, with evidence that specific mutations yield functional CFTR protein. In December 2024, the US FDA approved Vertex's ALYFTREK for patients aged 6 years and older with at least one F508del or other responsive mutation, and expanded TRIKAFTA's indication to include additional non-F508del mutations, reinforcing a mutation-driven precedent for label expansions.

Regulatory actions in 2025-2026 broadened eligibility in major markets. In February 2025, EMA CHMP adopted positive opinions supporting expanded use of KAFTRIO and KALYDECO across additional patient groups (including younger ages with eligible mutation classes). In April 2026, the US FDA approved label extensions for ALYFTREK and TRIKAFTA that expand eligibility to patients with any CFTR variant that produces CFTR protein, enlarging the treated population within established regulatory frameworks. EMA continued lifecycle oversight with updates such as the June 2026 EPAR update for ORKAMBI.

Competitive Landscape

Vertex Pharmaceuticals generated USD 11.02 billion in CF product sales during 2024, treating more than 75,000 patients worldwide and cementing its leadership within the cystic fibrosis therapeutics market. Its portfolio of four approved modulators plus freshly launched ALYFTREK provides multi-mutation coverage and an upgrade cycle narrative. Sionna Therapeutics, fortified by USD 182 million in Series C funding, is advancing NBD1 stabilizers meant to combine with existing correctors and potentially leapfrog triple cocktails.

Gene-therapy entrants bring disruptive potential. Boehringer Ingelheim and the UK CF Gene Therapy Consortium commenced the LENTICLAIR-1 trial of inhaled BI 3720931, targeting pan-mutation correction via a lentiviral vector. 4D Molecular Therapeutics and ReCode Therapeutics pursue AAV and LNP delivery, respectively, each eyeing the 10-15% of patients excluded from current modulators. Vertex and Moderna’s temporary VX-522 pause underscores technical complexity but illustrates a commitment to mutation-agnostic cures.

Strategic focus has widened to adjunct technologies. The Cystic Fibrosis Foundation funded Owlstone Medical’s breath test for Pseudomonas detection, adding diagnostic layers to treatment algorithms. Manufacturers pursue once-daily or inhaled small-molecule regimens to cut adherence burden, while pipeline assets for CF-related liver disease and diabetes hint at portfolio diversification. Patent cliffs loom for enzyme supplements and first-generation modulators, but sophisticated biologic manufacturing may shield incumbents from immediate biosimilar threats in the cystic fibrosis therapeutics market.

Cystic Fibrosis Therapeutics Industry Leaders

AbbVie Inc.

Gilead Sciences Inc.

Vertex Pharmaceuticals Inc.

Alaxia SAS

Mylan NV (Viatris)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Broader CFTR-modulator eligibility and earlier treatment windows create access and uptake opportunities for branded modulators and care pathways. A concrete anchor is that in April 2026 the US FDA expanded ALYFTREK and TRIKAFTA labels to include patients with any CFTR variant that results in CFTR protein production, effectively extending modulator eligibility to about 95% of people with CF in the United States. This mutation-inclusive approach, alongside expanding newborn screening, widens detection and supports demand for testing, genetic counseling, and earlier initiation protocols at CF care centers.

The remaining non-responsive segment outside expanded modulator coverage keeps attention on mutation-agnostic approaches, including inhaled gene or mRNA delivery. Vertex initiated global regulatory submissions for ALYFTREK in children aged 2 to 5, signaling a lifecycle expansion strategy aimed at younger patients and expanded labeling. Affordability and reimbursement remain defining areas, with national listing processes such as Canada’s public listing shaping how expanded labels translate into treated volumes across geographies.

Recent Industry Developments

- July 2026: Vertex signed a Letter of Intent with the pan-Canadian Pharmaceutical Alliance (pCPA) for a public listing pathway for ALYFTREK, following positive recommendations from Canada’s Drug Agency and INESSS. The step advances national reimbursement discussions that influence real-world access and volume conversion beyond private pay channels. It also improves Vertex's ability to standardize pricing and coverage terms across provinces for its next-generation CFTR modulator.

- June 2026: Vertex initiated global regulatory submissions for ALYFTREK in children aged 2 to 5. This expands regulatory engagement and supports lifecycle expansion by opening a pathway for younger patients. Payer discussions and care-center workflows will adjust as submissions progress.

- July 2024: AbbVie entered a license agreement transferring exclusive worldwide development and commercialization rights for three clinical-stage CF assets (galicaftor/ABBV-2222, navocaftor/ABBV-3067, and ABBV-2851) to Sionna Therapeutics. The transaction consolidated multiple CFTR modulator candidates under a CF-focused developer with dedicated capital formation and portfolio strategy around combination regimens. It also reshaped competitive dynamics by moving late-preclinical and clinical optionality away from a diversified pharma pipeline into a specialist platform.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues generated from medicines used to manage cystic fibrosis, including disease-modifying therapies and supportive drug treatments, across hospital and retail channels, and measured at ex-manufacturer values in USD.

Scope exclusions: We exclude diagnostics, medical devices (such as nebulizers), and non-drug care services, even when they are used in CF management.

Segmentation Overview

- By Drug Class

- Pancreatic Enzyme Supplements

- Mucolytics

- Bronchodilators

- Antibiotics

- Anti-inflammatory Agents

- CFTR Modulators

- By Route of Administration

- Inhaled Drugs

- Oral Drugs

- Intravenous Therapies

- Gene Delivery

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the treated CF population and the standard of care, and then aligning that to what is approved, reimbursed, and actually used in major countries. We rely on public sources such as the Cystic Fibrosis Foundation Patient Registry, the European Cystic Fibrosis Society registry, the US FDA drug labels and approval announcements, and the EMA public assessment reports to confirm indications, dosing, and launch timing.

To ground volumes and affordability, we also review sources such as OECD health statistics, World Bank macro indicators, and published articles in peer-reviewed respiratory and clinical journals for prevalence and treatment practice signals. Company filings, investor decks, and credible press coverage are used to validate brand-level dynamics, pipeline timelines, and geographic exposure, and selective paid subscriptions for company financials and patent databases help cross-check revenue linkage and innovation activity. These desk research sources are illustrative and not exhaustive, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from structured interviews and short surveys with clinicians, hospital pharmacists, payor-side experts, and distribution and market-access professionals, since each group sees different parts of uptake and persistence. For a global view, we cover demand signals across North America, Europe, and Asia-Pacific so that registry trends, treatment mix shifts, and price corridors can be checked and then tightened into the final model assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | APAC: 47% |

| Mid tier: 54% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 19% | Managers: 53% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool approach where CF prevalence is translated into an addressable treated cohort by country, and then adjusted for diagnosis rate, eligibility for disease-modifying therapy, and real-world persistence. Once that pool is built, value is estimated by applying therapy mix and typical annual treatment cost bands, followed by adjustments for tendering, reimbursement restrictions, and time since launch.

To keep totals realistic, results are corroborated using selective bottom-up approximations, such as sampled brand revenue directionality from public financial disclosures, channel checks on formulary access, and ASP progression sanity checks using published pricing references. The model also tracks market fingerprints like CFTR modulator penetration, shifts in pediatric versus adult treatment share, expected label expansions, and the pace of uptake after major guideline and reimbursement changes. Forecasting uses scenario analysis supported by expert views on pipeline readouts and switching behavior, and gaps in country detail are handled through proxying with comparable markets using similar registry coverage and payor structure.

Data Validation & Update Cycle

Outputs are checked against independent signals such as registry-reported treated population trends, reported sales momentum by therapy category, and visible reimbursement events, and then the biggest variances are investigated before numbers are finalized. When an assumption drives an outsized change, analysts re-check it with an alternate data point or re-contact a relevant expert to avoid reliance on a single source.

Before sign-off, the model goes through stepwise internal review, including logic checks on cohort sizing, mix, and pricing, followed by region-level consistency checks so no geography is overstated by a single input. Reports are refreshed annually, and interim updates are made when material events occur, such as a major approval, safety restriction, or a meaningful pricing and access shift. Right before delivery, we run a final pass to ensure the latest public events are reflected in the numbers and narrative.

Mordor Intelligence's Cystic Fibrosis Therapeutics Market Size Compared Against Other Published Estimates

Published market values for CF therapeutics can look far apart, even when everyone is discussing the same disease area, because the market is small in patient count but very sensitive to what is counted and how prices are treated. Differences usually come from therapy scope, the year picked as the base, and how fast uptake is assumed for high-value disease-modifying drugs.

Some estimates broaden scope by folding in adjacent respiratory drugs and non-CF supportive categories that are not specific to cystic fibrosis treatment lines. In Mordor Intelligence's model, only cystic fibrosis drug classes are counted, and totals are tied back to treated cohort sizing, therapy eligibility, and mix shifts that were rechecked through registry signals and physician feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.45 B (2026) | |

| Industry Publisher A | USD 10.30 B (2024) | Uses an earlier base year and a shorter forecast window, and its value can sit lower if treated-cohort expansion and persistence for disease-modifying therapies are modeled more conservatively at launch-to-maturity. |

| Industry Publisher B | USD 12.90 B (2024) | Reports a 2024 point estimate that can move upward when broader drug groupings or higher assumed annual therapy costs are applied, with less transparency on how eligibility and switching are handled across countries. |

Across the table, the spread is mainly explained by base-year choice and what gets bundled into the definition of CF therapeutics, followed by different assumptions on uptake and annual cost progression. By keeping the sizing steps traceable to treated patients, eligibility, and therapy mix, we can explain each number change and update it cleanly when approvals, access, or registry trends shift.

Key Questions Answered in the Report

What is the current size of the cystic fibrosis therapeutics market?

The cystic fibrosis therapeutics market size stood at USD 13.45 billion in 2026 and is projected to reach USD 23.31 billion by 2031.

Which drug class dominates sales?

CFTR modulators captured 64.88% of total revenue in 2025, making them the leading class.

Which region is growing fastest?

Asia-Pacific is forecast to expand at a 16.55% CAGR through 2031, driven by improved diagnostics and regulatory reforms.

What share does North America hold?

North America accounted for 43.21% of cystic fibrosis therapeutics market revenue in 2025.

When will generics impact pancreatic enzyme therapies?

Zenpep patents expire in February 2028, setting the stage for generic entry and potential price reductions.

What innovation could disrupt current treatment paradigms?

Inhaled gene-delivery platforms such as lentiviral and mRNA vectors aim to provide mutation-agnostic correction, potentially offering functional cures for patients unresponsive to modulators.

Page last updated on: