Neuralgia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 3.62 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

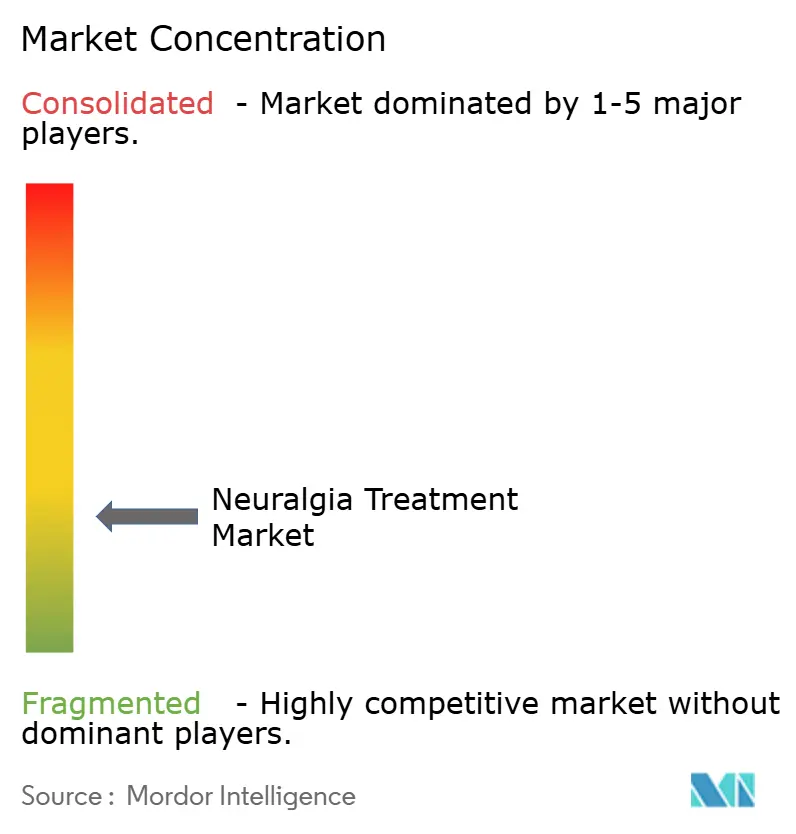

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neuralgia Treatment Market Analysis by Mordor Intelligence

Neuralgia treatment market size in 2026 is estimated at USD 2.67 billion, growing from 2025 value of USD 2.51 billion with 2031 projections showing USD 3.62 billion, growing at 6.29% CAGR over 2026-2031. Advancing neuromodulation technologies, an expanding pool of patients with neuropathic pain, and a global push for non-opioid pain solutions underpin this growth. The January 2025 FDA clearance of Suzetrigine, the first highly selective NaV1.8 inhibitor for pain, validates novel molecular targets and accelerates industry investment. Device innovation has amplified demand for closed-loop spinal cord stimulators that personalize therapy in real time, while demographic shifts—especially aging populations—are swelling postherpetic neuralgia incidence. At the same time, the neuralgia treatment industry is navigating reimbursement complexity and raw-material shortages, both of which underscore the need for diversified supply chains and value-based coverage frameworks.

Key Report Takeaways

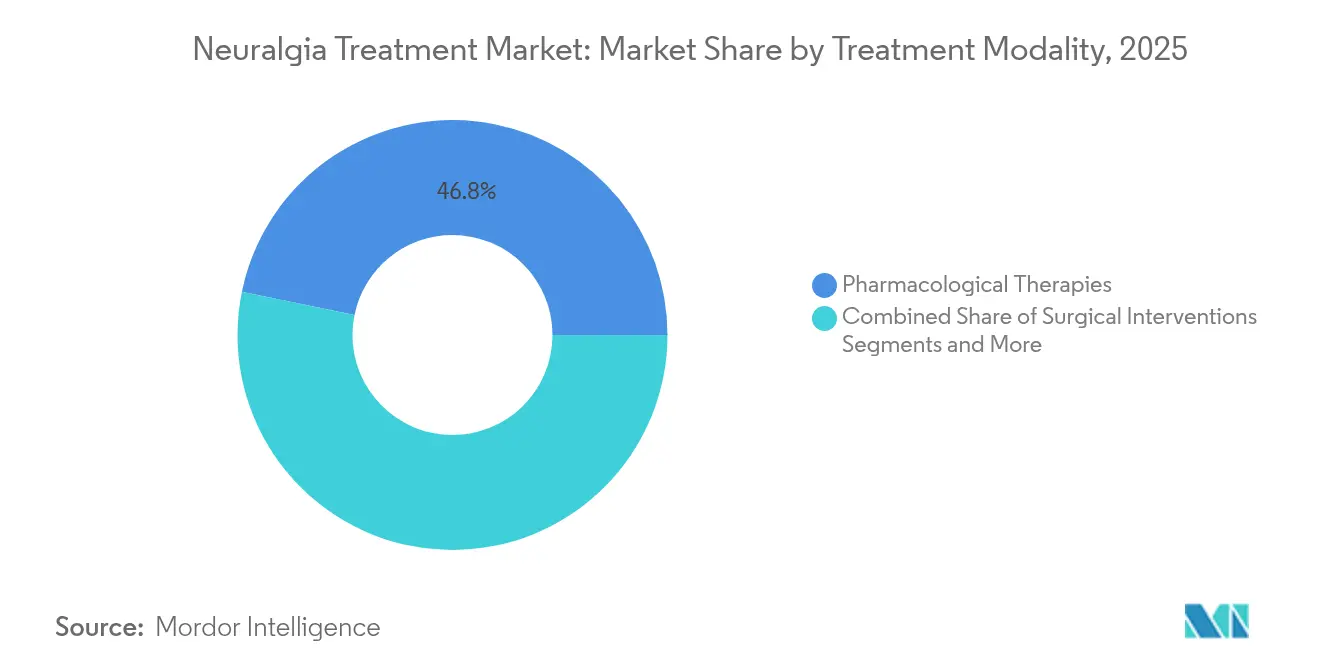

- By treatment modality, pharmacological therapies led with 46.78% of the neuralgia treatment market share in 2025; device-based neuromodulation is projected to expand at a 10.55% CAGR to 2031.

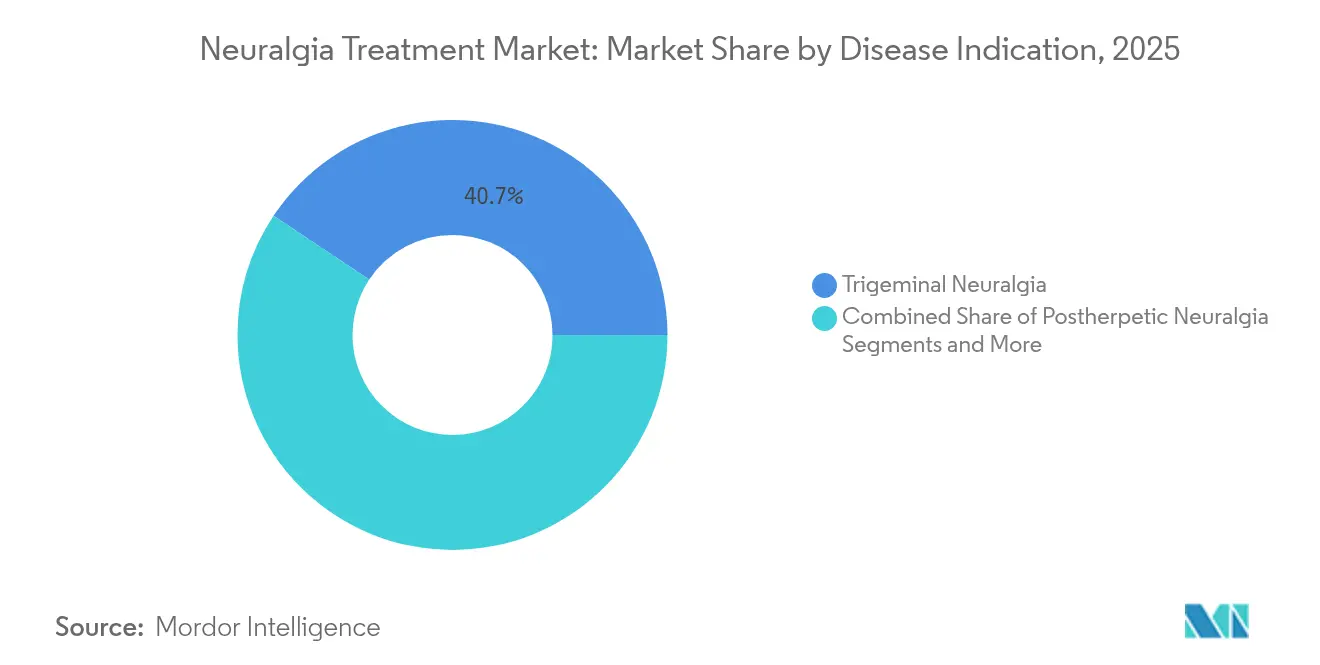

- By disease indication, trigeminal neuralgia captured 40.65% of the neuralgia treatment market size in 2025, whereas postherpetic neuralgia is set to grow at 9.18% CAGR through 2031.

- By end user, hospitals and clinics held a 55.62% share of the neuralgia treatment market in 2025; ambulatory surgery centers recorded the fastest trajectory at an 8.41% CAGR.

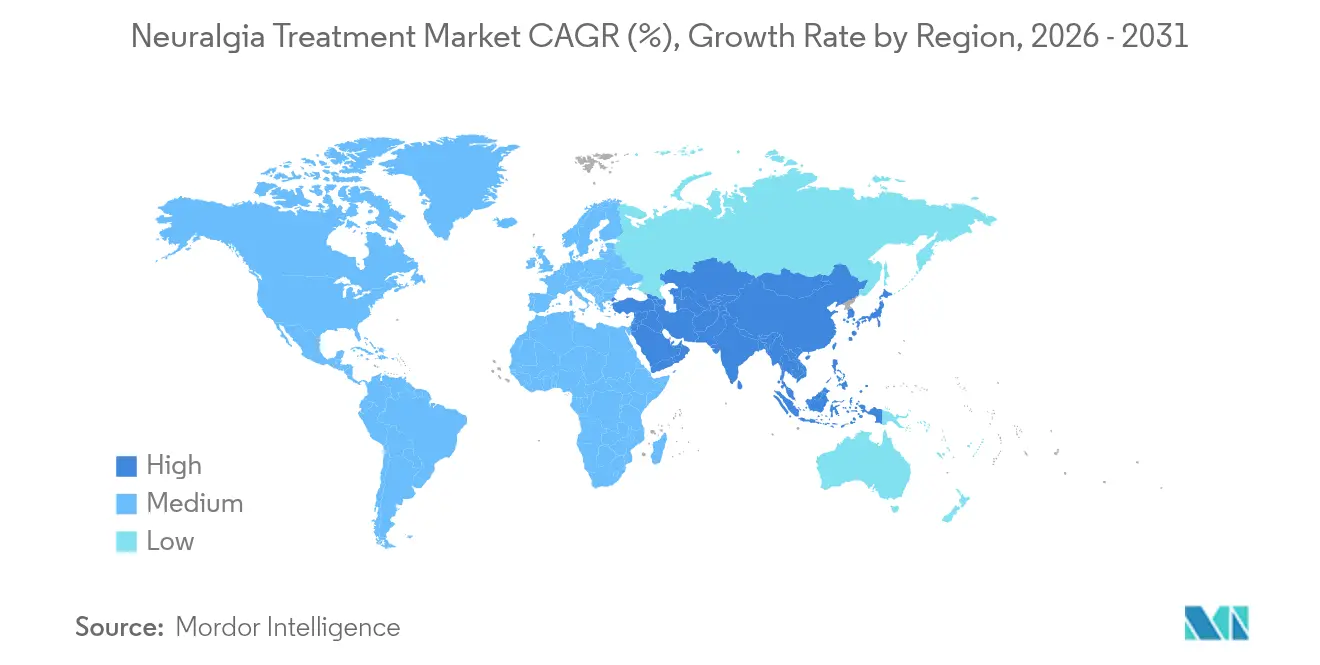

- By geography, north america commanded 36.12% revenue share in 2025, yet Asia-Pacific is poised for the highest regional CAGR at 8.93% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neuralgia Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Neuropathic & Neuralgic Pain Disorders | + 1.8% | Global, with higher concentration in North America & Europe | Long term (≥ 4 years) |

| Rapid Innovation In Neuromodulation & Neurostimulation Devices | + 2.1% | North America & EU leading, APAC adoption accelerating | Medium term (2-4 years) |

| Growing R&D Funding And Late-Stage Drug Pipeline Momentum | + 1.4% | Global, concentrated in major pharmaceutical hubs | Medium term (2-4 years) |

| Expansion Of Ambulatory Surgery & Day-Care Microsurgery Centers | + 0.9% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| AI-Driven Personalised Stimulation Algorithms Enhance Outcomes | + 1.2% | North America & EU initially, global expansion | Long term (≥ 4 years) |

| Cross-Border Medical Tourism For Low-Cost Radiosurgery In Asia | + 0.7% | APAC core, attracting patients from North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neuropathic and Neuralgic Pain Disorders

Trigeminal neuralgia alone affects about 150,000 Americans each year.[1]Naum Shaparin, “Peripheral Neuromodulation for the Treatment of Refractory Trigeminal Neuralgia,” onlinelibrary.wiley.com Higher life expectancy, rising diabetes incidence, and broader diagnostic awareness are pushing overall caseloads upward. The resulting quality-of-life impact propels healthcare systems to earmark new funds, which sustains elevated demand for both first-line anticonvulsants and newer device-based therapies. Economic losses from diminished productivity further justify continued investment in innovation.

Rapid Innovation in Neuromodulation and Neurostimulation Devices

April 2024 saw FDA clearance of Medtronic’s Inceptiv closed-loop spinal cord stimulator with real-time biosignal monitoring. Artificial-intelligence algorithms now fine-tune pulse output to patient physiology, enhancing pain relief and lowering side-effect incidence. Comparable approvals—such as Boston Scientific’s WaveWriter Alpha line for diabetic peripheral neuropathy—have widened eligible patient pools. Together, these advances position neuromodulation as a mainstream alternative to systemic pharmacotherapy.

Growing R&D Funding and Late-Stage Drug Pipeline Momentum

Vertex’s commercial launch of Suzetrigine illustrates the revenue potential of sodium-channel blockade, spurring additional pipeline assets across metabotropic glutamate, TRPV1, and CGRP pathways. Basimglurant (NOE-101) advanced into Phase 2/3 enrollment of 200 trigeminal neuralgia patients in 2025. Funding inflows have diversified into biologics and toxin-based injectables, signalling an era of mechanism-specific drug design.

Expansion of Ambulatory Surgery and Day-Care Microsurgery Centers

Payers are favoring outpatient leads for cost containment, accelerating migration of spinal cord stimulator implants to ambulatory settings. Shorter stays and bundled payments reduce per-procedure outlays, allowing centers to compete with tertiary hospitals on both price and convenience. Miniaturized hardware and imaging-guided techniques support this transition while maintaining safety profiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost Of Advanced Pharmacological & Device-Based Care | -1.6% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Adverse Effects & Safety Concerns Of Long-Term Anticonvulsant Use | -0.8% | Global, with regulatory scrutiny in North America & EU | Medium term (2-4 years) |

| Reimbursement Uncertainty For Novel Neuromodulation Techniques | -1.1% | North America & EU primarily, expanding globally | Short term (≤ 2 years) |

| API Supply Bottlenecks For Key Drugs Such As Carbamazepine | -0.5% | Global, with regional variations in severity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Advanced Pharmacological and Device-Based Care

A full spinal cord stimulation system ranges from USD 20,000 to USD 50,000, excluding long-term clinic visits. Suzetrigine lists at USD 15.50 per 50 mg tablet, a premium over generics. Premium pricing restricts uptake among under-insured patients and challenges cost-effectiveness assessments, particularly in emerging economies where out-of-pocket spending dominates.

Reimbursement Uncertainty for Novel Neuromodulation Techniques

Coverage parity has yet to converge across major US insurers, as seen in Cigna’s 2024 denial of peripheral nerve stimulation contrasted with Humana’s subsequent approval.[2]North American Neuromodulation Society, “NANS Leads Response Objecting to Cigna’s Depiction of PNS,” neuromodulation.org Providers face prolonged prior-authorization cycles, which defer therapy initiation and dilute the real-world impact of otherwise proven technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Device Innovation Challenges Traditional Dominance

Pharmacological therapies represented the largest slice of the neuralgia treatment market in 2025 with a 46.78% share, anchored by broad generic availability of carbamazepine and gabapentinoids. Device-based neuromodulation, however, is slated for the highest 10.55% CAGR, buoyed by AI-enabled stimulators and minimally invasive lead placements. This rapid rise reflects patient preference for drug-sparing solutions and the influx of positive long-term outcome data. The neuralgia treatment market size for neuromodulation could eclipse surgical interventions by 2030 if reimbursement aligns with clinical evidence. Botulinum toxin, once niche, is establishing itself as a mid-course alternative where systemic drugs fail, adding diversity to physician armamentaria.

The neuralgia treatment industry now pursues hybrid regimens: drug loading for immediate relief, followed by neurostimulation for maintenance. Cross-border medical travel for gamma-knife radiosurgery costs USD 3,500–7,000 in India—roughly one-tenth of Western tariffs—supporting procedure volumes in Asia-Pacific hospital chains. Such price differentials drive outbound demand, yet domestic adoption in high-income countries remains contingent on payer policy shifts toward bundled payments.

By Disease Indication: Trigeminal Dominance Faces Postherpetic Challenge

Trigeminal neuralgia controlled 40.65% of 2025 revenues, reinforcing its status as the archetype of neuralgic pain conditions. Intensive research pipelines, dedicated centers of excellence, and public awareness campaigns sustain its top billing. Postherpetic neuralgia is gaining momentum at a 9.18% CAGR, fueled by aging demographics and vaccination gaps that maintain herpes zoster prevalence. The neuralgia treatment market size attached to postherpetic cases could reach a value nearly double 2024 levels by 2030 if current diagnostic accuracy persists.

Evidence is mounting for botulinum toxin injections and temporary spinal cord stimulation with lidocaine patches in elderly cohorts, yielding pain-score reductions and sleep improvements.Glossopharyngeal, occipital, and sciatic neuralgias remain smaller niches yet benefit from overarching advances in imaging, biomarker stratification, and AI-based pain assessment tools that refine protocol selection.

By End User: Hospital Dominance Faces Ambulatory Disruption

Hospitals and clinics held 55.62% revenue share in 2025, backed by multidisciplinary teams and capital-intensive operating rooms. Yet ambulatory surgery centers are sprinting ahead at 8.41% CAGR, leveraging leaner staffing models and rapid-turnover theatres. These centers are increasingly preferred for outpatient stimulator trials and implantations, where same-day discharge meets patient expectations.

Pain-management specialty centers fill an integrative niche, coupling pharmacotherapy with cognitive-behavioral interventions. Tele-pain platforms—now used by 40% of Italian pain clinics—extend follow-up reach and reduce travel burdens. Wearable TENS and percutaneous electrical nerve stimulation devices enhance remote care, opening fresh pathways for home-based neuralgia treatment market adoption.

Geography Analysis

North America retained 36.12% of 2025 global revenues on the strength of robust payer systems, extensive neuromodulation expertise, and accelerated FDA pathways for breakthrough devices. Supply chain vulnerabilities, highlighted by the 2024 carbamazepine shortage, spurred diversification initiatives and validated the need for alternative modalities. Non-opioid stewardship programs create fertile ground for the neuralgia treatment market to integrate AI-driven stimulators and selective sodium-channel inhibitors.

Asia-Pacific is projected for a 8.93% CAGR, driven by expanding health-insurance penetration and inbound medical tourism. Gamma-knife radiosurgery priced at USD 3,500–7,000 attracts patients from North America and Europe, underscoring the region’s cost leadership. Japan faces an estimated chronic-pain economic burden of 2 trillion yen annually, galvanizing government and private sectors to accelerate adoption of device-based pain solutions. Parallel investments in training and manufacturing cement China and South Korea as emerging production hubs.

Europe commands mature reimbursement structures and rigorous health-technology assessment frameworks. CE-marked platforms such as Nevro’s HFX iQ are extending physician toolkits, while telemedicine uptake in pain management continues to rise despite persistent workflow hurdles. Emerging markets in South America, the Middle East, and Africa are bolstering tertiary-care facilities, opening incremental neuralgia treatment market opportunities tied to broader healthcare infrastructure upgrades.

Competitive Landscape

The neuralgia treatment industry remains moderately consolidated. Large pharmaceutical incumbents like Pfizer and GSK leverage scale in distribution, whereas device specialists—Medtronic, Boston Scientific, Abbott—compete on algorithmic sophistication and implant longevity. Globus Medical’s USD 250 million acquisition of Nevro in April 2025 underscores a trend toward vertically integrated pain-care portfolios.

AI differentiation is emerging as the key moat. Medtronic’s Inceptiv integrates live biosignal feedback to recalibrate therapy parameters, a feature not yet matched by many competitors. Biotechnology entrants are exploring gene-silencing and regenerative approaches, aiming to achieve durable neural repair rather than symptomatic relief. Meanwhile, digital-health upstarts offer cloud-based analytics that personalize dosing schedules and stimulation patterns, potentially disrupting conventional clinic-based follow-ups.

Neuralgia Treatment Industry Leaders

Pfizer Inc.

GSK

Abbott Laboratories

Boston Scientific

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Globus Medical closed its USD 250 million purchase of Nevro, adding the HFX spinal cord stimulation franchise.

- April 2025: NeuroOne filed a 510(k) for the OneRF Ablation System targeting trigeminal neuralgia facial pain.

- January 2025: Vertex Pharmaceuticals secured FDA approval for Suzetrigine (JOURNAVX) at USD 15.50 per 50 mg tablet, introducing the first selective NaV1.8 inhibitor.

Global Neuralgia Treatment Market Report Scope

Neuralgia is a type of pain caused by an irritated or damaged nerve. Its treatment involves managing and alleviating severe, often shooting pain along the nerve. This may include medications, physical therapy, and, in severe cases, surgical interventions.

The neuralgia treatment market is segmented into treatment type, end-user, and geography. By treatment type, the market is segmented into drug based and surgery based. The drug-based segment is further bifurcated into anticonvulsant medicines, tricyclic antidepressants, opioids, non-steroidal anti-inflammatory drugs and others. The other drug-based treatment includes anti-epileptic drugs, antiseizure medications, etc. The surgery-based segment is further bifurcated into radiofrequency thermal lesioning, stereotactic radiosurgery, microvascular decompression, and others. The other surgery-based segment includes balloon compression, gamma knife radiosurgery, etc. By end-user, the market is segmented into hospital & clinics, ambulatory surgery centers, and other end users. The other end user segment includes specialty clinics, research institutes & labs. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Pharmacological Therapies | Anticonvulsants | Tricyclic Antidepressants |

| Opioids | ||

| NSAIDs | ||

| Botulinum Neurotoxin | ||

| Device-based Neuromodulation | ||

| Surgical Interventions | Radiofrequency Thermal Lesioning | Stereotactic Radiosurgery (Gamma Knife) |

| Microvascular Decompression | ||

| Percutaneous Balloon Compression | ||

| Complementary / Alternative (e.g., TENS, acupuncture) | ||

| Trigeminal Neuralgia |

| Postherpetic Neuralgia |

| Glossopharyngeal Neuralgia |

| Occipital Neuralgia |

| Peripheral / Sciatic Neuralgia |

| Hospitals & Clinics |

| Ambulatory Surgery Centers |

| Pain Management Centers |

| Home-care / Tele-pain Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Pharmacological Therapies | Anticonvulsants | Tricyclic Antidepressants |

| Opioids | |||

| NSAIDs | |||

| Botulinum Neurotoxin | |||

| Device-based Neuromodulation | |||

| Surgical Interventions | Radiofrequency Thermal Lesioning | Stereotactic Radiosurgery (Gamma Knife) | |

| Microvascular Decompression | |||

| Percutaneous Balloon Compression | |||

| Complementary / Alternative (e.g., TENS, acupuncture) | |||

| By Disease Indication | Trigeminal Neuralgia | ||

| Postherpetic Neuralgia | |||

| Glossopharyngeal Neuralgia | |||

| Occipital Neuralgia | |||

| Peripheral / Sciatic Neuralgia | |||

| By End User | Hospitals & Clinics | ||

| Ambulatory Surgery Centers | |||

| Pain Management Centers | |||

| Home-care / Tele-pain Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current neuralgia treatment market size?

The neuralgia treatment market size is valued at USD 2.67 billion in 2026.

How fast is the neuralgia treatment market expected to grow?

The market is projected to register a 6.29% CAGR, reaching USD 3.62 billion by 2031.

Which treatment modality is growing the quickest?

Device-based neuromodulation is expanding at an anticipated 10.55% CAGR through 2031.

Which region shows the highest growth potential?

Asia-Pacific leads with a forecast 8.93% CAGR, aided by medical tourism and wider healthcare access.

What are the main barriers to wider therapy adoption?

High upfront costs for advanced devices and inconsistent reimbursement policies remain key obstacles.

Page last updated on: