Rare Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

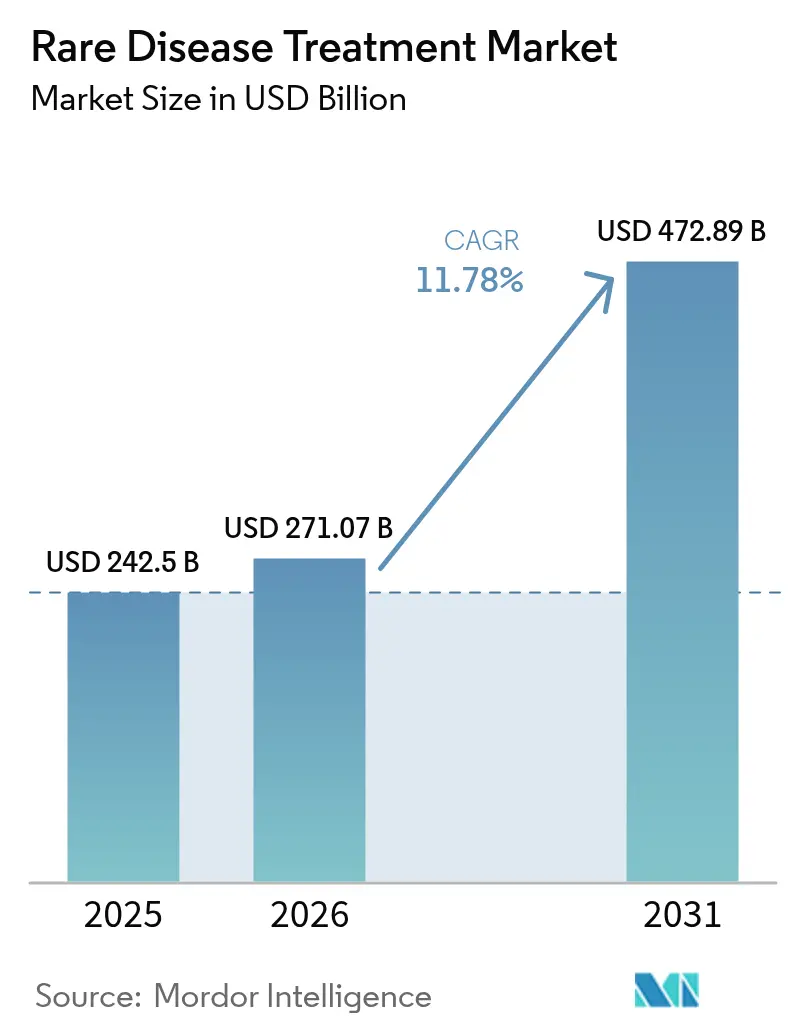

| Market Size (2026) | USD 271.07 Billion |

| Market Size (2031) | USD 472.89 Billion |

| Growth Rate (2026 - 2031) | 11.78% CAGR |

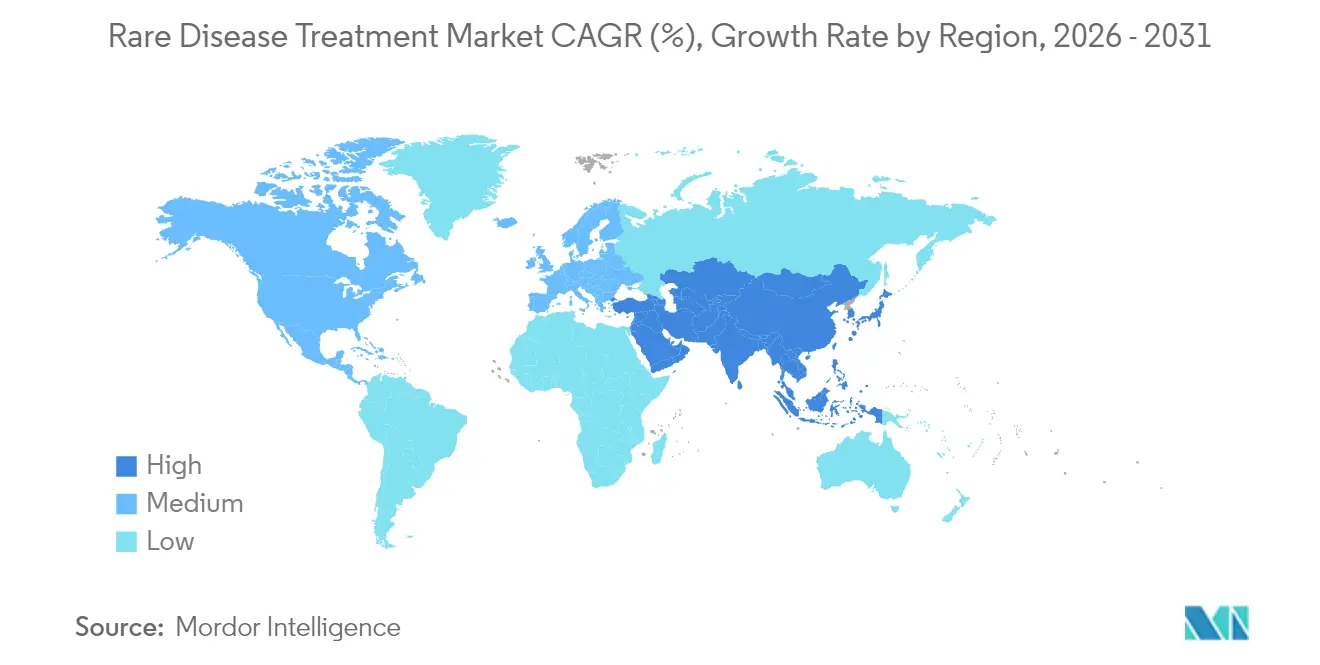

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rare Disease Treatment Market Analysis by Mordor Intelligence

The Rare Disease Treatment market size is expected to grow from USD 242.5 billion in 2025 to USD 271.07 billion in 2026 and is forecast to reach USD 472.89 billion by 2031 at 11.8% CAGR over 2026-2031.

Sustained global incentives, rapid maturation of gene therapy, and payer acceptance of high-value breakthroughs underpin this rise, even though patient pools remain small. Mergers between multinational pharmaceutical groups and specialist innovators intensify competitive positioning, while distributed manufacturing pilots begin easing viral-vector supply constraints. Asia-Pacific’s expanded rare-disease lists and accelerated review pathways complement North American leadership, broadening geographic reach. Neurological gene-therapy launches highlight the shift toward curative modalities, and oral biologic delivery technologies extend convenience for chronic orphan indications. The combined force of regulatory confidence and technological progress secures long-term market momentum.

Key Report Takeaways

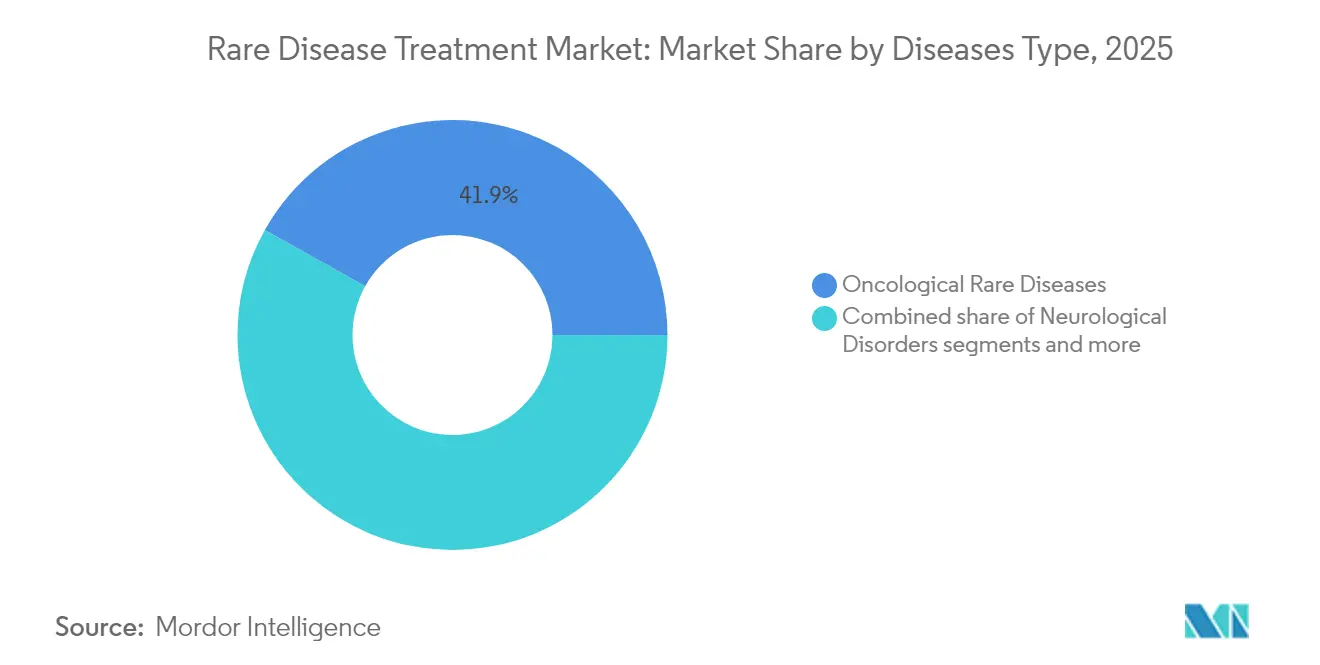

- By disease type, oncological rare diseases held 41.89% of the rare disease treatment market share in 2025; neurological disorders are forecast to expand at a 12.62% CAGR through 2031.

- By therapy type, biologics and monoclonal antibodies accounted for 50.74% of the market size for rare disease treatments in 2025. In contrast, gene and cell therapies are projected to advance at a 12.88% CAGR from 2025 to 2031.

- By route of administration, parenteral products accounted for 60.63% of the revenue in 2025, while oral formulations are expected to grow at a 13.05% CAGR between 2026 and 2031.

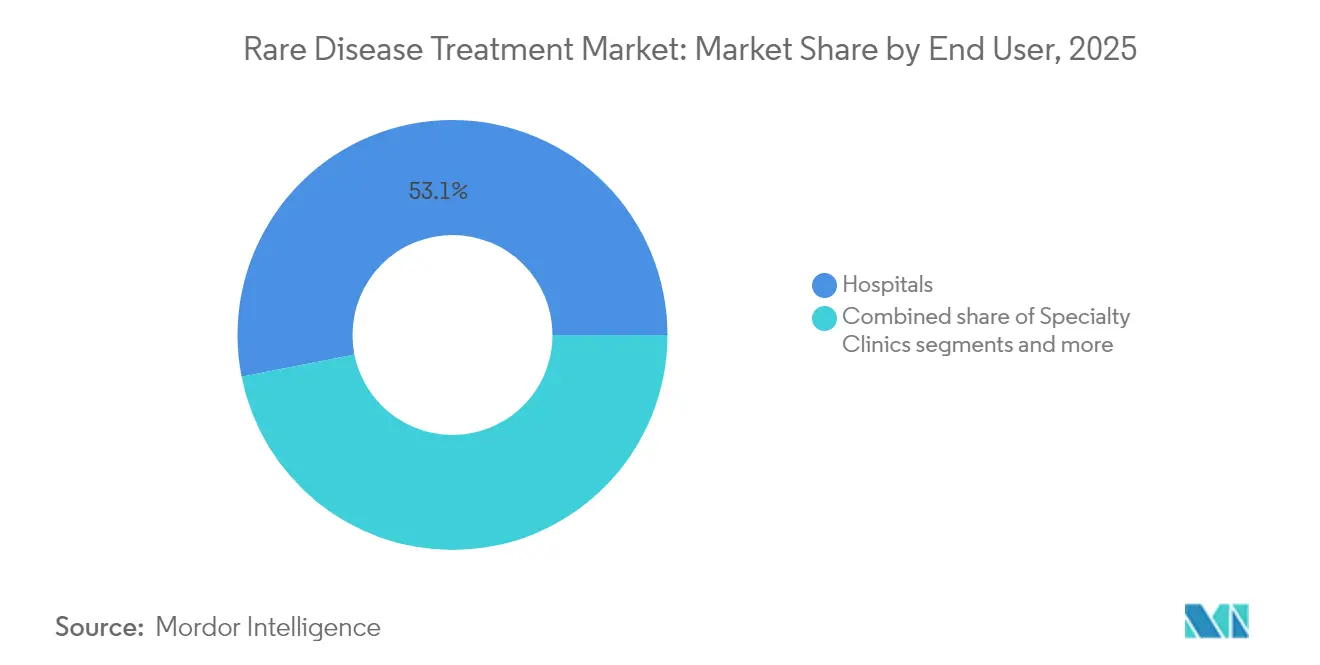

- By end user, hospitals captured 53.11% of the rare disease treatment market size in 2025; home-care settings registered the fastest 13.12% CAGR for the forecast period.

- Regionally, North America controlled 41.86% rare disease treatment market share in 2025, and Asia-Pacific is on course for a 13.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rare Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives & global orphan-drug exclusivity | +2.8% | Global, with strongest impact in North America & EU | Long term (≥ 4 years) |

| Growing FDA/EMA orphan-drug approvals pipeline | +2.1% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Premium pricing & favourable reimbursement frameworks | +1.9% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Rapid advances in gene & cell therapies | +2.4% | Global, with early gains in North America, EU, Japan | Long term (≥ 4 years) |

| Distributed manufacturing for personalised gene therapy | +0.8% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| AI-enabled virtual trials for ultra-rare cohorts | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentives & Global Orphan-Drug Exclusivity

Extended exclusivity and tax credits continue to underwrite innovation within the rare disease treatment market. In the United States, seven-year exclusivity and 25% clinical trial tax credits lower net risk, while the European Union grants 10-year protection that can extend to 12 years for pediatric compliance. Priority Review Vouchers worth roughly USD 150 million add further return potential, as shown by the sale following DAYBUE approval for Rett syndrome. Such incentives help translate basic-science breakthroughs into commercially viable therapies.

Growing FDA/EMA Rare-Disease Approvals Pipeline

Regulators have embraced expedited mechanisms. The FDA cleared multiple gene therapies in 2024, including Kebilidi for aromatic L-amino acid decarboxylase deficiency. The EMA granted 17 orphan designations in 2023, demonstrating a steady flow of candidates. Together with the FDA START pilot and EMA PRIME schemes, these frameworks reduce review uncertainty and accelerate launches, fuelling market expansion.

Premium Pricing & Favourable Reimbursement Frameworks

Annual therapy costs often top USD 500,000, yet payers endorse high-value medicines that demonstrate durable clinical benefit. Lenmeldy for metachromatic leukodystrophy secured reimbursement even at multi-million-dollar pricing. The U.S. Cell and Gene Therapy Access Model fosters instalment and outcome-based contracts that balance budget pressure with patient access.

Rapid Advances in Gene & Cell Therapies

Seven AAV gene therapies have earned approval to date, validating vector platforms and spurring investment in more than 700 active development programmes. CRISPR-based in-vivo editing offers promise for ultra-rare mutations, illustrated by single-patient protocols that underwent FDA review in 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited patient pools for conventional RCTs | -1.4% | Global, most acute in ultra-rare conditions | Medium term (2-4 years) |

| Escalating payor push-back on six-figure price tags | -2.1% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| Viral-vector manufacturing bottlenecks | -1.7% | Global, most severe in North America & EU | Medium term (2-4 years) |

| Post-gene-therapy long-term safety liabilities | -0.9% | Global, regulatory focus in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Patient Pools for Conventional RCTs

Ultra-rare conditions can involve only hundreds of patients worldwide, making standard randomised trials extremely difficult. Adaptive and basket designs help, but more than 50% of rare-disease studies still fail to publish results due to recruitment gaps.

Escalating Payor Push-Back on Six-Figure Price Tags

US legislation such as the Inflation Reduction Act has reduced the likelihood of companies seeking additional indications once exclusivity declines, reflecting concern over future pricing negotiation. The most recent data shows that Medicare Part D specialty drug spending (which includes many orphan drugs) increased by 43% from early 2024 to early 2025, with costs rising from approximately USD 1,200 to USD 1,700 per member per month for non-low income beneficiaries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Oncological Rare Diseases Lead but Neurological Disorders Accelerate

Oncological rare diseases captured 41.89% of the rare disease treatment market share in 2025, underscoring their revenue dominance within the overall rare disease treatment market. This leadership reflects the high clinical unmet need and premium pricing associated with niche cancer therapeutics, particularly hematologic malignancies that benefit from targeted biologics and immunotherapies. The rare disease treatment market size for oncological indications is projected to maintain mid-single-digit growth as additional precision drugs secure approvals and expand addressable sub-cohorts. Neurological disorders, by contrast, are forecast to grow at a 12.62% CAGR through 2031, propelled by gene therapies such as Lenmeldy and Kebilidi that penetrate the blood–brain barrier and deliver potentially curative benefits . Regulatory pilots that shorten review timelines for neurodegenerative indications add further momentum.

Growth outside these two pillars remains steady yet meaningful. Metabolic disorders continue to rely on enzyme replacement and emerging gene-editing modalities that broaden lifetime treatment options. In contrast, immunological disorders absorb advances in monoclonal antibodies and engineered T-cell platforms. Infectious-disease applications, although smaller in value, attract interest for antimicrobial-resistance niches where orphan incentives offset limited volumes. Pipeline analysis shows roughly 18% of phase III assets now target neurological diseases, signaling sustained capital reallocation toward high-growth categories. Overall, disease-type diversification reduces portfolio risk for manufacturers and helps the rare disease treatment market achieve balanced long-term expansion.

By Therapy Type: Biologics Retain Scale, Gene and Cell Therapies Drive Momentum

Biologics and monoclonal antibodies accounted for 50.74% of 2025 revenue, maintaining their position at the center of the rare disease treatment market size, thanks to their proven efficacy and payer familiarity with chronic infusion models. Even so, gene and cell therapies are outpacing every other modality at a 12.88% CAGR, driven by a pipeline exceeding 700 active clinical programmes that target both well-characterised and ultra-rare mutations. Recent approvals across neurologic and hematologic categories validate adeno-associated virus vectors and encourage investment in next-generation capsids with enhanced tissue tropism.

The competitive interplay among modalities is widening. Small-molecule drugs preserve niche relevance for metabolic pathways and allosteric enzyme modulation, offering convenience and lower manufacturing complexity. RNA-based interventions, particularly siRNA agents, continue to face adoption challenges despite broader coverage, because annual treatment costs range from USD 375,000 for first-generation options, such as patisiran (ONPATTRO), to more than USD 1.6 million for newer, highly specialized siRNA therapies. Vutrisiran (Amvuttra), administered quarterly, reduces the administration burden and related healthcare utilization, giving it a potential cost-effectiveness edge over patisiran without compromising clinical benefit. Enzyme-replacement therapies remain central for lysosomal storage diseases; however, long-term switching studies suggest a gradual shift toward single-administration gene transfers. Collectively, these dynamics transform the therapeutic mix and heighten innovation pressure on incumbent biologics franchises within the rare disease treatment market.

By Route of Administration: Parenteral Stronghold Faces Oral and Subcutaneous Push

Parenteral delivery retained 60.63% of 2025 revenue, reflecting the bioavailability needs of biologics, gene therapies, and high-molecular-weight enzymes. Hospital-based infusions dominate the initiation of gene therapy, while subcutaneous formats are gaining popularity for chronic antibody regimens. Nonetheless, oral formulations are projected to expand at a 13.05% CAGR to 2031, driven by permeation enhancers such as SNAC, which enable peptides and small proteins to survive gastrointestinal transit. These innovations provide precise adherence and quality-of-life benefits for long-term treatment courses.

Technology breakthroughs are expanding delivery options even further. Transmucosal routes and implantable depots are under active investigation for ultra-rare metabolic conditions requiring steady pharmacokinetic profiles. Post-marketing preference surveys indicate 82% of immunology and hematology patients would switch from hospital infusions to at-home subcutaneous administration if efficacy and safety were equivalent. As device design improves and stability data mature, parenteral exclusivity is expected to soften, enabling more patient-centric regimens that reinforce uptake across the rare disease treatment market.

By End User: Hospital Leadership Gives Way to Decentralised Care

Hospitals generated 53.11% of the rare disease treatment market revenue in 2025, as complex gene-therapy infusions and first-dose monitoring require specialized infrastructure. Yet home-care settings are forecast to grow at a 13.12% CAGR, supported by payer initiatives that encourage decentralised infusion nursing and digital adherence oversight. Cost studies on enzyme-replacement therapy for lysosomal storage diseases show parity between in-hospital and in-home delivery, eroding economic arguments for centralisation.

Specialty clinics and academic centres preserve a critical role in diagnostics, eligibility confirmation, and adverse-event adjudication, particularly for first-in-class modalities. Telehealth follow-up and remote lab collection further simplify long-term management, aligning with broader post-pandemic trends. Supply-chain providers are developing turnkey home-infusion capabilities to support the increasing demand for subcutaneous formulations. As these service ecosystems scale, patient autonomy rises, and hospitals transition toward high-acuity gene-therapy administration, collectively reshaping utilisation patterns within the rare disease treatment market.

Geography Analysis

North America accounted for 41.86% of rare disease treatment market share in 2025, reflecting the combination of FDA fast-track pathways, wide commercial insurance coverage, and strong academic research networks. Average launch timelines for orphan assets are two to three years shorter than in any other region, giving the United States an enduring first-mover advantage. Canada mirrors this momentum through its Priority Review program, although provincial budget caps delay uniform access by six to nine months. Europe follows closely; the EMA granted 17 new orphan designations in 2023, underscoring a robust centralised review process that cuts duplicative national filings. Nonetheless, disparate reimbursement rules mean Central and Eastern European countries cover fewer than half of approved therapies, creating a two-tier access environment.

Asia-Pacific is poised for the fastest 13.29% CAGR through 2031, driven chiefly by China’s regulatory reforms that expanded the National Rare Diseases List from 121 to 207 conditions. The NMPA CARE scheme compresses review cycles to 130 working days for qualifying drugs, yet only 38% of FDA-cleared orphan therapies later gain Chinese approval, signalling ongoing localisation hurdles. Japan sustains leadership in ultra-rare neuromuscular indications; its 2024 approval of aceneuramic acid for GNE myopathy illustrates the value of targeted subsidy programs.South Korea and Singapore roll out tax credits and clinical-trial infrastructure grants that attract multinational studies, although small domestic populations still limit revenue upside. Collectively, growing diagnostic capacity, newborn screening expansion, and rising household income underpin the long-run contribution of Asia-Pacific to rare disease treatment market size. Latin America, the Middle East, and Africa represent nascent yet strategic frontiers with single-digit current penetration. Brazil’s Health Surveillance Agency grants up to eight years of exclusivity for priority orphan drugs, but reimbursement remains case-by-case, creating unpredictable uptake. Saudi Arabia established a Rare Disease Registry in 2024, setting the stage for future market entry once local pharmacoeconomic guidelines mature.Multilateral organisations are piloting pooled procurement models to ease affordability barriers, though currency volatility and supply-chain gaps continue to restrain growth.

Competitive Landscape

The rare disease treatment market features prominent players like Pfizer, AstraZeneca, Novartis, Bristol-Myers Squibb, and Bayer AG, leading innovation and development. These companies are increasingly focusing on breakthrough therapies and biologics for treating rare genetic disorders, leveraging advanced research capabilities and extensive clinical trial networks. Strategic collaborations with research institutions and smaller biotech firms have become commonplace to accelerate drug development timelines and expand therapeutic portfolios. Companies are also investing heavily in gene therapy platforms and precision medicine approaches while simultaneously working to improve patient access through specialized distribution networks. The industry has seen a marked shift toward patient-centric development strategies, with companies establishing dedicated rare disease units and implementing comprehensive support programs for affected populations. Notably, orphan drug companies are playing a crucial role in this transformation, driving forward the development of orphan medicines to address unmet medical needs.

Rare Disease Treatment Industry Leaders

Amgen Inc.

Biomarin Pharmaceuticals

Bayer AG

Bristol-Myers Squibb Company

AstraZeneca (Alexion Pharmaceuticals Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sanofi announces intent to acquire Blueprint Medicines for USD 9.1 billion, expanding its rare immunology pipeline

- February 2025: Genentech secures FDA approval for Evrysdi tablet, the first tablet for spinal muscular atrophy, broadening at-home dosing options

Global Rare Disease Treatment Market Report Scope

As per the scope of this report, rare diseases are diseases that affect only a small population compared to the general population. Rare diseases are region specific in that a rare disease could be rare in one region while it is common in another. Rare diseases may be chronic or incurable, though many short-term medical conditions are also rare diseases.

The rare disease treatment market is segmented by drug type (biologics and non-biologics), therapeutic area (genetic diseases, neurological diseases, oncology, infectious diseases, cardiovascular diseases, and other therapeutic areas), mode of administration (oral, injection, and other modes of administration) and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values (in USD million) for the above segments.

| Oncological Rare Diseases |

| Neurological Disorders |

| Metabolic Disorders |

| Hematologic Disorders |

| Immunological Disorders |

| Infectious Diseases |

| Others |

| Small-Molecule Drugs |

| Biologics & Monoclonal Antibodies |

| Gene & Cell Therapy |

| RNA-based Therapy |

| Enzyme Replacement Therapy |

| Others |

| Oral |

| Parenteral |

| Others |

| Hospitals |

| Specialty Clinics |

| Home-Care Settings |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Disease Type | Oncological Rare Diseases | |

| Neurological Disorders | ||

| Metabolic Disorders | ||

| Hematologic Disorders | ||

| Immunological Disorders | ||

| Infectious Diseases | ||

| Others | ||

| By Therapy Type | Small-Molecule Drugs | |

| Biologics & Monoclonal Antibodies | ||

| Gene & Cell Therapy | ||

| RNA-based Therapy | ||

| Enzyme Replacement Therapy | ||

| Others | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Others | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Home-Care Settings | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current rare disease treatment market size?

The rare disease treatment market size is USD 271.07 billion in 2026 and is expected to reach USD 472.89 billion by 2031.

Which therapeutic area is growing fastest within the rare disease treatment market?

Neurological disorders are forecast to grow at a 12.62% CAGR through 2031, driven by breakthrough gene therapies.

Why do rare-disease treatments command premium prices?

Limited patient pools and extensive development costs, combined with exclusivity incentives and demonstrated clinical impact, sustain prices often exceeding USD 500,000 per year.

Which region is projected to grow most rapidly?

Asia-Pacific is projected to expand at a 13.29% CAGR to 2031 due to regulatory reforms and broadened rare-disease registries.

Page last updated on: