Infantile Spasms Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

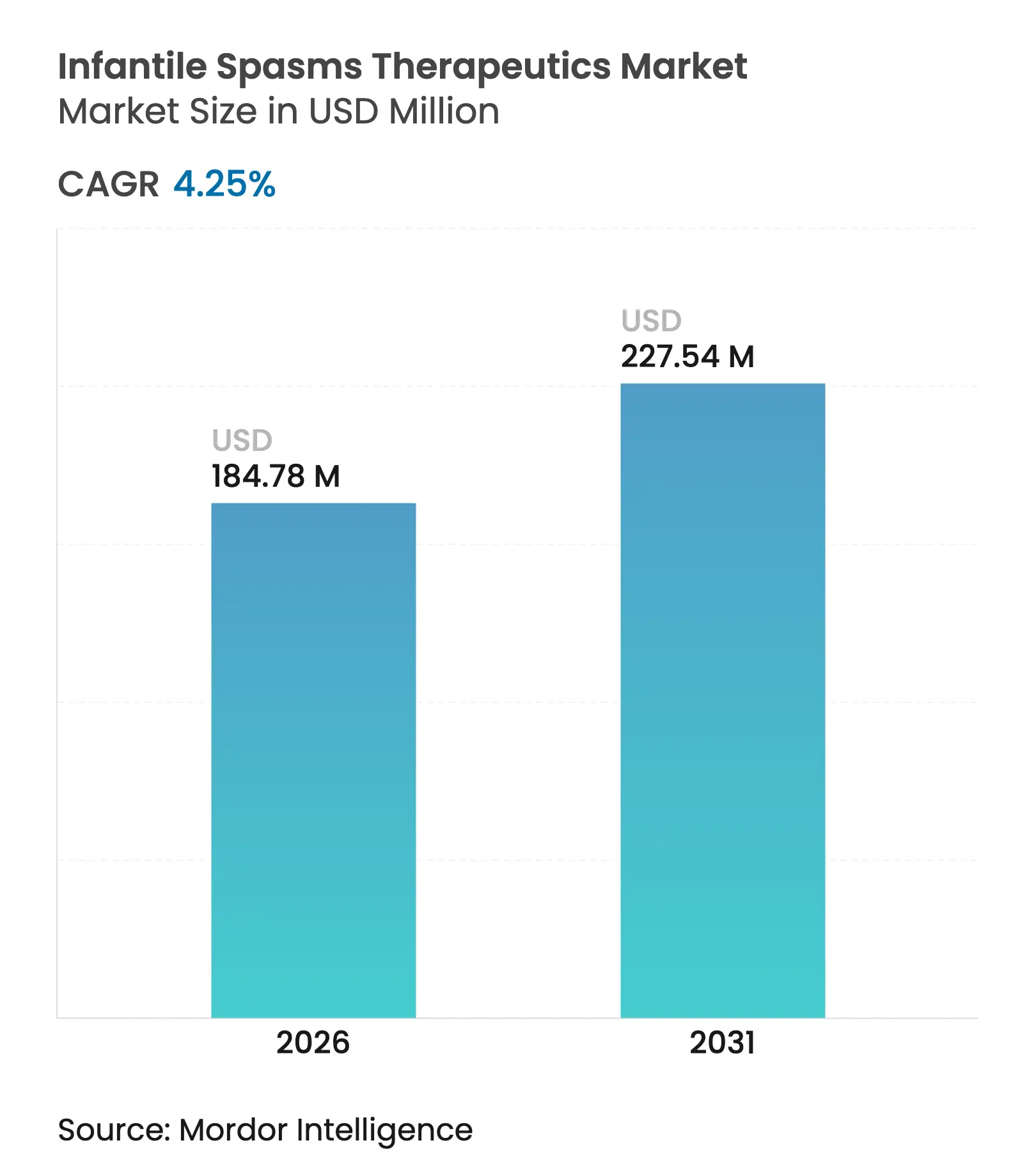

| Market Size (2026) | USD 184.78 Million |

| Market Size (2031) | USD 227.54 Million |

| Growth Rate (2026 - 2031) | 4.25 % CAGR |

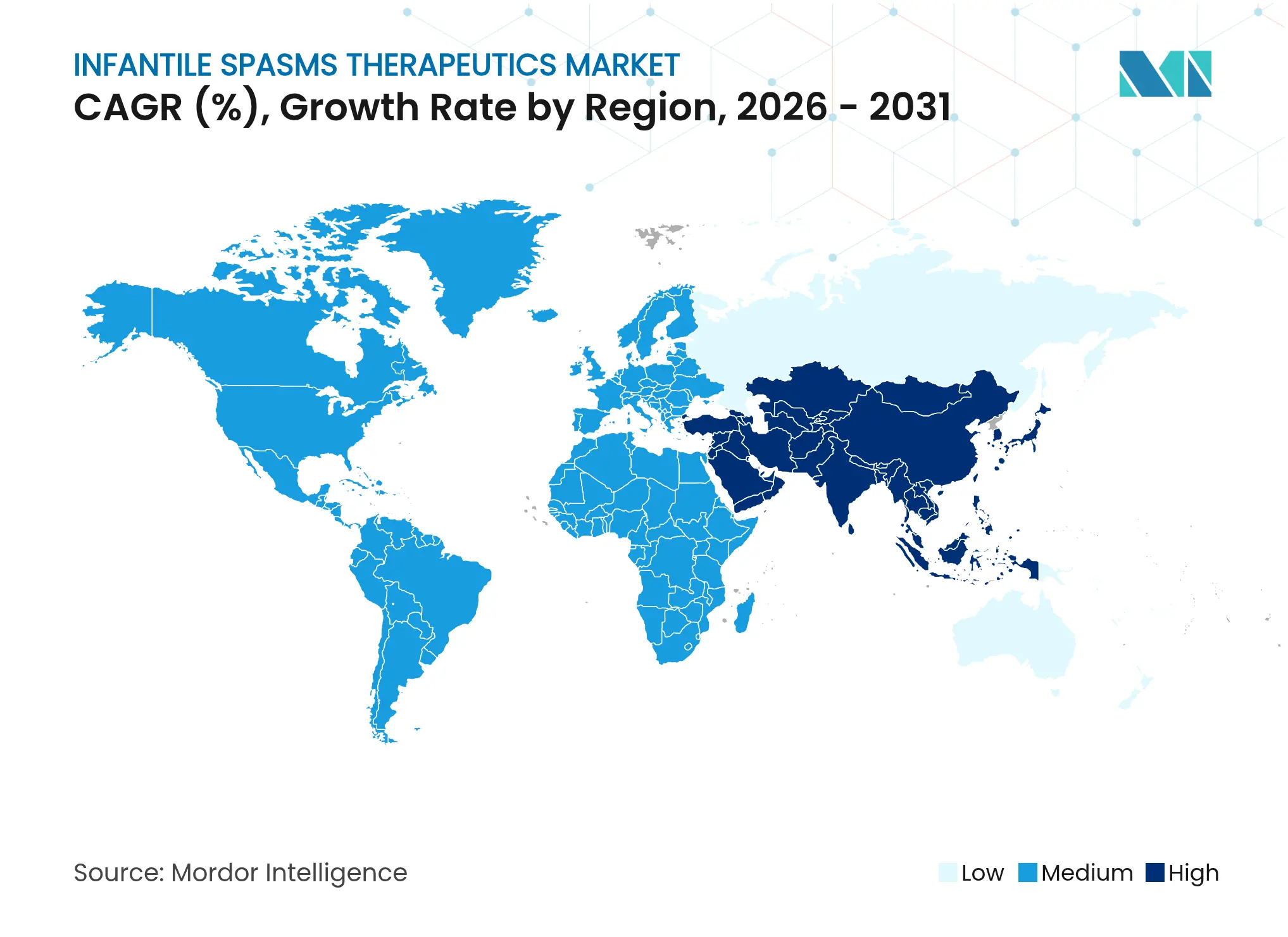

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Infantile Spasms Therapeutics Market Analysis by Mordor Intelligence

The infantile spasms therapeutics market size is expected to grow from USD 177.25 million in 2025 to USD 184.78 million in 2026 and is forecast to reach USD 227.54 million by 2031 at 4.25% CAGR over 2026-2031. The growth trajectory is steered by earlier seizure detection through AI-assisted video analytics, accelerated orphan-drug approvals, and precision therapies that target specific genetic pathways such as mTOR and GABA-A receptors. North America maintains clinical leadership through rapid adoption of breakthrough products, while Asia Pacific records the fastest regional CAGR of 6.73% on the back of expanding diagnostic infrastructure and synchronized regulatory reviews. Digital dispensing channels—especially online pharmacies—are the fastest-growing distribution route at an 8.73% CAGR, reflecting rising acceptance of tele-neurology and home-based monitoring solutions. Competitive dynamics reveal a shift from broad hormonal regimens toward mechanism-specific agents that command premium pricing yet serve narrowly defined patient subgroups.

Key Report Takeaways

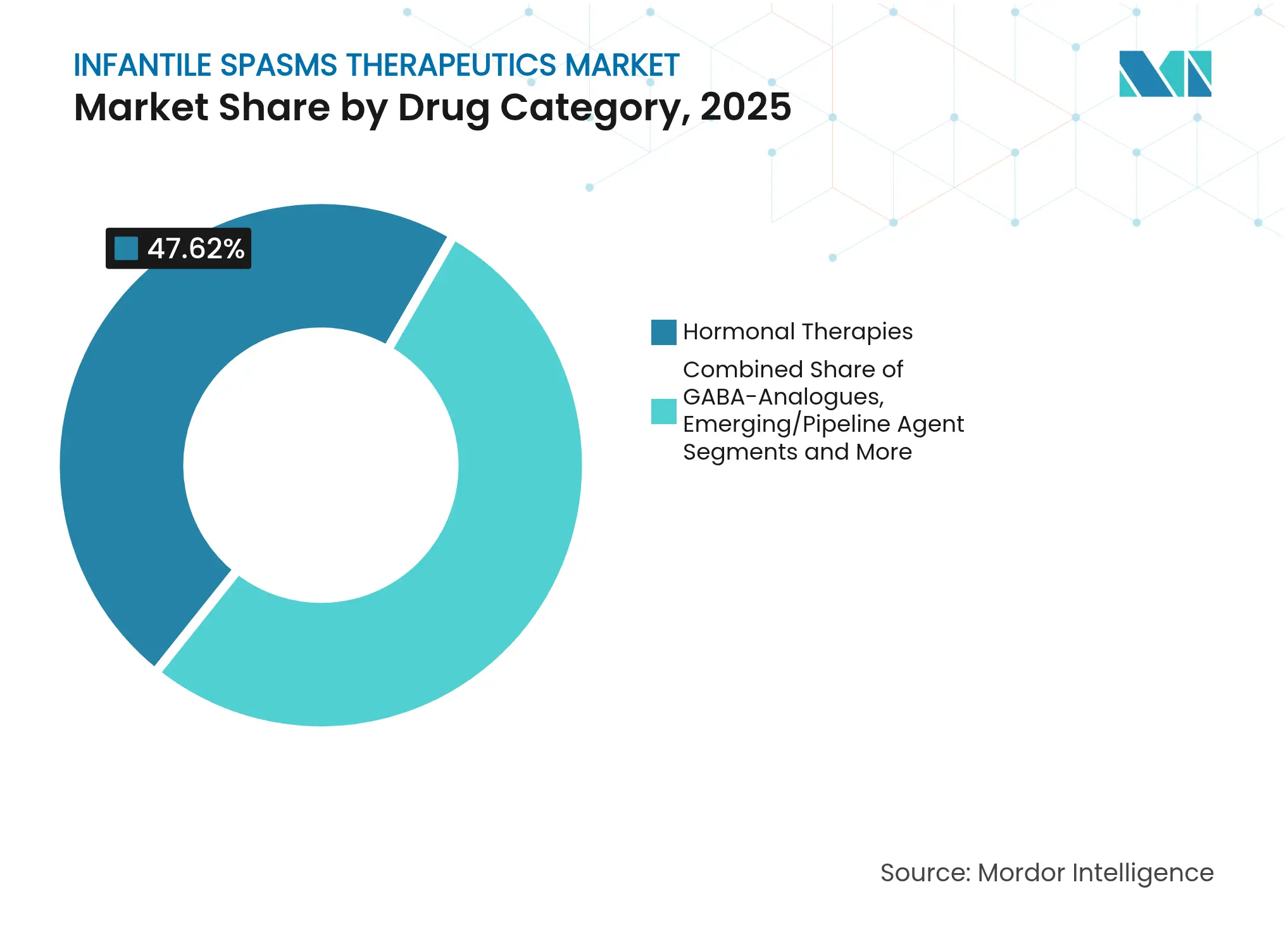

- By drug category, hormonal therapies held 47.62% of the infantile spasms therapeutics market share in 2025, whereas emerging pipeline agents are projected to advance at a 6.78% CAGR to 2031.

- By mechanism of action, neurosteroid modulation posted the highest growth outlook at 7.35% CAGR, while hormonal mechanisms retained 46.83% revenue share in 2025.

- By route of administration, parenteral products dominated with 55.76% share in 2025; oral formulations are forecast to expand at an 7.85% CAGR through 2031.

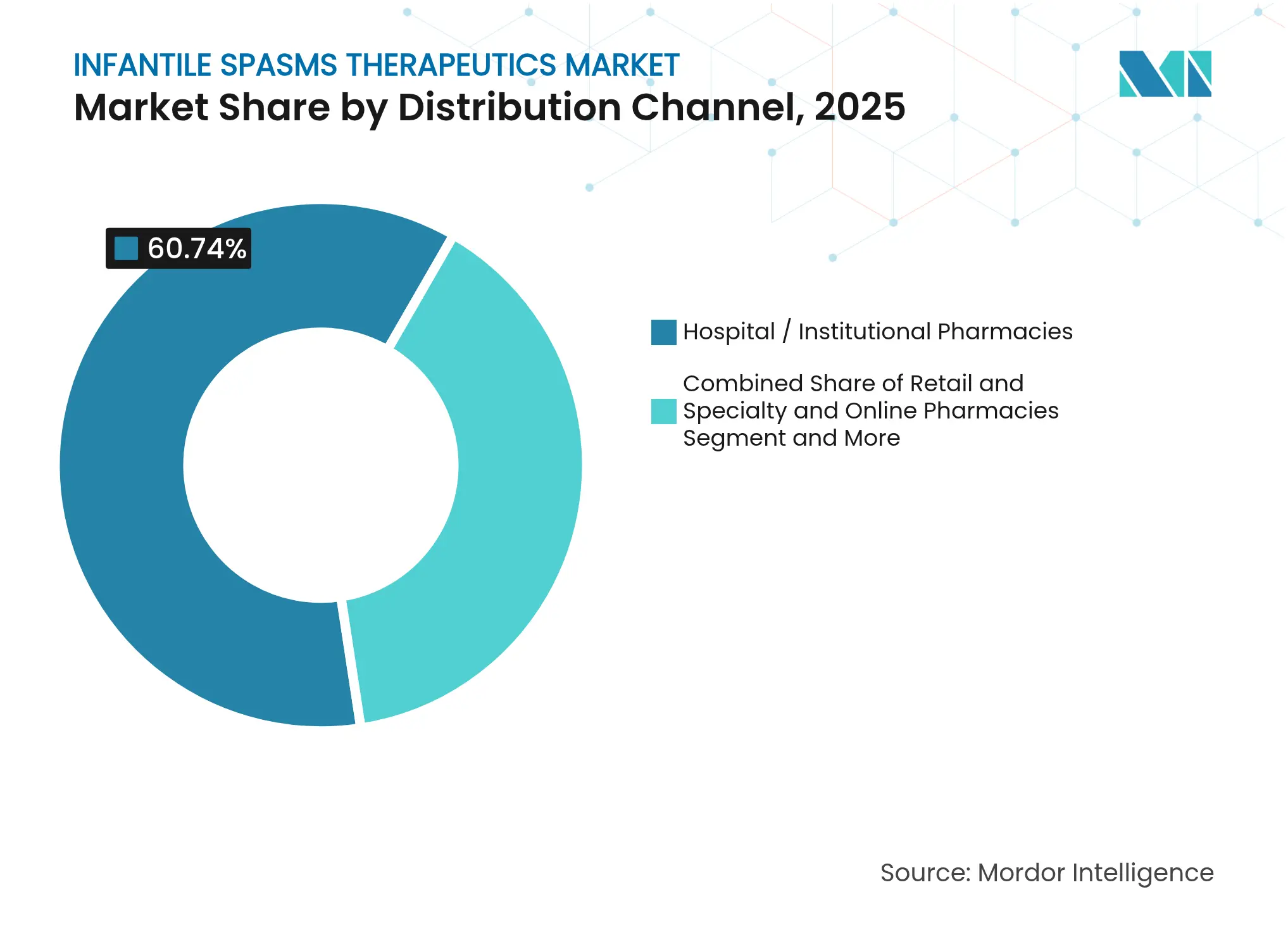

- By distribution channel, hospital and institutional pharmacies captured 60.74% of the infantile spasms therapeutics market in 2025; online pharmacies remain the quickest riser at 8.18% CAGR.

- By etiology, cryptogenic cases represented 39.22% of 2025 revenues, yet TSC-linked cases show the strongest CAGR at 6.56% through 2031.

- By geography, North America secured 36.98% revenue share in 2025, while Asia Pacific is projected to outpace all regions at 6.41% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infantile Spasms Therapeutics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Prevalence Of Infantile

Spasms & Earlier Diagnosis

Rising Prevalence Of Infantile

Spasms & Earlier Diagnosis

| +0.8% | Global, with concentrated impact in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+0.8%

|

Geographic Relevance

:

Global, with concentrated impact in

North America & EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Increasing Use Of Vigabatrin &

ACTH In Low- And Middle-Income Countries

Increasing Use Of Vigabatrin &

ACTH In Low- And Middle-Income Countries

| +0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) | |||

Gene-Panel Newborn Screening

Enabling Precision Therapies

Gene-Panel Newborn Screening

Enabling Precision Therapies

| +0.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) | |||

AI-Assisted Video/EEG Analytics

Accelerating Treatment Initiation

AI-Assisted Video/EEG Analytics

Accelerating Treatment Initiation

| +0.4% | Global, early adoption in developed markets | Short term (≤ 2 years) | |||

Fast-Track Orphan-Drug Approvals

& Reimbursement Pathways

Fast-Track Orphan-Drug Approvals

& Reimbursement Pathways

| +0.3% | North America & EU primarily | Medium term (2-4 years) | |||

Pipeline Of Neurosteroid &

mTOR‐Targeted Assets

Pipeline Of Neurosteroid &

mTOR‐Targeted Assets

| +0.7% | Global, with R&D concentration in North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of Infantile Spasms & Earlier Diagnosis

AI-driven video screening now detects infantile spasms with 82% sensitivity and 90% specificity, slashing the historic 2- to 3-month diagnostic lag that often closed critical neurodevelopmental windows.[1]Gadi Miron, “Detection of Epileptic Spasms Using Foundational AI and Smartphone Videos,” Nature Digital Medicine, nature.com Smartphone tools let caregivers capture seizure episodes for rapid specialist review, lifting the six-month seizure-freedom rate to 77.3% when treatment commences immediately after confirmation. Genomic sequencing in neonatal intensive care units delivers a 37% diagnostic yield, enabling targeted therapy selection within days and broadening the treated population. Earlier identification of cases increases treatment volumes and supports stable uptake of premium mechanism-based drugs, underpinning incremental market growth even under modest prevalence assumptions. As payer frameworks adjust coverage to favor swift intervention, the infantile spasms therapeutics market benefits from higher treated-patient counts and improved outcomes metrics.

Wider Use of Vigabatrin & ACTH in Low- and Middle-Income Countries

WHO’s inclusion of vigabatrin on its essential medicines list and streamlined ACTH dosing protocols broaden access across resource-constrained regions, notably South Asia and sub-Saharan Africa.[2]Jolanta Cross, “Mitigating Treatment Lag for Infantile Epileptic Spasms Syndrome in Low- and Middle-Income Countries,” UCL Discovery, discovery.ucl.ac.ukGeneric vigabatrin cuts therapy costs by up to 70%, increasing affordability for national health schemes. Tele-neurology platforms help offset specialist shortages, allowing rural clinics to implement standardized treatment regimens under remote supervision. Studies show that a ketogenic diet alongside conventional therapy achieves >50% seizure reduction in 73.7% of infants under 3 months, reducing reliance on costlier hormonal agents. Collectively, these initiatives enlarge the treated base in emerging economies and lift long-term demand for both legacy and novel therapeutics.

Gene-Panel Newborn Screening Enabling Precision Therapies

The 245-gene TREAT panel identifies actionable variants linked to developmental epileptic encephalopathies, including tuberous sclerosis complex and KCNQ2/3 mutations, with a 36% diagnostic yield in pediatric epilepsy cohorts.[3]Clara Saier, “TREAT: Systematic and Inclusive Selection Process of Genes for Genomic Newborn Screening,” Orphanet Journal of Rare Diseases, biomedcentral.comGenetic findings prompt therapy changes for 33% of patients, moving care from empirical polytherapy toward mechanism-specific regimens.[4]Magdalena Krygier, “Next-Generation Sequencing Testing in Children With Epilepsy,” Frontiers in Genetics, frontiersin.org mTOR inhibitors such as sirolimus have demonstrated seizure-prevention potential in high-risk infants enrolled in the STOP-2A study. Early-life genetic confirmation enables reimbursement for targeted drugs under orphan-disease programs, elevating premium-priced product penetration. As national newborn-screening mandates expand, precision-therapy uptake should sustain above-market growth rates for advanced agents.

AI-Assisted Video/EEG Analytics Accelerating Treatment Initiation

Deep-learning models trained on home videos deliver an AUC of 0.96 for spasm detection, allowing automated triage that eases pediatric neurologist workloads. FDA-authorized implantable EEG devices provide continuous brain-activity data that guide dose adjustments in drug-refractory cases. Integration of video analytics with tele-pharmacy platforms creates a feedback loop in which seizure data inform real-time prescription decisions, improving adherence and curbing hospital readmissions. Early adoption in the United States and Western Europe is already shortening time-to-treatment metrics reported by leading children’s hospitals. Wider roll-out across Asia Pacific is anticipated as reimbursement codes for digital monitoring mature, fostering incremental product utilization and service revenues.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost Of ACTH & Vigabatrin

Coupled With Limited Insurance Coverage

High Cost Of ACTH & Vigabatrin

Coupled With Limited Insurance Coverage

| -0.9% | Global, particularly acute in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-0.9%

|

Geographic Relevance

:

Global, particularly acute in

emerging markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Severe Visual-Field Toxicity Risk

With Vigabatrin

Severe Visual-Field Toxicity Risk

With Vigabatrin

| -0.4% | Global | Long term (≥ 4 years) | |||

Global Supply Bottlenecks For

Repository Corticotropin Injection

Global Supply Bottlenecks For

Repository Corticotropin Injection

| -0.5% | Global, concentrated in North America | Short term (≤ 2 years) | |||

Slow Enrollment In Rare-Disease

Clinical Trials Delaying Launches

Slow Enrollment In Rare-Disease

Clinical Trials Delaying Launches

| -0.3% | Global, R&D-intensive regions | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of ACTH & Vigabatrin Coupled With Limited Insurance Coverage

A single ACTH course often exceeds USD 40,000, a figure that remains beyond reach for many families in markets lacking robust rare-disease benefits. Prior-authorization delays of up to three weeks risk missing optimal treatment windows. Mandatory ophthalmologic monitoring for vigabatrin adds USD 500-1,000 in annual costs, and complex distribution mandates restrict generic competition. Although manufacturer assistance programs exist, administrative hurdles limit timely uptake, reinforcing socioeconomic disparities in access and compressing potential demand growth for high-cost therapies.

Global Supply Bottlenecks for Repository Corticotropin Injection

ACTH production relies on single-source manufacturing with cold-chain logistics, exposing the supply chain to facility-level disruptions. DEA quotas on controlled substances and FDA investigations into pricing practices periodically impede output, generating shortages that force clinicians to substitute less-preferred regimens. Even short-lived stockouts disrupt treatment continuity and erode clinician confidence, restraining volume growth during the forecast horizon while highlighting the need for supply diversification.

Segment Analysis

By Drug Category: Hormonal Dominance Faces Pipeline Pressure

The infantile spasms therapeutics market size reached USD 184.78 million in 2026, with hormonal therapies holding 47.62% of 2025 revenues. These agents remain first-line due to rapid seizure control but face intensifying competition from emerging mechanistic drugs that are advancing at a 6.78% CAGR. Scan-to-treatment times are shrinking, yet ACTH and high-dose corticosteroids continue to anchor acute protocols in tertiary centers. Parallel growth in generic vigabatrin improves affordability in TSC-linked cases, preserving share for GABA analogues even as innovation surges elsewhere.

Premium-priced neurosteroids and mTOR inhibitors move through orphan-drug channels, attracting investment by promising superior efficacy in genetically defined subpopulations. The infantile spasms therapeutics market benefits from FDA priority reviews that lower clinical-development risk, energizing small-cap biotech entrants. Over the forecast window, incremental hormonal sales will persist, but the fastest-rising revenue stacks will stem from mechanism-targeted newcomers that steadily erode reliance on broad hormonal regimens.

Note: Segment shares of all individual segments available upon report purchase

By Mechanism of Action: Neurosteroid Modulation Leads Innovation

Hormonal actions still underpin 46.83% of 2025 sales, yet neurosteroid modulators are charting a 7.35% CAGR through 2031 and increasingly frame prescribing debates. Ganaxolone’s launch validated GABA-A receptor potentiation as a pediatric-friendly pathway that spares infants systemic steroid exposure while delivering median seizure reductions exceeding 30%.

mTOR inhibitors continue to build an evidence base for seizure prevention in TSC infants, fostering prospects for combination regimens that simultaneously dampen epileptogenesis and mitigate developmental delays. GABAergic modulation via vigabatrin remains standard in TSC care algorithms, offering near-90% response rates and ensuring the infantile spasms therapeutics market retains a GABA backbone even as molecular diversity expands. Senolytic compounds under preclinical review add another mechanistic layer, illustrating how maturing knowledge of epileptogenic cascades is triggering multi-target drug design.

By Route of Administration: Oral Formulations Gain Momentum

Parenteral injections owned 55.76% of 2025 turnover, reflecting reliance on intramuscular ACTH and intravenous loading strategies in critical-care settings. Yet oral formulations carry the highest growth at 7.85% CAGR, catalyzed by FDA approval of ready-to-use Vigafyde, which simplifies vigabatrin dosing and reduces compounding errors.

Taste-masked suspensions such as ganaxolone facilitate at-home management, shrinking inpatient days and aligning with payer cost-containment goals. Nanoparticle carriers that boost oral bioavailability while safeguarding blood-brain-barrier transit are under active investigation, and their commercialization could expand outpatient care models. Collectively, these shifts underpin the rising share of oral products in the infantile spasms therapeutics market, especially in regions where community health nurses oversee ongoing therapy.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Distribution Channel: Digital Transformation Accelerates

Hospitals and institutional pharmacies generated 60.74% of 2025 revenue, justified by the need for EEG monitoring and multidisciplinary oversight during initiation phases. However, online pharmacies are scaling at an 8.18% CAGR as caregivers turn to tele-neurology consults that integrate e-prescriptions and home-delivery services. Integrated platforms link wearable seizure detectors with pharmacy refill alerts, creating a closed therapeutic loop that sustains adherence and flags breakthrough events.

Specialty pharmacies remain relevant as reimbursement navigators for high-ticket items like ACTH, expediting prior-authorization workflows and ensuring cold-chain integrity. The infantile spasms therapeutics industry gains incremental revenue streams from data-rich service propositions that accompany digital dispensing, widening the moat for technology-enabled distributors.

Note: Segment shares of all individual segments available upon report purchase

By Etiology Segment: TSC-Linked Cases Drive Precision Medicine

Cryptogenic or unknown etiologies led with 39.22% share in 2025, underscoring ongoing diagnostic gaps despite broader sequencing access. Conversely, TSC-linked cases are set to grow fastest at 6.56% CAGR as newborn genetic panels become routine and prophylactic mTOR inhibition gains empirical support.

Reliable genotype-phenotype correlations allow clinicians to move straight to vigabatrin or everolimus, bypassing trial-and-error escalation. This precision markedly improves seizure-freedom odds and fuels higher willingness to pay among insurers for mechanism-aligned therapeutics, reinforcing the expansion of targeted sub-segments within the broader infantile spasms therapeutics market.

Geography Analysis

The infantile spasms therapeutics market size in North America was USD 65.56 million in 2025, translating to the largest regional contribution thanks to early access programs and favorable reimbursement. FDA breakthrough designations, such as bexicaserin’s fast-track status, shorten launch cycles, and strong payer support ensures broad uptake of premium modalities. Academic children’s hospitals remain hubs for gene-panel testing, driving demand for precision-aligned drugs and digital monitoring services.

Asia Pacific adds the highest incremental volume, propelled by 6.41% CAGR forecast through 2031 as public hospitals in China, India, and Southeast Asia integrate AI seizure detection and expand neonatal screening. China’s 2024 approval of ganaxolone demonstrates regulatory convergence with Western benchmarks while national reimbursement pilots promise wider affordability for orphan-tagged products. Japan’s continued investment in hospital EEG capacity and specialized formulations such as Fycompa injection further cements the region’s appetite for advanced therapies.

Europe represents a mature yet innovation-sensitive corridor, where EMA’s parallel scientific advice procedures reduce duplicated trials and speed pan-region access. Unified health technology assessments increasingly place value on quality-adjusted life-years gained from early seizure control, supporting penetration of high-cost gene-informed treatments. Latin America and the Middle East/Africa collectively trail in absolute dollars but are beginning to adopt the South Asia allied IESS mitigation playbook that reduces diagnostic delays, laying groundwork for sustained albeit smaller percentage growth in the infantile spasms therapeutics market.

Competitive Landscape

Market Concentration

The infantile spasms therapeutics market exhibits moderate concentration, with top five players collectively holding an estimated 58% revenue share. Lundbeck’s USD 2.6 billion purchase of Longboard Pharmaceuticals secures rights to bexicaserin and strengthens its mechanism-specific neurology portfolio. Immedica’s USD 151 million agreement to acquire Marinus Pharmaceuticals underscores industry conviction that neurosteroid modulators have durable commercial legs in rare epilepsies.

Mallinckrodt continues defending Acthar Gel’s share via lifecycle management and recently agreed to merge with Endo to create a diversified rare-disease specialist with deeper geographic reach. UCB’s USD 125 million takeover of Engage Therapeutics extends its franchise into rapid-acting seizure solutions such as Staccato alprazolam. Digital-health entrants collaborate with incumbents to embed AI diagnostic modules into therapy bundles, shifting competition toward integrated care ecosystems that reward data fluency as much as drug innovation.

Patent expiries—Acthar Gel’s suite ends 2031-2034—present opportunities for biosimilar developers, although complex manufacturing may curb immediate threats. Venture-backed biotechs are pursuing gene-editing and senolytic strategies that could disrupt traditional pharmacotherapy; however, those assets remain pre-commercial for most of the outlook period. Overall, moderate consolidation and robust pipeline diversity set the stage for competitive coexistence rather than monopolistic dominance.

Infantile Spasms Therapeutics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mallinckrodt presented late-breaking Acthar Gel data in systemic lupus erythematosus at LUPUS 2025, reaffirming its commitment to chronic-use indications.

- March 2025: PANTHERx Rare was selected by Upsher-Smith to distribute VIGAFYDE™, the first ready-to-use vigabatrin oral solution for infants.

- March 2025: Mallinckrodt and Endo announced a merger aimed at building a global rare-disease powerhouse spanning infantile spasms therapeutics and adjacent neurology franchises.

Table of Contents for Infantile Spasms Therapeutics Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Infantile Spasms & Earlier Diagnosis

- 4.2.2Increasing Use Of Vigabatrin & ACTH In Low- And Middle-Income Countries

- 4.2.3Gene-Panel Newborn Screening Enabling Precision Therapies

- 4.2.4AI-Assisted Video/EEG Analytics Accelerating Treatment Initiation

- 4.2.5Fast-Track Orphan-Drug Approvals & Reimbursement Pathways

- 4.2.6Pipeline Of Neurosteroid & mTOR‐Targeted Assets

- 4.3Market Restraints

- 4.3.1High Cost Of ACTH & Vigabatrin Coupled With Limited Insurance Coverage

- 4.3.2Severe Visual-Field Toxicity Risk With Vigabatrin

- 4.3.3Global Supply Bottlenecks For Repository Corticotropin Injection

- 4.3.4Slow Enrollment In Rare-Disease Clinical Trials Delaying Launches

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Drug Category

- 5.1.1Hormonal Therapies

- 5.1.1.1ACTH (repository corticotropin)

- 5.1.1.2Oral Corticosteroids (prednisone, prednisolone)

- 5.1.2GABA-Analogues

- 5.1.2.1Vigabatrin

- 5.1.3Other Antiepileptic Drugs

- 5.1.3.1Topiramate

- 5.1.3.2Zonisamide

- 5.1.4Emerging / Pipeline Agents

- 5.1.4.1Neurosteroids (ganaxolone)

- 5.1.4.2mTOR-inhibitors (everolimus, sirolimus)

- 5.2By Mechanism of Action

- 5.2.1Hormonal (ACTH / steroids)

- 5.2.2GABAergic Modulation

- 5.2.3mTOR Pathway Inhibition

- 5.2.4Neurosteroid Modulation

- 5.3By Route of Administration

- 5.3.1Parenteral

- 5.3.2Oral

- 5.4By Distribution Channel

- 5.4.1Hospital / Institutional Pharmacies

- 5.4.2Retail & Specialty Pharmacies

- 5.4.3Online Pharmacies

- 5.5By Etiology Segment

- 5.5.1Tuberous Sclerosis Complex (TSC)-linked

- 5.5.2Cryptogenic / Unknown

- 5.5.3Structural-Acquired

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Mallinckrodt plc

- 6.3.2H. Lundbeck A/S

- 6.3.3Zydus Lifesciences Ltd.

- 6.3.4Dr. Reddy’s Laboratories Ltd.

- 6.3.5Lupin Ltd.

- 6.3.6Catalyst Pharmaceuticals Inc.

- 6.3.7Marinus Pharmaceuticals Inc.

- 6.3.8Sun Pharma Industries Ltd.

- 6.3.9Teva Pharmaceuticals Ltd.

- 6.3.10Hikma Pharmaceuticals plc

- 6.3.11Orphelia Pharma SA

- 6.3.12Pyros Pharmaceuticals Inc.

- 6.3.13Anavex Life Sciences Corp.

- 6.3.14GW Pharmaceuticals plc

- 6.3.15Takeda

- 6.3.16Novartis AG

- 6.3.17Aquestive Therapeutics Inc.

- 6.3.18Glenmark Pharma Ltd.

- 6.3.19Sandoz

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet Need Assessment

Global Infantile Spasms Therapeutics Market Report Scope

As per the scope of the report, infantile spasms, also called West syndrome, is a rare type of epilepsy that typically begins in infancy, usually between 3 and 8 months of age. It is characterized by sudden, jerking movements or spasms of the body, often in clusters. Medications that aim to suppress infantile spasms are considered under infantile spasms therapeutics.

The infantile spasms therapeutics market is segmented into drug type, route of administration, distribution channel, and geography. By drug category, the market is segmented into adrenocorticotropic hormone (ACTH), corticosteroids, and antiepileptic drugs. The antiepileptic drugs include vigabatrin and other antiepileptic drugs. By route of administration, the market is segmented into oral and parenteral. By distribution channels, the market is segmented into offline pharmacies and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market sizing and forecasts are based on the value (USD) for each segment.