Botulinum Toxin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

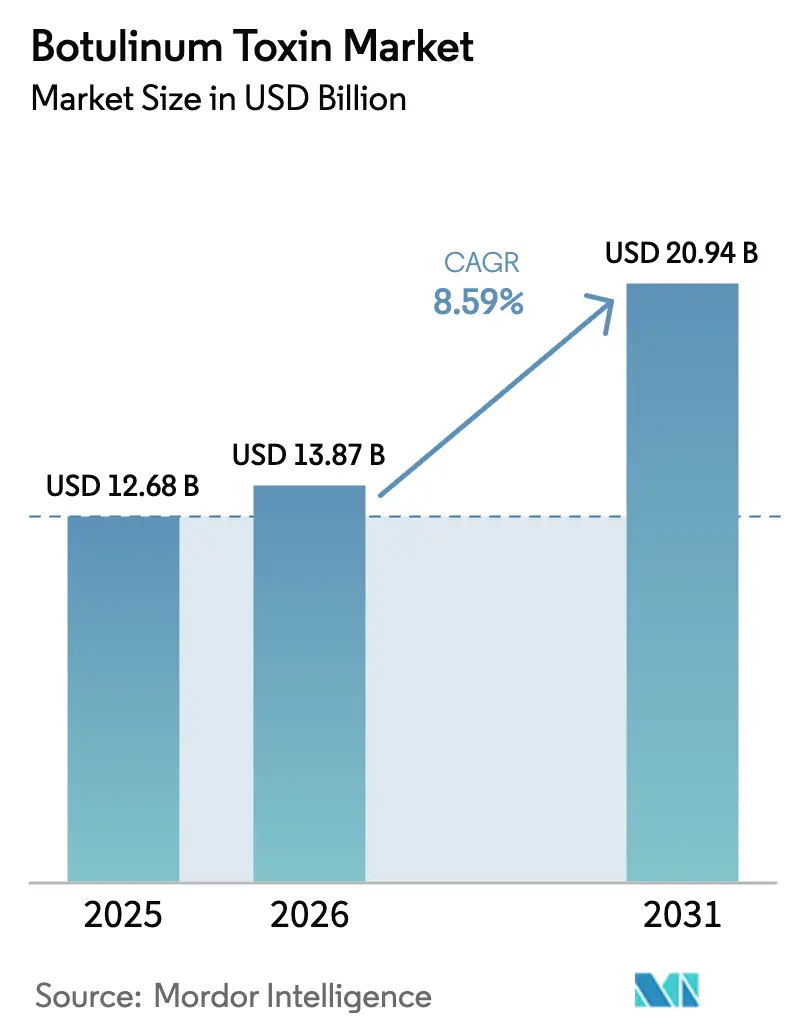

| Market Size (2026) | USD 13.87 Billion |

| Market Size (2031) | USD 20.94 Billion |

| Growth Rate (2026 - 2031) | 8.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

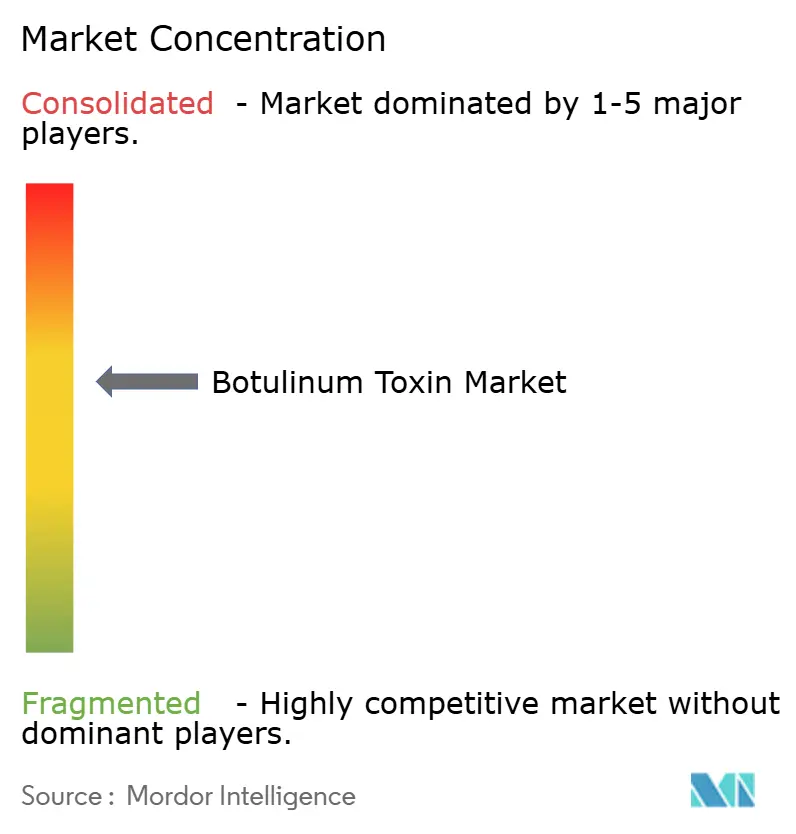

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Botulinum Toxin Market Analysis by Mordor Intelligence

The Botulinum Toxin Market size is projected to expand from USD 12.68 billion in 2025 and USD 13.87 billion in 2026 to USD 20.94 billion by 2031, registering a CAGR of 8.59% between 2026 to 2031.

Demand momentum is shifting toward reimbursed therapeutic indications such as chronic migraine prophylaxis and neurogenic bladder, even as aesthetic use continues to dominate overall procedure volumes. Competitive pressure now centers on protein-free and longer-lasting formulations, which promise lower immunogenicity and fewer clinic visits, themes that are reshaping both payer policies and provider workflow economics.

Key Report Takeaways

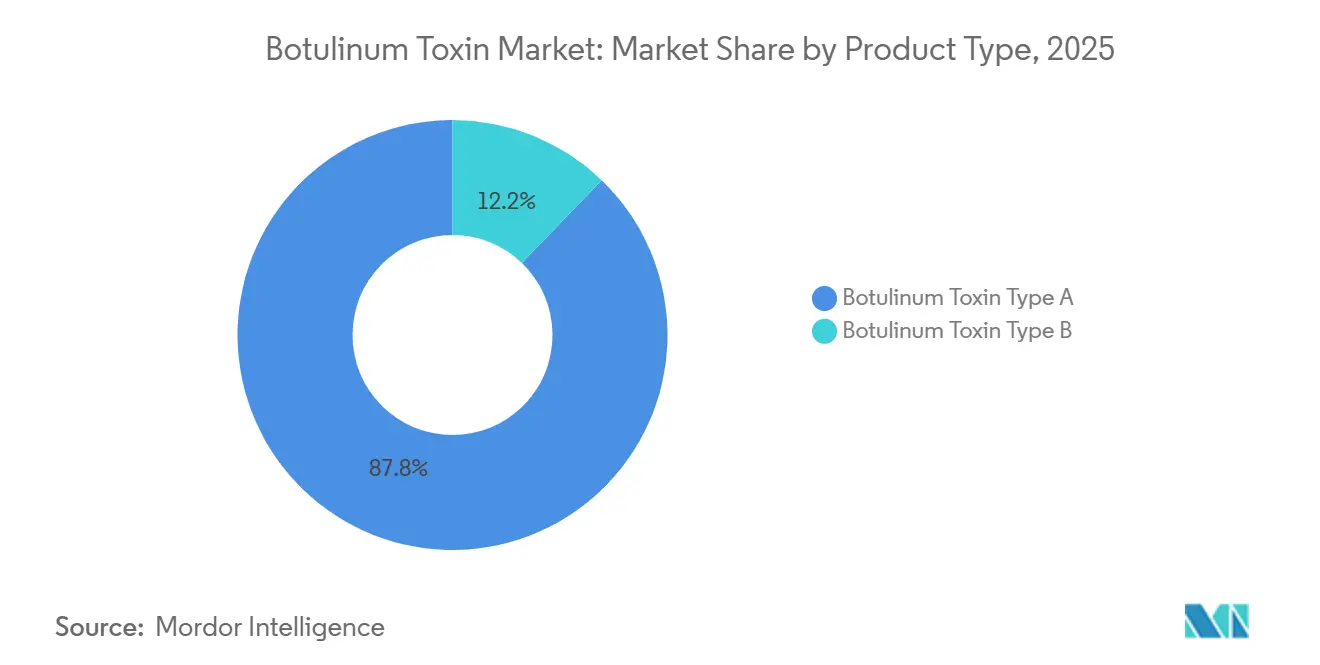

- By product type, Type A captured 87.81% revenue share of the botulinum toxin market in 2025, while Type B is advancing at a 10.58% CAGR through 2031.

- By application, aesthetic procedures accounted for 54.73% of 2025 sales; chronic migraine prophylaxis is forecast to expand at a 11.28% CAGR to 2031, outpacing cosmetics by 2.7 percentage points.

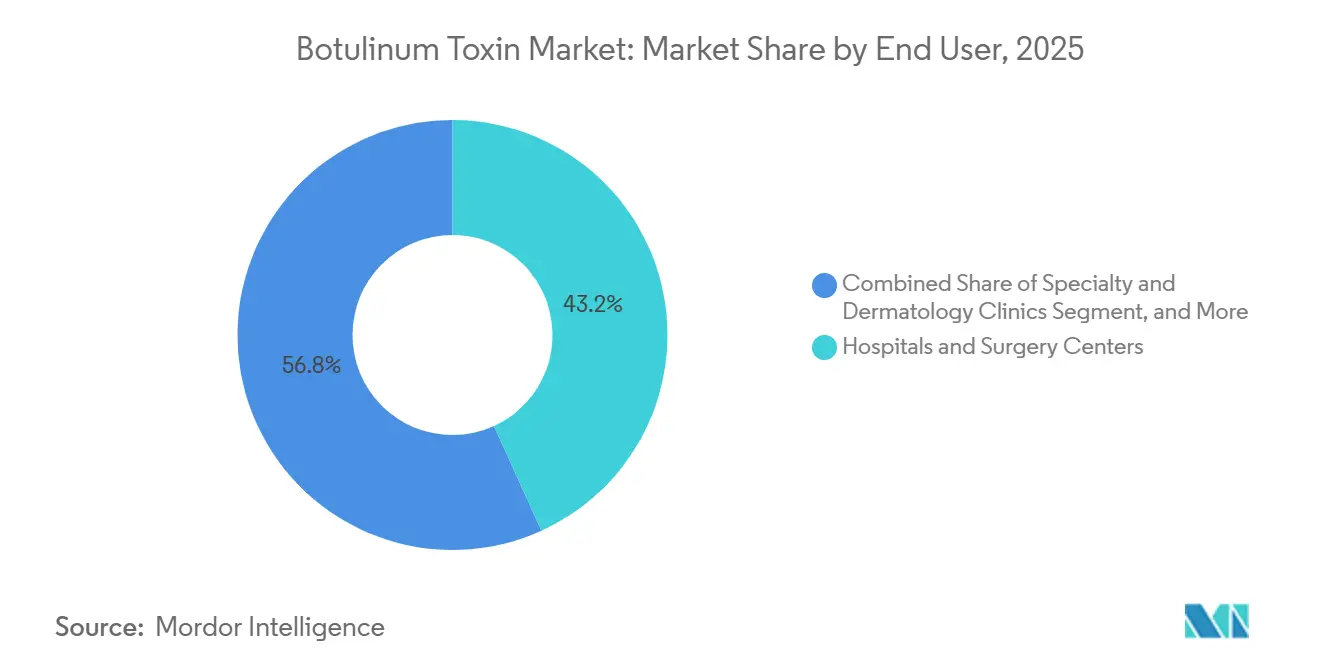

- By end user, hospitals and surgery centers held 43.18% of the 2025 volume, whereas specialty and dermatology clinics are projected to grow at a 9.25% CAGR, driven by cash-pay “same-day” treatments.

- By geography, North America led the botulinum toxin market in 2025, with a 42.36% market share; however, the Asia-Pacific region is expected to be the fastest-growing region, with a 12.13% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Botulinum Toxin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Minimally Invasive Aesthetics | +2.1% | Global, led by North America, Europe, urban APAC | Medium term (2-4 years) |

| Growing Adoption in Chronic Migraine Prophylaxis | +1.8% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Expansion in APAC via Indigenous Manufacturers | +1.5% | APAC core, spillover to Middle East & Africa | Short term (≤ 2 years) |

| Longer-Lasting, Protein-Free Formulations | +1.3% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising Male and “Pre-Juvenation” Segments | +0.9% | North America, Europe, affluent APAC metros | Short term (≤ 2 years) |

| Reimbursement Gains for Neurogenic Bladder & OAB | +0.7% | North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Aesthetic Procedures

Global procedure counts continue to climb because neuromodulators offer immediate, reversible results without surgical downtime, qualities highly valued in social-media-driven cultures. The American Society of Plastic Surgeons recorded 9.88 million U.S. neuromodulator sessions in 2024, a 4% year-over-year uptick that masks even steeper growth among first-time male users and patients under 30.[1]American Society of Plastic Surgeons, “2024 Procedural Statistics,” plasticsurgery.org Instagram and TikTok compress consideration windows, pushing patients from awareness to treatment in under 18 months. Clinics that can schedule same-day consults capture these impulse conversions and report a 3.2-visit annual cadence per patient, sustaining recurring revenue. The “tweakment” culture favors subtle, repeat interventions rather than dramatic facelifts, which in turn stabilizes volume even when macroeconomic conditions soften and reinforces botulinum toxin market growth. Yet the surge also invites non-physician injectors where regulation is light, prompting quality concerns that authorities are beginning to police.

Growing Adoption in Chronic Migraine Prophylaxis

Chronic migraine affects roughly 2% of the population; onabotulinumtoxinA now holds first-line status under 2024 American Headache Society guidelines, supported by Level A evidence from multi-year trials.[2]American Headache Society, “2024 Migraine Guidelines,” americanheadache.org UnitedHealthcare removed prior-authorization requirements in 2025, resulting in a 34% reduction in dropout rates within six months. Health-economic analyses show that emergency department visits decrease by 47% and opioid prescriptions by 52% once patients initiate toxin prophylaxis, resulting in an annual net savings of USD 4,200 per case. Neurologists are increasingly administering injections in-office, thereby broadening the treatment base. As accountable-care organizations shoulder downside risk, botulinum toxin fits neatly into value-based care models, accelerating its therapeutic adoption.

Expansion in APAC Via Indigenous Manufacturers

South Korean and Chinese factories have reached annual capacities of 50 million vials, which is double that of many Western rivals, resulting in ex-factory prices of USD 80 per 100-unit vial, compared to USD 550 for BOTOX in Southeast Asia.[3]Medytox, “Annual Report 2024,” medytox.com Regulatory harmonization is quickening: China’s National Medical Products Administration cleared Lanzhou Hengli for 11 indications in 2024, including pediatric cerebral palsy. Daewoong’s Nabota received Health Canada approval in late 2024, signaling ambitions that extend beyond Asia. Indigenous firms therefore shift from regional players to global challengers, pressuring incumbents to either lower their price points or prove premium differentiation through superior clinical data, thereby influencing botulinum toxin market growth.

Longer-Lasting, Complexing-Protein-Free Formulations

Complexing proteins such as hemagglutinins can trigger antibody formation over time. IncobotulinumtoxinA, which omits these proteins, earned a 2024 FDA label allowing for the simultaneous treatment of all three upper-face areas, thereby reducing chair time by 40%. Revance’s daxibotulinumtoxinA claims a six-month duration, doubling the norm; early adopters report 22% higher satisfaction from fewer visits, but Q2 2025 revenue missed forecasts because injectors struggled with novel reconstitution steps. Clinical differentiation thus needs a complementary training infrastructure to translate into commercial traction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Immunoresistance & Neutralizing Antibody Risk | −0.9% | Global, higher in repeat therapeutic users | Long term (≥ 4 years) |

| Cold-Chain & Handling Gaps in Low-Income Markets | −0.7% | Sub-Saharan Africa, South Asia, rural Latin America | Medium term (2-4 years) |

| Counterfeit / Grey-Market Supply | −0.5% | APAC, Middle East, Eastern Europe | Short term (≤ 2 years) |

| High Out-of-Pocket Cosmetic Costs | −0.6% | Global, most acute in North America & Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Immunoresistance & Neutralizing Antibody Risk

Neutralizing antibodies arise in 1–3% of repeat users, typically after seven cycles or cumulative doses exceeding 200 units, which can lead to treatment failure and necessitate product switching. Comparative data on protein-free versus conventional toxins remain sparse, leaving clinicians reliant on pragmatic dosing strategies and wider inter-treatment intervals. Payers watching real-world effectiveness may introduce antibody testing, adding cost and administrative steps that could dampen uptake, especially in aesthetic settings where patients pay out-of-pocket.

Cold-Chain & Handling Gaps in Low-Income Markets

The World Health Organization found that 38% of health facilities in sub-Saharan Africa experienced temperature excursions above 8 °C for more than four hours per month, jeopardizing the potency of toxins. Training deficits compound the problem: nearly one-third of rural Indian clinics stored reconstituted toxin past the 24-hour manufacturer limit. Until thermostable formulations move beyond early-stage trials, botulinum toxin market growth in these regions will remain urban-centric.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Type A’s Scale Conceals Type B’s Niche Resurgence

The botulinum toxin market size for Type A products accounted for 87.81% of total revenue in 2025, reflecting their broad FDA labeling across both aesthetic and therapeutic domains. Complex-protein-free formulations, such as Xeomin, are gradually eroding legacy share because the single-session upper-face indication, cleared in 2024, reduces chair time and appeals to volume-driven clinics. Jeuveau increased its U.S. market share from 4% in 2019 to 14% in 2025 by targeting millennials with social media-centric campaigns at prices 20–30% lower than the market leader. Daxxify’s six-month duration differentiator has not yet translated into proportional uptake because provider training requirements slow onboarding. Korean entrants with 30–40% lower pricing continue gaining traction in Asia and parts of Latin America, further shaping botulinum toxin market share.

Type B’s contribution is small yet rising at a 10.58% CAGR through 2031 as antibody-induced non-responders to Type A accumulate. RimabotulinumtoxinB offers a 24- to 48-hour onset, making it appealing for acute cervical dystonia cases. Eisai logged 19% European revenue growth in 2024, driven by neurologist switches rather than new-to-therapy patients. Duration is shorter, but where functional improvement outweighs cosmetic longevity, clinicians are willing to trade repeat visits for efficacy. The result is a stable, if niche, revenue driver that diversifies the botulinum toxin industry portfolio.

By Application: Reimbursed Therapeutics Outpace Elective Aesthetics

Aesthetic procedures accounted for 54.73% of 2025 revenue, yet therapeutic indications are projected to expand at an annual rate of 11.28%, underscoring a fundamental realignment toward insurance-backed use. Within aesthetics, the traditional glabellar segment remains the anchor, but masseter reduction surged 89% in 2024 as male and Asian patients sought jawline contouring. Emerging body-contouring injections are experimental and lack FDA endorsement, limiting their contribution to the botulinum toxin market size. Hyperhidrosis, covered by many payers, serves as an entry point for cosmetic upsell.

Chronic migraine prophylaxis is the fastest-growing therapeutic use, buoyed by guideline upgrades and payer rule relaxation that eliminate prior-authorization steps. Spasticity across stroke, cerebral palsy, and multiple sclerosis maintains dependable volume, while OAB gains traction because Medicare now requires failure of just one oral agent. Pipeline data hint at new frontiers: AbbVie’s positive Phase II tremor results could pave the way for a fresh therapeutic avenue by 2027. In effect, reimbursement stability shields therapeutic lines from swings in consumer confidence, providing manufacturers with a predictable base to hedge against aesthetic cyclicality.

By End User: Clinics Gain Ground as Hospitals Face Reimbursement Compression

Hospitals and surgery centres controlled 43.18% of procedures in 2025, primarily driven by complex therapeutic cases that required multidisciplinary oversight. Nonetheless, a 12% facility-fee reduction for toxin administration under the 2024 CMS Outpatient Prospective Payment System prompts payers to nudge volume toward lower-cost sites. Time-motion analyses reveal that spasticity injections take 22 minutes in an outpatient setting, compared to 90 minutes for surgical alternatives, reinforcing hospitals’ productivity push while also highlighting the attractiveness of ambulatory centers.

Specialty and dermatology clinics are projected to expand at a 9.25% CAGR to 2031 and already deliver the bulk of cash-pay aesthetic sessions. Same-day booking, evening hours, and Instagram-friendly décor resonate with younger demographics. Upsell synergy is strong: 38% of hyperhidrosis patients convert to cosmetic toxin within 12 months. Spa-based and mobile services form a micro-segment, appealing to ultra-convenience seekers, but draw regulatory scrutiny; the FDA dispatched 14 warning letters to med-spas in 2024 for unlicensed use. Nurse-led clinics, such as those under public health pilots, further decentralize delivery, as seen in the UK NHS program for OAB.

Geography Analysis

North America accounted for 42.36% of global revenue in 2025 and remains the leading market for new product launches and regulatory precedents. U.S. volume reached 9.88 million procedures in 2024, concentrated in coastal metros for aesthetic purposes and dispersed across neurology and urology practices for therapeutic use. Health Canada’s 2024 approval of Nabota injects pricing competition that may expand access among cost-sensitive consumers. Mexico’s medical-tourism flow offers 50–60% cost savings but faces counterfeit risk, curbing its scale. The FDA's openness to novel serotypes, exemplified by TrenibotE’s 2025 BLA, signals ongoing innovation, although distant-spread safety communications raise concerns about malpractice insurance.

The Asia-Pacific region is forecast to grow at a 12.13% CAGR, the fastest worldwide, driven by domestic manufacturing scale and an expanding middle class. South Korea’s per-capita usage rivals that of the U.S., driven by cultural acceptance and government export incentives. China’s market divides along quality perceptions: tier-1 cities prefer Western labels, whereas tier-2 and tier-3 cities opt for domestic products priced at USD 80–100 per vial. Japan’s aging population pushes therapeutic demand; Xeomin only secured PMDA clearance in 2024, but uptake is accelerating. India’s aesthetic segment grows at a rate of 20–25% annually in urban centers, yet cold-chain gaps constrain its broader penetration. Southeast Asian hubs, such as Bangkok, treat approximately 120,000 international aesthetic patients annually at 40% discounts, thereby extending the regional reach of the botulinum toxin market.

Europe holds a mid-tier share, with growth tempered by the European Medicines Agency’s 2025 mandate for enhanced distant-spread warnings, which lengthen sales cycles in France and Italy. Germany and the UK lead therapeutic uptake through national health coverage for chronic migraine and spasticity; the UK’s nurse-led OAB clinics have reduced wait times from nine months to six weeks. Eastern European countries are catching up as incomes rise and Western-trained physicians return to their homeland. In the Middle East, the UAE and Saudi Arabia drive growth, leveraging their high per-capita wealth and medical tourism infrastructure. South Africa exhibits steady private-sector growth, but wider sub-Saharan penetration is limited by infrastructure and public health priorities. South America pivots on Brazil, where ANVISA reviews Korean and Chinese toxins, potentially democratizing access once approvals land.

Competitive Landscape

Three incumbents, AbbVie, Ipsen, and Merz, held a combined significant share in 2025; however, the botulinum toxin market is becoming increasingly contested as Korean and Chinese firms scale up production and secure Western approvals. AbbVie defends its premium status through continuous indication expansions; the positive Phase II tremor data announced in October 2025 could unlock a fresh therapeutic domain. Korean manufacturers undercut prices by 30–40%, gaining footholds in tier-2 geographies and cash-pay clinics. Revance introduces peptide-exchange technology for a longer duration, but learns that workflow friction can blunt the commercial payoff of innovation. Meanwhile, AEON Biopharma’s ABP-450, identical in amino-acid sequence to BOTOX, completed pivotal trials in 2025, signaling a near-term biosimilar challenge.

Technology plays an increasing role. AbbVie integrated blockchain serialization in 2025 to combat counterfeiting, thereby differentiating its supply chain integrity. Evolus leverages AI-driven facial mapping in Jeuveau consultations, which is credited with propelling its 14% U.S. market share. Regulatory dynamics are decisive: the FDA’s willingness to license new serotypes contrasts with the EMA’s tightening of safety standards, creating asymmetric compliance costs. Ultimately, companies must juggle clinical superiority, cost competitiveness, regulator relationships, and anti-counterfeit initiatives, all while educating injectors to ensure adoption.

Botulinum Toxin Industry Leaders

Evolus

AbbVie

Merz

Ipsen Pharma

Galderma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AbbVie submitted a Biologics License Application (BLA) to the FDA for TrenibotE (trenibotulinumtoxinE), the first botulinum toxin serotype E product, targeting rapid-onset aesthetic applications with effects appearing within 24 hours versus 3–7 days for Type A toxins. This submission leverages Phase III data showing non-inferiority to BOTOX in glabellar line reduction, potentially opening a new segment for patients seeking immediate results before events.

- February 2025: AbbVie announced the launch of 3 new Allergan Medical Institute (AMI) training centers in Shanghai, São Paulo, and Dubai, expanding its global injector education network to 28 facilities. These centers train 15,000 practitioners annually on advanced injection techniques, reinforcing AbbVie's ecosystem lock-in strategy by ensuring injectors remain proficient with BOTOX-specific protocols.

- October 2024: Allergan Aesthetics received U.S. FDA approval for BOTOX Cosmetic to temporarily improve moderate to severe platysma bands in adults.

- September 2024: Allergan Aesthetics launched BOTOX Cosmetic for masseter muscle prominence in adults in China.

Global Botulinum Toxin Market Report Scope

As per the report's scope, botulinum toxin is a neurotoxic protein produced by the bacterium Clostridium botulinum. As a result, highly diluted concentrations of botulinum toxin are used for cosmetic and non-cosmetic purposes, such as for the treatment of frown lines between the eyebrows, dystonia, chronic migraine, and other purposes.

The botulinum toxin industry is segmented by product, application, end user, and geography. By product, the market is segmented into botulinum toxin type A and botulinum toxin type B. By application, the market is segmented into cosmetic applications and non-cosmetic applications. By cosmetic applications, the market is segmented into glabellar lines, lateral canthal lines (Crow's Feet), forehead lines, and other cosmetic applications. By non-cosmetic applications, the market is segmented into dystonia, chronic migraine, ophthalmic disorders, and other non-cosmetic applications. By end user, the market is segmented into spas & beauty centers and clinics & hospitals. By geography, the global market is segmented into North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, Rest of Middle East and Africa), and South America (Brazil, Argentina, Rest of South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD billion) for the above segments.

| Botulinum Toxin Type A | OnabotulinumtoxinA (Botox) |

| AbobotulinumtoxinA (Dysport) | |

| IncobotulinumtoxinA (Xeomin) | |

| PrabotulinumtoxinA (Jeuveau) | |

| DaxibotulinumtoxinA (Daxxify) | |

| Complexing-protein-free (Coretox & others) | |

| Botulinum Toxin Type B |

| Aesthetic | Glabellar Lines |

| Crow’s Feet | |

| Forehead Lines | |

| Masseter Reduction & Jaw Contouring | |

| Body Contouring & Hyperhidrosis | |

| Therapeutic | Chronic Migraine |

| Spasticity | |

| Cervical Dystonia | |

| Neurogenic Detrusor Overactivity / OAB | |

| Sialorrhea | |

| Others (Strabismus, Tremor, TMD) |

| Specialty & Dermatology Clinics |

| Hospitals & Surgery Centers |

| Spas & Beauty Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Botulinum Toxin Type A | OnabotulinumtoxinA (Botox) |

| AbobotulinumtoxinA (Dysport) | ||

| IncobotulinumtoxinA (Xeomin) | ||

| PrabotulinumtoxinA (Jeuveau) | ||

| DaxibotulinumtoxinA (Daxxify) | ||

| Complexing-protein-free (Coretox & others) | ||

| Botulinum Toxin Type B | ||

| By Application | Aesthetic | Glabellar Lines |

| Crow’s Feet | ||

| Forehead Lines | ||

| Masseter Reduction & Jaw Contouring | ||

| Body Contouring & Hyperhidrosis | ||

| Therapeutic | Chronic Migraine | |

| Spasticity | ||

| Cervical Dystonia | ||

| Neurogenic Detrusor Overactivity / OAB | ||

| Sialorrhea | ||

| Others (Strabismus, Tremor, TMD) | ||

| By End User | Specialty & Dermatology Clinics | |

| Hospitals & Surgery Centers | ||

| Spas & Beauty Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What growth rate is expected for the botulinum toxin market through 2031?

The botulinum toxin market is projected to expand at an 8.59% CAGR, rising from USD 13.87 billion in 2026 to USD 20.94 billion by 2031.

Which region will add the most new revenue?

The Asia-Pacific region is forecast to post the fastest regional growth at a 12.13% CAGR, driven by lower-priced domestic products and rising demand from the middle class.

Why are therapeutic indications outpacing aesthetics?

Therapeutic uses like chronic migraine and OAB receive insurance reimbursement, producing an 11.28% CAGR that exceeds driven by aesthetic procedure.

How big is Type A’s lead over Type B?

Type A held 87.81% share in 2025, while Type B is growing quickly but from a small base as it serves patients who develop antibodies to Type A toxins.

What is the main risk to long-term efficacy?

Neutralizing antibodies form in 1–3% of repeat users, particularly at high cumulative doses, potentially rendering treatment ineffective over time.

Page last updated on: