Pain Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 85.63 Billion |

| Market Size (2031) | USD 106.86 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pain Management Market Analysis by Mordor Intelligence

pain management market size in 2026 is estimated at USD 85.63 billion, growing from 2025 value of USD 81.92 billion with 2031 projections showing USD 106.86 billion, growing at 4.53% CAGR over 2026-2031. Greater life expectancy, stringent opioid regulations and expanding use of connected neuromodulation platforms anchor this growth trajectory. Clinicians now favor multimodal regimens that blend non-opioid pharmacology with device-based therapies, a shift reinforced by payer incentives rewarding durable outcomes over pill counts. Digital health integration improves longitudinal monitoring, aligning treatment intensity with real-time patient-reported pain scores while curbing hospital readmissions. Heightened ESG scrutiny of legacy opioid makers meanwhile accelerates capital flows toward developers of non-addictive alternatives and AI-driven dosing algorithms.

Key Report Takeaways

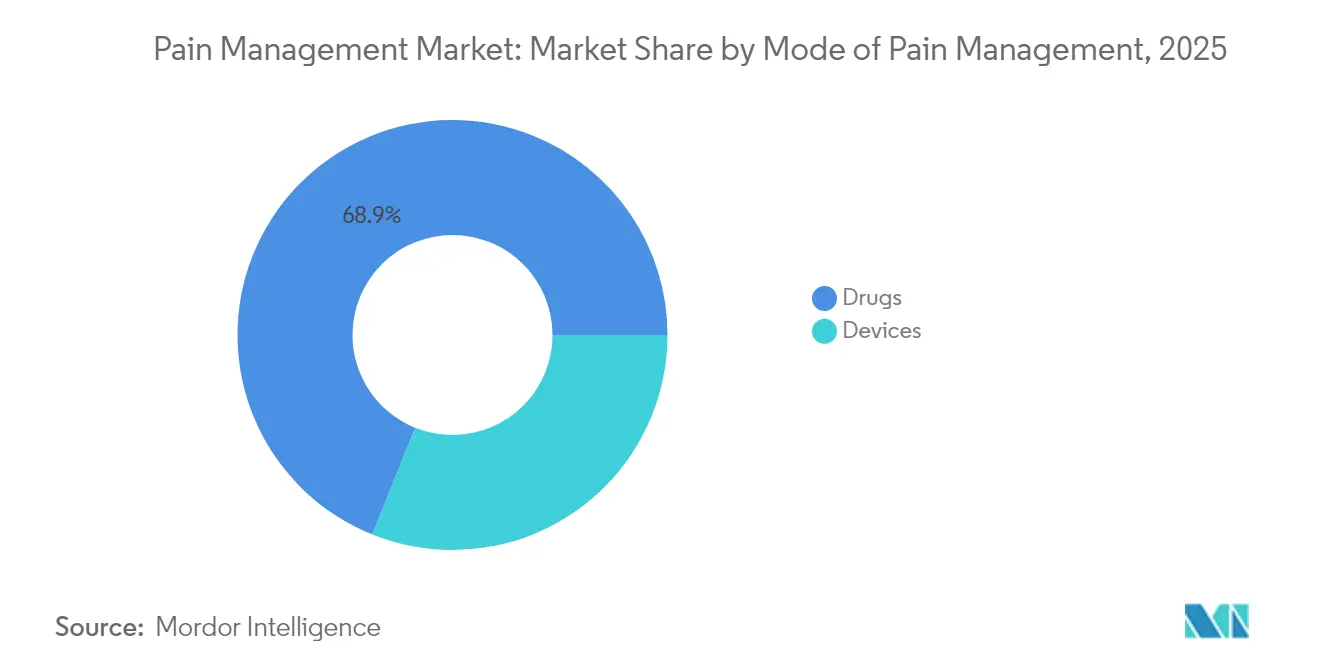

- By mode of pain management, drugs commanded 68.92% pain management market share in 2025, while devices are forecast to record the fastest 9.99% CAGR through 2031.

- By application, neuropathic pain led with 32.10% revenue share in 2025; facial pain and migraine therapies are set to expand at an 8.67% CAGR to 2031.

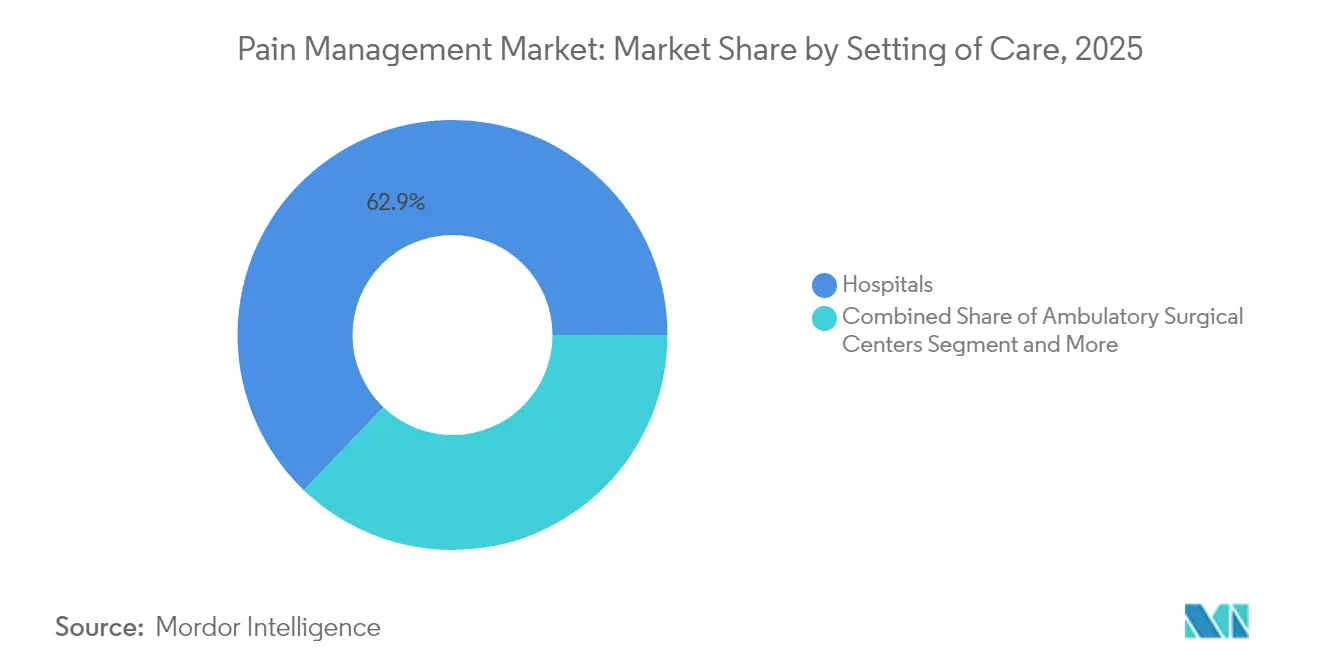

- By setting of care, hospitals accounted for 62.85% of the pain management market size in 2025 and home-care is projected to grow at an 11.55% CAGR through 2031.

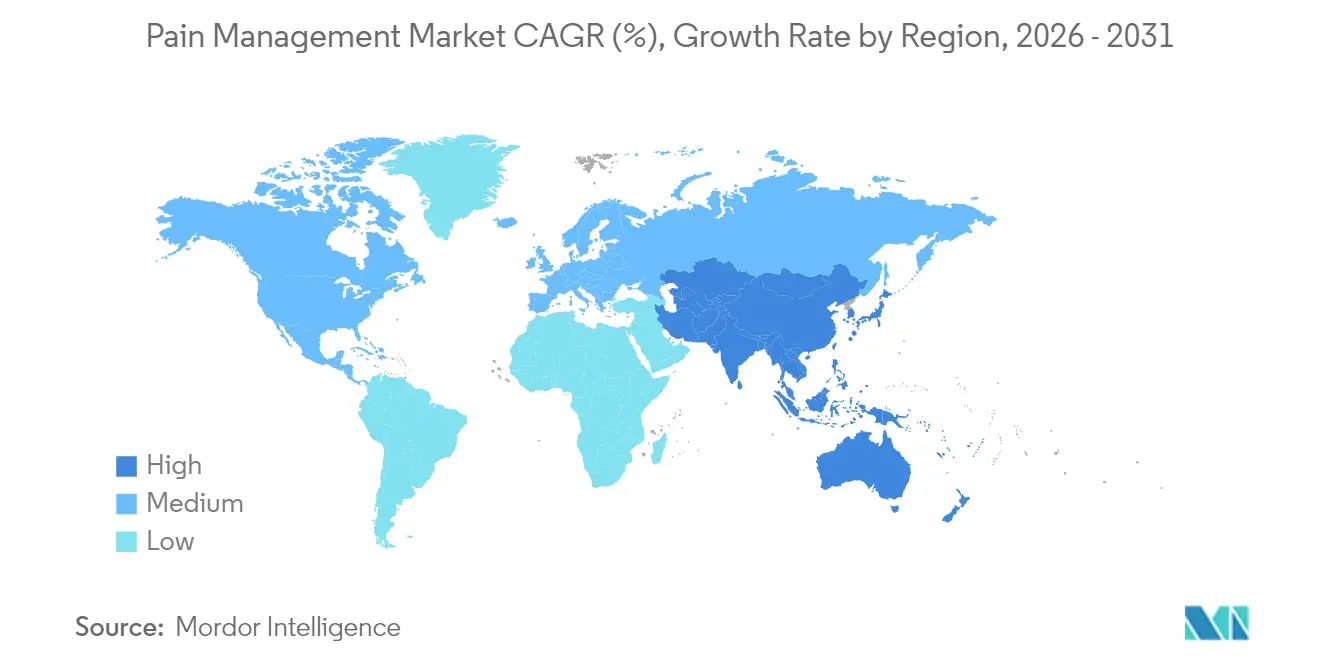

- By geography, North America contributed 38.10% revenue in 2025, whereas Asia-Pacific is expected to post a 10.55% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pain Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-Related Rise in Chronic Pain Prevalence | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Clinical Validation of Neuro-Modulation Efficacy | +0.8% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Opioid-Sparing Multimodal Protocols | +0.9% | Global, led by North America regulatory frameworks | Medium term (2-4 years) |

| Rapid ASC Adoption for Pain Procedures | +0.6% | North America & Europe | Short term (≤ 2 years) |

| Venture Funding for Closed-Loop Stimulation Platforms | +0.4% | North America & Europe | Long term (≥ 4 years) |

| AI-Driven, Patient-Specific Dosing Algorithms | +0.3% | North America & Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing-Related Rise in Chronic Pain Prevalence

Growing cohorts aged ≥ 45 now represent the highest incidence of chronic musculoskeletal and neuropathic complaints. In 2024, 24.3% of U.S. adults reported chronic pain, with prevalence peaking in the 65+ group. European meta-analysis places adult prevalence at 21.45%, propelled by diabetes, arthritis, and postsurgical syndromes. Patients living with persistent pain incur double the healthcare expenditure of age-matched peers and lose USD 12,167 annually in productivity within high-income countries[1]Caroline Rometsch et al., “Chronic Pain in European Adult Populations: A Systematic Review and Meta-Analysis,” PAIN, lww.com. Payers, therefore, channel funds toward longitudinal programs combining pharmaceutical, device, and behavioral elements. Recognition of chronic pain as a standalone disease entity further unlocks dedicated reimbursement codes and specialty clinic capacity worldwide.

Clinical Validation of Neuromodulation Efficacy

Landmark cost-utility studies show spinal cord stimulation paired with best medical therapy remains cost-effective over 10 years, outperforming pharmacologic management at typical willingness-to-pay thresholds[2]Xiaofeng Zhou et al., “Economic Evaluation of Management Strategies for Complex Regional Pain Syndrome,” Frontiers in Pharmacology, frontiersin.org. Dorsal root ganglion technology delivers even higher quality-adjusted life years for focal neuropathic syndromes, despite steeper upfront costs. Closed-loop platforms now auto-adjust amplitude based on evoked compound action potentials, sustaining analgesia as physiologic states shift. Regulatory bodies accelerate market entry through Breakthrough Device designations, trimming review times and incentivizing venture investment. Expanded reimbursement in select EU member states confirms recognition of durable neuromodulation value, increasing hospital purchasing confidence and physician adoption rates.

Shift Toward Opioid-Sparing Multimodal Protocols

Enhanced Recovery After Surgery programs institutionalize multimodal analgesia that blends NSAIDs, regional blocks and non-opioid adjuncts, matching or exceeding opioid-based regimens for pain control. Insurers reward such protocols with bundled-payment bonuses and prior-authorization waivers. Early opioid exposure correlates with long-term disability, spurring professional societies to elevate non-opioid options as first-line therapy. Pharma pipelines respond through non-addictive sodium-channel inhibitors and peripherally acting kappa agonists, several of which now carry FDA Breakthrough Therapy labels. Multimodal platforms that integrate digital coaching with pharmacologic and interventional tools improve adherence and document patient-reported outcomes for pay-for-performance contracts.

Rapid ASC Adoption for Pain Procedures

Ambulatory surgical centers (ASCs) deliver radiofrequency ablation, neurolytic blocks and generator replacements at 30-50% lower facility cost than inpatient theaters while maintaining similar safety profiles. Advanced imaging, lighter anesthesia requirements and rapid mobilization protocols let patients return home the same day, boosting satisfaction scores. U.S. state regulators have expanded licensure scopes, letting ASCs add intrathecal pump refills and trial stimulator placements. Device makers now design low-profile leads and single-incision insertion kits tailored to the ASC workflow. Health systems form joint ventures with surgeons to capture this outpatient volume, further decentralizing the pain management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX/OPEX for Implantable Devices | -0.7% | Global, particularly emerging markets | Medium term (2-4 years) |

| Limited Reimbursement in Emerging Markets | -0.5% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Cyber-Security Risks in Connected Pumps | -0.3% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| ESG Scrutiny on Opioid Manufacturers | -0.4% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX/OPEX for Implantable Devices

Implantable pulse generators priced between USD 20,000 – 50,000 per patient exceed many public-sector budgets in emerging economies. Replacement surgeries every 4-7 years add anesthesia and hospitalization charges, straining payer tolerance. Health technology assessment agencies now demand ten-year real-world evidence before approving high-cost neuromodulation reimbursement lines. Manufacturers react by migrating to rechargeable batteries and automated programming that lower clinician touchpoints. Leasing models and outcome-based contracts have begun surfacing, yet capital intensity remains a gating factor across low- and middle-income settings.

Limited Reimbursement in Emerging Markets

National insurance schemes in India, Indonesia and Brazil prioritize infectious disease and maternal health, leaving limited coverage for chronic pain interventions. Out-of-pocket spend still represents more than 50% of total medical expenditure in several ASEAN states, restricting access to spinal cord stimulators and novel biologics. Lengthy regulatory timelines compound launch costs, often delaying product availability by three to five years versus the United States. Localized clinical-evidence mandates further lift trial expenses. Stakeholders explore tiered-pricing strategies and public-private partnerships to widen therapy reach, but meaningful reimbursement expansion is unlikely before broader health-system funding reforms mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Pain Management: Devices Drive Innovation Despite Drug Dominance

Drugs retained 68.92% of pain management market share in 2025, anchored by NSAIDs, anticonvulsants and selective antidepressants used for neuropathic indications. Non-opioid innovations, including sodium-channel blockers, sustain momentum as guideline authors promote opioid-sparing regimens. In value terms, the drugs segment added USD 3.2 billion year-over-year, supported by strong generic uptake in Asia-Pacific and Latin America. Devices are set to outpace pharmaceuticals at a 9.99% CAGR, adding roughly USD 11 billion to the pain management market size by 2031.

Closed-loop spinal cord stimulators and dorsal root ganglion systems headline this surge, leveraging real-time physiologic feedback to fine-tune amplitude and pulse width. Analgesic infusion pumps shrink in form factor while gaining Bluetooth-enabled dosage logs that feed clinician dashboards. FDA Breakthrough Device designations granted in 2024 and 2025 shave six to nine months from review cycles, accelerating commercial rollout. As value-based procurement spreads, hospital buyers increasingly weigh total cost of ownership, a metric favoring rechargeable stimulators with extended battery life.

By Application: Neuropathic Pain Leadership Faces Migraine Innovation

Neuropathic disorders captured 32.10% revenue in 2025, underpinned by rising diabetes incidence and postsurgical nerve injuries. Peripheral neuropathy cases now account for one in four clinic visits at tertiary pain centers, prompting expanded use of dual-mechanism anticonvulsants and high-frequency stimulators. Cancer pain remains sizable but grows more modestly as palliative care protocols mature.

Facial pain and migraine present the swiftest trajectory, advancing 8.67% annually on the back of CGRP monoclonal antibodies and small-molecule gepants. Digital therapeutics delivering cognitive-behavioral modules for migraine prophylaxis reached U.S. Medicare coverage in 2025, broadening patient access. Targeted occipital nerve stimulators also move into pivotal trials, promising device-based relief for refractory migraineurs. Precision medicine approaches that genotype sodium-channel variants could soon guide therapy selection across both neuropathic and migraine cohorts, deepening clinical adoption.

By Setting of Care: Home-Care Revolution Challenges Hospital Dominance

Hospitals still represent 62.85% of pain management market size in 2025 owing to complex implantations, pump refills and comorbidity management. Tertiary centers retain an edge in imaging infrastructure and multidisciplinary staffing, sustaining procedure volumes. Yet the cost differential between inpatient and outpatient venues widens under bundled-payment schemes, nudging health systems toward decentralized models.

Home-care and remote monitoring are projected to climb 11.55% annually. Connected intrathecal pumps now transmit dose logs and battery status to cloud dashboards, letting clinicians pivot therapy before adverse events occur. Wearable biosensors capture gait, sleep and heart-rate variability, producing objective endpoints for reimbursement and clinical decision support. Cybersecurity protocols grounded in zero-trust architecture safeguard data streams, reinforcing payer and patient confidence in distributed care.

Geography Analysis

North America retained 38.10% revenue in 2025, supported by mature reimbursement, extensive ASC networks and swift FDA clearance pathways. Continued litigation over opioid marketing drives diversification toward non-addictive modalities, inflating demand for neuromodulation and non-opioid analgesics. Medicaid expansion in additional U.S. states during 2025 further widens patient pools for comprehensive pain management programs.

Europe displays balanced maturation; Western states sustain incremental gains while Eastern markets accelerate device adoption under EU cohesion funding. The European Medicines Agency’s rolling review procedures shortened average approval times for biosimilars and novel analgesics by 15% in 2025. National health technology assessment bodies increasingly recognize quality-of-life outcomes, prompting broader reimbursement for validated neuromodulation indications.

Asia-Pacific delivers the fastest regional CAGR at 10.55% through 2031. China’s Healthy 2030 blueprint earmarks chronic pain as a priority, enabling tier-two hospitals to establish specialty pain clinics. India’s telemedicine guidelines passed in 2025 legitimize e-prescriptions of non-schedule drugs, spurring digital consultation platforms. However, uneven insurance penetration and fragmented provider markets still limit uptake of high-cost implantables, constraining absolute market size relative to demographic potential.

Competitive Landscape

Competitive intensity stays moderate as legacy pharmaceutical firms leverage expansive patent estates and global distribution to defend share. Their pipelines now tilt toward peripheral sodium-channel blockers, N-type calcium-channel inhibitors and biologics targeting inflammatory cascades. Several multinationals divested opioid portfolios into separate legal entities during 2025 to mitigate ESG risk, reallocating capital to non-addictive assets.

Device players differentiate through algorithmic personalization, battery longevity and MRI conditionality. First-in-class closed-loop stimulators launched in 2025 showcase double-digit improvements in responder rates versus open-loop comparators at 12 months. Hybrid cloud platforms overlay predictive analytics onto stimulation logs, letting providers tune settings remotely.

Digital therapeutics innovators secure regulatory nods for app-based behavioral programs treating low back pain, migraine and fibromyalgia. Strategic alliances pair these apps with pharmacologic starter kits, creating bundled offerings that satisfy payer preferences for holistic care. The top five enterprises collectively control roughly 48% of global revenue, underscoring a moderately concentrated structure that still leaves ample room for specialized entrants.

Pain Management Industry Leaders

Abbott Laboratories

Becton, Dickinson and Company

Boston Scientific Corporation

Johnson & Johnson (DePuy Synthes, Ethicon)

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The FDA cleared Tonmya (cyclobenzaprine HCl sublingual) for fibromyalgia, expanding non-opioid options for widespread chronic pain.

- January 2025: The U.S. Food and Drug Administration approved Journavx (suzetrigine) 50 mg tablets, a first-in-class non-opioid analgesic for moderate to severe acute pain in adults.

Global Pain Management Market Report Scope

Pain is an unpleasant sensation in the body due to ongoing or impending tissue damage. Pain management includes therapies, drugs, and devices that help alleviate the pain. The pain management market is segmented by mode of pain management (drugs and devices), drugs is further sub-segmented by (opioids and non-narcotic analgesics), and non-narcotic is sub-sub-segmented by (non-steroidal anti-inflammatory drugs, anesthetics, anticonvulsants, anti-depressants, and other non-narcotic analgesics), devices is sub-segmented by (neurostimulation devices and analgesic infusion pumps), neurostimulation devices is sub-sub-segmented by (transcutaneous electrical nerve stimulation devices and brain and spinal cord stimulation devices), and analgesics infusion pumps is sub-sub-segmented by (intrathecal infusion pumps and external infusion pumps), by application (neuropathic pain, cancer pain, facial pain and migraine, musculoskeletal pain, and other applications), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Drugs | Opioids | |

| Non-narcotic Analgesics | NSAIDs | |

| Anesthetics | ||

| Anticonvulsants | ||

| Antidepressants | ||

| Devices | Neuro-modulation Devices | TENS |

| Spinal Cord Stimulation (SCS) | ||

| Dorsal Root Ganglion (DRG) | ||

| Vagus & Peripheral Nerve Stimulators | ||

| Analgesic Infusion Pumps | Intrathecal Pumps | |

| External PCA Pumps | ||

| Radio-frequency Ablation Systems | ||

| Neuropathic Pain |

| Cancer Pain |

| Musculoskeletal Pain |

| Facial Pain & Migraine |

| Post-operative & Acute Pain |

| Hospitals |

| Ambulatory Surgical Centers |

| Home-care & Remote Monitoring |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Mode of Pain Management | Drugs | Opioids | |

| Non-narcotic Analgesics | NSAIDs | ||

| Anesthetics | |||

| Anticonvulsants | |||

| Antidepressants | |||

| Devices | Neuro-modulation Devices | TENS | |

| Spinal Cord Stimulation (SCS) | |||

| Dorsal Root Ganglion (DRG) | |||

| Vagus & Peripheral Nerve Stimulators | |||

| Analgesic Infusion Pumps | Intrathecal Pumps | ||

| External PCA Pumps | |||

| Radio-frequency Ablation Systems | |||

| By Application | Neuropathic Pain | ||

| Cancer Pain | |||

| Musculoskeletal Pain | |||

| Facial Pain & Migraine | |||

| Post-operative & Acute Pain | |||

| By Setting of Care | Hospitals | ||

| Ambulatory Surgical Centers | |||

| Home-care & Remote Monitoring | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the pain management market?

The market generated USD 85.63 billion in 2026 and is projected to climb to USD 106.86 billion by 2031.

Which therapy class leads global revenue?

Pharmacological products remain dominant, contributing 68.92% of 2025 revenue.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 10.55% CAGR through 2031 due to healthcare digitization and rising incomes.

Which application is growing quickest?

Facial pain and migraine interventions are on track for an 8.67% CAGR, propelled by CGRP-based drugs and targeted neurostimulation.

How quickly are pain management devices advancing?

The devices category is projected to post a 9.99% CAGR between 2026 and 2031, led by closed-loop neuromodulation platforms.

Page last updated on: