Mexico AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

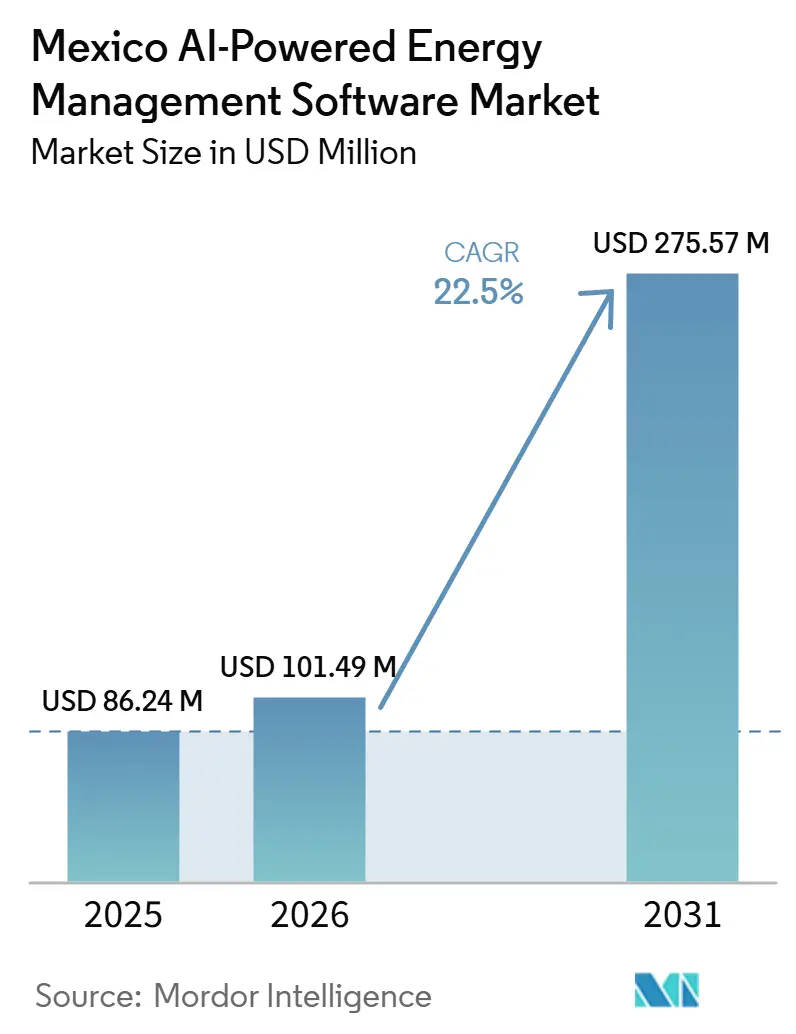

| Base Year Market Size (2025) | USD 86.24 Million |

| Market Size (2026) | USD 101.49 Million |

| Market Size (2031) | USD 275.57 Million |

| Growth Rate (2026 - 2031) | 22.50% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The Mexico AI-powered energy management software market size is projected to expand from USD 86.24 million in 2025 and USD 101.49 million in 2026 to USD 275.57 million by 2031, registering a CAGR of 22.50% between 2026 and 2031. Rising power tariffs under CFE time-of-use billing continue to make automated load planning and demand control financially relevant for industrial and commercial users. The March 2025 sector changes also increased the need for software that can help customers respond to changing grid rules, distributed resource management needs, and compliance demands within one operating layer. Nearshoring-led manufacturing growth in northern and central corridors is pushing more facilities to treat energy intelligence as an operating requirement instead of a secondary efficiency tool. Vendors are responding with broader platforms, stronger cloud delivery, and larger service capabilities that reduce deployment friction for multi-site customers. The clearest opportunities remain in applications tied to tariff optimization, renewable integration, reporting automation, and equipment-level control across facilities with rising electricity complexity.

Key Report Takeaways

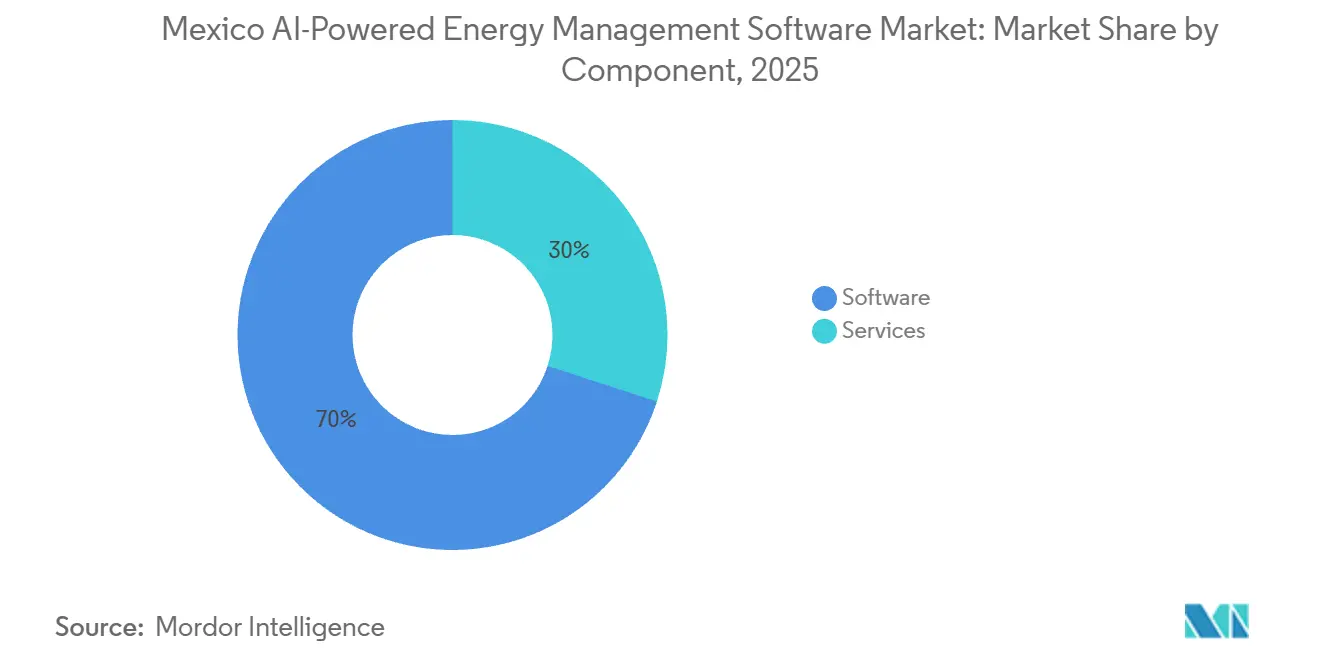

- By component, software led with 70.00% share of the Mexico AI-powered energy management software market in 2025, while services is projected to expand at a 25.00% CAGR through 2031.

- By deployment mode, cloud-based held 52.00% share of the Mexico AI-powered energy management software market in 2025 and is projected to record the highest CAGR at 25.40% through 2031.

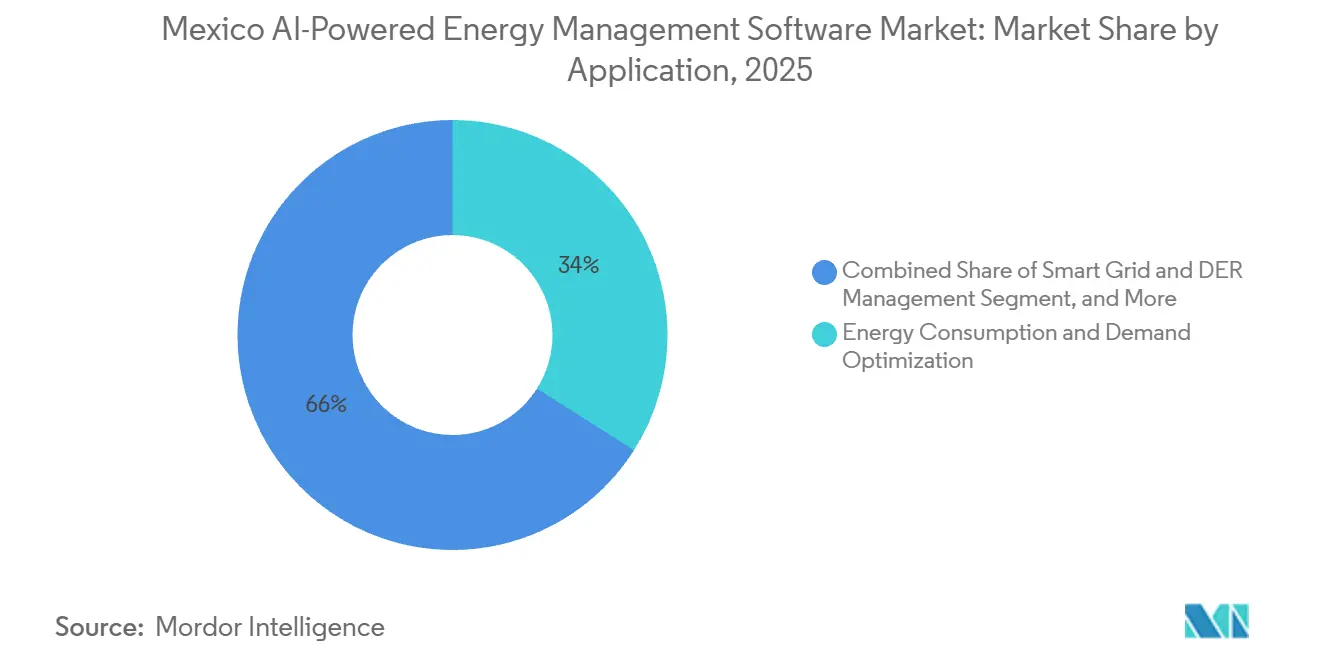

- By application, energy consumption and demand optimization accounted for 34.00% share in 2025, while renewable energy forecasting and integration is projected to grow at a 27.50% CAGR through 2031.

- By end user, industrial facilities held 34.00% share in 2025, while residential buildings is projected to advance at a 25.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Utility Tariffs and Time-of-Use Optimization Needs | +5.5% | National, with strongest ROI concentration in industrial GDMTH-tariff corridors of Nuevo León, Jalisco, and Querétaro | Short term (≤ 2 years) |

| Accelerating Building Electrification and Distributed Energy Resource Adoption | +4.8% | National, with highest DG density in Jalisco, Nuevo León, and Chihuahua | Medium term (2-4 years) |

| Utility-Grade Demand Response and Virtual Power Plant Integration | +4.0% | National, concentrated in grid-constrained Peninsular and Central SIN regions | Medium term (2-4 years) |

| Stricter Corporate Energy Reporting and Decarbonization Targets | +3.2% | National, with primary compliance demand among BMV-listed entities in Mexico City, Monterrey, and Guadalajara | Short term (≤ 2 years) |

| AI-Enabled Load Forecasting for Grid-Constrained Facilities | +2.5% | National, strongest demand in data center clusters and nearshoring parks | Medium term (2-4 years) |

| Edge Analytics for Real-Time Equipment-Level Energy Control | +1.8% | National, primary demand in manufacturing-dense states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Utility Tariffs and Time-of-Use Optimization Needs

CFE's GDMTH structure separates industrial charges by time block, which keeps electricity bills highly sensitive to when a facility consumes power. The 2026 tariff schedule maintained differentiated charges across these periods, which supports the business case for software that can actively schedule demand instead of only tracking historical use.[1]Comisión Federal de Electricidad, “Tarifas Finales del Suministro Básico a Partir del 1 de Enero de 2026,” Diario Oficial de la Federación, sidofqa.segob.gob.mx The Mexico AI-powered energy management software market benefits from this structure because many buyers can justify deployment through measurable cost control rather than through longer-term sustainability goals alone. Facilities with variable production schedules are especially exposed because monthly demand peaks can shift quickly when output, shift patterns, or order books change. That makes static audits less useful than continuous software-based optimization that can respond in real time. As a result, tariff management remains one of the clearest starting points for adoption across industrial corridors and larger commercial sites.

Accelerating Building Electrification and Distributed Energy Resource Adoption

The electrification shift is expanding the number of sites that need software to coordinate grid imports, rooftop solar, storage, and internal loads within a single control logic. Mexico's distributed energy resource framework is becoming more important for software demand because larger behind-the-meter systems now sit closer to day-to-day facility operations than they did before. Rule changes in April 2026 formally integrated battery storage into distributed generation provisions, which widened the optimization role for software beyond solar dispatch alone. The International Bar Association noted that distributed energy resource growth in Mexico will require at least a 50% expansion of electrical distribution networks, which reinforces the need for tools that can reduce unmanaged grid stress and improve operating decisions at the site level. The Mexico AI-powered energy management software market is therefore seeing stronger demand for platforms that can decide when to self-consume, store, or export power without relying on manual coordination. This demand is strongest where industrial parks, logistics facilities, and larger commercial sites are adding electrified equipment while also increasing their on-site energy assets.

Utility-Grade Demand Response and Virtual Power Plant Integration

Grid constraints are making flexible demand more valuable for utilities and large electricity users across Mexico. Uplight published Brattle Group findings in May 2026 showing that an integrated demand-stack approach could raise flexible capacity by 60% by 2030, from 146 MW to 235 MW for a representative utility.[2]Uplight, “New Brattle Group Report Shows Integrated Demand Stack Unlocks 60% More Peak Reduction Capability by 2030,” Uplight, uplight.com Peer-reviewed research published in PLOS One in January 2026 also showed that attention-augmented bidirectional LSTM models delivered stronger multi-timescale forecasting for virtual power plant operations than more conventional approaches. Better forecasting helps operators aggregate loads, plan curtailment, and respond to grid conditions with less disruption to site operations. The Mexico AI-powered energy management software market benefits because buyers increasingly want platforms that combine demand response, distributed resource coordination, and operating analytics instead of treating them as separate systems. This is strengthening the case for software that can turn flexible demand into an active grid-facing capability rather than a passive efficiency program.

Stricter Corporate Energy Reporting and Decarbonization Targets

Sustainability disclosure requirements are moving energy software spending closer to the compliance budget for listed and large private companies. Mexico's CNBV mandated IFRS S1 and IFRS S2 sustainability disclosures for all Bolsa Mexicana de Valores listed companies on January 28, 2025, with first reports covering FY2025 data due in 2026. Large issuers also face mandatory Scope 3 reporting from FY2026 data, which increases pressure on suppliers to provide better facility-level energy records to customers and corporate partners. Private companies reporting under Mexican Financial Reporting Standards also faced Sustainability Information Standards requirements from January 1, 2025, including disclosure of environmental indicators and Scope 1 and 2 emissions. The Mexico AI-powered energy management software market is therefore shifting toward platforms that can connect meter data, equipment data, and emissions logic without manual reconciliation. This also increases the value of audit trails, standardized outputs, and multi-site reporting workflows for customers that need both operational and disclosure-ready records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy Building Systems | -4.5% | National, especially acute in older industrial plants and government-owned facilities across all regions | Short term (≤ 2 years) |

| Cybersecurity and Data Governance Concerns | -3.2% | National, with heightened exposure in OT-IT convergence environments of utilities and industrial sectors | Medium term (2-4 years) |

| Limited In-House Analytics Capability Among Mid-Market Buyers | -2.5% | National, most acute in SME-heavy states outside major industrial corridors | Medium term (2-4 years) |

| Unclear Payback Periods for Advanced AI Features | -1.8% | National, primarily affecting mid-tier commercial and residential segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Building Systems

A large share of industrial and commercial facilities still run older building management and control systems that were not built for easy data exchange. This slows deployment because vendors must bridge proprietary signals, incomplete telemetry, and uneven sensor quality before analytics can create practical value. The International Bar Association also noted that Mexico's distributed energy resource expansion will require at least a 50% increase in distribution network capacity, which adds complexity when software must coordinate legacy site controls with changing grid interfaces. The Mexico AI-powered energy management software market, therefore, continues to rely heavily on integration, commissioning, and managed services even when software remains the larger revenue category. Vendors with prebuilt support for common protocols such as Modbus RTU and OPC UA are better positioned to shorten commissioning timelines and reduce buyer hesitation. This restraint is most visible in older plants and public facilities where modernization budgets are phased over several years.

Cybersecurity and Data Governance Concerns

Cybersecurity remains a meaningful barrier because these platforms aggregate real-time data from operating environments that utilities and industrial operators consider sensitive. GovInfoSecurity reported in February 2026 that an AI-assisted intrusion campaign targeted the operational technology environment of Monterrey's water utility, while the IT environment was fully compromised. Chambers and Partners stated in its 2026 Mexico guide that the country still lacked unified cybersecurity legislation for critical infrastructure operators, which left companies without a single sector-wide compliance benchmark for OT environments. This gap forces procurement teams to run their own security reviews, which extends vendor evaluations and raises due diligence demands. The Mexico AI-powered energy management software market is therefore seeing security credentials become a major buying criterion alongside analytics capability. Vendors that can demonstrate stronger readiness around ISO/IEC 27001 and IEC 62443 enter discussions with a clearer advantage when customers want deeper integration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Monetization Anchors Share as Services Spend Accelerates

Software captured 70.00% of the Mexico AI-powered energy management software market share in 2025, which kept the segment at the center of vendor monetization. That lead reflected buyer preference for recurring analytics subscriptions over one-time engineering projects, especially where tariff conditions and facility operating patterns change throughout the year. The segment also benefited from the fact that optimization, forecasting, visualization, and digital twin functions all depend on continuous updates rather than on a one-off system installation. In the Mexico AI-powered energy management software market, software remains the main delivery layer because users need active decision support instead of static efficiency reports. Schneider Electric's software-led grid and DER orchestration strategy shows how value is concentrating in platforms that combine visibility, forecasting, and control within one architecture

Services is projected to expand at a 25.00% CAGR through 2031, which confirms that implementation and optimization work will rise alongside license growth. This reflects a local reality where many Mexican facilities still combine older controls, mixed sensor estates, and multiple software layers that need hands-on integration before savings can be realized. Service demand also stays elevated because first-time buyers often need training, change management, and ongoing tuning support after the initial rollout. Johnson Controls' Metasys 15.0 launch in November 2025 showed how leading vendors are trying to reduce setup effort and speed the move from installation into active energy management. Even with that progress, the Mexico AI-powered energy management software market continues to generate meaningful service revenue because software value depends on how well local systems, equipment, and operational practices are connected.

By Deployment Mode: Cloud Infrastructure Leads Share and Pace Growth Simultaneously

Cloud-based deployment held 52.00% share in 2025 and is projected to grow at a 25.40% CAGR through 2031, which means the largest segment is also the fastest-growing segment. That pattern shows that migration from older on-premises systems is still active and that the market has not yet reached a stable deployment balance. In the Mexico AI-powered energy management software market, cloud delivery fits multi-site industrial groups, commercial portfolios, and industrial parks that need shared visibility without building local server infrastructure at every location. It also supports easier software updates, faster onboarding, and broader access for finance, operations, sustainability, and maintenance teams. ABB's 2026 launch of Ability BuildingPro Suites reflected continued vendor investment in unified environments that can connect building automation, energy, IT, and IoT systems in a scalable architecture.[3]ABB, “ABB Launches Ability BuildingPro Suites to Unify Building and IoT Systems for Data-Driven Performance,” ABB, new.abb.com

On-premises deployment still held a role for utilities and industrial operators that handled sensitive operational data or worked with connectivity constraints. Some buyers continue to prefer local control because they want tighter data custody or because parts of their operating environment require low-latency response without reliance on external networks. Hybrid models are also gaining traction because they allow local edge control for equipment response while moving historical analytics and reporting into a broader digital layer. This is especially relevant where facilities want fast operational control at the asset level but still need centralized reporting across several sites. The Mexico AI-powered energy management software market, therefore, supports multiple deployment paths, but demand continues to move toward options that preserve flexibility while reducing the complexity of long-term system administration.

By Application: Demand Optimization Holds Dominance While Renewable Forecasting Leads Growth

Energy consumption and demand optimization accounted for 34.00% share in 2025, giving it the largest application footprint in the Mexico AI-powered energy management software market. That leadership came from the direct link between CFE tariff complexity and the practical need to manage load timing across base, intermediate, and peak periods. Industrial buyers also favored this application because energy cost directly affects plant economics, contract performance, and site competitiveness under fixed-price supply arrangements. The application remains commercially strong because it addresses a day-to-day operating issue rather than a long-horizon strategic goal. Smart grid and distributed energy resource management is also gaining traction as buyers seek tools that can coordinate site-level assets with market-facing grid participation models.

Renewable energy forecasting and integration is projected to advance at a 27.50% CAGR through 2031, making it the fastest-growing application area. The Mexico AI-powered energy management software market is seeing faster expansion here because solar growth, storage integration, and larger clean energy flows all increase the value of accurate forecasting and automated balancing. This application also becomes more relevant as operators move from simple monitoring toward decisions on curtailment, load shaping, and power availability planning. C3 AI's expanded collaboration with Shell in June 2026 showed how enterprise users are placing greater weight on AI-driven reliability, root cause analysis, and predictive decision support across energy assets. That direction supports wider adoption of renewable forecasting tools not only for utilities, but also for industrial operators that need tighter coordination between power strategy, reliability, and operating performance.

By End User: Industrial Facilities Command Volume as Residential Uptake Accelerates

Industrial facilities held 34.00% share in 2025, making them the volume anchor of the Mexico AI-powered energy management software market. Their position reflected the concentration of energy-intensive manufacturing across nearshoring corridors where electricity cost, uptime, and throughput all influence site profitability. These users also tend to adopt broader software stacks because they need tariff control, predictive maintenance, and multi-site visibility at the same time. The operating case is strong because energy decisions in factories often affect production schedules, quality stability, and delivery timing, in addition to utility spend. Utilities remained strategically important as well because grid modernization and distributed asset coordination require software that can manage flexibility, visibility, and dispatch logic across larger networks.

Residential buildings is projected to grow at a 25.80% CAGR through 2031, which makes it the fastest-growing end-user segment. This growth is linked to rooftop solar adoption, rising awareness of high-consumption residential tariffs, and increasing interest in home systems that can automate energy use without constant manual oversight. Commercial buildings are also adding demand because sustainability reporting obligations and green-building standards are raising the value of verified performance data. Private-company sustainability reporting obligations in Mexico further support the need for stronger facility-level energy records across offices, mixed-use properties, and large building portfolios. The Mexico AI-powered energy management software market is therefore broadening beyond factories, even though industrial facilities remain the largest revenue pool.

Geography Analysis

The Mexico AI-powered energy management software market remained concentrated in the industrial north and the Bajio-Occidente corridor, where nearshoring, energy intensity, and digital readiness overlapped. Nuevo León accounted for 12% of Mexico's distributed generation capacity at the end of 2025, which supported stronger demand for load optimization and forecasting tools around Monterrey's industrial base. Chihuahua and Baja California also remained important because export-oriented manufacturing sites there operate with tight uptime and cost targets that favor equipment-level analytics and energy control. Northern states matter because electricity management there often sits close to plant profitability and delivery performance, not just to sustainability positioning. This pattern keeps the Mexico AI-powered energy management software market closely tied to manufacturing investment and grid pressure in border and industrial states.

Jalisco accounted for 17% of the nationally distributed generation capacity at the end of 2025, which gave the state the strongest link to renewable forecasting and distributed resource management demand. Mexico City showed a different demand profile because corporate headquarters, commercial buildings, and public facilities needed software that could combine tariff control with sustainability reporting. Querétaro also stood out as a growing center for intelligent electrification and energy-intensive digital infrastructure, which increased the need for forecasting, resilience planning, and multi-site oversight. The Mexico AI-powered energy management software market therefore expands through different local use cases, with Jalisco leaning into distributed assets, Mexico City into reporting and building efficiency, and Querétaro into industrial and data center performance.

The Yucatán Peninsula presented a more localized opportunity because grid constraints there made reliability and demand response software more relevant than in better-connected mainland areas. Pacific states such as Sonora and Sinaloa are also emerging demand pockets, where agri-industrial loads and cold-chain operations support early adoption of predictive maintenance and asset performance applications. CFE's transmission modernization program is expected to improve telemetry and grid visibility across regions, which should widen the addressable base for smarter grid-facing applications. As network observability improves, the Mexico AI-powered energy management software market is likely to see more activity beyond the main industrial clusters and into secondary demand centers with grid reliability needs.

Competitive Landscape

The Mexico AI-powered energy management software market remained fragmented at the product level, but platform consolidation is becoming easier to see as large automation vendors expand their software scope. Schneider Electric strengthened its position through continued EcoStruxure development and AutoGrid integration, which brought distributed energy orchestration and grid management functions closer together within one architecture. Honeywell's June 2025 launch of Honeywell Connected Solutions also showed a move toward unified platforms that combine energy management, predictive maintenance, cybersecurity monitoring, and remote diagnostics. ABB reinforced the same direction in 2026 with Ability BuildingPro Suites, which unified building automation, HVAC, energy, IT, and IoT controls in one environment. This gives large vendors an advantage when buyers want fewer integration points, stronger support depth, and clearer accountability for performance.

Even so, the Mexico AI-powered energy management software market still leaves room for specialists who can translate CFE tariff structures and Mexico-specific operating conditions into practical deployment models. Mid-market industrial operators outside the Monterrey, Guadalajara, and Querétaro triangle remain less fully served, especially when they need Spanish-language support and local integration depth rather than global templates. Another open space sits in emissions-native platforms that can connect sensor-level consumption data directly to greenhouse gas accounting workflows without requiring a separate reporting layer. This matters because many buyers increasingly want one operating system for energy cost control, equipment visibility, and disclosure readiness instead of several loosely connected applications.

Uplight's March 2026 majority stake acquisition by Octopus Energy showed that demand-side flexibility platforms are becoming a clearer competitive tier within the broader market. Schneider Electric's strategic investment in the same transaction underscored how established players are aligning with grid-edge software to deepen their reach in flexible demand. C3 AI's expanded work with Shell in June 2026 also signaled that enterprise customers continue to value AI tools that go beyond monitoring and support root cause analysis across operating assets.[4]C3 AI, “C3 AI and Shell Expand Collaboration, Scaling Reliability AI Deployment Across Global Asset Operations,” C3 AI, c3.ai The Mexico AI-powered energy management software market is therefore competitive across both building and grid use cases, with differentiation increasingly shaped by integration depth, analytics quality, deployment execution, and the ability to support local operating needs.

Mexico AI-Powered Energy Management Software Industry Leaders

AutoGrid Systems, Inc.

EnergyHub, Inc.

Uplight, Inc.

GridPoint, Inc.

C3.ai, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: C3 AI and Shell Information Technology International B.V. announced an expanded multi-year collaboration extending C3 AI Reliability across Shell's global operations, incorporating AI agent-based root cause analysis and predictive maintenance capabilities deployed on Microsoft Azure. The expansion signals growing enterprise confidence in agentic AI architectures for energy asset management.

- May 2026: Trane Technologies and BrainBox AI formally opened the BrainBox AI Lab in Montréal, dedicated to advancing AI-powered HVAC and building energy management R&D following Trane's January 2025 acquisition. The lab supports approximately 100 researchers developing autonomous building control systems capable of reducing energy consumption by up to 25% and GHG emissions by up to 40%.

- May 2026: Uplight and The Brattle Group published findings showing that an integrated demand-stack approach can grow flexible capacity by 60% by 2030 for a representative North American utility, providing a commercial case study for AI-driven demand response platforms targeting Mexico's grid-constrained industrial regions.

- March 2026: Schneider Electric launched EcoStruxure Foresight Operation, a unified platform controlling energy and building management systems in critical data center and industrial infrastructure environments, claiming up to 50% improvement in operational efficiency and 90% faster resolution of electrical-mechanical issues through AI-powered diagnostics.

Mexico AI-Powered Energy Management Software Market Report Scope

The Mexico AI-powered energy management software market comprises AI-driven software solutions and related services that optimize energy production, distribution, storage, and consumption through intelligent analytics, automation, and predictive modeling. These platforms leverage machine learning, artificial intelligence, digital twins, advanced forecasting, and real-time monitoring technologies to improve energy efficiency, enhance asset utilization, facilitate renewable energy integration, and support Canada's decarbonization and net-zero objectives.

The Mexico AI-Powered Energy Management Software Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the 2026 to 2031 outlook for the Mexico AI-powered energy management software market size?

The Mexico AI-powered energy management software market size is expected to move from USD 101.49 million in 2026 to USD 275.57 million by 2031, at a 22.50% CAGR.

Which component leads revenue generation in Mexico AI-powered energy management software?

Software led the component mix with a 70.00% share in 2025, supported by recurring analytics, forecasting, and optimization use cases across industrial and commercial sites.

Which deployment model is expanding the fastest in Mexico?

Cloud-based deployment held the largest share at 52.00% in 2025 and is also projected to post the fastest growth at a 25.40% CAGR through 2031.

What application area is creating the strongest current demand?

Energy consumption and demand optimization held the largest application share at 34.00% in 2025 because CFE tariff complexity makes active load management a direct cost-control tool.

Which end-user group is driving the largest volume of spending?

Industrial facilities led with a 34.00% share in 2025 because manufacturing sites need tariff management, uptime support, and multi-site visibility in one platform.

Why is renewable forecasting gaining so much traction in Mexico?

Renewable energy forecasting and integration is projected to grow at a 27.50% CAGR through 2031 as solar growth, storage integration, and grid constraints increase the need for automated balancing and better forward visibility.

Page last updated on: