SOFT Framework Implementation Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

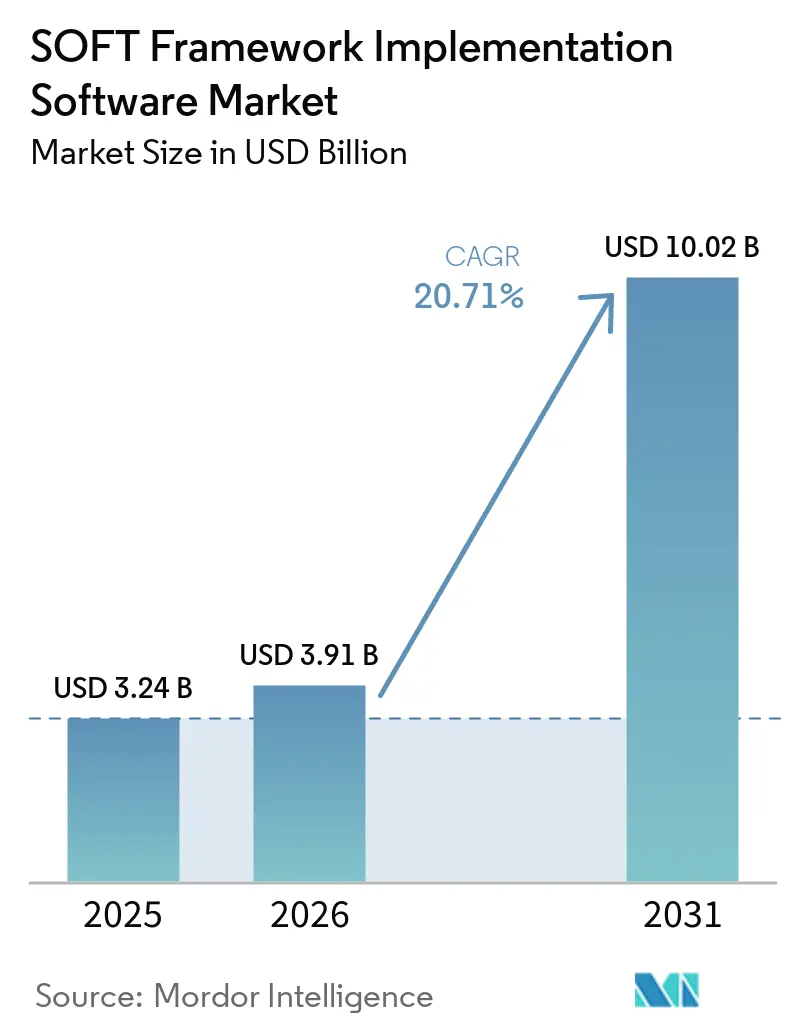

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 10.02 Billion |

| Growth Rate (2026 - 2031) | 20.71% CAGR |

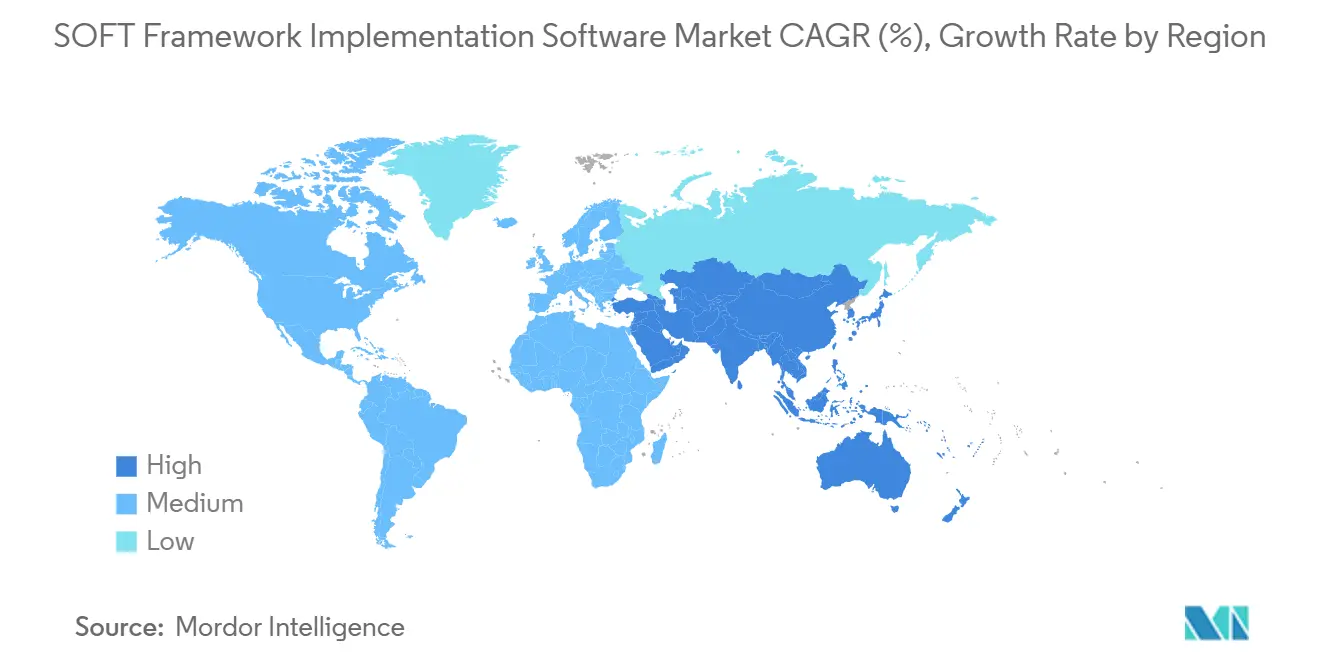

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SOFT Framework Implementation Software Market Analysis by Mordor Intelligence

The SOFT Framework implementation software market size was valued at USD 3.24 billion in 2025 and estimated to grow from USD 3.91 billion in 2026 to reach USD 10.02 billion by 2031, at a CAGR of 20.71% during the forecast period (2026-2031). Growth is being supported by the move from broad sustainability commitments to more structured software programs that can be mapped to strategy, implementation, operational, and compliance needs across large organizations. Demand is also rising because disclosure rules, audit expectations, and supply chain reporting needs now require traceable workflows instead of manual spreadsheets and isolated tools. The market is also benefiting from the way sustainability metrics are being linked more closely with ERP, procurement, finance, and operations systems, which is widening software scope beyond reporting alone. Vendors are responding by pairing software modules with implementation services, training, and managed support, which is raising contract depth and expanding opportunities after the first deployment. Competitive activity remains active because large enterprise software vendors are using installed bases to extend sustainability offerings, while specialist providers are competing on methodology depth, workflow coverage, and more focused execution.

Key Report Takeaways

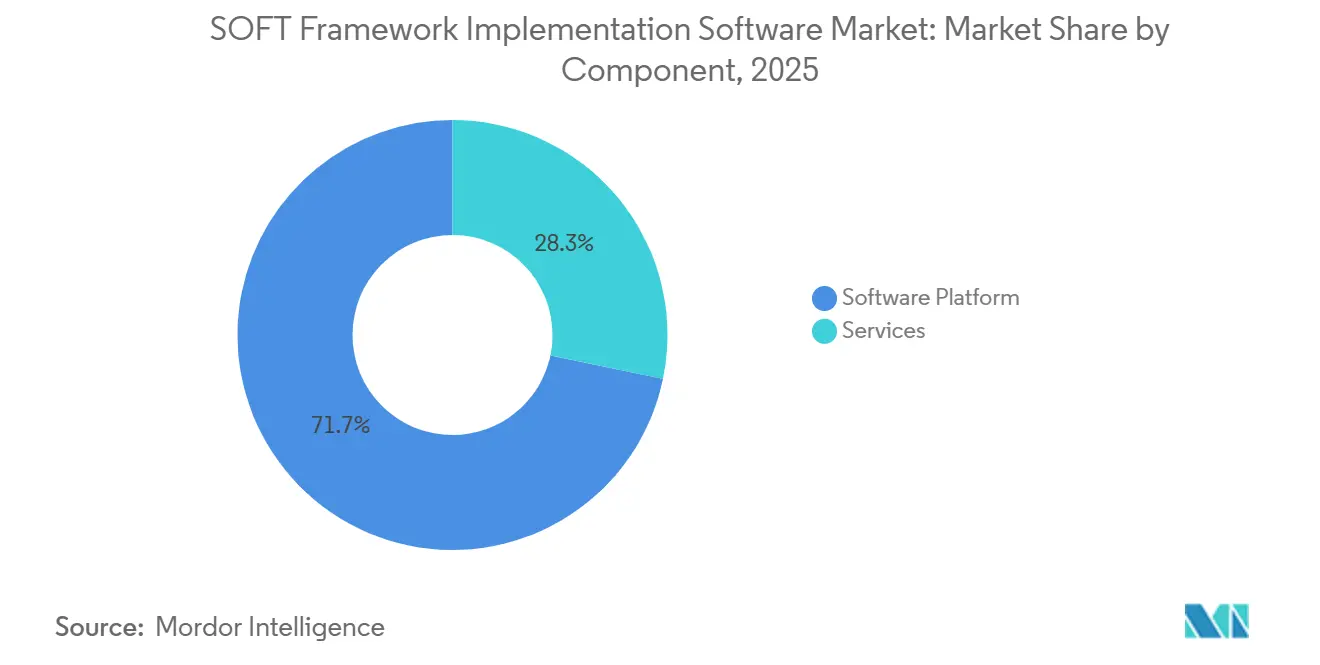

- By component, software platforms held 71.73% share in 2025 in the SOFT framework implementation software market, while services are projected to expand at a 24.67% CAGR through 2031.

- By deployment mode, cloud-based deployments held 74.15% share in 2025, while on-premise deployments are projected to grow at an 18.83% CAGR through 2031.

- By organization size, large enterprises held 52.46% share in 2025, while small and medium enterprises are projected to expand at a 21.77% CAGR through 2031.

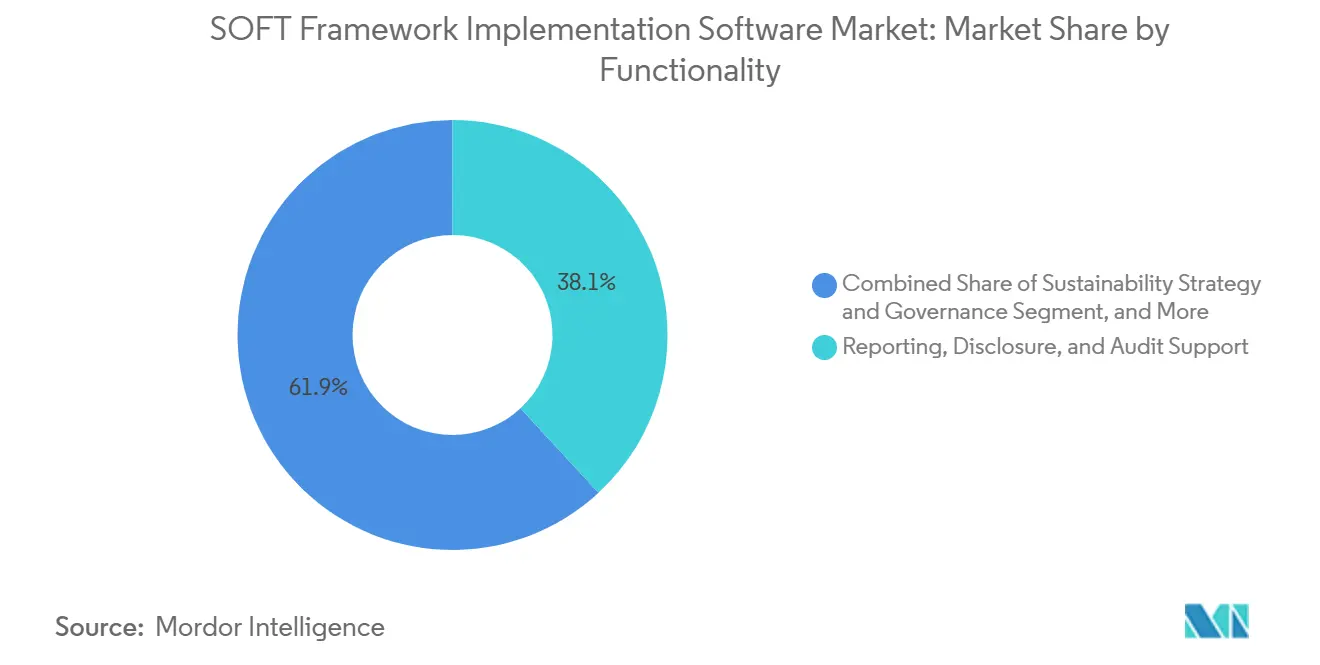

- By functionality, reporting, disclosure, and audit support accounted for 38.11% share in 2025, while strategy and governance management is projected to advance at a 21.43% CAGR through 2031.

- By end-user industry vertical, energy and utilities held 26.55% share in 2025, while manufacturing is projected to grow at a 22.19% CAGR through 2031.

- By geography, North America held 36.64% of the SOFT framework implementation software market share in 2025, while Asia-Pacific is projected to expand at a 23.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SOFT Framework Implementation Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Enterprise Demand for Framework-Led Sustainability Governance | +4.8% | Global | Medium term (2-4 years) |

| Regulatory Pressure for Audit-Ready ESG and Carbon Reporting | +4.2% | North America and EU, spill-over to APAC and Middle East and Africa | Short term (≤ 2 years) |

| Integration of Sustainability Metrics into Core Business Workflow | +3.5% | Global, with early gains in North America, Germany, and Japan | Medium term (2-4 years) |

| Shift Toward Automated Data Collection and Continuous Monitoring | +2.8% | Global | Medium term (2-4 years) |

| Expansion of Procurement-Led Scope 3 Accountability | +2.1% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Need for Cross-Functional Decarbonization Planning Across IT and Operations | +1.6% | Global, with early gains in European manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Demand for Framework-Led Sustainability Governance

The November 2025 ratification of the SOFT framework has given the SOFT Framework implementation software market a clearer structure for enterprise adoption and procurement. The framework organizes sustainability work across strategy, implementation, operations, and compliance domains, providing buyers with a common structure for evaluating software needs rather than relying on fragmented internal requirements. This matters because software selection is no longer centered only on carbon accounting or disclosure tools, and it is moving toward broader programs that support governance, execution, and compliance together. The framework was also shaped with input from major enterprise participants, which improves its credibility in procurement discussions and supports the SOFT Framework implementation software market as larger organizations standardize vendor requirements. The planned development of SOFT v2.0, following live pilots at global organizations, also points to a market moving from framework introduction into a more commercial implementation phase

Regulatory Pressure for Audit-Ready ESG and Carbon Reporting

The SOFT Framework implementation software market is also being boosted by regulation, as reporting obligations now require more consistent data, stronger controls, and clearer audit trails. The European Union brought CSRD into force for large public-interest entities for the 2024 financial year, with reporting published in 2025, which pushed many organizations to strengthen their sustainability reporting systems.[1]European Commission, “Corporate Sustainability Reporting,” European Commission, ec.europa.eu The 2025 shift in the SEC position reduced one source of federal pressure in the United States, but it did not remove the need for structured reporting tools because large enterprises still face investor, customer, and state-level disclosure demands.[2]U.S. Securities and Exchange Commission, “SEC Climate Disclosure Rule Litigation Update,” U.S. Securities and Exchange Commission, sec.gov The SOFT Framework implementation software market is benefiting from limited-assurance-style requirements that place greater weight on methodology documentation, data lineage, and version control, which are difficult to manage in spreadsheet-based workflows. The result is that many buyers are treating audit readiness as the starting point for software adoption, and that continues to support near-term demand in the SOFT Framework implementation software market.

Integration of Sustainability Metrics into Core Business Workflows

A major growth factor for the SOFT Framework implementation software market is the shift from stand-alone sustainability reporting toward integration with core business systems. When sustainability data flows through ERP, procurement, asset management, and finance systems, it becomes part of operational decisions rather than a year-end reporting exercise. SAP reinforced this direction in May 2026 when it announced sustainability AI agents, including a Footprint Optimization Agent designed to reduce scenario simulation time and a Packaging Compliance Agent designed to cut manual review work. This kind of product development supports the market for software implementing the SOFT Framework because buyers increasingly want sustainability features within familiar enterprise software environments rather than as disconnected overlays. As organizations move in this direction, the commercial value of implementation expands from disclosure support into planning, workflow management, and continuous performance use cases.

Shift Toward Automated Data Collection and Continuous Monitoring

The SOFT Framework implementation software market is also growing because manual ESG and emissions data processes do not scale well as reporting expectations expand. Large organizations need more granular data across facilities, suppliers, and business units, and that creates pressure to automate collection, validation, and monitoring. The need is even greater when software must support ongoing audit review, because repeated manual inputs weaken consistency and make it harder to manage methodology controls. SAP's May 2026 launch updates showed how automation is moving beyond simple data capture into scenario analysis and compliance review workflows, thereby raising the operational value of these platforms. In practice, this means the SOFT Framework implementation software market is increasingly being sold as a control and workflow platform rather than just a reporting tool. That broader role strengthens renewal potential and increases the relevance of software across more internal teams.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Enterprise Data and Inconsistent Emissions Methodologies | -2.2% | Global | Medium term (2-4 years) |

| Limited Internal Ownership Across Sustainability, Finance, and IT Teams | -1.8% | Global, with acute gaps in South America and Africa | Medium term (2-4 years) |

| High Integration Effort With Legacy ERP and Workflow Systems | -1.4% | Global, concentrated in large manufacturing and utilities enterprises | Long term (≥ 4 years) |

| Budget Scrutiny for Non-Revenue Software Programs | -1.0% | Global, intensified in markets with delayed regulatory timelines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Enterprise Data and Inconsistent Emissions Methodologies

Data fragmentation remains a significant brake on the implementation of the SOFT Framework in software markets because sustainability information often resides across ERP systems, procurement tools, HR systems, utility records, and facility platforms. Even when enterprises invest in software, they still need to harmonize source systems, boundaries, calculation rules, and governance practices before outputs are reliable. The challenge becomes more serious when reporting moves beyond Scope 1 and Scope 2 into supplier-related Scope 3 categories, where primary data is often missing or inconsistent. The SOFT framework addresses implementation and compliance requirements, but turning that guidance into standardized operating data across legacy systems still takes time and specialist effort. This slows deployment speed, raises delivery complexity, and can delay expansion phases in the SOFT Framework implementation software market.

Limited Internal Ownership Across Sustainability, Finance, and IT Teams

The SOFT Framework implementation software market also faces friction because ownership often sits across sustainability teams, finance functions, and IT departments that do not share the same priorities or budgets. Sustainability teams usually define metrics, finance teams focus on reporting and assurance, and IT teams control systems, architecture, and integration choices. When these functions are not aligned, projects can stall after vendor selection and before enterprise-wide rollout. The SOFT framework itself reflects cross-functional governance needs, which means implementation is strongest when organizations have clear leadership and executive sponsorship behind the program. Without that structure, the SOFT Framework implementation software market can see longer deployments, lower tool utilization, and weaker follow-on revenue from broader module adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Lead While Services Deepen Engagement

Software platforms accounted for 71.73% of the SOFT Framework implementation software market in 2025, reflecting earlier investment by large enterprises in core sustainability data management and reporting infrastructure. The leading role of software platforms is tied to the need for multi-framework support, centralized data models, and consistent workflows across strategy, implementation, operational, and compliance functions. The SOFT Framework implementation software market has favored broader platforms, as buyers seek to reduce duplication across reporting, carbon accounting, and governance activities. That preference becomes even stronger when enterprises operate across multiple jurisdictions and need a single system that supports multiple internal teams.

Services are projected to grow at a 24.67% CAGR between 2026 and 2031, making them the fastest-expanding part of the SOFT Framework implementation software market. This reflects a shift from initial license deployment toward implementation support, training, managed services, and guided rollout work as programs become more complex. IFS supported this direction in May 2026 with the launch of IFS Zero, an emissions operating system built for asset-intensive sectors, demonstrating how vendors are combining software capabilities with deeper operational use cases.[3] IFS, “IFS Zero Launch Announcement,” IFS, ifs.com The SOFT Framework implementation software industry is moving toward a model in which long-term value depends not only on product breadth but also on the ability to support execution across live enterprise environments.

By Deployment Mode: Cloud Leads While On-Premise Demand Remains Structural

Cloud-based deployment accounted for 74.15% of the market in 2025, indicating that most buyers in the SOFT Framework implementation software market still prefer scalable, centrally managed systems. Cloud deployment supports faster rollout across subsidiaries, easier updates, and wider access for teams working across different locations. It also aligns well with organizations that need a single record system for reporting, analytics, and supplier collaboration, without maintaining separate local infrastructure. For many enterprises, cloud remains the default starting point because it shortens implementation time and enables more efficient multi-entity reporting.

On-premise deployment is projected to grow at a 18.83% CAGR through 2031, indicating that the SOFT Framework implementation software market is not moving toward a cloud-only model. Data sovereignty requirements, cybersecurity concerns, and procurement preferences in regulated sectors such as government, utilities, and finance are supporting demand. Hybrid architectures also remain relevant because some organizations want sensitive operational data under tighter local control while using cloud environments for analytics and reporting workflows. This creates a more layered deployment picture, and it means vendors in the SOFT Framework implementation software market need flexibility across cloud, on-premises, and hybrid models to address the full enterprise opportunity.

By Organization Size: Large Enterprises Set the Base While SMEs Expand Faster

Large enterprises held 52.46% of the market in 2025, making them the largest spenders in the SOFT Framework implementation software market. Their lead reflects earlier investment cycles, larger compliance exposure, dedicated sustainability teams, and procurement capacity for multi-module platforms. Many large organizations had already deployed sustainability tools before SOFT was ratified, and they are now in a position to align existing systems with the framework's broader domain structure. This makes large enterprises the main installed base for upgrades, integrations, and service-led expansion in the SOFT Framework implementation software market.

Small and medium enterprises are projected to grow at a 21.77% CAGR through 2031, and that gap is narrowing as software delivery becomes more accessible. The VSME-related direction in Europe and supply chain reporting pressure from larger buyers are making structured sustainability data management more relevant for smaller firms. ASUENE's 2026 launch of SSBJ and CSRD-compliant financial impact management services shows how newer platforms are targeting practical adoption needs with tools that can suit a broader customer base.[4]ASUENE, “Financial Impact Management Service Announcement,” ASUENE, asuene.com The SOFT Framework implementation software market is also attracting SMEs through supplier obligations, as large enterprises increasingly need better upstream data from partner networks rather than relying solely on direct operations.

By Functionality: Disclosure Anchors Spending While Governance Gains Weight

Reporting, disclosure, and audit support accounted for 38.11% of the SOFT Framework implementation software market share in 2025, which confirms that compliance-related workflows remain the main entry point for adoption. This segment stays central because organizations need traceable data pipelines, structured outputs, and documentation that can support disclosure obligations and internal review. The first years of CSRD application strengthened this pattern by pushing larger companies to improve systems for report preparation and data control. As a result, the SOFT Framework implementation software market continues to rely on disclosure-led demand as the foundation of current spending.

Strategy and governance management is projected to grow at a 21.43% CAGR through 2031, which shows that the SOFT Framework implementation software market is broadening beyond reporting alone. This area gains relevance when boards and executive teams want sustainability embedded into planning, oversight, target setting, and cross-functional management processes. The SOFT framework explicitly includes strategy as a core domain, which supports this shift toward more formal governance software and longer-term decision support. The SOFT Framework implementation software industry therefore has an opportunity to capture more durable value in governance workflows, because these functions are harder to replace than basic reporting tools once they are tied to management routines.

By End-User Industry Vertical: Energy And Utilities Lead While Manufacturing Accelerates

Energy and utilities held 26.55% of the market in 2025, making the segment the largest vertical in the SOFT Framework implementation software market. This reflects the sector's direct exposure to emissions tracking, decarbonization planning, investor scrutiny, and infrastructure-related reporting needs. Sustainability software in this vertical is expected to support operational detail, project transparency, and standardized environmental measurement across large physical assets. Hitachi Energy reinforced this need in April 2026 when it launched EcoSpace for power grid projects using a DNV-endorsed methodology to quantify and visualize environmental footprints.

Manufacturing is projected to grow at a 22.19% CAGR through 2031, making it the fastest-growing vertical in the SOFT Framework implementation software market. Growth comes from product carbon footprint requirements, supply chain disclosure needs, and pressure to manage purchased goods and services emissions with greater precision. NTT's March 2026 development of CO2 calculation rules for software products across procurement, development, operation, and disposal shows how lifecycle-based accounting is becoming more structured and more operational. The SOFT Framework implementation software market is therefore becoming more important in manufacturing because emissions data is moving closer to product design, procurement, and supplier coordination rather than remaining inside broad annual reporting cycles.

Geography Analysis

North America held 36.64% of the SOFT Framework implementation software market share in 2025, making it the leading regional segment by current revenue. The region benefits from a mature base of large enterprises, stronger familiarity with sustainability software categories, and a deeper professional services ecosystem that can support implementation. The United States remains central because many large organizations have already built governance programs that can be extended into broader SOFT-aligned software deployment. California-related disclosure requirements also help sustain demand for structured reporting and emissions management even after the SEC stepped back from defending its climate disclosure rule in 2025. This leaves North America with a relatively advanced adoption curve in the SOFT Framework implementation software market, especially among enterprises with broad compliance exposure and complex operating footprints.

Europe remains a structurally important region in the SOFT Framework implementation software market because disclosure requirements continue to shape enterprise procurement behavior. CSRD application for large public-interest entities reporting financial year 2024 data in 2025 created a direct need for stronger disclosure systems, documentation, and audit-ready workflows. That demand is not limited to the largest companies, because smaller supplier networks are also being affected by broader sustainability information requirements tied to enterprise reporting chains. Germany stands out as a strong deployment environment because regulated sectors and industrial supply chains both require more structured and locally trusted reporting infrastructure. South America is at an earlier stage, but multinational exposure to European reporting expectations is creating preparatory demand that supports gradual entry into the SOFT Framework implementation software market.

Asia-Pacific is projected to expand at a 23.17% CAGR through 2031, giving it the fastest regional growth rate in the SOFT Framework implementation software market. Japan is a key driver because disclosure standards, enterprise digitalization, and technology-led sustainability programs are advancing in parallel. NTT's March 2026 work on software product CO2 calculation rules shows the depth of operational focus that is now emerging in Japan's sustainability management environment.[5]NTT, “CO2 Emission Calculation Rules For Software Products,” NTT, group.ntt ASUENE's 2026 service launch also indicates that domestic platforms are aligning offerings to local and international disclosure expectations, which supports wider adoption among mid-sized enterprises. Across the broader region, ISSB-aligned disclosure efforts in markets such as Singapore, Australia, and South Korea are helping create a stronger long-term base for the SOFT Framework implementation software market. The Middle East and Africa remain earlier-stage opportunities, but national sustainability frameworks and governance-led disclosure expectations are beginning to build demand in selected countries. This keeps the geographic outlook broadening even though regional maturity still differs widely.

Competitive Landscape

The SOFT Framework implementation software market has a moderately concentrated structure, with competition shaped by both large enterprise software vendors and specialist sustainability providers. Microsoft Corporation, SAP SE, IBM Corporation, and Salesforce, Inc. benefit from installed enterprise relationships and from the ability to place sustainability tools inside broader business software environments. That approach helps them reduce switching friction and expand contract value through integration with existing ERP, cloud, workflow, and analytics systems. The SOFT Framework implementation software market also includes purpose-built vendors such as Workiva Inc., Sphera Solutions, Inc., Persefoni AI, Inc., Watershed Technology, Inc., Normative AB, and others that compete on regulatory depth, carbon accounting detail, and audit-oriented workflows.

Large platform vendors are strengthening their position through product development that extends sustainability features deeper into day-to-day enterprise systems. SAP's May 2026 announcement of sustainability AI agents is a clear example because it tied emissions optimization and compliance tasks more closely to business process software rather than leaving them as stand-alone reporting tools. In the SOFT Framework implementation software market, that strategy matters because enterprise buyers often favor vendors that can connect sustainability data with procurement, packaging, finance, and scenario planning in one operating environment. Microsoft, IBM, and Salesforce continue to benefit from this same logic because broad software stacks create an advantage when customers want fewer platforms and tighter integration across functions.

Specialist vendors are still important because they often move faster in focused use cases and can offer more direct workflow coverage in areas such as Scope 3, product footprints, and multi-framework reporting. Makersite's acquisition of Siemens' SiGREEN platform, effective June 1, 2026, is a strong example of how the SOFT Framework implementation software market is evolving through capability expansion around supply chain carbon data exchange. Hitachi Energy's EcoSpace launch also shows that sector-focused players can compete by building software for specific operational settings rather than trying to match broad platform suites feature for feature. Fujitsu's May 2026 launch of an AI-based non-financial information disclosure analysis service in Japan points to a similar move toward targeted reporting and disclosure support in local enterprise contexts. White space remains in the SOFT Framework implementation software market around real-time carbon-aware deployment, green procurement workflow automation, and developer-level emissions tracking tied to DevOps. That means the competitive field is still open enough for focused entrants, even as larger vendors strengthen their reach through integration and installed-base leverage.

SOFT Framework Implementation Software Industry Leaders

Microsoft Corporation

SAP SE

International Business Machines Corporation

Salesforce, Inc.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Makersite announced the acquisition of SiGREEN, Siemens' product carbon footprint and supply chain data exchange platform, effective June 1, 2026. SiGREEN powers the Together for Sustainability PCF Exchange, connecting chemical and industrial sector supply chains, and natively supports TfS, Catena-X, and PACT data exchange frameworks. The transaction significantly strengthens Makersite's Scope 3 and product carbon footprint capabilities for manufacturers.

- May 2026: SAP announced that new sustainability AI agents, including a Footprint Optimization Agent that reduces scenario simulation time from approximately 1 day to roughly 20 minutes and a Packaging Compliance Agent that delivers an over 50% reduction in manual compliance review hours, will reach general availability by the the end of 2026.

- May 2026: Fujitsu launched an AI-based non-financial information disclosure analysis service in Japan, using AI trained on disclosures from over 1,000 Japanese listed companies to help enterprises improve ESG evaluation outcomes and support strategic sustainability reporting aligned with SSBJ standards.

- April 2026: Hitachi Energy launched EcoSpace, a digital sustainability platform for power grid projects, at WindEurope in Madrid. The platform uses a DNV-endorsed methodology to quantify and visualize the environmental footprint of energy infrastructure, addressing transparency needs for utilities, grid developers, and institutional investors.

Global SOFT Framework Implementation Software Market Report Scope

SOFT Framework Implementation Software refers to a category of enterprise sustainability platforms designed to help organizations adopt the SOFT (Sustainable Organizational Framework for Technology) model. This software enables businesses to integrate carbon accounting, ensure ESG compliance, automate workflows, and manage sustainability data within their IT and operational processes. It facilitates audit-ready reporting, ensures regulatory compliance, and drives measurable progress toward achieving decarbonization objectives.

The SOFT Framework Implementation Software Market Report is Segmented by Component (Software Platform, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Functionality (Sustainability Strategy and Governance, Data Management and Collection, Carbon and Environmental Accounting, Reporting and Disclosure Management, Workflow and Performance Management, and Platform Integration and Analytics), End-User Industry Vertical (Energy and Utilities, Manufacturing, BFSI, IT and Telecommunications, Retail and Consumer Goods, Healthcare and Life Sciences, Transportation and Logistics, Government and Public Sector, and Other End-User Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software Platform |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Sustainability Strategy and Governance |

| Data Management and Collection |

| Carbon and Environmental Accounting |

| Reporting and Disclosure Management |

| Workflow and Performance Management |

| Platform Integration and Analytics |

| Energy and Utilities |

| Manufacturing |

| BFSI |

| IT and Telecommunications |

| Retail and Consumer Goods |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Government and Public Sector |

| Other End-User Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Singapore | |

| Rest of Asia-pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Software Platform | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Functionality | Sustainability Strategy and Governance | |

| Data Management and Collection | ||

| Carbon and Environmental Accounting | ||

| Reporting and Disclosure Management | ||

| Workflow and Performance Management | ||

| Platform Integration and Analytics | ||

| By End-User Industry Vertical | Energy and Utilities | |

| Manufacturing | ||

| BFSI | ||

| IT and Telecommunications | ||

| Retail and Consumer Goods | ||

| Healthcare and Life Sciences | ||

| Transportation and Logistics | ||

| Government and Public Sector | ||

| Other End-User Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the SOFT Framework implementation software market?

The SOFT Framework implementation software market was valued at USD 3.24 billion in 2025 and is estimated at USD 3.91 billion in 2026, with projected growth to USD 10.02 billion by 2031 at a 20.71% CAGR.

What is driving growth in SOFT Framework implementation software?

Growth is being supported by structured sustainability governance, rising demand for audit-ready ESG and carbon reporting, stronger integration with core business workflows, and the move toward automated data collection and monitoring.

Which deployment model leads adoption?

Cloud-based deployment led with 74.15% share in 2025 because enterprises value scalability, centralized management, and faster rollout across entities and regions.

Which customer group is expanding the fastest?

Small and medium enterprises are projected to grow at a 21.77% CAGR through 2031 as implementation tools become more accessible and large-company supply chain requirements push structured reporting into supplier networks.

Which functional use case is most established today?

Reporting, disclosure, and audit support held the largest functionality share at 38.11% in 2025 because compliance and audit readiness remain the main entry point for enterprise adoption.

Which regions are most important for future expansion?

North America remained the largest regional segment with 36.64% share in 2025, while Asia-Pacific is expected to grow the fastest at a 23.17% CAGR through 2031 as disclosure standards and enterprise digitalization advance across the region.

Page last updated on: