Europe Creative Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

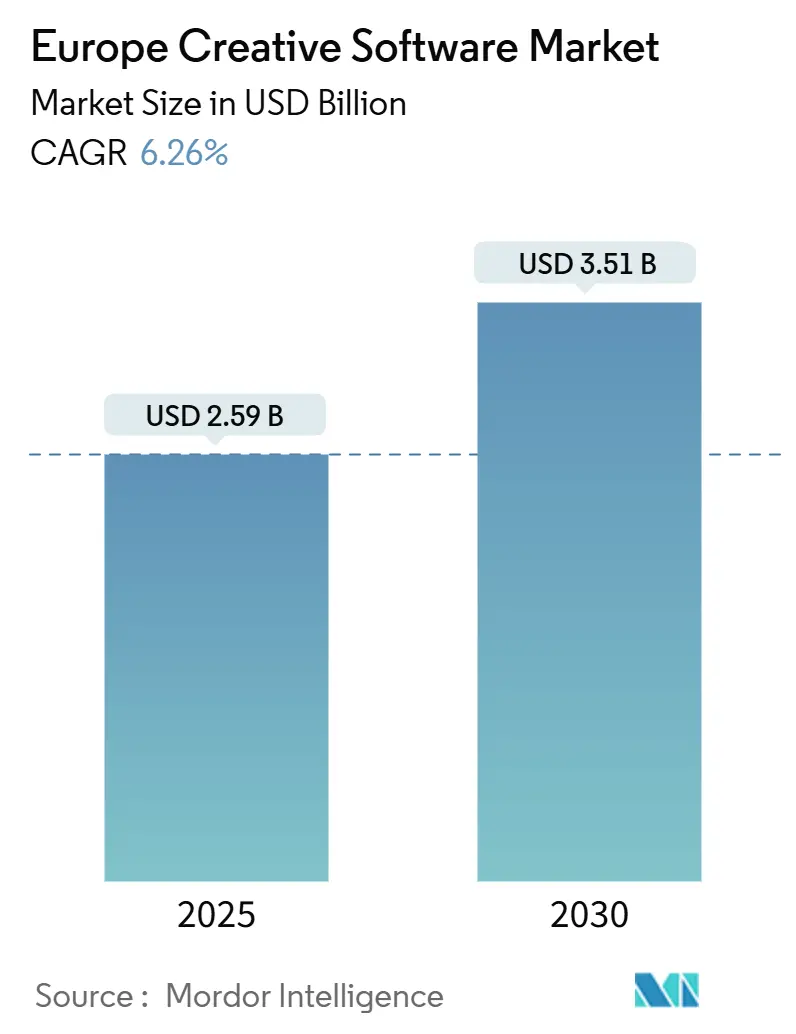

| Market Size (2025) | USD 2.59 Billion |

| Market Size (2030) | USD 3.51 Billion |

| Growth Rate (2025 - 2030) | 6.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Creative Software Market Analysis by Mordor Intelligence

The Europe Creative Software market size is estimated at USD 2.59 billion in 2025 and is projected to reach USD 3.51 billion by 2030, growing at a 6.26% CAGR from 2025 to 2030. This outlook reflects enterprises’ firm pivot toward subscription pricing, the rapid diffusion of generative AI across design workflows, and surging demand from small and medium enterprises that previously relied on lower-tier tools. Continuous cloud migration, deeper 3D content pipelines for media and gaming, and EU-backed digitization grants are expanding the addressable market, while open-source alternatives help keep price sensitivity in check. Market leaders differentiate themselves through ecosystem breadth and AI roadmaps, whereas challengers focus on intuitive interfaces that shorten the learning curve. Data-residency compliance now influences vendor selection, particularly following the Schrems II ruling, prompting some companies to favor EU-hosted clouds.

Key Report Takeaways

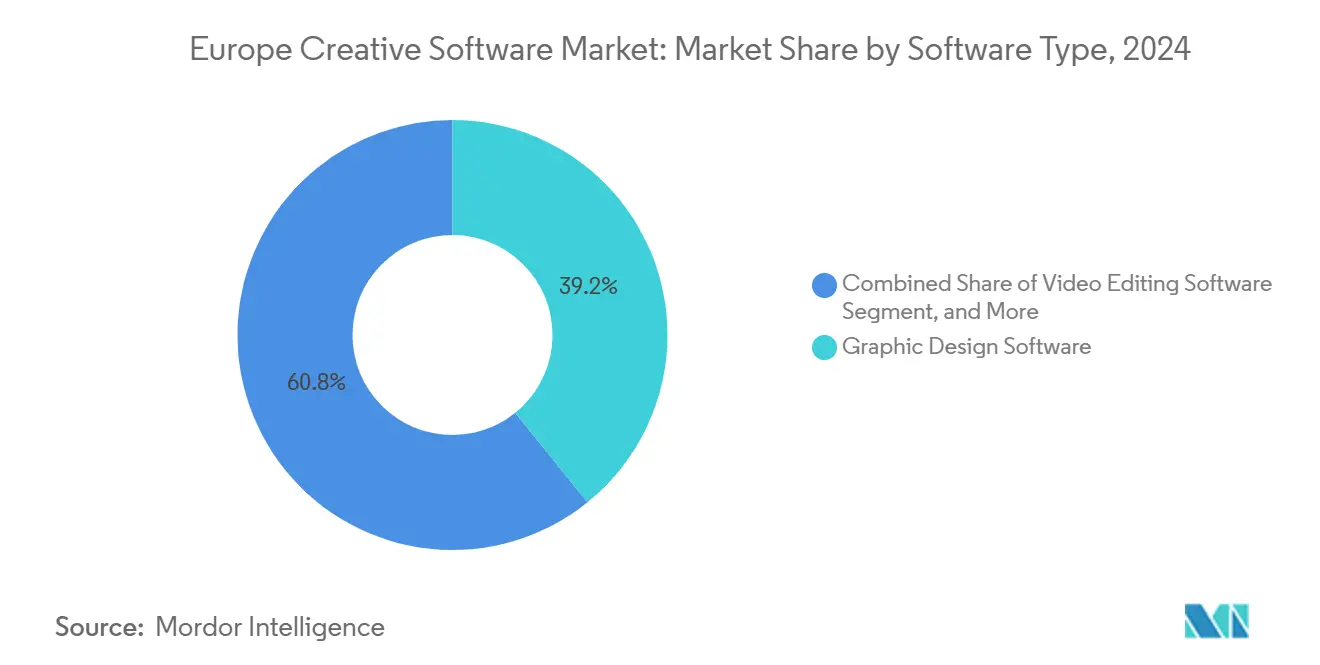

- By software type, graphic design software accounted for 39.19% of the Europe Creative Software market share in 2024; 3D Modeling and Animation Software is projected to advance at a 7.29% CAGR through 2030.

- By deployment mode, cloud-based platforms captured 56.11% of the Europe Creative Software market share in 2024 and are forecast to expand at a 6.77% CAGR.

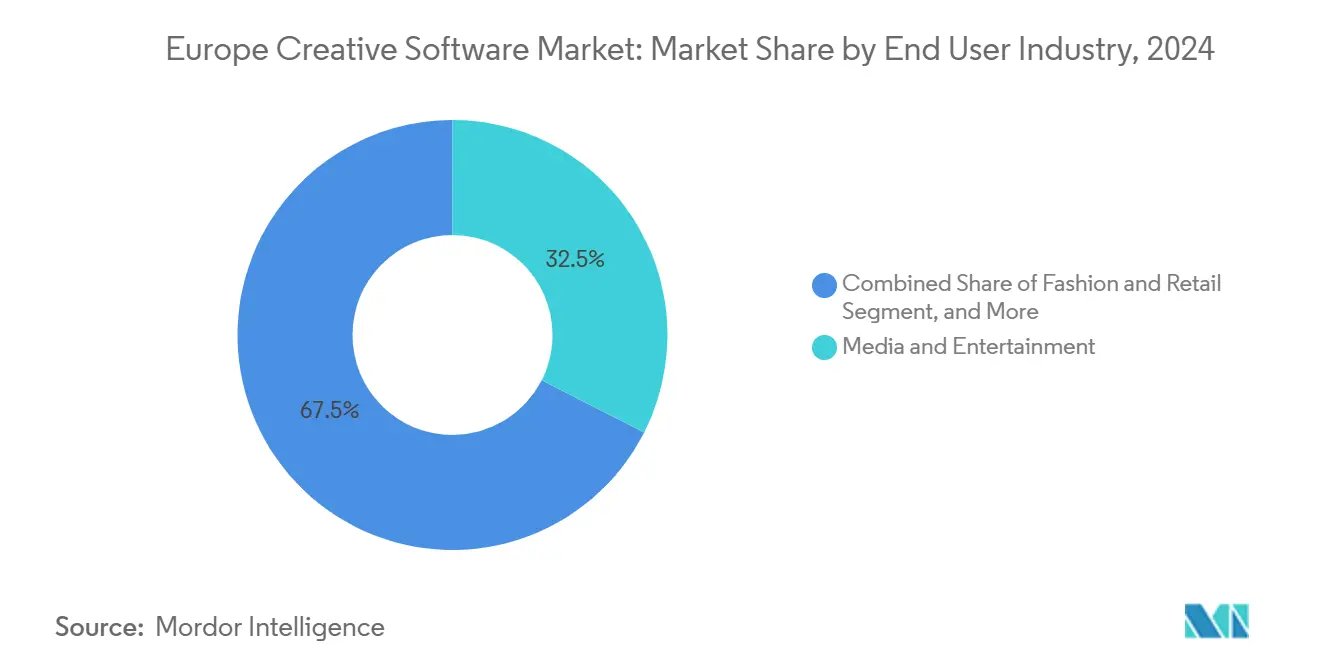

- By end-user industry, the media and entertainment sector generated 32.49% of the Europe Creative Software market share in 2024, whereas the fashion and retail sector is set to grow at a 7.31% CAGR through 2030.

- By revenue model, subscription-based services generated 63.74% of the Europe Creative Software market share in 2024, whereas freemium and in-app purchases are set to grow at a 6.86% CAGR through 2030.

- By country, Germany commanded 19.82% of the Europe Creative Software market share in 2024, while Poland is expected to register a 7.14% CAGR during 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Creative Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Subscription-Based Creative Suites | +1.2% | Europe-wide, strongest in Germany, UK, France | Medium term (2-4 years) |

| Surge in Digital Content Creation Among SMEs | +1.1% | Europe-wide, accelerated in Poland, Nordic countries | Short term (≤ 2 years) |

| Rising Demand for 3D Animation in Gaming and Media | +0.9% | UK, Germany, France, spillover to Eastern Europe | Long term (≥ 4 years) |

| Expansion of E-Learning and Remote Workflows | +0.8% | Europe-wide, notably Nordic and DACH regions | Medium term (2-4 years) |

| EU Funding for Creative Europe Media Production Tools | +0.6% | EU member states, media hubs | Long term (≥ 4 years) |

| Integration of Generative AI Plug-Ins Expanding User Base | +0.7% | Europe-wide, early adoption in tech-forward markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Subscription-Based Creative Suites

Subscription pricing has redrawn revenue models across the Europe Creative Software market, with Adobe reporting USD 1.8 billion in annual recurring revenue from EMEA in 2024.[1]Adobe Inc., “Adobe Reports Record Q4 and Fiscal Year 2024 Revenue,” investors.adobe.com Pay-as-you-go access lowers entry barriers for freelancers and micro-agencies, replacing hefty perpetual licenses with predictable monthly outlays. Vendors leverage cloud delivery to issue frequent feature drops, heightening perceived value and curbing piracy. SMEs gain budgeting flexibility, while vendors capture steadier cash flows that fund AI development. Centralized cloud storage simplifies GDPR governance compared to disparate on-premise installations, further accelerating subscription preferences in data-sensitive sectors.

Surge in Digital Content Creation Among SMEs

Seventy-three percent of European firms under 250 employees now deploy professional creative software, up from 58% in 2023, as measured by the European Commission’s DESI survey.[2]European Commission, “Digital Economy and Society Index (DESI) 2024,” digital-strategy.ec.europa.eu Polish SMEs benefited from digital vouchers that reimbursed software expenses, resulting in a 68% year-over-year increase in adoption in 2024. Manufacturing, retail, and service companies are broadening their use cases beyond core marketing, applying design suites to product visualization, social media assets, and interactive catalogs. Cloud platforms eliminate infrastructure hurdles, while freemium tiers enable risk-free trials that later convert to paid seats, expanding the Europe Creative Software market.

Rising Demand for 3D Animation in Gaming and Media

The United Kingdom’s VFX sector contributed GBP 1.8 billion (USD 2.3 billion) to national output in 2024, underscoring the economic weight of 3D pipelines.[3]UK Screen Alliance, “UK VFX Industry Economic Impact Report 2024,” ukscreenalliance.co.uk Streaming giants vie for immersive content, driving studios to scale render capacity and adopt real-time engines. Autodesk reported double-digit growth in Europe subscriptions for Maya and 3ds Max in 2024. Unity’s engine user base in the region climbed 22% as indie developers tapped easier asset creation workflows. Talent scarcity in London and Berlin inflates salaries, but AI-assisted rigging and motion-capture tools help offset cost pressures, making high-quality output feasible for boutique houses.

Expansion of E-Learning and Remote Workflows

Hybrid work has integrated design tools into daily corporate processes; European enterprises logged 45% higher creative software usage in 2024 compared to pre-pandemic baselines, according to the Digital Strategy 2025 report by Germany’s economics ministry. Universities equip students with cloud-first platforms, ensuring fluency before entering the labor market and reinforcing vendor lock-in. Collaboration-centric apps such as Figma and Canva gain traction because synchronous editing shortens review cycles. Vendors with desktop legacies accelerate SaaS transitions to match user expectations for anywhere access and automated version control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Software Licensing Costs for Freelancers | -0.8% | Europe-wide, especially Southern and Eastern Europe | Medium term (2-4 years) |

| Piracy and Availability of Open-Source Alternatives | -0.6% | Eastern and Southern Europe | Long term (≥ 4 years) |

| Data Residency Compliance Complexities Post-Schrems II | -0.4% | EU member states | Short term (≤ 2 years) |

| Talent Shortages in Niche CGI and VFX Pipelines | -0.5% | UK, Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Software Licensing Costs for Freelancers

Monthly subscription fees account for 8-12% of the median freelancer income in parts of Eastern Europe, creating churn risk as individuals pause or downgrade plans between projects. Unified EU pricing accentuates affordability gaps caused by purchasing-power differentials. Vendors respond with tiered packages, student-to-pro transitions, and regional discounts, but friction persists, capping penetration among price-sensitive creators.

Piracy and Availability of Open-Source Alternatives

Blender logged 35 million downloads in 2024, representing an 18% annual increase, signaling growing interest in free tools that rival proprietary suites in core features. Academic institutions favor open code for budget reasons and to avoid vendor lock-in, while government procurement rules mandating neutrality further level the field. Although enterprise support gaps remain, accelerated community innovation increases pressure on paid vendors to justify their premiums through AI capabilities, cloud services, and deeper integration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Type: Graphic Design Leads Digital Transformation

Graphic Design Software captured 39.19% of the European Creative Software market revenue in 2024, reflecting a cross-industry reliance on visual storytelling. The Europe Creative Software market size for this segment benefits from ubiquitous brand refresh cycles, social marketing content, and packaging redesigns. Adobe’s suite maintains a de facto standard status, yet newcomers such as Canva and Affinity nibble share among non-experts through simplified interfaces and aggressive freemium tiers. AI-driven template generation speeds iteration, while cloud storage eases remote collaboration.

3D Modeling and Animation, the fastest-growing segment with a 7.29% CAGR, accelerates on the back of gaming, metaverse proofs of concept, and architectural visualization. The Europe Creative Software market sees converging creative-technical workflows where parametric modeling, physics-based rendering, and virtual production require seamless data exchange. Video Editing tools cater to streaming platforms’ appetite for localized series, whereas Audio Editing grows steadily due to podcast monetization and multilingual voice-over demand. Illustration Software retains niche pockets in publishing and comics, sustained by the uptake of stylus-driven hardware.

By Deployment Mode: Cloud Dominance Accelerates

Cloud-based deployments accounted for 56.11% of the revenue in 2024 and are projected to achieve a 6.77% CAGR, underscoring the shift in the Europe Creative Software market toward real-time collaboration and device-agnostic access. Remote teams favor browser-native editors to avoid version-conflict headaches. Vendors release cloud-exclusive features first, nudging laggards away from desktop installs. The Schrems II ruling, however, prompts some public-sector users to migrate to EU-hosted clouds or hybrid stacks that preserve sovereignty for sensitive assets.

On-premise installations endure in defense, banking, and intellectual property-heavy film studios, which seek deterministic latency and air-gapped security. Hybrid models are gaining favor among multinationals that balance compliance with creative agility. The Europe Creative Software market size allocated to hybrid is expected to expand as containerized microservices enable IT teams to orchestrate private rendering farms while connecting to SaaS libraries.

By End User Industry: Media and Entertainment Drives Adoption

Media and Entertainment generated 32.49% of 2024 revenue, making it the largest industry slice of the Europe Creative Software market. Streaming platforms commissioning European originals intensify demand for color-grading, compositing, and 3D character software. The Europe Creative Software market share in this vertical will stay robust as real-time engines shorten production timelines.

Fashion and Retail, with a 7.31% CAGR outlook, tap design suites for digital prototyping, virtual try-ons, and social storefront assets. Luxury houses in France and Italy deploy AI to generate pattern variations, accelerating seasonal drops. Advertising agencies remain heavy buyers of full creative suites, whereas universities embed licenses into curricula, building early loyalty. Architecture and Engineering teams expand 3D and visualization spending to comply with green-building regulations and win tenders through immersive pitches. Independent creators rely on flexible pricing to scale toolkits incrementally, supporting the long-tail growth of the Europe Creative Software market.

By Revenue Model: Subscription Transformation Continues

Subscription plans dominated with a 63.74% share in 2024, illustrating end-user preference for OPEX over CAPEX. Predictable, metered billing aligns with project-based cash flows, especially for SMEs. The Europe Creative Software market size for subscription offerings is poised to rise as macroeconomic uncertainty steers buyers toward lower upfront commitments.

Freemium and in-app purchases grow at the fastest rate, with a 6.86% CAGR, as validated by Canva’s 100 million monthly users, many of whom upgrade to paid tiers once brand control and asset limits are reached. License-based models persist in procurement-heavy enterprises that require perpetual ownership, yet their share continues to decline as cloud functionality expands. Usage-based billing experiments emerge, charging for render minutes or AI-generation tokens, further diversifying revenue mixes within the Europe Creative Software market.

Geography Analysis

Germany held 19.82% of 2024 revenue, cementing its status as the largest national contributor to the Europe Creative Software market. Strong manufacturing clusters require 3D visualization for Industry 4.0 initiatives, while Berlin’s startup scene fuels demand for agile design stacks. Cloud penetration sits at 68%, reflecting mature infrastructure and clear GDPR guidance, which collectively underpin sustained spend.

The United Kingdom and France continue to generate sizable volumes despite post-Brexit regulatory friction. London’s finance and VFX ecosystems, as well as Paris’s luxury fashion houses, rely on high-end suites for content localization and e-commerce. Data-transfer rules add compliance overhead yet have not dampened adoption momentum. Both markets invest in AI-augmented workflows to offset wage inflation in creative roles.

Poland, the fastest-growing geography at 7.14% CAGR, benefits from EU structural funds and a burgeoning game-development community. Regional incubators subsidize software onboarding, expanding the Europe Creative Software market to new adopters. The Nordics record elevated per-capita spending thanks to digital-first government programs and high remote work rates. Southern Europe remains price-sensitive, encouraging the uptake of freemium models and open-source evaluations, yet rising tourism and fashion exports gradually increase investment in design tools. The Netherlands and Switzerland exhibit premium spending patterns, driven by fintech and pharma visualization needs, as well as multilingual content mandates.

Competitive Landscape

The Europe Creative Software market reveals moderate concentration. Adobe leads through its comprehensive Creative Cloud stack, but competitors gain ground by solving specific pain points with a frictionless user experience. Canva’s USD 380 million buyout of Affinity in March 2024 bundles pro-grade vector and raster editors into its web-native platform, broadening its appeal among power users while retaining its novice-friendly approach. Autodesk strengthens virtual-production credentials through the May 2024 acquisition of Wonder Dynamics, embedding AI-driven VFX automation and reinforcing its hold on media pipelines.

Generative AI emerges as the core battleground: Adobe’s Firefly injects text-to-image workflows, Unity embeds AI-assisted asset creation, and Maxon enriches Cinema 4D with machine-learning-based modeling. Vendors also compete for ecosystem extensibility; Adobe’s Firefly Services API and Unity’s developer grants entice third-party plug-ins, which deepen platform lock-in. European champions like Maxon leverage geographic proximity and data-sovereignty assurances to secure regulated clients wary of US cloud jurisdiction.

Open-source momentum, led by Blender, tempers pricing power at the low and mid tiers. Commercial vendors respond with freemium entry points that funnel users into paid cloud features such as asset libraries, team administration, and AI credits. Strategic alliances target vertical niches: Epic Games collaborates with the European Space Agency on visualization tools, while Figma courts enterprise design system deployments. The Europe Creative Software industry thus balances scale incumbency, agile upstarts, and community projects within a dynamic innovation cycle.

Europe Creative Software Industry Leaders

Adobe Inc.

Autodesk Inc.

Corel Corporation

Avid Technology Inc.

Dassault Systemes SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Canva rolled out Canva Enterprise Suite featuring advanced GDPR controls and European data-residency options, securing 2,000 corporate sign-ups in Germany, France, and the United Kingdom during the first month.

- May 2025: Unity Software teamed with the European Commission’s Digital Europe Programme to supply subsidized creative-tool licenses to 50,000 SMEs in Poland, Romania, and Bulgaria through a EUR 75 million (USD 82.5 million) initiative aimed at speeding digital adoption in emerging markets.

- March 2025: Autodesk acquired Chaos Group’s V-Ray division for about USD 410 million, reinforcing its architectural-visualization lineup and enlarging its customer base in Europe’s architecture and engineering sectors.

- February 2025: Adobe introduced Adobe Firefly Image 3 Model, adding more photorealistic generation, GDPR-compliant training-data documentation, and multilingual prompts across 24 European languages to meet commercial design needs.

Europe Creative Software Market Report Scope

| Graphic Design Software |

| Video Editing Software |

| 3D Modeling and Animation Software |

| Audio Editing Software |

| Illustration Software |

| Other Software Types |

| On-Premises |

| Cloud-Based |

| Hybrid |

| Media and Entertainment |

| Advertising and Marketing Agencies |

| Education |

| Architecture and Engineering |

| Fashion and Retail |

| Independent Creators / Freelancers |

| License-Based |

| Subscription-Based |

| Freemium and In-App Purchases |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Norway |

| Denmark |

| Finland |

| Poland |

| Switzerland |

| Belgium |

| Austria |

| Ireland |

| By Software Type | Graphic Design Software |

| Video Editing Software | |

| 3D Modeling and Animation Software | |

| Audio Editing Software | |

| Illustration Software | |

| Other Software Types | |

| By Deployment Mode | On-Premises |

| Cloud-Based | |

| Hybrid | |

| By End User Industry | Media and Entertainment |

| Advertising and Marketing Agencies | |

| Education | |

| Architecture and Engineering | |

| Fashion and Retail | |

| Independent Creators / Freelancers | |

| By Revenue Model | License-Based |

| Subscription-Based | |

| Freemium and In-App Purchases | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Norway | |

| Denmark | |

| Finland | |

| Poland | |

| Switzerland | |

| Belgium | |

| Austria | |

| Ireland |

Key Questions Answered in the Report

What is the forecast value of the Europe Creative Software market by 2030?

The market is expected to reach USD 3.51 billion by 2030.

Which software segment is growing fastest in Europe?

3D Modeling and Animation Software is projected to expand at a 7.29% CAGR through 2030.

Why are subscription models dominant in European creative tools?

They match SME cash-flow preferences, lower upfront costs, and simplify GDPR compliance through centralized cloud management.

Which country is the fastest-growing market in Europe?

Poland, driven by EU digitization funding, is set to grow at a 7.14% CAGR.

How is AI influencing competitive dynamics among creative software vendors?

Vendors race to embed generative capabilities, using AI to automate tasks, differentiate feature sets, and lock in ecosystems.

Page last updated on: