Application Modernization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

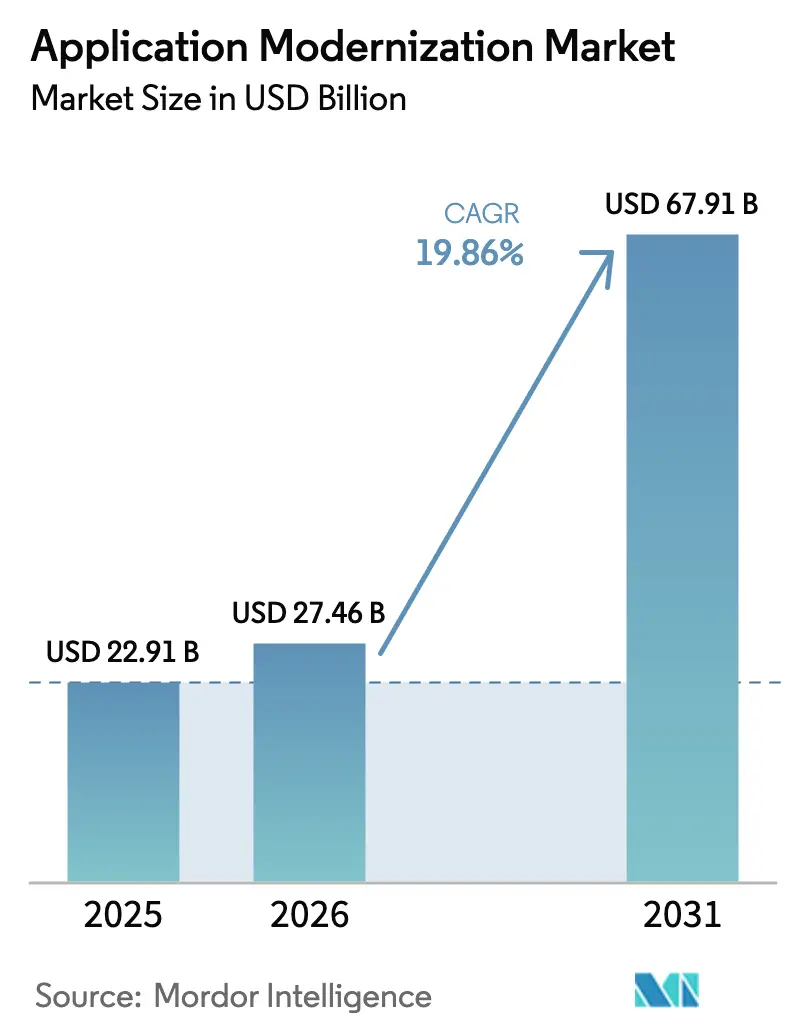

| Market Size (2026) | USD 27.46 Billion |

| Market Size (2031) | USD 67.91 Billion |

| Growth Rate (2026 - 2031) | 19.86% CAGR |

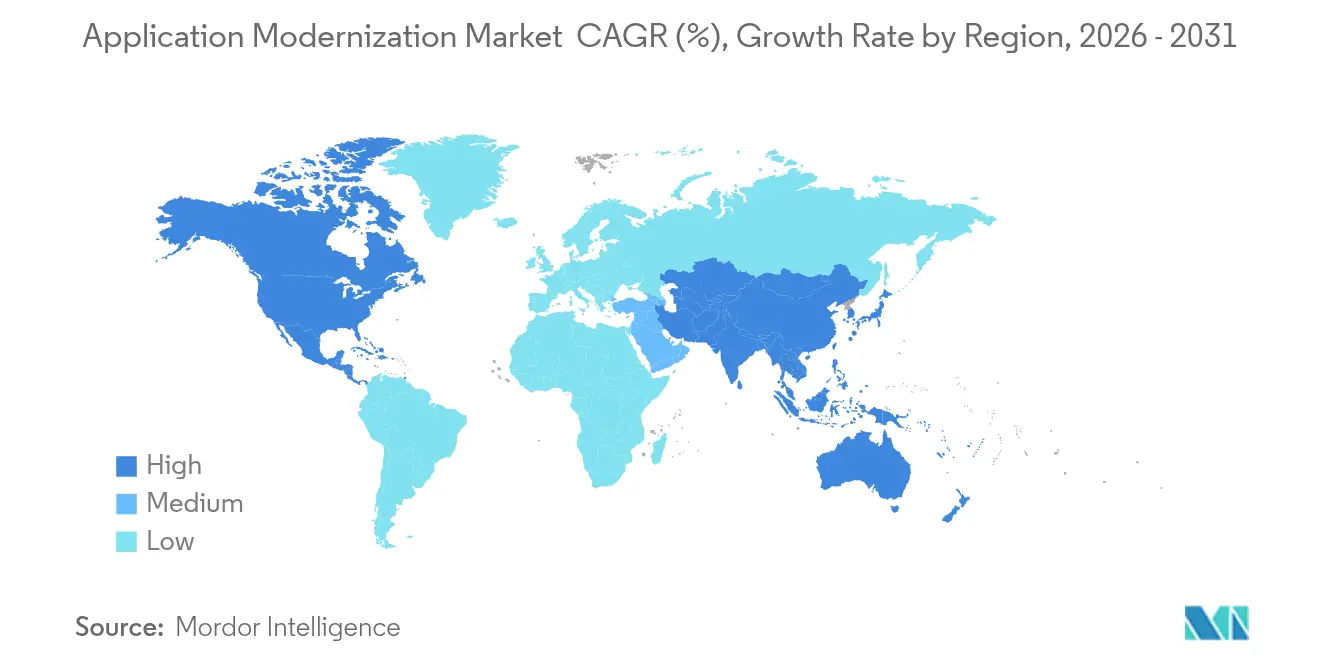

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

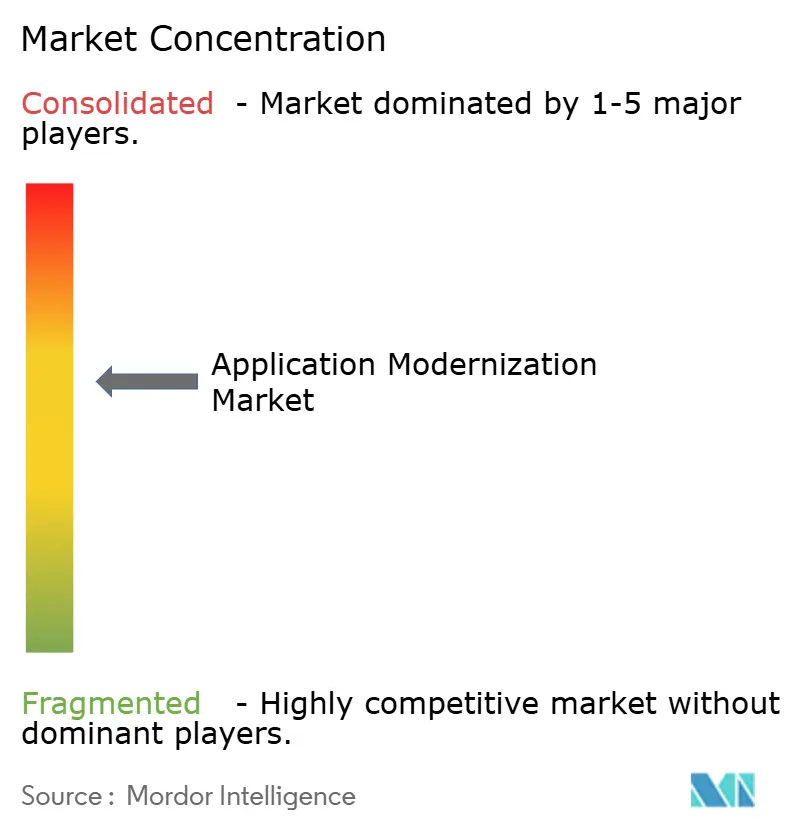

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Modernization Market Analysis by Mordor Intelligence

The application modernization market size is expected to grow from USD 22.91 billion in 2025 to USD 27.46 billion in 2026 and is forecast to reach USD 67.91 billion by 2031 at 19.86% CAGR over 2026-2031. The surge reflects enterprises’ need to convert aging, costly systems into agile digital platforms that sustain new revenue streams. Market momentum is reinforced by rising adoption of cloud-native architectures, growing regulatory scrutiny that exposes legacy vulnerabilities, and an expanding ecosystem of automated migration tools. Intensifying competition among hyperscalers and systems integrators is lowering entry barriers, while platform-engineering practices are shifting modernization from bespoke projects to repeatable products. Strategic spending is also buoyed by sustainability mandates that encourage moving compute-intensive workloads to energy-efficient cloud environments.

Key Report Takeaways

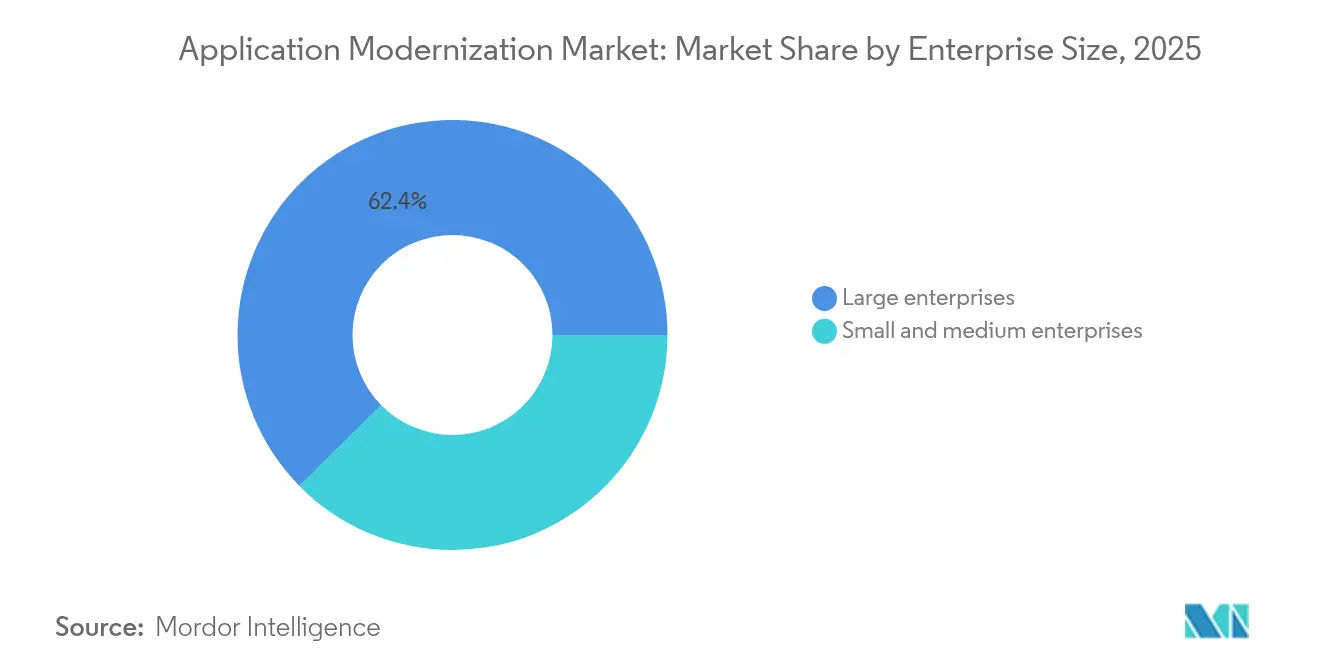

- By enterprise size, large enterprises held 62.38% of the application modernization market share in 2025, while small and medium enterprises are advancing at a 15.84% CAGR through 2031.

- By service type, re-platforming led with 25.93% revenue share in 2025; re-architecting is projected to grow at a 20.18% CAGR to 2031.

- By deployment mode, hybrid cloud commanded 49.63% share of the application modernization market size in 2025, and public cloud is accelerating at a 21.69% CAGR through 2031.

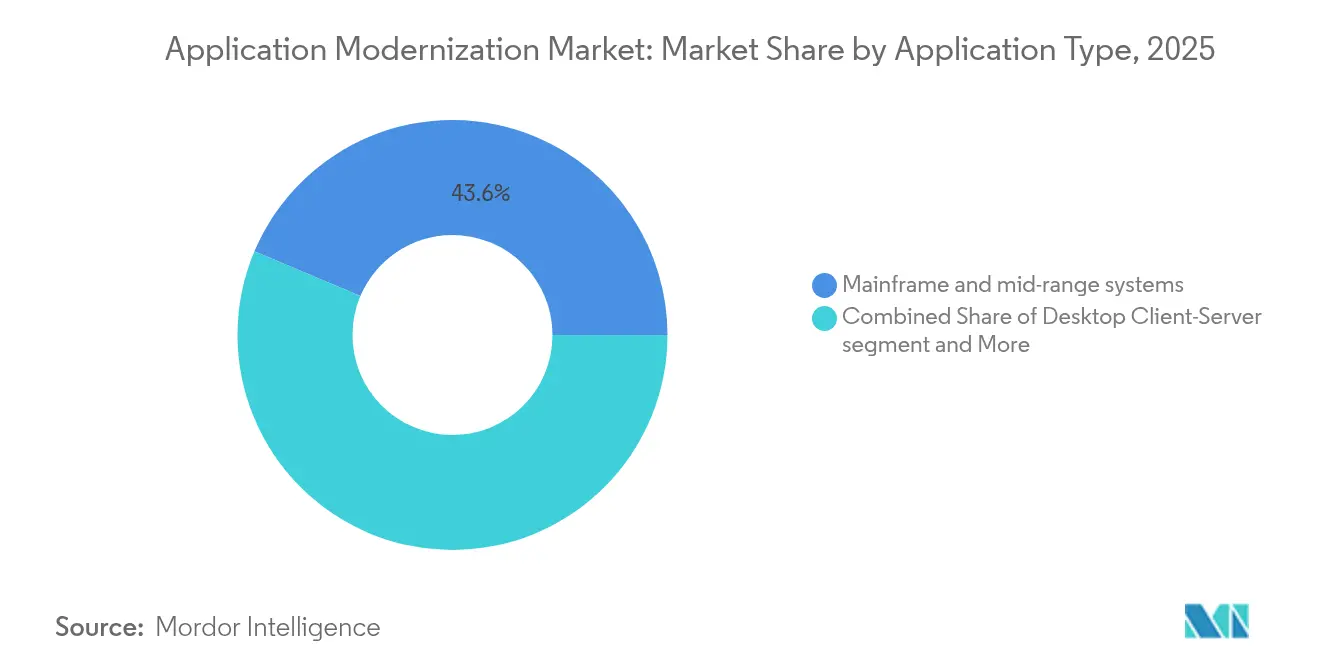

- By application, Mainframe and Mid-range segment commanded 43.64% of the overall application modernization market size in 2025, and ERP / CRM Suites is accelerating at a 15.1% CAGR through 2031.

- By end-user industry, BFSI accounted for 28.97% share of the application modernization market size in 2025, while healthcare and life sciences are growing at an 17.9% CAGR through 2031.

- By geography, North America captured 35.78% of 2025 revenue; Asia-Pacific is poised to expand at a 16.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Application Modernization Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of cloud-native and micro-services architectures | +4.2% | Global, with strongest adoption in North America and EU | Medium term (2-4 years) |

| Cost-reduction and agility benefits | +3.8% | Global, particularly pronounced in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Regulatory push in BFSI and public sector | +3.1% | North America and EU core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Platform-engineering and IDP tooling momentum | +2.9% | North America and EU early adopters, global expansion | Medium term (2-4 years) |

| Green-software mandates driving legacy code overhaul | +2.4% | EU leadership, North America following, Asia-Pacific emerging | Long term (≥ 4 years) |

| Post-digital-first spending surge | +2.1% | Global, with sustained momentum in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption of Cloud-Native and Microservices Architectures

Modernization strategies increasingly center on decomposing monoliths into containerized microservices that can be deployed independently at scale. Fortune-100 enterprises report Kubernetes production use nearing 96%, turning the technology from an experiment into an operational backbone[1]CNCF, “Cloud Native Survey 2024,” cncf.io. Cloud-native design shortens feature release cycles, enables blue-green deployments that reduce downtime risk, and supports multi-cloud portability. Organizational structures evolve in tandem as DevOps and platform-engineering teams provide internal developer portals that standardize tooling and security policies. The resulting velocity gains unlock new business models such as consumption-based pricing and embedded services.

Cost-Reduction and Agility Benefits

Legacy estates absorb up to 80% of annual IT operating budgets, leaving scant resources for innovation. Enterprises that modernize core platforms report 30–50% lower run costs alongside double-digit performance improvements, freeing capital for data analytics and AI pilots. In Asia-Pacific, cost pressure is acute; CFOs prioritize projects that shrink maintenance overheads and accelerate time-to-market for localized digital products. Proven migration blueprints and cloud financial-operations practices help CIOs quantify savings, turning modernization into a board-level efficiency lever.

Regulatory Push in BFSI and Public Sector

The European Union’s Digital Operational Resilience Act mandates granular reporting and zero-tolerance downtime thresholds, forcing banks to swap mainframe batch cycles for real-time API architectures. Parallel mandates in the United States, Canada, and Singapore further tighten controls around data residency and cyber risk. Public-sector agencies confront similar pressure to integrate authentication, payments, and citizen records via secure microservices. Compliance deadlines anchor multi-year modernization roadmaps and guarantee sustained spend even during macroeconomic slowdowns.

Platform-Engineering and IDP Tooling Momentum

Enterprises are shifting from scattered DevOps scripts to curated internal developer platforms that expose golden-path templates, automated policy checks, and self-service environments. The approach abstracts infrastructure, letting product teams deploy in minutes rather than weeks. IDP adoption cuts cognitive load, narrows the cloud-native skills gap, and directly boosts developer productivity metrics such as change-failure rate and mean time to recovery. Vendors offering out-of-the-box platform modules gain rapid traction among firms that lack in-house site-reliability engineering depth.

Restraints Impact Analysis of Application Modernization Market*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native skills gap | -2.8% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Up-front migration cost and downtime risk | -2.1% | Global, particularly challenging for SMEs | Short term (≤ 2 years) |

| Legacy licensing lock-in | -1.7% | North America and EU, where legacy investments are highest | Long term (≥ 4 years) |

| Data-sovereignty complexity in multi-cloud | -1.4% | Asia-Pacific and EU leadership, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Skills Gap

Demand for architects who can refactor COBOL code into microservices far exceeds available talent. Sixty-four percent of technology executives cite staffing scarcity as their top modernization challenge[3]Red Hat, “State of Enterprise Open Source 2024,” redhat.com. The shortage is most acute in Kubernetes operations and DevSecOps, where certifications have yet to scale beyond early adopters. Organizations respond with aggressive reskilling programs, joint ventures with managed services providers, and low-code toolchains that narrow expertise requirements. Even so, talent pipelines lag project demand, restraining potential revenue growth.

Up-Front Migration Cost and Downtime Risk

Modernization projects often require 12–18 months of parallel operations that double infrastructure spending before savings accrue. Small and medium enterprises with lean cash positions delay initiatives because they cannot absorb extended payback periods. Outage fears further inhibit progress, since mission-critical workloads—especially in payments and healthcare—cannot tolerate prolonged switchovers. To de-risk, vendors promote phased strangler-fig patterns and automated regression testing that keep legacy systems live until new services stabilize. However, the perceived financial and operational exposure still dampens near-term adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Application Modernization Market Segment Analysis

By Enterprise Size:

Large Enterprises Anchor Spend, SMEs Ignite VelocityLarge enterprises generated 62.38% of 2025 revenue, underpinning the application modernization market with multi-year programs that touch hundreds of interconnected systems. Engagements frequently exceed USD 10 million and include global rollouts, redundant testing environments, and stringent compliance audits. Strategic objectives revolve around mainframe re-platforming, domain-driven decomposition, and event-stream architectures that support billions of daily transactions. Vendor selection favors systems integrators with proven reference sites in regulated industries and the capacity to orchestrate global change-management campaigns.

Small and medium enterprises, though smaller in baseline spend, expand at a 15.84% CAGR through 2031. Their modernization journey often begins with SaaS substitution for on-premise workloads, followed by containerized micro-services that handle customer-facing functions. The democratization of migration accelerators and pay-as-you-go cloud pricing lowers capital barriers. Many SMEs engage in “evergreen” refactoring cycles aligned with product sprints rather than monolithic transformation projects, compressing feedback loops and showcasing nimble models that larger incumbents now emulate. The competitive ripple effects reinforce cyclical growth across the broader application modernization market.

By Service Type:

Re-Platforming Dominates While Re-Architecting ScalesRe-platforming held 25.93% of 2025 revenue, cementing its role as the default modernization starting point for risk-averse enterprises. The approach shifts workloads to cloud infrastructure almost intact, yielding quick hardware savings and basic automation benefits. Cloud providers supply migration toolkits that map VMware images to containers and automate network rewiring, accelerating delivery timelines. However, performance gains plateau when legacy monoliths persist, prompting organizations to allocate second-phase budgets toward decomposing core business domains.

Re-architecting accelerates at a 20.18% CAGR and increasingly represents the strategic end-state. This path replaces rigid monoliths with polyglot microservices, event streams, and API gateways that expose real-time data to partners. Advanced engagements leverage domain-driven design workshops, service mesh layers for east-west traffic, and GitOps pipelines that codify continuous delivery. Generative AI copilots now parse legacy codebases to suggest service boundaries and flag dead code. The outcomes create scalable foundations that support AI inferencing, predictive maintenance, and embedded fintech use cases, extending the lifetime value of modernization initiatives across the application modernization market.

By Deployment Mode:

Hybrid Leads, Public Cloud AcceleratesHybrid architectures secured 49.63% of 2025 spending and remain the anchor of the application modernization market because they align with compliance, latency, and data-sovereignty imperatives. Banks keep core-ledger processing on on-premise LinuxOne mainframes yet burst fraud-detection microservices into cloud regions during peak loads. Manufacturers replicate this pattern by retaining plant-level SCADA systems locally while pushing analytics to cloud data fabrics. Kubernetes-based control planes provide a unified policy layer, allowing workloads to shift seamlessly according to cost or resilience priorities.

Public cloud, expanding at a 21.69% CAGR, gains credibility as hyperscalers achieve parity with on-premise security certifications. Sovereign-cloud constructs where customer keys never leave local jurisdiction calm regulatory fears. Enterprises capitalize on AI-optimized infrastructure and serverless runtimes that compress release cycles from months to days. Emerging patterns such as edge-to-cloud pipelines place inference engines on factory gateways while streaming outputs to centralized models, further blurring the boundaries between deployment modes and enriching the addressable application modernization market size.

By Application Type:

Mainframe Estates Persist as ERP Modernization QuickensMainframe and mid-range systems still account for 43.64% of 2025 revenue, underscoring the centrality of COBOL, PL/I, and RPG workloads that encode decades of business logic. Use cases span credit-card clearing, airline reservations, and public-sector payroll, where up-time mandates hit five nines. Modernization teams adopt strangler-fig methods, wrapping APIs around discrete functions before migrating each slice into cloud microservices. Automated code converters and unit-test generators expedite translation but final validation hinges on subject-matter experts who know the original logic paths.

Packaged ERP and CRM suites represent the fastest-growing slice at 15.1% CAGR as vendors time support sunsets to stimulate cloud migrations. Organizations replace heavily customized on-premise instances with modular SaaS that embeds AI-driven forecasting, procure-to-pay automation, and vertical compliance configurations out-of-the-box. The business case pivots on rapid functional updates, native mobile experiences, and consumption-based pricing that scales elastically with transaction volumes. Successful implementations free talent to focus on differentiation-oriented microservices, reinforcing demand in adjacent segments of the application modernization market.

By End-User Industry:

BFSI Sets the Pace, Healthcare Takes FlightBanking, financial services, and insurance maintained 28.97% of 2025 revenue as institutions rewired payment rails, risk engines, and customer-engagement platforms to meet open-banking mandates. Core-bank transformation projects prioritize zero-downtime cutovers because every second of service interruption carries steep regulatory fines. Vendors embed observability, chaos-engineering drills, and blue-green deployment pipelines to safeguard stability. Fintech challengers accelerate incumbent urgency, demonstrating cloud-native operating profit margins that incumbents struggle to match.

Healthcare and life sciences grow at an 17.9% CAGR amid relentless pressure to integrate electronic medical records, diagnostics, and telehealth apps. Interoperability rules such as the United States’ TEFCA and Europe’s EHDS formalize data-sharing frameworks. Providers modernize to incorporate AI-supported clinical decision systems, IoT patient devices, and privacy-by-design architectures. Emerging trials deploy synthetic data to train algorithms without exposing personal information, highlighting the sector’s dual focus on innovation and compliance that translates into robust demand across the broader application modernization market.

Geography Analysis

North America Application Modernization Market

North America retained leadership with a 35.78% share in 2025 as enterprises executed aggressive cloud-first mandates underpinned by abundant hyperscaler regions and venture capital that fuels modernization start-ups. Regulatory catalysts such as the U.S. Executive Order on cyber resilience push critical infrastructure operators to re-platform insecure legacy stacks. BFSI and healthcare account for the volume core, yet media and retail firms likewise refactor digital channels to support immersive experiences and generative-AI-driven personalization.

APAC Application Modernization Market

Asia-Pacific exhibits the fastest-expanding trajectory at a 16.9% CAGR through 2031. Governments in India, Japan, and Australia tie tax incentives to migration milestones, while digital-sovereignty laws encourage hybrid strategies that localize citizen data. Bank modernizers in Singapore pilot event-driven core banking engines with settlement times measured in milliseconds. Manufacturing and telecom sectors embrace modernization to harness 5G edge compute and real-time supply-chain analytics, positioning the region as a crucible for innovation that exports best practices globally.

Europe and Nordics Application Modernization Market

Europe advances steadily, guided by GDPR, DORA, and climate-neutral data-center policies that favor cloud-native workloads with energy-elastic characteristics. Public-sector digitization grants fund refactoring projects that open government APIs to fintechs and health-tech start-ups. Nordic utilities modernize SCADA systems to integrate renewables, while automotive OEMs shift monolithic engineering platforms to microservices that streamline over-the-air updates. Collectively, these dynamics sustain a balanced growth arc within the application modernization market and diversify demand across every major sub-region.

Competitive Landscape

The application modernization market remains moderately fragmented. Incumbent systems integrators, IBM, Accenture, Tata Consultancy Services, and Infosys—bundle advisory, change-management, and vertical accelerators into multi-year managed services. IBM’s USD 6.4 billion acquisition of HashiCorp broadens its infrastructure-as-code portfolio and deepens cross-plane orchestration, strengthening its hybrid-cloud credentials. Accenture expands its myWizard automation suite with generative-AI copilots that scan millions of code lines to surface refactor candidates.

Hyperscalers converge on modernization by embedding migration toolchains within their infrastructure stacks. Microsoft Azure’s Spring Apps and AWS’s Babelfish abstract code translation and database lift-and-shift, while Google Cloud offers Dual-Run emulation that cuts regression testing time. These consumption-linked services intensify competitive pressure on professional-services billing models and incentivize integrators to forge joint go-to-market motions.

Specialized disruptors exploit platform gaps: vFunction automates service boundary extraction, while Modernization.ai uses large language models to generate target microservice schematics. Such offerings attract midsized enterprises that seek speed and predictable outcomes. Strategic acquisitions continue as larger players purchase niche tools to secure differentiators, signaling ongoing consolidation even as the market welcomes fresh entrants, ultimately balancing concentration and innovation inside the application modernization market.

Application Modernization Industry Leaders

IBM

Accenture Plc

HCL Technologies

TCS

Cognizant Corporation

- *Disclaimer: Major Players sorted in no particular order

Application Modernization Market Companies Covered in this Report

- International Business Machines Corporation (IBM)

- Accenture plc

- Tata Consultancy Services Ltd (TCS)

- Cognizant Technology Solutions Corp

- HCL Technologies Ltd

- Capgemini SE

- Wipro Ltd

- Infosys Ltd

- Dell Technologies Inc

- DXC Technology Company

- Amazon Web Services, Inc

- Microsoft Corporation

- Google Cloud (Alphabet Inc)

- Oracle Corporation

- SAP SE

- VMware, Inc

- Red Hat, Inc

- Atos SE

- Fujitsu Ltd

- CGI Inc

Recent Industry Developments in Application Modernization Market

- May 2025: IBM completed its USD 6.4 billion acquisition of HashiCorp, expanding hybrid-cloud automation capabilities.

- April 2025: NTT Data launched the Smart AI Agent Ecosystem, a platform that accelerates IT modernization through machine-learning-driven code analysis.

- March 2025: Microsoft and Silverlake extended their partnership to modernize banking applications across Asia-Pacific, integrating Azure services with domain-specific accelerators.

- January 2025: MongoDB acquired Voyage AI to embed trustworthy AI into its database platform and enrich data-modernization features.

Application Modernization Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the application modernization market as all revenue generated from services that upgrade or transform legacy, monolithic, or on-premises software into cloud-ready, micro-services-oriented, DevOps-enabled applications. Activities covered include re-hosting, re-platforming, re-architecting, re-engineering, containerization, and associated program management for both large enterprises and SMEs.

Scope exclusion: tool-only refactoring platforms sold without a paid professional-services component are not counted.

Segments Covered in This Report

- By Enterprise Size

- Small and Medium Enterprises (SME)

- Large Enterprises

- By Service Type

- Re-platforming

- Re-hosting (Lift and Shift)

- Re-architecting

- Re-engineering

- Containerization / Kubernetes enablement

- Others

- By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Application Type

- Mainframe and Mid-range Legacy

- Desktop Client-Server

- Monolithic Web Applications

- Packaged ERP / CRM Suites

- By End-User Industry

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- IT and Telecom

- Government and Defense

- Manufacturing

- Retail and e-Commerce

- Energy and Utilities

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- GCC

- Israel

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Our team interviewed cloud architects at hyperscalers, CIOs in BFSI and healthcare, and regional integrators across North America, Europe, and Asia-Pacific. These conversations validated average project ticket sizes, emerging contract structures (fixed-price versus outcome-based), and typical legacy portfolios slated for action, allowing us to refine assumed penetration rates and ramp-up curves that desk sources alone could not surface.

Desk Research

We began with structured secondary scans of open sources such as the U.S. Bureau of Labor Statistics for IT wage trends, Eurostat ICT spending files, and UN Comtrade shipment codes that hint at server de-commissioning volumes. Industry bodies like the Cloud Native Computing Foundation and TM Forum provided adoption and certification statistics, while peer-reviewed journals in IEEE Xplore supplied defect-density benchmarks before and after modernization. Company 10-Ks, investor decks, and reputable media helped our analysts gauge deal flow, pricing spreads, and pipeline health. D&B Hoovers and Dow Jones Factiva, part of Mordor's paid toolkit, added hard numbers on vendor revenue mix. This list is illustrative; many other public and proprietary records fed initial estimates and sanity checks.

Market-Sizing & Forecasting

A top-down model converts enterprise IT capex and opex pools into a modernization-eligible spend pool, which is then filtered through project-level penetration rates gathered from primary work. Select bottom-up cross-checks, supplier roll-ups and sampled average selling price times volume, tighten the range. Key drivers in the model include cloud-migration intensity, mainframe installed base, DevOps toolchain adoption, regulatory cyber mandates, and talent day-rate inflation. Forecasts rely on multivariate regression with lagged cloud-spend growth, GDP-weighted digital transformation indices, and regional skills capacity as predictors, before scenario analysis flags upside or downside cases.

Data Validation & Update Cycle

Outputs pass three layers of variance checks, anomaly flags, and senior-analyst review. Our models refresh each year, and analysts push interim updates whenever major M&A, regulation, or macro shocks move underlying variables. A final pre-publication sweep ensures clients receive the latest calibrated view.

How Mordor Intelligence's Application Modernization Market Size Compares to Other Published Estimates

Published figures differ because firms select dissimilar service mixes, assume unique cloud-adoption speeds, and apply varied currency conversions.

Mordor analysts state results in constant 2025 dollars, align scope to end-to-end professional services, and revisit inputs annually; others may bundle tooling revenue, freeze FX rates, or use once-off surveys.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.91 B (2025) | Mordor Intelligence | - |

| USD 19.82 B (2024) | Global Consultancy A | Excludes containerization services; FX fixed at announcement date |

| USD 20.82 B (2024) | Regional Consultancy B | Counts only large-enterprise contracts; uses one-time vendor survey |

| USD 13.58 B (2025) | Trade Journal C | Tracks "application transformation" but omits re-hosting revenues |

Taken together, the comparison shows that when scope breadth, refresh cadence, and multi-variable forecasting are harmonized, as we do, market value stabilizes. Clients therefore gain a dependable, transparent baseline they can trace back to clear levers and reproduce with their own assumptions.

Key Questions Answered in the Report

What is the current size of the application modernization market?

The application modernization market is valued at USD 27.46 billion in 2026 and is projected to reach USD 67.91 billion by 2031.

Which region grows the fastest in application modernization?

Asia-Pacific records the highest growth, expanding at a 16.9% CAGR through 2031 due to government digitization drives and data-sovereignty rules.

Which enterprise segment contributes the most revenue?

Large enterprises contribute 62.38% of 2025 revenue because of extensive legacy estates and sizable modernization budgets.

What deployment mode dominates current spending?

Hybrid cloud leads with 49.63% of 2025 revenue as organizations balance control, compliance, and cloud scalability.

Why is re-architecting gaining momentum?

Re-architecting grows at a 20.18% CAGR because it delivers scalable, resilient microservices that unlock full cloud-native benefits beyond lift-and-shift migrations.

What key restraint limits modernization speed?

A cloud-native skills gap reduces potential growth by 2.8%, as demand for Kubernetes and DevSecOps expertise exceeds available talent.

Page last updated on: