Low-Power Software Design Framework Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 4.23 Billion |

| Growth Rate (2026 - 2031) | 12.28% CAGR |

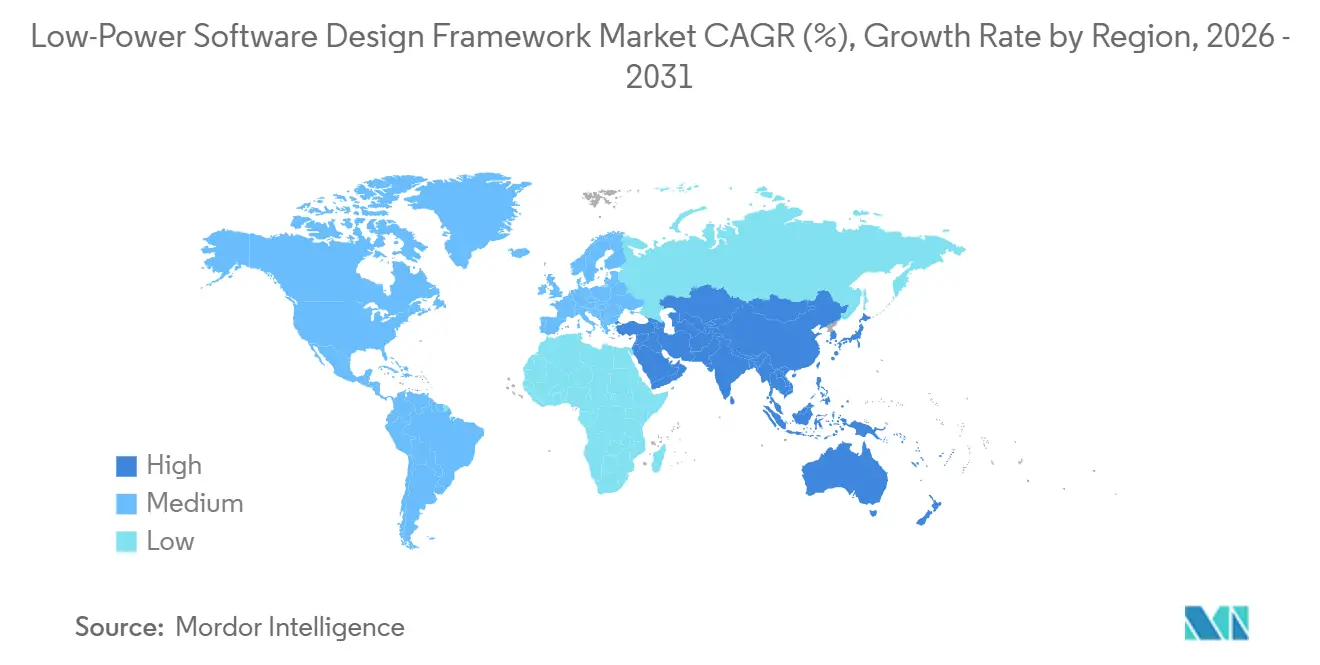

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

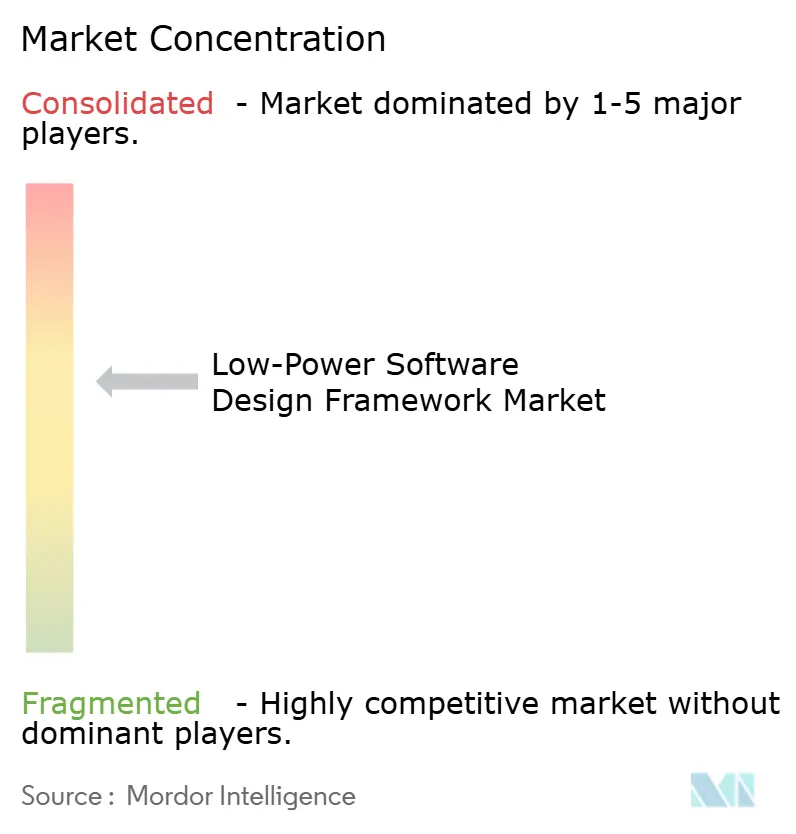

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low-Power Software Design Framework Market Analysis by Mordor Intelligence

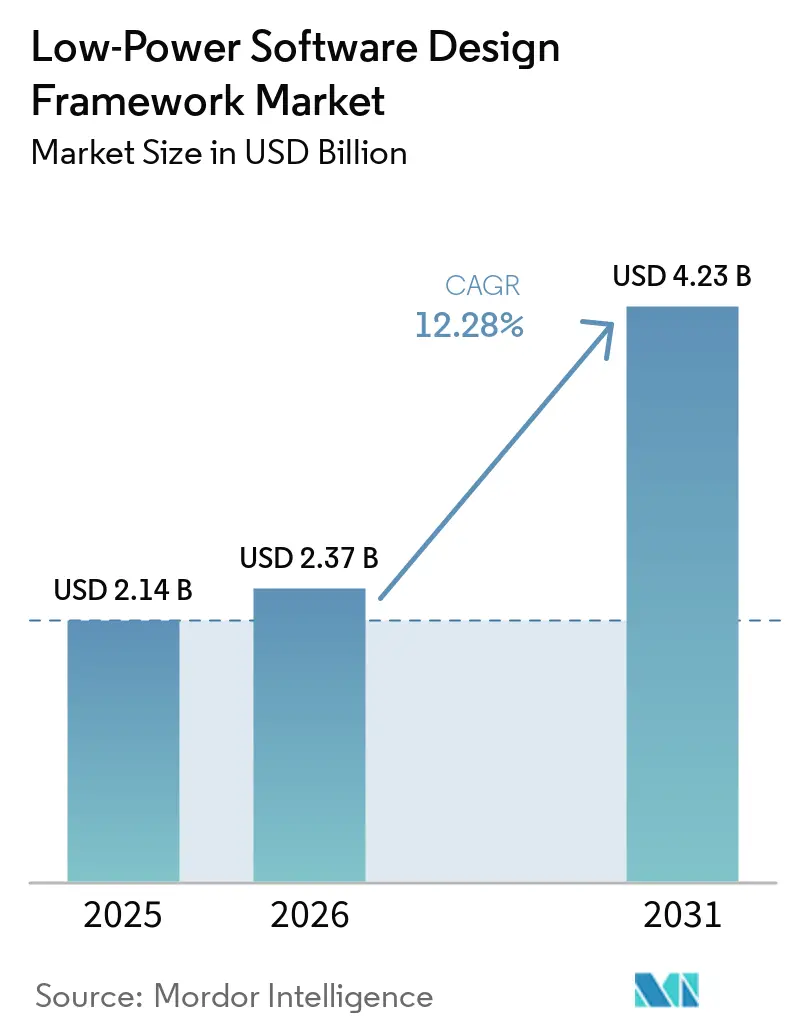

The low-power software design framework market size is expected to increase from USD 2.14 billion in 2025 to USD 2.37 billion in 2026 and reach USD 4.23 billion by 2031, growing at a CAGR of 12.28% over 2026-2031. Growth is being supported by the spread of always-on connected devices, the rising need to run AI inference on edge hardware with tight power limits, and stricter compliance requirements that now link power intent with software security and documentation. The low-power software design framework market is also benefiting from the shift to advanced process nodes, where leakage and energy efficiency concerns are forcing design teams to validate power behavior much earlier in the development flow. Asia-Pacific remained the largest regional base in 2025 because semiconductor design activity is concentrated across China, South Korea, Japan, and Taiwan, while Europe is set to expand the fastest as standby power rules and product cybersecurity obligations reshape procurement priorities. On-premises tools still lead in deployment because embedded development workflows remain closely tied to proprietary intellectual property protection, while cloud delivery is advancing rapidly as distributed teams need shared environments for simulation and firmware collaboration. Consumer electronics continue to anchor revenue, while IoT and smart devices are creating stronger forward demand because battery-life economics, energy-aware software design, and long-lived connected fleets now matter more than hardware efficiency alone.

Key Report Takeaways

- By product type, Power Analysis and Optimization Software held 28.74% of the low-power software design framework market in 2025, while Deployment and Lifecycle Management Software is projected to expand at a 13.45% CAGR through 2031.

- By technology, Model-Based Design accounted for 27.63% share in 2025, while AI-Assisted Low-Power Design is expected to record the highest CAGR of 14.12% through 2031.

- By deployment model, on-premises held 52.34% of the low-power software design framework market share in 2025, while cloud-based deployment is projected to grow at a 13.89% CAGR through 2031.

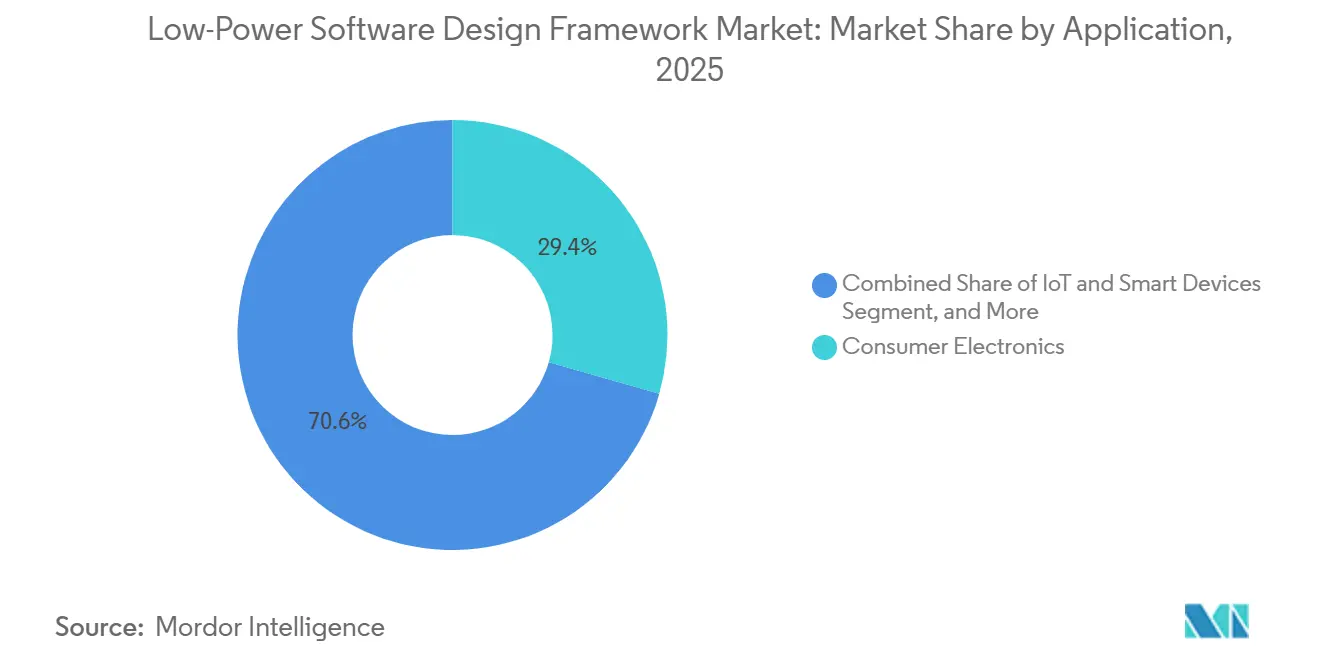

- By application, consumer electronics captured 29.41% of the market in 2025, while IoT and smart devices are projected to expand at a 14.25% CAGR through 2031.

- By end user, semiconductor and fabless design houses accounted for 30.12% share in 2025, while engineering service providers are expected to grow at a 13.78% CAGR through 2031.

- By geography, Asia-Pacific led with 36.45% share in 2025, while Europe is projected to record the fastest regional CAGR of 13.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low-Power Software Design Framework Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Efficient Edge AI Adoption | +3.5% | Global, with intensity in Asia-Pacific and North America | Short term (≤ 2 years) |

| Battery Lifetime Optimization in Connected Devices | +2.8% | Global, with concentrated demand in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Rise of Energy-Harvesting MCU Toolchains | +2.0% | Global, with early adoption in North America, Europe, and China | Medium term (2-4 years) |

| Software-Defined Power Budgeting in Always-On Devices | +1.5% | Global, particularly in IoT hubs in Asia-Pacific and North America | Medium term (2-4 years) |

| Model-Based Design Adoption for Early Power Validation | +1.2% | North America, Europe, and automotive hubs in Germany and Japan | Medium term (2-4 years) |

| Secure-By-Design Firmware and Compliance Pressure | +0.8% | Europe, with spillover to North America and Asia-Pacific export markets | Short term (≤ 2 years), with long-tail compliance obligations through December 2027 |

| Source: Mordor Intelligence | |||

Energy-Efficient Edge AI Adoption

Energy-efficient edge AI adoption is becoming one of the clearest drivers of demand for the low-power software design framework market. Neural network inference is now moving closer to the sensor and controller levels, where devices operate at milliwatt or sub-milliwatt levels and cannot tolerate inefficient firmware behavior. That shift is forcing engineering teams to link model compression, memory use, and power-state control much earlier in the design cycle than before. Forschungszentrum Jülich presented its Automaton Engine project at Hannover Messe 2026, with latency per watt as a core optimization target, demonstrating how edge AI design priorities are moving away from peak compute claims and toward usable energy efficiency.[1]Forschungszentrum Jülich, “Automaton Engine, Edge-KI-System Für Deterministische Echtzeit-Intelligenz,” Hannover Messe 2026 Project Page, fz-juelich.de MathWorks reinforced this direction in April 2026, releasing R2026a with Simulink Copilot, which allows engineers to examine model behavior and embedded code generation within a common workflow that now includes AI-assisted development support. As TinyML runtimes become more standardized, the low-power software design framework market is likely to see stronger competition around toolchain-level energy profiling during training and pre-deployment validation, rather than just basic inference deployment.[2]Y. Pan et al., “From Tiny Machine Learning to Tiny Deep Learning, A Survey,” ACM Computing Surveys, dl.acm.org

Battery Lifetime Optimization in Connected Devices

Battery lifetime optimization in connected devices is pushing the low-power software design framework market toward deeper software-centric energy management. Product teams are no longer treating battery life as a hardware-only issue because large sensor fleets, wearables, and remote nodes often operate in places where manual battery replacement is expensive or impractical. Research published in 2025 showed that adaptive soft-actor-critic reinforcement learning applied to NB-IoT power-saving parameters could extend battery life by more than 3x without hardware changes, which shifts more value toward firmware policy design and verification tools. Nordic Semiconductor added to this trend in March 2026 with nRF Fuel Gauge v2.0, which introduced adaptive battery health monitoring and real-time state-of-health reporting across changing discharge conditions. The broader implication is that intermittent and adaptive energy behavior must now be managed in software, not just measured after the fact. That is why the low-power software design framework market is benefiting from demand for checkpointing, state retention, and runtime scheduling methods that can respond to the uncertainty of energy availability in connected devices.[3]E. Sahin et al., “LoLiPoP-IoT, Advancing the Energy-Efficient Internet of Things,” Microelectronics Journal, sciencedirect.com

Rise of Energy-Harvesting MCU Toolchains

The rise of energy-harvesting MCU toolchains is opening a distinct growth lane for the low-power software design framework market. Energy harvesting is no longer confined to niche industrial sensing, because it is also being explored for consumer wearables, smart-building nodes, and remote monitoring systems where long-life operation matters more than peak performance. Silicon Labs supported this shift with Simplicity SDK 2025.6.2, which included an energy harvesting extension with applications, drivers, and integrated development support for intermittent embedded deployments. Work published in 2026 also showed that multi-year battery-equivalent operation in harvesting systems depends on combining hardware energy capture with intelligent software scheduling, since modern MCU hardware is already highly optimized and remaining gains must come from system software behavior. This is changing vendor priorities from simple power-profile reporting toward energy-state modeling, simulation, and recovery logic across uncertain power events. As a result, the low-power software design framework market is moving into a stage where vendors that can simulate stochastic energy availability are better placed than those that only report deterministic consumption after execution.

Software-Defined Power Budgeting in Always-On Devices

Software-defined power budgeting in always-on devices is strengthening the position of the low-power software design framework market in embedded development workflows. Power intent is increasingly treated as a design constraint that belongs in firmware policy and verification logic, rather than as a late-stage correction after synthesis or board testing. Research shared by Espressif in February 2026 showed that a firmware-level power management governor on ESP32-based NuttX RTOS implementations could extend operating life from 77 hours to more than 3,700 hours on the same hardware, illustrating the value of software policy.[4]Espressif, “Power Management in NuttX,” Espressif Developer Portal, developer.espressif.com This raises the importance of tools that can model governor behavior, sleep-state entry, and wake-event timing before silicon or final firmware integration. It also aligns with the spread of always-on sensing and on-device inference, where transitions between idle, active, and inference states must be named, simulated, and verified rather than left to trial-and-error optimization. The low-power software design framework market is therefore gaining from a design approach in which power governance becomes part of the formal software architecture rather than an isolated tuning exercise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Verification Burden for Cross-Domain Power Models | -1.4% | Global, most acute in North America and Asia-Pacific advanced-node design centers | Medium term (2-4 years) |

| Fragmented Toolchains Across MCU, RTOS, and Compiler Stacks | -1.1% | Global, most disruptive in Europe and Southeast Asia engineering service hubs | Long term (≥ 4 years) |

| Shortage of Low-Power Embedded Verification Talent | -0.8% | Global, with most acute shortfall in South and Southeast Asia | Medium term (2-4 years) |

| Higher Qualification Cost for AI-Assisted Autogeneration | -0.5% | North America, Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Verification Burden For Cross-Domain Power Models

The high verification burden for cross-domain power models remains a significant restraint on the market for low-power software design frameworks. As SoC and embedded architectures combine electrical, thermal, and mechanical behavior more tightly, teams can no longer validate power behavior through isolated workflows owned by separate engineering groups. The challenge becomes more severe in automotive, industrial automation, and advanced-node semiconductor programs where design changes in one domain can affect timing, heat, leakage, and reliability in another. Synopsys highlighted this issue in 2026 when it introduced Ansys 2026 R1 and its Multiphysics Fusion approach, which links multiphysics engines with EDA tools and was still in the process of expanding customer trials during 2026. Even with better integration, every change to power domains or AI-assisted layout decisions expands the number of interactions that must be checked for power-intent compliance and sign-off consistency. This means the low-power software design framework market faces a practical ceiling where design automation is advancing faster than full verification capacity in the most demanding programs.

Fragmented Toolchains Across MCU, RTOS, And Compiler Stacks

Fragmented toolchains across MCU, RTOS, and compiler stacks continue to slow adoption in the low-power software design framework market. Many embedded teams still have to support multiple compiler environments and operating system variants within a single product family, which creates inconsistent instrumentation points, debugging paths, and energy measurement workflows. That fragmentation makes it difficult to build a repeatable power design process when firmware must move across multiple controller families and meet customer qualification requirements. Partial standards, such as CMSIS and POSIX-aligned APIs, improve portability, but they do not provide a universal power-intent interchange model that can move cleanly across the full toolchain. The problem is especially evident for engineering service providers and multi-platform product teams, because they need reusable methods that span multiple stacks rather than vendor-specific optimization routines. Until interoperability improves, the low-power software design framework market will continue to lose time and budget to manual handoffs, duplicated validation work, and inconsistent power model exchange.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Power Sign-Off Tools Lead While Lifecycle Platforms Expand Faster

Power Analysis and Optimization Software held 28.74% of the low-power software design framework market size in 2025, while Deployment and Lifecycle Management Software is projected to grow at a 13.45% CAGR through 2031. The leadership of Power Analysis and Optimization Software recognizes that power sign-off remains one of the final gates before tapeout, especially at advanced nodes, where missed violations can trigger costly redesigns. In the low-power software design framework market, this type benefits from the fact that leakage, state transitions, and thermal interactions are now being treated as production risks rather than secondary tuning issues. That position gives power analysis tools a durable revenue base even as adjacent categories gain momentum.

Cadence introduced Conformal AI Studio in March 2025, featuring its Conformal AI Low Power capability, demonstrating how hierarchical and distributed verification flows are used to manage design scale in power sign-off environments. Design and Architecture, Software, Simulation, and Modeling Software continue to see stable adoption because teams still need early-stage exploration before sign-off begins. Verification and Sign-Off Software is also benefiting from stronger documentation requirements in automotive and industrial programs, where power behavior has to be traceable alongside safety and security expectations. At the same time, the low-power software design framework industry is seeing stronger growth in Deployment and Lifecycle Management Software because over-the-air update planning, fleet energy behavior, and long-term device maintenance are becoming part of the same value chain. Siemens supported this direction in 2026 with its Fuse EDA AI Agent, which more closely linked manufacturing readiness and design workflows and signaled that the boundary between design-time and operational power management is narrowing.

By Technology: Model-Based Design Holds The Base As AI-Native Methods Gain Ground

Model-Based Design accounted for 27.63% share in 2025, while AI-Assisted Low-Power Design is projected to record the fastest CAGR of 14.12% through 2031. Model-Based Design remains central to the low-power software design framework market because it offers traceable workflows, supports regulated engineering environments, and helps teams connect simulation with code generation. Its installed base in automotive and aerospace is difficult to displace quickly because those programs depend on consistent model-to-code lineage and established validation routines. In the low-power software design framework market, this gives incumbent model-based workflows a defensible position even as newer AI-centric methods expand.

MathWorks strengthened this segment in April 2026 when it released R2026a with Simulink Copilot and extended embedded support for Renesas platforms, which connected AI-assisted development more directly with hardware-oriented execution flows. Hardware-In-The-Loop Simulation, Rapid Control Prototyping, and Embedded System Prototyping continue to gain attention because power validation now extends beyond logic behavior into more realistic operating conditions. AI-Assisted Low-Power Design is advancing faster as it shifts from post-synthesis tuning toward front-end design governance, where power limits are introduced earlier and handled more systematically. Cloud-Native Collaborative Development is also advancing because distributed firmware teams increasingly need shared environments for versioning, simulation, and cross-site power analysis. The low-power software design framework industry is therefore entering a two-speed phase where mature workflows keep the installed base stable while AI-assisted methods capture incremental complexity and new project starts.

By Deployment Model: On-Premises Strength Persists As Hybrid Adoption Builds

On-premises deployment retained 52.34% of the low-power software design framework market share in 2025, while cloud-based deployment is projected to grow at a 13.89% CAGR through 2031. On-premises systems continue to lead because many fabless design houses, automotive suppliers, and defense-related programs cannot move sensitive design data into shared environments without breaching contractual or regulatory conditions. In the low-power software design framework market, this keeps proprietary verification, netlist handling, and sign-off work closely tied to internal infrastructure. The result is not simple resistance to change, but a security-driven deployment preference that remains strong across several high-value use cases.

Cloud-based delivery is still expanding because it reduces the cost of compute-intensive simulation and enables globally distributed teams to collaborate more effectively during design exploration. Cadence moved into that space in February 2026 with ChipStack AI Super Agent, which supported cloud, hybrid, and on-premises configurations and reflected the growing need for flexible deployment models. Siemens also aligned with this direction through its AI-focused EDA workflow strategy, which uses NVIDIA GPU infrastructure to accelerate design tasks across broader computing environments. The more important shift inside the low-power software design framework market is therefore toward hybrid usage, where pre-silicon exploration moves to scalable environments while final sign-off remains under stricter enterprise control. That structure fits the current mix of security needs, distributed engineering teams, and rising simulation loads better than either pure-cloud or pure on-premises alone.

By Application: Consumer Electronics Leads Revenue While IoT And Smart Devices Set The Pace

Consumer electronics accounted for 29.41% of the low-power software design framework market size in 2025, while IoT and smart devices are projected to expand at a 14.25% CAGR through 2031. Consumer electronics remain the largest application because smartphones, wearables, tablets, and smart-home products are shipped at high volumes and face steady pressure to improve battery life and standby efficiency. In the low-power software design framework market, these products create repeat demand for tools that can validate low-power states, optimize software activity, and document efficiency behavior before launch. The segment also benefits from updated European ecodesign rules that are making energy budgeting more visible in product development and compliance workflows. Automotive, healthcare, wearables, and aerospace and defense continue to support spending because certification, long product lifecycles, and complex power-state transitions all increase the value of reliable, software-centric power validation.

IoT and smart devices are the fastest-growing applications because their economics depend on long-life operation, distributed fleets, and devices that often run under uncertain or highly constrained energy budgets. The low-power software design framework market is seeing this segment move beyond simple duty-cycling and into lifecycle-level optimization, where updates, connectivity, sensing, and inference all affect usable battery life. Standards-linked secure development processes are also pulling power and security documentation closer together in industrial and connected-device programs. Nordic Semiconductor highlighted this broader lifecycle view in May 2026, when it announced an AI-assisted workflow spanning SDK development, firmware development, and deployed fleet management for wireless IoT products. That extension from design-time tooling to ongoing fleet optimization is expanding the addressable scope of the low-power software design framework market in connected-device applications.

By End User: Design Houses Provide Scale While Service Providers Gain Strategic Weight

Semiconductor and fabless design houses accounted for 30.12% share in 2025, while engineering service providers are projected to grow at a 13.78% CAGR through 2031. Design houses remain the largest end-user group because they are usually the first adopters of new verification and power analysis capabilities, and their choices shape downstream toolchain standards across the broader supply chain. In the low-power software design framework market, their influence is amplified by early access programs with EDA vendors, advanced-node design needs, and their role in setting expectations for documentation and sign-off quality. Electronic OEMs continue to form the next major demand layer because they need power-aware development tools across consumer, industrial, and automotive product lines.

Academic and research institutions still play a smaller but important role because they incubate new methods that later move into commercial tooling, especially in energy-aware AI inference and embedded optimization. Engineering service providers are growing faster because many OEMs lack sufficient internal specialists to manage firmware, RTOS behavior, power-domain modeling, and compliance documentation simultaneously. That outsourcing trend is pushing more software tool investment toward service firms that can spread licensing costs across multiple client programs and deliver specialized validation-as-a-service. The ITU-T L.1341 recommendation, published in December 2025, also added formal energy-efficiency requirements for intelligent IoT platforms, which supports a standards-based role for service providers that help clients meet new validation expectations. As a result, the low-power software design framework market is increasingly influenced not only by product builders, but also by service organizations that sit between tool vendors and OEM deployment programs.

Geography Analysis

Asia-Pacific accounted for 36.45% of the low-power software design framework market in 2025, making it the leading regional market. The region benefits from dense semiconductor design activity across China, Japan, South Korea, and Taiwan, where advanced-node programs and large-volume embedded product pipelines create a steady demand for power-signoff, simulation, and verification tools. The low-power software design framework market is particularly strong in Asia-Pacific, where countries combine leading chip design ecosystems with major downstream manufacturing and product development capacity. India is also becoming more important as engineering service providers expand in cities such as Bangalore, Hyderabad, and Pune, which increases demand for development, prototyping, and compliance-oriented software environments. Australia adds a smaller but relevant layer through research and pilot activity around sustainable remote sensing and energy-harvesting connected systems.

North America ranked second in the low-power software design framework market, supported by hyperscaler silicon programs, automotive semiconductor activity, and the regional presence of major EDA vendors. The United States remains central because many platform vendors, advanced design teams, and AI-driven verification programs are concentrated there. Synopsys stated in May 2026 that 20 customers were evaluating agentic design solutions across more than 25 specialized AI agents, reflecting the strong testing of next-generation EDA methods in the region. Canada and Mexico add supporting demand through fabless design growth and electronics manufacturing services, which increase the regional need for lifecycle- and deployment-focused tools.

Europe is projected to expand at a 13.92% CAGR through 2031, making it the fastest-growing regional segment in the low-power software design framework market. The main drivers are regulatory and industrial rather than volume-based, with new standby power rules and cybersecurity obligations changing how product teams specify firmware and validation tools. The EU updated standby power limits with a regulation effective from May 2025, which raised the priority of energy budgeting and verification in procurement decisions for networked and consumer devices. The Cyber Resilience Act also adds vulnerability reporting and software documentation obligations from September 2026, which increases demand for frameworks that can support auditable firmware design and software bill of materials practices alongside power-state management. Germany remains the regional center of gravity because industrial automation and advanced EDA collaboration are strong there, while the Middle East, Africa, and South America remain earlier-stage opportunities tied mainly to selective smart-city and edge-sensing deployments.

Competitive Landscape

The low-power software design framework market is moderately concentrated, with leading vendors holding a large share of advanced-node power sign-off and simulation revenue while a wider group of specialist suppliers competes in embedded deployment, verification, and modeling niches. Scale matters most in high-end semiconductor workflows, but there is still room for focused competitors in adjacent software layers. The competitive field tightened materially in 2025 when Siemens completed its USD 10 billion acquisition of Altair Engineering in March and Synopsys completed its USD 35 billion acquisition of Ansys in July. Those transactions broadened the reach of both companies across simulation, multiphysics, and semiconductor design tasks, leaving less strategic space for mid-tier vendors that lack comparable platform depth. Consolidation is making integrated workflows more important because customers increasingly want design, simulation, verification, and operational support from a smaller set of providers.

AI is becoming the clearest competitive lever across the low-power software design framework market. Siemens launched the Fuse EDA AI Agent in 2026 to connect generative and agentic AI with semiconductor and printed circuit board design workflows, while tying those capabilities to broader manufacturing-readiness tasks. Cadence entered the same race with ChipStack AI Super Agent in February 2026, aiming to improve RTL coding, testbench generation, and verification productivity through a more automated design flow. Synopsys also pushed its combined EDA and multiphysics position in 2026 through Ansys 2026 R1 and its work with Samsung Foundry on AI-powered design and technology co-optimization. These moves show that vendor rivalry is no longer limited to individual point tools and is increasingly centered on AI-enabled design ecosystems.

Openings still remain in parts of the market that the largest vendors less fully cover. Intermittent computing for energy-harvesting architectures, long-horizon firmware lifecycle management for IoT fleets, and AI-assisted power policy synthesis for always-on sensing workloads are still developing areas rather than locked positions. Specialist firms and engineering service providers can compete there if they combine domain knowledge with flexible delivery and stronger compliance support. At the same time, larger vendors are likely to keep strengthening their hold on premium programs because integrated portfolios, platform acquisitions, and AI-led workflow expansion are raising switching costs for customers.

Low-Power Software Design Framework Industry Leaders

Synopsys, Inc.

Cadence Design Systems, Inc.

Siemens Industry Software Inc.

Ansys, Inc.

The MathWorks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Cadence extended its ChipStack AI Super Agent to Level-5 full autonomy at Computex 2026, making it the industry's first fully autonomous virtual agentic AI design engineer. Built in collaboration with NVIDIA, the system automates dynamic simulations within verification workflows and demonstrated over 40x faster RTL validation cycles, reducing a typical five-week verification loop to less than a day at NVIDIA's design centers.

- May 2026: Nordic Semiconductor announced an AI-assisted development solution covering the entire IoT device product lifecycle, from SDK and MCU firmware through to deployed device fleet management, described as the first "chip to cloud" AI-assisted embedded development offering in the wireless IoT sector. The announcement highlights an AI-assisted workflow that spans SDK prototyping, production programming, and over-the-air fleet monitoring.

- May 2026: Synopsys demonstrated production-ready AI-powered digital and analog EDA flows for Samsung Foundry's third-generation 2nm-class process at the Samsung Advanced Foundry Ecosystem Forum 2026, validating measurable power and performance improvements over the second-generation 2nm-class node through AI-driven design and technology co-optimization.

- May 2026: Keysight Technologies introduced electrical-optical-electrical co-simulation in PathWave ADS 2026, enabling engineers to model complete high-speed signal chains within a single design environment, a capability directly relevant to power modeling in photonic computing interconnects for AI infrastructure.

Global Low-Power Software Design Framework Market Report Scope

The Low-Power Software Design Framework market comprises platforms and solutions that enable engineers, developers, and enterprises to design, simulate, verify, and optimize software and hardware systems, with a focus on minimizing energy consumption and improving efficiency. These frameworks integrate capabilities such as low-power design architecture, simulation and modeling, verification and sign-off, power analysis, optimization, and lifecycle management.

The Low-Power Software Design Framework market report is segmented by Product Type (Design and Architecture Software, Simulation and Modeling Software, Verification and Sign-Off Software, Power Analysis and Optimization Software, Deployment and Lifecycle Management Software), Technology (Model-Based Design, Hardware-In-The-Loop Simulation, Rapid Control Prototyping, Embedded System Prototyping, AI-Assisted Low-Power Design, Cloud-Native Collaborative Development), Deployment Model (On-Premises, Cloud-Based, and Hybrid), Application (Consumer Electronics, Automotive, Industrial Automation, Healthcare and Wearables, Aerospace and Defense, IoT and Smart Devices), End User (Semiconductor and Fabless Design Houses, Electronic OEMs, Engineering Service Providers, Academic and Research Institutions), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Design and Architecture Software |

| Simulation and Modeling Software |

| Verification and Sign-Off Software |

| Power Analysis and Optimization Software |

| Deployment and Lifecycle Management Software |

| Model-Based Design |

| Hardware-In-The-Loop Simulation |

| Rapid Control Prototyping |

| Embedded System Prototyping |

| AI-Assisted Low-Power Design |

| Cloud-Native Collaborative Development |

| On-Premises |

| Cloud-Based |

| Hybrid |

| Consumer Electronics |

| Automotive |

| Industrial Automation |

| Healthcare and Wearables |

| Aerospace and Defense |

| IoT and Smart Devices |

| Semiconductor and Fabless Design Houses |

| Electronic OEMs |

| Engineering Service Providers |

| Academic and Research Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Design and Architecture Software | |

| Simulation and Modeling Software | ||

| Verification and Sign-Off Software | ||

| Power Analysis and Optimization Software | ||

| Deployment and Lifecycle Management Software | ||

| By Technology | Model-Based Design | |

| Hardware-In-The-Loop Simulation | ||

| Rapid Control Prototyping | ||

| Embedded System Prototyping | ||

| AI-Assisted Low-Power Design | ||

| Cloud-Native Collaborative Development | ||

| By Deployment Model | On-Premises | |

| Cloud-Based | ||

| Hybrid | ||

| By Application | Consumer Electronics | |

| Automotive | ||

| Industrial Automation | ||

| Healthcare and Wearables | ||

| Aerospace and Defense | ||

| IoT and Smart Devices | ||

| By End User | Semiconductor and Fabless Design Houses | |

| Electronic OEMs | ||

| Engineering Service Providers | ||

| Academic and Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the low-power software design framework market?

The low-power software design framework market was valued at USD 2.14 billion in 2025, stood at USD 2.37 billion in 2026, and is forecast to reach USD 4.23 billion by 2031 at a CAGR of 12.28%.

What is driving adoption of low-power software design frameworks?

Growth is being driven by always-on connected devices, edge AI workloads with strict energy limits, tighter compliance demands, and the need to validate power behavior earlier in the software and silicon design flow.

Which deployment model currently leads demand?

On-premises led with 52.34% share in 2025 because intellectual property protection, security rules, and final sign-off requirements still keep many high-value programs inside enterprise infrastructure.

Which application area is expanding the fastest?

IoT and smart devices is projected to grow at a 14.25% CAGR through 2031 as battery life, energy harvesting, firmware updates, and fleet-level optimization become more important in connected products.

Which region is growing the fastest for low-power software design frameworks?

Europe is projected to expand at a 13.92% CAGR through 2031, supported by stricter standby power rules and cybersecurity obligations that are changing firmware design and validation requirements.

Who are the main end users of these frameworks?

Semiconductor and fabless design houses held the largest share at 30.12% in 2025, while engineering service providers are growing the fastest as OEMs increasingly outsource specialized power optimization and validation work.

Page last updated on: