Software Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 380.26 Billion |

| Market Size (2031) | USD 801.43 Billion |

| Growth Rate (2026 - 2031) | 16.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software Consulting Market Analysis by Mordor Intelligence

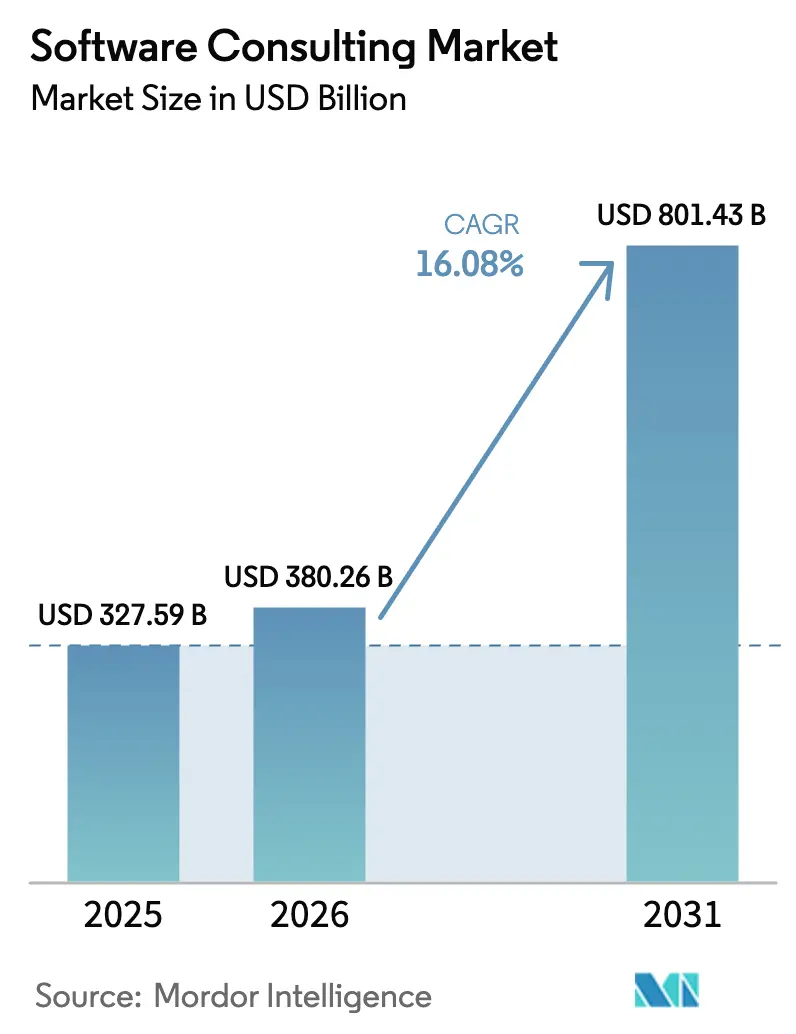

The software consulting market size was valued at USD 327.59 billion in 2025 and estimated to grow from USD 380.26 billion in 2026 to reach USD 801.43 billion by 2031, at a CAGR of 16.08% during the forecast period (2026-2031). Enterprises have shifted from cost-containment toward revenue-growth goals, driving large-scale modernization programs anchored in cloud-native platforms, AI-enabled business processes, and data-centric operations. The looming retirement of SAP ECC is adding urgency as more than two-thirds of installed customers still need to move to S/4HANA. At the same time, public-sector digitalization and sector-specific regulations, especially in healthcare and financial services, are broadening consulting opportunities. Competitive intensity centers on AI partnerships, with leading firms earmarking multi-billion-dollar budgets for generative AI tooling and domain models.

Key Report Takeaways

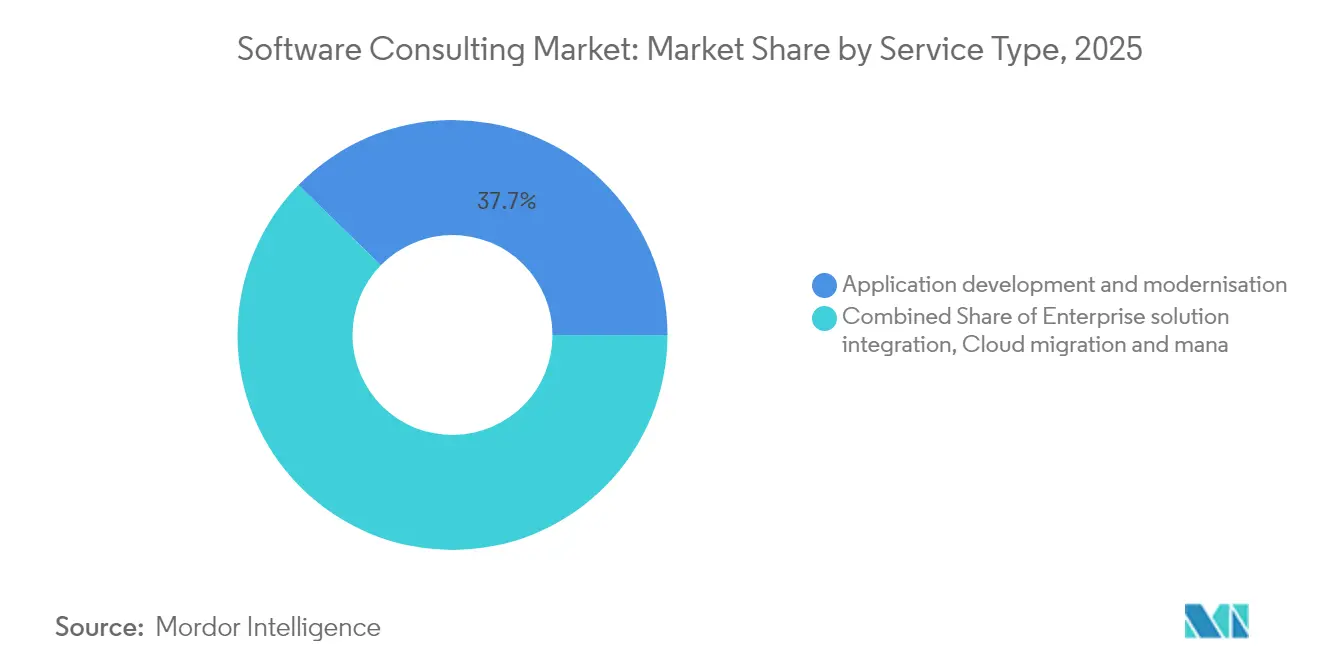

- By service type, application development and modernization led with 37.72% of software consulting market share in 2025, while data and AI/ML consulting is projected to expand at a 17.02% CAGR to 2031.

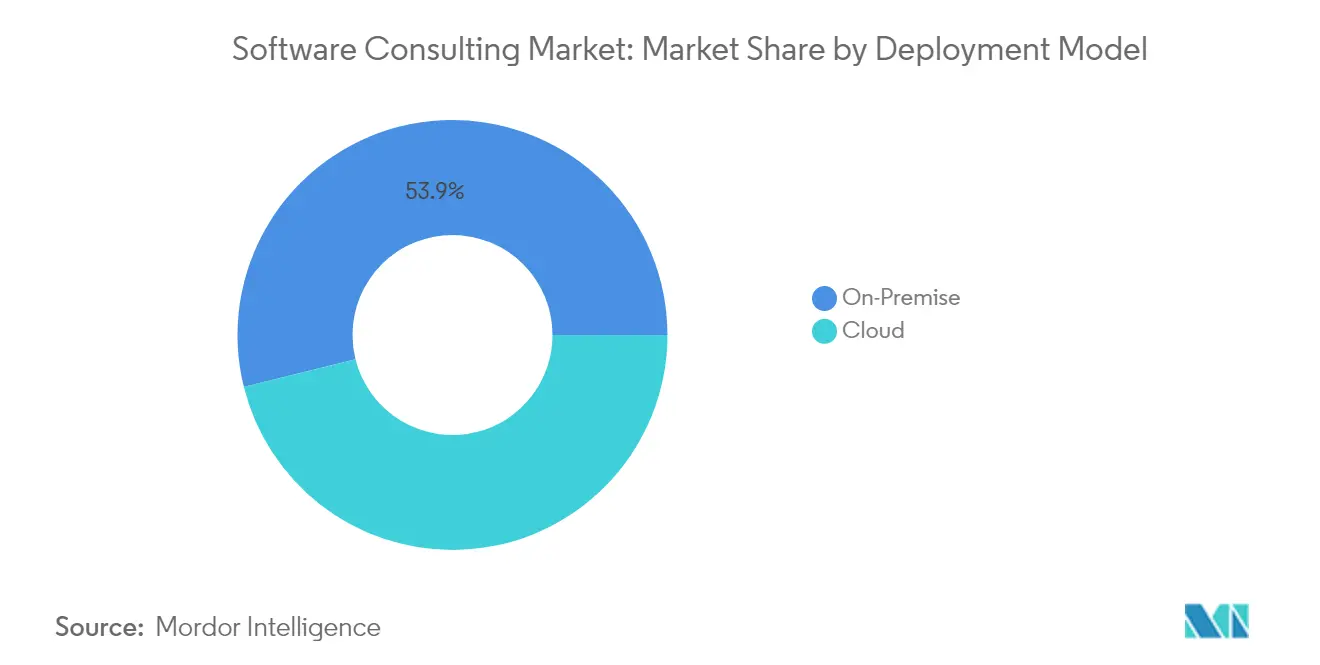

- By deployment model, public cloud solutions accounted for 46.12% share of the software consulting market size in 2025 and hybrid/multi-cloud architectures are advancing at a 19.12% CAGR through 2031.

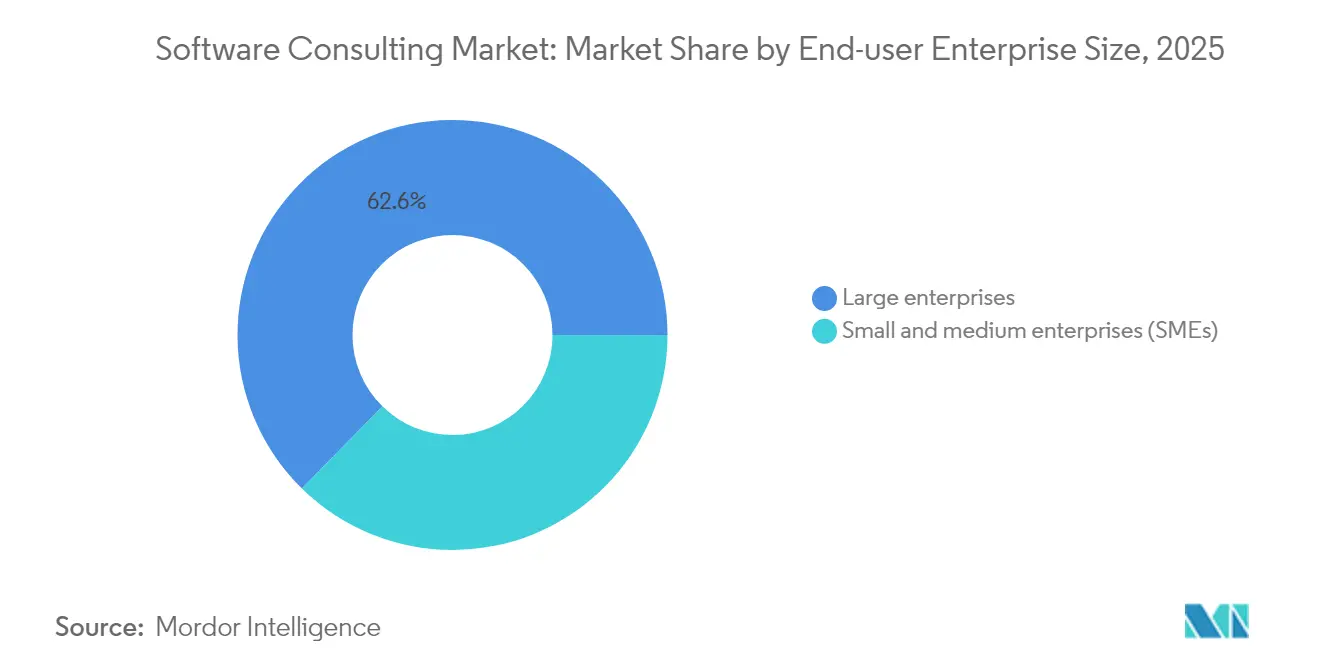

- By enterprise size, large enterprises held 62.65% share of the software consulting market size in 2025, whereas the SME segment records the fastest 16.84% CAGR to 2031.

- By end-user industry, the BFSI sector commanded 24.18% share of the software consulting market size in 2025; healthcare and life sciences is set to grow at a 16.42% CAGR through 2031.

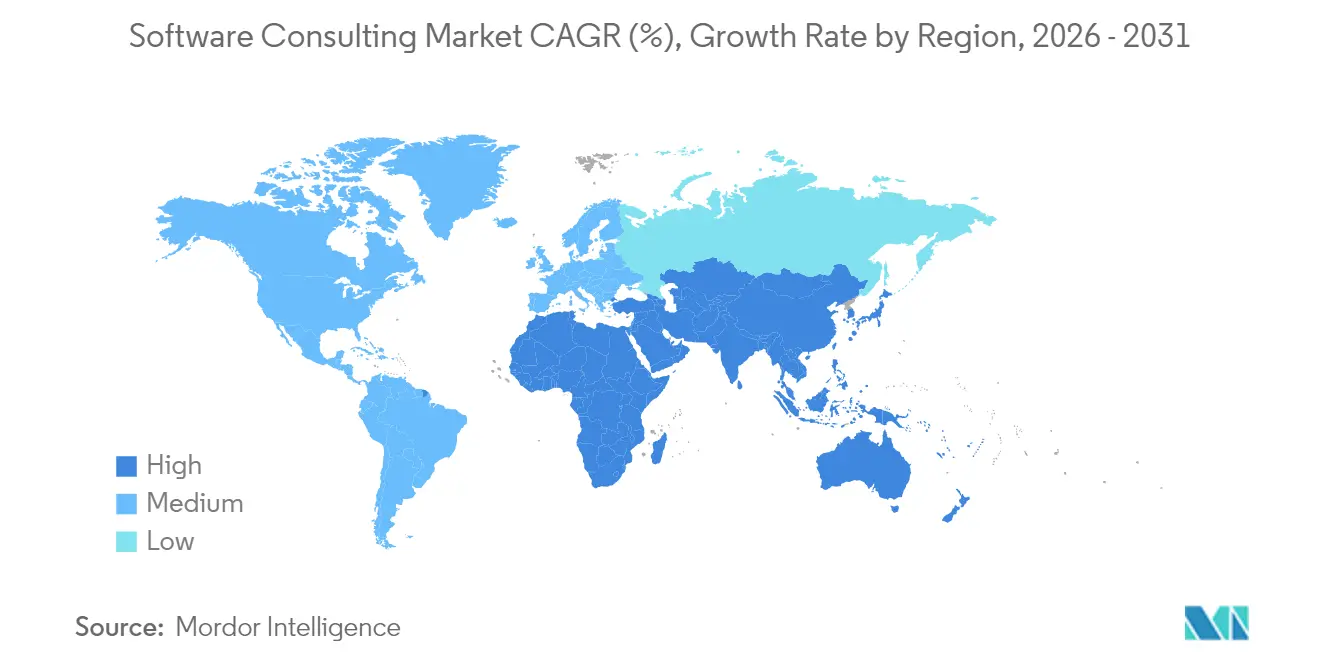

- By geography, North America captured 27.55% software consulting market share in 2025; Asia-Pacific is forecast to post the strongest 18.02% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Software Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise cloud-migration acceleration | +3.2% | Global, North America and Europe leading | Medium term (2-4 years) |

| Digital-transformation mandates post-COVID | +2.8% | Global, strongest in Asia-Pacific | Short term (≤ 2 years) |

| Need for operational efficiency and cost optimisation | +2.1% | Global, manufacturing-led | Long term (≥ 4 years) |

| Growing data-analytics and AI adoption | +4.5% | North America and Europe core, Asia-Pacific spill-over | Medium term (2-4 years) |

| Looming SAP ECC sunset fuelling S/4HANA consulting demand | +2.7% | Global, DACH concentration | Short term (≤ 2 years) |

| Emerging AI-governance and compliance mandates | +1.9% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Cloud-Migration Acceleration

Cloud migration has become foundational for digital agendas. Enterprises are shifting mission-critical workloads to public and hybrid clouds to support distributed workforces and real-time analytics. European software spending climbed 5.1% in 2024, and off-the-shelf AI software investments in Germany, France, and the United Kingdom are rising 21% each year. Nordic economies recorded USD 44 billion in software revenues with 16% annual growth, underscoring how cloud-first strategies underpin export competitiveness.[1]Julie Sweet, “Accenture Reports Fourth-Quarter and Full-Year 2024 Results,” accenture.com With 85% of organizations adopting cloud-first development, global cloud outlays are set to surpass USD 675.4 billion. These complex transitions require consultants skilled in multi-cloud architecture, data-sovereignty design, and workload refactoring, areas where in-house teams often lack depth.

Digital-Transformation Mandates Post-COVID

Post-pandemic priorities have reframed digital transformation as a survival requirement. Surveys show 87% of consulting clients launched enterprise-wide programs in the last three years and 92% relied on external partners for execution. Technology consulting spend exceeds USD 400 billion in 2025, with implementation services representing more than half. Public-sector agencies are especially active; only 17% of UK decision makers deemed earlier initiatives successful, and 63% expect higher budgets for third-party support. This momentum sustains demand across all industries as digital capabilities shift from optional efficiency plays to the baseline for competitiveness.

Growing Data-Analytics and AI Adoption

AI consulting now represents the steepest growth slope. Leading consultancies tripled AI revenues to roughly USD 900 million annually, and one major strategy firm generated one-fifth of total fees from AI within two years. With 79% of executives convinced generative AI will reshape their companies and 91% expecting productivity lifts, advisory needs span strategy, data-fabric design, model governance, and workforce re-skilling. The value proposition rests on turning proof-of-concept pilots into scaled, production-grade systems that integrate compliantly with core business processes.

Looming SAP ECC Sunset Fuelling S/4HANA Consulting Demand

SAP will cease mainstream maintenance for Business Suite 7 on 31 December 2027. Only 28% of the original 35,000 ECC customers were live on S/4HANA by end-2023. Projects involve data cleansing, process standardization, and change management that can span seven years. Studies show 65% of early adopters missed quality targets and 55% overshot budgets, reinforcing the premium on seasoned consulting talent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened cybersecurity and data-privacy concerns | -1.8% | Global, strongest in Europe | Medium term (2-4 years) |

| Talent shortage and rising consulting rates | -2.3% | Global, North America and Europe acute | Short term (≤ 2 years) |

| Rapid low-code / no-code adoption | -1.5% | Global, SME-led | Long term (≥ 4 years) |

| Gen-AI automating basic advisory tasks | -1.1% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Cybersecurity and Data-Privacy Concerns

Cyber risk escalates faster than defensive postures. Three-quarters of enterprises raised security budgets, yet execution lags as talent shortages stretch project timelines. The United States needs 225,000 additional cybersecurity professionals, while Europe faces overlapping mandates such as the EU AI Act and Data Act.[2]Clar Rosso, “Cybersecurity Workforce Study 2024,” isc2.org These frameworks lengthen deployment schedules and inflate engagement costs as consultants navigate privacy-by-design requirements alongside business goals. The dilemma both fuels security consulting demand and constrains overall delivery velocity.

Talent Shortage and Rising Consulting Rates

Global shortfalls could leave 85 million technical jobs vacant by 2030, with potential USD 8.4 trillion revenue at risk. The United States already tracks 918,000 open technology roles. Major Indian IT firms plan aggregate hiring of more than 60,000 graduates for FY26, yet attrition persists. Wage inflation and aggressive retention incentives pressure margins, particularly for mid-tier consultancies.[3]US Bureau of Labor Statistics, “Employment Projections 2024-2030,” bls.gov Firms have responded with expanded training programs, automation of repeatable tasks, and offshore delivery hubs, but the skills gap continues to limit project throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: AI Consulting Drives Premium Growth

Application development and modernization retained 37.72% software consulting market share in 2025, reflecting the urgency to re-platform legacy applications on cloud-native, API-centric stacks. Enterprises depend on these services to unlock continuous deployment, improve system resilience, and reduce ownership costs. The segment remains anchored in large-scale refactoring and containerization projects that support omnichannel and real-time use cases across verticals.

Data and AI/ML consulting posts the fastest 17.02% CAGR toward 2031. Clients view machine learning models, predictive analytics, and generative AI frameworks as differentiators rather than efficiency levers. Advisory scope is expanding from algorithm selection to data-fabric design, ethical guardrails, and value-tracking dashboards. As model risks attract regulatory scrutiny, demand is shifting toward explainability assessments and governance protocols embedded into end-to-end AI pipelines.

By Deployment Model: Hybrid Architectures Gain Momentum

On Premises retained 53.88% share of the software consulting market size in 2025, propelled by scalability and pay-as-you-go economics that appeal to both greenfield and modernization programs. Offerings now span platform refactoring, DevSecOps automation, and cloud FinOps advisory that helps enterprises rein in rising consumption costs.

Also the cloud architectures record the highest 19.12% CAGR. Clients favor workload portability for data sovereignty and vendor risk mitigation. Consulting demand concentrates on cloud center-of-excellence design, unified observability stacks, and secure connectivity between on-premise, edge, and public cloud nodes. Edge computing adds complexity as 75% of enterprise data is processed closer to its source, generating new opportunities for architects versed in distributed data governance.

By Enterprise Size: SME Adoption Accelerates

Large enterprises continued to command 62.65% of the software consulting market size in 2025, leveraging deep budgets and global footprints that require multifaceted transformation programs. Engagements range from strategic road-mapping to full-stack implementation, often spanning finance, supply chain, and customer-experience revamps delivered across multiple continents.

SMEs show the briskest 16.84% CAGR, fueled by lower entry barriers from cloud-delivered consulting models and the democratization of low-code development. “Citizen developer” programs are proliferating, yet governance gaps remain, opening advisory niches in platform oversight, security, and skills enablement. Fixed-price, outcome-based packages are gaining favor among SMEs seeking predictable costs.

By End-User Industry: Healthcare Leads Growth Trajectory

BFSI accounted for 24.18% share of the software consulting market size in 2025. Regulatory reporting automation, open-banking API strategies, and AI-driven fraud detection dominate project pipelines. Consultancies with sector-specific accelerators and compliance frameworks command premium rates.

Healthcare and life sciences expand to 16.42% CAGR. Telemedicine platforms, IoMT ecosystems, and AI-powered diagnostics drive complex integrations with electronic health records. Data-privacy mandates such as HIPAA intensify the need for specialized domain knowledge. Supporting services now include algorithm-bias audits, clinical-workflow redesign, and secure cloud migration for sensitive patient data.

Geography Analysis

North America led with 27.55% market share in 2025, backed by strong enterprise IT budgets and a dense ecosystem of technology vendors and hyperscale clouds. US consulting expenditure approaches USD 400 billion annually, with advanced analytics outlays expected to rise 11% in 2025. Canada contributes meaningful growth through public-sector modernization and energy-sector digitization projects.

Asia-Pacific is the fastest-growing region, advancing at an 18.02% CAGR. India’s technology spending will reach USD 59 billion in 2025, driven by government digital initiatives and manufacturing modernization. China’s enterprises invest heavily in AI-enabled supply chains and smart factories, while Southeast Asian governments ramp up e-services and cybersecurity frameworks that require external advisory capabilities. Japan and South Korea sustain momentum through advanced manufacturing and 5G-driven applications.

Europe demonstrates steady expansion anchored by Germany, which holds roughly one-quarter of regional software value. SMEs are upgrading ERP and customer-experience platforms to compete globally. The EU AI Act introduces stringent governance obligations, boosting consulting demand for compliance assessments and audit-ready AI architectures. Nordic countries maintain outsized influence thanks to export-oriented software ecosystems and early adoption of cloud-first policies.

Mordor Intelligence provides coverage of the software consulting market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The software consulting market features moderate fragmentation. Accenture leads with USD 67.2 billion FY24 revenue, propelled by a USD 3 billion investment commitment in generative AI partnerships and talent.[5]Julie Sweet, “Accenture Reports Fourth-Quarter and Full-Year 2024 Results,” accenture.comThe firm’s Copilot collaboration with Microsoft underpins end-to-end productivity solutions across finance, supply chain, and customer service.

Indian majors strengthen share based on cost-effective global delivery. TCS posted USD 30.18 billion FY25 revenue and is scaling AI services through its proprietary cognitive suite. Infosys earned USD 4.94 billion during its most recent quarter and focuses on AI-first transformation, cloud modernization, and ESG reporting solutions.

Strategic acquisitions shape competitive dynamics. IBM added Hakkoda to deepen Snowflake and data-engineering expertise, complementing earlier purchases of Accelalpha and Applications Software Technology for Oracle-cloud consulting. Cognizant’s proposed USD 1.3 billion Belcan deal extends engineering R&D capabilities. Big Four professional-services firms collectively invested more than USD 4 billion in AI tooling to defend share against IT-services incumbents.

White-space prospects lie in quantum-safe cryptography advisory, AI governance frameworks, and verticalized large-language-model offerings. Boutique firms with niche IP and accelerator assets remain attractive targets as large players seek differentiation through specialized capability bundles.

Software Consulting Industry Leaders

Capgemini

Accenture PLC

Cognizant

Deloitte

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Accenture and Yumemi announced a strategic partnership to enhance digital product development capabilities, leveraging combined expertise to deliver innovative solutions.

- April 2025: IBM acquired Hakkoda to expand its data analytics and AI consulting offerings within a broader AI-first strategy.

- April 2025: Capgemini entered talks to acquire India’s WNS Holdings, potentially broadening its BPO and consulting reach.

- January 2025: Intel and Softtek partnered to drive digital transformation in Latin America and the United States with AI solutions built on Intel Gaudi accelerators and the openVINO toolkit.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the software consulting market as fee-based professional services that assess, design, integrate, modernize, or secure software systems across enterprise workloads, whether hosted on-premise or in public, private, or hybrid clouds. Engagements can span discrete advisory mandates through multi-year transformation programs but always center on software-focused guidance rather than hardware resale or pure staffing.

Scope exclusion: Pure infrastructure break-fix contracts, staff-augmentation body-shops, and packaged software license revenue remain outside this view.

Segmentation Overview

- By Service Type

- Application development and modernisation

- Enterprise solution integration

- Cloud migration and managed services

- Software security consulting

- Data and AI/ML consulting

- Others

- By Deployment Model

- On-premise

- Cloud

- By End-user Enterprise Size

- Large enterprises

- Small and medium enterprises (SMEs)

- By End-user Industry

- BFSI

- Healthcare and life-sciences

- Manufacturing and industrial

- Retail and e-commerce

- Government and public sector

- Telecom and media

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Switzerland

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Vietnam

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- Nigeria

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed software leaders in North America, Europe, and fast-growing Asian hubs, along with procurement heads at mid-market banks, health-systems CIOs, and cloud platform alliance managers. Their insights refined deal-size distributions, price erosion curves, and cloud migration velocities that desktop sources could only hint at.

Desk Research

We began with structured desk work, tapping statistical portals such as UN Comtrade for cross-border software service exports, US Bureau of Economic Analysis tables for management and IT consulting receipts, and Eurostat's ICT usage surveys. Industry bodies like the Information Services Group Index and CompTIA's State of the Tech Workforce add spend patterns, while academic journals in IEEE Xplore clarify emerging demand triggers around cloud-native and AI engineering. Subscription resources from D&B Hoovers and Dow Jones Factiva helped our analysts map the financial weight of leading vendors. These sources, among others, supplied baseline ratios on project size, service mix, and regional adoption. The list above is illustrative; many additional references informed our work.

The spectrum of secondary inputs built the skeleton, yet sector granularity often lags real-time shifts. Therefore, we focused our primary outreach on filling those gaps.

Market-Sizing & Forecasting

A top-down view starts with national ICT service output and trade data, which are then filtered through consulting-specific intensity ratios and adjusted for service scope. Select bottom-up checks, including sample vendor revenue roll-ups and typical average-selling-price times project counts, validate and tune totals. Key inputs include:

1. Public cloud spend as a share of enterprise IT budgets, 2. Average digital transformation deal value, 3. Utilization of agile and DevOps contracts, 4. Regional consulting wage inflation, 5. Penetration of Gen-AI pilot projects.

We project each driver via multivariate regression, stress-testing with scenario analysis before blending into our five-year CAGR. Any data voids in bottom-up estimates are bridged by weighted averages from comparable regions or adjacent service lines.

Data Validation & Update Cycle

Outputs pass a three-layer review: analyst peer check, senior domain lead sign-off, and automated variance alerts versus independent indicators. The model refreshes annually, with interim updates triggered by material M&A, regulation, or macro shocks.

Why Mordor's Software Consulting Baseline Is Reliably Grounded

Published figures diverge because firms choose different service scopes, pricing curves, and refresh cadences.

Our disciplined scoping and driver selection minimize such variance.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 327.59 B (2025) | Mordor Intelligence | - |

| USD 342.10 B (2024) | Global Consultancy A | Counts one-off staff-augmentation deals within consulting totals |

| USD 282.40 B (2024) | Research Firm B | Excludes cloud-native advisory that we and most clients view as core |

| USD 305.55 B (2023) | Industry Publisher C | Uses historical three-year average ASPs, muting recent price inflation |

Differences mainly stem from whether modernization and security advisory are in scope, how hybrid cloud premiums are priced, and the vintage of cost indices applied. By anchoring numbers to clear variables and revisiting them every year, Mordor Intelligence delivers a baseline that decision-makers can retrace and trust.

Key Questions Answered in the Report

What is the software consulting market size in 2026?

The software consulting market size is USD 380.26 billion in 2026.

What compound annual growth rate (CAGR) is expected for the market through 2031?

The market is projected to expand at a 16.08% CAGR between 2026 and 2031.

Which service line is growing the fastest?

Data and AI/ML consulting services post the highest 17.02% CAGR as enterprises prioritize intelligent automation and predictive analytics.

Which geography shows the strongest growth outlook?

Asia–Pacific leads regional growth with an 18.02% CAGR driven by India’s rising tech outlays and China’s enterprise-modernization programs.

Why does the SAP ECC sunset matter for consulting demand?

SAP will end mainstream maintenance for Business Suite 7 on 31 December 2027, and 70% of customers have yet to migrate, creating a surge in S/4HANA consulting projects .

Page last updated on: