Software Bill Of Materials (SBOM) Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

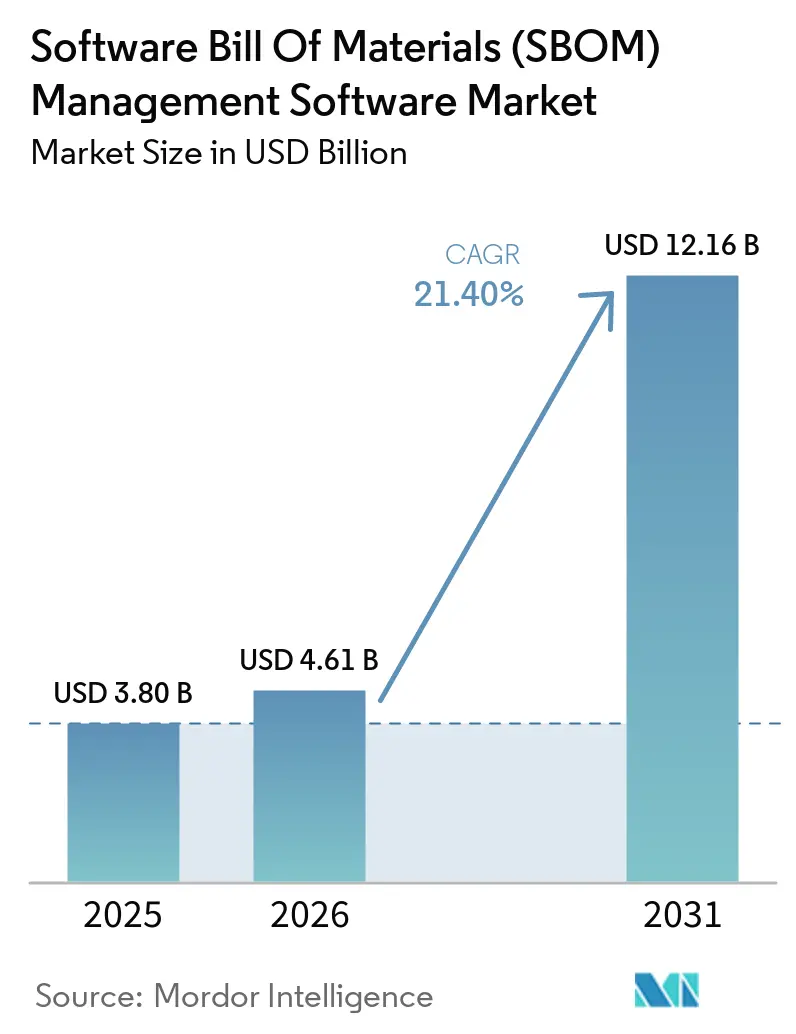

| Market Size (2026) | USD 4.61 Billion |

| Market Size (2031) | USD 12.16 Billion |

| Growth Rate (2026 - 2031) | 21.40% CAGR |

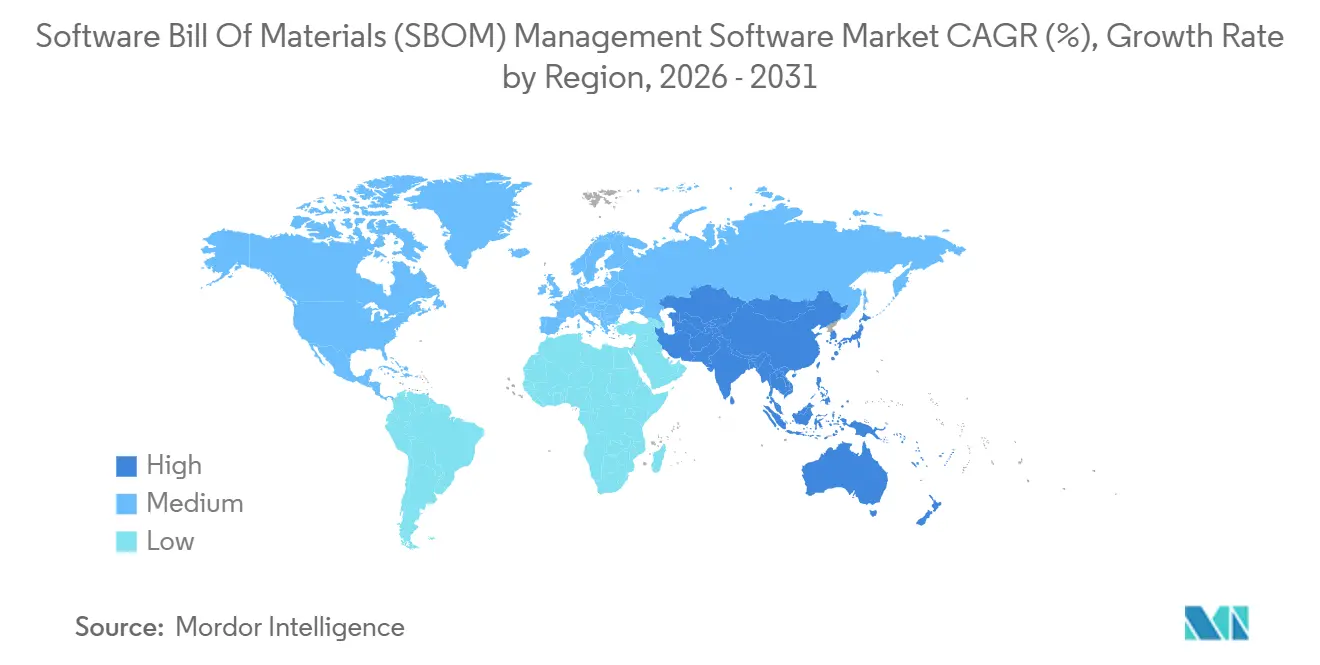

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software Bill Of Materials (SBOM) Management Software Market Analysis by Mordor Intelligence

The Software Bill of Materials market size was valued at USD 3.8 billion in 2025 and estimated to grow from USD 4.61 billion in 2026 to reach USD 12.16 billion by 2031, at a CAGR of 21.4% during the forecast period (2026-2031). Growing global mandates for supply-chain visibility, a surge in open-source attacks, and the mainstreaming of DevSecOps are shifting SBOM adoption from optional compliance to routine engineering practice. Vendors are racing to automate SBOM creation inside continuous integration pipelines, while enterprises look beyond generation toward automated vulnerability triage and supplier governance. Format interoperability between SPDX and CycloneDX remains an operational hurdle, especially for small and medium enterprises, and is stalling uniform data exchange. Meanwhile, artificial-intelligence engines embedded in SBOM tools are helping security teams collapse remediation windows, reinforcing the technology’s strategic value.

Key Report Takeaways

- By geography, North America led with 37.2% of the Software Bill of Materials (SBOM) Management Software Market share in 2025 and is forecast to maintain leadership through aggressive federal procurement rules and medical-device oversight.

- By application, healthcare held 24.2% of the Software Bill of Materials (SBOM) Management Software Market demand in 2025, while defense is projected to advance at an 18.6% CAGR through 2031, the fastest among all use cases.

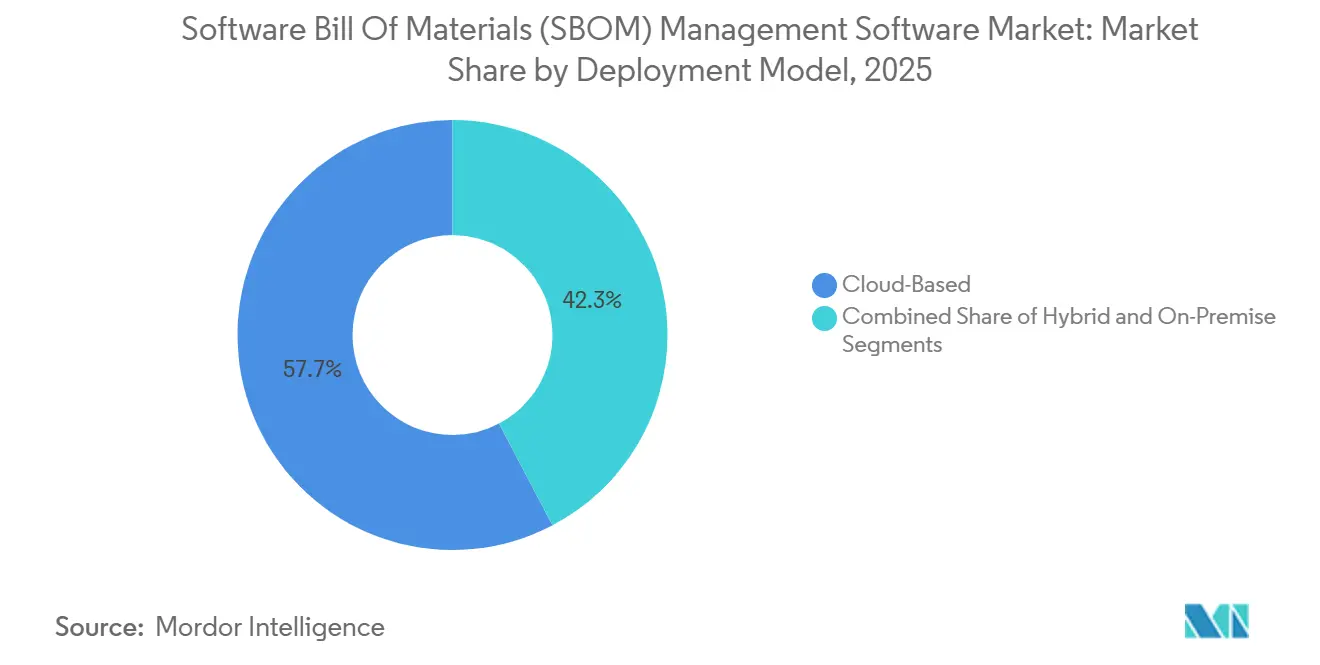

- By deployment mode, cloud platforms captured 57.7% revenue of the Software Bill of Materials (SBOM) Management Software Market in 2025; hybrid models are expanding at a 17.2% CAGR as regulated industries blend on-premise control with cloud scalability.

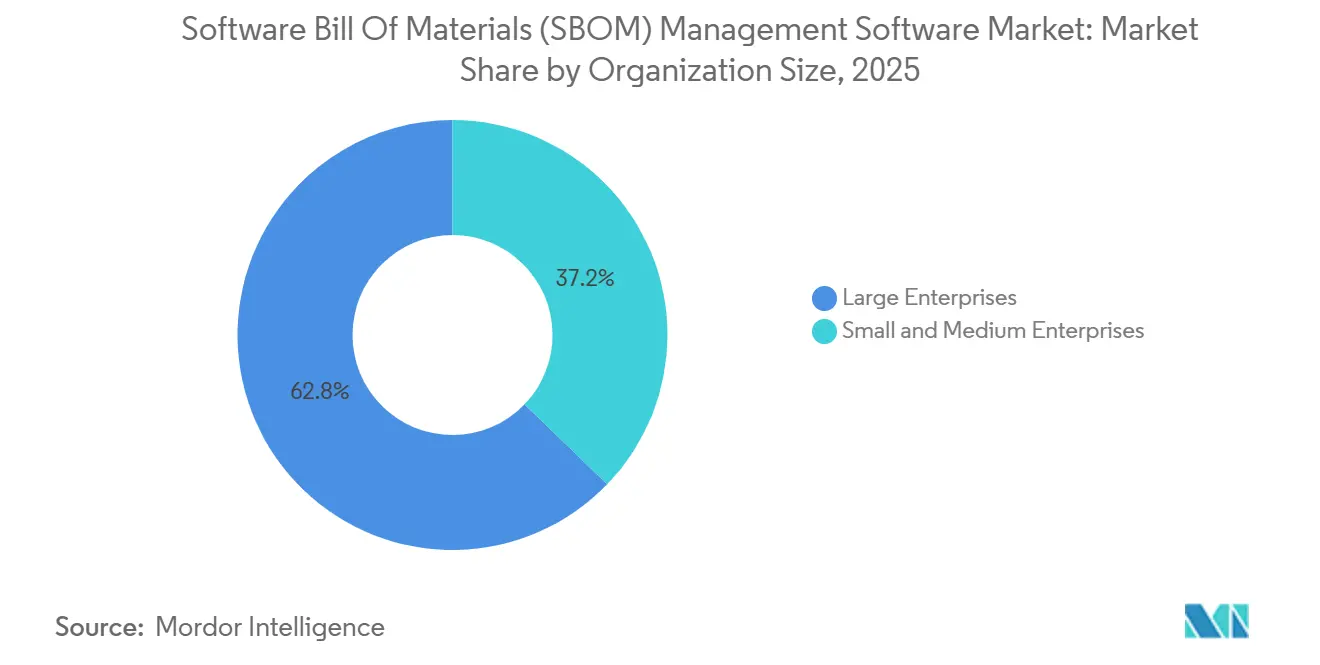

- By organization size, large enterprises accounted for 62.8% revenue of the Software Bill of Materials (SBOM) Management Software Market in 2025, whereas small and medium enterprises represent the fastest-growing cohort at a 19.6% CAGR.

- By component, software platforms delivered 70.9% of the Software Bill of Materials (SBOM) Management Software Market 2025 revenue, yet services will post an 18.3% CAGR as operationalization complexity deepens.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Software Bill Of Materials (SBOM) Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Regulatory Mandates for Software Supply Chain Transparency | 6.20% | Global, early enforcement in North America and Europe | Short term (≤ 2 years) |

| Escalating Cybersecurity Threats Targeting Open-Source Components | 5.80% | Global, acute exposure in North America and Asia-Pacific | Medium term (2–4 years) |

| Rising Adoption of DevSecOps Practices Across Enterprises | 4.10% | North America and Europe, spillover to Asia-Pacific | Medium term (2–4 years) |

| Increasing Integration of SBOM Platforms with CI/CD Pipelines | 3.70% | Global, concentrated in technology hubs | Short term (≤ 2 years) |

| Emergence of AI-Powered Vulnerability Prioritization in SBOM Tools | 2.90% | North America and Europe | Long term (≥ 4 years) |

| Expansion of Software Composition Analysis into IoT Firmware SBOM | 2.60% | Global, early uptake in healthcare and automotive | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Regulatory Mandates for Software Supply Chain Transparency

Governments worldwide codified SBOM disclosure as a purchasing prerequisite, transforming a voluntary best practice into an enforceable obligation. In January 2025, the United States Cybersecurity and Infrastructure Security Agency directed all federal bodies to verify SBOM accuracy for critical systems by September 2026, extending Executive Order 14028’s reach.[1]Cybersecurity and Infrastructure Security Agency, “SBOM Sharing Roles and Considerations,” cisa.govThe European Union’s Cyber Resilience Act, effective December 2024, compels manufacturers of products with digital elements to produce machine-readable SBOMs starting September 2026, widening the obligation to hardware with embedded firmware.[2]Federal Office for Information Security, “Technical Guideline TR-03183-2,” bsi.bund.de Parallel rules from the United States Food and Drug Administration now bind medical-device approval to SBOM submission timelines, further institutionalizing transparency.[3]U.S. Food and Drug Administration, “Cybersecurity in Medical Devices,” fda.gov Multinational vendors are therefore investing in platforms that export multiple formats and map policies automatically to divergent regional schemas, converting regulatory complexity into a catalyst for tooling spend.

Escalating Cybersecurity Threats Targeting Open-Source Components

Supply-chain attacks rose sharply as adversaries seeded malicious libraries into public repositories and exploited dormant flaws in legacy dependencies. Sonatype logged more than 245,000 rogue packages uploaded in 2024, up 156% year on year, underscoring the scale of opportunistic infiltration. The United States Known Exploited Vulnerabilities catalog topped 1,200 entries by early 2026, with a growing share linked to unpatched open-source modules inside commercial products. A March 2026 breach attempt on Trivy, an open-source SBOM generator, demonstrated that even security tooling itself is now a target.[4]Chainguard, “Supply Chain Attack on Trivy,” chainguard.devOrganizations increasingly view SBOMs as the only practical way to pinpoint exposure quickly when zero-days emerge, compressing mean time to remediation and limiting lateral attack movement.

Rising Adoption of DevSecOps Practices Across Enterprises

Embedding security checks in developer workflows accelerated between 2024 and 2026 as teams acknowledged that post-deployment scans cannot keep pace with rapid release cadences. SBOM creation shifted left inside integrated development environments, giving coders instantaneous feedback on risky dependencies before commits land. Snyk’s June 2025 acquisition of Invariant Labs fused runtime insights with build-time SBOM analysis, signaling a competitive pivot from compliance dashboards toward developer experience. Enterprises that re-engineered pipelines reported 40% faster remediation cycles in 2025, converting security from a bottleneck into a parallelized capability.

Increasing Integration of SBOM Platforms with CI/CD Pipelines

Continuous-integration plugins now auto-generate SBOM artifacts at build time, erasing manual inventory tasks that once delayed releases. Anchore rolled out a lightweight CLI in May 2025 that exports both SPDX and CycloneDX, reflecting market appetite for integrated generation and format flexibility. Chainguard’s Repository beta, launched March 2026, attaches SBOMs automatically to every pushed container, giving DevOps teams a zero-touch path to compliance. Companies adopting these automated flows shaved compliance-audit preparation by 60% in 2025, translating process efficiency into tangible cost savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Standardization Across SBOM Formats and Exchange Protocols | -3.40% | Global, acute in cross-border supply chains | Medium term (2–4 years) |

| Limited Awareness Among Small and Medium Enterprises | -2.80% | Global, highest impact in emerging markets and Asia-Pacific | Short term (≤ 2 years) |

| Concerns Over Intellectual Property Exposure in SBOM Disclosure | -1.90% | Global, concentrated in competitive technology sectors | Long term (≥ 4 years) |

| Inadequate Integration With Legacy Application Security Tools | -1.60% | North America and Europe, where legacy infrastructure persists | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardization Across SBOM Formats and Exchange Protocols

The coexistence of SPDX and CycloneDX, each advancing on separate roadmaps, forces enterprises to juggle parallel toolchains or resort to lossy conversion utilities. The United States National Telecommunications and Information Administration recognized both schemas but stopped short of naming a single canonical standard, inadvertently entrenching fragmentation. Small vendors in industrial and consumer sectors struggle to fund adapters, delaying ecosystem-wide interoperability and shaving 3.4 percentage points from forecast growth.

Limited Awareness Among Small and Medium Enterprises

Many small and medium enterprises still regard SBOMs as a large-buyer compliance hurdle rather than a security imperative, especially in markets where government outreach is nascent. These enterprises often lack the financial resources and technical expertise to implement robust SBOM processes, leading to a continued reliance on manual spreadsheets. This reliance perpetuates blind spots in their security frameworks, leaving them vulnerable to potential risks. While managed service providers began integrating SBOM capabilities into broader security offerings during 2025, the adoption rate remains slow. This is particularly evident in regions such as Asia-Pacific and Latin America, where knowledge gaps and limited awareness of SBOM benefits hinder widespread implementation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Architectures Emerge as the Preferred Model

Hybrid setups are on track to expand at a 17.2% CAGR through 2031 as highly regulated verticals reconcile cloud agility with strict data-sovereignty rules. While cloud services commanded 57.7% revenue in 2025, organizations handling classified, patient, or financial data increasingly split workloads, keeping raw SBOM files on-premise and sending analytics to the cloud. The Food and Drug Administration’s 2025 guidance spurred medical-device makers to adopt such dual architectures, safeguarding proprietary firmware details while satisfying disclosure mandates.

Enterprises adopting hybrid models reported 30% shorter evidence-collection cycles for ISO 27001 and SOC 2 audits compared with pure on-premise users, underscoring a practical payoff. As cloud platforms embed SBOM hooks into container registries and vulnerability scanners, on-premise components increasingly act as secure enclaves rather than analytic engines. This structural shift positions hybrid designs as the default for the Software Bill of Materials market by late decade, fostering ecosystem demand for unified dashboards that span private data centers and hyperscale clouds.

By Application: Defense and Regulated Industries Drive Adoption Momentum

Defense workloads are projected to register an 18.6% CAGR, the highest among all applications. This growth is primarily driven by the Department of Defense’s mandate to incorporate Software Bill of Materials (SBOM) verification into Cybersecurity Maturity Model Certification (CMMC) 2.0 assessments. The requirement compels contractors to provide continuous attestations, ensuring compliance with stringent cybersecurity standards. This shift is pushing automation into traditionally waterfall development processes, which have historically been slower to adopt such technologies. The demand for real-time verification and reporting is expected to drive innovation in SBOM tools, enabling defense contractors to streamline their workflows while meeting regulatory requirements.

Healthcare remains the revenue leader thanks to a 24.2% share in 2025, yet its growth moderates because mandates apply chiefly to new device submissions. Automotive and industrial manufacturers are moving up the adoption curve as United Nations WP.29 rules and industrial safety norms increasingly reference component transparency. These cross-sector pressures reinforce the centrality of SBOMs to physical-safety risk management, broadening total addressable demand for the Software Bill of Materials market.

By Organization Size: SMEs Emerge as the Fastest-Growing Segment

Large enterprises continue to dominate spending in the Software Bill of Materials (SBOM) market, accounting for 62.8% of the projected revenue in 2025. These organizations benefit from well-established DevSecOps pipelines and dedicated security teams, enabling them to integrate SBOM practices seamlessly into their workflows. Their ability to allocate significant resources toward compliance and security measures ensures they remain at the forefront of SBOM adoption. However, small and medium enterprises (SMEs) are emerging as the fastest-growing segment in this market, with a compound annual growth rate (CAGR) of 19.6%. The availability of cloud marketplaces offering push-button SBOM generation and license-compliance checks has been a game-changer for SMEs.

Supply-chain pressures are further driving the adoption of SBOM practices, particularly among SMEs. Industries such as automotive and aerospace are increasingly enforcing stricter compliance measures, with prime contractors blacklisting suppliers unable to provide machine-readable SBOMs. This trend has created a significant demand for managed service providers (MSPs) to bridge the skills gap. MSPs are now offering comprehensive solutions that include SBOM generation, triage, and audit-ready reporting, all bundled into affordable monthly subscription models. As the cost of these services continues to decline and awareness of SBOM benefits grows, SMEs are transitioning from being laggards in adoption to becoming key drivers of market growth.

By Component: Services Gain Traction as Implementation Complexity Rises

Software platforms accounted for 70.9% of 2025 revenue, highlighting their dominant role in the market. However, services are rapidly gaining traction, growing at a robust CAGR of 18.3%. This growth is driven by the fact that while generating an SBOM is relatively straightforward, translating it into actionable risk-reduction measures remains a significant challenge for many enterprises. Organizations face difficulties in integrating SBOM feeds into critical operational processes, such as incident-response playbooks, supplier scorecards, and procurement decision-making frameworks. These challenges have created opportunities for consultancies and managed service providers to step in and offer tailored solutions.

Training and certification programs surfaced in 2025 to close practitioner gaps, while platform vendors bundle advisory bundles to upsell high-margin engagements. Unified suites from Veracode and Snyk now merge static, dynamic, and composition analyses, shrinking implementation cycles but increasing the need for change-management assistance. The shift underscores a maturation path where technology alone cannot unlock full value, propelling steady service uptake across the Software Bill of Materials market.

Geography Analysis

North America accounted for 37.2% of 2025 revenue, anchored by federal procurement mandates and a dense concentration of medical-technology and SaaS vendors. The January 2025 CISA directive and the Food and Drug Administration’s Section 524B guidance jointly heighten disclosure expectations, turning SBOM creation into a go-to-market necessity rather than a best practice. Canadian suppliers mirror the United States momentum to remain viable in cross-border supply chains, while Mexico’s adoption clusters around automotive and aerospace export hubs.

Europe follows with robust growth as the Cyber Resilience Act pushes compliance deadlines toward September 2026. Germany’s technical guideline TR-03183-2 serves as a blueprint for critical-infrastructure operators and ripples outward to the wider European Union. Post-Brexit, the United Kingdom keeps tight alignment to preserve single-market access, underlining the region’s unified trajectory. Hardware makers embedding firmware now fall under the same transparency rules as pure software publishers, broadening the European Software Bill of Materials market addressable base.

Asia-Pacific is forecast to rise at a 16.4% CAGR, the fastest globally, thanks to China’s Multi-Level Protection Scheme 2.0, Japan’s Information-technology Promotion Agency guidelines, and India’s CERT-In advisories. Domestic sovereignty policies drive Chinese demand for locally hosted tools and data-residency guarantees. Japan’s automotive giants, responding to WP.29 export obligations, embed SBOM workflows into supply-chain contracts, radiating requirements to component suppliers. While Middle East and Africa plus South America lag in formal mandates, multinational operators import their own standards, seeding initial footprints for the Software Bill of Materials market across energy, telecom, and banking sectors.

Competitive Landscape

The Software Bill of Materials market shows moderate fragmentation, with consolidation moves by incumbent security vendors and disruptive plays by cloud-native specialists. Veracode’s January 2025 purchase of Phylum extended its static and dynamic testing suite with malicious-package analytics, reflecting a one-stop-shop thesis. This acquisition highlights the growing demand for comprehensive solutions that address multiple aspects of software security within a single platform. Similarly, Snyk’s acquisition of Invariant Labs six months later provided developers with runtime context inside integrated environments, emphasizing the importance of seamless integration and real-time insights in the DevSecOps ecosystem. These moves underscore a competitive race among vendors to dominate the unified DevSecOps console, catering to the evolving needs of development and security teams.

Startups such as Chainguard and Stacklok differentiate themselves through innovative offerings like distroless images and sigstore-based attestations. These solutions appeal to cloud-first teams that prioritize reducing the attack surface and implementing zero-trust pipelines. By focusing on these specialized needs, these startups are carving out a niche in the market. Additionally, FOSSA’s 2026 acquisition of EdgeBit signals a strategic interest in runtime correlation capabilities. This enables customers to identify and deprioritize dormant code that remains present in build artifacts, addressing a critical gap in software security. Such developments highlight the increasing focus on precision and efficiency in managing software vulnerabilities.

As hyperscale cloud providers integrate SBOM generation into their native registries, standalone tools face the risk of commoditization. This shift is driving competition toward advanced analytics, policy automation, and ecosystem integrations that enhance the overall value proposition and increase the cost of switching for customers. Vendor positioning in the market now revolves around three critical areas: the depth of CI/CD automation, the accuracy of detecting transitive dependencies across polyglot stacks, and the ability to seamlessly interchange between SPDX and CycloneDX files. These factors are becoming key differentiators as vendors strive to meet the complex demands of modern software development and security practices.

Software Bill Of Materials (SBOM) Management Software Industry Leaders

Synopsys Inc.

Sonatype Inc.

Snyk Limited

JFrog Ltd.

Anchore Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Chainguard launched Commercial Builds and Repository beta, delivering on-push SBOM generation inside a managed container registry.

- March 2026: Snyk released Agent Security and Evo AI-SPM, fusing large-language-model insights with SBOM data for tailored remediation guidance.

- March 2026: A supply-chain attack targeted open-source tool Trivy, prompting Chainguard to publish forensic findings and intensify distroless-image promotion.

- January 2026: FOSSA bought EdgeBit to integrate runtime SBOM correlation into its composition-analysis platform.

Global Software Bill Of Materials (SBOM) Management Software Market Report Scope

The Software Bill of Materials (SBOM) Management Software Market refers to tools and platforms that generate, manage, and distribute detailed inventories of software components, including open-source and third-party dependencies. These solutions help organizations track component origins, licenses, and vulnerabilities to enhance software supply chain transparency and security. They are widely used in DevSecOps environments to support compliance with regulatory requirements and secure software development practices.

The Software Bill of Materials Report is Segmented by Deployment Mode (On-Premise, Cloud-Based, Hybrid), Application (Healthcare, Automotive, Defense, Consumer Electronics, Industrial, Other Applications), Organization Size (Large Enterprises, Small and Medium Enterprises), Component (Software Platform, Services), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud-Based |

| Hybrid |

| Healthcare |

| Automotive |

| Defense |

| Consumer Electronics |

| Industrial |

| Other Applications |

| Large Enterprises |

| Small and Medium Enterprises |

| Software Platform |

| Services |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Deployment Mode | On-Premise | |

| Cloud-Based | ||

| Hybrid | ||

| By Application | Healthcare | |

| Automotive | ||

| Defense | ||

| Consumer Electronics | ||

| Industrial | ||

| Other Applications | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Component | Software Platform | |

| Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Software Bill of Materials market today and what is its growth outlook?

The Software Bill of Materials market size stood at USD 4.61 billion in 2026 and is projected to reach USD 12.16 billion by 2031, reflecting a 21.4% CAGR.

Which region leads adoption of SBOM platforms?

North America held 37.2% revenue share in 2025, propelled by federal cybersecurity mandates and medical-device regulations.

What application area is expanding the fastest?

Defense use cases are forecast to grow at an 18.6% CAGR as the Department of Defense embeds SBOM checks into contractor certification.

Why are hybrid deployments gaining traction?

Hybrid models offer the cloud's scalability while allowing regulated sectors to retain sensitive SBOM data on-premise, driving a 17.2% CAGR through 2031.

How are small and medium enterprises adopting SBOMs?

Managed service providers now bundle generation and compliance reporting, enabling small and medium enterprises to post a 19.6% CAGR despite limited in-house security staff.

What is the biggest technical hurdle to widespread SBOM exchange?

Lack of harmonized standards between SPDX and CycloneDX formats forces many organizations to support dual workflows, slowing seamless data sharing.

Page last updated on: