Rapid Application Development Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

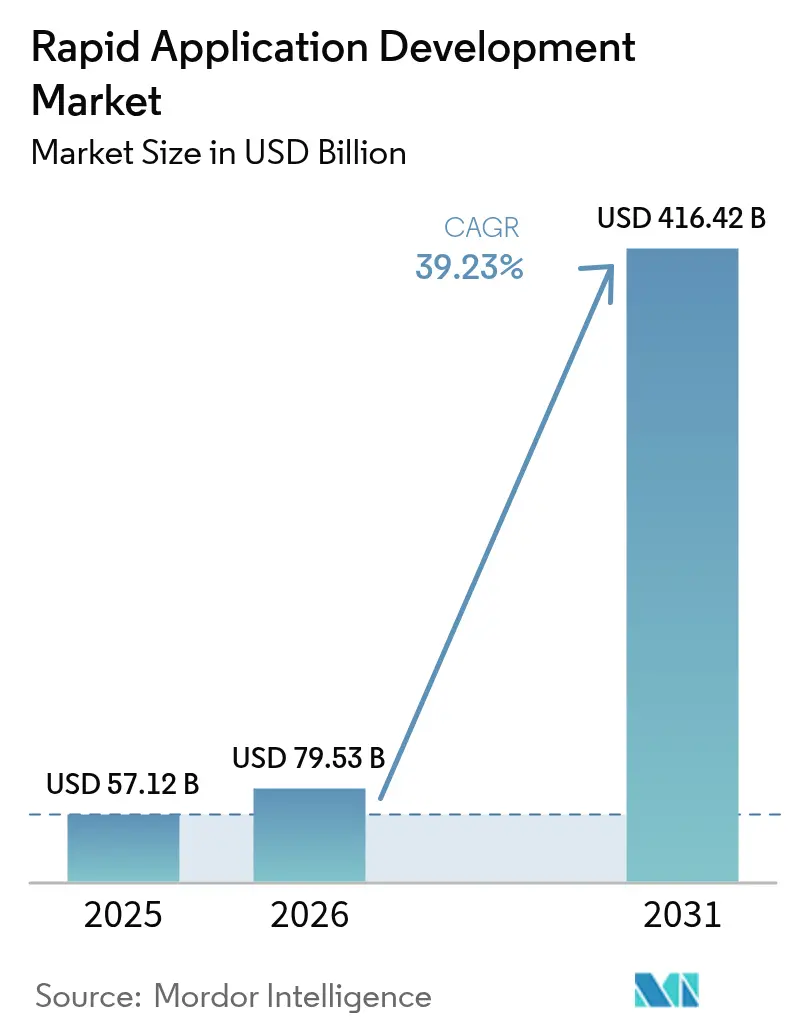

| Market Size (2026) | USD 79.53 Billion |

| Market Size (2031) | USD 416.42 Billion |

| Growth Rate (2026 - 2031) | 39.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

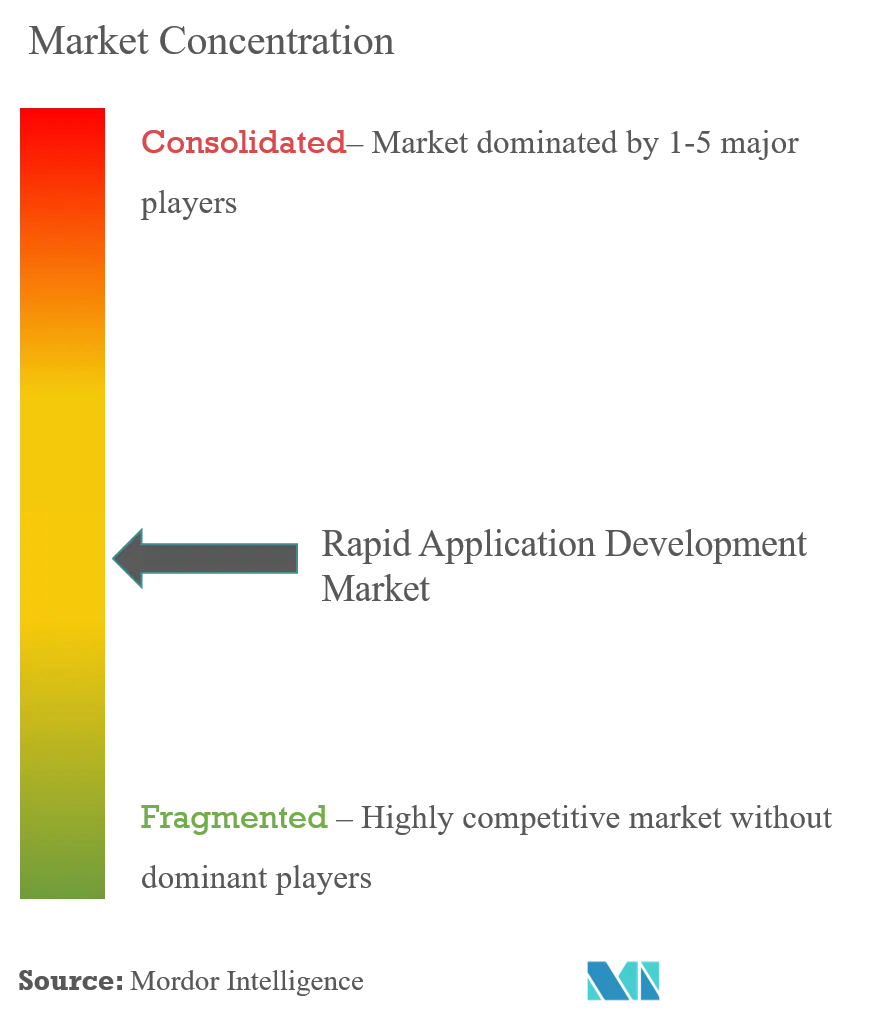

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rapid Application Development Market Analysis by Mordor Intelligence

The rapid application development market size was valued at USD 57.12 billion in 2025 and estimated to grow from USD 79.53 billion in 2026 to reach USD 416.42 billion by 2031, at a CAGR of 39.23% during the forecast period (2026-2031). Demand accelerates as enterprises shift from lengthy waterfall cycles to platforms that compress build times from quarters to weeks, a trend intensified by chronic software developer shortages and initiatives to digitize aging workflows. Low-code platforms support professional developers who want speed without sacrificing control, while no-code tools empower business users to build departmental apps, expanding the total creator base. Cloud deployment continues to outpace on-premise installations because it delivers elastic scalability, automatic updates, and consumption-based pricing that aligns operating costs with usage. Meanwhile, generative AI embedded in platforms such as Salesforce Einstein GPT and Microsoft Copilot Studio drafts logic from natural language prompts, further reducing the time-to-market for customer-facing and internal tools. Competitive intensity is rising as hyperscalers bundle RAD features into broader cloud subscriptions, pressuring standalone vendors on pricing, even as verticalized templates and AI-assisted governance offer new avenues for differentiation.

Key Report Takeaways

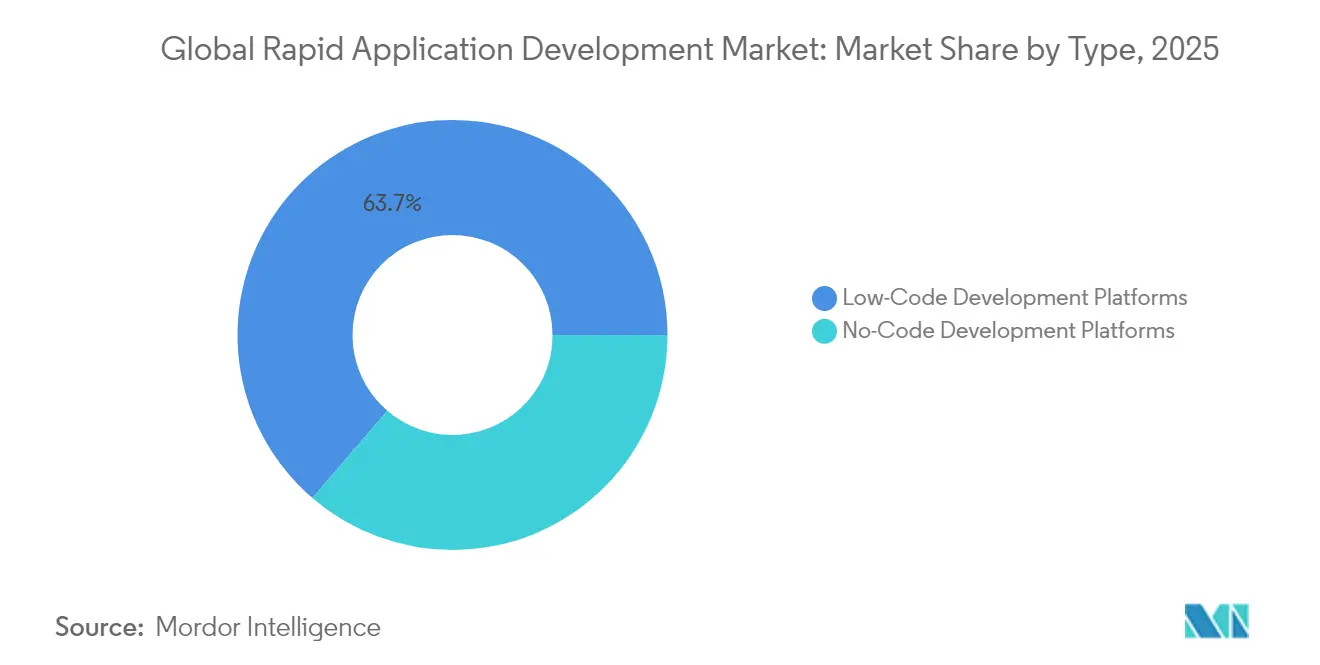

- By type, low-code development platforms led with 63.70% revenue share of the rapid application development market in 2025; no-code development platforms are forecast to register a 41.20% CAGR through 2031, the fastest among all categories.

- By deployment mode, cloud deployment captured 73.15% share of the rapid application development market in 2025; cloud deployment is projected to grow at a 40.95% CAGR through 2031, outpacing on-premise installations.

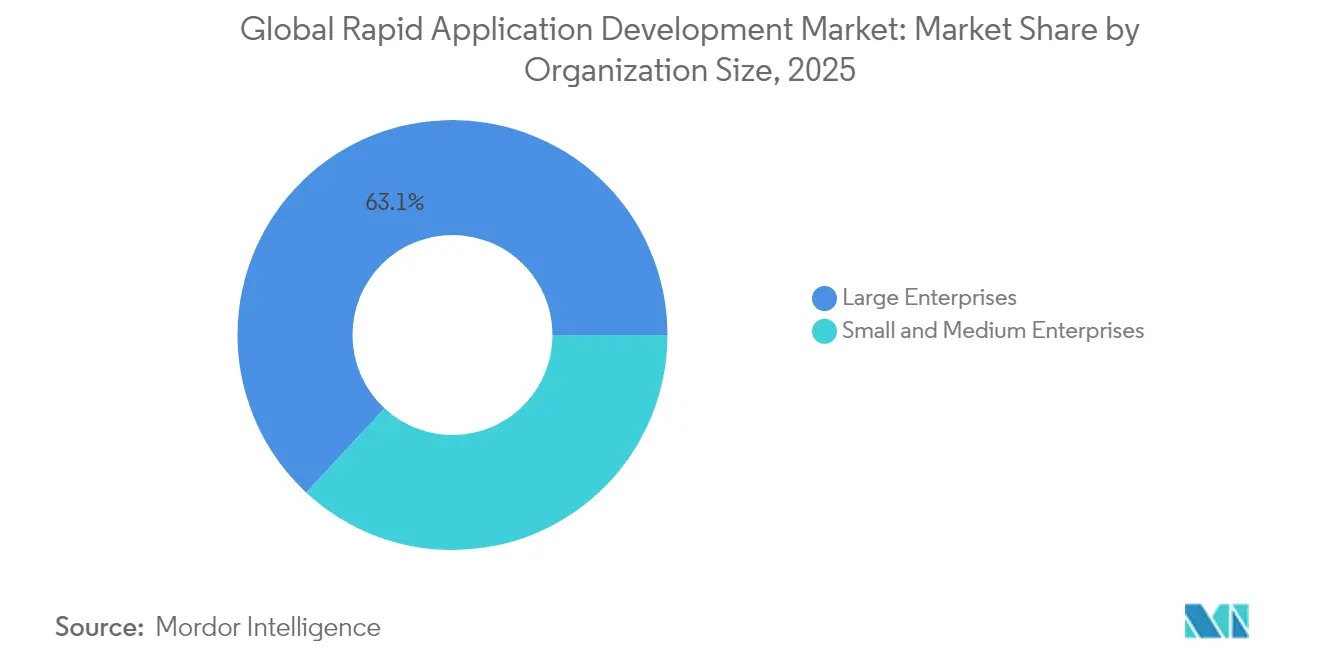

- By organization size, large enterprises held a 63.10% share of the rapid application development market in 2025; small and medium enterprises are expected to expand at a 41.65% CAGR through 2031, the quickest across company tiers.

- By end-user industry, Banking, Financial Services, and Insurance accounted for a 28.65% share of the rapid application development market in 2025; the Information Technology segment is set to rise at a 42.80% CAGR through 2031, the highest among all verticals.

- By geography, North America dominated the rapid application development market with a 38.90% share in 2025; the Asia Pacific is forecast to post a 41.95% CAGR through 2031, the fastest regional expansion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rapid Application Development Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in businesses and integration of advanced technologies | +6.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Flexibility to customize solutions as per dynamic enterprise requirements | +5.2% | Global, particularly strong in Asia Pacific and North America | Short term (≤ 2 years) |

| Rising demand for low-code platforms amid software-developer shortages | +7.9% | Global, acute in North America, Europe and developed Asia Pacific markets | Short term (≤ 2 years) |

| Accelerating digital transformation initiatives among small and medium enterprises | +6.5% | Global, with rapid uptake in Asia Pacific, Latin America and Middle East | Medium term (2-4 years) |

| AI-assisted application generation capabilities embedded in RAD tools | +8.1% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Corporate citizen-developer programs scaling under revised IT governance | +5.4% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Innovation in Businesses and Integration of Advanced Technologies

Enterprises are pivoting to microservices, event-driven architectures, and serverless compute, and RAD platforms have evolved to integrate these components through visual connectors. ServiceNow and Appian expose pre-built microservice templates that shorten provisioning time for workflow engines from days to minutes. Manufacturers exploit Siemens Mendix to fuse IoT sensor data with low-code dashboards that run at the network edge, unlocking predictive maintenance use cases. These integrations reduce technical debt by abstracting complex infrastructure behind declarative models, while ensuring that applications remain cloud-agnostic as strategies mature. Adoption is most advanced in North America and Europe, where 5G rollouts and mature DevOps cultures support continuous improvement cycles.

Rising Demand for Low-Code Platforms Amid Software-Developer Shortages

The United States Bureau of Labor Statistics projected in 2024 that software developer employment would grow 25% from 2022 to 2032, outpacing supply growth.[1]U.S. Bureau of Labor Statistics, “Software Developers, Quality Assurance Analysts, and Testers,” bls.gov Low-code tools mitigate the shortfall by enabling business analysts to build web and mobile apps through drag-and-drop interfaces, freeing senior engineers to focus on core algorithms. An OutSystems study reported that 74% of organizations planned to deliver at least 10 applications via low-code in the next year, with 31% using embedded AI for faster delivery. Financial institutions such as JPMorgan Chase compressed loan-origination cycles from 18 months to 6 weeks after adopting Appian. Wage inflation exceeding 15% for developers in 2024 raised pressure on operating budgets and boosted demand for citizen-developer programs that stretch limited talent.

Accelerating Digital Transformation Initiatives Among Small and Medium Enterprises

SMEs historically relied on off-the-shelf software that seldom matched niche workflows. Subscription-priced RAD products provide ready-made templates for inventory management, field service automation, and omnichannel commerce. Government digital-filing mandates in India and Brazil encouraged SMEs to integrate tax portals with legacy accounting packages using low-code connectors. Cloud deployment eliminates infrastructure burdens, enabling a mid-sized retailer to launch an inventory system on Zoho Creator within weeks at a fraction of the traditional development cost.[2]Zoho Corporation, “Creator Platform Updates,” zoho.com Network effects emerge as SMEs monetize templates on vendor marketplaces, spreading best practices and reducing duplicate coding effort.

AI-Assisted Application Generation Capabilities Embedded in RAD Tools

Generative AI elevates RAD from visual assembly to intelligent co-creation. Salesforce Einstein GPT converts plain-English process descriptions into Apex code, validation rules, and screen flows.[3]Salesforce, “Einstein GPT for Developers,” salesforce.com Microsoft Copilot Studio extends Power Platform with chat-based interfaces that output Power Apps canvases and Power Automate flows, cutting first-draft build time by 40%. OutSystems AI Mentor Studio scans low-code artifacts to flag inefficient queries and propose refactoring, thereby shrinking technical debt remediation cycles. Enterprises that pair these tools with prompt engineering training realize outsized productivity gains, although the full value will be realized over four years or more when models ingest proprietary codebases and compliance policies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of skilled professionals to scale, govern and secure RAD deployments | -3.2% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Security and data-governance concerns within highly regulated sectors | -4.1% | Global, concentrated in BFSI, Healthcare, Government and Defense | Medium term (2-4 years) |

| Vendor lock-in risks owing to proprietary metadata models | -2.8% | Global, affecting enterprises with multi-cloud strategies | Long term (≥ 4 years) |

| Performance limitations for complex, compute-intensive workloads | -2.3% | Global, impacting Financial Services, Energy and Manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security and Data-Governance Concerns Within Highly Regulated Sectors

Financial services and healthcare institutions face strict mandates for audit trails, encryption, and data residency that many RAD platforms only recently addressed. The Open Web Application Security Project reported common weaknesses such as insecure direct object references in citizen-built apps. Deutsche Bank limited low-code use to non-customer-facing workflows until vendors achieved SOC 2 Type II and ISO 27001 certifications. Healthcare providers cited HIPAA compliance gaps in default permission settings, delaying production launches. Stricter frameworks, such as GDPR, require regional data centers, prompting vendors like Betty Blocks to open a Frankfurt facility for European customers. Until platforms deliver end-to-end governance as the default, adoption in regulated verticals will lag behind less-regulated industries.

Lack of Skilled Professionals to Scale, Govern, and Secure RAD Deployments

RAD lowers coding barriers but not governance complexity. A KPMG survey revealed that 62% of firms lacked formal low-code oversight teams, resulting in duplicated functionality and orphaned projects. Architects who bridge business logic and security policy remain scarce, especially in emerging markets with shallow talent pools. ServiceNow App Engine Studio embeds automated policy checks, yet it still requires skilled administrators to configure guardrails. Enterprises are therefore investing in centers of excellence that curate components, run code reviews, and ensure integration with service catalogs; however, recruiting delays slow program maturity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: No-Code Platforms Capture Non-Technical Users

Low-code platforms held a 63.70% market share in the rapid application development market in 2025, led by Microsoft Power Platform and OutSystems, which combine drag-and-drop design with optional custom code for performance-critical paths. No-code platforms are forecast to grow at a 41.20% CAGR through 2031 as business users tap Airtable and Quickbase to build approval workflows and dashboards without IT involvement. This trajectory illustrates growing trust in visual tools for departmental productivity while IT retains oversight for enterprise-wide systems.

No-code growth complements rather than replaces low-code. Departments often experiment with no-code for rapid prototyping and later migrate to low-code when user counts increase or real-time data synchronization is required. The interplay expands the rapid application development market by matching tool complexity to workload requirements, driving broader adoption across mixed skill profiles.

By Deployment Mode: Cloud Dominance Driven by Scalability and Automatic Updates

Cloud deployment accounted for 73.15% of revenue in 2025 and is forecast to expand at a 40.95% CAGR through 2031, capturing both new workloads and migrations. Bundled identity management, consumption-based billing, and real-time collaboration give cloud platforms a decisive advantage over on-premise alternatives.

On-premise solutions persist where data sovereignty or air-gapped networks are mandatory, for example, in defense installations and select financial institutions. Oracle APEX and hybrid OutSystems stacks cater to these needs; however, the total cost of ownership remains higher than that of cloud equivalents. As compliance frameworks evolve, more users switch, reinforcing cloud as the primary growth engine for the rapid application development market.

By Organization Size: SMEs Drive Growth as Subscription Models Lower Barriers

Large enterprises contributed 63.10% of 2025 revenue by embedding RAD within enterprise architecture and leveraging dedicated vendor support. They modernize legacy COBOL forms, automate multi-step approvals, and integrate global data sources through platforms tied to existing cloud ecosystems.

SMEs, however, are expected to register a 41.65% CAGR through 2031. Affordable per-user subscriptions enable a regional retailer to deploy a reservation system for USD 500, rather than commissioning bespoke development at USD 50,000. Government mandates for e-invoicing in India and Brazil are compelling many SMEs to digitize their operations quickly, thereby further expanding the rapid application development market.

By End-User Industry: Information Technology Sector Leads Growth as Vendors Embed RAD into DevOps

Banking, Financial Services, and Insurance accounted for 28.65% of 2025 revenue, driven by compliance-driven iteration cycles. Yet, the Information Technology sector is set to grow at a 42.80% CAGR through 2031 as software vendors embed low-code builders into IT service suites. ServiceNow, Atlassian, and GitLab each added visual workflow designers that enable teams to ship internal tools without relying on external contractors.

Healthcare, Retail, Manufacturing, and Government each adopt RAD for sector-specific imperatives. Siemens Mendix empowers manufacturers to visualize IoT data. Retailers build customized curbside pickup portals. Governments are using low-code to modernize their permitting systems. The breadth of scenarios underscores how domain templates expand the addressable market for Rapid Application Development.

Geography Analysis

North America accounted for 38.90% of 2025 revenue, driven by mature IT budgets and widespread citizen-developer programs. Microsoft, Salesforce, and ServiceNow leverage extensive ecosystems of implementation partners, making platform adoption straightforward for Fortune 500 companies. Canada’s public sector adopted RAD to refresh legacy systems while meeting local data-residency laws. Mexico’s manufacturing plants share supplier portals built on AWS Honeycode with U.S. partners, illustrating cross-border workflow digitization.

Asia Pacific is projected to grow at 41.95% CAGR through 2031, the highest regional pace. India’s Digital India initiative and China’s 14th Five-Year Plan encourage local firms to minimize custom coding hours, fueling the uptake of Zoho Creator and Alibaba Cloud's low-code suites. Japan uses RAD to offset developer shortages amid an aging workforce, while Australia’s banks adopt low-code to comply with open banking requirements. Local data-protection rules, such as China’s PIPL, force vendors to establish regional data centers; yet, this investment expands addressable demand across diverse markets.

Europe, South America, the Middle East, and Africa make steady contributions. GDPR compliance raised the bar for security features, slowing uptake in highly regulated sectors yet accelerating demand for platforms with robust audit logs and on-shore hosting. Brazil’s SMEs prefer subscription-priced RAD tools that match revenue volatility. Gulf Cooperation Council states fund e-government programs built on ServiceNow and OutSystems, and Kenya’s startups leverage mobile-first RAD suites to leapfrog desktop development.

Competitive Landscape

The rapid application development market tilts toward moderate concentration. Microsoft, Salesforce, Oracle, and Amazon Web Services anchor the top tier by bundling RAD with existing PaaS and productivity clouds. Microsoft Power Platform surpassed 22 million monthly active users in October 2025, following the addition of AI agents to Copilot Studio. Salesforce Einstein 1 Studio, generally available in November 2025, automates workflow generation and targets industries with pre-trained models. Oracle APEX 24.1 introduced AI-assisted SQL creation that resonates with database administrators. AWS Honeycode enhancements attract startups already running compute workloads on EC2.

Specialists defend share through vertical depth and governance tools. OutSystems partnered with NVIDIA in September 2025 to embed GPU inference, unlocking predictive-maintenance apps for industrial users. Siemens Mendix 10 added edge-computing support for shop-floor analytics. Appian partnered with AWS on compliance packs for the regulated sector. ServiceNow acquired Moveworks to embed conversational AI within employee portals.

Emerging disruptors target departmental buyers. Airtable added multi-step automation that draws marketing teams, while Quickbase inserts AI data-quality checks to reduce errors in SME dashboards. Betty Blocks satisfies GDPR data residency requirements by hosting in Germany. Creatio delivers no-code CRM with embedded AI for cost-sensitive Latin American customers. The field remains competitive as generative AI, template marketplaces, and vertical solution packs reshape value propositions within the rapid application development market.

Rapid Application Development Industry Leaders

Microsoft Corporation

Salesforce Inc.

Oracle Corporation

International Business Machines Corporation

Amazon Web Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Zoho Creator added templates for Education, Logistics, and Hospitality, supporting strong SME growth in Asia Pacific and Latin America.

- March 2025: Google Cloud integrated Gemini AI into AppSheet, enabling conversational app building for Google Workspace customers.

- February 2025: Pegasystems launched Pega GenAI Blueprint, an AI tool that converts legacy code into low-code equivalents to accelerate modernization.

- January 2025: Airtable introduced enhanced automation features, including conditional logic and multi-step workflows, expanding departmental use cases.

Global Rapid Application Development Market Report Scope

The Rapid Application Development Market Report is Segmented by Type (Low-Code Development Platforms, No-Code Development Platforms), Deployment Mode (On-Premise, Cloud), Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (Banking, Financial Services and Insurance, Retail and E-Commerce, Government and Defense, Healthcare, Information Technology, Energy and Utilities, Manufacturing, Other End-User Industries), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Low-Code Development Platforms |

| No-Code Development Platforms |

| On-Premise |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance |

| Retail and E-Commerce |

| Government and Defense |

| Healthcare |

| Information Technology |

| Energy and Utilities |

| Manufacturing |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Low-Code Development Platforms | ||

| No-Code Development Platforms | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | Banking, Financial Services and Insurance | ||

| Retail and E-Commerce | |||

| Government and Defense | |||

| Healthcare | |||

| Information Technology | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the Rapid Application Development market expected to grow through 2031?

It is projected to expand from USD 79.53 billion in 2026 to USD 416.42 billion by 2031, reflecting a 39.23% CAGR.

Which deployment model leads new spending on Rapid app platforms?

Cloud deployment held 73.15% share in 2025 and will grow the quickest at a 40.95% CAGR through 2031 thanks to elastic scalability and automatic updates.

Why are small and medium enterprises adopting RAD tools rapidly?

Subscription pricing, pre-built templates, and no infrastructure overhead allow SMEs to digitize workflows quickly, driving a 41.65% CAGR for this segment.

What role does generative AI play in today’s low-code platforms?

Embedded models such as Salesforce Einstein GPT and Microsoft Copilot Studio translate natural language into app logic, cutting initial build effort by roughly 40%.

Which vertical shows the fastest growth outlook for RAD adoption?

The Information Technology segment is forecast to log the highest 42.80% CAGR through 2031 as vendors embed low-code builders into DevOps pipelines.

What is a primary risk associated with citizen-developer programs?

Security and data-governance gaps can emerge when non-technical users publish apps without adequate oversight, especially in highly regulated industries.

Page last updated on: