South Korea Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

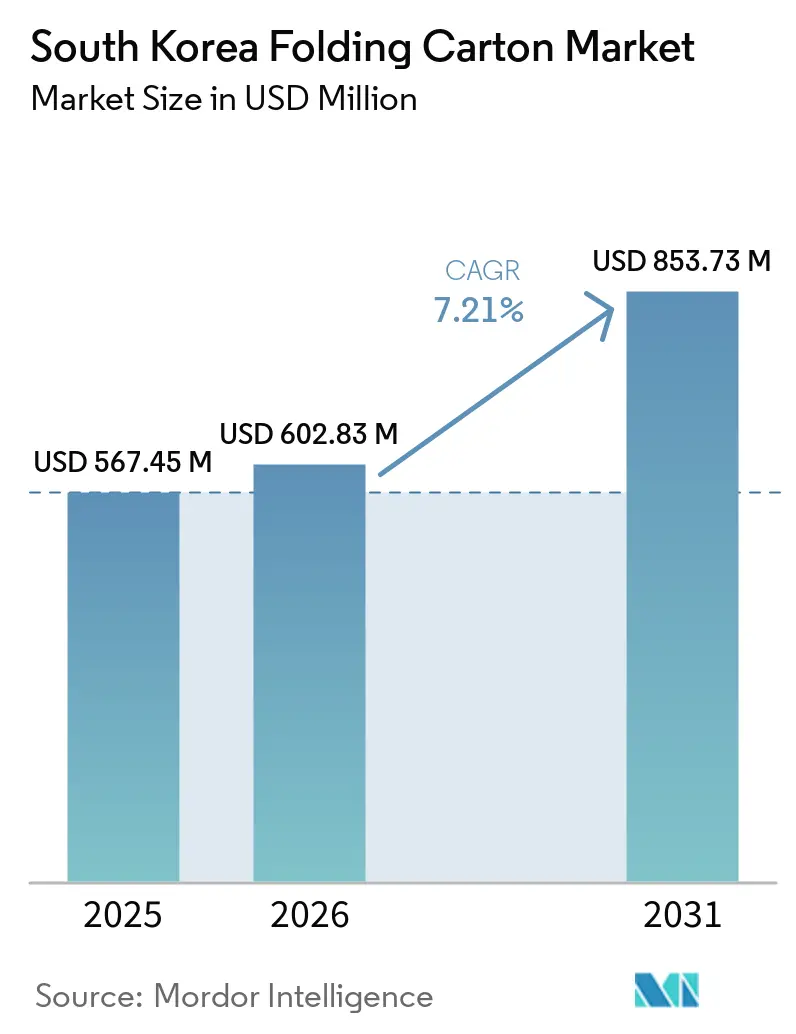

| Base Year Market Size (2025) | USD 567.45 Million |

| Market Size (2026) | USD 602.83 Million |

| Market Size (2031) | USD 853.73 Million |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Folding Carton Market Analysis by Mordor Intelligence

The South Korea folding carton market size was valued at USD 567.45 million in 2025 and is estimated to grow from USD 602.83 million in 2026 to reach USD 853.73 million by 2031, at a CAGR of 7.21% during the forecast period (2026-2031). Intensifying sustainability mandates, rapid growth in e-commerce parcel volumes, and a wave of premiumization in cosmetics and pharmaceuticals are reinforcing demand for paper-based secondary packaging. Converters are migrating toward lighter substrates and shorter production runs to balance rising fiber costs with brand requirements for vivid graphics and quick turnaround. Regulatory incentives that reward paper over plastic cushioning are further shifting capital toward mills that can supply barrier-enhanced, low-basis-weight boards. Meanwhile, import competition from Southeast Asia is testing pricing power in commodity grades, urging domestic mills to differentiate through digital printing capacity, recycled-content offerings, and certified chain-of-custody systems.

Key Report Takeaways

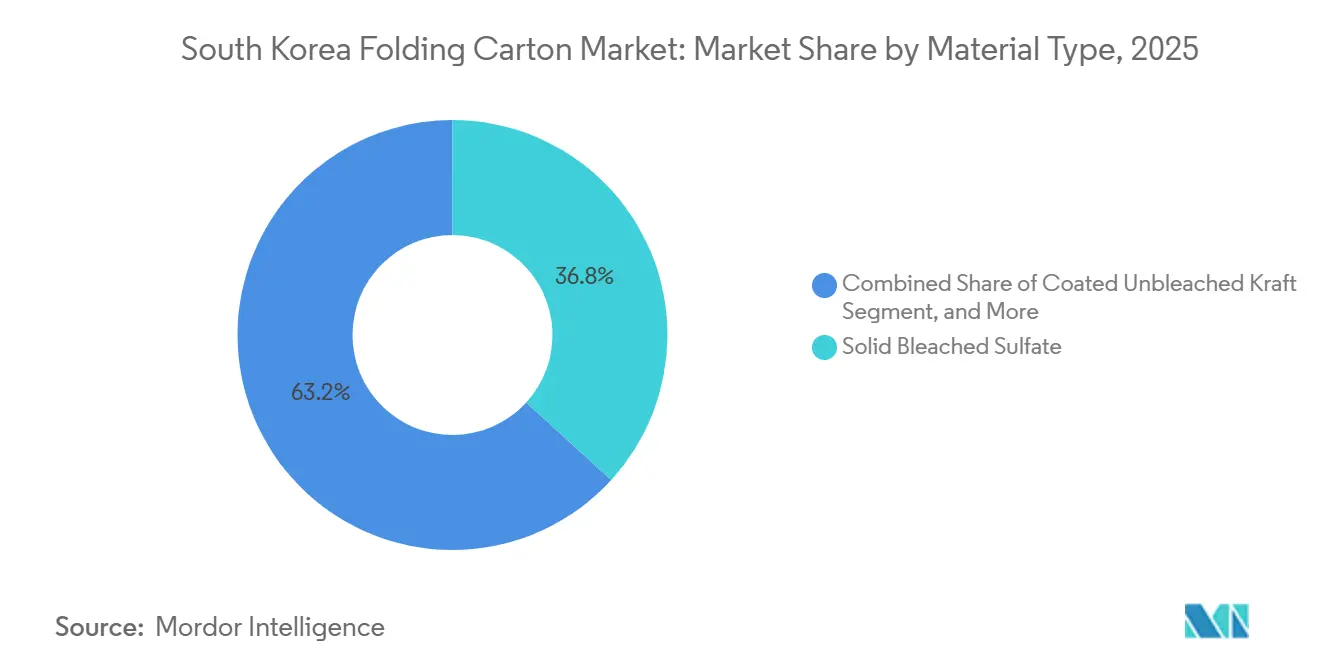

- By material type, solid bleached sulfate captured with 38.53% of the South Korea folding carton market share in 2025.

- By printing technology, the South Korea folding carton market size for digital printing is projected to grow at a 9.12% CAGR to 2031.

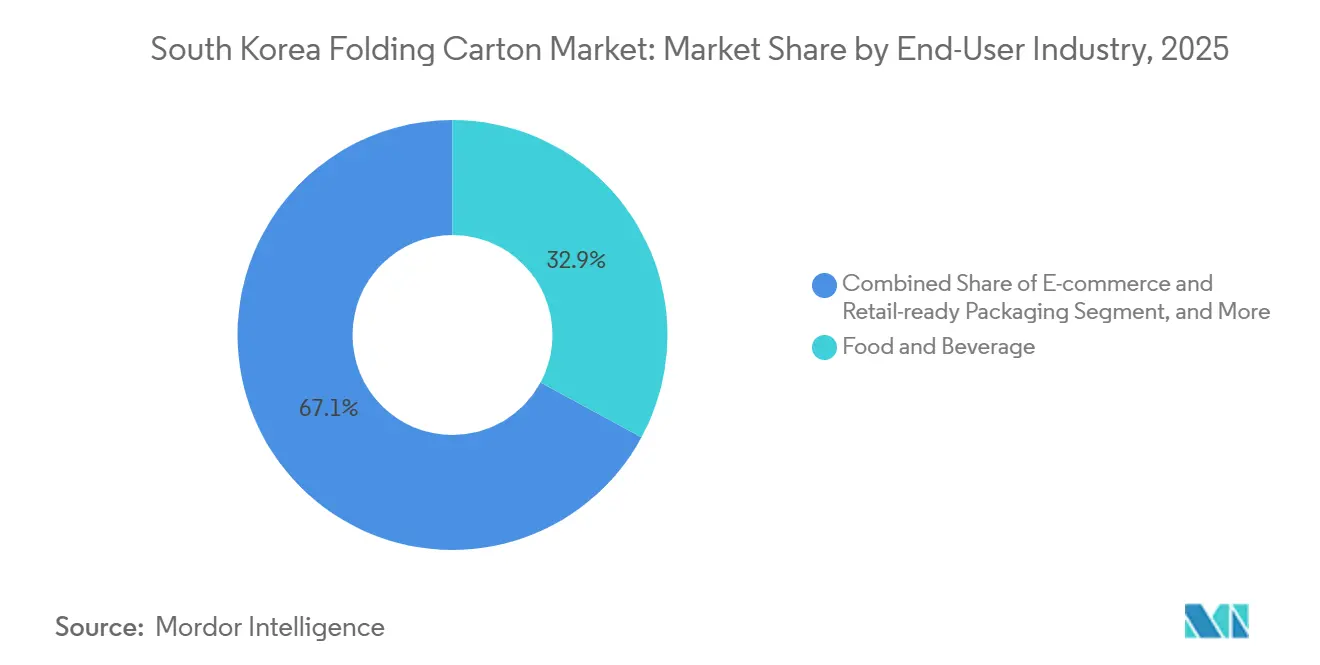

- By end-user industry, the food and beverage industry captured 32.89% of the South Korea folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Eco-Friendly Packaging Solutions | +1.8% | National, strong in Seoul, Busan, Incheon logistics hubs | Medium term (2-4 years) |

| Growth of South Korea's E-Commerce Fulfilment Networks | +1.5% | Nationwide, spill-over to Gyeonggi and Chungcheong export clusters | Short term (≤ 2 years) |

| Brand Premiumization in Cosmetics and K-Beauty Exports | +1.3% | Seoul, Gyeonggi, Incheon Free Economic Zone | Medium term (2-4 years) |

| Government Incentives for Paper-Based Substitutes to Plastic | +1.2% | Urban centers with high parcel density | Short term (≤ 2 years) |

| AI-Enabled Short-Run Digital Carton Printing Adoption | +0.9% | Converters serving cosmetics, pharma, premium foods | Medium term (2-4 years) |

| Expansion of Cold-Chain Ready Folding Cartons for Meal Kits | +0.5% | Urban meal-kit networks in Seoul, Busan, Daegu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Eco-Friendly Packaging Solutions

Amendments to the Resource Recycling Promotion Act, effective April 30, 2026, loosen packaging-space ratios from 50% to 70% when paper cushioning replaces plastic, providing a clear economic incentive to switch to folding cartons.[1]Dashan Packing, “South Korea Recycling Policy and Food Packaging,” dashanpacking.com Coupang’s move to paper bags is eliminating about 7,000 tons of plastic each year, signaling cascading adoption among rival platforms. Export-oriented converters are also responding to the EU Packaging and Packaging Waste Regulation, which mandates Grade A recyclability starting in August 2026, prompting launches such as Hansol Paper’s Protego HS range. Cosmetics suppliers report a 3x increase in requests for paper formats, spanning cream jars to lip-balm sticks, to maintain European shelf access.

Growth of South Korea's E-Commerce Fulfilment Networks

Parcels surpassed 5 billion units in 2025, and new courier rules reward paper cushioning with higher space allowances, slashing void costs for major 3PLs. CJ Logistics and Taelim Packaging recycle roughly 5,000 tonnes of boxes annually into new courier cartons, proving closed-loop economics at scale. Patent-pending retention packs that dispense with bubble wrap cut damage by two-thirds while meeting KS T 5055 tests, underscoring how folding-carton engineering can align cost, protection, and sustainability.

Brand Premiumization in Cosmetics and K-Beauty Exports

K-beauty exports hit USD 2.6 billion in Q1 2025 and continue climbing, with mono-material tubes, refillable compacts, and recyclable droppers now table stakes for global beauty brands. The KRW 40 billion (USD 30 million) K-Beauty Fund is underwriting R&D for paper tubes and stone-paper sticks, while KKR’s USD 528 million acquisition of Samhwa underscores investors’ readiness to pay premiums for compliant packaging capabilities. Kolmar Korea’s one-hand pump paper pack, fully recyclable, showcases the leap from food-grade paper packs to prestige beauty formats.

Government Incentives for Paper-Based Substitutes to Plastic

Under extended producer responsibility, material fees now scale with recyclability grades, awarding lower costs to mono-material PET and paper while penalizing multilayer plastics. Bottled-beverage firms must blend 10% recycled PET in 2026, rising to 30% by 2030, creating recycled resin volatility that makes paper a more predictable cost base. Paperboard certified to FSC and REACH standards is gaining priority in retailer tenders, locking in carton demand for compliant mills.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Pulp Prices Impacting Producer Margins | -1.1% | Global, pronounced for Korea’s import-reliant mills | Short term (≤ 2 years) |

| Rising Imports of Low-Cost Cartons from Southeast Asia | -0.8% | Domestic market, especially commodity grades | Medium term (2-4 years) |

| Packaging Line Compatibility Issues in Legacy Plants | -0.5% | Mid-sized converters with older presses | Medium term (2-4 years) |

| Shrinking Tobacco Packaging Volumes After 2025 Tax Hikes | -0.3% | Producers serving tobacco OEMs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp Prices Impacting Producer Margins

SCA lifted European NBSK pulp to USD 1,710 per tonne in March 2026, and eucalyptus pulp in China breached USD 590, squeezing Korean converters who import most of their fiber pulp. Fires in Chile and restrictions in Indonesia are choking roughly 4 million tonnes of global supply, keeping price swings acute. Thin margins delay capital upgrades, limiting the speed at which mills can pivot to lightweight or barrier-coated boards.

Rising Imports of Low-Cost Cartons from Southeast Asia

Vietnam, Indonesia, and Thailand are exporting larger volumes into Korea as free-trade pacts lower duties and labor arbitrage widens. Price-sensitive buyers in household goods and industrial bulk packs are switching to imported blanks, compressing domestic price realizations. Local producers retain an edge in cosmetics and pharma, where regulatory paperwork, color fidelity, and rapid turnaround outweigh unit cost, yet commodity carton margins remain under pressure. Trade statistics show a sustained uptick in corrugated and folding carton import licenses issued at Busan and Incheon ports during 2025-2026, underscoring the structural threat to undifferentiated grades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Boards Maintain the Value Center

Solid bleached sulfate accounted for 36.78% of the South Korea folding carton market share in 2025, driven by premium cosmetics and pharmaceutical packs that demand high brightness and barrier coatings. Folding boxboard is forecast to outpace all rivals at an 8.26% CAGR through 2031 as converters use lighter calipers to reduce freight costs and meet recycling targets, supporting the South Korean folding carton market's expansion in e-commerce sleeves and retail-ready packs. In response, Daehan Paper introduced a 46 g/m² reinforced corrugated medium that claims a world-leading basis-weight reduction while retaining crush strength.

The material mix is tilting further toward coated and functional-barrier grades. Hansol’s Protego family, verified to cut lifecycle emissions by 39%, illustrates how moisture- and oxygen-barrier papers can displace PE-coated substrates in frozen meals and confectionery. Recycled-content innovations such as Tarim Packaging’s high-strength three-layer board save up to 20% on paper and reduce carbon by the equivalent of planting 8,300 trees annually, pointing to a blended strategy of lightweighting and circular fiber flow that underpins long-term competitiveness.

By Printing Technology: Digital Momentum Reshapes Run-Length Economics

Lithographic presses held 47.21% of the 2025 volume thanks to established workflows and unmatched offset quality in long runs. Yet digital output is growing at a 9.12% CAGR as AI-enhanced RIPs and high-speed single-pass inkjet lines make runs up to 20,000 m² economically viable, enabling the South Korean folding carton market to support mass personalizations and fast seasonal turns. Canon’s corrPRESS iB17 can deliver 8,000 m² per hour on 1.7 m-wide boards, offering converters a bridge from prototyping to mid-volume production.[2]Youssef Mai, “Canon Announces the corrPRESS iB17,” financialinsight.africa

Flexographic lines are not standing still; automation and extended-color-gamut plates now reproduce more than 90% of Pantone colors, and hybrid flexo-inkjet units overlay serialized QR codes without a second pass, preserving relevance in the South Korean folding carton industry. Gravure remains niche for ultra-long tobacco or liquor runs, but workflow software that clusters litho and digital jobs by substrate and die line is steadily eroding the break-even advantage of legacy presses, widening digital’s future share.

By End-User Industry: Parcel-Ready Formats Eclipse Traditional Food Service

Food and beverage maintained the largest slice at 32.89% in 2025, yet parcel-driven demand is accelerating fastest. E-commerce and retail-ready packaging are tracking a 9.78% CAGR through 2031, lifting the South Korean folding carton market, as brand owners insist on frustration-free unboxing and minimal void ratios. Healthcare and pharmaceuticals continue to expand on the back of sterile medical cartons, following Amcor’s USD 35 million Malaysian coating plant, which brought regional air-knife capacity closer to Korean device exporters.

Personal care and cosmetics are pivoting to paper tubes, refill kits, and recyclable droppers, aligning with K-beauty’s export trajectory. Tobacco volumes, conversely, face regulatory headwinds: proposed KRW 1,799-per-milliliter levies on synthetic-nicotine e-liquids could triple retail prices, curbing carton demand for this once-stable revenue stream. Cold-chain-ready boards that hold 2-8 °C for 120 hours, like Smurfit WestRock’s Fresko Box, underscore a cross-sector that marries sustainability with functional performance.

Geography Analysis

Demand clusters around Seoul, Incheon, and Gyeonggi, where e-commerce fulfillment centers aggregate parcel volumes, anchoring more than half of national folding-carton shipments in 2025. The South Korean folding carton market benefits from the proximity of large cosmetic OEMs in Suwon and carton makers in nearby Paju, which shortens lead times and enables synchronized design sprints for limited-edition launches. Busan and Daegu, with busy cold-chain networks feeding meal-kit and seafood channels, are early adopters of insulated paperboard shippers that replace EPS.

Export-oriented ports at Incheon and Busan are also gateways for imported low-cost cartons, adding to competitive pressure on domestic mills. Chungcheong’s manufacturing corridors, historically tied to automotive and electronics, now host pharmaceutical fillers that demand GMP-compliant cartons with serialized 2D codes, attracting investment in UV-inkjet lines. Jeolla and Gangwon, while smaller, are courting eco-industry parks pairing biomass energy with recycled-fiber pulping to offset high logistics costs to the Seoul metro.

Rising land prices in the capital region are pushing new converting capacity southward, with several mid-sized converters announcing relocations to Cheonan and Daejeon industrial sites, where municipal grants cover up to 30% of equipment outlays for FSC-certified lines. Coastal regions face typhoon-linked supply disruptions; contingency planning now includes dual-port shipping routes and redundant converting nodes inland to sustain the South Korea folding carton market during peak typhoon season. Local governments are trialing green-credit schemes that rebate up to KRW 50 per kilogram (USD 0.04 for each kilogram) of recycled content supplied to municipal agencies, creating micro-demand pockets that reward mills able to segregate and certify post-consumer fiber.

Competitive Landscape

The South Korean folding carton market features a blend of multinationals, including Amcor, Rengo, Graphic Packaging International, Mondi, International Paper Company, and Smurfit Kappa, alongside domestic players such as Seohae Paper, Kyung Woo Paper, and Daehan Pulp. Global majors leverage balance-sheet strength to automate plants and secure pulp at scale, while Korean firms exploit proximity to brand owners and deep knowledge of local compliance to win agile orders. Stora Enso’s EUR 30 million (USD 32.9 million) bioenergy retrofit at Heinola cut 113,000 tonnes of CO₂ annually, demonstrating how sustainability investments double as cost hedges.[3]Edipap Srl, “Stora Enso Completes EUR 30 Million Investment,” papnews.com

Smurfit Westrock’s target of USD 7 billion in EBITDA by 2030 and USD 14 billion in free cash flow earmarked for dividends and buybacks signal disciplined capital deployment and underscore confidence in corrugated and cartonboard demand.[4]Smurfit Westrock, “Medium-Term Investor Update,” smurfitwestrock.com Rengo’s height-adjustable J-RexS machine illustrates automation moves that cut labor and board waste, while FineNatura cellulose-nanofiber sheets open new flame-resistant applications. Domestic converters invest in hybrid presses and AI workflow tools to bridge shorter runs without sacrificing litho quality, yet margin pressure from imported cartons persists, pushing consolidation and technology partnerships.

White-space growth will likely coalesce around cold-chain ready cartons, PPWR-compliant secondary boxes for cosmetics exporters, and serialized pharmaceutical packs that integrate anti-counterfeit features. Suppliers able to pair lightweight substrate science with digital post-press embellishment stand to capture premium share, anchoring medium-term differentiation amid pulp volatility and import competition.

South Korea Folding Carton Industry Leaders

Amcor plc

Graphic Packaging International LLC

Tetra Laval International S.A.

Rengo Co., Ltd.

APP Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Amcor opened a USD 35 million healthcare coating facility in Subang Jaya, Malaysia, adding regional air-knife capacity for sterile medical paper.

- April 2026: Hansol Paper hosted a customer seminar unveiling Protego HS, a Grade A-recyclable heat-sealable secondary board tailored for EU regulations.

- April 2026: Coupang shifted all dawn-delivery packaging from plastic to paper bags, eliminating about 7,000 tons of plastic per year.

- March 2026: Canon introduced the corrPRESS iB17 high-speed corrugated inkjet press, targeting runs up to 20,000 m².

South Korea Folding Carton Market Report Scope

The South Korea folding carton market is defined as the industry focused on the production and conversion of paperboard into collapsible containers used for protective and promotional packaging across diverse commercial sectors. It further evaluates the market based on dominant printing technologies, including lithographic, flexographic, digital, and gravure.

The South Korea Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value and forecast value of the South Korea folding carton market?

The South Korea folding carton market size was valued at USD 567.45 million in 2025 and is estimated to grow from USD 602.83 million in 2026 to reach USD 853.73 million by 2031.

Which material type leads demand in South Korea?

Solid bleached sulfate dominates with 36.78% share in 2025, favored for high-end cosmetics and pharmaceutical packs.

Why is digital printing gaining share in Korean folding cartons?

AI-enabled inkjet presses now make short- to mid-run runs cost-competitive, supporting SKU proliferation and personalized packs.

How are new courier rules affecting packaging choices?

The amended Resource Recycling Promotion Act allows more interior space when paper cushioning is used, incentivizing cartons over plastic.

What threatens margins for Korean carton converters?

Imported low-cost cartons from Southeast Asia and volatile pulp prices tighten spreads, spurring investment in differentiation and automation.

Which end-use sector is growing fastest through 2031?

E-commerce and retail-ready packaging for parcel shipments is projected to expand at a 9.78% CAGR.

Page last updated on: