Malaysia Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

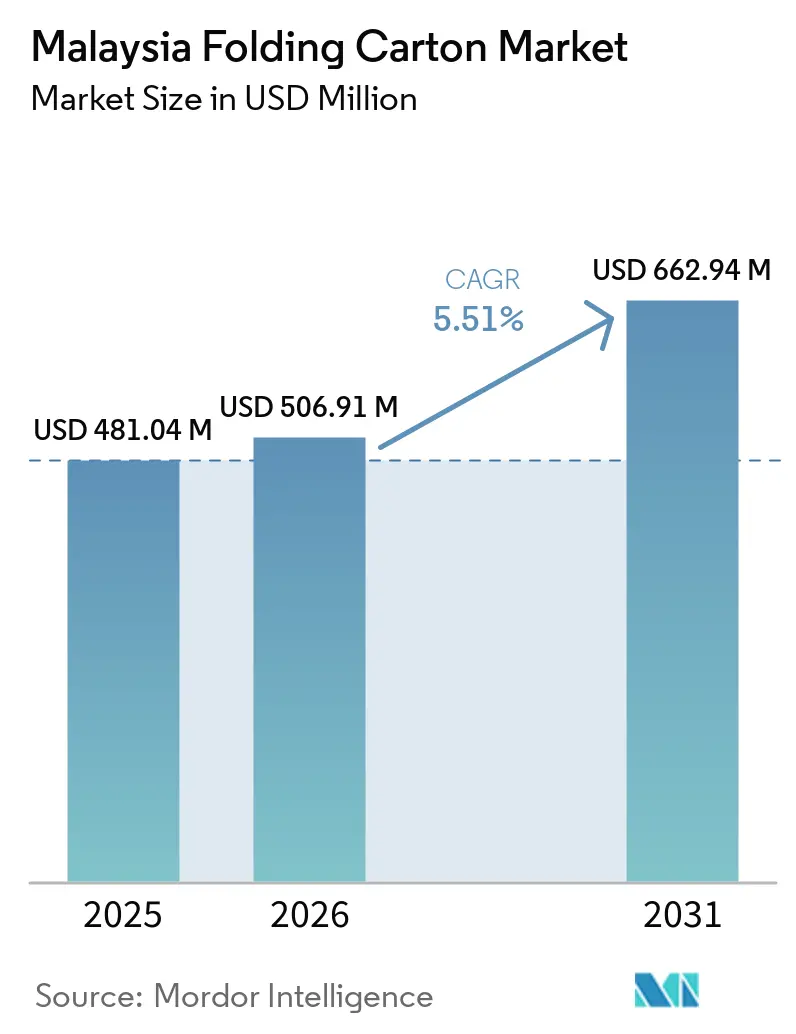

| Base Year Market Size (2025) | USD 481.04 Million |

| Market Size (2026) | USD 506.91 Million |

| Market Size (2031) | USD 662.94 Million |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

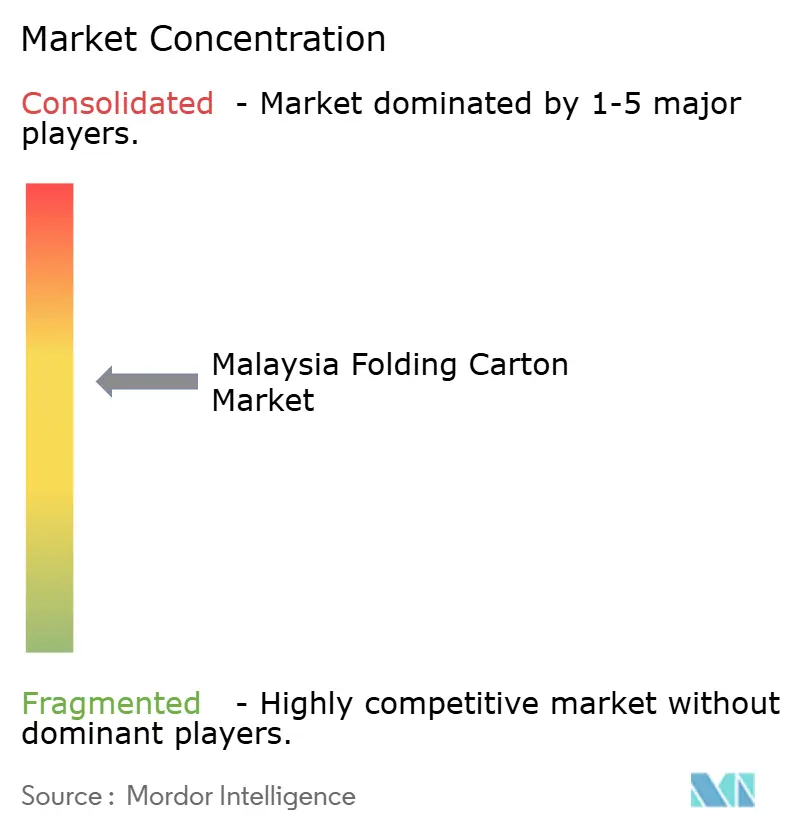

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Folding Carton Market Analysis by Mordor Intelligence

The Malaysia folding carton market size is projected to expand from USD 481.04 million in 2025 and USD 506.91 million in 2026 to USD 662.94 million by 2031, registering a CAGR of 5.51% between 2026 to 2031. Rising quick-commerce activity, aggressive mill reinvestment, and a tightening sustainability rule-set are widening demand far beyond the traditional food and beverage core. Domestic kraft-liner and pulp additions worth MYR 2.8 billion (USD 590 million) are already shortening lead-times and dampening logistics risk, while platform operators such as Grab and Shopee are dictating certification and ink requirements that few un-automated converters can meet. Multinational fast-moving consumer-goods (FMCG) brands, lured by near-shoring electronics and consumer-goods clusters, are locking in long-term supply agreements that reward traceability and waste-reduction investments. Against this backdrop, the Malaysia folding carton market is pivoting from price-led competition toward speed-to-shelf, substrate versatility, and verifiable end-of-life outcomes, themes that collectively underpin the sector’s mid-single-digit growth profile to 2031.

Key Report Takeaways

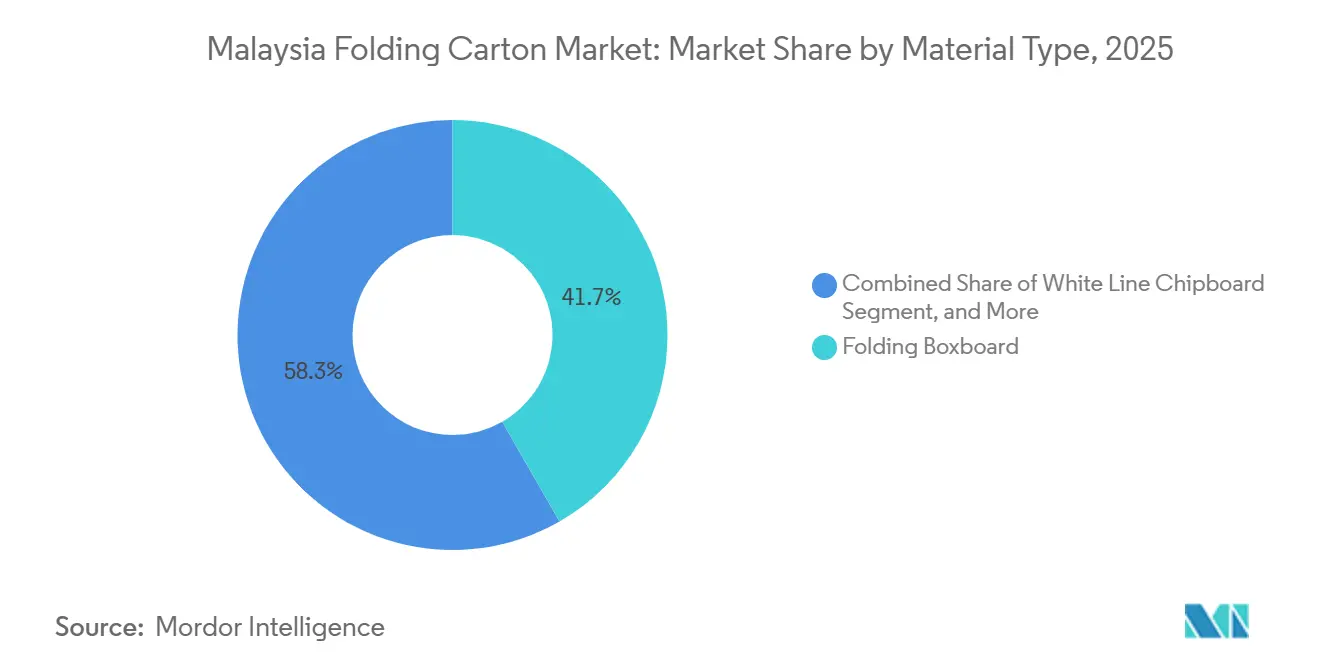

- By material type, folding boxboard captured 41.71% of the Malaysia folding cartons market share in 2025.

- By printing technology, the Malaysia folding cartons market size for the digital printing segment is forecast to advance at a 7.24% CAGR through 2031.

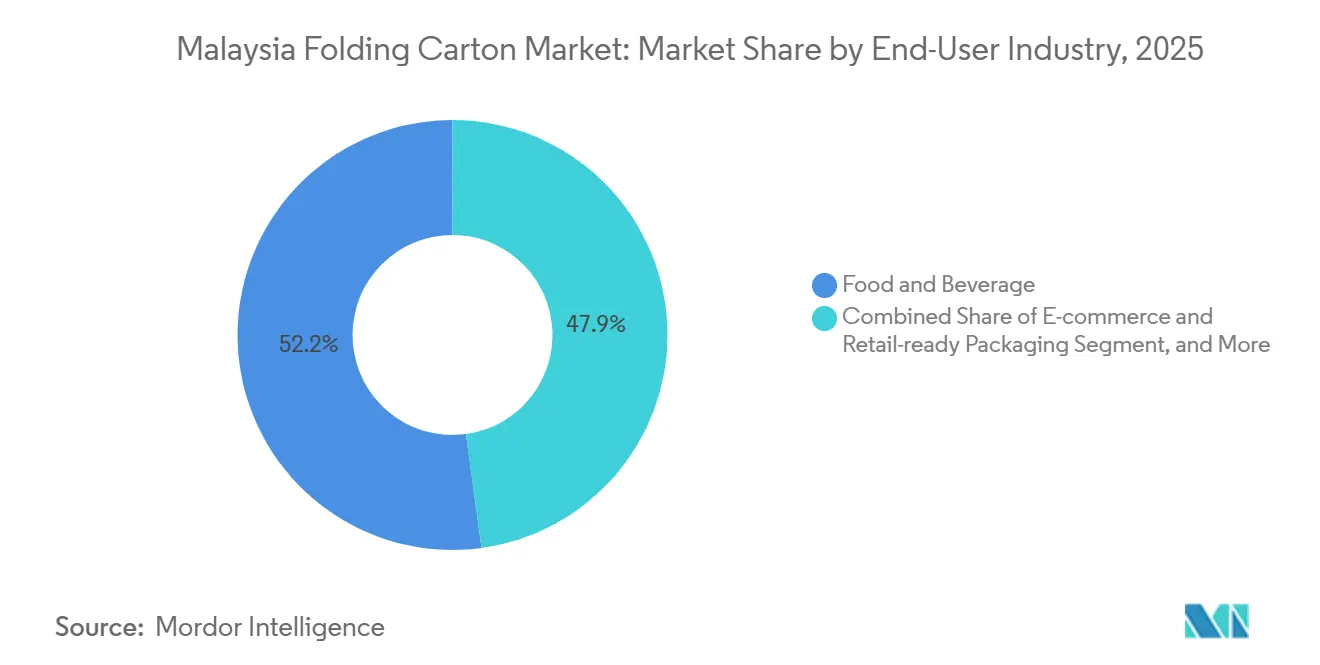

- By end-user industry, food and beverage captured 52.15% of the Malaysia folding cartons market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption Of Premium Packaged Goods | +1.2% | Klang Valley, Penang | Medium term (2-4 years) |

| Government Push For Sustainable Packaging Standards | +1.0% | National, early enforcement in Selangor and Johor | Long term (≥ 4 years) |

| Surge In Quick-Commerce Grocery Delivery | +1.5% | Major urban centers | Short term (≤ 2 years) |

| Capacity Expansion By Domestic Paper Mills | +0.9% | Selangor and Pahang hubs | Medium term (2-4 years) |

| AI-Enabled Quality Inspection Systems | +0.6% | Klang Valley early adopters | Medium term (2-4 years) |

| Near-Shoring Of Regional Consumer-Goods Production | +0.8% | Penang and Melaka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Premium Packaged Goods

Demand for premium cosmetics, confectionery, and healthcare SKUs is reshaping substrate specifications as brand owners insist on cartons that accept embossing, metallic inks, and tactile varnishes. Nestlé Malaysia’s ready-to-drink KitKat beverages and portable Maggi bowls exemplify the shift toward grease-resistant coatings that preserve brand imagery under high-speed filling lines.[1]Nestlé Malaysia, “FY2024 Financial Results,” nestle.com.my Urban consumers, 60-70% of survey respondents, now favor brands that publish recyclability information, even when price sensitivity remains high.[2]Milieu Insight, “Malaysian Consumer Packaging Preferences Survey 2025,” milieuinsight.com Solid bleached sulfate board, priced at a 15-20% premium to folding boxboard, is therefore holding share in luxury goods despite cost headwinds. The Ministry of Domestic Trade’s 2026 advertising code compels clear labeling of recyclability, accelerating the exit of non-certified converters. Collectively, prestige positioning and regulatory nudges are expanding the value pool available to converters capable of delivering high-definition graphics on certified substrates, reinforcing upward momentum in the Malaysian folding carton market.

Government Push for Sustainable Packaging Standards

Malaysia’s Circular Economy Blueprint 2025-2035 transitions from voluntary to mandatory extended producer responsibility by 2030, requiring converters to track sourcing, energy intensity, and recycling outcomes, or face MYR 50,000 (USD 12,337) in fines per violation. Lazada and Shopee magnified the pressure by levying a 3% surcharge on non-compliant packaging starting July 2026, instantly raising the entry bar for uncertified suppliers.[3]Lazada Malaysia, “Green Packaging Whitepaper 2026,” lazada.com.my Box-Pak Malaysia pre-empted the rule change by certifying chain-of-custody systems across three countries, giving the group pole position for multinational FMCG tenders. Ink sludge re-classification under the 2025 scheduled-waste rules is further motivating investments in closed-loop water treatment. In combination, these measures channel volume toward large, well-capitalized firms and cement sustainability as a non-negotiable qualifier within the Malaysian folding carton market.

Surge in Quick-Commerce Grocery Delivery

GrabMart’s 20 million app downloads and ShopeeFood’s 8 million monthly orders have entrenched 30-minute delivery expectations, prompting converters to engineer cartons with reinforced corners, moisture barriers, and tamper-evident locks. Such designs add 8-12% to material cost but cut damage rates to below 1%. Digital printing now enables profitable 500-unit runs, empowering brands to localize artwork and launch micro-campaigns without carrying excess inventory. The Malaysian regulator’s 2025 directive that platforms disclose packaging waste intensifies traceability requirements. Consequently, the Malaysia folding carton market is migrating toward on-demand, digitally printed formats that marry sustainability, speed, and personalization.

Capacity Expansion by Domestic Paper Mills

Jingxing Paper’s MYR 1.9 billion (USD 0.46 billion) kraft-liner complex and Nextgreen IOI’s MYR 900 million (USD 222.06 million) palm-fiber pulp mill reduced dependency on imported furnish and trimmed procurement lead-times from 8-12 weeks to 4-6 weeks. Local fiber now shields converters from recovered-paper spikes, while tax allowances under the National Investment Aspirations framework sweeten project economics. Shorter supply chains reduce working capital and price volatility, allowing converters to quote tighter spreads on rush orders. As domestic capacity continues to ramp, the Malaysian folding carton market gains a cost and agility edge over neighboring sourcing hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Recovered Paper Import Prices | -0.8% | Klang Valley, Penang clusters | Short term (≤ 2 years) |

| Shortage Of Skilled Press Operators | -0.6% | Selangor and Johor | Medium term (2-4 years) |

| Rising Popularity Of Flexible Pouches For Beverage | -0.5% | Juice and dairy segments | Medium term (2-4 years) |

| Logistic Bottlenecks At Port Klang | -0.3% | National, radiating from Klang Valley | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Recovered Paper Import Prices

Mixed-paper grades traded between USD 180 and USD 260 per tonne in 2025, a 44% spread that erased 3-5 percentage-point margins for converters locked into quarterly contracts.[4]Recycling Today, “Southeast Asia Recovered Paper Import Prices 2024-2025,” recyclingtoday.com U.S. shipments to Southeast Asia fell from 1.8 million tonnes in 2023 to 1.2 million tonnes in 2025 as domestic mills hoarded fiber. Spot OCC prices spiked 28% in Q1 2025 before retreating, complicating inventory valuation for converters on 60-day terms. While Jingxing’s new mill eases virgin-fiber tightness, most white-lined chipboard still relies on imported recovered paper. Until additional domestic furnish arrives, price turbulence will continue to cap upside in the Malaysia folding carton market.

Shortage of Skilled Press Operators

The printing workforce rose only 1.7% year-on-year to 71,281 in 2023, trailing sector revenue growth and signaling a widening talent gap. In 2025, 42% of converters surveyed needed more than 90 days to fill press-operator roles, especially on six-color UV lithographic lines. Salaries run 25-30% above general manufacturing, yet negative perceptions deter graduates from entering the trade. AI-enabled vision systems from Cognex now allow one operator to oversee multiple presses, halving labor per shift. Still, until vocational training reforms yield a larger talent pool, constrained headcount will suppress throughput and incremental gains in the Malaysian folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Substrates Gain Ground

Folding boxboard retained 41.71% of Malaysia's folding carton market share in 2025 on the back of its stiffness and print fidelity for branded food, pharma, and cosmetic lines. Yet white-lined chipboard, built from 100% recycled fiber, is on track for a 6.41% CAGR as cost-conscious household-goods brands and e-commerce shippers embrace its 20-25% unit-price advantage. The Malaysian folding carton market for white-lined chipboard is poised to expand sharply once Nextgreen IOI’s palm-fiber pulp is blended into grades that comply with ISO 22002-4:2025 migration norms. Solid bleached sulfate remains the substrate of choice for prestige cosmetics, sustaining premium positioning even though import dependency from Scandinavia and North America inflates landed cost. Coated unbleached kraft is capturing ambient grocery items where its natural brown look aligns with sustainability messaging and trims freight weight by up to 10%. Hybrid micro-flute laminates, although niche, are carving a share in electronics where drop resistance trumps price.

Converters are mixing virgin and recycled furnish to hit brand-mandated barriers on odor, migration, and brightness while juggling cost. Lazada’s 2026 FSC-certification rule cements recycled-content demand but simultaneously weeds out mills lacking chain-of-custody audits, concentrating volume with ISO 14001 holders. Over the forecast window, domestic pulp additions should narrow the cost gap between folding boxboard and white-lined chipboard, softening the latter’s price edge yet cementing recycled substrates as the structural growth engine of the Malaysian folding carton market.

By Printing Technology: Digital Lifts Short-Run Economics

Lithographic printing captured 48.01% of Malaysia's folding carton market size in 2025, thanks to its unit-cost leadership on runs above 50,000 cartons and its capacity for metallic inks and spot varnishes. Digital printing, however, is scaling at a 7.24% CAGR by eliminating plate stripping, making-ready waste, and long lead times. EAN Label’s HP Indigo fleet now profits on sub-1,000 quantity runs, meeting SKU proliferation tied to regional language packs and influencer-driven micro-launches. The Malaysian folding carton market is therefore leaning into a hybrid production model, lithography for baseline volume, digital for surge, and personalization.

Flexographic printing is repositioning toward corrugated and flexible laminations where line speeds provide a cost edge, leaving folding carton share to drip toward litho-digital hybrids. Gravure remains a niche reserved for ultra-long tobacco, and confectionery runs where cylinder amortization still pays. Vision-inspection automation is bridging the historical quality gap between digital and offset, prompting large converters to add seven-color digital units beside ten-color UV lithographic lines. As brand owners tighten waste metrics, digital’s 40-50% reduction in makeready sheets will unlock incremental share across the Malaysian folding carton market.

By End-User Industry: E-Commerce Reshapes Carton Design

Food and beverage consumers accounted for 52.15% revenue share in 2025, anchored by instant noodles, ready-to-drink beverages, and confectionery that rely on grease-resistant folding boxboard. The Malaysian folding carton market, however, is projected to expand fastest at a 7.81% CAGR, tied to e-commerce and retail-ready packaging as direct-to-consumer fulfillment normalizes daily micro-orders. Healthcare and pharmaceuticals order tamper-evident cartons that meet ISO 22002-4:2025 migration standards, absorbing material cost premiums in exchange for mitigated recall risk. Personal care and cosmetics continue to premiumize, switching rigid plastics to solid bleached sulfate cartons embossed for shelf impact.

Electrical and electronics assemblers in Penang and Melaka increasingly specify anti-static, micro-flute hybrids that double as retail packaging, a crossover that blurs the historical boundary between corrugated and folding cartons. Tobacco’s share is eroding under plain-pack rules, while flexible pouches cannibalize juice and dairy cartons where ambient retort stability trumps rigidity. Across segments, platform mandates for FSC and water-based inks are universalizing compliance costs, tilting the competitive field toward converters able to service multiple end-user requirements under a single, digitally traceable roof, and deepening specialization within the Malaysian folding carton market.

Geography Analysis

Converter capacity clusters around the Klang Valley, Penang, and Johor, jointly representing more than 70% of national volume. Klang Valley suppliers enjoy 24- to 48-hour truck delivery to food processors and pharma fillers, offsetting rental and labor premiums with lower inventory buffers. Port Klang’s record 15.14 million TEU throughput in 2025 underscores logistical centrality, yet Ramadan-related vessel bunching in January 2026 stalled berths for an average of 2.7 days, prompting converters to hold four to six weeks of buffer stock. Penang, anchored by USD 10 billion in active semiconductor investments, sustains a high-mix, high-precision demand for anti-static, die-cut folding cartons, routinely priced 15-20% above commodity food-grade prices. Johor leverages the Iskandar Malaysia corridor into Singapore, supplying cross-border e-commerce flows that doubled between 2023 and 2025.

Lazada and Shopee have co-located automated fulfillment centers here, standardizing carton dimensions to fit high-speed packing cells. Secondary nodes such as Melaka, Perak, and Pahang serve niche agrifood and aftermarket auto-parts producers that prefer same-week turnaround over volume discounts. Melaka’s proximity to Nextgreen IOI’s palm-fiber mill shortens pulp haulage, enticing converters to trial mixed-fiber recipes that meet food-contact rules without importing Scandinavian virgin grades.

Perak’s legacy automotive estates are retrofitting lines for retail-ready detergent and hardware cartons, replacing corrugated outers and improving shelf presentation. Pahang’s tropical-fruit exporters still rely on Klang Valley converters, absorbing freight and two-day lead penalties that smaller regional plants cannot yet undercut. As domestic pulp and linerboard capacity expands, the Malaysian folding carton market will likely see incremental shifts toward inland production, but coastal logistics hubs will remain indispensable for export-oriented converters through 2031.

Competitive Landscape

The top five converters, Muda Holdings, Can-One Berhad, Oji’s GS Paperboard and Packaging, Orient Press, and KYM Holdings, share roughly 40-45% of national output, leaving a long competitive tail of family-owned mills and regional specialists. Certification is emerging as the primary moat. Can-One’s April 2026 acquisition of Kian Joo Can Factory consolidates metal-can and folding-carton assets, unlocking cross-selling to multinational beverage accounts and boosting integrated share capture.

Tetra Pak’s 95% share of Malaysian aseptic carton consumption, sourced from its expanded Vietnam hub, illustrates the region’s cross-border supply integration and pressures local converters to differentiate through speed and substrate variety rather than pure scale. White-space opportunities cluster around e-commerce retail-ready cartons where inline digital print and automated die-cutting command 20-30% premiums. Technology deployment separates contenders from followers. EAN Label Malaysia allocates 80% of its capital budget to HP digital presses, enabling 48-hour delivery for micro-runs.

Cognex vision systems double operator throughput by cutting defect-scan time from 30 seconds to 0.6 seconds. Meanwhile, Lazada and Shopee’s surcharge on non-certified packaging from July 2026 is flushing sub-scale players out of tier-one supply lists, accelerating share consolidation. Over the forecast window, the Malaysian folding carton market will likely settle into a barbell structure a lean cohort of large, multi-plant groups serving FMCG, electronics, and pharma majors, and a nimble cadre of digital-first specialists addressing niche, quick-turn demand.

Malaysia Folding Carton Industry Leaders

Muda Holdings Berhad

Oji Holdings Corporation

Can-One Berhad

Tetra Pak Malaysia Sdn Bhd

New Toyo International Holdings Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Can-One Berhad completed the 97.48% acquisition of Kian Joo Can Factory Berhad for MYR 3.10 (USD 0.76) per share, integrating metal-can and folding-carton assets under one roof.

- April 2026: Tetra Pak Malaysia introduced a 1-liter aseptic carton containing 90% renewable material and cutting carbon footprint by 50% versus polyethylene-laminated legacy packs.

- April 2026: Mondi Group formed PT Mondi Indo Prakarsa Kemasan, a 60-40 venture with Indocement, adding 200 million paper-bag capacity in Indonesia and signaling Southeast Asian expansion.

- February 2026: Can-One Berhad divested its food and beverage Nutrition creamer unit for MYR 1.0 billion (USD 210 million) to re-allocate capital toward packaging growth.

Malaysia Folding Carton Market Report Scope

The Malaysia folding cartons market refers to the production and commercialization of paperboard-based packaging solutions that are folded into cartons for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The Malaysia Folding Cartons Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-Commerce and Retail-Ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-Commerce and Retail-Ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the Malaysia folding carton market and how fast will it grow?

The market is valued at USD 506.91 million in 2026 and is projected to reach USD 662.94 million by 2031, growing at a 5.51% CAGR.

Which material type is expanding fastest within Malaysian folding cartons?

White-lined chipboard is forecast to record the quickest rise, advancing at a 6.41% CAGR through 2031 as cost-sensitive brands and e-commerce shippers adopt recycled fiber boards.

How are e-commerce platforms shaping folding-carton specifications?

Grab, Lazada, and Shopee now require FSC-certified substrates and water-based inks, favor tamper-evident locks, and penalize non-compliant suppliers with a 3% surcharge, pushing converters toward digital, traceable production lines.

What role do domestic pulp and paper mills play in market pricing?

New mills from Jingxing Paper and Nextgreen IOI have cut procurement lead-times to 4-6 weeks and reduced freight outlays by up to 15%, buffering converters against imported recovered-paper volatility.

Why is digital printing gaining share in Malaysian folding cartons?

Digital presses eliminate plate costs, cut make-ready waste by roughly 40-50%, and enable profitable runs as small as 500 units, matching the SKU fragmentation that dominates quick-commerce channels.

Which regions inside Malaysia host the densest folding-carton capacity?

Klang Valley accounts for the lion's share due to proximity to Port Klang and FMCG plants, while Penang and Johor follow as electronics and cross-border e-commerce hubs, respectively.

Page last updated on: