South Africa Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

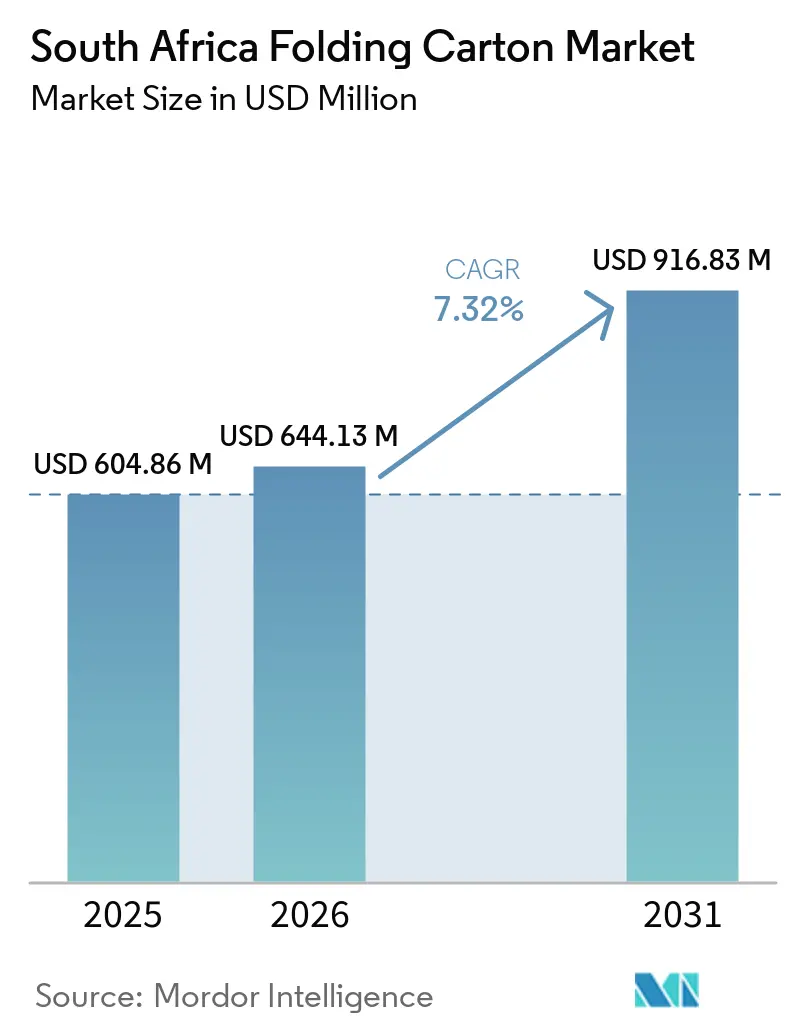

| Base Year Market Size (2025) | USD 604.86 Million |

| Market Size (2026) | USD 644.13 Million |

| Market Size (2031) | USD 916.83 Million |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

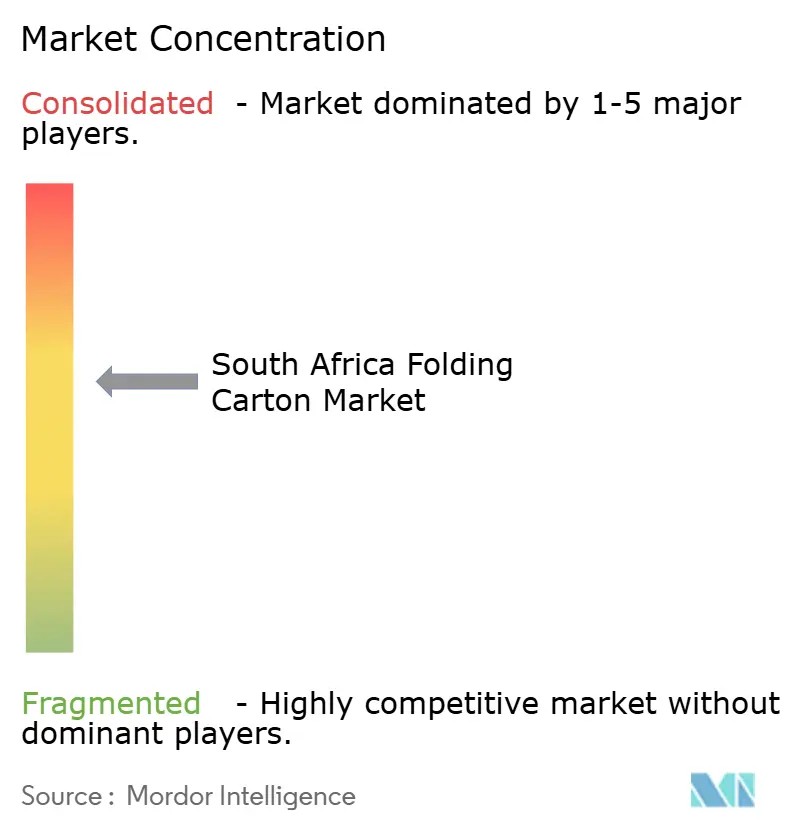

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Folding Carton Market Analysis by Mordor Intelligence

The South Africa folding carton market size was valued at USD 604.86 million in 2025 and is estimated to grow from USD 644.13 million in 2026 to reach USD 916.83 million by 2031, at a CAGR of 7.32% during the forecast period (2026-2031). Structural shifts in domestic packaging demand are lifting the South Africa folding carton market, most notably the rapid build-out of quick-commerce grocery platforms, rising localization of pharmaceutical secondary-packaging lines, and a brand-owner pivot toward premium shelf-ready formats that cut merchandising labor. Imports priced up to 20% below domestic cartonboard production costs continue to challenge local mills, yet converters that integrate digital printing, secure certified fiber streams, and design for Extended Producer Responsibility compliance are capturing a disproportionate share. Investment in solar generation, water-based barrier coatings, and inline quality-control systems is helping mitigate electricity instability and labor constraints. Although flexible pouches threaten volumes in dry foods, the South Africa folding carton market benefits from the country’s 63.3% paper-recycling rate and a tightening regulatory focus on plastic-waste diversion.

Key Report Takeaways

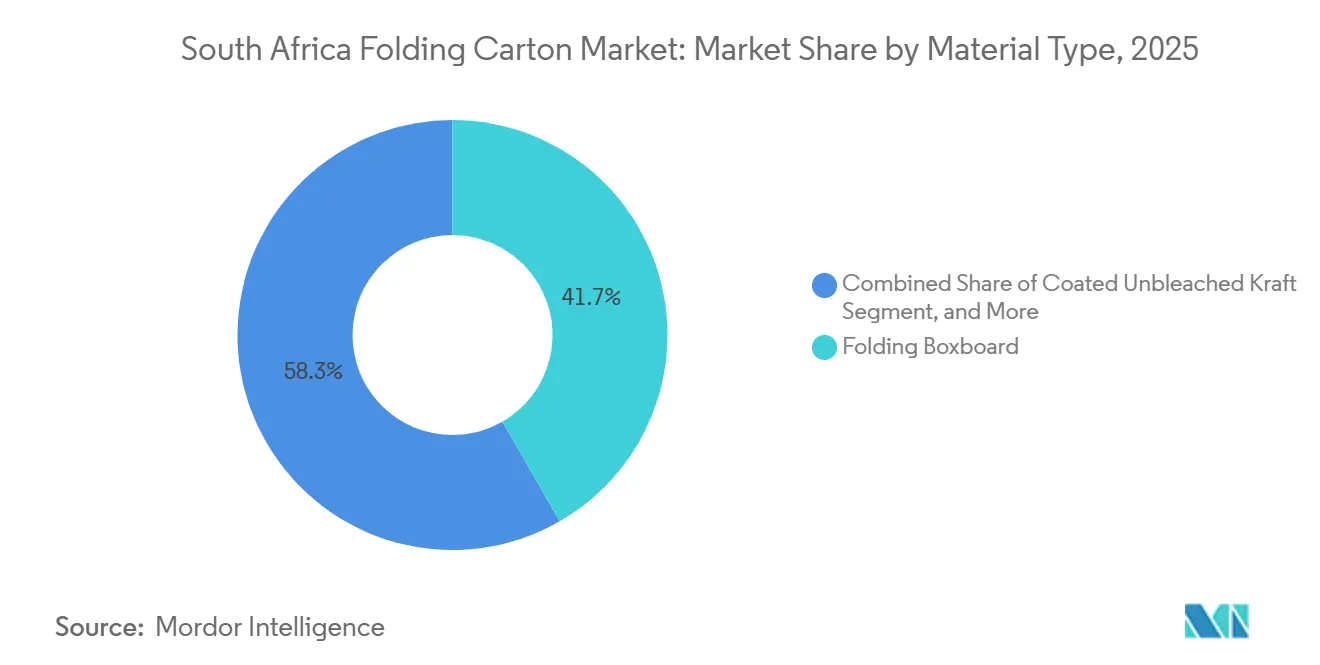

- By material type, folding boxboard captured with 41.68% of the South Africa folding carton market share in 2025.

- By printing technology, the South Africa folding carton market size for digital printing is projected to grow at a 8.74% CAGR to 2031.

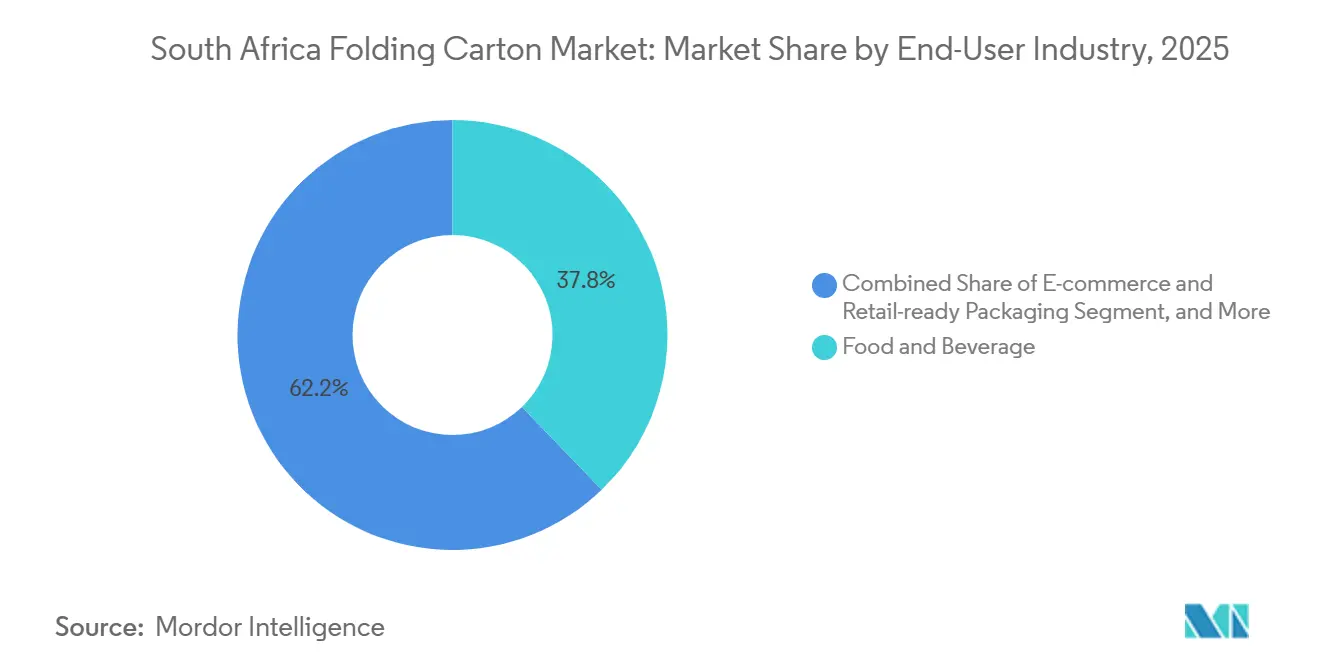

- By end-user industry, the food and beverage industry captured 37.78% of the South Africa folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Recyclable Primary Packaging in Foodservice | +1.8% | National, concentrated in Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Growth of Quick-Commerce Grocery Platforms | +1.5% | National, early gains in Johannesburg, Cape Town, Durban | Short term (≤ 2 years) |

| Localization of Pharmaceutical Packaging Supply Chains | +1.2% | National, anchored in Cape Town, OR Tambo SEZ | Medium term (2-4 years) |

| Brand Owner Shift to Premium Shelf-Ready Formats | +1.0% | National, major metro retail hubs | Medium term (2-4 years) |

| Surge in Digital Printing Adoption for Short Runs | +0.9% | National, converter clusters in Gauteng, Western Cape | Short term (≤ 2 years) |

| Government Incentives for Post-Consumer Fiber Collection | +0.7% | National, PRO infrastructure rollout nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Recyclable Primary Packaging in Foodservice

Foodservice chains are replacing single-use plastics with grease-resistant, compostable folding cartons to meet municipal diversion targets, taking advantage of South Africa’s 63.3% paper-recycling rate. Quick-service restaurants and ghost kitchens specify water-based barrier coatings that maintain carton recyclability, spurring coating-formulation innovation among converters. Draft National Waste Management Strategy 2026 proposals to introduce deposit-return schemes could further tilt cost-benefit calculations in favor of fiber. Investments in mono-material structures and FSC-certified substrates are therefore rising fastest in Gauteng and Western Cape urban centers, where municipal enforcement is strongest.

Growth of Quick-Commerce Grocery Platforms

10- to 30-minute delivery services demand durable, pre-glued cartons that double as shelf displays and shipping containers, reshaping the South Africa folding carton market. Pick n Pay’s asap! Service has reached 600 locations with 60% year-on-year delivery growth, driving converters located in Johannesburg, Cape Town, and Durban to align production schedules with fulfillment-center replenishment cycles.[1]Bizcommunity, “Pick n Pay asap expands to 600 locations,” bizcommunity.com Compact tear-strip designs and tamper-evident closures dominate these orders, while SKU proliferation favors digital and hybrid printing for economical runs of 5,000 units or fewer.

Localization of Pharmaceutical Packaging Supply Chains

Pandemic-era disruption and new regulatory alignment with International Council for Harmonization guidelines have pushed multinational pharma firms to onshore secondary packaging. Haleon’s ZAR 500 million (USD 27.68 million) Cape Town expansion and the OR Tambo SEZ pharmaceutical cluster are creating demand for serialized, traceable folding cartons that must integrate Braille embossing and vision-inspection verification. Converters holding ISO 15378 certification and offering inline serialization are winning multi-year contracts.

Brand Owner Shift to Premium Shelf-Ready Formats

Retailers mandate shelf-ready packaging to reduce replenishment labor, especially in beauty, personal care, and beverage aisles. The national beauty market exceeded ZAR 64.5 billion (USD 3.57 billion) in 2024, and premiumization has accelerated demand for high-graphics cartons incorporating perforated tear-away fronts and reinforced bases. FSC-certified board demand has increased by more than 40% since 2023, underscoring how sustainability credentials intertwine with shelf appeal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recovered Paper Export Prices | -1.1% | National, affects recyclers and converters using recycled content | Short term (≤ 2 years) |

| Power Grid Instability Affecting Converting Operations | -1.3% | National, acute in Gauteng, KwaZulu-Natal industrial zones | Medium term (2-4 years) |

| Slow Certification of Sustainable Forestry Plantations | -0.6% | National, forestry regions in Mpumalanga, KwaZulu-Natal | Long term (≥ 4 years) |

| Growing Popularity of Flexible Pouches in Dry Foods | -0.8% | National, cereals, snacks, pet-food categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recovered Paper Export Prices

Red Sea shipping disruptions added USD 1,000-3,000 per container to freight surcharges in 2025, squeezing converters that rely on recycled-content substrates. Sudden price swings complicate quarterly contract negotiations and can push brand owners to shift volumes into flexible packaging when carton surcharges rise. Dual-sourcing and investments in domestic de-inking capacity offer partial insulation, yet closure of Mpact’s Springs mill would increase reliance on imported board grades and exacerbate currency-linked volatility.

Power Grid Instability Affecting Converting Operations

Load-shedding has reduced paper, publishing, and printing output by 7.9% year-on-year, forcing converters to install standby generators and rooftop solar. These stopgap solutions add 8-12% to total conversion costs and shorten equipment life due to frequent start-stop cycles. Smaller converters unable to fund energy diversification continue to lose uptime, widening the competitive gap with import sources operating on stable, lower-cost electricity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Virgin Grades Anchor Share, Kraft Leads Growth

Folding Boxboard accounted for 41.68% of the South African folding carton market revenue in 2025, thanks to its high stiffness and FDA-compliant coatings, which are well-suited to food, pharma, and beauty applications. Coated Unbleached Kraft is on track for a 9.13% CAGR through 2031, as its natural-fiber appearance aligns with consumer expectations for eco-friendly, premium packaging. Solid Bleached Sulfate retains a niche among luxury cosmetics and electronics, although its share is slipping as brands introduce recycled-content and unbleached options. White Line Chipboard remains popular in dry groceries and household goods, yet flexible pouches erode its volumes by offering weight and logistics savings.

Sappi’s plantation network and Mpact’s virgin-pulp upgrade ensure local supply of high-quality fiber, though strong rand periods have compressed export competitiveness.[2]Sappi, “Sappi Q2 FY2026 Results,” sappi.com Converters blend certified virgin pulp with post-consumer fiber to satisfy EPR recycled-content rules while maintaining structural integrity. Expansion notes that FSC natural-forest standards became effective in 2026, gradually improving certified-fiber access, while the South African Forestry Assurance Scheme’s PEFC endorsement application raises expectations for broader plantation certification. This momentum should expand the addressable pool of responsibly sourced substrates as brand owners phase in tighter chain-of-custody audits from 2027 onward.

By Printing Technology: Litho Dominates, Digital Scales Fast

Lithographic Printing earned 48.16% of the South African folding carton market share in 2025, thanks to its cost efficiency for mid- to long-run printing and its compatibility with foil stamping and embossing. Digital Printing is forecast to post an 8.74% CAGR to 2031 as SKU proliferation, versioning, and personalization outpace litho’s economic advantages on runs below 5,000 blanks. Hybrid presses that add inkjet stations to offset lines are emerging as a bridge, giving converters variable-print capability without sacrificing litho unit costs.

Flexography maintains a share in corrugated and coated-liner applications where substrate range, speed, and cost trump color fidelity, while gravure remains restricted to ultra-long tobacco and beverage orders. A growing number of converters offer web-to-print portals that integrate directly with fulfillment center order systems, enabling same-day printing and 48-hour delivery of digitally printed cartons for flash-sale promotions. These service models complement the South Africa folding carton market’s shift toward just-in-time inventory management and lower obsolescence risk.

By End-User Industry: Food Anchors Demand, E-Commerce Surges

Food and Beverage accounted for 37.78% of South Africa's folding carton market in 2025, as dairy, bakery, and ready meals favored tamper-evident formats and clear consumer messaging. E-commerce and Retail-Ready Packaging is expected to clock a 9.28% CAGR through 2031, riding on the expansion of quick-commerce grocery models and private-label lines. Healthcare and Pharmaceuticals consumption is accelerating alongside localized blister-pack and vial-carton assembly in Cape Town and the OR Tambo logistics corridor.

Personal Care and Cosmetics growth parallels premiumization, with retailers launching exclusive ranges that need tactile varnishes, soft-touch laminates, and metallic foils on certified boards. Electronics and tobacco continue to face headwinds from minimalist unboxing trends and plain-pack legislation, respectively, while pet food and agricultural inputs create niche opportunities for grease- and moisture-barrier board constructions.

Geography Analysis

Gauteng, Western Cape, and KwaZulu-Natal dominate the South Africa folding carton market, jointly housing most converting lines, distribution hubs, and brand-owner headquarters. Gauteng’s proximity to Johannesburg’s corporate base and OR Tambo International Airport makes it the country’s largest folding-carton production cluster, yet recurring load shedding and long inland freight distances inflate costs.

Western Cape benefits from Cape Town’s port access, Haleon’s pharma investment, and an export-oriented wine and fruit industry that values certified, cold-chain-compatible folding cartons.[3]Engineering News, “Haleon invests R500m in Cape Town facility,” engineeringnews.co.za KwaZulu-Natal leverages Durban’s port and the Dube TradePort SEZ to attract flexible-packaging investment that directly competes with traditional cartons. Inland forestry provinces Mpumalanga and Limpopo supply virgin pulp and recovered fiber but lack finishing capacity, forcing converters to ship board long distances to coastal fulfillment centers.

Eastern and Northern Cape remain largely served by shipments from Gauteng and Western Cape. Cross-border flows into Botswana, Namibia, and Zimbabwe are growing as local brands seek higher-spec packaging that meets South Africa’s EPR compliance benchmarks. If Mpact shuts down its Springs mill in 2026, coastal converters near ports would gain a lead on import logistics, while inland plants face inventory inflation and extended lead times that could erode competitiveness.

Competitive Landscape

Market concentration is moderate, with Mpact, Mondi, Smurfit WestRock, and Graphic Packaging leading but collectively facing pressure from over ten regional converters and an influx of flexible-pack newcomers. Mpact booked ZAR 14 billion (USD 0.78 billion) in 2025 revenue and has installed 18 MWp of solar to counter power costs, yet considers closing its Springs mill because European and Asian imports undercut local board prices.

Mondi restructured into two business units in 2025 and reported EUR 7.41 billion (USD 8.32 billion) sales, citing subdued demand but maintaining capital-expenditure discipline on high-return packaging lines.[4]Mondi, “Results and Reports,” mondigroup.com All4Labels’ EUR 1.6 million (USD 1.80 million) carton and label investment positions it for pharma and premium FMCG niches, while Packaging World's private-equity backing highlights investor interest in recyclable flexible platforms that could cannibalize carton share.

Technology differentiation is sharpening: converters adding BOBST digital-ready gluing lines and automated inspection command pricing premiums and faster turnaround for serialized pharma cartons and limited-edition consumer launches. Compliance with FSC or PEFC chain-of-custody standards, and a clear plan to integrate post-consumer fiber, are becoming non-negotiable for multinational FMCG tenders, accelerating capital outlays for de-inking plants and traceability systems.

South Africa Folding Carton Industry Leaders

Mpact Limited

Mondi plc

Huhtamaki Oyj

Novus Holdings

Graphic Packaging Holding Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Wyda Packaging bought Hulamin Containers’ assets, raising foil-container press capacity by 340% and reinforcing local foodservice supply.

- February 2026: RMB Corvest and Alito Fund 2 took a majority stake in Packaging World to scale recyclable flexible solutions for FMCG foods.

- December 2025: Packamama began South African production of its 25% rPET eco-flat wine bottle with Safripol and Polyoak, advancing beverage sustainability goals.

- January 2025: RMB Corvest and Dlondlobala Capital led a management buy-out of Nampak Liquid Cartons operations worth R450 million (USD 24.9 million), forming Diversified Liquid Packaging Group.

South Africa Folding Carton Market Report Scope

The scope of this report covers the analysis of the folding carton market in South Africa. Folding cartons are paper-based packaging solutions widely used across various industries, including food and beverage, personal care, pharmaceuticals, and others. These cartons are lightweight, customizable, and recyclable, making them a preferred choice for sustainable packaging. The report examines market trends, growth drivers, challenges, and opportunities, providing insights into the current market dynamics and future prospects.

The South Africa Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current South Africa folding carton market size and its forecast growth?

The South Africa folding carton market size stood at USD 604.86 million in 2025 and is projected to reach USD 916.83 million by 2031, expanding at a 7.32% CAGR over 2026-2031.

Which material type leads the market, and which is growing fastest?

Folding Boxboard leads with a 41.68% market share, while Coated Unbleached Kraft is the fastest-growing material, forecast to grow at a 9.13% CAGR through 2031.

Why is digital printing adoption rising in South Africa’s folding-carton sector?

SKU proliferation, personalization demands and economical short-run requirements under 5,000 units make digital presses attractive, supporting an 8.74% CAGR for the technology to 2031.

How are power-grid challenges affecting converters?

Load-shedding cuts machine uptime and adds 8-12% to conversion costs, prompting investments in solar arrays and backup generation to maintain production continuity.

Which end-use sector will grow the quickest in folding cartons?

E-commerce and Retail-Ready Packaging is expected to post the highest 9.28% CAGR as quick-commerce grocery services multiply across major metros.

What sustainability certifications are most important for folding-carton suppliers?

FSC and impending PEFC chain-of-custody certification, coupled with compliance to South Africa’s Extended Producer Responsibility regulations, have become essential for winning FMCG contracts.

Page last updated on: