Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 103.12 Billion |

| Market Size (2031) | USD 147.56 Billion |

| Growth Rate (2026 - 2031) | 7.43% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

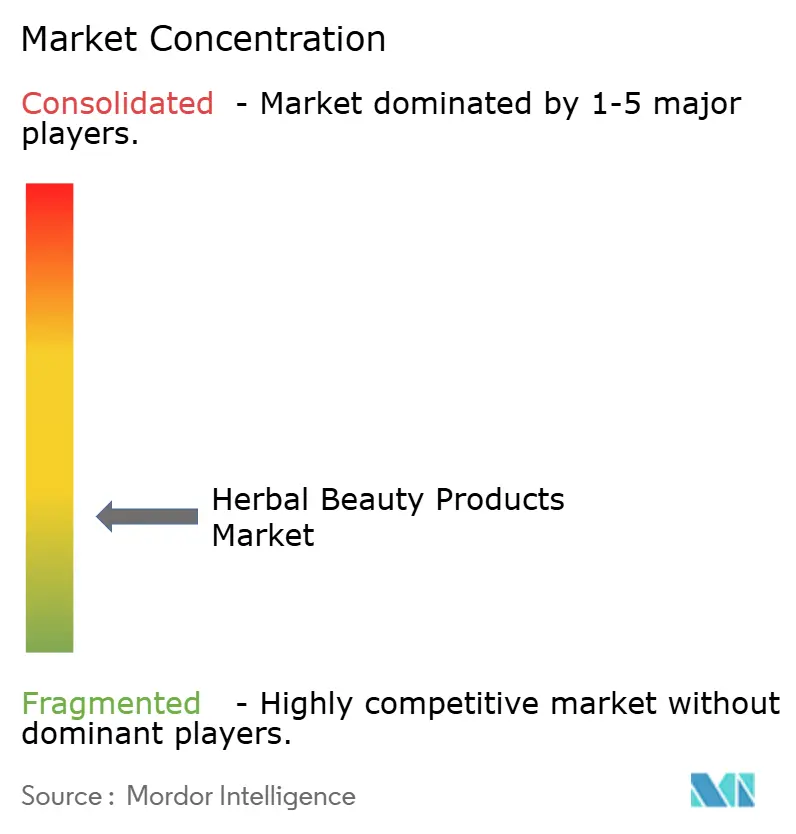

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Herbal Beauty Products Market Analysis by Mordor Intelligence

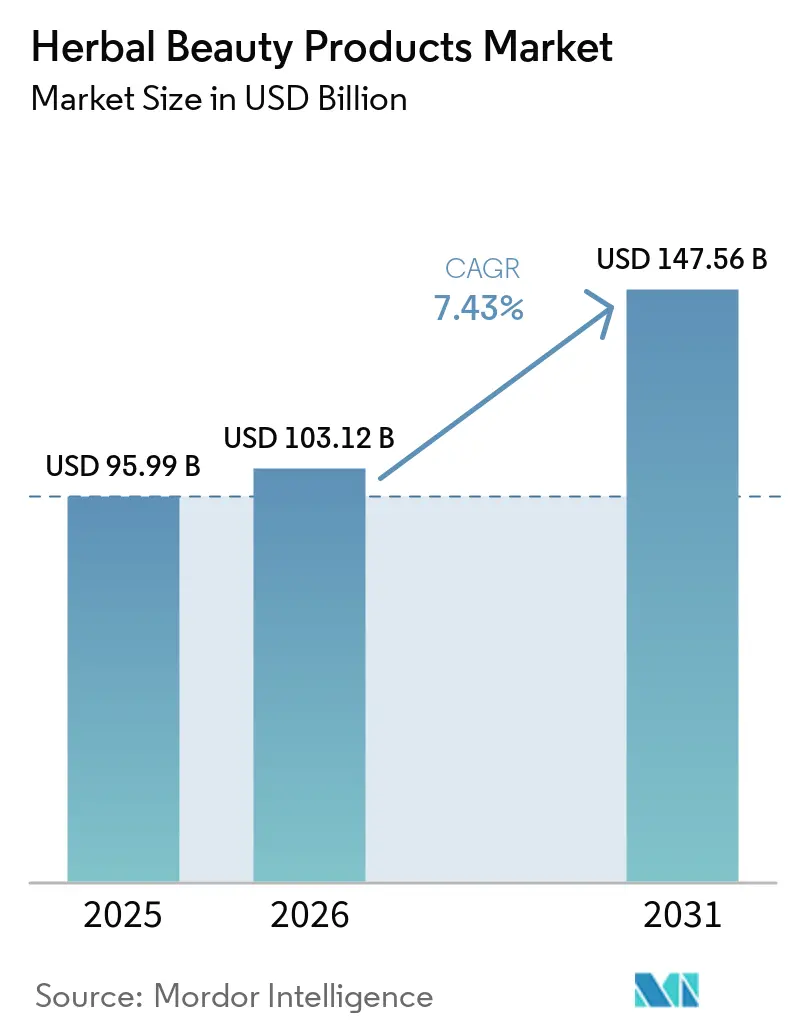

The herbal beauty products market size in 2026 is estimated at USD 103.12 billion, growing from 2025 value of USD 95.99 billion with 2031 projections showing USD 147.56 billion, growing at 7.43% CAGR over 2026-2031. Demand accelerates as consumers embrace plant-based alternatives that align with clean-label expectations, stricter chemical bans, and wellness-centric lifestyles. Brand storytelling around traditional medicine, coupled with verifiable clinical data on botanical actives, raises perceived product value. Digital engagement amplifies ingredient transparency, while innovation in sustainable sourcing and circular packaging reshapes competitive positioning across the herbal beauty products market. Companies that integrate traceable supply chains, AI-assisted formulation, and omnichannel retail strategies are gaining early-mover advantages within this expanding landscape.

Key Report Takeaways

- By product type, personal care products led with 93.72% revenue share in 2025; cosmetics/make-up products are projected to expand at a 8.92% CAGR through 2031.

- By category, the mass segment held 70.02% of the herbal beauty products market share in 2025, while the premium segment is forecast to grow at an 8.46% CAGR between 2026 and 2031.

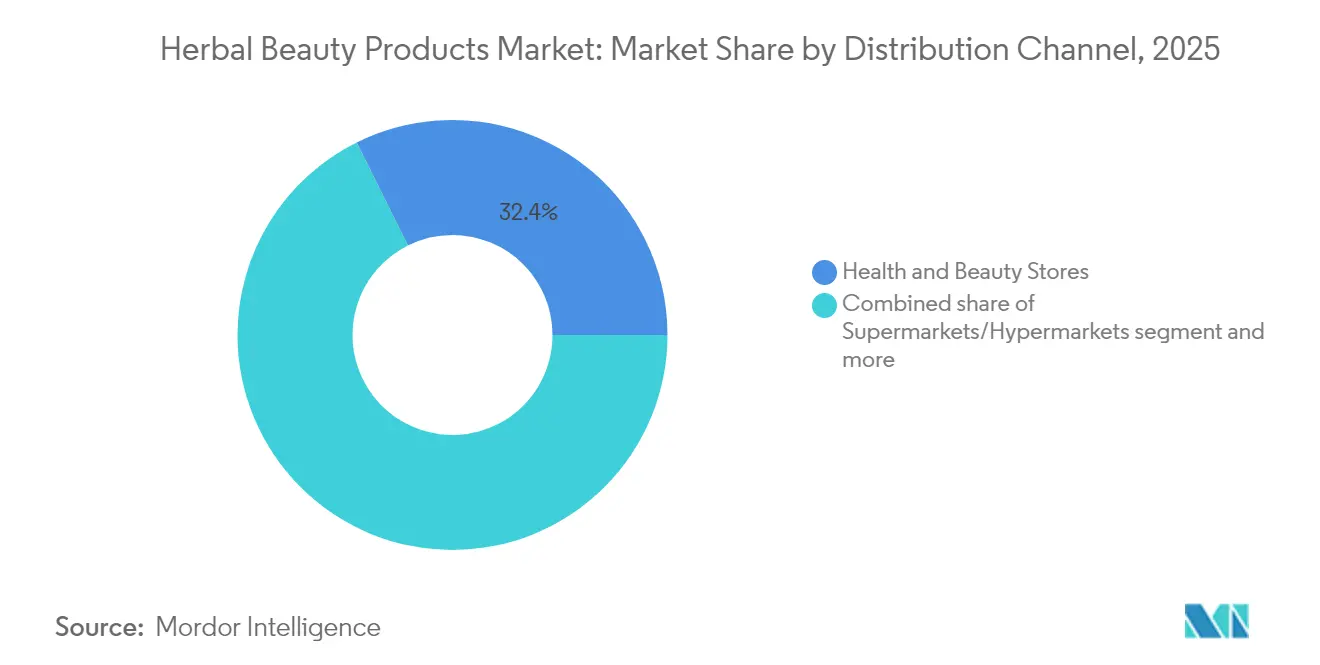

- By distribution channel, health and beauty stores captured 32.35% share of the herbal beauty products market size in 2025, and online retail stores are advancing at an 7.78% CAGR through 2031.

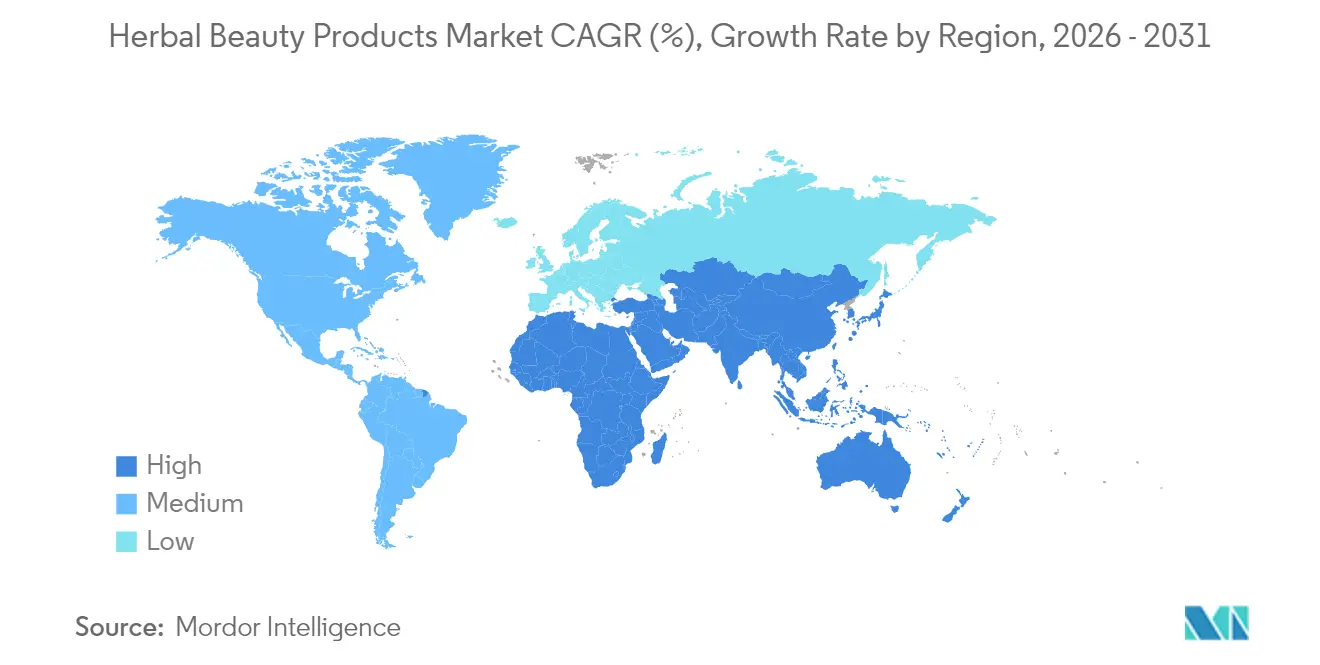

- By geography, Asia-Pacific accounted for 48.20% of the herbal beauty products market share in 2025, and the Middle East and Africa are expanding at an 7.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Herbal Beauty Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for natural, chemical-free ingredients in cosmetics | +1.4% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Growing health consciousness and wellness trends driving demand for plant-based beauty solutions | +1.1% | Global, particularly pronounced in Asia-Pacific and North America | Long term (≥ 4 years) |

| Influence of social media and beauty influencers promoting herbal product benefits | +0.9% | Global, with highest penetration in North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Regulatory restrictions and bans on certain synthetic chemicals boosting herbal alternatives | +0.8% | Europe and North America primarily, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expanded product portfolios featuring innovative herbal ingredient combinations and formulations | +0.6% | Global, with innovation centers in North America, Europe, and Japan | Medium term (2-4 years) |

| Shift toward sustainable manufacturing and transparent ingredient sourcing | +0.5% | Europe and North America leading, expanding to Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for natural, chemical-free ingredients in cosmetics

Consumer demand for natural, chemical-free ingredients continues to increase, with 62% of global consumers in 2023 indicating their willingness to modify purchasing decisions to minimize environmental impact, as per Consumers International [1]Source: Consumers International, "New Report: Unlocking sustainable living through global consumer insights", consumersinternational.org. This market shift stems from heightened awareness of health risks linked to synthetic ingredients like parabens, sulfates, and preservatives, leading consumers to choose herbal alternatives. Digital technology, particularly mobile apps and social media platforms, enables consumers to research ingredient information and make informed decisions. Third-party certifications from organizations like COSMOS and NATRUE provide validation for natural formulations, addressing the needs of health-conscious consumers. The trend encompasses broader product considerations, with consumers supporting companies that demonstrate commitment to sustainable sourcing and ethical procurement of botanical ingredients. Companies like Weleda and Forest Essentials demonstrate this trend by offering certified herbal beauty products with eco-friendly credentials and sustainable packaging. This comprehensive consumer approach drives market growth by integrating health, sustainability, and ethical values into purchasing decisions, strengthening the herbal segment's position within the natural beauty category. The combination of digital empowerment, regulatory standards, and increasing environmental awareness indicates sustained market expansion in the coming years.

Growing health consciousness and wellness trends driving demand for plant-based beauty solutions

The increasing health awareness and wellness trends have significantly influenced the demand for plant-based beauty products in the global market. Consumers now consider herbal beauty products as essential components of their overall health practices, rather than just cosmetic products. This shift reflects a broader movement toward preventive health measures and stress management, drawing from traditional practices like Ayurveda and Traditional Chinese Medicine. Peer-reviewed research has strengthened consumer confidence, particularly for products containing proven ingredients such as turmeric, green tea, and botanical peptides. The market has responded with multifunctional products that combine skincare with aromatherapy benefits and hair care products containing stress-reducing botanical ingredients. Consumers demonstrate a willingness to purchase premium-priced herbal products, indicating their preference for long-term health benefits over short-term cosmetic results. Companies like Weleda have successfully combined scientific research with traditional wellness practices to create premium herbal products that appeal to health-conscious consumers. The integration of wellness and beauty has transformed plant-based products into essential lifestyle components that support both physical and mental well-being. The growth in plant-based beauty products indicates increased demand for natural ingredients and wellness-focused product development. This trend continues to drive growth in the market as consumers seek products that emphasize health benefits and therapeutic effectiveness. Consumer preferences for wellness-oriented products continue to influence innovation and market expansion in the global herbal beauty industry.

Influence of social media and beauty influencers promoting herbal product benefits

The market for herbal beauty products has evolved through digital platforms that transform consumer discovery, evaluation, and purchasing patterns globally. Instagram has become the primary channel for 91% of female Gen Z consumers in the GCC region in 2024 (Chalhoub Group) [2]Source: Chalhoub Group, "Gen Z’s Skincare eEvolution in GCC: UNFILTERED", chalhoubgroup.com. Beauty influencers and content creators educate audiences about botanical ingredients, traditional preparation methods, and the cultural heritage of herbal formulations, which builds consumer understanding and trust. Social media platforms allow herbal beauty brands to showcase natural ingredients, sustainable packaging, and brand stories that connect with environmentally-conscious consumers. User-generated content and testimonials influence purchasing decisions, as consumers trust peer recommendations over traditional advertising when evaluating herbal product effectiveness. Through social media, smaller herbal brands can build communities focused on sustainability and natural wellness, enabling them to compete with large corporations. Social platforms facilitate direct consumer engagement, which strengthens brand loyalty and makes herbal beauty information more accessible. This digital connectivity increases market penetration for herbal products by meeting consumers' demands for transparency, authenticity, and ethical sourcing. Social media and influencer marketing drive the growth of the global herbal beauty products market by combining education with community engagement.

Regulatory restrictions and bans on certain synthetic chemicals boosting herbal alternatives

Regulatory changes in major markets are transforming product development and manufacturing strategies in the beauty and personal care industry. The EU's new restrictions on carcinogenic, mutagenic, or toxic for reproduction (CMR) substances, effective September 2025, include bans on specific nanomaterials in cosmetic formulations. In the US, the FDA's implementation of the Modernization of Cosmetics Regulation Act requires facility registration and product listing, increasing compliance costs for synthetic ingredient suppliers while benefiting established herbal ingredient producers who meet these requirements. The European Chemicals Agency's (ECHA) pilot inspections in 2024 found a 6.4% non-compliance rate for cosmetics containing perfluorinated compounds and cyclic siloxanes, creating opportunities for plant-based alternatives to provide safer, compliant options [3]Source: European Chemicals Agency (ECHA), "Hazardous Chemicals Found in Cosmetic Products", echa.europa.eu . These regulations accelerate product reformulation timelines and increase research and development investments in natural alternatives as companies aim to reduce risks associated with synthetic substances under safety review. Companies such as Dr. Hauschka have adapted to this environment by developing botanical formulations that meet regulatory requirements. The regulatory environment influences manufacturers to develop safer, plant-based active ingredients while encouraging consumers to choose botanical products that meet safety and compliance standards. This regulatory framework alters market dynamics in favor of natural beauty products that address safety and compliance requirements. The increased regulatory oversight serves as a growth driver for the natural ingredients segment, highlighting its importance for both manufacturers and consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain inconsistency and raw material scarcity | -0.7% | Global, with acute impact in regions dependent on wild-harvested botanicals | Short term (≤ 2 years) |

| Higher prices for herbal beauty products compared to synthetic alternatives | -0.6% | Most pronounced in price-sensitive markets across South America and parts of Asia-Pacific | Medium term (2-4 years) |

| Regulatory grey zones for CBD/hemp-infused cosmetics | -0.5% | North America and Europe primarily, with varying state/country regulations | Medium term (2-4 years) |

| Consumer skepticism toward the efficacy of some herbal products versus conventional cosmetics | -0.4% | Global, particularly in mature markets with established synthetic product preferences | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply‐chain inconsistency and raw-material scarcity

Supply chain disruptions affect botanical ingredient availability due to climate change and unsustainable harvesting practices. Medicinal plants experience habitat loss and over-exploitation, creating sourcing difficulties, particularly for wild-harvested ingredients that depend on agricultural cycles and weather conditions. These factors contribute to fluctuations in raw material costs and availability. Quality standardization presents additional complexities, as active compound concentrations vary based on soil conditions, harvesting techniques, and post-harvest processing across different regions. The industry also faces increased operational requirements through regulatory demands for traceability and sustainability documentation, requiring extensive third-party certifications that increase costs and logistical complexity. The limited availability of certified organic suppliers creates production bottlenecks, forcing manufacturers to either adjust production schedules or accept compromises in ingredient quality and cost management. Companies like Organic Harvest address these challenges through direct partnerships with certified organic farmers, prioritizing transparency and sustainable sourcing to maintain product quality despite supply uncertainties. In response, manufacturers are increasing investments in supply chain diversification, traceability technologies, and strategic partnerships. These initiatives aim to maintain product quality and ensure consistent supply while meeting consumer demand for sustainable, authentic botanical products.

Higher prices for herbal beauty products compared to synthetic alternatives due to costly ingredients and processes

The global market demonstrates significant price variations between natural and synthetic cosmetic products, driven by multiple operational factors, including elevated raw material costs, specialized processing requirements, and limited production volumes that prevent economies of scale. This pricing structure particularly affects price-sensitive markets, where consumers often choose affordability over natural ingredients, limiting herbal product adoption in lower-income segments. The manufacturing process presents specific challenges in preserving botanical active compounds during production, packaging, and storage, requiring specialized equipment and expertise that increase production costs beyond those of synthetic ingredients. The costs of organic and natural certifications, along with required testing for regulatory compliance, add to the final retail price. The industry's commitment to sustainable sourcing, fair trade practices, and eco-friendly production methods further increases operational costs, affecting the competitive position of herbal products against conventional cosmetics. Some brands incorporate these additional costs while marketing their sustainability and quality standards to premium consumers who value ethical and authentic beauty products. These combined factors position herbal beauty products in the premium category, creating adoption barriers in mainstream markets despite increasing consumer interest in natural and safer alternatives. Companies must strategically manage these pricing factors while meeting consumer demand to maintain growth and expand their global market presence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominance Drives Market Foundation

In 2025, the personal care products segment dominates the market with a commanding 93.72% share, driven by consumer preference for daily-use herbal formulations across categories such as hair care, skin care, bath and shower, and oral care. These products have seamlessly integrated into established routines. The segment's stronghold is attributed to its lower trial barriers, especially when compared to color cosmetics. Consumers are more inclined to experiment with herbal shampoos, moisturizers, and cleansers, paving the way to eventual makeup product trials. Hair care, the largest subsegment of personal care, leverages traditional knowledge of botanical ingredients. Time-tested components like henna, amla, and coconut oil have demonstrated their efficacy over centuries. Skin care, closely trailing hair care, benefits from scientific validations. Herbal actives such as turmeric, neem, and aloe vera have undergone clinical studies, supporting their anti-inflammatory and moisturizing claims.

Although cosmetics and makeup products currently hold a smaller market share, they are positioned for significant growth, with a projected 8.92% CAGR from 2026 to 2031. This growth is fueled by increasing consumer demand for herbal alternatives to conventional color cosmetics, which often contain synthetic dyes and preservatives. The acceleration in growth is supported by successful innovations, including mineral-based foundations enriched with botanical extracts, herbal lipsticks crafted from natural waxes and plant-derived pigments, and eye cosmetics featuring organic ingredients that appeal to consumers with sensitive skin. A notable example of this trend is Weleda's major brand modernization in 2025. This marked the company's first comprehensive rebrand in over a century, reflecting strategic investments by established players to capture growth in the premium herbal cosmetics segment.

By Category: Premium Segment Accelerates Despite Mass Market Leadership

In 2025, the mass category holds a dominant 70.02% market share, driven by extensive distribution networks through supermarkets, hypermarkets, and drugstore chains. This accessibility targets mainstream consumers seeking cost-effective herbal beauty solutions. The success of the mass market is attributed to simplified formulations that effectively balance natural ingredients with cost-efficient manufacturing processes. This approach ensures competitive pricing against synthetic alternatives while maintaining a strong herbal identity. Leading corporations, such as Procter & Gamble, have expanded their herbal product portfolios within the mass market. For instance, the company launched Herbal Essence hair care products in February 2024, integrating botanical extracts at affordable price points. Additionally, the segment benefits from economies of scale in ingredient sourcing and manufacturing, enabling brands to offer herbal products at prices comparable to conventional options.

Between 2026 and 2031, the premium segment is expected to grow at a CAGR of 8.46%, reflecting a shift in consumer preferences toward higher-priced products that emphasize superior ingredient quality, sustainable sourcing, and clinically validated botanical actives with enhanced efficacy. This growth aligns with broader premiumization trends in the beauty industry, where consumers increasingly view herbal products as investments in long-term skin and hair health rather than basic functional purchases. The focus on ingredient transparency, ethical sourcing, and scientific validation strengthens consumer trust and drives demand for premium herbal formulations. Brands like Forest Essential exemplify this trend by offering luxury herbal skincare solutions that combine indulgence with proven botanical benefits. The growing consumer inclination toward premium herbal beauty products highlights evolving priorities centered on wellness, efficacy, and sustainability, supporting significant market expansion in this segment globally.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Health and beauty stores dominate distribution channels with a 32.35% market share in 2025, leveraging their expertise in specialized products, curated offerings, and consumer trust in expert recommendations. These strengths are particularly advantageous for products requiring ingredient education, such as herbal beauty items. The channel's competitive edge lies in delivering personalized consultation services, enabling consumers to navigate complex botanical ingredient profiles and select products tailored to specific skin types and concerns. Store associates, trained in the benefits of herbal products, effectively communicate value propositions that justify premium pricing compared to mass-market alternatives available through other channels. The perception of authenticity and expertise associated with specialized retailers further strengthens this channel, especially for products where ingredient sourcing and processing methods significantly influence efficacy.

Online retail stores exhibit the highest growth trajectory, with an 7.78% CAGR, driven by digital-native brands, personalized product recommendations, and convenience factors that appeal to younger demographics who extensively research ingredients before making purchases. E-commerce platforms allow brands to provide detailed ingredient information, customer reviews, and educational content, supporting informed decision-making. This channel particularly benefits smaller brands that lack the resources for extensive physical retail distribution but can compete effectively through targeted online marketing and direct-to-consumer sales models. Supermarkets, hypermarkets, and other distribution channels maintain steady market positions by offering convenience and competitive pricing for established brands. However, their growth rates lag behind specialized and digital channels that focus on enhancing customer experience and product education.

Geography Analysis

In 2025, Asia-Pacific holds a commanding 48.20% market share, driven by its integration of traditional botanical expertise, advanced manufacturing capabilities, and cost advantages. These factors not only strengthen the region's domestic market leadership but also enhance its global export competitiveness. India plays a pivotal role in this growth, with companies like Dabur making significant investments. In August 2024, Dabur allocated Rs 400 crore (USD 48 million) to establish a new manufacturing facility in Tamil Nadu, aimed at scaling production for both local and international markets. The region's vast biodiversity provides a reliable supply of raw materials for herbal formulations, while established systems like Ayurveda and Traditional Chinese Medicine offer scientifically-backed frameworks for product innovation. China's evolving market sophistication is fueling premiumization trends, as consumers increasingly invest in clinically-validated herbal products that combine traditional ingredients with modern technologies. Additionally, Japan and South Korea drive innovation through advanced extraction techniques and high consumer standards, setting benchmarks for product efficacy and safety.

The Middle East and Africa are projected to achieve an impressive 7.96% CAGR from 2026 to 2031, supported by favorable demographic and economic conditions. In the MENA region, a youthful population, particularly in Saudi Arabia, is prioritizing sustainability and authenticity in purchasing decisions. Economic diversification initiatives across GCC countries are increasing disposable incomes and enhancing retail infrastructure, while cultural preferences for natural ingredients and traditional beauty practices create a receptive market environment. The region's strategic location, bridging Europe, Asia, and Africa, positions it as an emerging distribution hub for herbal products. Dubai's thriving cosmetics trade highlights this potential. Moreover, regulatory developments, such as halal cosmetics certification requirements in Vietnam and Indonesia, open new growth avenues for products aligned with local cultural and religious values.

North America and Europe, as mature markets, are characterized by stringent regulatory frameworks and a focus on premium positioning. These regions emphasize quality, sustainability, and clinical validation of ingredients. The EU's upcoming CMR substance bans, effective September 2025, provide a competitive edge to herbal alternatives that avoid synthetic chemicals under scrutiny. European consumers increasingly favor products with eco-friendly packaging and sustainability certifications, creating opportunities for brands that prioritize environmental responsibility. In South America, growth is fueled by abundant botanical resources, traditional knowledge, and rising investments in local manufacturing. Brazilian companies are gaining international recognition through participation in global trade shows and export market expansion initiatives.

Competitive Landscape

The competitive landscape of the global herbal beauty products market is shaped by diverse consumer preferences, regulatory challenges, and specialized botanical expertise. Leading companies such as Himalaya Global Holdings, Procter & Gamble, and Dabur leverage their scale advantages in ingredient sourcing, manufacturing, and distribution to maintain their market leadership. These established players utilize extensive networks to strengthen their positions, while emerging niche brands differentiate themselves through premium formulations and direct-to-consumer sales models. By focusing on authenticity and personalized brand experiences, these smaller players cater to the growing demand for natural and ethical products, highlighting the market's complexity and opportunities.

Strategic trends indicate a growing emphasis on vertical integration as companies aim to secure ingredient quality and reduce dependency on third-party suppliers, mitigating cost volatility. This approach is further supported by the adoption of advanced technologies, including AI-driven product development and sophisticated digital marketing strategies. These innovations enable brands to engage directly with younger, ingredient-conscious consumers and optimize their e-commerce platforms. The integration of technology enhances competitive positioning and allows companies to respond swiftly to evolving market demands. Additionally, smaller digital-native brands are disrupting traditional retail models by leveraging sustainable packaging innovations and social media influence to build intimate consumer communities without relying heavily on physical stores.

Significant growth opportunities exist in underserved segments such as men’s herbal grooming, anti-aging products for older consumers, and specialized formulas for sensitive skin that utilize gentle botanical actives. Brands like Forest Essentials effectively capitalize on these niches by combining premium natural ingredients with personalized marketing strategies. Companies that excel in botanical science, sustainable sourcing, and regulatory compliance are better positioned to succeed in this dynamic market. By integrating technology and innovative business models, these players can meet rising consumer expectations and thrive in the global herbal beauty products market.

Herbal Beauty Products Industry Leaders

-

Procter & Gamble Company

-

Groupe Rocher

-

Marico Limited

-

Dabur Ltd

-

Himalaya Global Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Dabur India entered the children's toothpaste market with Dabur Herb'l Kids Toothpaste, designed for cavity protection in children over three years of age. The toothpaste featured strawberry flavor and included character designs of Iron Man and Elsa from Frozen. The product excluded fluoride, parabens, peroxide, triclosan, SLS, and artificial flavors, positioning it as a natural alternative in the children's oral care segment.

- June 2024: My Green Space launched its herbal cosmetics brand in the B2C market. The product range featured 100% natural ingredients and was cruelty-free, paraben-free, sulphate-free, and chemical-free. The initial collection included women's skincare, haircare, and facial products formulated with essential oils.

- February 2024: Herbal Essences launched 11 new shampoo and conditioner products featuring a blend of pure aloe and camellia oil. The ingredients, certified by plant experts at The Royal Botanic Gardens, KEW, aimed to improve hair hydration and softness during winter.

Global Herbal Beauty Products Market Report Scope

Herbal beauty products are beauty products made of natural herbal ingredients such as aloe vera, almond, avocado, carrot, castor, clay, cocoa, coconut oil, cornmeal, and cucumber, avoiding chemical usage. The herbal beauty products market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into skin care products, hair care products, makeup and color cosmetics, fragrances, and other product types. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

By Product Type

| Personal Care Products | Hair Care | Shampoo |

| Conditioners | ||

| Hair Oils | ||

| Others (Hair Colorants, Hair Styling Products) | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gel/Body Wash | |

| Soaps | ||

| Others | ||

| Oral Care | ||

| Perfumes and Fragrances | ||

| Cosmetics/Make-up Products | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Make-up Products | ||

By Category

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Personal Care Products | Hair Care | Shampoo |

| Conditioners | |||

| Hair Oils | |||

| Others (Hair Colorants, Hair Styling Products) | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip and Nail Care Products | |||

| Bath and Shower | Shower Gel/Body Wash | ||

| Soaps | |||

| Others | |||

| Oral Care | |||

| Perfumes and Fragrances | |||

| Cosmetics/Make-up Products | Facial Cosmetics | ||

| Eye Cosmetics | |||

| Lip and Nail Make-up Products | |||

| By Category | Mass | ||

| Premium | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Health and Beauty Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What was the value of the herbal beauty products market in 2026?

Herbal beauty products market reached USD 103.12 billion in 2026.

Which region currently leads sales of herbal beauty products?

Asia-Pacific contributed 48.20% of global revenue in 2025.

Which product category is growing fastest through 2031?

Cosmetics/make-up products are forecast to expand at a 8.92% CAGR during 2026-2031.

Which distribution channel is gaining the most momentum?

Online retail is set to grow at 7.78% CAGR through 2031 due to ingredient transparency tools and D2C models.

Page last updated on: