Sun Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

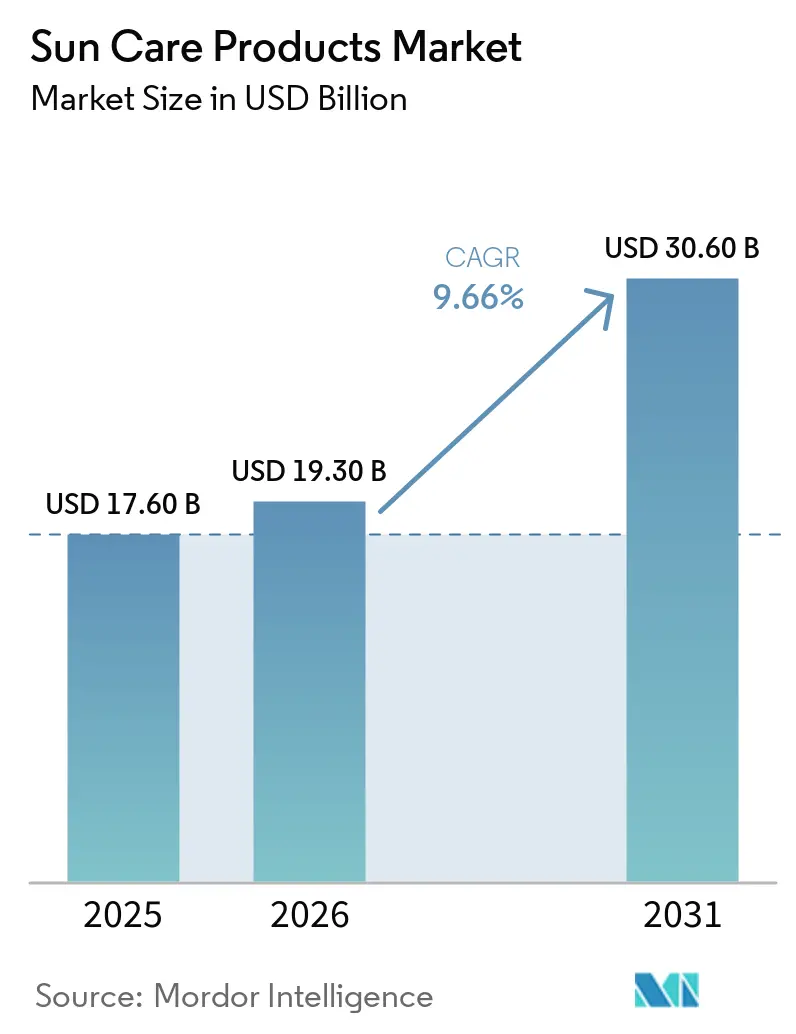

| Market Size (2026) | USD 19.30 Billion |

| Market Size (2031) | USD 30.60 Billion |

| Growth Rate (2026 - 2031) | 9.66% CAGR |

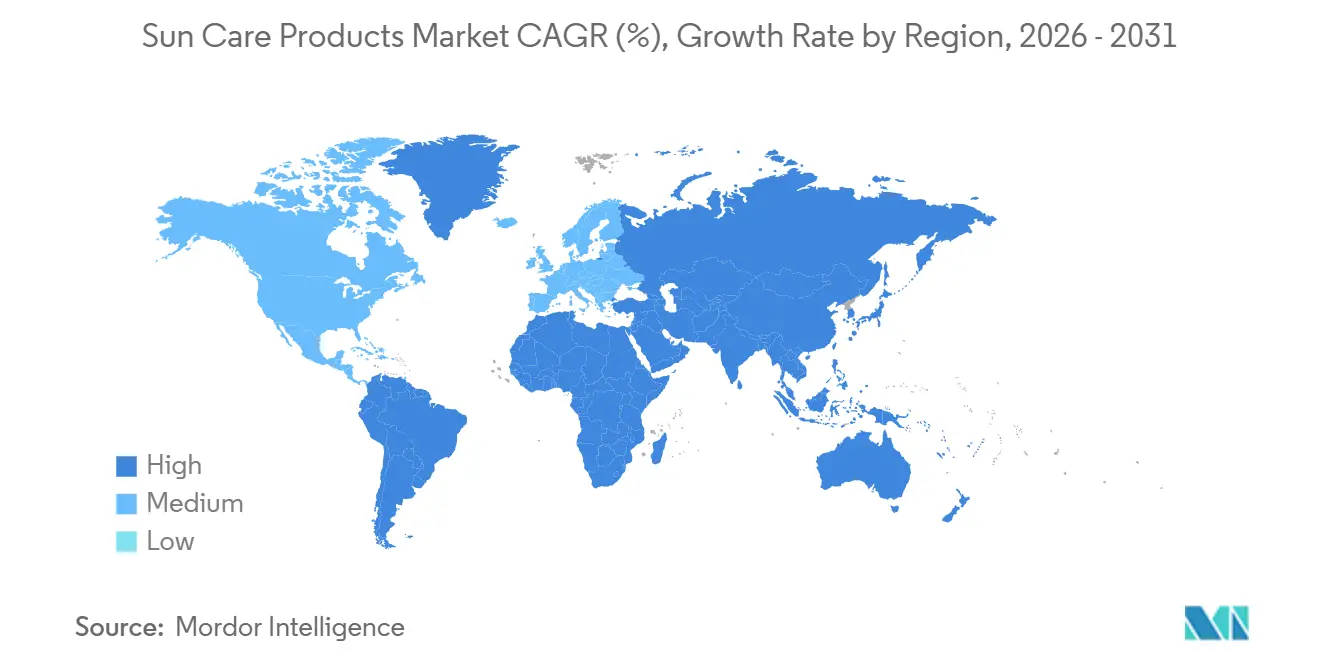

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

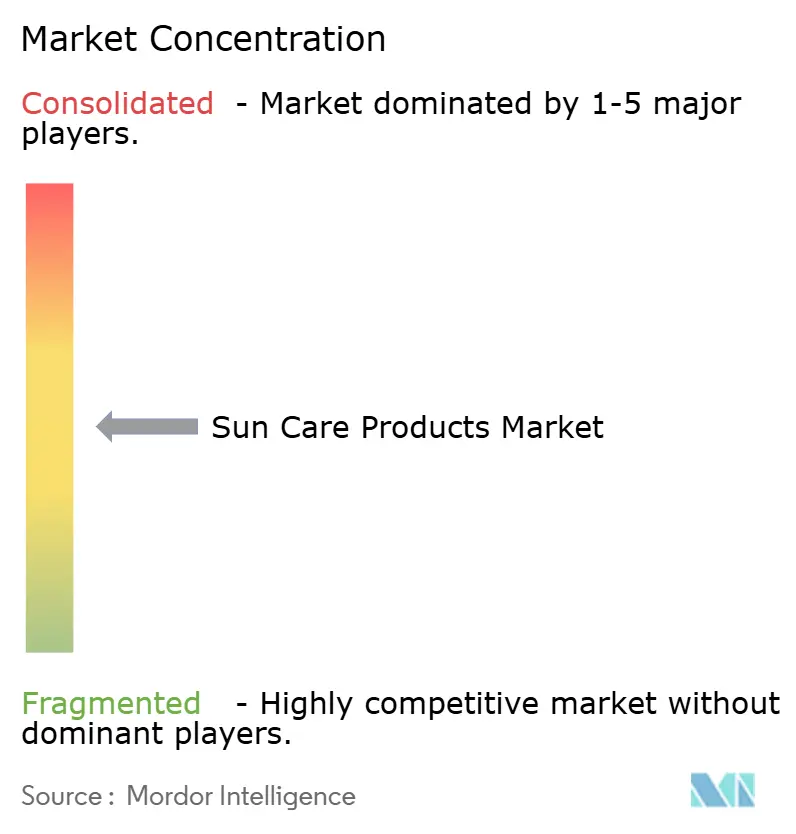

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sun Care Products Market Analysis by Mordor Intelligence

The sun care products market size was valued at USD 17.60 billion in 2025 and estimated to grow from USD 19.30 billion in 2026 to reach USD 30.60 billion by 2031, at a CAGR of 9.66% during the forecast period (2026-2031). This acceleration reflects a confluence of public health imperatives and evolving consumer preferences that extend well beyond traditional sunburn prevention. Melanoma incidence climbed to approximately 331,700 new cases globally in 2022, with 267,000 of those directly attributable to ultraviolet radiation exposure, according to the National Cancer Institute. That epidemiological burden translates into heightened regulatory scrutiny and consumer demand for products that deliver verified broad-spectrum protection, creating a structural tailwind for manufacturers able to navigate ingredient approvals and substantiate efficacy claims. Asia-Pacific is becoming the growth epicenter, driven by rising disposable incomes and accelerating omnichannel retail, while reef-safe legislation is steering R&D toward mineral and hybrid filters. Digital-first challengers leverage influencer marketing to rapidly gain awareness, yet established multinationals still dominate through patent portfolios, dermatology endorsements, and scaled distribution.

Key Report Takeaways

- By product type, sun protection products held 79.32% of the sun care products market share in 2025, while after-sun products are expected to advance at a 9.89% CAGR through 2031.

- By category, conventional formulations accounted for 70.03% of revenue in 2025; organic/natural alternatives are forecast to expand at a 10.47% CAGR to 2031.

- By price, mass offerings represented 68.04% of sales in 2025, whereas premium lines are growing at a 10.84% CAGR on the strength of dermatologist endorsements.

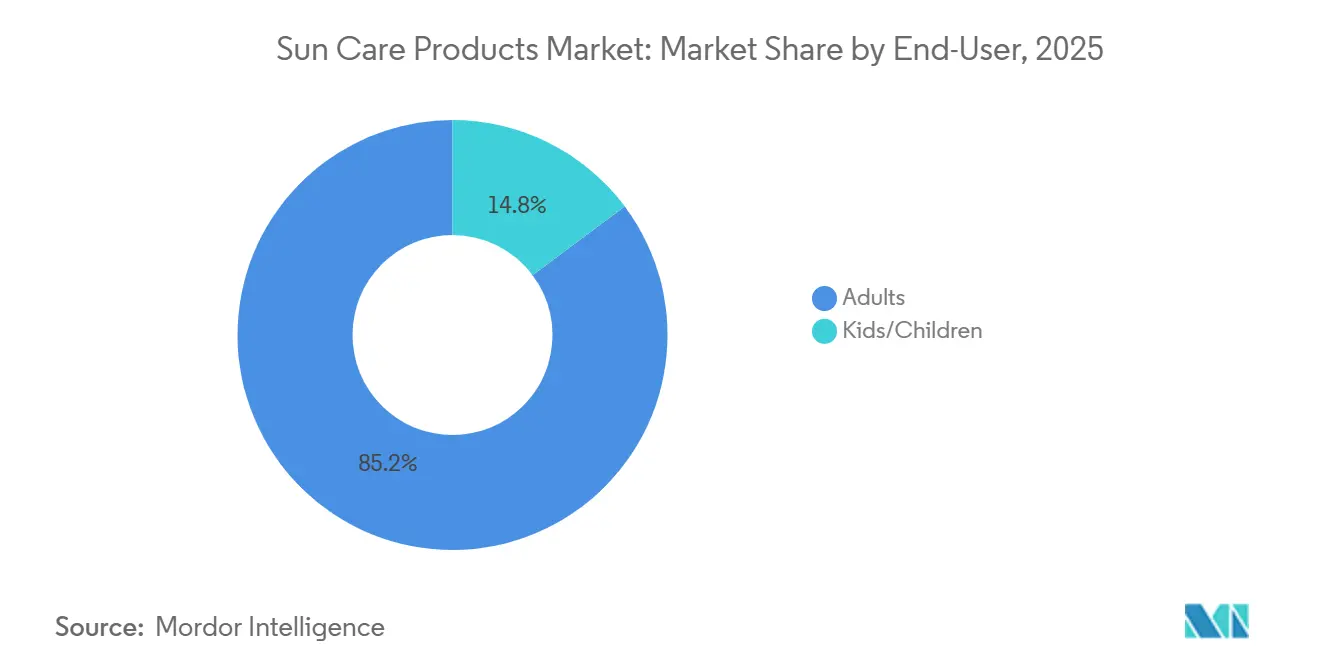

- By end-user, adults contributed 85.21% of the 2025 turnover; however, the kids/children lines are projected to rise at a 10.42% CAGR through 2031.

- By distribution channel, specialty stores led with 33.66% share in 2025, while online retail stores are pacing at an 11.44% CAGR as direct-to-consumer models scale.

- By geography, North America led with a 33.12% share in 2025, while the Asia-Pacific region is pacing at an 11.21% CAGR as direct-to-consumer models scale.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sun Care Products Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Skin Cancer and UV Awareness | +2.1% | Global, with highest impact in North America and Australia | Medium term (2-4 years) |

| Growing Popularity of Outdoor Recreational Activities | +1.8% | Global, particularly strong in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Preference for Natural and Organic Products | +1.4% | North America and Europe leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Product Innovation and Diversification | +1.6% | Global, with innovation hubs in North America, Europe and Japan | Medium term (2-4 years) |

| Influence of Social Media and Celebrity Endorsements | +1.2% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Growing Adoption of Baby Personal Care Products | +0.9% | Global, with premium adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Skin Cancer and UV Awareness

Consumer awareness about skin cancers and the irreversible effects of UV rays on the skin is rising, driving demand for sun care products worldwide. According to Melanoma Foundation data from 2023, 186,680 melanoma cases were diagnosed in the United States[1]Source: AIM at Melanoma Foundation, "Number of Melanoma Incidences in 2023", aimatmelanoma.org. The shift toward prevention-focused healthcare spending amplifies the sun care market growth, particularly in aging populations where skin cancer prevention becomes economically advantageous compared to treatment costs. Regulatory bodies such as the FDA and European Medicines Agency are tightening efficacy standards, requiring in vivo testing for broad-spectrum claims and water-resistance labeling, which raises barriers to entry but also legitimizes premium pricing for compliant brands. This dynamic favors incumbents with established clinical pipelines and creates acquisition opportunities for smaller innovators holding novel UV filter patents.

Growing Popularity of Outdoor Recreational Activities

The past few years have seen an increase in participation in sports, especially in outdoor games. According to the Sports England data from 2024, 7,169,700 people in England participated in cycling [2]Source: Outdoor Foundation, "Number of hiking participants in the United States", outdoorindustry.org. Additionally, recreational activities such as hiking, camping, and others are also growing among the young population. Due to this, the demand for sun protection products like sunscreens, moisturizers, and others is increasing across the world. According to the Outdoor Foundation data from 2024, the number of hiking participants in the United States was 63.43 million 2024 [3]Source: Sports England, "Number of people participating in cycling in England", sportengland.org. Additionally, as a result of their light-colored skin and reduced melanin production (melanin absorbs sunlight before it damages the skin cell's DNA), Western consumers prefer to use sun care products when they are outside, especially on beaches. Those with light-colored skin are more likely to suffer damage from sunlight. Hence, the higher participation rate of Western individuals in outdoor recreational activities contributed to the rise in sales of sun care products.

Preference for Natural and Organic Products

COSMOS-certified sunscreens, which adhere to strict sourcing and processing standards for organic cosmetics, are gaining shelf space in specialty retailers and online platforms. The COSMOS standard version 4.2, updated in 2024, permits titanium dioxide and zinc oxide as UV filters but imposes particle-size restrictions to minimize nano-material concern. European Union Regulation 2018/848 governs organic agricultural ingredients, creating a compliance framework that differentiates certified products from greenwashed alternatives. Consumer willingness to pay a premium for clean-label formulations is most pronounced in North America and Western Europe, where environmental consciousness intersects with health anxiety around synthetic chemicals. Brands such as Naos (Bioderma) and Clarins are leveraging this trend by highlighting botanical extracts and biodegradable packaging, while mass-market players like Beiersdorf are reformulating flagship lines to meet natural certification thresholds. The challenge lies in maintaining sensory appeal; many mineral-based formulas leave a white cast, prompting R&D investment in micronized particles and tinted variants that address aesthetic objections without compromising efficacy.

Product Innovation and Diversification

The FDA's December 2025 proposal to add bemotrizinol to the over-the-counter monograph represents a watershed moment for UV filter innovation in the United States, potentially unlocking formulations that combine high SPF with lightweight textures. Bemotrizinol, already approved in Europe and Asia, absorbs both UVA and UVB radiation and exhibits photostability superior to older chemical filters. This regulatory shift will enable U.S. brands to compete on sensory attributes with European counterparts, addressing a long-standing consumer complaint about greasy residues. Concurrently, manufacturers are exploring hybrid products, moisturizers with SPF 50, and foundations with broad-spectrum protection that simplify morning routines and appeal to time-constrained professionals. Blue-light protection claims are proliferating, though clinical evidence remains mixed; the American Academy of Dermatology has not issued formal guidance on high-energy visible light, creating a gray area that savvy marketers exploit while awaiting definitive research. Patent filings for encapsulated UV filters, which release protection gradually to extend wear time, are accelerating, signaling that the next competitive frontier will be duration of efficacy rather than peak SPF values.

Restraints Impact Analysis*

| Restraints | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Concerns over Chemical Ingredients | -1.3% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Stringent and Varying Sunscreen Regulations Across Regions | -1.1% | Global, with highest friction in cross-border markets | Long term (≥ 4 years) |

| Availability of Counterfeit Products | -0.8% | Asia-Pacific, Middle East, Latin America, with spillover to e-commerce globally | Short term (≤ 2 years) |

| Fluctuation in Raw Material Prices | -0.7% | Global, with highest impact on mass-market brands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety Concerns over Chemical Ingredients

Oxybenzone and octinoxate, two widely used chemical UV filters, have faced mounting scrutiny over potential endocrine disruption and coral reef toxicity. Hawaii enacted legislation in 2018 banning these ingredients effective January 2021, followed by similar measures in Palau and the U.S. Virgin Islands. The FDA's ongoing review of sunscreen active ingredients has placed 12 chemical filters in a "needs more data" category, leaving only zinc oxide and titanium dioxide with confirmed GRASE (Generally Recognized as Safe and Effective) status. This regulatory uncertainty has prompted reformulation efforts, with brands pivoting toward mineral-based alternatives or seeking approval for newer filters like bemotrizinol. Consumer advocacy groups amplify these concerns through social media campaigns, creating reputational risk for companies perceived as slow to adapt. The challenge is balancing safety perceptions with sensory performance, as mineral sunscreens often leave a white residue that discourages consistent use, potentially undermining public health goals.

Stringent and Varying Sunscreen Regulations Across Regions

The FDA regulates sunscreens as over-the-counter drugs under 21 CFR Part 352, requiring extensive clinical testing for SPF and broad-spectrum claims, while the European Union treats them as cosmetics under Regulation (EC) No 1223/2009, allowing faster approval for new filters. This divergence forces multinational brands to maintain separate formulations and labeling for different markets, inflating compliance costs and delaying global launches. Japan's Ministry of Health, Labour and Welfare imposes additional requirements for quasi-drug classification, while China's National Medical Products Administration mandates animal testing for imported cosmetics, complicating entry for cruelty-free brands. The lack of harmonization also creates arbitrage opportunities for gray-market distributors, who exploit price differentials by importing products across borders without proper regulatory clearance. Industry associations such as the Personal Care Products Council are lobbying for mutual recognition agreements, but progress remains slow amid divergent public health priorities and political sensitivities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Prevention Dominates, Recovery Accelerates

Sun protection products captured 79.32% of market share in 2025, reflecting entrenched consumer habits around daily SPF application and beach-season stockpiling. This segment benefits from regulatory clarity: FDA and EU standards provide well-defined testing protocols for SPF and broad-spectrum claims, and from cross-category expansion, as moisturizers, foundations, and lip balms increasingly incorporate UV filters. However, after-sun products are growing at a 9.89% CAGR through 2031, driven by heightened awareness of post-exposure skin repair and the proliferation of aloe vera-infused gels and cooling lotions that address redness and peeling.

The shift toward multifunctional products is reshaping this segmentation. L'Oréal's La Roche-Posay line, for instance, combines SPF 50 with antioxidants and anti-aging peptides, blurring the boundary between sun protection and skincare treatment. This convergence appeals to consumers who prioritize efficiency and are willing to pay premium prices for products that deliver multiple benefits in a single application. Regulatory bodies have yet to issue comprehensive guidance on hybrid claims, creating a gray area that innovative brands exploit while awaiting formal standards.

By Category: Conventional Leads, Organic Gains Momentum

Conventional formulations held a 70.03% share in 2025, anchored by mass-market brands that leverage economies of scale and established distribution networks. These products typically rely on chemical UV filters such as avobenzone and octocrylene, which offer lightweight textures and high SPF values at accessible price points. However, Organic/Natural products are expanding at a 10.47% CAGR through 2031, propelled by COSMOS certification uptake and consumer demand for clean-label ingredients. Brands such as Naos (Bioderma) and Clarins are investing in botanical extracts, green tea, chamomile, and vitamin E, which provide antioxidant benefits alongside UV protection, differentiating their offerings in crowded premium channels.

The challenge for organic players is overcoming sensory objections. Mineral-based sunscreens often leave a white cast and feel heavier on the skin, discouraging repeat use among consumers accustomed to invisible chemical formulas. Manufacturers are addressing this through micronization and tinting, creating products that blend seamlessly with diverse skin tones. Retailers are supporting the shift by dedicating shelf space to certified organic lines and training staff to educate shoppers on ingredient benefits, though price premiums, often 30-50% above conventional equivalents, remain a barrier for price-sensitive segments.

By Price: Mass Accessibility, Premium Aspiration

Mass-market products commanded 68.04% share in 2025, reflecting widespread availability in supermarkets, hypermarkets, and drugstores, where brands like Neutrogena, Coppertone, and Banana Boat compete on price and promotional intensity. These offerings prioritize affordability and functional efficacy, with SPF 30 and SPF 50 variants dominating shelf space. However, premium products are growing at 10.84% CAGR through 2031, driven by dermatologist endorsements, luxury packaging, and claims around anti-aging and skin-brightening benefits. Brands such as La Roche-Posay, Supergoop!, and EltaMD (Colgate-Palmolive) position themselves as science-backed solutions for discerning consumers, often selling through specialty retailers, dermatology clinics, and direct-to-consumer channels that allow for higher margins and brand storytelling.

The premium segment is also benefiting from the rise of "skinimalism", the trend toward streamlined routines with fewer, higher-quality products. Consumers are consolidating their morning regimens, opting for a single high-performance sunscreen over multiple layered products. This shift favors brands that invest in clinical trials, publish peer-reviewed research, and secure endorsements from medical professionals. The challenge is maintaining exclusivity while scaling distribution; as premium brands expand into mass channels to capture growth, they risk diluting brand equity and alienating core customers who value scarcity and prestige.

By End-User: Adults Anchor, Kids Surge

Adults accounted for 85.21% of end-user revenue in 2025, reflecting both demographic scale and established purchasing habits. This segment spans a wide age range, from millennials integrating SPF into daily skincare to older adults seeking anti-aging formulations with UV protection, and supports diverse product formats, including lotions, sprays, sticks, and powders. However, kids/children products are projected to grow at a 10.42% CAGR through 2031, spurred by updated pediatric dermatology guidelines that recommend sunscreen application for infants as young as 6 months, according to the American Academy of Pediatrics. This expanded age range has unlocked a high-margin segment characterized by repeat purchase and brand loyalty, as parents gravitate toward hypoallergenic, fragrance-free formulations endorsed by paediatricians.

Brands are tailoring products to address parental concerns around safety and ease of use. Mineral-based formulas dominate the kids' segment, as titanium dioxide and zinc oxide are perceived as gentler than chemical filters. Packaging innovations, such as roll-on applicators and color-changing lotions that turn clear when fully rubbed in, simplify application and engage children in the sun protection routine. Retailers are bundling kids' sunscreen with beach toys and swimwear, embedding UV protection into the broader family vacation ecosystem. In Asia-Pacific markets, rising birth rates among urban middle-class families are fuelling demand for premium baby sun care, with brands like Shiseido and Kao Corporation launching dedicated lines that emphasize gentle mineral filters and tear-free formulas.

By Distribution Channel: Online Retail Transforms Traditional Commerce

Specialty stores led distribution with a 33.66% share in 2025, benefiting from knowledgeable staff, curated assortments, and the ability to offer product trials and personalized recommendations. Chains such as Sephora, Ulta Beauty, and independent pharmacies provide an environment where consumers can explore premium and niche brands, ask questions about ingredient safety, and receive guidance on SPF selection based on skin type and activity level. However, Online Retail Stores are surging at 11.44% CAGR through 2031, driven by direct-to-consumer brands, subscription models, and the convenience of home delivery. E-commerce platforms enable brands to bypass traditional retail markups, invest savings in digital marketing, and gather first-party data on consumer preferences, creating a virtuous cycle of personalization and loyalty.

Supermarkets/hypermarkets and other distribution channels (including convenience stores and gas stations) serve the mass market, prioritizing accessibility and promotional pricing. These channels are critical for seasonal spikes, Memorial Day, Fourth of July, and Labor Day in the United States, when sunscreen purchases surge. Brands are optimizing packaging for impulse buys, offering travel-size formats and multi-packs that appeal to families stocking up for vacations. The challenge for brick-and-mortar retailers is competing with online convenience and price transparency; many are responding by integrating omnichannel strategies, such as buy-online-pick-up-in-store and same-day delivery, to retain foot traffic and capture last-minute purchases.

Geography Analysis

North America held 33.12% of the market share in 2025, underpinned by mature consumer awareness, stringent FDA regulations, and a well-established retail infrastructure spanning supermarkets, specialty stores, and e-commerce platforms. The region's dominance reflects decades of public health campaigns by the CDC and American Academy of Dermatology, which have normalized daily SPF application and positioned sunscreen as a non-negotiable component of skincare routines. However, growth is moderating as penetration rates approach saturation, with incremental gains now tied to premiumization, consumers trading up to higher-SPF formulations, anti-aging hybrids, and dermatologist-endorsed brands. Canada and Mexico contribute to regional growth, with Mexico's beach tourism sector driving seasonal demand and Canada's focus on outdoor recreation supporting year-round sales.

Asia-Pacific is expanding at 11.21% CAGR through 2031, the fastest rate among all geographies, fuelled by rising disposable incomes, urbanization-linked pollution concerns, and aggressive digital marketing by multinational brands. China, India, Japan, South Korea, and Southeast Asian markets are experiencing a cultural shift toward preventive skincare, with UV protection increasingly viewed as essential for maintaining fair complexions and preventing premature aging. K-beauty trends, lightweight essences, cushion compacts with SPF, and multi-step routines are normalizing daily sunscreen use among younger demographics, while e-commerce platforms such as Tmall and JD.com provide direct access to international brands. Regulatory frameworks vary widely: Japan's Ministry of Health, Labour and Welfare classifies high-SPF sunscreens as quasi-drugs, requiring additional testing, while China's National Medical Products Administration mandates animal testing for imported cosmetics, complicating entry for cruelty-free brands. Local players such as Shiseido (Japan) and Kao Corporation (Japan) leverage deep distribution networks and cultural insights to compete with Western multinationals, often launching region-specific formulations that address humidity, pollution, and skin-tone preferences.

Europe captured a significant share in 2025, supported by the stringent EU Cosmetics Regulation (EC) No 1223/2009, which treats sunscreens as cosmetics and allows faster approval for new UV filters compared to the FDA's drug classification. This regulatory environment has enabled European brands such as Beiersdorf (Nivea), L'Oréal (La Roche-Posay), and Clarins to lead in formulation innovation, incorporating photostable filters like bemotrizinol and tinosorb that deliver broad-spectrum protection without the white cast associated with mineral sunscreens. Sustainability mandates are reshaping the competitive landscape: the EU's Single-Use Plastics Directive and Green Deal are pushing brands to adopt refillable packaging and biodegradable formulations, creating differentiation opportunities for eco-conscious players. Southern European markets, Spain, Italy, and Greece, drive seasonal demand tied to beach tourism, while Northern Europe exhibits year-round usage linked to outdoor sports and wellness trends. South America and the Middle East & Africa are smaller but growing, with Brazil's beach culture and the GCC's intense sun exposure creating pockets of high per-capita consumption.

Competitive Landscape

The sun care products market maintains a moderate consolidation, allowing both multinational corporations and specialized companies to compete through distinct positioning strategies. Major players in the market include Beiersdorf AG, Shiseido Company, Limited, L'Oréal S.A., Edgewell Personal Care, and Unilever PLC. Market leaders maintain competitive advantages through their global distribution networks, regulatory expertise, and research and development capabilities. Emerging brands target niche segments through direct-to-consumer channels and specialized formulations. The market structure enables diverse business models and encourages innovation across different price points and consumer segments.

Companies differentiate themselves through technology integration, including smart beauty devices, AI-powered formulation optimization, and personalized skincare solutions. These technological advancements enhance consumer engagement and create stronger brand relationships. The integration of digital solutions enables companies to gather consumer insights and develop targeted products. Technology investments also help companies streamline their operations and improve product development processes.

Significant opportunities exist in underserved segments, such as men's suncare, children's specialized formulations, and emerging markets with low penetration rates. Companies with strong regulatory expertise hold advantages in markets with complex approval processes, particularly in regions with stringent safety standards. Environmental sustainability has become a crucial factor in consumer decision-making and brand loyalty. The growing awareness of sun protection in developing markets presents expansion opportunities for both established and new players.

Sun Care Products Industry Leaders

-

Beiersdorf AG

-

Shiseido Company, Limited

-

L'Oréal S.A.

-

Edgewell Personal Care

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ultra Violette, an Australian brand, launched its new Future Sunscreen products in the United States. The sunscreen is rich in SPF 50. The company's products are available on Sephora stores in the United States.

- February 2025: Deconstruct, a skincare brand focused on scientific formulations, launched its sun protection range through a partnership with Nykaa. The collection includes three formulations for face, body, and hair protection, featuring sun protection technology and lightweight ingredients.

- September 2024: Garnier entered the suncare category by introducing its UV Invisible Serum Sunscreen. The company's new product features a lightweight formula that provides comprehensive broad-spectrum protection with SPF50 and PA++++ ratings. The sunscreen's advanced formulation is designed to protect the skin from 99% of sun damage, offering users significant protection against harmful UV rays.

- June 2024: FRÉ, a US-based clean skincare brand, has launched its suncare and skincare products in India through Shoppers Stop. The brand's formulations focus on protecting, repairing, and enhancing the skin of active women.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the sun-care products market as retail sales of creams, lotions, sticks, sprays, and gels whose primary label claim is protection, repair, or enhancement of skin exposed to ultraviolet radiation. This includes SPF-rated sunscreens, after-sun soothers, and self-tanning formulations that carry on-pack sun-related benefits.

Scope exclusions: devices (e.g. UV meters), ingestible supplements, and tanning beds fall outside this assessment.

Segmentation Overview

-

Product Type

- Sun Protection Products

- After-sun Products

- Self-tanning Products

-

Category

- Conventional

- Organic/Natural

-

Price Range

- Mass

- Premium

-

End-User

- Adults

- Kids/Children

-

Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Others Distribution Channel

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We conducted interviews with dermatologists, contract manufacturers, retail buyers, and regulatory officers across North America, Europe, and Asia Pacific. Their inputs helped us validate average selling prices, typical reorder cycles, and ingredient-cost pass-throughs, closing gaps left by public statistics.

Desk Research

Analysts first mapped volumes and price bands from open sources such as the US FDA sunscreen monograph log, Eurostat Prodcom codes for sun-preparation outputs, UN Comtrade HS-3304 export flows, Japanese Cosmetic Industry Association shipment surveys, and peer-reviewed dermatology journals that track SPF adoption rates. Company 10-Ks, retailer scanner data snapshots, and reputable business press provided channel margin and seasonality clues. Paid datasets like D&B Hoovers (brand financial splits) and Dow Jones Factiva (news frequency on new SPF launches) supplied additional signals. The sources cited illustrate our desk work; many more were consulted to corroborate facts and clarify definitions.

Market-Sizing & Forecasting

Mordor Intelligence applies a single top-down demand pool build, beginning with household skin-care expenditures and isolating the sun-care share through penetration and usage-rate datasets, which are then cross-checked with selective bottom-up roll-ups of leading supplier shipments. Key variables include SPF mix shifts, consumer outdoor leisure hours, dermatology visit rates, reef-safe regulation timelines, and online channel share. Forecasts rest on multivariate regression with error-corrected ARIMA overlays; coefficient ranges are stress-tested with scenario opinions gathered in primary research. Where bottom-up estimates showed data gaps, price-elasticity bands were used to normalize totals to the validated demand pool.

Data Validation & Update Cycle

Outputs pass a three-layer review: algorithmic variance scans, senior analyst sign-off, and quarterly peer audit. Models are refreshed annually, with interim updates triggered by material events such as regulatory SPF caps or large M&A moves, ensuring clients receive the latest view.

Why Mordor's Sun Care Products Baseline Commands Reliability

Published values often diverge because firms choose different product mixes, price assumptions, and refresh cadences. By anchoring on clear scope and openly published skin-care spending benchmarks, our baseline remains both transparent and reproducible for decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.67 bn (2025) | Mordor Intelligence | - |

| USD 12.44 bn (2024) | Global Consultancy A | Excludes self-tanning lines; relies on static EU price averages |

| USD 14.90 bn (2024) | Industry Association B | Uses conservative SPF-30 cap and 2023 exchange rates; update cycle biennial |

In short, our disciplined scope selection, yearly refresh, and dual-track validation let us deliver a balanced, decision-ready baseline while other figures swing on narrower definitions or slower updates.

Key Questions Answered in the Report

How fast is demand growing for premium SPF lotions?

Premium sales are expanding at a 10.84% CAGR through 2031 as consumers trade up for dermatologist-endorsed, multifunctional formulas.

Which region contributes the highest growth to sun protection sales?

Asia-Pacific leads with an 11.21% CAGR, propelled by rising incomes, pollution concerns, and digital retail penetration.

What regulatory change could reshape U.S. sunscreen formulations?

The FDA plans to approve bemotrizinol in 2026, allowing brands to launch lighter, more photostable products that match European standards.

Why are mineral sunscreens gaining momentum?

Reef-safe laws and safety debates around chemical filters drive consumers toward zinc oxide and titanium dioxide options, especially in Hawaii and Palau.

Page last updated on: