Organic Skin Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 49.74 Billion |

| Market Size (2031) | USD 61.92 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

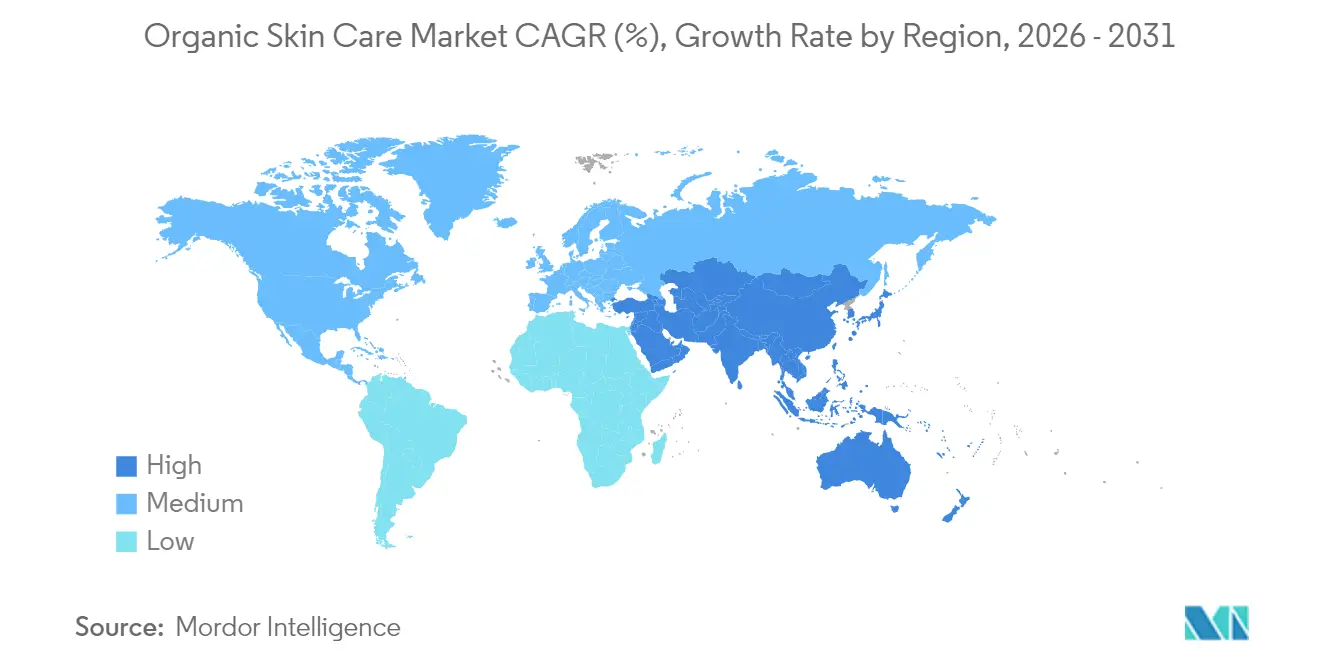

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Skin Care Market Analysis by Mordor Intelligence

The organic skin care market is projected to grow from USD 47.51 billion in 2025 to USD 49.74 billion in 2026, eventually reaching USD 61.92 billion by 2031, marking a CAGR of 4.48% from 2026 to 2031. Once the domain of synthetic cosmetics, clinical-grade performance now embraces innovations like exosome serum delivery systems and microbiome-targeted actives, offering tangible benefits such as wrinkle reduction and barrier repair. In 2024, L’Oréal highlighted a significant shift, with biobased raw materials accounting for 66% of its total feedstock, underscoring the feasibility of large-scale natural sourcing for multinationals without compromising margins. The Asia-Pacific region, holding a 40.43% revenue share in 2025, is further solidifying its lead, driven by China's stringent ingredient-transparency regulations and Japan's rising demand for anti-aging botanicals, especially among adults aged 65 and older. While shelf-life limitations have nudged distribution towards online and health and beauty channels, advancements in biotechnology hint at extended stability windows by decade's end.

Key Report Takeaways

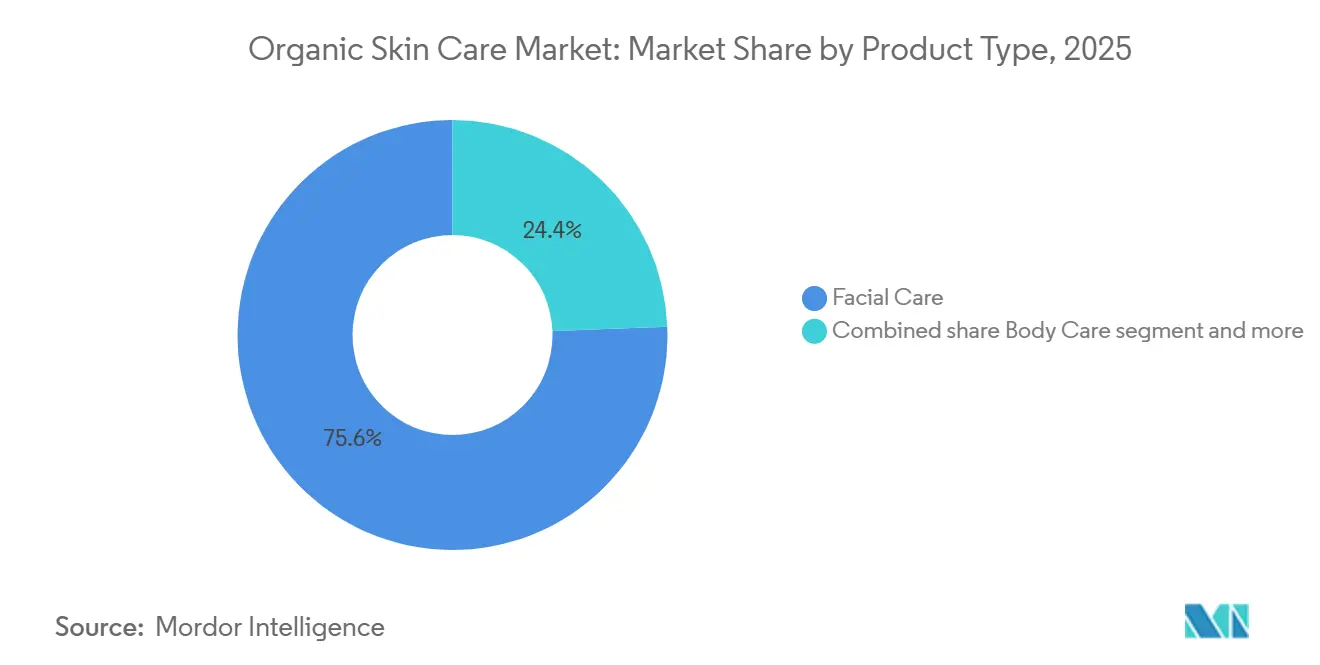

- By product type, facial care captured 75.62% of the 2025 value, while body care is advancing at a 5.92% CAGR to 2031.

- By Category, mass-market lines held 64.74% of 2025 sales, but premium offerings are expanding at a 6.11% CAGR over the same horizon.

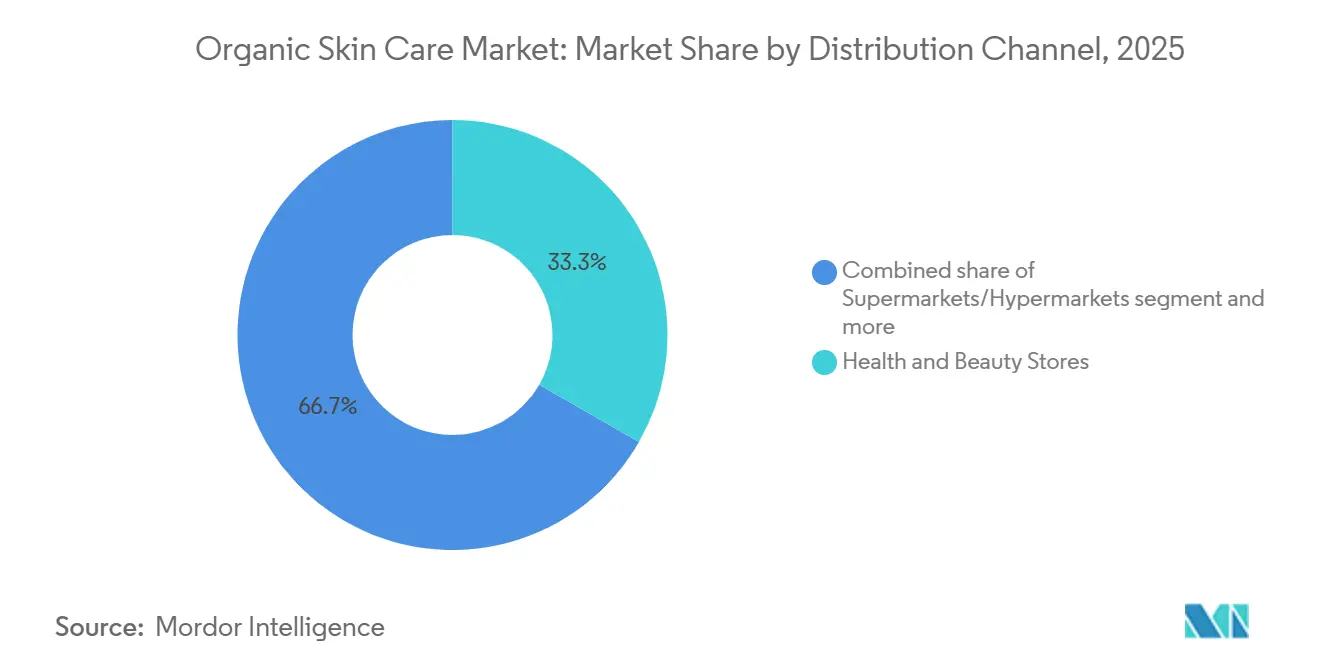

- By distribution channel, health and beauty stores accounted for 33.62% of 2025 distribution, whereas online retail is projected to grow at a 6.02% CAGR through 2031.

- By geography, Asia-Pacific led with 40.43% global share in 2025; it also posts the fastest regional CAGR at 6.22% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Skin Care Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inclination towards clean-label products | +0.8% | Global, with the strongest uptake in North America and Europe | Medium term (2-4 years) |

| Technological innovations in product formulations | +0.7% | Global, led by the Asia-Pacific innovation hubs and North America research and development centers | Short term (≤ 2 years) |

| Growing concerns over the effects of synthetic products on the body | +0.6% | Global, particularly Europe and North America | Medium term (2-4 years) |

| Awareness of vegan and cruelty-free beauty products | +0.5% | Europe and North America core, expanding to the Asia-Pacific urban centers | Medium term (2-4 years) |

| Expansion of organic farming practices reduces the cost of raw materials | +0.4% | Global, with early gains in South America and Southeast Asia | Long term (≥ 4 years) |

| Increasing focus on anti-aging solutions using natural ingredients | +0.5% | The Asia-Pacific (aging demographics) and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inclination towards clean label products

Consumer demand for ingredient transparency has escalated from niche preference to mainstream expectation, compelling brands to reformulate legacy SKUs or risk obsolescence. The USDA National Organic Program (NOP) reported a 12% year-on-year increase in certified organic personal-care product registrations in 2024, reflecting heightened scrutiny of synthetic additives[1]Source: USDA, “National Organic Program Annual Summary 2024,” usda.gov. Clean-label positioning extends beyond ingredient exclusion; it now encompasses supply-chain traceability, with L'Oréal achieving 92% traceability for botanical raw materials by end-2024, a metric the company ties directly to consumer trust scores in its annual sustainability report. Estee Lauder's Nutritious line, launched with 92% naturally derived content and EWG Verified status, illustrates how legacy prestige brands are adopting third-party certifications to compete with indie clean-beauty disruptors. Pregnancy-safe skincare formulations, free from retinoids, salicylic acid, and phthalates, are emerging as a high-growth sub-segment, with brands like Pai Skincare and Weleda capturing share by explicitly addressing maternal safety concerns that mainstream lines historically overlooked. This driver is amplifying online retail's 6.02% CAGR, as e-commerce platforms enable granular ingredient filtering that brick-and-mortar cannot replicate at scale.

Technological innovations in product formulations

Biotechnology convergence is enabling organic brands to deliver clinical-grade efficacy without synthetic actives, fundamentally altering the performance-versus-purity trade-off. Exosome serum technology, utilizing extracellular vesicles derived from plant stem cells or biofermentation, has progressed from the experimental to the commercial stage, with peer-reviewed studies in the Journal of Cosmetic Dermatology demonstrating collagen synthesis rates comparable to those of prescription retinoids. Microbiome skincare formulations incorporating live probiotics, prebiotics, and postbiotics are gaining traction; research published in Frontiers in Microbiology in 2024 showed that topical Lactobacillus strains reduced transepidermal water loss by 23% over 8 weeks, validating the mechanism for barrier repair. Shiseido allocated JPY 15 billion (USD 100 million) to biotechnology research and development in fiscal 2024, focusing on precision fermentation to produce peptides and ceramides without animal or petrochemical inputs. Green chemistry methodologies, such as supercritical CO₂ extraction, are replacing hexane-based processes, yielding higher-purity botanical extracts while satisfying Cosmos and Ecocert solvent restrictions. These innovations are propelling the premium segment's 6.11% CAGR, as consumers willingly pay a 30-50% price premium for demonstrable clinical outcomes anchored in natural ingredients.

Growing concerns over the effects of synthetic products on the body

Regulatory and academic scrutiny of endocrine-disrupting chemicals (EDCs) in cosmetics has intensified, catalyzing consumer migration toward certified organic alternatives. The European Commission's 2024 update to Annex II of the Cosmetics Regulation added 12 synthetic UV filters and preservatives to the banned-substances list, citing reproductive toxicity data from multi-year cohort studies[2]Source: European Commission, “Cosmetics Regulation Annex II Update 2024,” ec.europa.eu . In parallel, the FDA's MoCRA framework mandates adverse-event reporting, creating a public database that amplifies safety concerns around synthetic ingredients and indirectly benefits organic brands that can claim cleaner safety profiles. Pregnancy safe skincare searches surged 47% year-over-year on Google in 2025, per the company's trend data, as expectant mothers proactively avoid parabens, phthalates, and synthetic fragrances linked to developmental risks in preclinical studies. Japan's Ministry of Health, Labour and Welfare tightened labeling requirements for "quasi-drugs" (medicated cosmetics) in 2024, mandating disclosure of all synthetic actives above 0.01% concentration, a move that favors botanical formulations with simpler ingredient decks. This regulatory tightening is accelerating facial care's dominance, 75.62% of 2025 sales, since facial skin exhibits higher absorption rates and thus greater EDC exposure risk compared to body applications.

Awareness of vegan and cruelty-free beauty products

Ethical consumerism has matured from values signaling to a purchase determinant, particularly among Gen Z and Millennial cohorts that represent a majority of organic skincare buyers in North America and Europe. Leaping Bunny certification, administered by Cruelty Free International, reported a 34% increase in cosmetic brand applications in 2024, with organic brands disproportionately represented due to alignment between animal welfare and natural positioning[3]Source: Cruelty Free International, “Leaping Bunny Annual Report 2024,” crueltyfreeinternational.org . The European Union's 2024 enforcement sweep identified 18 brands falsely claiming cruelty-free status, resulting in EUR 4.2 million in fines and heightened consumer skepticism toward unverified claims. Additionally, China's 2024 regulatory reforms eliminated mandatory animal testing for imported "general" cosmetics, unlocking a USD 8 billion market for certified vegan brands that previously faced de facto exclusion. For instance, L'Oréal's China revenue grew 11% in 2024, partly attributable to its cruelty-free portfolio expansion. Vegan formulations inherently avoid lanolin, beeswax, and carmine, common allergens, thus appealing to consumers with self-reported sensitive skin. This driver is particularly potent in the premium segment (6.11% CAGR), where brands can command higher margins by bundling ethical certifications with clinical efficacy narratives.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory gaps fuel the growth of uncertified organic and natural products | -0.6% | Global, acute in South America, the Middle East and Africa, and Southeast Asia | Medium term (2-4 years) |

| Shorter shelf-life limiting mass-retail listings | -0.5% | Global, most constraining in North America and Europe, mass retail | Short term (≤ 2 years) |

| Limited availability of organic ingredient suppliers creates potential supply bottlenecks | -0.4% | Global, with acute pressure in the Asia-Pacific and Europe | Medium term (2-4 years) |

| Lower product stability and formulation variations | -0.3% | Global, particularly affecting mass-market scaling | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory gaps fuel the growth of uncertified organic and natural products

Fragmented certification frameworks and lax enforcement in emerging markets enable "greenwashing," diluting the value proposition of genuinely certified organic brands. Unlike food, cosmetics face no harmonized global organic standard; USDA NOP, Cosmos, Ecocert, and NSF/ANSI 305 each impose distinct thresholds for organic content (ranging from 70% to 95%), creating consumer confusion and enabling opportunistic brands to self-declare "natural" status without third-party verification, according to the U.S. Department of Agriculture. A 2024 audit by the European Commission found that 22% of "organic" cosmetics sampled in online marketplaces failed to meet Cosmos minimum standards, yet faced no penalties due to jurisdictional gaps in e-commerce oversight. Similarly, in India, the absence of a dedicated organic cosmetics regulation allows brands to use "natural" and "organic" interchangeably, undermining premium pricing for certified products. For instance, Nykaa's acquisition of Earth Rhythm in 2024 was partly motivated by the need to consolidate fragmented indie brands under a credible certification umbrella. This restraint disproportionately impacts the mass segment, where price-sensitive consumers lack the expertise to differentiate certified from pseudo-organic offerings, eroding trust and slowing category expansion in price-competitive channels.

Shorter shelf-life limiting mass-retail listings

Natural preservatives, such as tocopherol, rosemary extract, and radish root ferment, offer 12-18 months of stability under controlled conditions, compared to 36+ months for synthetic parabens and phenoxyethanol, creating inventory risk for mass retailers operating on thin margins. Supermarkets and hypermarkets, historically the largest distribution channel, are reducing organic SKU counts by 15-20% according to category management data, favoring hybrid "natural-plus" formulations that incorporate minimal synthetic preservatives to extend shelf-life while retaining clean-label appeal. This dynamic is accelerating online retail's 6.02% CAGR, as direct-to-consumer models enable just-in-time production and cold-chain logistics that mitigate spoilage risk. For instance, Hain Celestial's 62% SKU reduction in personal care during fiscal 2024, including exits from slower-turning organic lines, exemplifies how even dedicated natural-products companies are rationalizing portfolios in response to shelf-life economics. Furthermore, biotechnology offers a potential solution: precision-fermented antimicrobial peptides are entering commercial trials, promising 24+ month stability without synthetic preservatives, though regulatory approval timelines extend to 2027-2028.

Segment Analysis

By Product Type: Facial Care Dominance Masks Body Care Velocity

In 2025, facial care products dominated the market, capturing 75.62% of the total value. This trend highlights consumers' focus on facial skin health and the premium pricing of these products. However, the body care segment is growing fastest, with a 5.92% CAGR through 2031, as clean-label preferences expand beyond facial applications. The facial segment's lead stems from higher active ingredient concentrations and stringent clinical validation. For example, premium exosome serum formulations are priced at USD 80-150 for 30ml, compared to USD 20-40 for body lotions with similar organic certifications. Estee Lauder's Nutritious line, featuring 92% naturally derived serums with EWG Verified status, exemplifies the industry's shift toward green chemistry. Microbiome skincare innovations, using Lactobacillus and Bifidobacterium strains, primarily target facial applications due to the face's microbial diversity and consumers' willingness to try new technologies on visible skin.

Body care's 5.92% CAGR growth surpasses facial care, driven by three factors: lower price points attracting mass-market consumers (64.74% of 2025 sales), simpler formulations reducing stability challenges, and growth in pregnancy-safe skincare sub-segments. Products like stretch mark creams and belly oils address unmet maternal needs. Body lotions and washes dominate revenue, with organic body wash demand rising as consumers seek sulfate-free alternatives to synthetic surfactants linked to skin barrier issues. Lip care, the smallest segment, benefits from frequent repurchase cycles, 4-6 times annually, versus 2-3 for facial serums, and regulatory changes. The FDA's 2024 guidance classifying lip products as "drugs" for therapeutic claims has favored organic brands using botanical actives like shea butter and jojoba oil, already compliant with over-the-counter monographs. While Cosmos and Ecocert certifications are more common in facial care, their limited presence in body care presents an opportunity for organic expansion.

Note: Segment shares of all individual segments available upon report purchase

By Category: Premium Acceleration Challenges Mass Incumbency

In 2025, mass-market organic skincare held a 64.74% market share, while premium lines are projected to grow at a 6.11% CAGR through 2031. This trend shows consumers either opting for uncertified "natural" products or upgrading to clinically validated organic options. Premium brands leverage third-party certifications like USDA Organic, Cosmos, and Leaping Bunny, along with clinical trials, to justify a 40-60% price premium over mass-market counterparts. For example, Weleda's Skin Food, priced at USD 18 for 75ml, stands out with its 95+ year heritage and biodynamic farming partnerships. The premium segment's growth reflects a shift in consumer values, moving beyond the "natural but ineffective" versus "synthetic but effective" dichotomy. Consumers now seek products delivering measurable results, such as wrinkle reduction and barrier repair, using botanical actives validated by peer-reviewed studies.

Mass-market brands face challenges like shelf-life economics and certification costs, which strain already thin margins. For instance, Hain Celestial's personal-care revenue dropped 20% in fiscal 2024 due to SKU rationalization and exiting low-margin organic lines, highlighting structural issues. However, mass brands benefit from scale advantages in raw-material procurement and distribution, helping them better absorb a 0.4% CAGR drag from organic ingredient supply bottlenecks compared to smaller premium players. Regulatory gaps weigh heavily on the mass segment, causing a -0.6% CAGR impact, as price-sensitive consumers often turn to uncertified "natural" substitutes that undercut certified organic prices by 30-50%. Conversely, premium brands gain a 0.5% CAGR boost from rising vegan and cruelty-free awareness, with their target demographic 2.3 times more willing to pay for ethical certifications, according to surveys.

By Distribution Channel: Online Gains as Shelf-Life Constraints Bite

In 2025, health and beauty stores accounted for 33.62% of the distribution value. However, online retail channels are growing at a 6.02% CAGR through 2031, driven by direct-to-consumer models that bypass mass-retail shelf-life constraints and enable detailed ingredient storytelling. In 2024, Sephora and Ulta Beauty launched 140 organic skincare SKUs, focusing on Cosmos or USDA Organic-certified brands to differentiate from mainstream "natural" products. However, their 18-month shelf-life requirement excludes many small-batch organic producers. Online retail thrives due to three advantages: no shelf-space limits, real-time inventory management reducing spoilage, and effective consumer education through ingredient glossaries and clinical-study links. For instance, L'Oréal's e-commerce sales reached 28.2% of total revenue in 2024, with organic brands like Kiehl's and Biotherm achieving 35-40% online penetration.

Supermarkets and hypermarkets are losing share as shorter shelf-lives (12-18 months for natural preservatives vs. 36+ months for synthetics) increase markdown risks, causing a -0.5% CAGR impact on mass retail and accelerating the shift to health and beauty stores and online channels. Other channels, including pharmacies, direct sales, and hotel/spa retail, hold significant shares. Pharmacies are gaining traction in Europe, where organic skincare is marketed as "dermaceuticals" with pharmacist endorsements. China's 2024 cross-border e-commerce reforms unlocked a USD 3 billion organic skincare market for international brands on Tmall Global and JD Worldwide, driving Asia-Pacific's 6.22% regional CAGR. Technological innovations, like exosome serums and microbiome formulations, add a 0.7% CAGR boost, benefiting online and health and beauty channels catering to early adopters.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific accounts for 40.43% of the organic skin care market in 2025 and is projected to grow at a 6.22% CAGR from 2026 to 2031. The region's market dominance is driven by increasing disposable incomes, growing health consciousness, and traditional skincare practices in Japan, South Korea, and China. Shiseido's launch of the "ANESSA Sunshine Project" across 12 Asian countries in May 2024 highlights the region's importance. The company's "Mirai Shift NIPPON 2025" strategy emphasizes sustainable growth, profitability, and human capital development through technology and Research and Development investments.

North America continues its market growth, with consumers seeking transparency in ingredient sourcing and sustainability practices. The United States Department of Agriculture (USDA)'s Strengthening Organic Enforcement (SOE) rule, implemented on March 19, 2024, introduces major changes to the National Organic Program (NOP). These include expanded certification requirements for brokers and traders, mandatory NOP Import Certificates for organic imports, and enhanced supply chain traceability measures to prevent fraud.

Europe strengthens its market position through robust regulatory frameworks and growing consumer awareness of sustainability. The Soil Association's 2023 report reveals that organic health and beauty product sales in the UK reached GBP 136 million, driven by environmental consciousness, strict certification standards, and expanded organic retail channels. South America, the Middle East, and Africa offer growth potential, with the Middle East showing rising demand for natural personal care products due to a preference for organic over synthetic ingredients.

Competitive Landscape

The organic skin care market exhibits a fragmented competitive structure, characterized by the presence of multinational corporations, specialized natural brands, and new market entrants. The competitive environment is marked by strategic initiatives from established companies such as L'Oréal S.A., The Estée Lauder Companies Inc., Shiseido Company, Limited, Natura & Co Holding SA, and Weleda AG, which maintain their market positions through continuous portfolio expansion in the organic segment.

These industry leaders implement comprehensive research and development programs, leveraging their substantial technical capabilities and economies of scale to address complex formulation challenges in natural products. Their competitive advantage stems from established distribution networks, brand recognition, and significant investment capabilities in product innovation and market expansion.

The market presents considerable opportunities in specialized segments, particularly in products for sensitive skin, multicultural beauty, and age-specific formulations. Small and emerging brands successfully capture market share by focusing on these niche segments while emphasizing sustainability credentials and ingredient transparency. The competitive landscape continues to evolve with the increasing adoption of direct-to-consumer business models, enabling emerging brands to establish direct consumer relationships through digital channels, circumventing traditional retail distribution networks.

Organic Skin Care Industry Leaders

L'Oréal S.A.

The Estée Lauder Companies Inc.

Shiseido Company, Limited

Weleda AG

Natura & Co Holding SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Natural Grocers, an organic and natural grocery retailer, introduced a new house brand skincare collection. The product line includes body washes, scrubs, butters, and body creams manufactured in small batches with selected ingredients to ensure quality and effectiveness.

- March 2025: Weleda AG, a natural skincare company with certified products, collaborated with Princess Madeleine Bernadotte to develop minLen, a natural skincare brand.

- February 2025: Organic skincare company Puddles introduced a skincare range for teenagers. The product line features plant-based ingredients with scientific validation, targeting common teenage skin concerns, including acne, while providing gentle and effective skincare solutions.

- September 2024: Dr. Squatch introduced a natural body wash that incorporates the properties of its cold-processed bar soap. The body wash contains more than 98% natural ingredients, including coconut-derived components that hydrate and maintain skin moisture throughout the day.

Global Organic Skin Care Market Report Scope

Organic skincare products contain ingredients grown without pesticides through organic farming methods.

The organic skincare products market segments include product type, category, distribution channel, and geography. The product type segment comprises facial care (cleansers, moisturizers, oils/serums, and other facial care products), body care (lotions, body wash, and other body care products), and lip care. The category segment is divided into premium and mass products. Distribution channels include supermarkets/hypermarkets, health and beauty stores, online retail stores, and other channels. Geographically, the market covers North America, South America, Europe, Asia-Pacific, the Middle East, and Africa. The market sizing has been done in USD value terms for all the aforementioned segments.

| Facial Care | Cleansers |

| Moisturizers and Oils/Serums | |

| Other Facial Care Product | |

| Body Care | Body Lotions |

| Body Wash | |

| Other Body Care Products | |

| Lip Care |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| Product Type | Facial Care | Cleansers |

| Moisturizers and Oils/Serums | ||

| Other Facial Care Product | ||

| Body Care | Body Lotions | |

| Body Wash | ||

| Other Body Care Products | ||

| Lip Care | ||

| Category | Mass | |

| Premium | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the organic skin care market in 2031?

Forecasts show USD 61.92 billion by 2031, up from USD 49.74 billion in 2026.

Which region leads current sales?

Asia-Pacific commanded 40.43% of global revenue in 2025 and also posted the fastest growth.

Which product type brings in the most revenue?

Facial care held 75.62% of the 2025 value because consumers prioritize visible skin.

Why are premium organic brands growing faster than mass labels?

Clinical validation and third-party certifications allow premiums to justify higher prices, resulting in a 6.11% CAGR to 2031.