Saudi Arabia Formwork Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.08 Billion |

| Market Size (2026) | USD 0.09 Billion |

| Market Size (2031) | USD 0.11 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Formwork Market Analysis by Mordor Intelligence

The Saudi Arabia Formwork Market size is projected to be USD 0.08 billion in 2025, USD 0.09 billion in 2026, and reach USD 0.11 billion by 2031, growing at a CAGR of 4.10% from 2026 to 2031.

The market remains closely tied to the broader construction sector in the Kingdom, where changes in contract awards, public investment, and site execution drive demand for formwork very quickly. Construction activity is still supported by Vision 2030 spending, with Saudi Arabia recording SAR 30.03 billion (USD 8.0 billion) in project awards in May 2026 and the Construction Business Confidence Index reaching 55.7 in April 2026, pointing to sustained on-site momentum across the Kingdom. The FY2026 budget projects real Gross Domestic Product (GDP) growth of 4.6%. It sets capital expenditure at SAR 162 billion (USD 43.2 billion), which keeps infrastructure, transport, housing, and urban development works active for the Saudi Arabia formwork market. The Public Investment Fund is also directing 80% of its portfolio to domestic deployment in 2026-2030, keeping concrete-intensive developments in housing, logistics, tourism, and sports facilities moving even as project sequencing changes within the giga-project pipeline. At the same time, project phasing and material cost pressures are keeping growth measured rather than sharp. Yet, the shift toward Expo 2030, FIFA World Cup infrastructure, and urban rail is preserving demand for higher-specification systems in the Saudi Arabia formwork market.

Key Report Takeaways

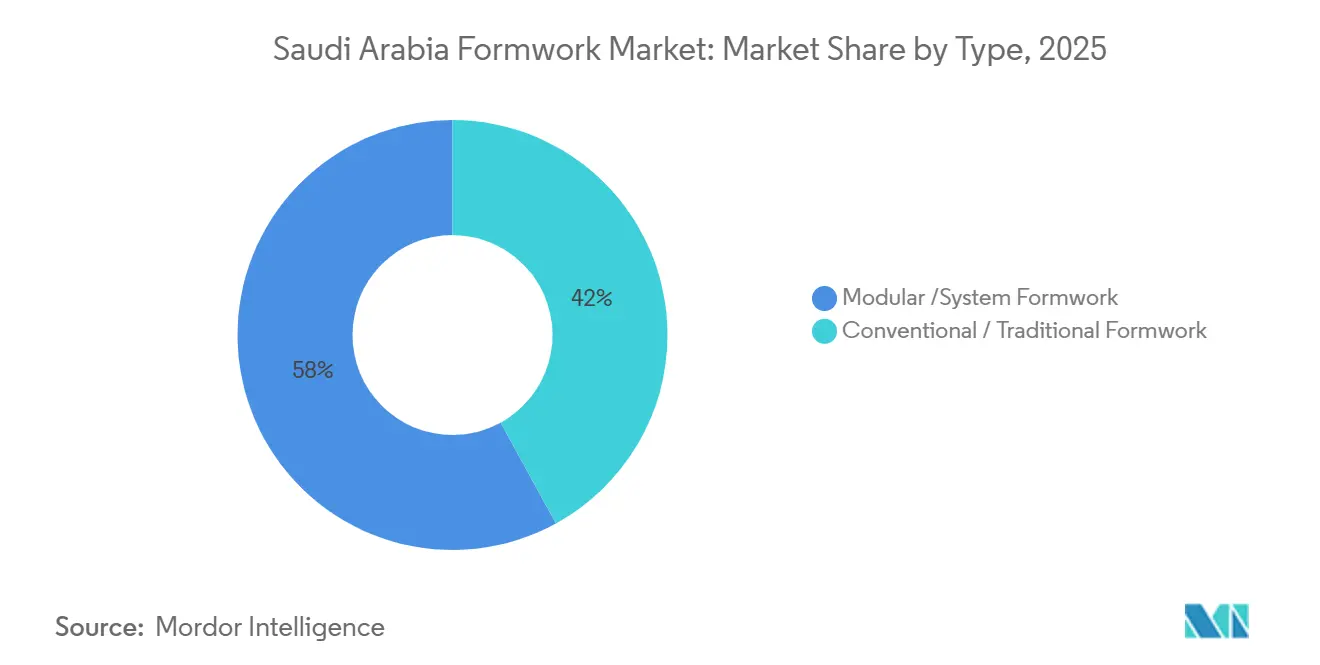

- By type, modular / system formwork accounted for 58% of the Saudi Arabia formwork market share revenue in 2025 and is projected to expand at a 4.42% CAGR through 2031.

- By configuration, static formwork led with a 46% share in 2025, while climbing formwork is forecast to record the highest CAGR at 4.56% through 2031.

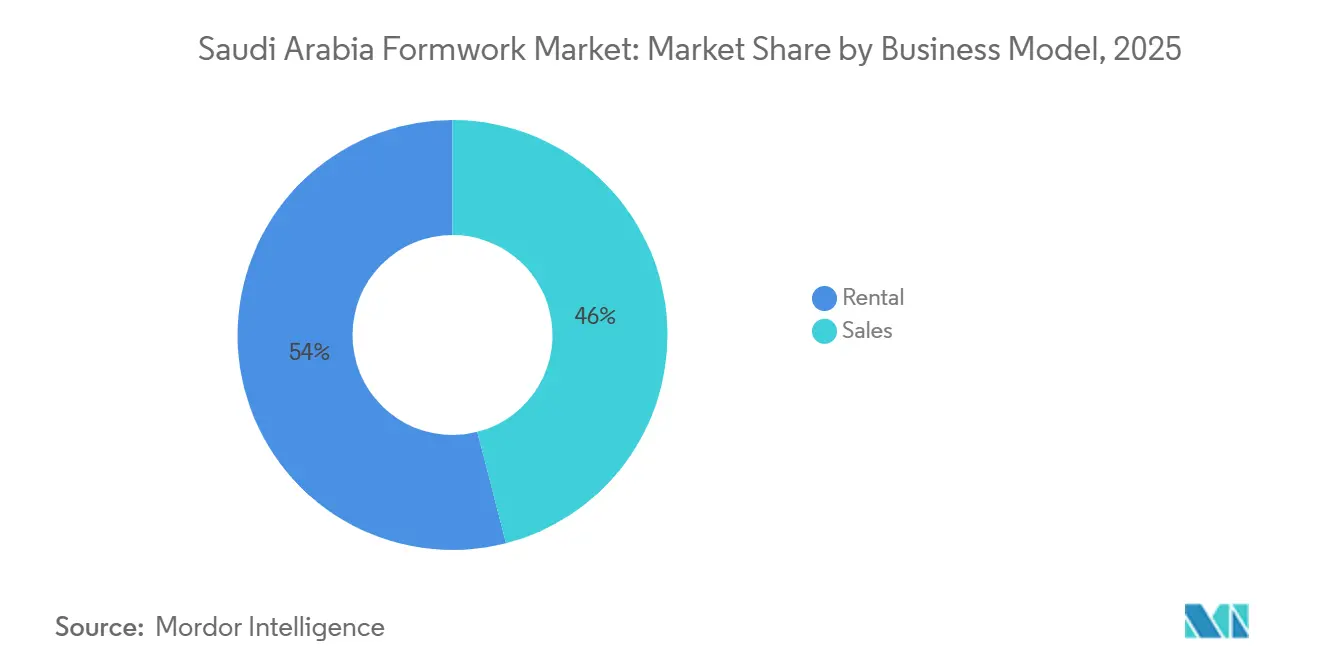

- By business model, rental held 54% of the Saudi Arabia formwork market share in 2025, while rental also posted the highest projected CAGR at 4.98% through 2031.

- By sector, infrastructure accounted for 39% of the Saudi Arabia formwork market size in 2025, and it is also advancing at the fastest CAGR of 5.00% through 2031.

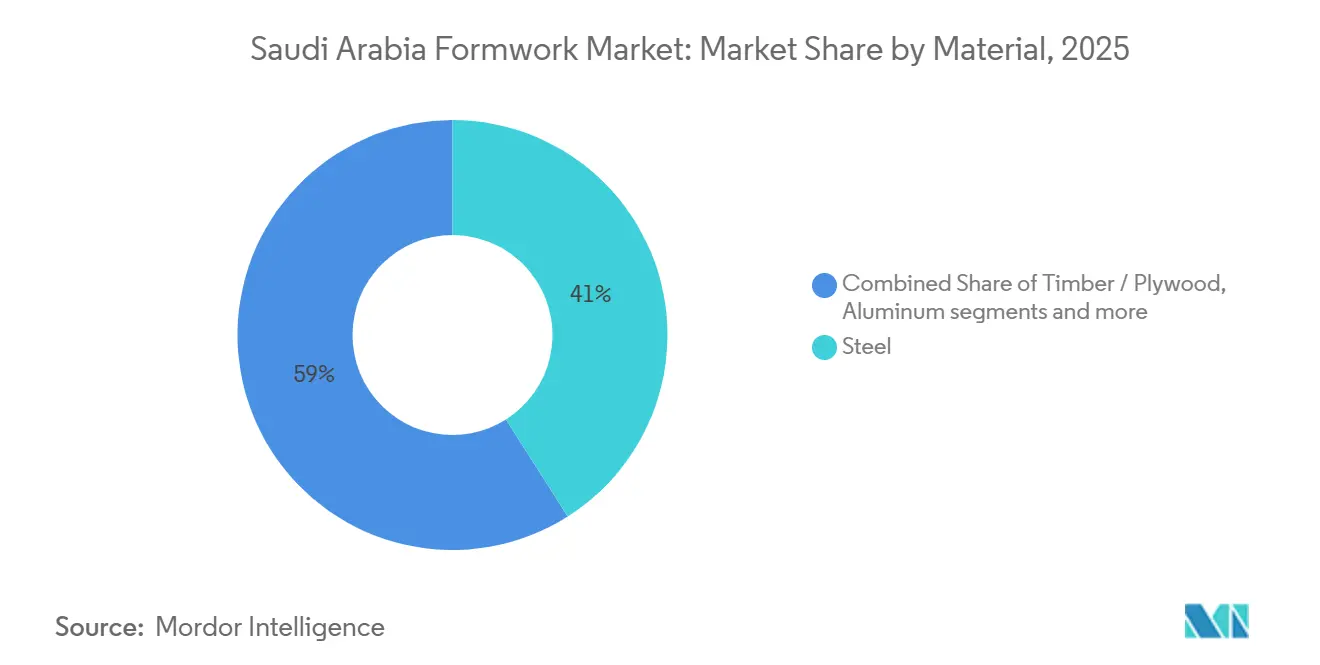

- By material, steel captured a 41% share in 2025, while aluminum is projected to grow the fastest at a 4.88% CAGR through 2031.

- By city, Riyadh accounted for 34% of the market in 2025 and is also expected to expand at the highest CAGR of 5.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Formwork Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Megaprojects Drive Formwork Demand | +1.2% | National, with stronger activity in Riyadh, Makkah, and Eastern Province | Medium term (2-4 years) |

| Riyadh Construction Boom Accelerates Formwork Adoption | +0.8% | Riyadh primary, with spillover into Greater Makkah Region | Short term (≤ 2 years) |

| Eastern Province Industrial Expansion Boosts Formwork Requirements | +0.5% | Eastern Province, especially Jubail, Dammam, and Khobar | Medium term (2-4 years) |

| Preference for Modular / System Formwork Supports Market Growth | +0.5% | National | Medium term (2-4 years) |

| Residential and Mixed-Use Developments Increase Formwork Utilization | +0.4% | Riyadh, Eastern Province, Makkah, and Madinah | Short term (≤ 2 years) |

| Rental and Service-Based Procurement Expands Market Accessibility | +0.3% | National, with faster adoption in Riyadh and Eastern Province | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Megaprojects Drive Formwork Demand

Saudi Arabia’s large development pipeline remains the main demand base for the Saudi Arabia formwork market, even though project sequencing is changing within the giga-project program. The change that matters most is that slower activity in some NEOM packages is being offset by faster execution in Riyadh, Makkah, Diriyah, Qiddiya, and transport works, so formwork demand is shifting rather than disappearing. The PIF’s 2026-2030 plan prioritizes domestic deployment, keeping industrial, tourism, and infrastructure projects funded and supporting the Saudi Arabia formwork market through a broader set of project categories. Saudi Arabia also recorded USD 11 billion in project awards in Q1 2026, indicating that the pipeline remains active beyond a few headline projects and that contractors are still mobilizing for reinforced concrete works. Diriyah Company’s SAR 18.75 billion (USD 5 billion) in contract awards in H1 2025 adds another steady stream of premium superstructure activity, supporting demand for engineered systems, climbing solutions, and specialist site services.

Riyadh Construction Boom Accelerates Formwork Adoption

Riyadh is shaping the near-term direction of the Saudi Arabia formwork market because the city now carries the broadest mix of public, commercial, residential, and infrastructure projects in the Kingdom. In March 2026, construction contracts in Riyadh rose to SAR 15.6 billion (USD 4.2 billion), up 457% from the previous month, and the spread across hospitals, education, recreation, housing, and commercial work lowers dependence on a single demand stream. The FY2026 budget keeps Riyadh Metro expansion and the Main Roads and Ring Axes Development Program on track, with more than 500 kilometers of new road network requiring bridges, retaining structures, culverts, and associated concrete works. The Wadi Laban parallel bridge project adds another visible source of multi-year demand for climbing systems and heavy-duty support applications on the western side of the capital. Riyadh is also adding new demand from data center construction, including the Hexagon government data center project, where reinforced concrete vaults and precision slabs require tighter dimensional control than standard residential jobs.

Eastern Province Industrial Expansion Boosts Formwork Requirements

The Eastern Province supports the Saudi Arabia formwork market through industrial and energy construction, which creates longer hire periods and more specialist applications than standard building work. Investments in Jubail and Yanbu passed SAR 1.5 trillion (USD 400 billion) by end-2025, and the Amiral complex in Jubail is expected to unlock downstream petrochemical projects that extend concrete works into the later years of the forecast period. Aramco’s iktva program had already supported 350 active manufacturing investments with a cumulative value of over USD 9 billion by 2025, and that localization push increases construction demand for bases, industrial floors, containment structures, and processing facilities[1]Saudi Aramco, “Aramco Signs 145 Agreements and MoUs Worth USD 9bn at iktva Forum & Exhibition 2025,” Saudi Aramco, korea.aramco.com . TKE ALAT’s June 2026 groundbreaking in Dammam shows that this demand is not limited to mega complexes and is now extending across smaller but steady industrial facilities in the province. The rail connection work in Dammam adds bridge and corridor structures to the mix, which keeps the Saudi Arabia formwork market tied to both logistics and industrial expansion in the Eastern Province.

Preference for Modular / System Formwork Supports Market Growth

The shift from conventional timber shuttering to engineered systems is moving faster than the overall Saudi Arabia formwork market, which shows that contractors are choosing these products for productivity reasons rather than novelty. Modular and system solutions reduce cycle times, improve surface finish, and cut the amount of follow-on rework, which matters in a project environment where deadlines are tight and multi-site execution is common. PERI Saudi Arabia reported a strong 2024 performance across housing, Diriyah, Qiddiya, and NEOM-related work, and highlighted digital construction tools such as the InSite cement sensor, which shows how the system segment is moving beyond hardware alone. The Al Rimal villa project in Riyadh shows why contractors are adopting aluminum systems for repetitive layouts, because lighter panels and crane-free handling fit large housing programs with tight delivery schedules. As more residential and mixed-use developments move into active construction, the system segment should continue to take share in the Saudi Arabia formwork market because it aligns with speed, finish quality, and service-led procurement.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Project Phasing and Delays Create Demand Uncertainty | -0.4% | National, with strongest effect in the northwest corridor | Short term (≤ 2 years) |

| Material and Logistics Cost Inflation Pressures Project Budgets | -0.3% | National, with higher exposure along import corridors in the Eastern Province | Short term (≤ 2 years) |

| Skilled Labor Constraints Limit Efficient Formwork Installation | -0.2% | National, especially in climbing and slipform applications | Medium term (2-4 years) |

| Geographic Demand Concentration Restricts Balanced Market Growth | -0.1% | Peripheral regions remain underserved, while Riyadh and Eastern Province dominate | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Project Phasing and Delays Create Demand Uncertainty

Project sequencing remains the main constraint on the Saudi Arabia formwork market because suppliers often build fleet plans around large packages long before site activity stabilizes. The cancellation of Webuild’s Trojena artificial lake package in 2026 clearly shows the risk, since specialty systems can be committed early and then left underused when project scope changes. Giga-project awards had already slowed from USD 34.6 billion in 2023 to USD 8.5 billion through November 2025, putting pressure on fleet utilization and the planning assumptions of service-led formwork suppliers. Even so, the demand profile is not falling evenly across the Kingdom, because Expo 2030 works, metro projects, stadiums, airport structures, and regional transport links are still moving ahead and need more advanced concrete systems. The result is a market where volume visibility can weaken for standard civil works, while premium applications remain active in the Saudi Arabia formwork market

Material and Logistics Cost Inflation Pressures Project Budgets

Material and logistics costs remain a second restraint on the Saudi Arabia formwork market because engineered systems depend heavily on steel and aluminum components that are exposed to global price swings. Saudi construction activity continued through the regional disruption of March and April 2026. However, contractors still reported pressure from higher material costs and fees during that period, affecting both owned fleets and rental replacement economics. Imported aluminum panels and precision steel elements make system suppliers more exposed than conventional timber users, especially when freight costs or delivery timing change during active build phases. The Eastern Province’s industrial base partly reduces steel exposure over time as local manufacturing capacity deepens. Still, aluminum systems remain more import-dependent across much of the Saudi Arabia formwork market. Large framework housing contracts also increase buyer concentration in panel procurement, leaving smaller rental operators with less pricing leverage than national-scale contractors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modular / System Formwork Consolidate Structural Dominance

Modular / system formwork held 58% of the Saudi Arabia formwork market share in 2025, making it the largest type segment by a clear margin. Conventional / traditional formwork accounted for the remaining 42% and remained relevant for remote projects, irregular designs, and work where engineered system logistics were harder to justify. Modular / system formwork is also projected to post the highest growth at a 4.42% CAGR through 2031, indicating the leading segment is further widening its position in the Saudi Arabia formwork market. The main reason is not only speed on large sites, but also the ability to standardize pours, reduce finishing work, and support predictable quality across repeated layouts. This matters in both high-volume housing and large public projects, where schedule control is becoming increasingly strict.

The economics of modular systems are especially strong in repetitive concrete work, where reuse rates and faster turnaround improve cost visibility for both contractors and rental suppliers. PERI’s monolithic aluminum system has been used in the 511-unit Al Rimal villa project in Riyadh, demonstrating how lightweight panels support large housing programs without relying on cranes continuously. The company’s product positioning also stresses surface quality and faster cycles, which helps explain why system adoption is rising faster than the overall Saudi Arabia formwork market[2]PERI Saudi Arabia, “PERI Monolithic Solution for Residential Construction,” PERI Saudi Arabia, peri.com.sa. Conventional solutions still have a place in custom work, secondary regional sites, and projects where one-off geometry limits the benefits of reusable panels. Over time, the mix is likely to keep tilting toward engineered systems because Saudi project owners are placing more weight on execution speed, finish consistency, and service-backed supply.

By Configuration: Static Formwork Leads While Climbing Systems Gain Momentum

Static formwork held the largest share at 46% in 2025, reflecting its wide use across residential slabs, wall pours, commercial podiums, and industrial structures. Climbing formwork is the fastest-growing configuration with a 4.56% CAGR through 2031, and that growth tracks the rise of high-rise cores, bridge pylons, stadium structures, and other vertical works in the Saudi Arabia formwork market. Slipform stays smaller but is durable for use in silos, shafts, cooling towers, and some infrastructure projects that require continuous pours. Tunnel formwork remains the smallest configuration segment in 2025, though future transport and utilities works could improve its role later in the forecast period. The configuration mix shows that demand is becoming more specialized as project complexity rises.

The Al Rajhi Bank Headquarters Tower in Riyadh is a clear example of climbing technology being used in the local market, with TMS deploying its Climbex hydraulic climbing system across reinforced concrete core walls. That case matters because it shows that advanced climbing systems are no longer limited to a narrow set of flagship buildings. Infrastructure programs in Riyadh and the Eastern Province are also expanding the addressable base for climbing and slipform solutions, especially where crane reliance needs to be reduced, or vertical progress needs to stay continuous. Compliance requirements for structural concrete performance further support the use of rated and documented systems over improvised setups. That gives engineered configurations a stronger position as the Saudi Arabia formwork market shifts toward larger and more regulated projects.

By Business Model: Rental Economics Reshape Capital Decisions

Rental accounted for 54% of the Saudi Arabia formwork market size in 2025 and is also the fastest-growing business model, with a projected CAGR of 4.98% through 2031. Sales represented the remaining 46% and continued to suit contractors with long, repetitive housing programs or stable design templates. The strong rental position reflects how large Saudi projects are financed and executed, as contractors often need flexibility across multiple sites rather than carrying full ownership costs on every job. This is especially true when payment cycles are phased, contract durations are extended, and project sequencing can change. In that setting, rental gives contractors access to equipment, engineering support, and redeployment options without locking up capital.

The sales model still has a clear place in high-volume housing. Saudi contracts awarded to Chinese firms for around 4,500 housing units in Riyadh and Dammam, as part of a wider 100,000-unit target by 2030, show the sort of repetitive layouts where owned aluminum formwork can amortize efficiently. Rental remains stronger in the broader Saudi Arabia formwork market because service breadth now matters as much as hardware availability. PERI Saudi Arabia’s three-branch setup and 35,000 m² logistics yard demonstrate the operational model behind that trend, where planning, delivery, supervision, and cross-project asset movement are bundled. AlBawani’s SAR 6.4 billion (USD 1.7 billion) financing agreement in May 2026 also points to the wider contractor preference for flexible capital structures while large project portfolios stay active. That financing backdrop supports continued expansion of rental-led procurement in the Saudi Arabia formwork market.

By Sector: Infrastructure Leads but Housing Rebalances the Mix

Infrastructure held 39% of the Saudi Arabia formwork market share in 2025 and is also projected to post the fastest sector CAGR at 5.00% through 2031. That dual leadership shows that infrastructure is not only the largest source of demand today, but also the main direction of incremental growth through the forecast period. The FY2026 budget allocated SAR 35 billion (USD 9.3 billion) to infrastructure and transportation, which keeps roads, airports, rail, and related concrete structures active for formwork suppliers. The Aseer-Jazan Expressway award adds a major multi-year demand stream that will support heavy-duty systems, bridge works, and associated retaining structures. Infrastructure, therefore, remains the anchor segment for the Saudi Arabia formwork market even when the balance of project types shifts within the Kingdom.

Residential construction is smaller than infrastructure in 2025, but it is still reshaping the demand mix because the housing delivery target remains large. Saudi homeownership reached 66.24% by end-2025, below the 70% Vision 2030 target, indicating housing programs will continue to absorb aluminum and modular systems over the next several years. Commercial demand remains steady across office, hospitality, and cultural work, including the SAMoCA project in Diriyah, where architectural quality underscores the need for precision formwork. Industrial and logistics work is also becoming more important in the Eastern Province, with projects such as TKE ALAT’s facility in Dammam adding specialist steel formwork needs. This broader sector mix gives the Saudi Arabia formwork market a more balanced demand base than a pure giga-project story would suggest.

By Material: Steel Holds Share as Aluminum Accelerates

Steel held a 41% share in 2025, making it the largest material segment in the Saudi Arabia formwork market. Its position reflects strong use in infrastructure, industrial construction, and jobs where high load ratings, durability, and heavy concrete pressures matter more than weight. Aluminum is the fastest-growing material segment, projected to expand at a 4.88% CAGR through 2031. That growth is tied to housing, repetitive floor plans, and project environments where lighter systems support faster cycles and simpler handling. The material split, therefore, reflects two different demand centers, with steel tied more to heavy civil and industrial work, and aluminum tied more to residential and system-based construction.

PERI’s monolithic solution in scaleon helps explain why aluminum is gaining momentum, as the company markets it for faster construction cycles, lighter panels, and a finish quality that reduces downstream site work. Timber / plywood still plays a practical role in the Saudi Arabia formwork market for irregular geometry, one-off sections, and smaller regional works, where reverse logistics can undermine the economics of engineered systems. Plastic and fiberglass remain niche and are mostly relevant in specialized environments, such as precast or tunnel-related applications. Composite and hybrid systems are still small, but they are becoming more visible as sustainability and lifecycle considerations enter procurement discussions for public projects. Even so, the material hierarchy remains clear, with steel leading today and aluminum gaining ground fastest across the Saudi Arabia formwork market.

Geography Analysis

Riyadh held a 34% share in 2025 and is projected to record the fastest city-level CAGR of 5.1% through 2031, keeping it at the center of the Saudi Arabia formwork market. In March 2026, construction contracts in the capital reached SAR 15.6 billion (USD 4.2 billion), and the range of project categories indicates broad demand rather than a focus on a single type of development. The city’s pipeline includes preparations for Expo 2030, metro expansion, road and ring-axis works, and major bridge construction, all of which support demand for static, climbing, and specialist support systems. Housing also remains a strong support base, with residential stock expected to rise beyond 3.3 million units by 2030, keeping aluminum and modular demand active in the city. New project types, such as the Hexagon data center, add another layer to the Saudi Arabia formwork market in Riyadh, as they require precision concrete work that differs from that of standard housing and retail structures.

The Eastern Province is the second-largest demand center and is more industrial in character than Riyadh. Investments in Jubail and Yanbu crossed SAR 1.5 trillion (USD 400 billion) by end-2025, which keeps heavy concrete work active across energy, manufacturing, and downstream petrochemicals. Aramco’s iktva-linked manufacturing expansion and the Dammam rail connection project add sustained demand for foundations, industrial floors, bridge elements, and containment structures. This gives the Saudi Arabia formwork market a strong second pole of demand that is less exposed to housing cycles and more tied to industrial buildout.

Makkah and Madinah form a separate cluster linked to pilgrimage, hospitality, and related access infrastructure. The FY2026 budget includes spending on pilgrimage access improvements, miqat development, and urban works in Makkah, which support retaining walls, elevated structures, and transport-related concrete jobs. The King Salman Gate project adds another layer of high-specification demand in Makkah, while Madinah remains smaller and more episodic, with support from restoration and religious tourism-linked construction. The Rest of Saudi Arabia is still the smallest cluster in 2025, but major regional projects such as the Aseer-Jazan Expressway show that demand is widening geographically and could modestly rebalance the Saudi Arabia formwork market in the later years of the forecast period.

Competitive Landscape

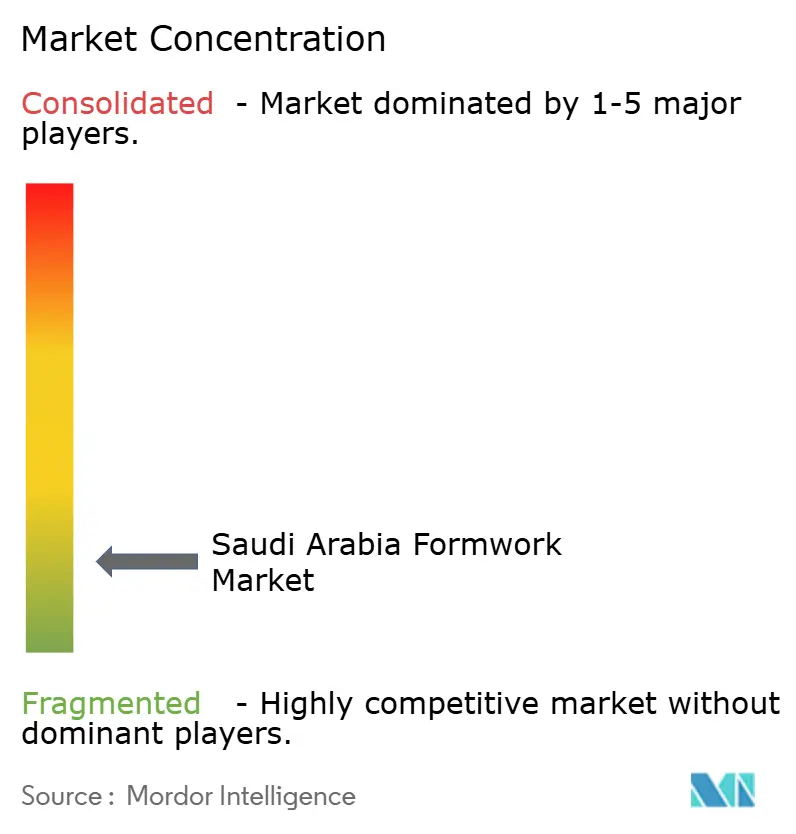

The Saudi Arabia formwork market is fragmented, with international system providers competing alongside a broad base of local rental companies, fabricators, and regional service firms. No single supplier holds a dominant market position, as competition is spread across residential, commercial, industrial, and infrastructure projects throughout the Kingdom. International companies differentiate themselves through engineered systems, technical support, digital construction tools, and project engineering, while local firms compete through pricing, faster mobilization, regional presence, and close relationships with contractors. This creates a competitive environment in which both global and domestic suppliers serve different project requirements across the Saudi Arabia formwork market.

PERI Saudi Arabia remains one of the leading engineered system providers through its branch network, 35,000 m² logistics yard, and project experience across KAFD, KAIA Jeddah, the Haramain High-Speed Railway, Diriyah, and Qiddiya. However, the company operates alongside several international and domestic competitors rather than dominating the market. MFS Aluminium Formwork Systems has established a strong presence across Riyadh, Jeddah, and Dammam, particularly in repetitive residential construction, while TMS Saudi Arabia has strengthened its position in specialized applications through systems such as the Climbex hydraulic climbing platform used on the Al Rajhi Bank Headquarters Tower in Riyadh. These examples demonstrate that suppliers can compete successfully by offering specialized systems, technical expertise, or strong project execution capabilities.

Competition is also shaped by geographic coverage and localized service capability. Secondary cities such as Abha, Taif, Yanbu, and Tabuk continue to offer opportunities for suppliers that can respond quickly and build stronger regional support networks. At the same time, increasing emphasis on iktva-linked procurement encourages suppliers to expand in-Kingdom manufacturing, sourcing, and service capabilities. Certified system providers continue to benefit from compliance, engineering documentation, and proven performance on complex projects, while regional operators remain competitive through flexibility, local market knowledge, and responsive customer support. As a result, the Saudi Arabia formwork market is expected to remain fragmented, with competition driven by service quality, technical capability, geographic reach, and project execution rather than by a small group of dominant suppliers.

Saudi Arabia Formwork Industry Leaders

PERI Saudi Arabia Ltd.

Manar Al Omran

Al Najm Al Thaqib Scaffolding Company

Najd Scaffolding and Formwork

Alrowad Scaffolding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: TKE ALAT (a TK Elevator–Alat joint venture) broke ground on a SAR 285 million (USD 76 million) elevator and escalator manufacturing facility in Dammam's Third Industrial City, scheduled for completion by end-2027. The facility spans over 40,000 m² and generates industrial concrete formwork demand tied to the Eastern Province's advanced manufacturing buildout.

- June 2026: Saudi Arabia Railways awarded a contract for the Dammam 2nd Industrial City Railway Connection Project to OHL Arabia and Hassan Allam Construction, including a 265-meter highway bridge and 118-meter Aramco pipeline corridor crossing, both requiring specialist climbing or slipform formwork for pier and abutment construction.

- May 2026: Saudi Arabia recorded SAR 30.03 billion (USD 8 billion) in construction contract awards, the highest monthly total of 2026. Major awards included the SAR 18 billion (USD 4.8 billion) Aseer–Jazan Expressway, the Khuzam–Nour residential district in Riyadh, and several additional projects across Riyadh and the Eastern Province.

Saudi Arabia Formwork Market Report Scope

The Saudi Arabia Formwork Market is Segmented by Type (Conventional / Traditional, Modular / System Formwork), Configuration (Static, Climbing, Slipform, and Tunnel), Business Model (Sales, and Rental), Sector (Residential, and More), Material (Timber / Plywood, Steel, Aluminum, and More), and City (Riyadh, Eastern Province, Makkah, Madinah, and Rest of Saudi Arabia). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional / Traditional |

| Modular / System Formwork |

| Static |

| Climbing |

| Slipform |

| Tunnel |

| Sales |

| Rental |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| Riyadh |

| Eastern Province |

| Makkah |

| Madinah |

| Rest of Saudi Arabia |

| By Type | Conventional / Traditional |

| Modular / System Formwork | |

| By Configuration | Static |

| Climbing | |

| Slipform | |

| Tunnel | |

| By Business Model | Sales |

| Rental | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By Material | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By City | Riyadh |

| Eastern Province | |

| Makkah | |

| Madinah | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

What is the current size of the Saudi Arabia formwork market?

The Saudi Arabia formwork market stands at USD 0.091 billion in 2026 and is forecast to reach USD 0.110 billion by 2031 at a 4.10% CAGR.

Which segment leads by type in Saudi Arabia formwork demand?

Modular /system formwork led by type with 58% share in 2025 and is also the fastest-growing type segment through 2031.

Why is rental the leading business model in Saudi Arabia formwork procurement?

Rental held 54% share in 2025 because contractors prefer lower upfront capital use, better cash flow flexibility, and access to engineering support across multiple projects.

Which end-use sector drives the strongest demand for formwork in Saudi Arabia?

Infrastructure led with 39% share in 2025 and is also projected to grow the fastest at a 5.00% CAGR through 2031, supported by roads, rail, airports, and urban works.

Which city is the main demand center for formwork systems in Saudi Arabia?

Riyadh held 34% share in 2025 and is expected to post the fastest city CAGR at 5.10% through 2031 because of Expo 2030, metro, roads, housing, and large civic projects.

Page last updated on: