Saudi Arabia Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

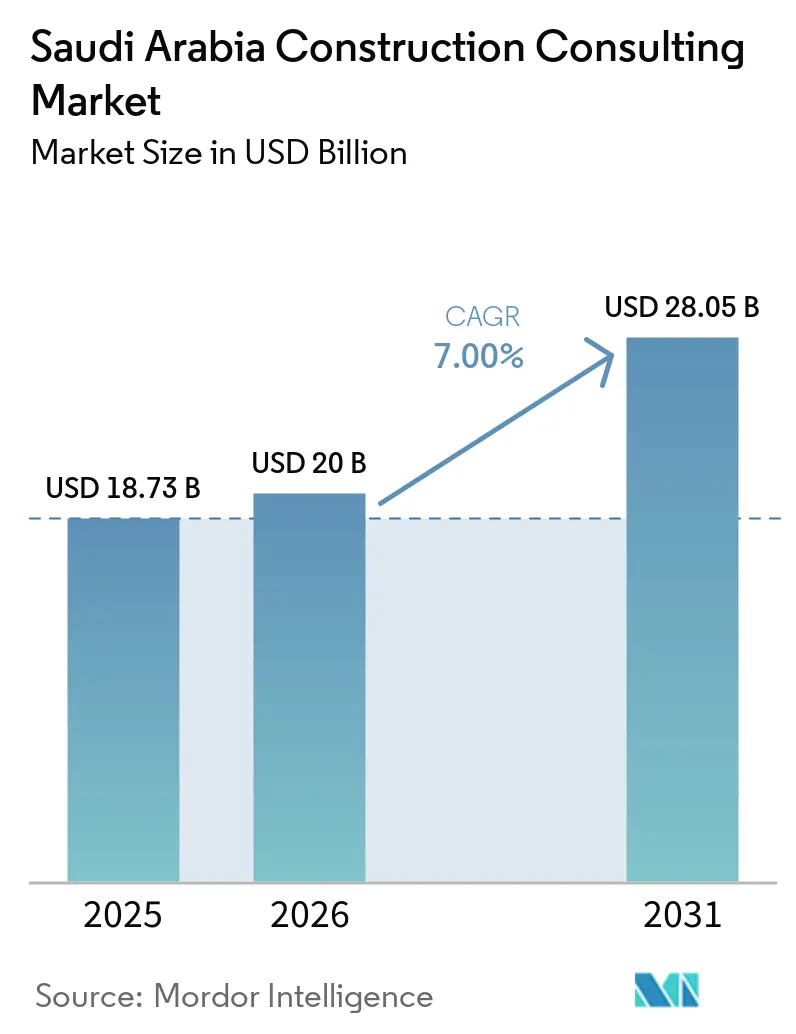

| Base Year Market Size (2025) | USD 18.73 Billion |

| Market Size (2026) | USD 20 Billion |

| Market Size (2031) | USD 28.05 Billion |

| Growth Rate (2026 - 2031) | 7.00% CAGR |

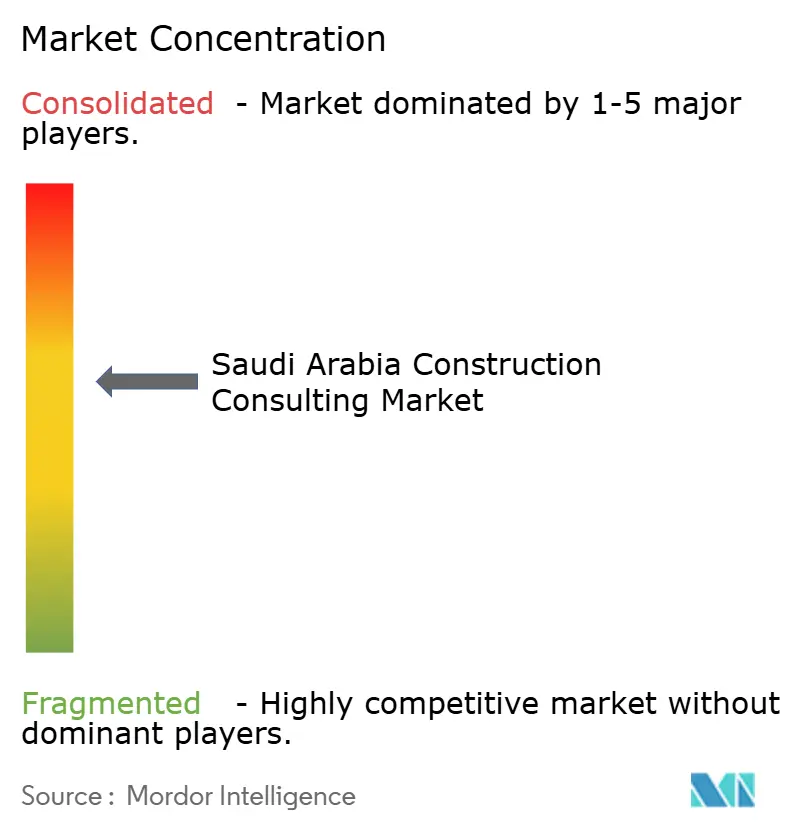

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Construction Consulting Market Analysis by Mordor Intelligence

The Saudi Arabia Construction Consulting Market size is projected to be USD 18.73 billion in 2025, USD 20 billion in 2026, and reach USD 28.05 billion by 2031, growing at a CAGR of 7% from 2026 to 2031.

Continuing progress on Vision 2030, the National Privatization Strategy, and a USD 600 billion giga-project pipeline anchor multi-year advisory demand. Restructuring at NEOM has redirected budgets from The Line to revenue-generating assets such as Sindalah, Oxagon, and Trojena, ensuring a steady flow of feasibility and project-management mandates. PPP concessions in water, power, and transport are widening the scope for transaction and lender-engineer services, while mandatory Saudization quotas and BIM-driven digital-twin requirements are reshaping talent priorities and technology spending. Price swings in diesel, steel, and cement are prompting a move toward cost-reimbursable contracts, and heritage-restoration projects in Diriyah and AlUla are boosting demand for niche conservation expertise.

Key Report Takeaways

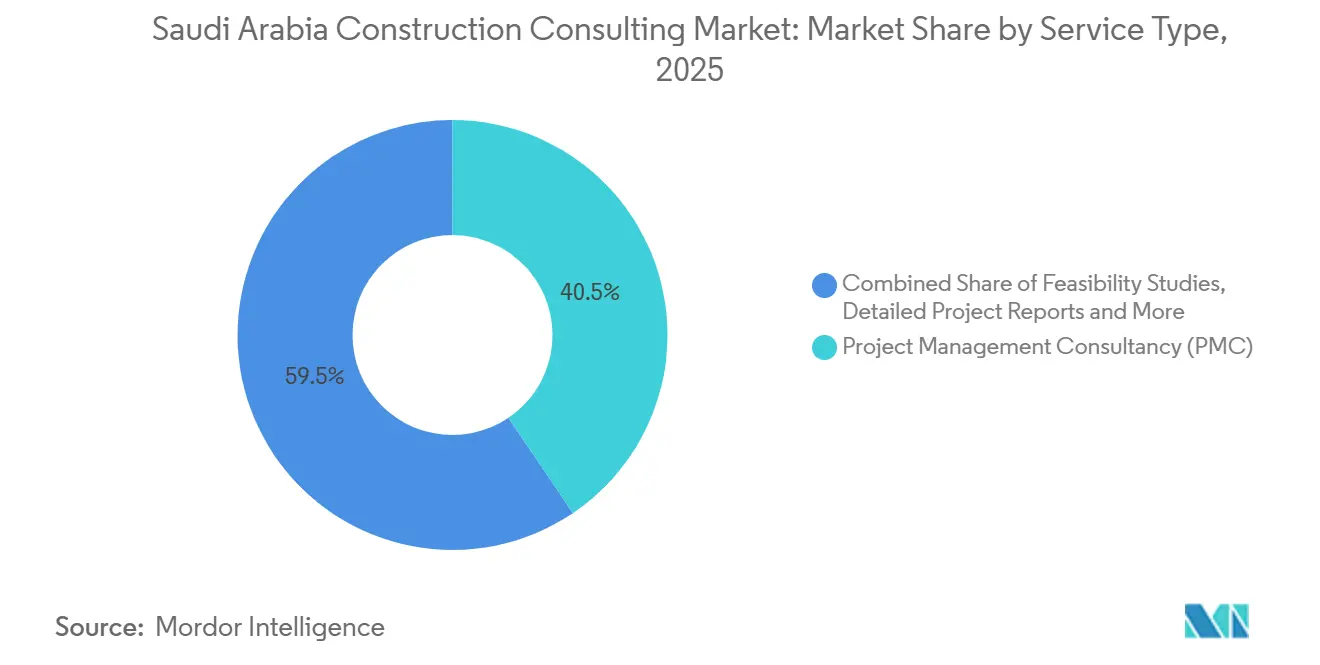

- By service type, Project Management Consultancy captured 40.54% of the Saudi Arabia construction consulting market share in 2025; Master Planning and Other Services are projected to grow at an 8.25% CAGR between 2026 and 2031.

- By sector, infrastructure and civil works accounted for 40.5% of the Saudi Arabia construction consulting market in 2025, while residential assignments are advancing at a 7.98% CAGR through 2031.

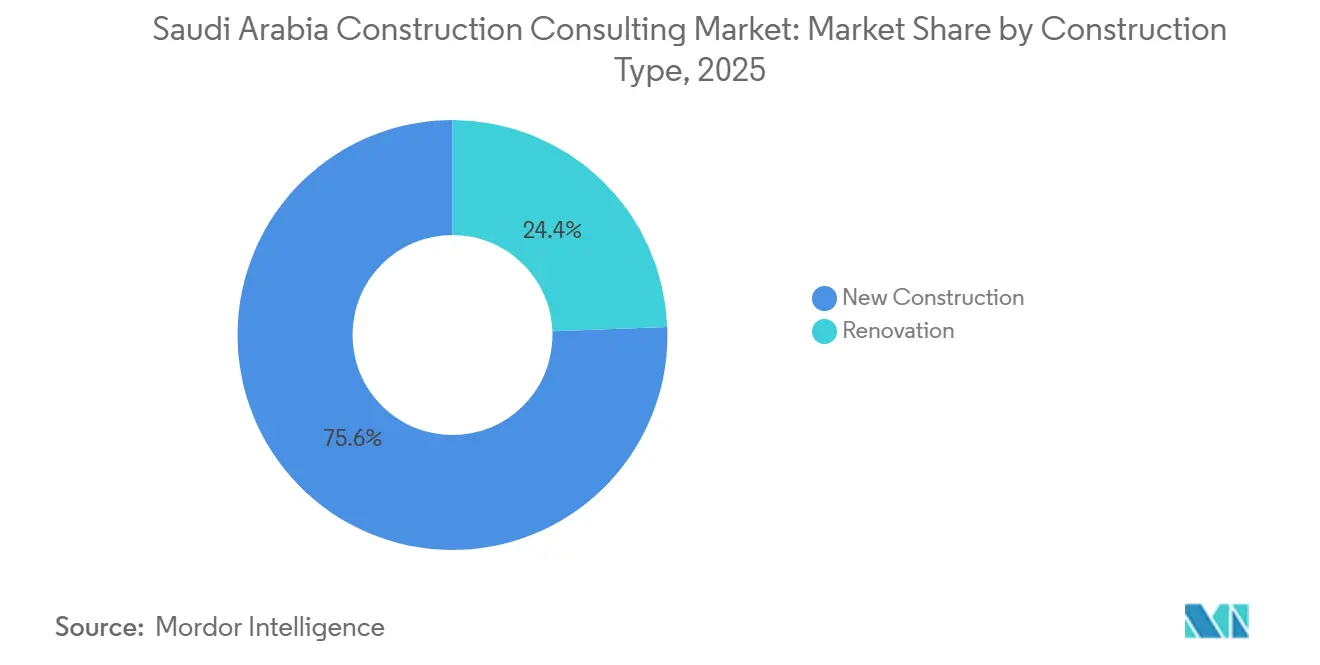

- By construction type, new-build work accounted for 75.6% of the Saudi Arabia construction consulting market share in 2025; renovation consulting is forecast to expand at an 8.5% CAGR over 2026-2031.

- By investment source, private sponsors accounted for 75.69% of 2025 spending, whereas public-sector PPP advisory is set to grow at an 8.8% CAGR through 2031.

- By geography, Riyadh led the Saudi Arabia construction consulting market with 39.60% of the market share in 2025; the rest of Saudi Arabia is on track for a 7.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USD 600 billion giga-project pipeline | +2.1% | Riyadh, NEOM, Qiddiya, AlUla, Red Sea | Long term (≥ 4 years) |

| Accelerated privatization & PPP model | +1.8% | Riyadh, Jeddah, Dammam | Medium term (2–4 years) |

| Digital-twin mandates on flagship assets | +1.4% | NEOM, Red Sea, Riyadh Metro | Medium term (2–4 years) |

| Mandatory Saudization quotas | +1.0% | Nationwide | Short term (≤ 2 years) |

| Green Building Code (SBC 601) adoption | +0.9% | Major cities | Short term (≤ 2 years) |

| Modular construction for desert logistics | +0.8% | NEOM, Red Sea, Eastern Province | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

USD 600 Billion Giga-Project Pipeline Under Vision 2030

Saudi Arabia is advancing a USD 600 billion slate of mega-developments, led by NEOM, Qiddiya City, the Red Sea destination, Diriyah Gate, and large-scale ROSHN housing programs. Each scheme requires layered feasibility, design, cost, and risk oversight that only seasoned consultants can provide. Even after NEOM downsized The Line to a 2.4-kilometer pilot, spending has rolled into Sindalah’s luxury island, Oxagon’s industrial complex, and Trojena’s mountain resort, preserving advisory volume[1]NEOM, “Restructuring Announcement 2025,” neom.com . Stadium, theme park, and infrastructure packages at Qiddiya, plus heritage restoration at Diriyah, add specialist roles in acoustics, ride engineering, and conservation. As lenders insist on stringent oversight, the pipeline secures long-dated revenue visibility for firms able to field multidisciplinary teams.

Accelerated Privatization & PPP Model Unlocks Advisory Opportunities

The January 2026 National Privatization Strategy seeks USD 64 billion in private capital and more than 220 PPP contracts by 2030, converting what were once government civil-works tenders into bankable concessions[2]National Center for Privatization, “Privatization Strategy 2026,” ncp.gov.sa . Consultants are now hired to structure deals, run financial models, and act as lenders’ engineers on desalination, inter-city rail, and airport projects. Examples include the USD 5.5 billion Yanbu 4 Independent Water and Power Project and the USD 1.8 billion Jubail 3B plant, each requiring technical due diligence on reverse-osmosis technologies and tariff escalators[3]ACWA Power, “Yanbu 4 IWPP Award,” acwapower.com . Because concession contracts fall under IFRS 16 lease rules and Saudi Capital Market Authority disclosure requirements, advisers with finance and regulatory fluency enjoy a clear competitive edge.

Digital-Twin Mandates on NEOM & Red Sea Assets

NEOM launched the USD 1 billion XVRS platform in March 2026, fusing BIM, IoT, and AI analytics into a live digital-twin environment for its island, industrial, and mountain clusters. Red Sea Global’s 16 prefabricated hotels also run cloud-hosted twins that automate clash detection and predictive maintenance. Project owners now specify ISO 19650 compliance and cybersecurity protocols aligned with Saudi Aramco standards, forcing consultants to invest in enterprise BIM licenses and six-figure cyber-liability cover. This technology premium is driving market share toward firms such as AECOM, AtkinsRéalis, and WSP that can absorb the upfront IT cost.

Mandatory Saudization Quotas Heighten Talent-Development Demand

Revised labor rules, effective June 2026, raise Saudi national participation to 30% in engineering and 70% in procurement. Firms that fail to comply risk suspension of Balady platform permits, so demand is rising for organizational design, training, and workforce planning consulting. Initiatives such as KEO Academy and academic partnerships with King Fahd University channel fresh graduates into BIM roles, but the three-year competency lag fuels a short-term wage spike. International consultancies are forming joint ventures or acquiring local players, as seen in Egis’ March 2026 purchase of Omrania, to lock in Arabic-speaking talent and protect profit margins.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Arabic-speaking Tier-1 consultants | -0.7% | Nationwide, more acute in heritage projects | Short term (≤ 2 years) |

| Construction-material price volatility | -0.5% | Nationwide | Short term (≤ 2 years) |

| Fragmented permitting outside Riyadh | -0.4% | Secondary cities | Medium term (2–4 years) |

| Cyber-liability exposure on cloud BIM | -0.3% | Firms with 50–200 staff | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Arabic-Speaking Tier-1 Consultants

Large projects require bilingual engineers to secure municipal approvals, yet the talent pool is thin. Bill rates for senior, Arabic-fluent project managers now run 30-40% above global benchmarks, squeezing margins on fixed-price PMC contracts. Heritage work at Diriyah and AlUla, where submissions must be in Arabic, magnifies the shortage and tilts awards toward domestic firms. International players are racing to set up in-house language academies or buy local outfits, as Egis did with Omrania. Still, skills take years to mature, keeping the supply crunch in place until at least 2028.

Construction-Material Price Volatility

Diesel jumped 27.3% year-on-year in July 2025, lifting freight, cement, and steel input costs beyond contingencies built into older feasibility models. Rebar hit USD 584 per ton in January 2026, while ready-mix concrete crossed USD 58 per cubic meter, forcing consultants to re-run quantity-take-off and escalation scenarios quarterly. PPP bidders are negotiating cost-pass-through clauses, but government owners prefer lump-sum designs, exposing advisers to commodity cycles they cannot hedge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: PMC Dominates, Master Planning Accelerates

Project Management Consultancy held 40.54% of the Saudi Arabia construction consulting market share in 2025, reflecting owner preference for single-point accountability on multi-billion-dollar schemes. AECOM’s oversight of New Murabba and the King Salman Park master plan exemplifies integrated cost, schedule, and risk control across sprawling supply chains. Down the value chain, feasibility studies remain essential for PPP lenders, as shown in ACWA Power’s water-and-energy concessions.

Master Planning and Other Services are forecast to produce the fastest 8.25% CAGR through 2031 as new-city blueprints such as Qiddiya, AlUla, and ROSHN communities move from concept to phased execution. These assignments blend land-use programming, mobility modeling, and utility corridor sizing, and often run 10-15 years, locking advisers into subsequent design packages. Because green codes and heritage constraints are embedded early, planners who combine environmental, archaeological, and stakeholder skills are positioned for repeat awards.

By Sector: Infrastructure Leads, Residential Surges

Infrastructure and civil works accounted for 40.5% of the Saudi Arabia construction consulting market in 2025, buoyed by megaprojects such as Riyadh Metro Line 7 and the USD 8 billion King Salman International Airport. Transit, power, and desalination projects require specialized tunneling, systems, and utility engineers, often spanning engagements over a decade.

Residential consulting is the fastest-growing segment, with a 7.98% CAGR to 2031, as PIF-backed ROSHN accelerates the delivery of more than 150,000 units nationwide. The ALAROUS launch in April 2026 and ALMANAR groundbreaking later the same year each triggered master-plan, geotechnical, and value-engineering packages worth USD 5-10 million apiece. Energy-efficiency mandates under SBC 601 and large-scale off-site fabrication are prompting advisers to integrate BIM energy models and modular cost studies into their scope of work.

By Construction Type: New-Build Dominates, Renovation Gains

New construction commanded 75.6% of 2025 spending, thanks to greenfield assets at NEOM, Red Sea, and major data-center investments. Yet renovation and adaptive reuse are forecast to pace ahead at an 8.5% CAGR, propelled by UNESCO-driven heritage upgrades in Diriyah and AlUla. Consultants versed in non-destructive testing, seismic retrofits, and microclimate monitoring are in short supply, letting them command premium day rates.

Energy retrofits under SBC 601, plus office-to-residential conversions in older Riyadh and Jeddah towers, are further widening the workload. Owners facing CBAM-linked export tariffs also seek carbon-cutting roadmaps for legacy factories, expanding the advisory footprint into brownfield industrial sites.

By Investment Source: Private Capital Still Leads, Public PPPs Accelerate

Private sponsors delivered 75.69% of 2025 outlays, primarily through PIF subsidiaries such as NEOM and Qiddiya, as well as hyperscale data centers from Hexagon and HUMAIN. These clients value rapid turnaround and often award design-and-build or EPCM contracts that let consultants capture higher performance fees.

Public-sector PPP advisory is the fastest-growing segment, with a 8.8% CAGR to 2031. The National Center for Privatization’s one-stop portal lists more than 220 prospective concessions, each requiring independent certification, demand modeling, and O&M readiness oversight. Firms combining legal, financial, and technical talent under one roof are winning spots on framework panels that may run through the next decade.

Geography Analysis

Riyadh accounted for 39.60% of 2025 consulting revenues, anchored by marquee assignments such as New Murabba, the 13.4 square-kilometer King Salman Park, and ongoing metro and airport expansions. Continuous workflow across design, supervision, and operations planning makes the capital a stable hub for multidisciplinary teams and supports premium pricing on long-dated contracts.

Jeddah’s port- and tourism-oriented development underpins steady demand for airports, waterfronts, and heritage. The Terminal 1 expansion at King Abdulaziz International wrapped in late 2026, while a future Terminal 2 keeps preliminary design teams busy. Coastal housing at ALAROUS and canal-front retail at MARAFY generate niche roles in marine and tidal engineering that few inland consultants can fill.

The rest of Saudi Arabia is projected to grow at a 7.95% CAGR through 2031, led by AlUla’s USD 32 billion culture and tourism agenda and Qiddiya’s USD 53 billion entertainment city. These regions rely heavily on specialists in archaeology, environmental science, crowd simulation, and theme-park ride integration. Because logistics and infrastructure are less mature than in Riyadh or Jeddah, consultants able to coordinate supply chains, worker housing, and utilities gain a decisive competitive edge.

Competitive Landscape

Global majors AECOM, AtkinsRéalis, Dar Al-Handasah, WSP, and Egis control roughly half of gigaproject oversight thanks to ISO 19650-certified BIM suites, 24/7 cross-border delivery teams, and solid lender credentials. Domestic outfits such as Saudconsult and Zuhair Fayez capture mid-tier schemes where Arabic fluency and lower fees trump deep digital capabilities.

Strategic moves since 2025 include AECOM-Jacobs’ joint venture on The Mukaab, Mott MacDonald’s 25-airport framework, and Egis’ March 2026 acquisition of Omrania, which added 700 Arabic-speaking staff and strengthened heritage coverage. International firms regularly partner with local grade-A architects to meet Saudization quotas and Balady pre-qualification requirements. At the same time, mid-sized players pursue white-label BIM alliances with Autodesk and Bentley to remain competitive.

Technology disruption is edging commoditized design scope toward AI-based automation. NEOM’s XVRS platform and Red Sea Global’s modular hotel twins reduce traditional drafting hours by double digits, forcing consultants to pivot into higher-margin areas such as risk analytics, ESG assurance, and stakeholder engagement. Enterprises prepared to fund cybersecurity, ISO 27001 data centers, and continuous talent development are best placed to defend their share against both digital disruptors and low-cost regional entrants.

Saudi Arabia Construction Consulting Industry Leaders

AtkinsRéalis (Atkins Middle East)

AECOM Arabia

WSP Middle East

Dar Al Handasah Consultants

Zuhair Fayez Partnership

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AECOM won the PMC contract for New Murabba’s 400-meter Mukaab centerpiece.

- March 2026: NEOM unveiled the USD 1 billion XVRS digital-twin platform integrating BIM, IoT, and AI analytics.

- March 2026: MIS awarded a USD 501 million AI data-center EPC contract for HUMAIN in Riyadh.

- January 2026: The National Privatization Strategy set a USD 64 billion target with 220+ PPP opportunities.

Saudi Arabia Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design and Engineering Services |

| Master Planning and Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design and Engineering Services | ||

| Master Planning and Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Riyadh | |

| Jeddah | ||

| DMA (Dammam Metropolitan Area) | ||

| Rest of Saudi Arabia | ||

Key Questions Answered in the Report

How large will the Saudi Arabia construction consulting market be by 2031?

The Saudi Arabia construction consulting market size is projected to reach USD 28.05 billion by 2031, expanding at a 7% CAGR from 2026.

Which service type currently holds the largest share of the Saudi construction consulting market?

Project Management Consultancy accounted for 40.54% of 2025 revenues and remains the dominant service line.

What segment is expected to grow fastest through 2031?

Master Planning and Other Services are forecast to register the highest CAGR of 8.25% during 2026–2031 as new-city blueprints move into execution.

Which region inside the Kingdom drives the most consulting spend?

Riyadh led with 39.60% of 2025 revenue thanks to New Murabba, King Salman Park, and metro and airport expansions.

How is privatization influencing consulting demand?

Over 220 PPP concessions targeted by the National Privatization Strategy are opening new roles in transaction structuring and lenders’ engineering.

What impact do Saudization rules have on consulting firms?

Higher localization quotas, effective in 2026, are spurring demand for talent development advisory and driving acquisitions of Arabic-speaking firms.

Page last updated on: